Presentation Highlights

Takashi Owada (hereinafter, “Owada”): Thank you very much for taking the time to attend our financial results briefing today. I am Takashi Owada, President of TOYOKANETSU K.K. Let me begin the presentation.

Today, I will cover four topics: the FY2026 (Fiscal Year End) Consolidated Financial Summary, progress in the first year of the Mid-Term Management Plan and future developments, the earnings forecast for the current fiscal year, and future developments, including the transition to a holding company structure.

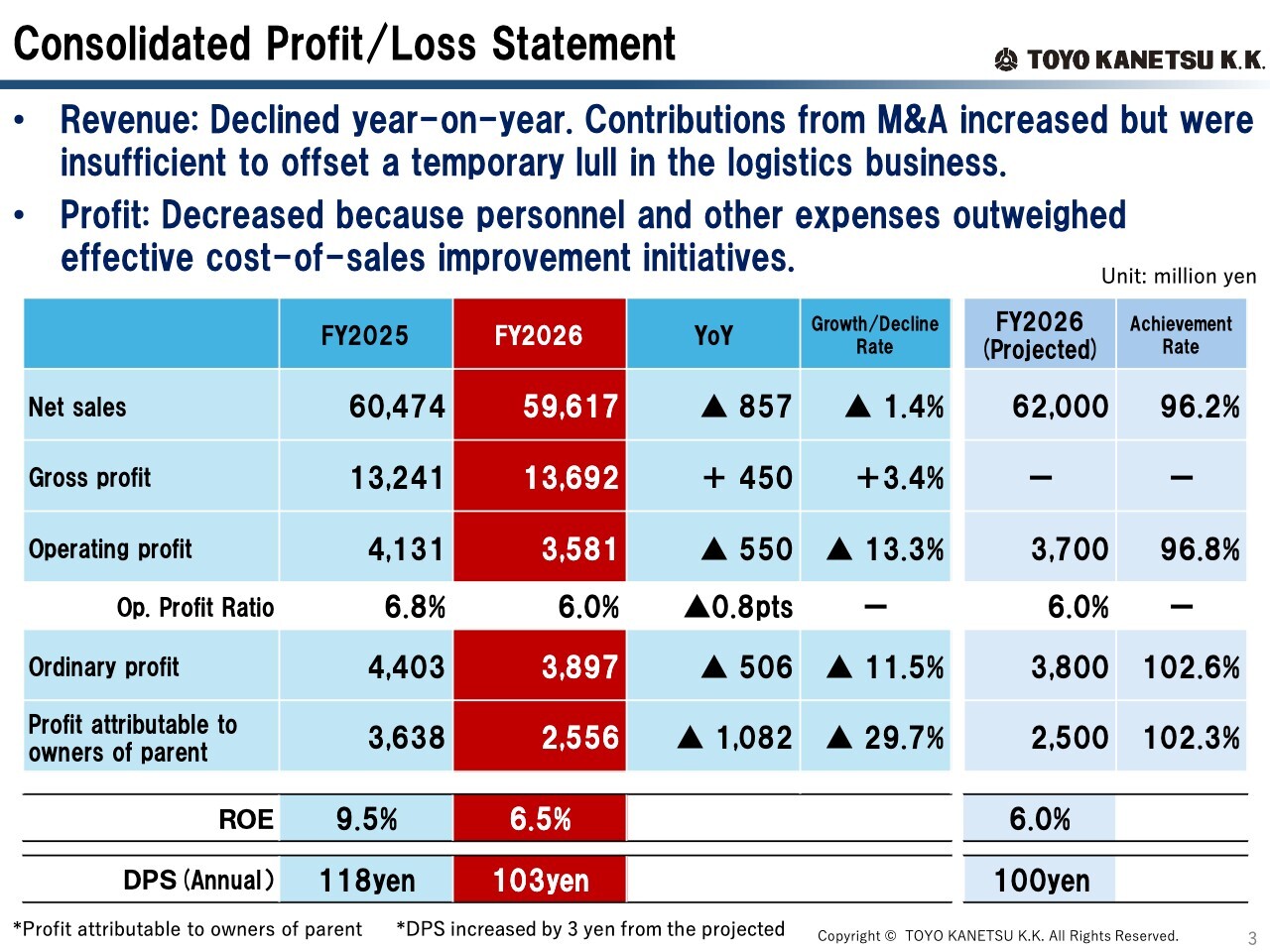

Consolidated Profit/Loss Statement

Let me now walk you through our FY2026 consolidated financial results. For the full year, revenue and earnings declined year-on-year. However, net sales were the second highest in our history, just below the record set in the prior fiscal year.

Net sales came in at ¥59,617 million. Although contributions from M&A added to revenue, net sales declined year-on-year as the Logistics Solutions Division fell below the previous fiscal year's level. Gross profit increased year-on-year as a result of our ongoing cost-of-sales improvement initiatives. Profit attributable to owners of parent decreased ¥1,082 million year-on-year to ¥2,556 million, reflecting the absence of the gain on sale of investment securities recorded as extraordinary income in the previous fiscal year.

Ordinary profit decreased ¥506 million year on year to ¥3,897 million. Profit attributable to owners of parent decreased ¥1,082 million year on year to ¥2,556 million, reflecting the absence of the gain on the sale of investment securities recorded as extraordinary income in the previous fiscal year. ROE was 6.5%.

The achievement rates against our full-year earnings forecast are shown in the far-right column of this slide. We had originally planned an annual dividend of ¥100 per share. However, in line with our shareholder return policy of maintaining a Dividend on Equity Ratio (DOE) of 4.0% or higher, we will increase the annual dividend by ¥3 from the full-year forecast to ¥103 per share.

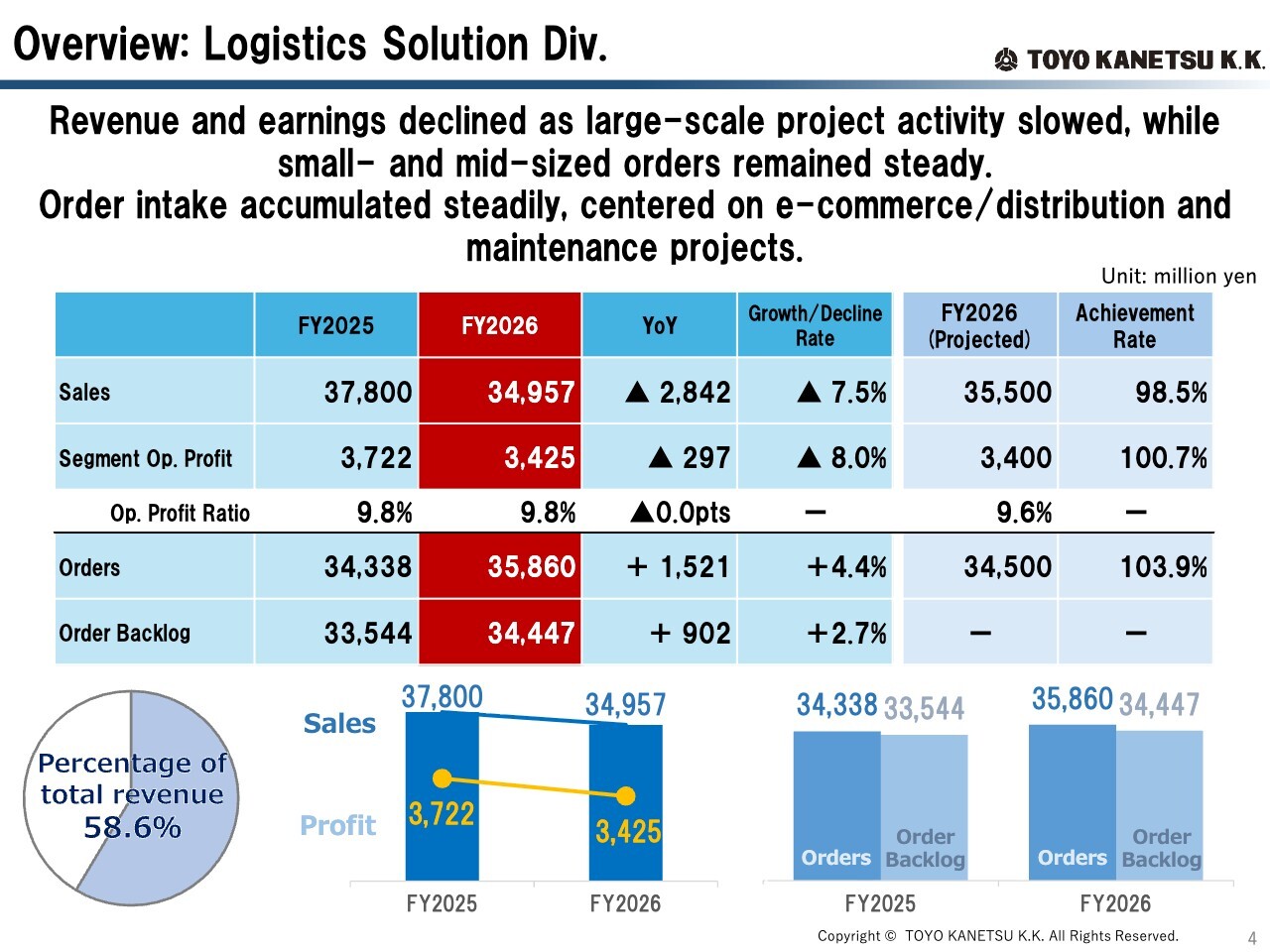

Overview: Logistics Solutions Div.

Let me walk you through the performance of each business segment. First, the Logistics Solutions Division. Sales came in at ¥34,957 million and operating profit came in at ¥3,425 million, with both revenue and earnings declining year on year. Large-scale project activity temporarily slowed. Although we actively captured small- and mid-sized orders, results fell short of the prior year. Overall, performance was broadly in line with our earnings forecast.

Meanwhile, order intake increased year-on-year to ¥35,860 million, remaining solid. Orders also exceeded the full-year target, reaching 103.9% of the plan and surpassing it by ¥1,360 million. Order backlog also remained high, increasing year-on-year to ¥34,447 million.

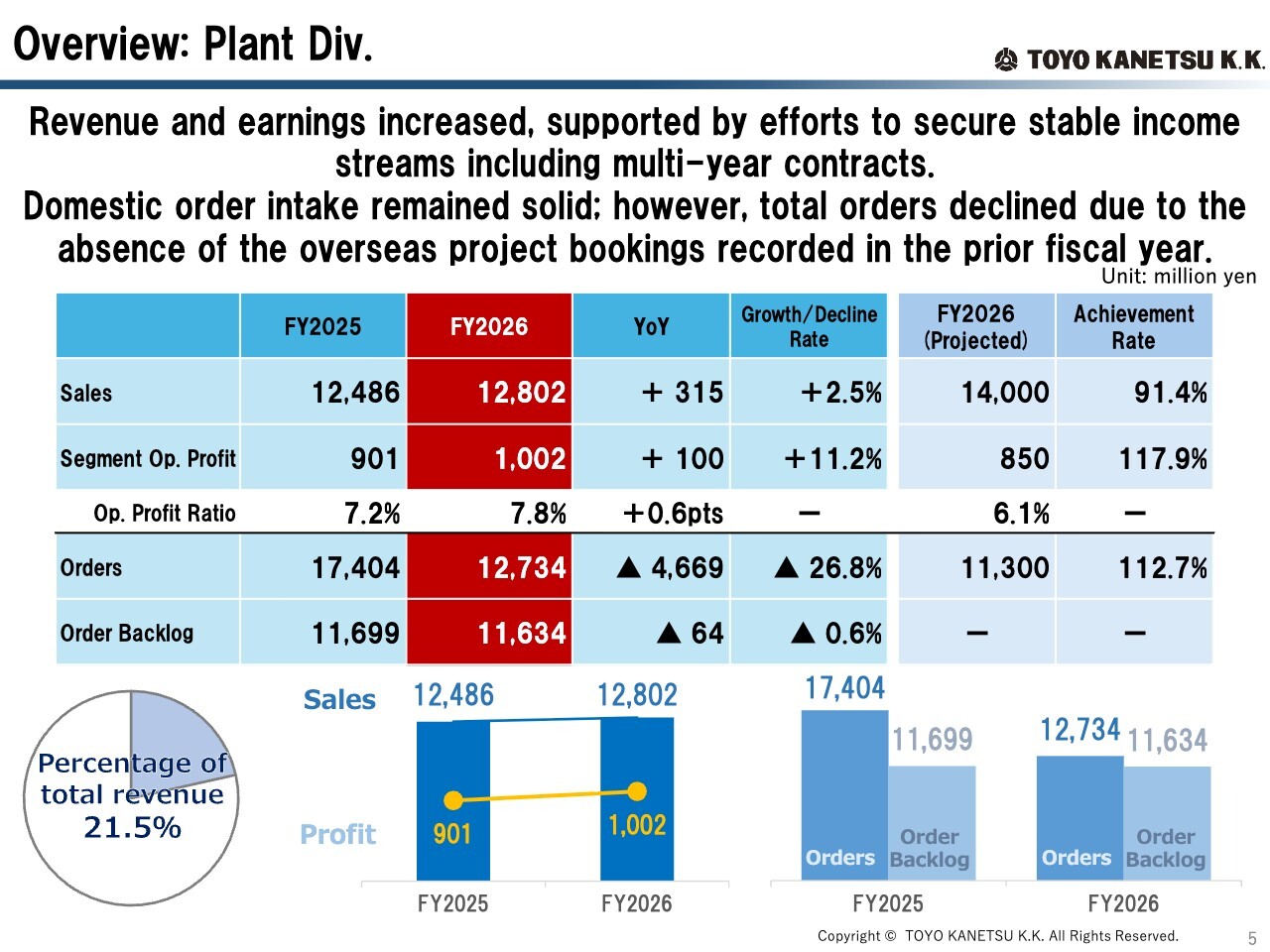

Overview: Plant Div.

Next, let me move on to the Plant Division. Sales came in at ¥12,802 million and operating profit came in at ¥1,002 million, with revenue and earnings increasing year-on-year. As a result of our continued focus on profitability, the operating profit margin also improved.

Although sales fell short of our forecast, this was primarily attributable to the inclusion of our overseas subsidiaries in this division following the organizational restructuring. Due to local conditions, progress on certain projects did not advance as originally anticipated.

Order intake decreased year-on-year to ¥12,734 million, primarily due to the absence of overseas tank refurbishment project bookings recorded in the prior fiscal year. We have established an order intake plan focused primarily on the domestic market, and we believe progress is generally on track. Order backlog stood at ¥11,634 million.

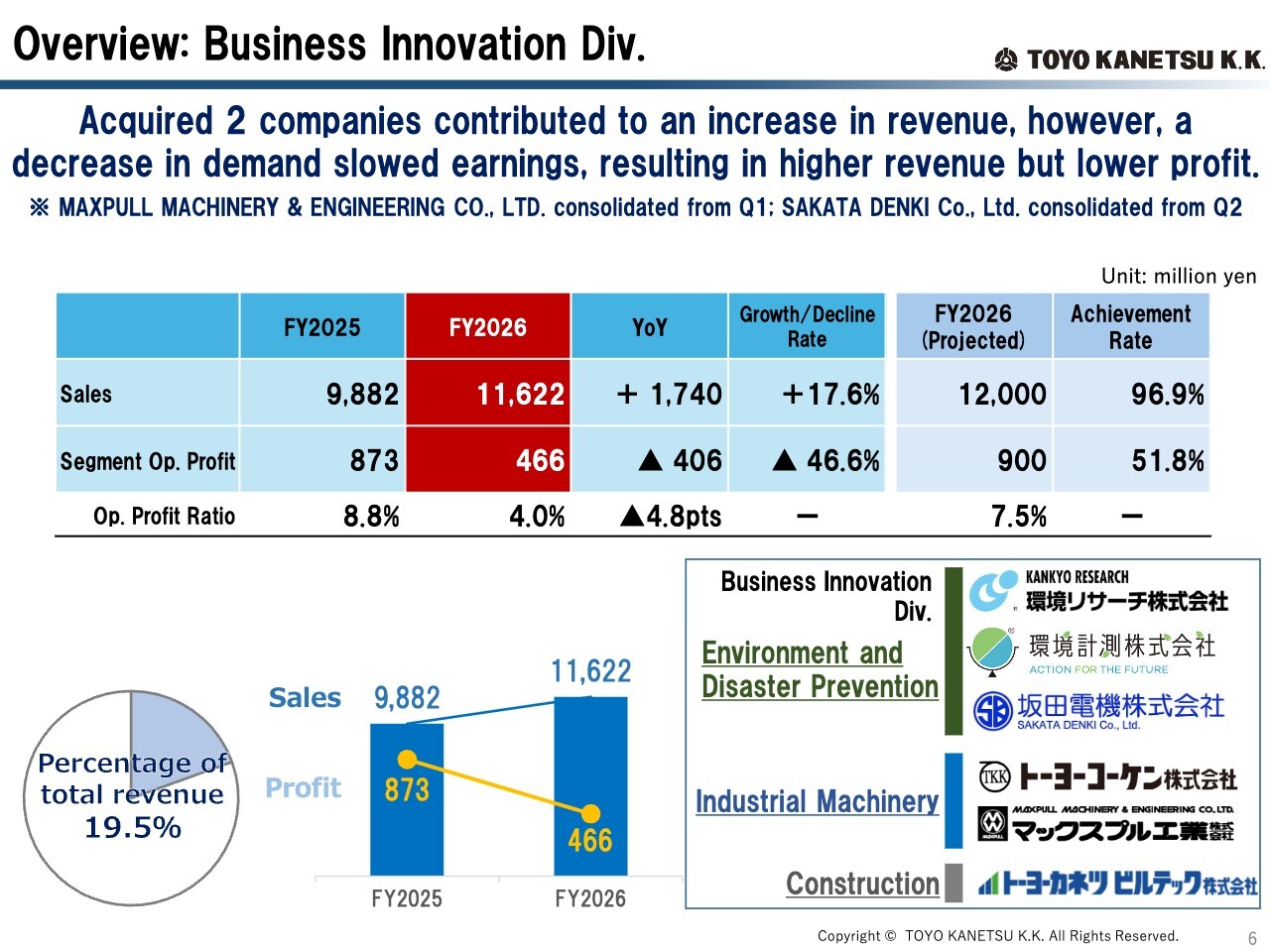

Overview: Business Innovation Div.

Finally, let me turn to the Business Innovation Division. Sales came in at ¥11,622 million and operating profit at ¥466 million, with revenue increasing but profit declining year on year. The increase in revenue was driven by the consolidation of two newly acquired companies. The decline in profit reflected reactionary declines at Kankyo Research Institute and Toyo Koken after they captured strong demand in the previous fiscal year.

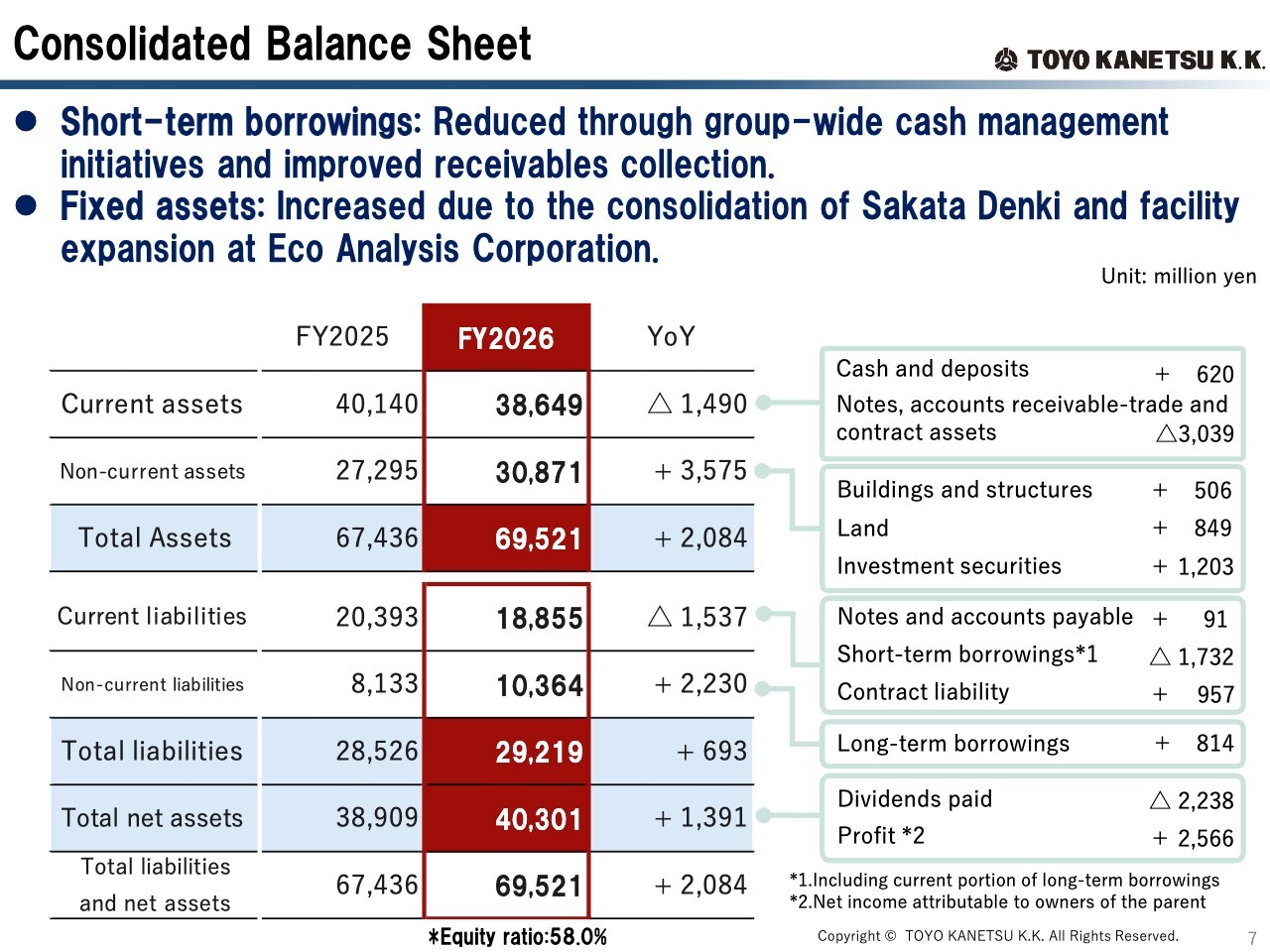

Consolidated Balance Sheet

Let me now turn to the consolidated balance sheet. Short-term borrowings were reduced through receivables collection and group-wide cash management initiatives. In addition, fixed assets and long-term borrowings increased, reflecting the consolidation of Sakata Denki and facility expansion at Eco Analysis Corporation.

The other major changes are as shown on this slide.

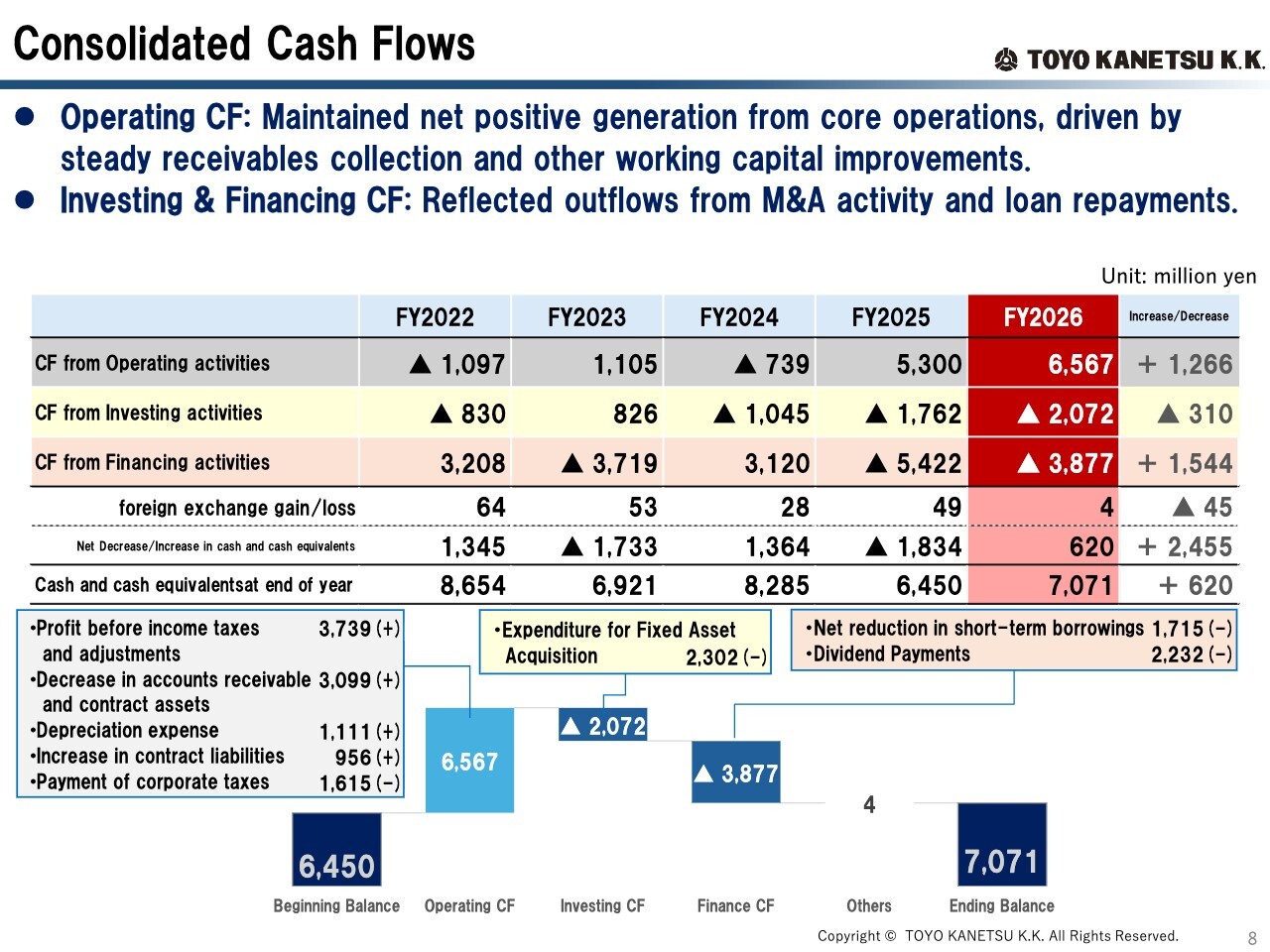

Consolidated Cash Flows

Turning to our consolidated cash flows, cash flows from operating activities improved, driven by steady receivables collection and an increase in contract liabilities, and were used to fund investing and financing cash outflows. Details on cash and cash equivalents and the key drivers are shown on the slide.

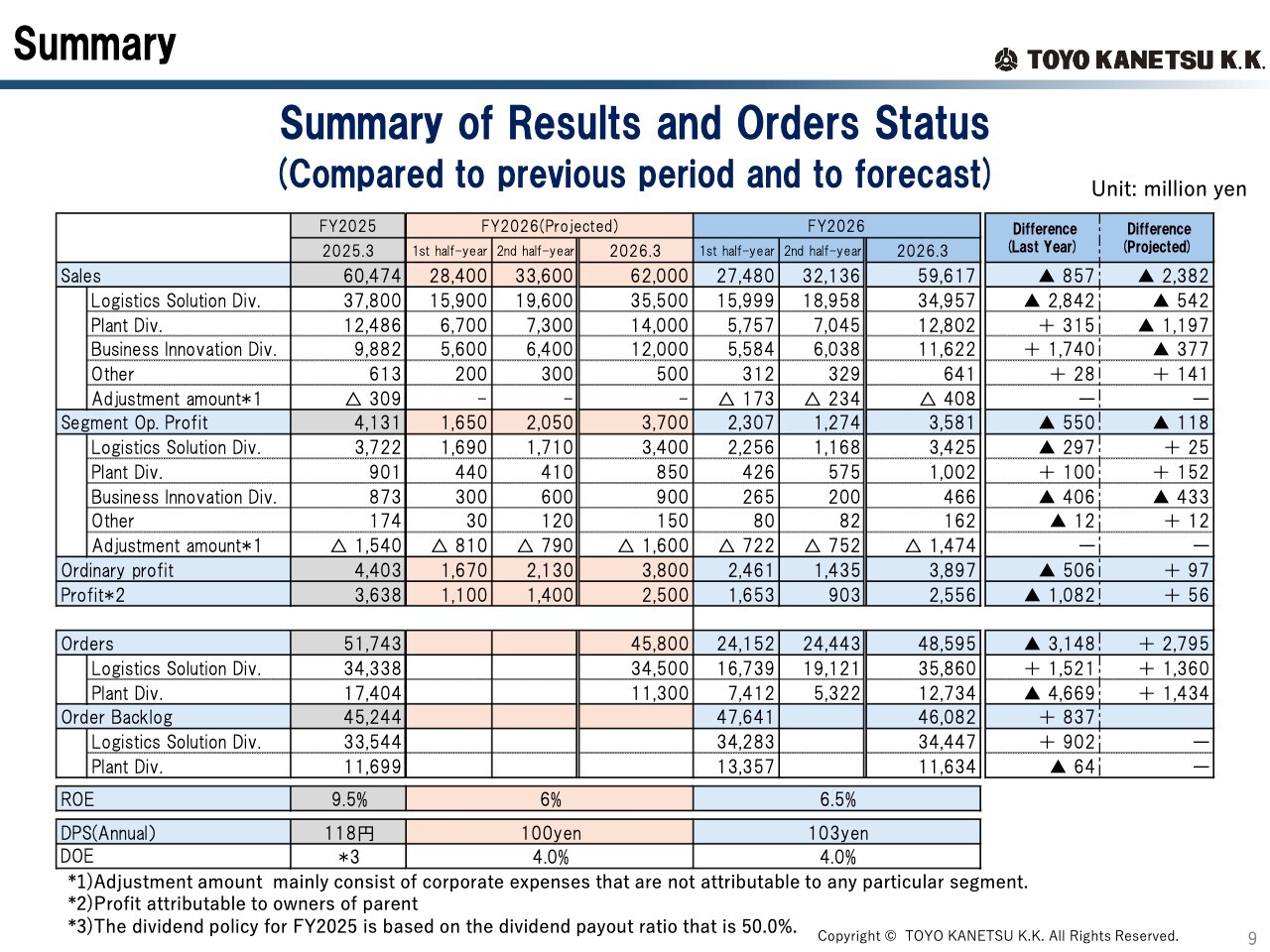

Summary

A summary of everything I have covered so far is shown on the slide. Please take a moment to review.

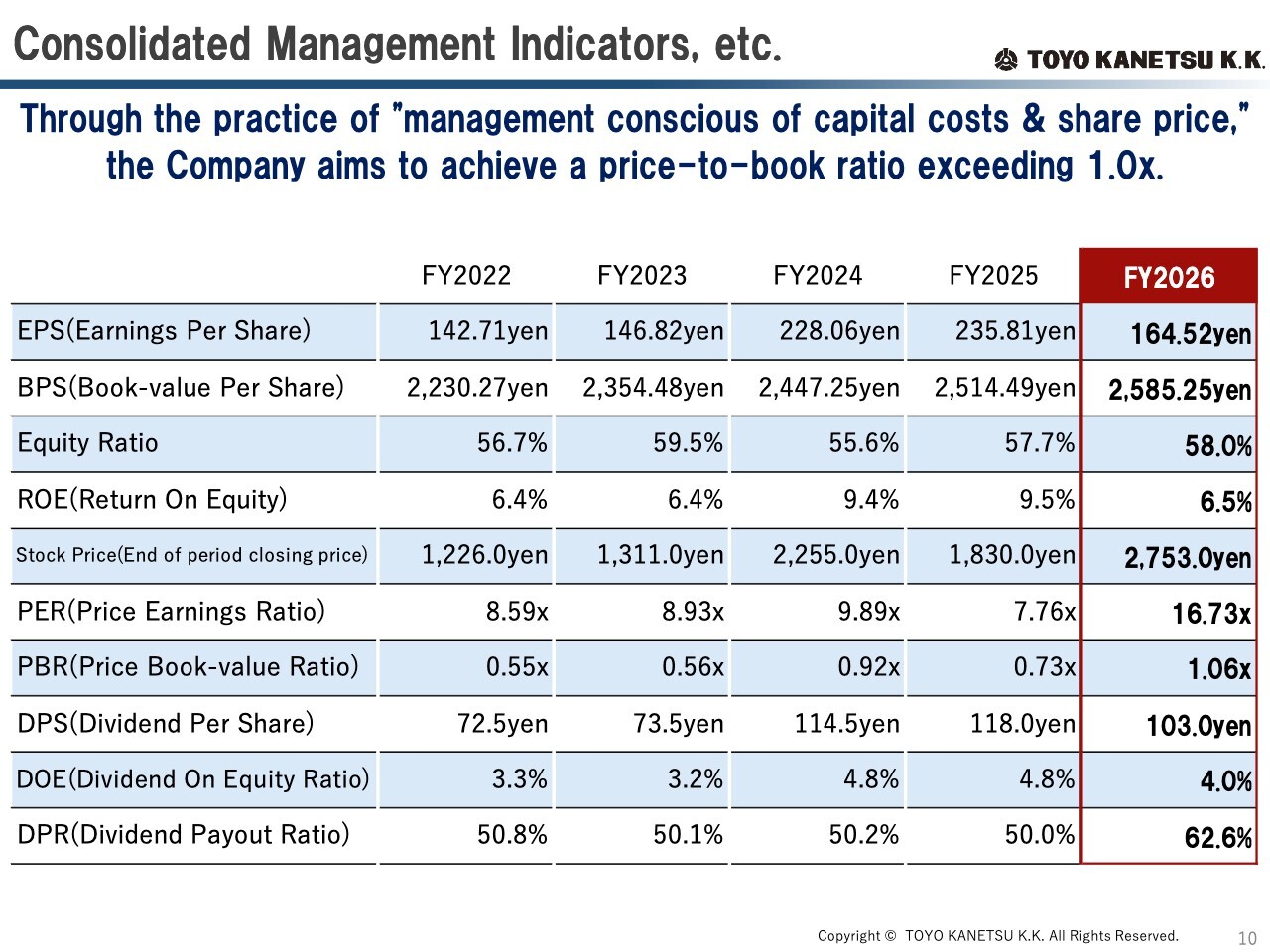

Consolidated Management Indicators, etc.

This slide shows our key consolidated management indicators. Through management with a focus on capital cost and share price, our price-to-book ratio has improved. Please also review this slide later.

This concludes our overview of the FY2026 financial results.

Toward the Future

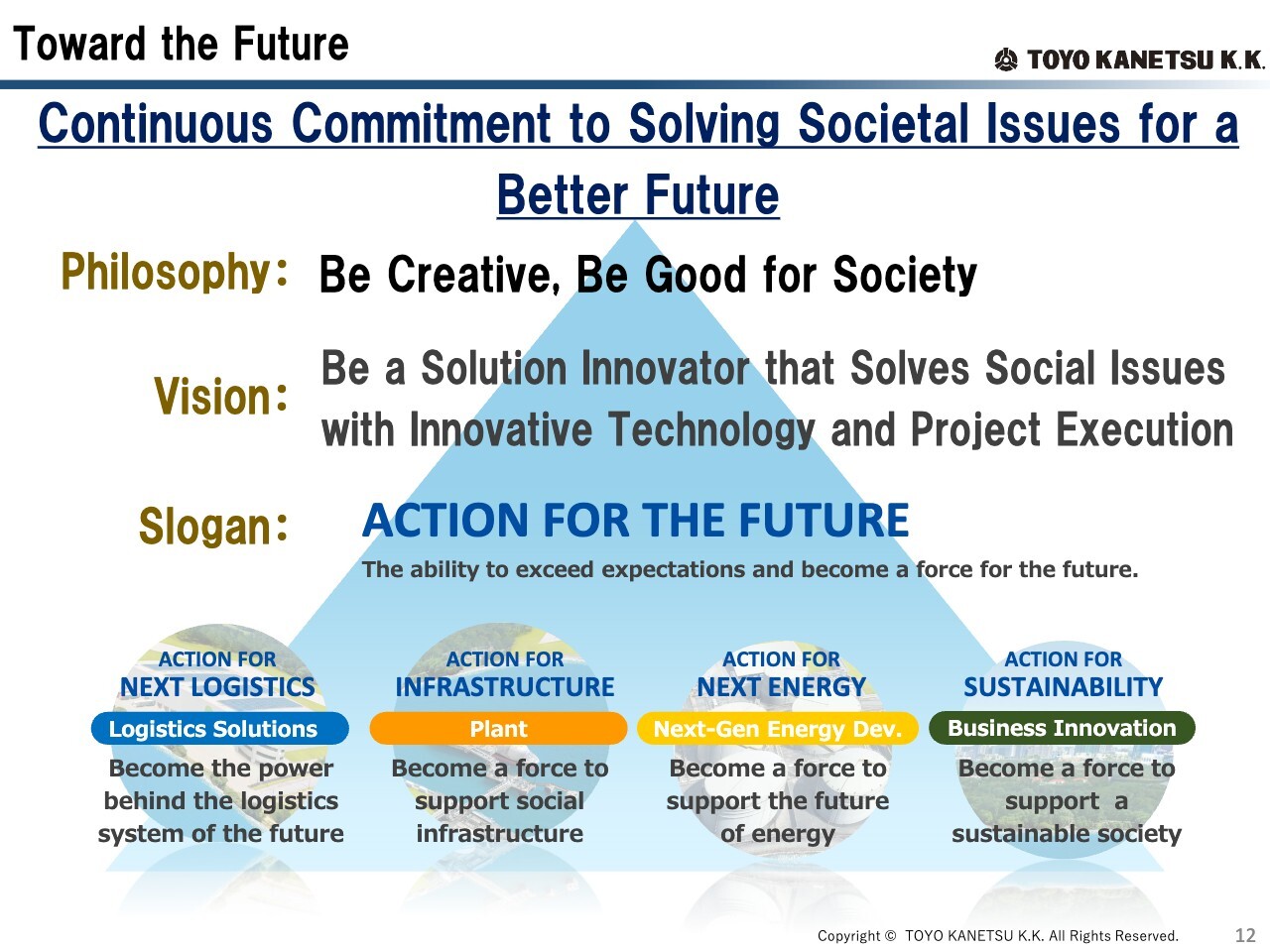

Next, I'd like to cover progress in the first year of our Mid-Term Management Plan and future developments. Let me begin with our vision for the future, which underpins the plan. Our Group's overarching goal is to be a company with a continuous commitment to solving societal issues for a better future.

Our corporate philosophy is rooted in our corporate motto, and our vision is to be a “Solution Innovator that Solves Social Issues with Innovative Technology and Project Execution.” As a manufacturing company, we are committed to continuously adopting new technologies and solutions to address challenges and support infrastructure. We believe that putting this into action is paramount, which is why our slogan is “ACTION FOR THE FUTURE.”

Toward the Future

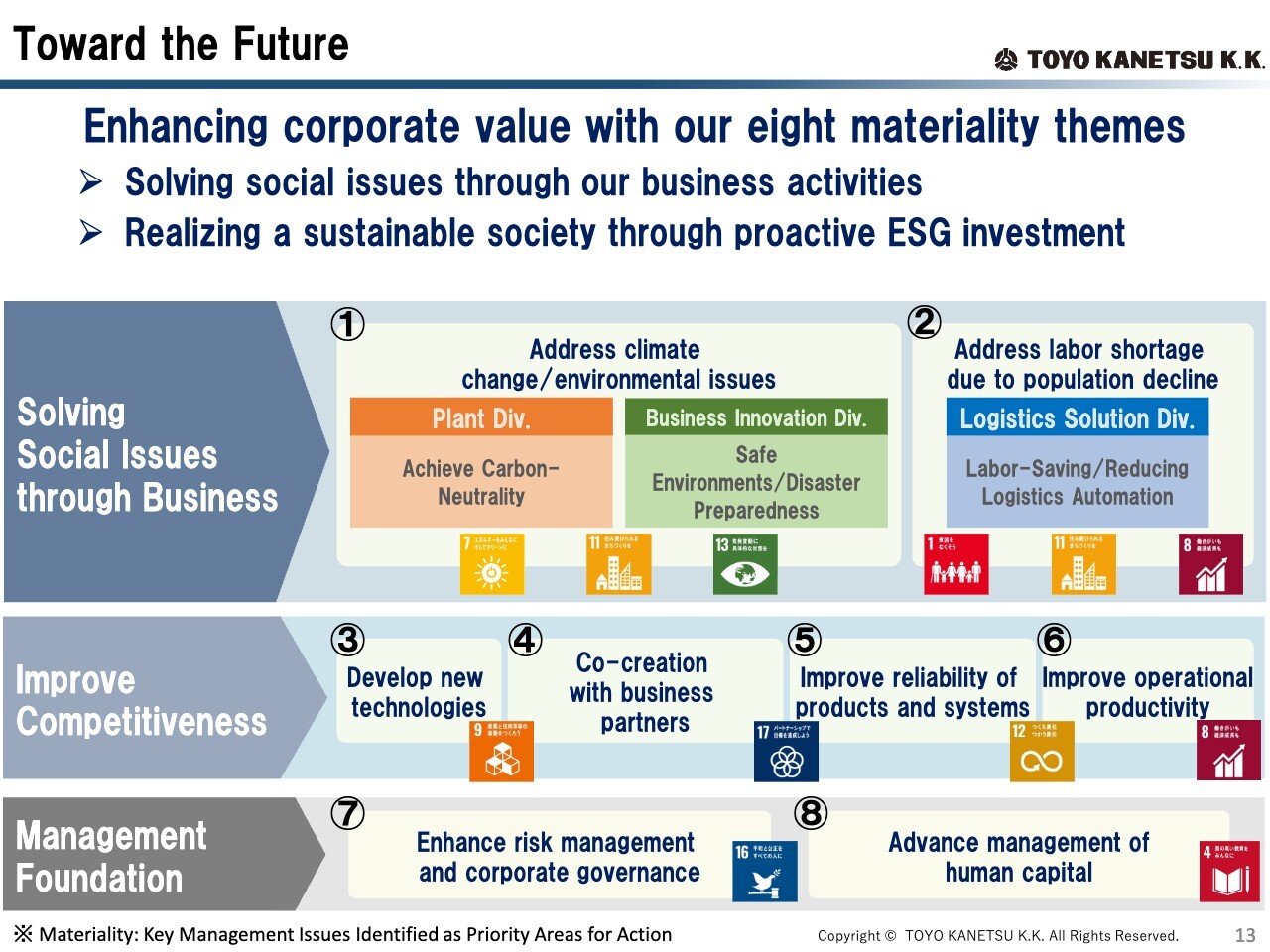

This slide outlines our key management priorities, or materialities, which represent priority areas for management action. In the previous fiscal year, we conducted a review and established eight new materialities, through which we are actively advancing ESG-focused management.

In particular, as key themes contributing to “Solving Societal Issues through Business,” we are driving three priority initiatives: achieving carbon neutrality through the Plant Division, building safe and resilient living environments with disaster preparedness through the Business Innovation Division, and promoting labor-saving and unmanned operations in the field through the Logistics Solutions Division. Through these efforts, we remain committed to contributing to the realization of a sustainable society.

Toward the Future (Medium-Term Plan)

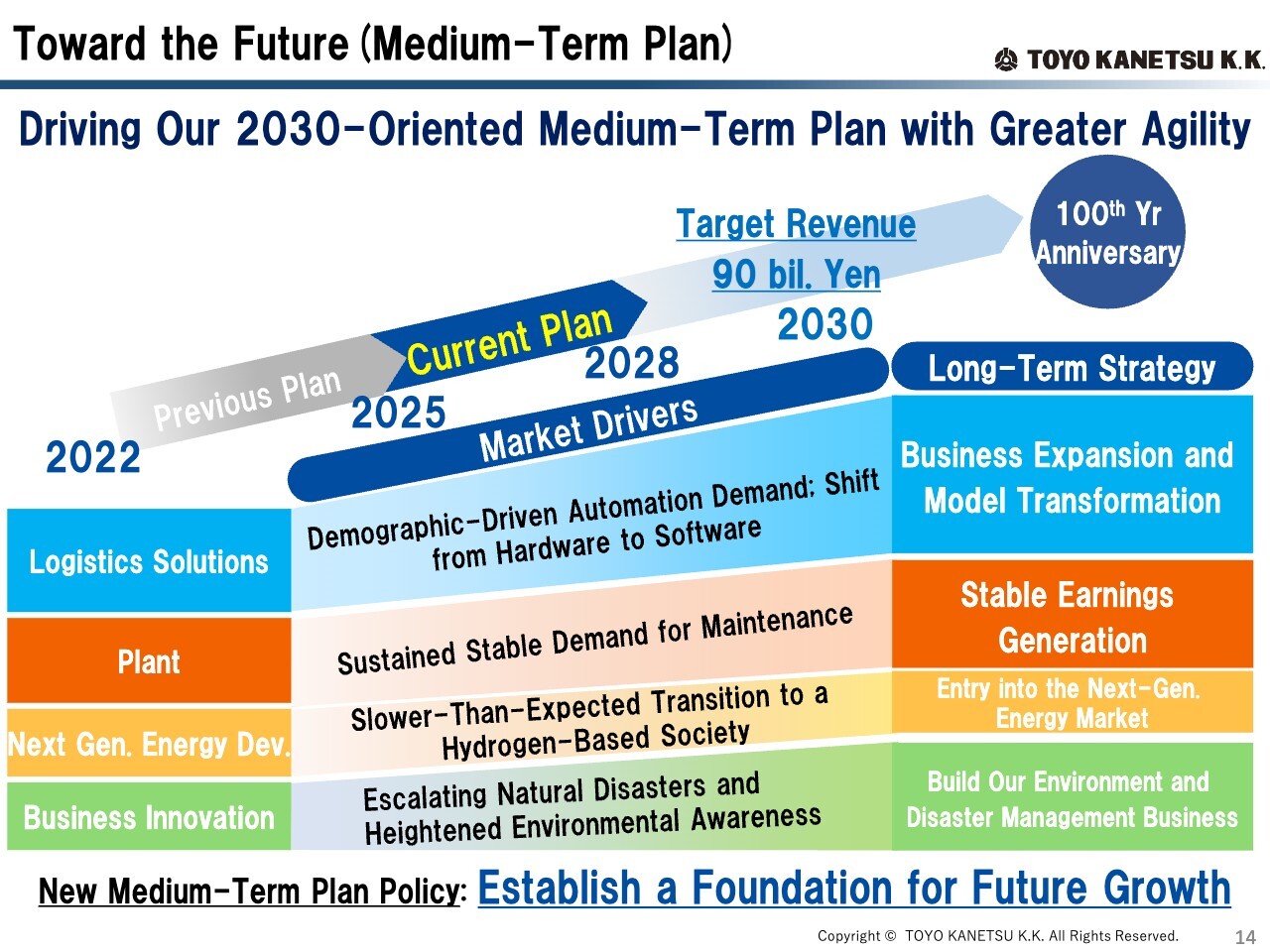

This slide shows the positioning of our current Medium-Term Management Plan within our long-term strategy. In the market served by our core Logistics Solutions Division, automation demand continues to grow against the backdrop of a declining working-age population, and the importance of software solutions, in addition to hardware, is increasingly recognized.

In the Plant Division, we expect maintenance demand to remain stable, given the current energy environment. In Next-Generation Energy Development, we will continue our research and development of hydrogen tanks in preparation for the transition to carbon neutrality. The Business Innovation Division, with its focus on environment and disaster prevention, will work to protect living environments through disaster prevention and prediction efforts in response to increasingly severe natural disasters.

With these factors in mind, we have established our Medium-Term Management Plan policy through FY2028 as “Establish a Foundation for Future Growth.”

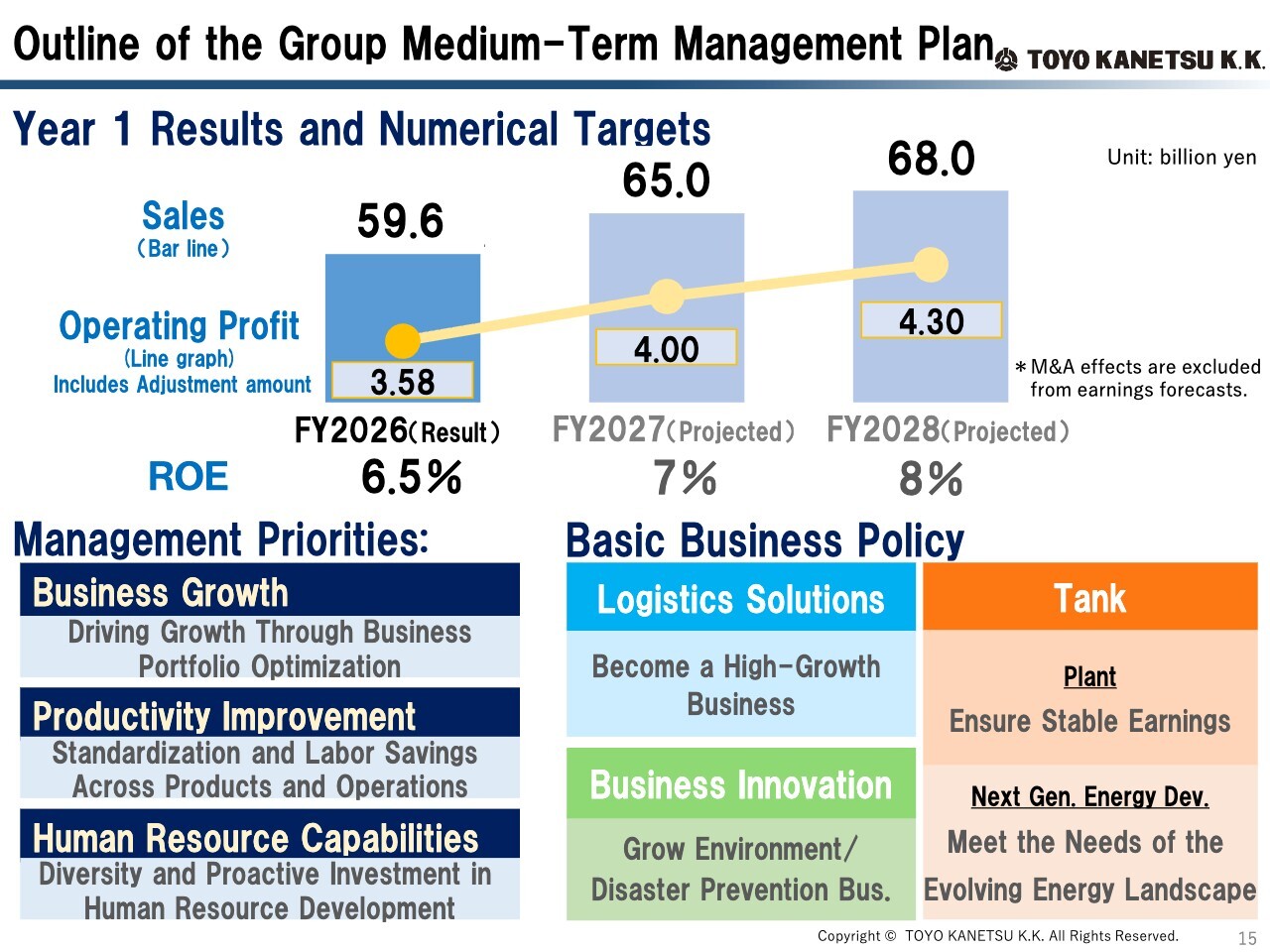

Outline of the Group Medium-Term Management Plan

I reported earlier on our first-year results under the Medium-Term Management Plan. As shown on the slide, we will continue to build on our performance in years two and three. Our KPI for the final year is to achieve an ROE of 8% or more from core businesses.

We have also clearly defined three management priorities to be addressed across the entire company. These three priorities are led by the directors, and based on these management initiatives, each division head is responsible for driving business expansion under the basic policy. I will cover the progress and future developments of each on the following slides.

Progress on Management Priorities

Let me now walk you through our initiatives for each of the three management priorities. Starting with the first priority, “Business Growth.” To enhance corporate value with greater speed, we have begun preparations for the transition to a holding company structure. I will cover this in more detail in the “Future Developments” section.

The second priority is “Productivity Improvement.” We have rolled out generative AI across the entire company. We determined that recent advances in AI technology had reached a level where they could be effectively leveraged to improve productivity across our operations, and moved quickly to implement them. We are already seeing tangible results in the field, including the development of AI agents that are reducing working hours.

The third priority is “Strengthening Human Resource Capabilities.” We are preparing a new HR system, which we plan to fully implement starting in October this year. As shown on the slide, we are moving beyond basic OJT. We will establish a formal system that encourages employees to proactively acquire new knowledge and put it into practice, directly linking these efforts to evaluations, promotions, and compensation. We will also incorporate behavioral assessments for managers to strengthen organizational management capabilities, thereby building a stronger organization. In addition, we will continue to implement base salary increases going forward.

Logistics Solutions Business: Progress and Developments

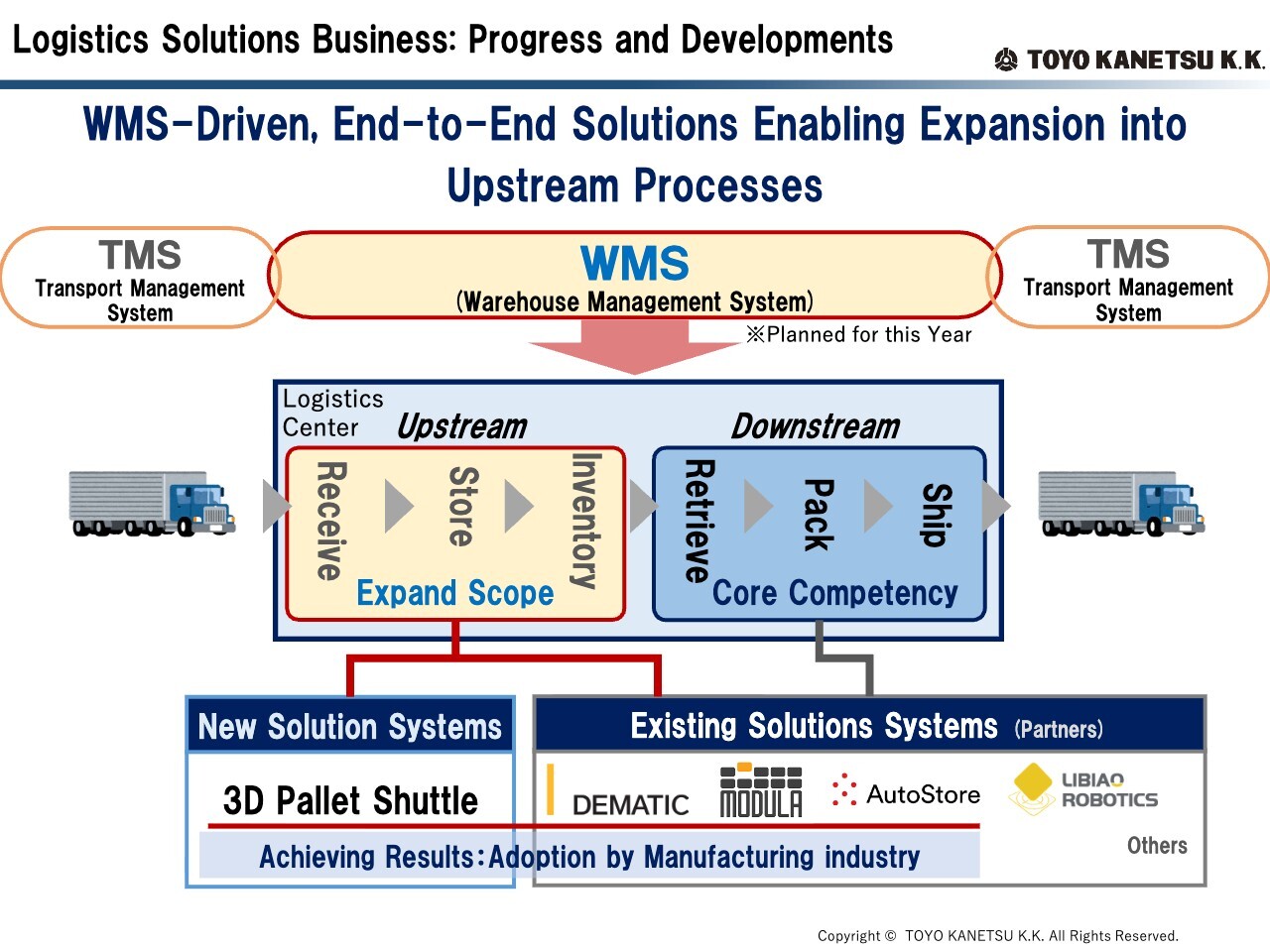

Let me now turn to progress and future developments across each of our business segments. Starting with the Logistics Solutions Division, our core competency lies in downstream processes at logistics centers — specifically retrieval, packing, and shipping — which are the most labor-intensive operations. However, there remains significant room to expand our business scope in upstream processes, particularly receiving and storage. To address this, we have been developing a Warehouse Management System, or WMS, over the past several years.

This enables us to capture data across the entire logistics center, making it possible to offer comprehensive solutions covering the full range of processes, including upstream operations. We have already built out a lineup of systems that cover all processes, and have begun delivering these solutions to clients in the manufacturing industry.

Once WMS is adopted and goes live, we expect the rollout of solutions covering the full range of processes — from upstream to downstream — to accelerate, driven by the increasing number of center-wide renewals going forward. Ultimately, by integrating WMS with a Transport Management System, or TMS, we aim to address the transportation challenges surrounding logistics centers — the so-called “2024 Logistics Problem” — through the power of software solutions.

Logistics Solutions Business: Progress and Developments

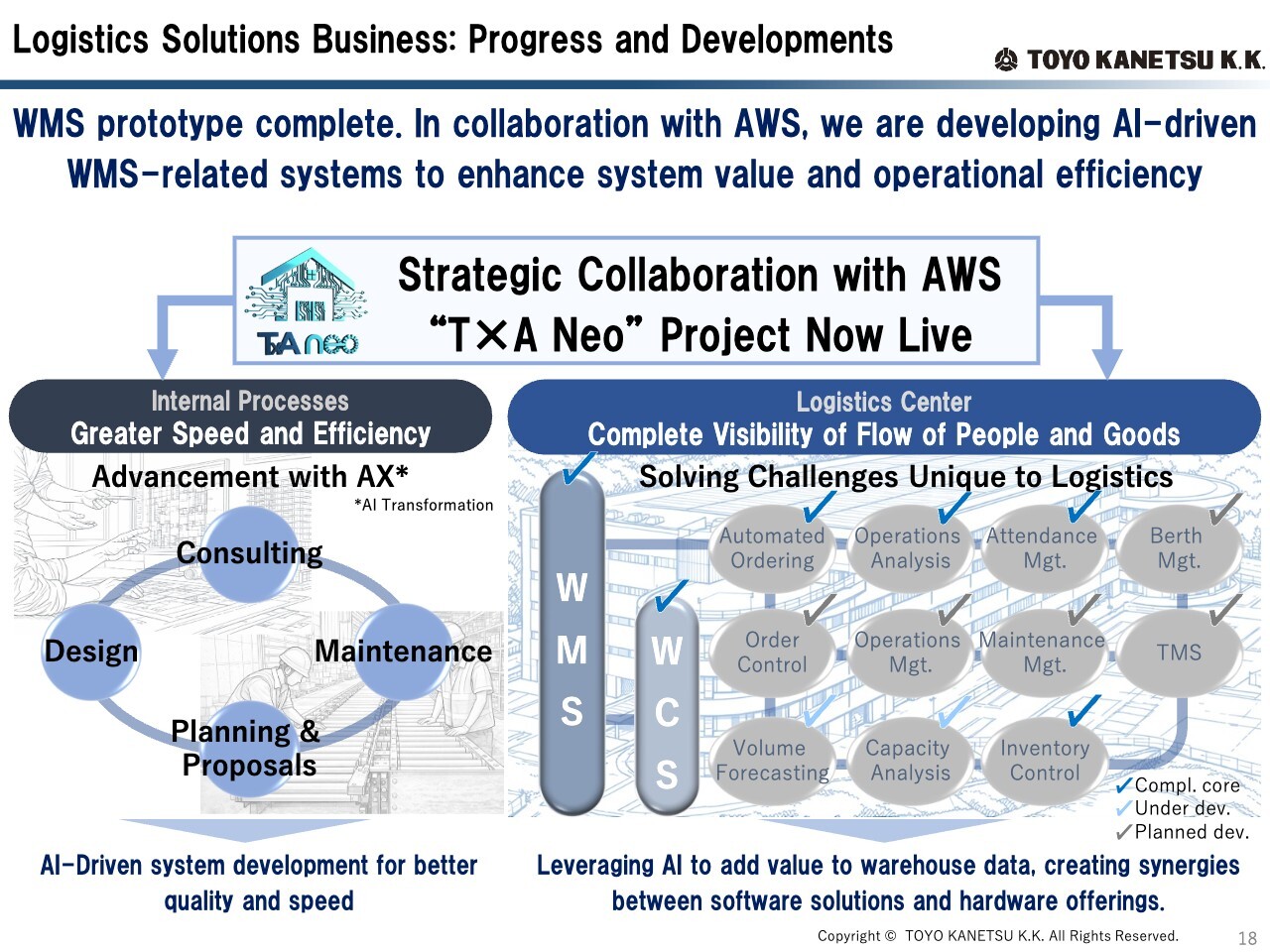

Let me now cover the progress and developments of our WMS. The WMS prototype is already complete, and we have entered the implementation phase. We have a deep understanding of the unique challenges and pain points of logistics center operations. With this in mind, we are developing a suite of supporting foundational systems to visualize not only the flow of goods but also the movement of people, enabling us to address the full range of logistics center challenges through the power of software solutions.

We have also launched the “T×A Neo” project in collaboration with AWS Professional Services, leveraging AI for business applications. This initiative combines AI with our suite of foundational systems to quickly customize and deliver solutions tailored to each customer's unique needs, even when their business requirements may appear similar on the surface.

Furthermore, by leveraging AI in upstream internal processes in particular, we aim to reduce lead times within our business workflows, increase the depth and frequency of customer dialogue, and broaden points of contact. We intend to be early adopters of the remarkable advances in AI, embedding them into both our internal and external business activities to build a more systematic revenue generation model.

Tank Business: Progress and Developments

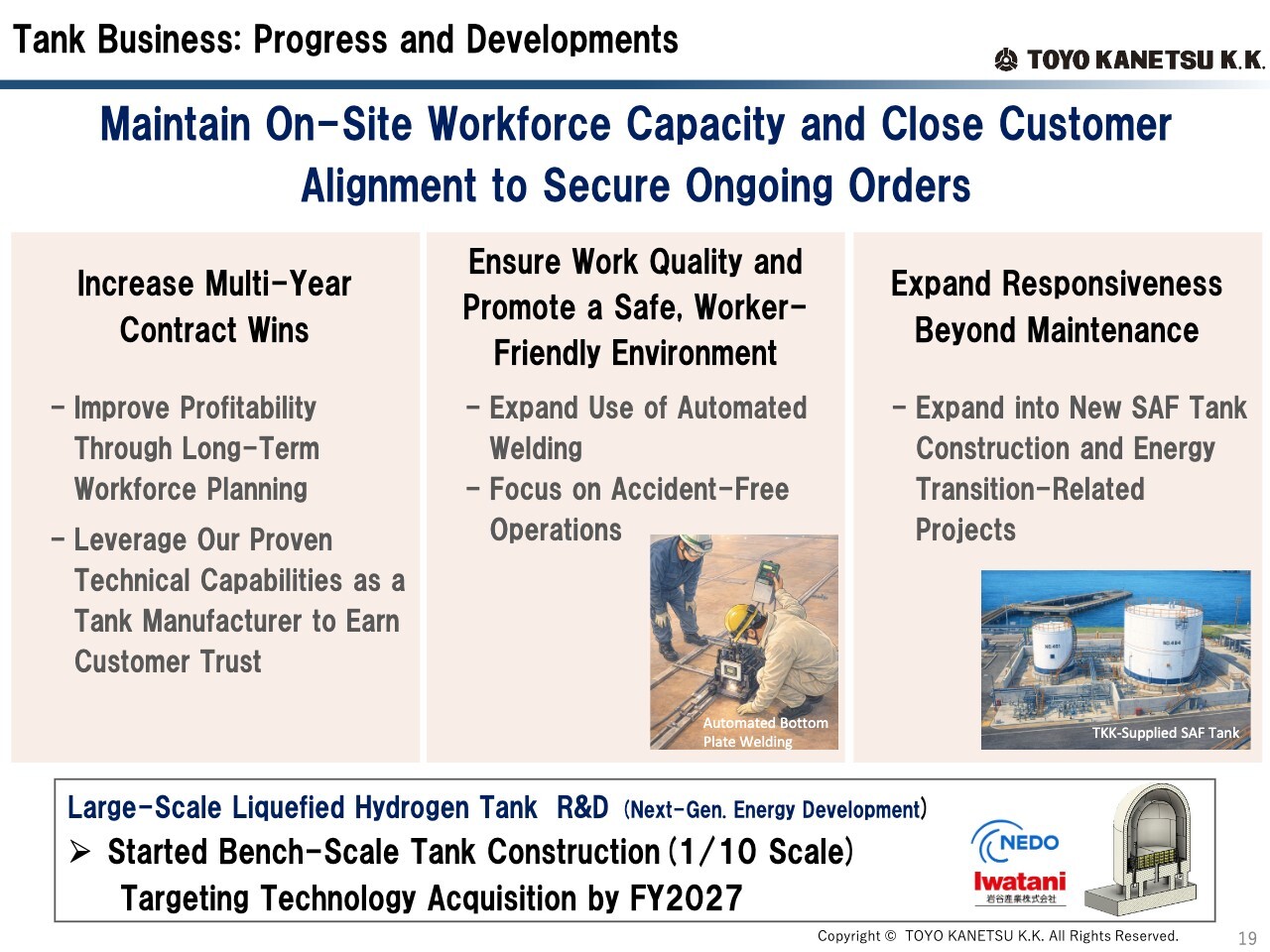

Next, let me turn to the Plant Division, which primarily handles maintenance of domestic crude oil tanks. Securing on-site personnel is a critical challenge in this industry. By proactively proposing multi-year contracts to our customers, we are able to establish longer-term workforce plans, creating a win-win arrangement for both our customers and ourselves, and enabling more efficient maintenance operations.

We are also bringing our proven technical capabilities and on-site management expertise as a tank manufacturer to our maintenance operations. Specifically, we are focused on creating a worker-friendly environment and ensuring work quality and safety, and have achieved accident-free operations.

Beyond our existing operations, we are also actively capturing new demand in the field, including new SAF tank construction and energy transition-related projects. Through these ongoing efforts, our operating profit ratio has also been improving.

Regarding large-scale liquefied hydrogen tanks, we have commenced construction of a one-tenth-scale bench-scale tank, with the goal of completing technology acquisition by the fiscal year ending March 2028. We will continue to advance our research and development in line with our plan.

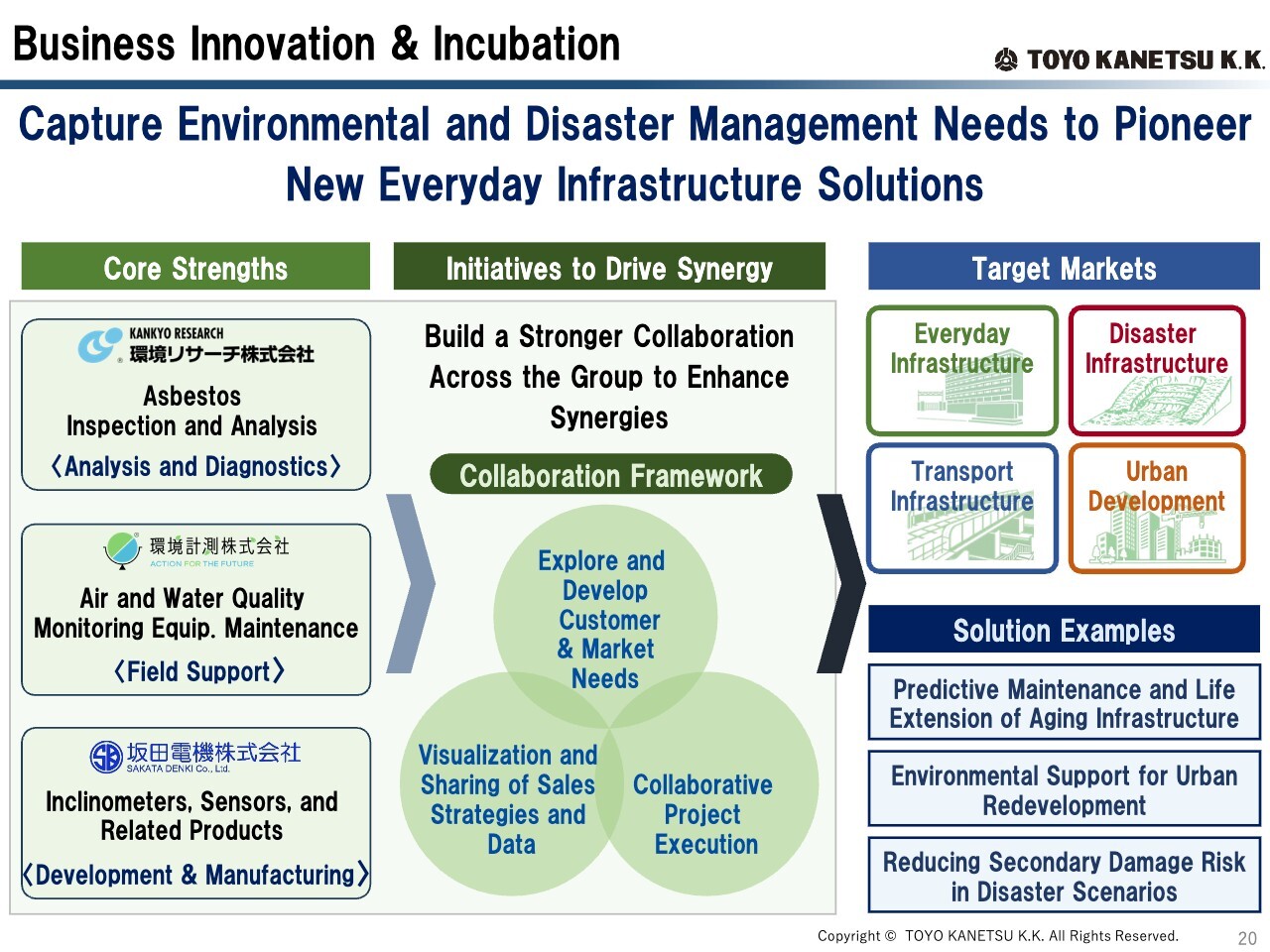

Business Innovation & Incubation

Let me now turn to the initiatives of the Business Innovation Division, which is focused on the environment and disaster prevention. We are identifying the strengths of each Group company and bringing together our proprietary technologies to lay the groundwork for generating synergies.

Specifically, we are establishing a collaboration framework among the three affiliated companies, increasing the frequency of business-focused information exchange, and raising the level of engagement across market exploration, customer information sharing, project formation, target identification, and solution concept development — all with the goal of bringing synergies to fruition. We will also expand our business in the direction of predictive maintenance and prevention for everyday infrastructure, and develop this into our third pillar of growth.

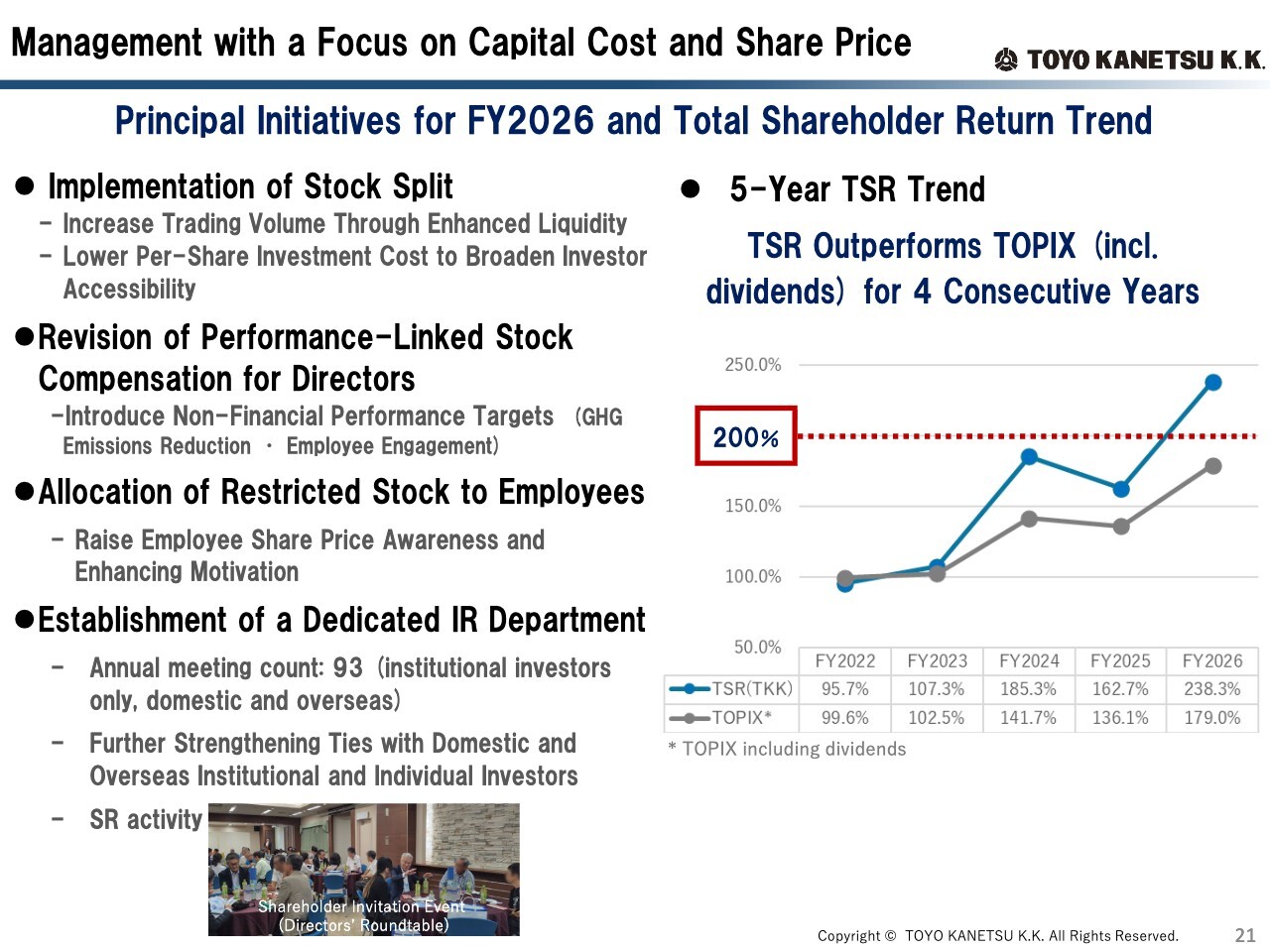

Management with a Focus on Capital Cost and Share Price

The final topic under progress is management with a focus on capital cost and share price. The left side of the slide outlines the initiatives we have already implemented. Through measures including a stock split to enhance liquidity, our Total Shareholder Return, or TSR, exceeded 200%.

Through our IR activities, we have been actively strengthening relationships with shareholders and holding briefings for individual investors. In particular, we held a total of 93 meetings with domestic and overseas institutional investors over the course of the year. We remain committed to continued engagement with the market through ongoing dialogue, and we look forward to your continued support.

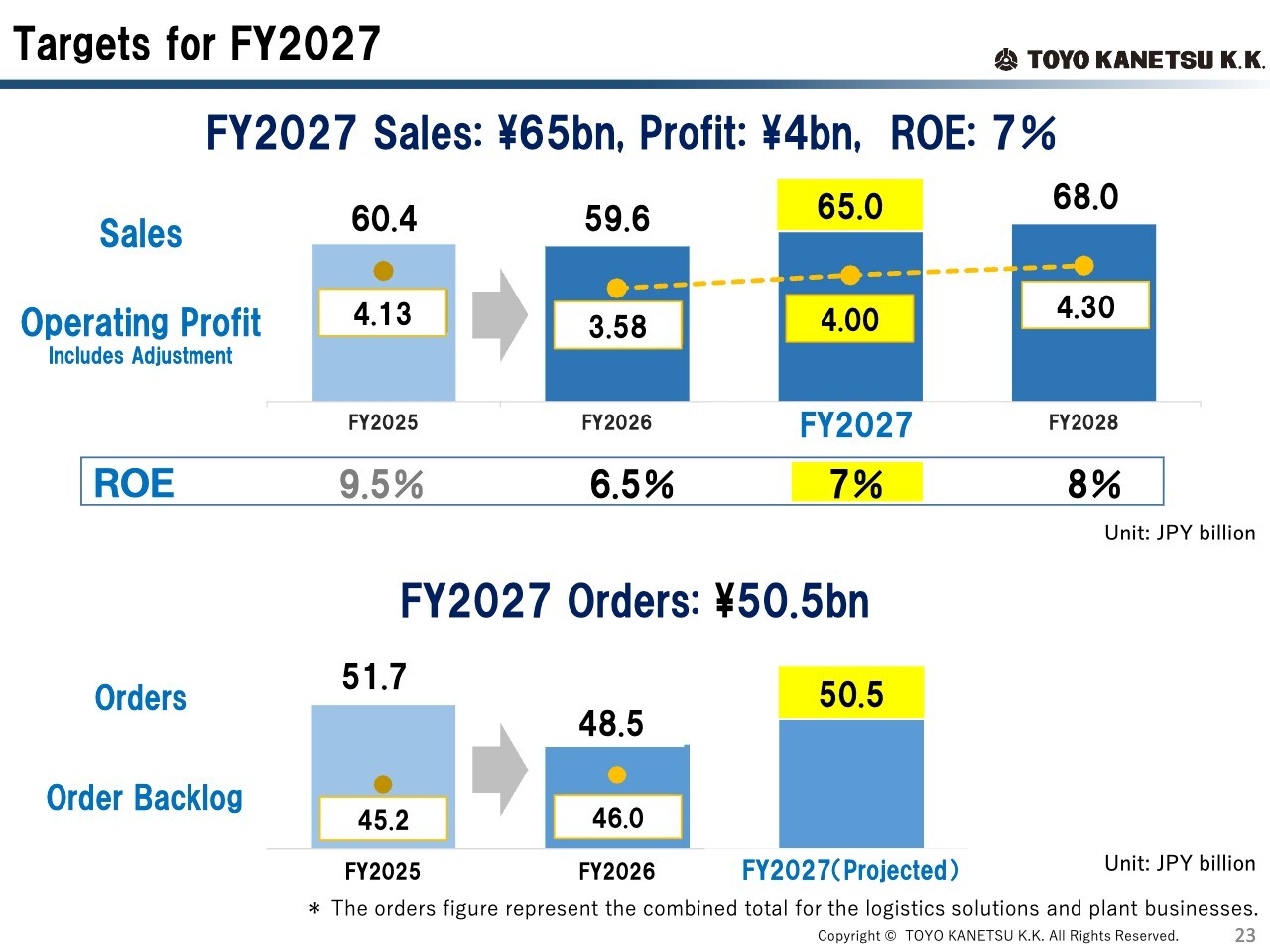

Targets for FY2027

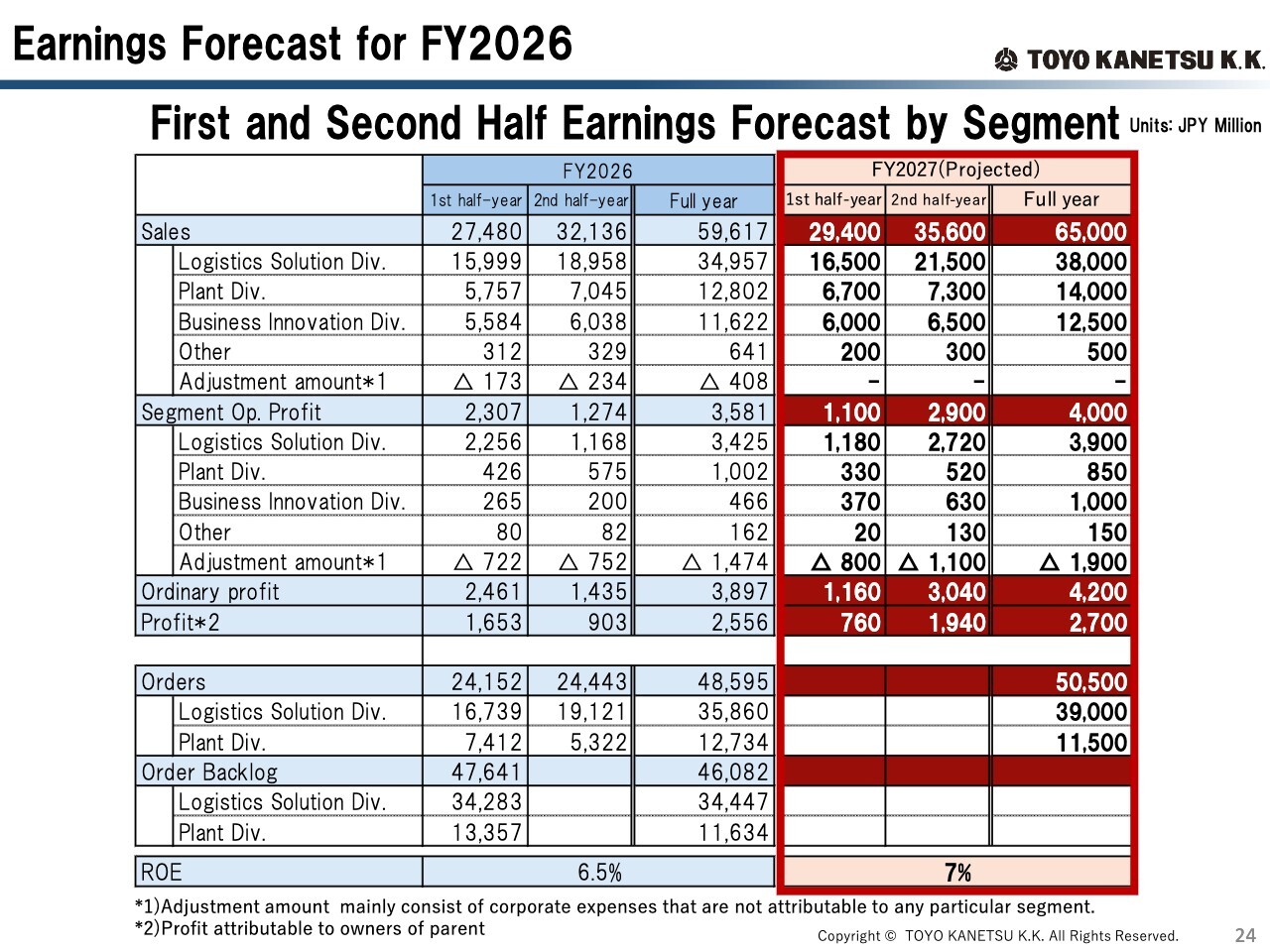

Moving on to our earnings forecast for FY2027. We expect sales to increase 9% year on year to ¥65.0 billion, operating profit to increase 12% year on year to ¥4.0 billion, and ROE of 7%. We are also targeting orders of ¥50.5 billion. Further details will be covered on the next slide.

Earnings Forecast for FY2027

The figures highlighted in red on the slide represent our FY2027 earnings forecast. The Logistics Solutions Division is expected to recover gradually over the course of the year. The Plant Division is expected to maintain stable earnings. The Business Innovation Division plans to build up earnings, including the full-year contribution from Sakata Denki.

Please refer to the slide for further details.

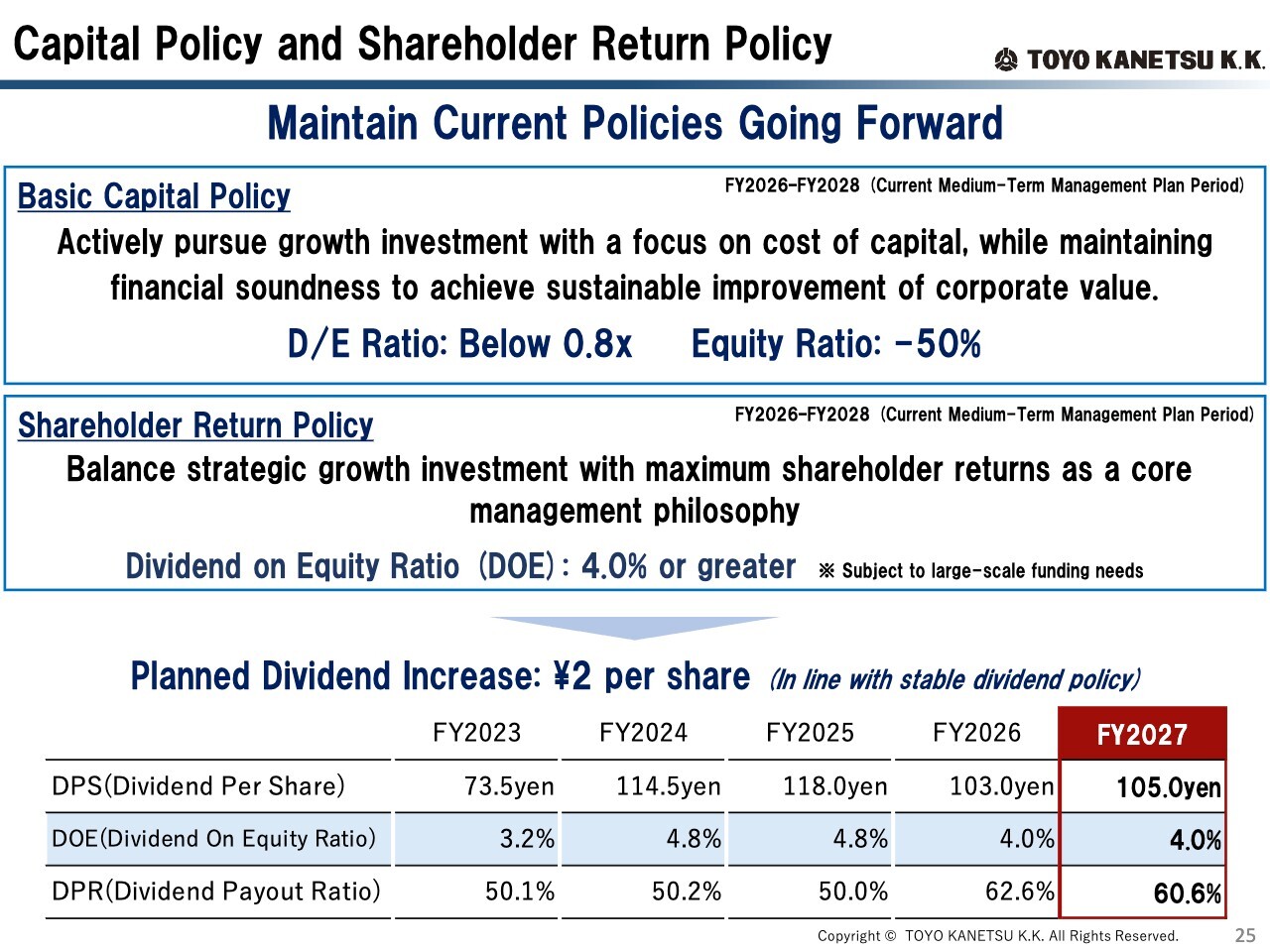

Capital Policy and Shareholder Return Policy

Our capital policy and shareholder return policy remain unchanged, as shown on the slide. For FY2027, we plan to increase the dividend by ¥2 to ¥105 per share, in line with our policy of maintaining a Dividend on Equity ratio, or DOE, of 4.0% or greater, with the aim of providing stable dividends. We intend to maintain the policies shown on the slide going forward.

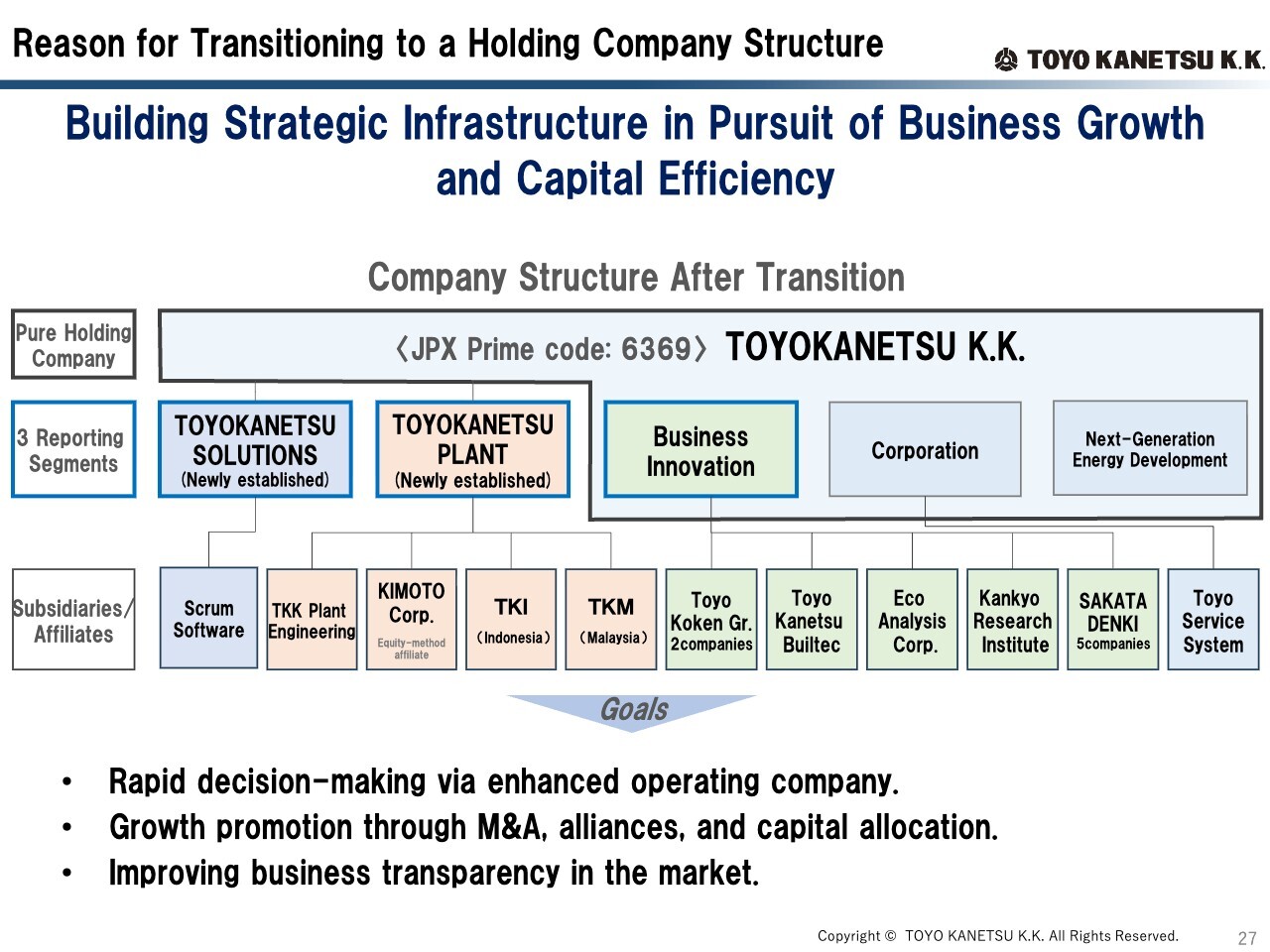

Reason for Transitioning to a Holding Company Structure

The final topic in today's presentation is our future developments. This slide outlines our planned transition to a holding company structure.

To drive our Group's future growth, we aim to develop the Logistics Solutions Division and the Plant Division — which together account for 80% of our Group's total revenue and profit — under management structures tailored to the unique characteristics of each business.

These two divisions differ significantly in terms of market environment, customer base, business partners, ways of working, and required technologies. For this reason, we have determined that transitioning to a holding company structure is the best course of action. Specifically, as shown on the slide, the Logistics Solutions Division and the Plant Division will each be established as new operating subsidiaries under the holding company.

There are three key goals and objectives. First, rapid decision-making by strengthening operating companies. Second, growth promotion through M&A, alliances both within and outside the Group, and other initiatives. Third, improving business transparency for the market. By pursuing these goals, we aim to further enhance corporate value through accelerated business growth.

This concludes today's presentation. Thank you very much for your attention.

Q&A: On the Expected Benefits of WMS and TMS Integration

Questioner: I have a question about the Logistics Solutions business. Could you tell us what benefits you expect from integrating WMS and TMS?

Owada: As I mentioned earlier, we discussed the “2024 Logistics Problem.” In considering what aspects of this problem we could address through our core focus on logistics center efficiency, we identified prolonged truck dwell time at logistics centers as a key challenge. This occurs because situations arise where goods for delivery cannot be received smoothly, or shipments cannot go out because the required items are not yet ready.

By integrating TMS — which manages truck transportation operations — with our WMS warehouse management system, we aim to align logistics center operations with truck schedules, thereby minimizing truck idle time as much as possible. We believe this will contribute to resolving the “2024 Logistics Problem,” and we are advancing our development efforts accordingly.

Questioner: You mentioned reducing truck idle time and shortening cargo waiting times. With the revised Logistics Efficiency Act also in mind, are you considering selling these solutions externally to shippers and logistics operators as well?

Owada: Regarding the integration of WMS and TMS, as the WMS is still at the prototype stage, it will take a little more time. However, as I explained earlier in the WMS progress update, we expect TMS to be incorporated once all the various components are in place. At that point, we intend to move forward with external sales. We would like to start by introducing these solutions into the consumer cooperative and e-commerce markets, where we have particular strength.

Questioner: So your initial target would be operators engaged in consumer cooperative and e-commerce logistics. Is that correct?

Owada: That is correct.

Q&A: On the Purpose of the Transition to a Holding Company Structure

Questioner: You mentioned the transition to a holding company structure for the Logistics Solutions business. Is the purpose to strengthen rapid decision-making at the operating company level, as well as to promote M&A and alliances both within and outside the Group?

Owada: Yes, that's right. We have a history of growing organically, centered on the Logistics Solutions and Tank businesses. By transitioning to a holding company structure, we intend to separate the Logistics Solutions Division and the Plant Division, build a collaborative framework that includes a wide range of alliances, expand our network of partners, and put both businesses on a solid growth trajectory.

Q&A: On Maintenance Revenue in the Logistics Solutions and Tank Businesses

Moderator: We have received the following question: “Could you provide the maintenance revenue figures for both the Logistics Solutions and Tank businesses for FY2026 and FY2027?”

Owada: Maintenance revenue at the Logistics Solutions Division came in at ¥12.3 billion in FY2026, and we are targeting ¥15.0 billion in FY2027. Regarding maintenance revenue for the Tank business, as maintenance revenue in the Plant Division is almost entirely attributable to the Tank business, we expect it to be approximately ¥14.0 billion in FY2027.

Q&A: On the Reasons for the Shortfall in the Business Innovation Division's Operating Profit Plan

Moderator: We have received the following question: “Could you provide more details on the reasons for the shortfall in the Business Innovation Division's operating profit in FY2026?”

Owada: As the Business Innovation Division comprises multiple companies, I will ask Yonehara to provide an overview.

Takeshi Yonehara: I am Takeshi Yonehara, Director, Senior Managing Executive Officer and Chief Financial Officer. As President Owada explained earlier, the main reason for the shortfall in the Business Innovation Division's operating profit versus plan was that earnings at two companies within the division — Toyo Koken and Kankyo Research Institute — fell short of our initial forecast.