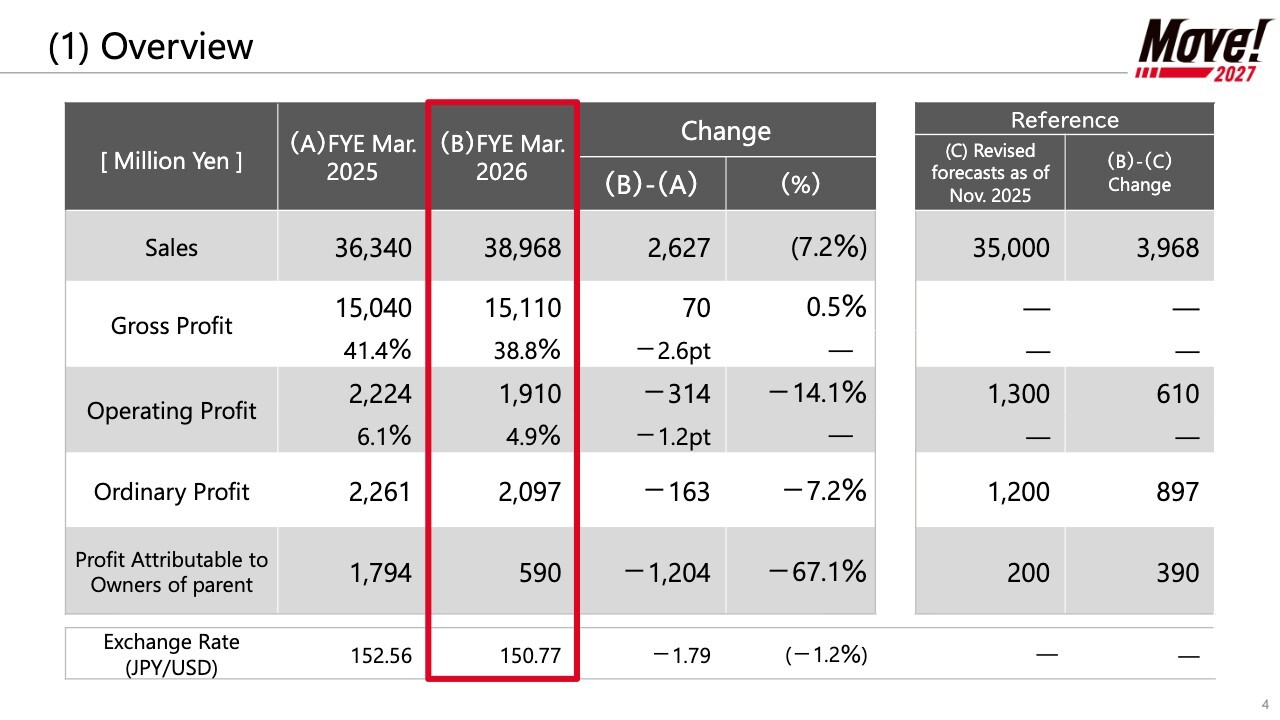

(1) Overview

Mr. Makoto Saito (hereinafter, “Saito”): Thank you very much for coming to the financial results briefing for JANOME Corporation for the fiscal year ended March 31, 2026. I am Saito, Representative Director and President. Today, I will explain three topics: the financial results for the FYE March 2026, progress on our Mid-term Business Plan “Move! 2027,” and our earnings forecasts for the FYE March 2027. Let me begin with the results overview for FYE March 2026.

First, I will explain the overview of consolidated results. Looking at the global economy during the current fiscal year, while the U.S. economy remained resilient, driven mainly by consumer spending, concerns persisted over the prolonged impact of monetary tightening and uncertainty surrounding trade policy.

Although Europe showed signs of recovery, economic growth in China remained sluggish due to a downturn in the real estate market and weak domestic demand, resulting in regional disparities in the business environment.

In the domestic economy, while a gradual recovery trend continued against the backdrop of improvements in the employment and income environment, the outlook remained uncertain due to persistently high resource prices and rising inflation.

In this environment, as the first year of our Mid-term Business Plan, “Move! 2027,” the Group focused its business operations on realizing our long-term vision: “A company that shares delight of ‘make.’”

Specifically, we worked to improve profitability by promoting aggressive sales activities aimed at expanding our market share, broadening our product lineup, and reducing manufacturing costs. We have also taken prompt action to address issues such as U.S. reciprocal tariffs.

However, the business environment surrounding the Group remained challenging. For the current fiscal year, the Group’s net sales amounted to 38,968 million yen, a year-on-year increase of 2,627 million yen, while operating profit came to 1,910 million yen, a year-on-year decrease of 314 million yen, ordinary profit was 2,097 million yen, a year-on-year decrease of 163 million yen, and profit attributable to owners of parent was 590 million yen, a year-on-year decrease of 1,204 million yen.

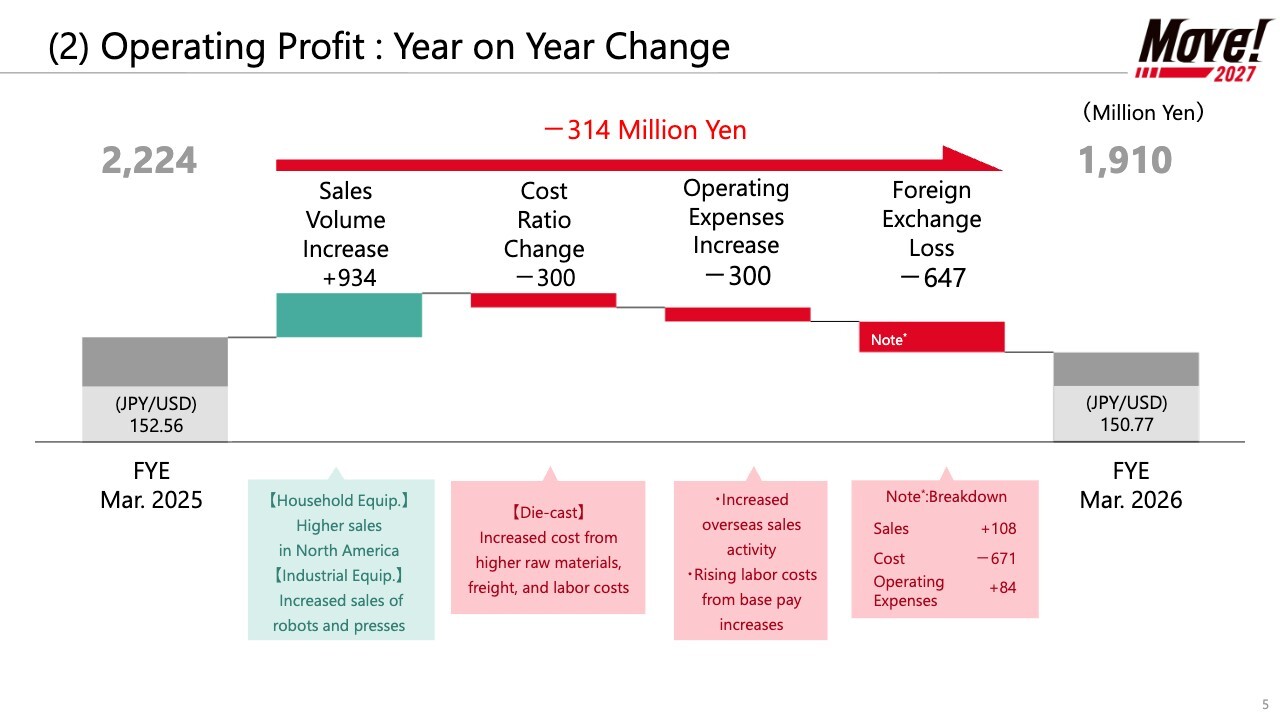

(2) Operating Profit : Year on Year Change

Next, I will explain the factors behind the change in operating profit. While higher net sales were a positive factor during the current period, profits were dragged down by a deterioration in cost ratios and the foreign exchange impacts.

I will start by explaining the improvement in gross profit resulting from the sales volume increase. Increased sales in North America in the household equipment business as well as increased sales of robots and presses in the industrial equipment business contributed to an increase in profit of 934 million yen.

Meanwhile, due to the cost ratio change, profit decreased by 300 million yen. The main factors were the impact of increased costs due to soaring raw material, freight, and labor costs in the die-cast business.

In addition, operating expenses also increased by 300 million yen year-on-year. This was mainly due to strengthened sales activities overseas and base pay increases aimed at securing and retaining human resources.

Regarding foreign exchange effects, while there was positive impact on sales due to the depreciation of the yen against the currencies used for sales pricing, costs and operating expenses increased due to the appreciation of local currencies at production bases in Taiwan and Thailand. As a result, overall foreign exchange loss was a factor in decreased profit of 647 million yen.

As a result, operating profit decreased by 314 million yen overall.

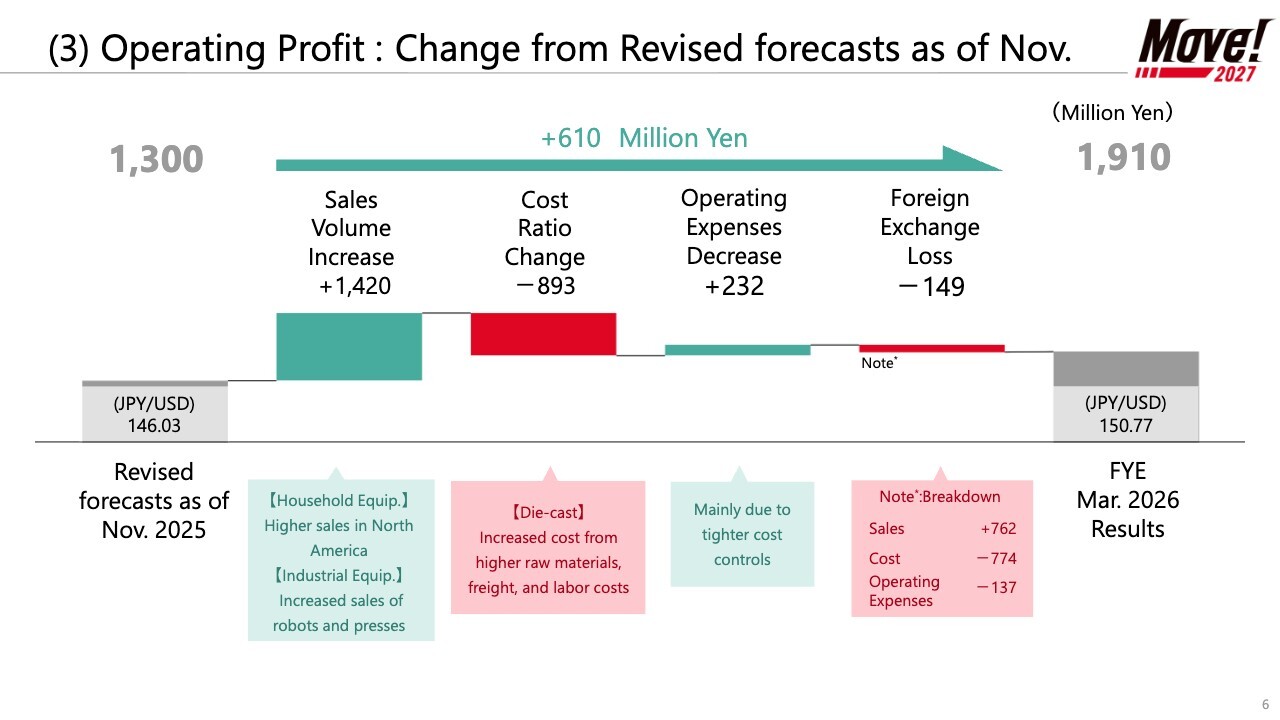

(3) Operating Profit : Change from Revised forecasts as of Nov.

Next, I will explain the factors behind the increase in operating profit from the forecasts announced in November. Although profits were pushed down year-on-year by a worsening cost ratio and foreign exchange impacts, results exceeded assumptions when compared with the forecasts announced in November, mainly due to an increase in sales volume.

First, an increase in sales volume resulted in a profit increase of 1,420 million yen. As mentioned earlier, this was due to increased sales in North America in the household equipment business and increased sales of robots and presses in the industrial equipment business.

On the other hand, profits decreased by 893 million yen due to changes in the cost ratio. The main reason was increased costs in the die-cast business from higher raw material, freight, and labor costs.

Regarding foreign exchange effects, while there was an impact of higher costs due to the appreciation of local currencies at production bases in Taiwan and Thailand, net sales increased due to the depreciation of the yen against the currencies used for sales pricing, resulting in a decrease in profit of 149 million yen.

As a result, operating profit came in 610 million yen above the forecast of 1,300 million yen announced in November.

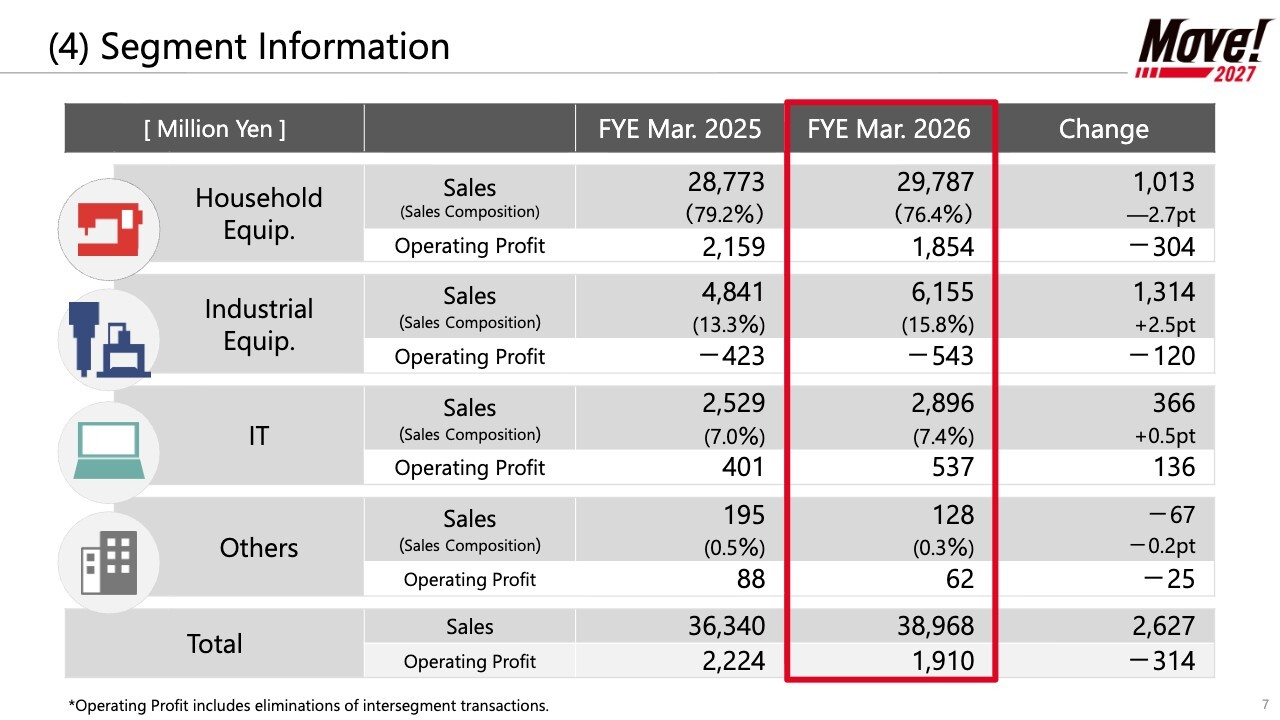

(4) Segment Information

Next, I will explain segment information.

In the household equipment business, while net sales increased by 1,013 million yen, operating profit declined by 340 million yen, resulting in higher sales and lower profit. Details will be explained on the following slide.

In the industrial equipment business, although net sales increased by 1,314 million yen, operating profit decreased by 120 million yen, resulting in higher sales and lower profit. I will also go over the breakdown of this segment later.

In the IT business, net sales increased by 366 million yen, and operating profit increased by 136 million yen to reach a record high, resulting in higher sales and profit.

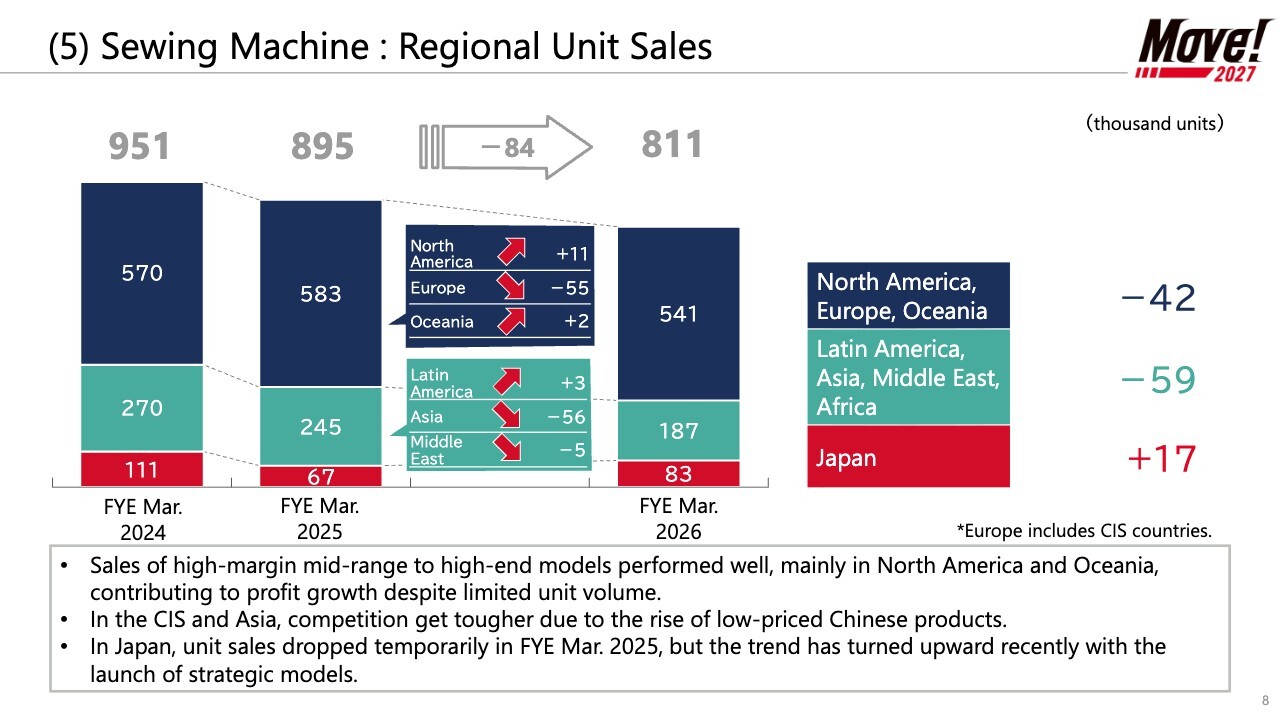

(5) Sewing Machine : Regional Unit Sales

Next, I will explain the trend in regional unit sales of household sewing machines. Overseas, unit sales growth was sluggish, mainly in the CIS and Asia, due to the impact of intensifying competition caused by the rise of low-priced Chinese products.

Meanwhile, sales of high-margin mid-range to high-end models performed well, mainly in North America and Oceania, contributing to profit growth. In Japan, unit sales dropped temporarily in the previous fiscal year due to the review of the product mix aimed at securing profitability, but has turned upward recently with the launch of strategic models.

Total unit sales of sewing machines in the household equipment business came to 810,000 units, a decrease of 84,000 units year-on-year. On the other hand, as explained earlier, net sales increased year-on-year, due to expanded sales of mid-range to high-end models.

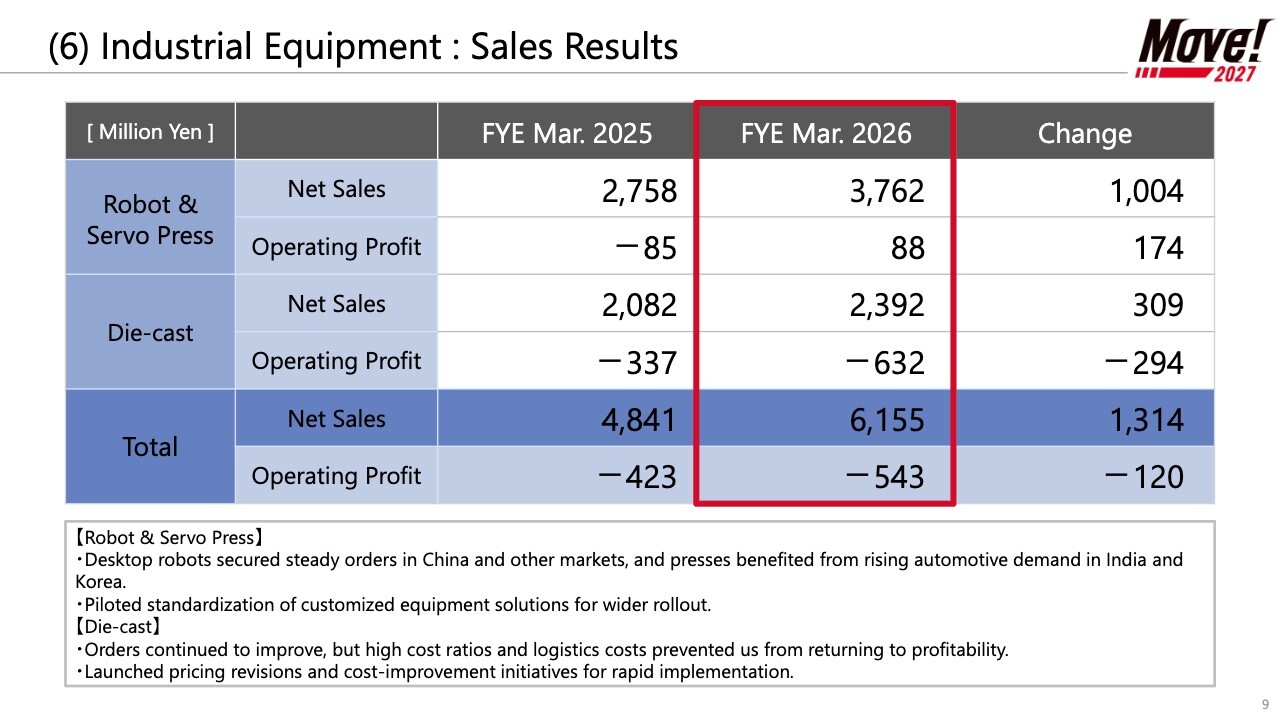

(6) Industrial Equipment : Sales Results

Next, in the industrial equipment business, desktop robots secured steady orders by capturing demand in China and other markets.

For servo presses, demand for automotive applications expanded in India and South Korea. In India, which is an important market, we increased the capital of our sales subsidiary and worked to strengthen our sales and technical support structure for market expansion.

In addition, we are currently gathering insights to standardize our integrated packages, which are currently customized on a case-by-case basis.

In the die-cast business, while orders continue to show signs of improvement, the situation remains challenging in terms of profitability due to persistently high cost ratios and the ongoing impact of logistics costs.

We have begun implementing reforms aimed at price revisions and cost reductions to return to profitability as soon as possible. As a result, the industrial equipment business as a whole recorded net sales of 6,155 million yen, up 1,314 million yen year-on-year. Operating loss was 543 million yen, compared to an operating loss of 423 million yen in the previous fiscal year.

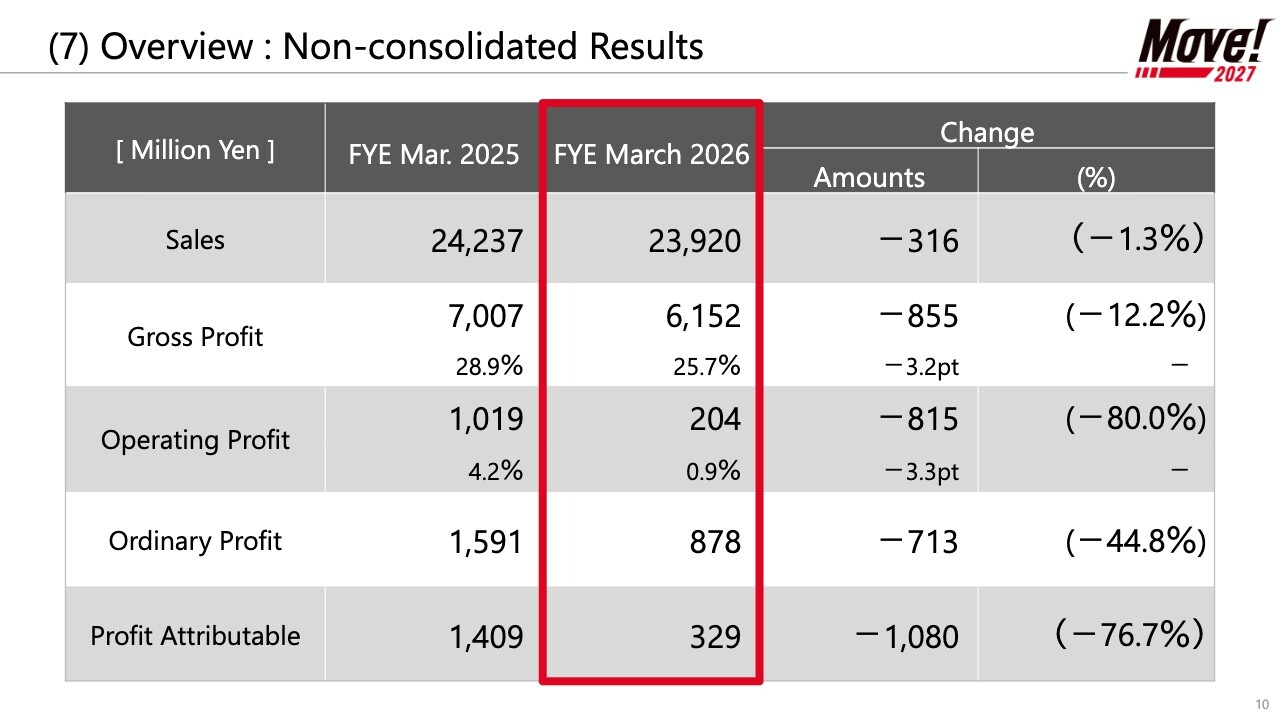

(7) Overview: Non-consolidated Results

Next, I would like to report the non-consolidated results for your reference. Net sales were 23,920 million yen, a decrease of 316 million yen year-on-year, and operating profit was 204 million yen, down 814 million yen year-on-year. Ordinary profit was 878 million yen, a decrease of 713 million yen year-on-year, and profit attributable was 329 million yen, down 1,080 million yen year-on-year.

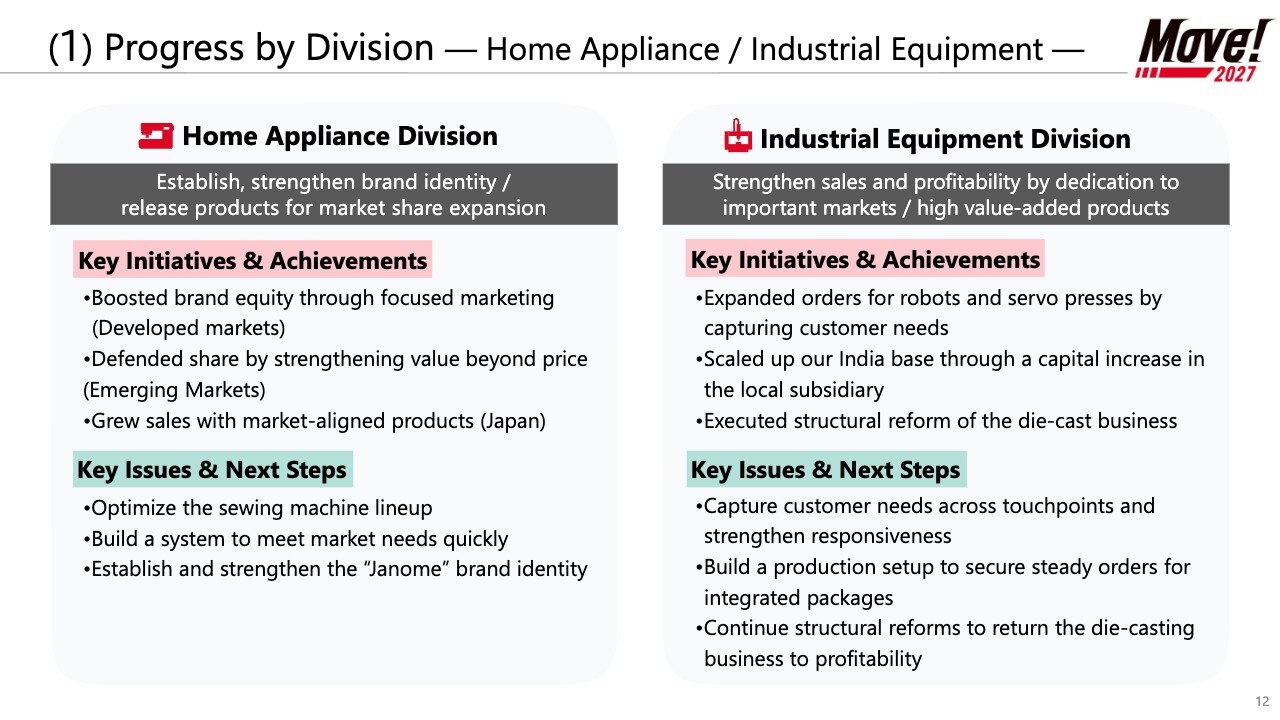

(1) Progress by Division ― Home Appliance / Industrial Equipment ―

Next, I will explain the progress in the first year of Mid-term Business Plan “Move! 2027.”

First, regarding the Home Appliance Division, our basic policy under the Mid-term Business Plan is to establish and strengthen our brand identity and release products for market share expansion.

Among our key initiatives and achievements, in developed markets, we clarified the reasons why customers choose us and boosted brand equity through strengthened marketing.

In emerging markets, we defended share by securing competitive advantages that go beyond price, such as design and distributor relationships. In Japan, we worked to grow sales with market-aligned products.

Going forward, key issues will be to optimize the sewing machine lineup by releasing new market-aligned products and reviewing the product mix, while also building a system that can quickly respond to market needs and the competitive environment, and further establish and strengthen the "Janome" brand identity.

Next, for the Industrial Equipment Division, the basic policy of the Mid-term Business Plan is to strengthen sales and profitability by dedication to important markets and high value-added products.

As for key initiatives and achievements, we expanded orders for robots and servo presses by capturing customer needs, including capturing demand for desktop robots in China, and also strengthened our sales and technical support structure through measures such as a capital increase in our local subsidiary in India, which is an important market. Furthermore, we also executed structural reform of the die-cast business.

In addition to strengthening a system that can capture customer needs across touchpoints and respond quickly from technology proposals through to delivery, our key issue going forward is to organize the insights gained from our current case-by-case approach and build a standardized delivery model and production system aimed at securing stable orders for integrated packages.

In addition, we continue to implement structural reforms to return the die-cast business to profitability.

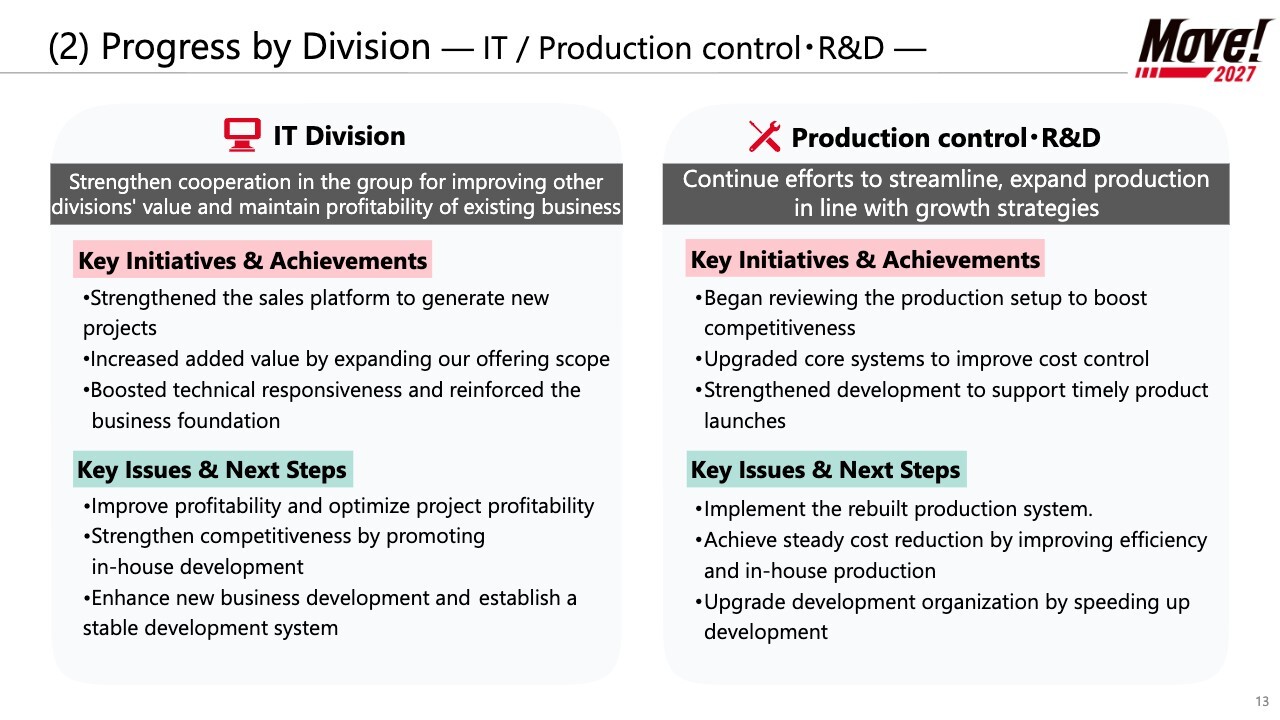

(2) Progress by Division ― IT/Production control・R&D ―

In the IT business, key initiatives and results included strengthening the sales base starting with externally sold software and implementation support, while promoting the creation of new projects and expanding customer touchpoints.

We expanded our offering scope by leveraging our existing track record and know-how across the organization, aiming to increase the added value from upstream processes through to operations. In addition, we worked to boost technical responsiveness and reinforced the business foundation with an eye toward future growth.

Going forward, key issues will be to improve profitability by streamlining low-margin projects and adjusting pricing to appropriate levels, as well as to optimize project profitability. In addition, we will work to build technical expertise, strengthen competitiveness, and improve profit margins by reducing outsourcing and promoting the use of internal resources.

In addition, to respond to the expansion of our project portfolio, we aim to establish a stable development system by optimizing personnel allocation and enhancing operational management.

With regards to production control and R&D, we will continue our current initiatives while working to streamline and expand production in line with our growth strategy.

As part of our key initiatives, we reviewed our production setup, including the use of external expertise, and explored ways to expand capacity, thereby clarifying the direction for optimizing our production system. In addition, we promoted the upgrade of our core systems and the in-house production of components, laying the groundwork for improved cost control and cost reduction.

In addition, we collaborated with the sales department to launch new models and strengthen our R&D framework based on customer needs.

As future key issues, we will focus on implementing specific measures to optimize our production system and expand capacity, and on generating results.

In addition to steadily reducing costs through infrastructure improvements, we will work to enhance our competitive R&D capabilities by accelerating the development process in line with new model development and by better addressing customer needs.

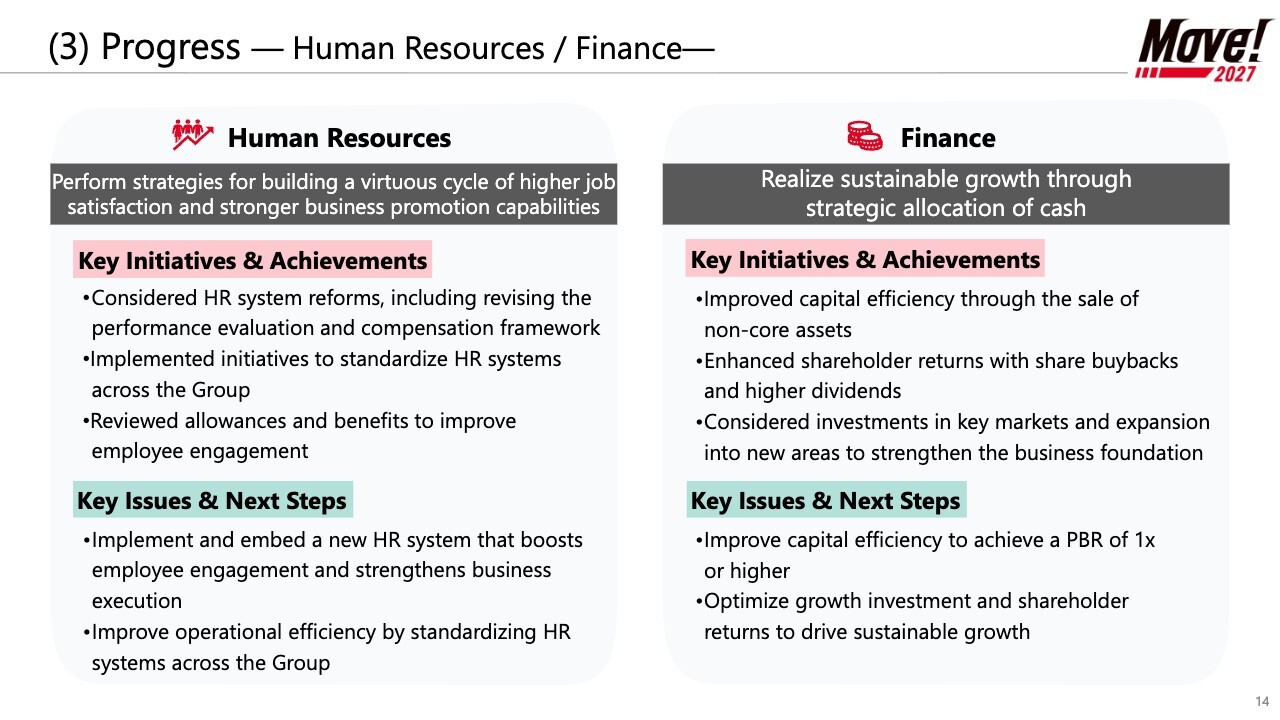

(3) Progress ― Human Resources / Finance —

Next, regarding human resources, our basic policy is to build a virtuous cycle of higher job satisfaction and stronger business promotion capabilities by carrying out human resources strategies.

Key initiatives and achievements include revising the performance evaluation and compensation framework and exploring other reforms to our human resources policies, with a focus on developing systems that reflect individual performance and roles. In addition, we also implemented initiatives to standardize HR systems across the Group, with the aim of centralizing personnel data and improving operational efficiency.

In addition, we are working to strengthen our workforce by reviewing allowances and benefits with the aim of improving employee engagement. Going forward, we will work to implement and embed a new HR system that boosts employee engagement and strengthens business execution, while also striving to improve operational efficiency by standardizing HR systems across the Group.

Lastly, I will talk about finance. Our basic policy is to realize sustainable growth through strategic allocation of cash.

As a key initiative and achievement, we have begun improving capital efficiency by reviewing non-core assets, mainly real estate. In addition, we enhanced return to shareholders by implementing share buybacks totaling 1,500 million yen and are planning to increase the dividend per share to 55 yen, an increase of 15 yen year-on-year.

In the industrial equipment business, we made investments to strengthen sales in the Indian and Chinese markets, while in the household equipment business, we invested approximately 1,500 million yen annually in the development of new models to strengthen our business foundation.

Going forward, we will strive to achieve an ROE of 8% and a PBR of 1x or higher, and we will work to improve capital efficiency and refine our capital allocation strategy to strike a balance between growth investments and return to shareholders.

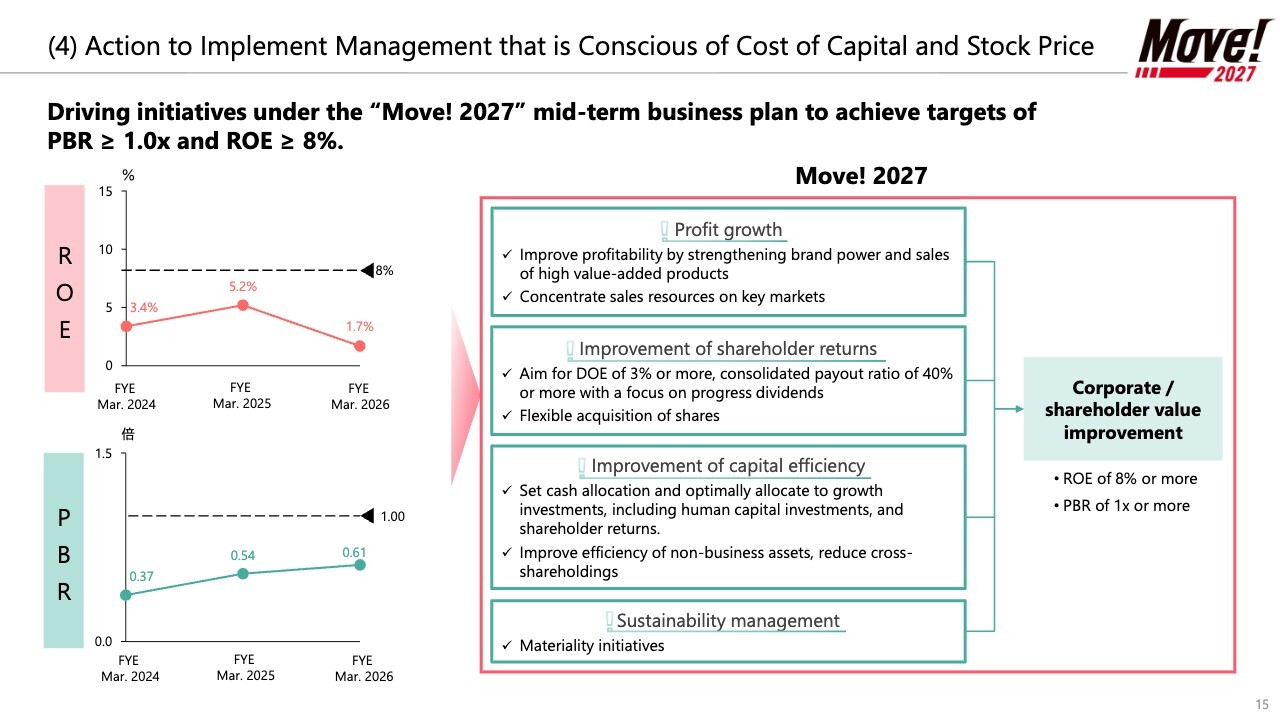

(4) Action to Implement Management that is Conscious of Cost of Capital and Stock Price

Next, I will explain the basic measures in the Mid-term Business Plan and the actions aimed at enhancing corporate value. For FYE March 2026, the Company reported a PBR of 0.61x and an ROE of 1.7%. Under our Mid-term Business Plan, we aim to achieve a PBR of 1.0x or higher and an ROE of 8% or higher by the FYE March 2028.

To achieve this goal, we will strive to enhance corporate value and shareholder value by driving profit growth, improving shareholder returns, improving capital efficiency, and promoting sustainable management.

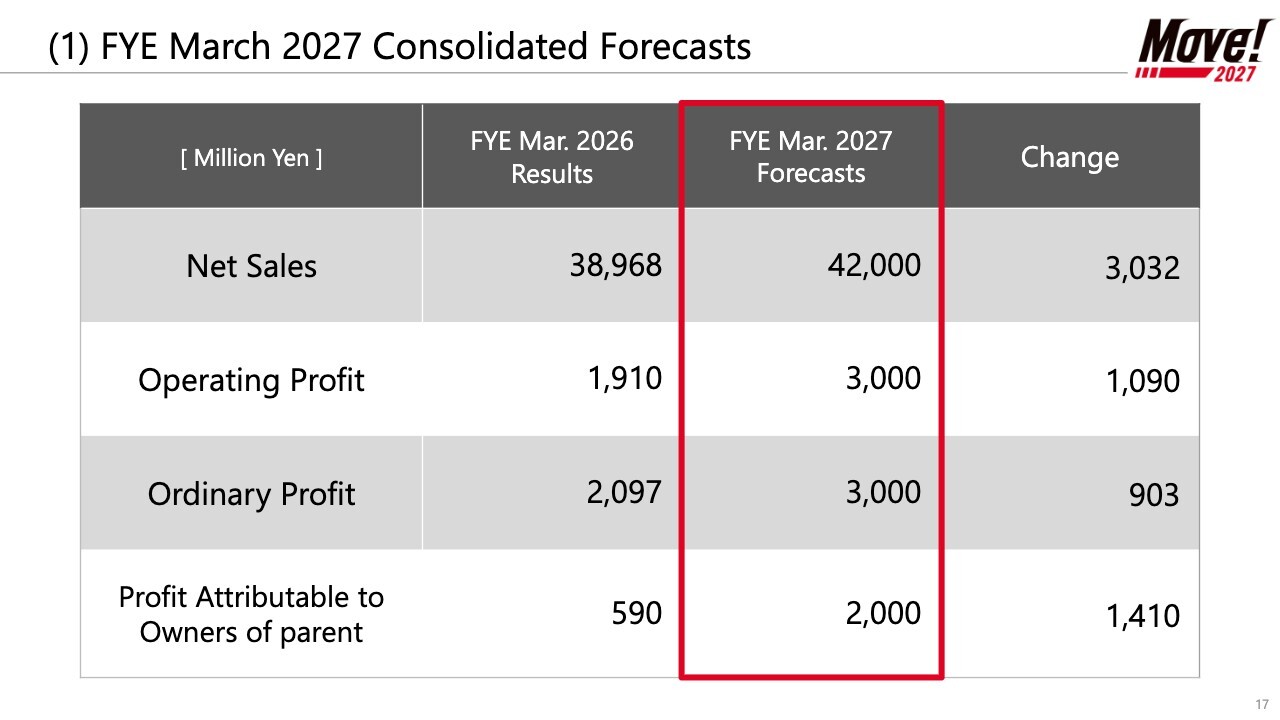

(1) FYE March 2027 Consolidated Forecasts

Hitoshi Doi (hereafter, Doi): I am Doi, Director and Senior Managing Officer. I will explain the forecasts for FYE March 2027.

On a consolidated basis, we expect net sales to increase by 3,032 million yen year-on-year to 42,000 million yen, operating profit to increase by 1,090 million yen to 3,000 million yen, ordinary profit to increase by 903 million yen to 3,000 million yen, and profit attributable to owners of parent to increase by 1,410 million yen to 2,000 million yen.

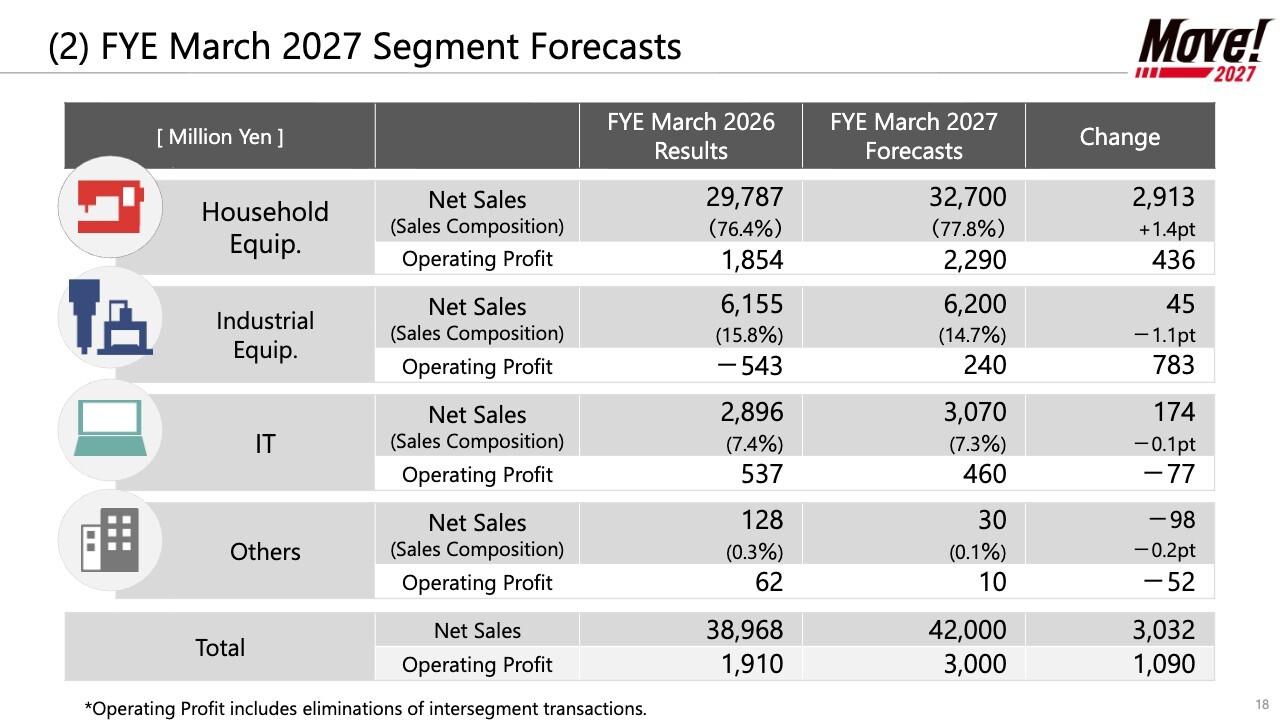

(2) FYE March 2027 Segment Forecasts

Next, I will explain the forecasts by business segment.

The household equipment business expects net sales of 32,700 million yen and operating profit of 2,290 million yen.

The industrial equipment business, including the die-cast business, expects net sales of 6,200 million yen and operating profit of 240 million yen.

The IT business expects net sales of 3,070 million yen and operating profit of 460 million yen. For the IT business, we expect stable orders in the FYE March 2027 as well, but profits are projected to decline compared to the previous fiscal year, which saw record-high profits.

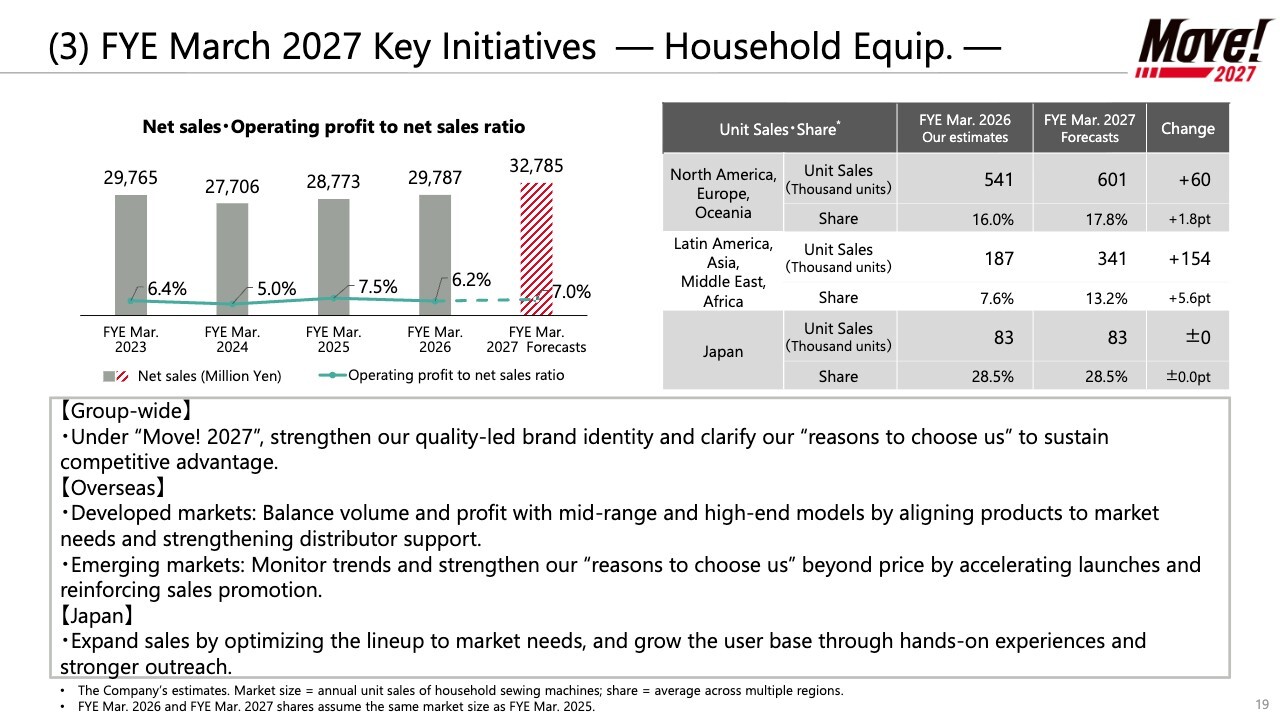

(3) FYE March 2027 Key Initiatives ― Household Equip. ―

I will explain the key initiatives for FYE March 2027. First, I will talk about the household equipment business.

For the Group as a whole, under the basic policy of our Mid-term Business Plan “Move! 2027”, we will strengthen our quality-led brand identity and clarify our “reasons to choose us” among customers to secure competitive advantage.

In overseas markets, mainly in developed markets such as North America, we will aim to balance volume and profit with mid-range and high-end models by aligning products to market needs. We will also work to strengthen our support system, including technical support and support for distributors.

In emerging markets such as India and the CIS countries, we plan to monitor market trends while strengthening the "reasons to choose us", such as design and quality rather than relying solely on price, and securing a competitive advantage. We will also proceed with the launch of new models to build a market foundation and strengthen our sales promotion efforts.

In Japan, in addition to expanding sales by optimizing the lineup to market needs, we will work to expand the user base through hands-on experiences, including workshops, and stronger outreach through social media and other channels.

As a result of these measures, we expect annual unit sales to increase by 60,000 units year-on-year in developed markets such as North America, Europe, and Oceania, and by 150,000 units year-on-year in emerging markets such as Latin America, Asia, the Middle East, and Africa. In Japan, we plan to maintain the same level as in the FYE March 2026.

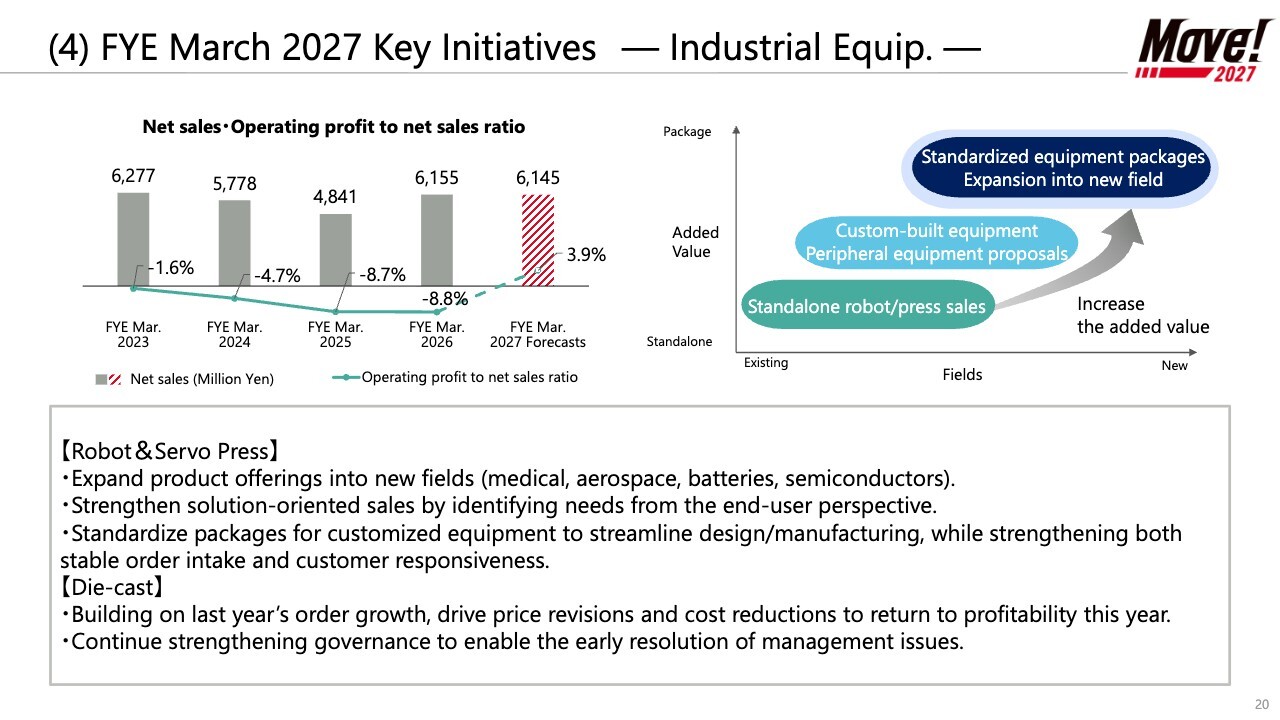

(4) FYE March 2027 Key Initiatives ―Industrial Equip. ―

Next, I will explain the strategy for the industrial equipment business.

In the robots and servo presses business, we plan to place greater emphasis on expanding product offerings into fields requiring high-quality management, such as medical, aerospace, batteries, and semiconductors. In addition, we will strive to enhance added value through strengthening solution-oriented sales by identifying needs from the end-user perspective.

For integrated packages, we will shift from the current custom-made approach to standardized packages, mainly in Japan, to streamline design/manufacturing. Through this, we will develop an R&D and production system that strengthens both stable order intake and customer responsiveness.

For the die-cast business, building on last year’s order growth, we will drive sales price revisions and cost reductions to return to profitability this year. In addition, we will continue strengthening governance to enable the early resolution of management issues.

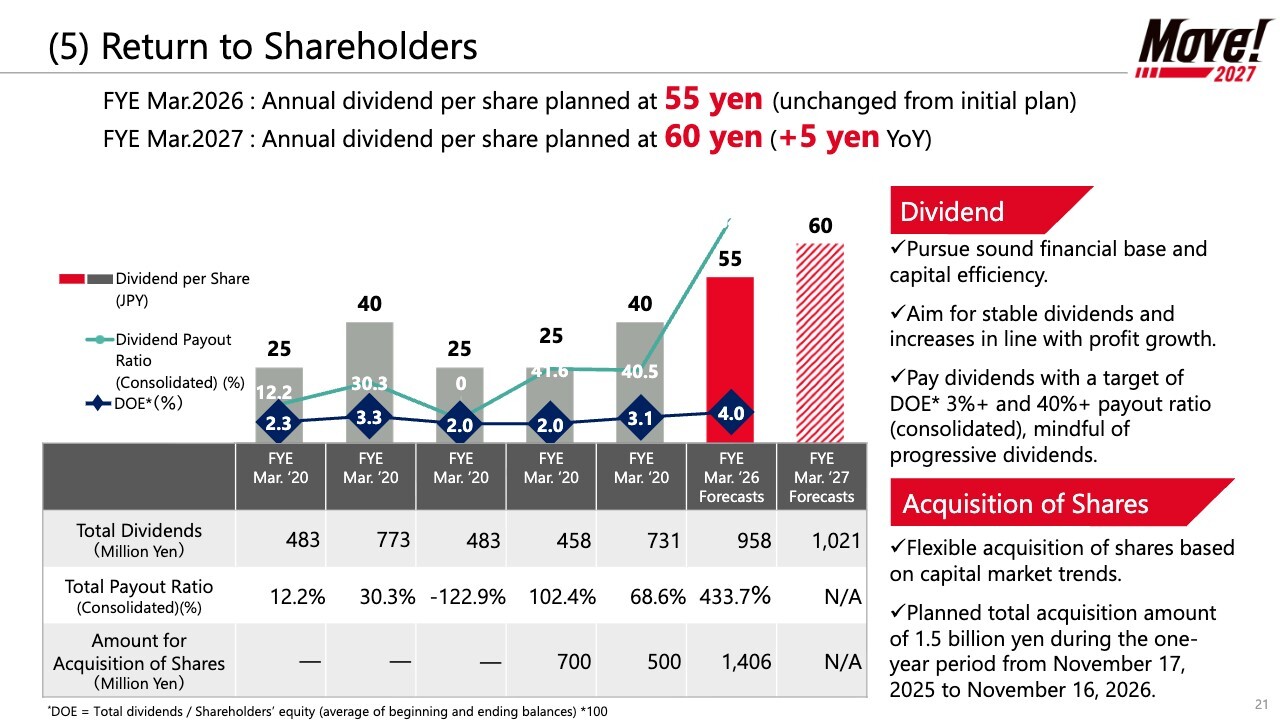

(5) Return to Shareholders

I will explain return to shareholders. In our Mid-term Business Plan, “Move! 2027,” we have established a dividend policy of aiming for DOE of 3% or more and a consolidated dividend payout ratio of 40% or more, with a focus on progressive dividends.

For the FYE March 2026, annual dividend per share is set at 55 yen. For the FYE March 2027, based on our earnings forecasts and financial position, we plan to increase the annual dividend per share by 5 yen year on year to 60 yen.

Going forward, we will continue to strive to enhance sustainable corporate value and strengthen return to shareholders while maintaining a balance between profit growth, improved capital efficiency, and growth investments.

This concludes our presentation. Thank you very much.

Q&A: Cruising speed of sales and profit in the current business environment

Questioner: Regarding the Company’s performance, it appears that you are on track for a V-shaped recovery this fiscal year. However, there was a time when the Company generated operating profit of around 5,000 million yen. Although there have been changes in the scope of operations, I find it somewhat difficult to gauge the actual level of net sales and profits.

Regarding the scale of the cruising speed for net sales and profit that the President has in mind under the current business environment, is it correct to understand that it is roughly just under 40,000 million yen in net sales and just over 2,000 million yen in ordinary profit posted in the previous fiscal year, with a profit margin of approximately 5%?

Could you share your view on the company-wide scale of profits at present, including any rough estimates?

Saito: As you pointed out, we believe net sales would exceed 40,000 million yen under normal operating conditions. As for operating profit, it did not reach 2,000 million yen this fiscal year due to various factors. Since the figure for two fiscal years ago was around 2,200 million yen, I believe there is a possibility of reaching 2,500 million yen if there is a slight recovery in North America, Europe, and Oceania.

We also have those figures in mind for our household equipment business. As for our industrial equipment business, we plan to further explore the Indian market. Given the significant potential of the Indian market, we believe that, taking this into account, it would not be surprising for operating profit to reach 3,000 million yen.

Q&A: Desktop robots and their sales performance

Questioner: Regarding the robot business, I understand that desktop robots are the Company’s only product. What were the net sales for desktop robots, that is, the robot business, in the previous fiscal year? Also, could you please tell us about the sales results for desktop robots, including price per unit for the desktop robots and how many units were sold in the previous fiscal year?

Doi: The industrial equipment business is divided into the robots and servo presses business and the die-cast business. However, figures for robots and presses are not disclosed separately but are treated as a single category.

Saito: As for the price per unit, it generally ranges from about 1 million to 2 million yen, with larger models costing around 3 million yen.

Questioner: That is quite a high price range. Generally, my impression is that large industrial robots typically cost around 6 million yen to 7 million yen, so would it be correct to understand that your desktop robots are robots of a comparable size?

Saito: In terms of size, the minimum workpiece size is 200 mm × 200 mm, and the maximum is 600 mm.

Desktop robots are products designed for standalone tasks. Specifically, these products are used for tasks such as soldering, adhesive dispensing, screw tightening, and bit inserting, and are integrated into specific stages of the manufacturing process.

When people hear the word "robot," they often picture a six-axis, multi-jointed robot, and I think many people imagine the kind used in automotive-related applications. However, our desktop robots are designed to handle automation tasks within inline production processes.

We also sell Cartesian robots. This product combines single-axis components to provide the same functionality as a desktop robot, and the size can be customized to meet the customer’s requirements.

Questioner: Regarding desktop robots, is it correct to understand that the Company basically does not have any partnerships with other companies, but rather sources all components, including servo motors and joint components, from various suppliers, assembles them in-house, and sells the finished products?

Saito: That is correct. Our desktop robots incorporate technology derived from sewing and embroidery machines. We utilized the XY mechanism from the sewing and embroidery machine that our company first introduced to the world in 1990. Desktop robots are based on this technology.

As for components, motors, ball screws, moving parts known as splines, frames made from extruded aluminum, and bearings are all purchased items. We assemble them in-house and provide them to customers.

In addition, we develop our own software. Our most distinctive feature is that we use our own proprietary software rather than standard robot programming languages in our robot-related products, including desktop robots. Given that it is based on sewing machine technology, we believe that it is designed to be extremely user-friendly.

Questioner: You mentioned that sales are strong in China, but based on what you’ve just said, what do you think is the driver for sales despite the fact that the prices are by no means low?

Given the various applications available, I assume these products are incorporated and are being offered in a form that appeals to customers in China. What specific features are being well received in the Chinese market?

Regarding unit sales, even if net sales figures are not disclosed, it is difficult to gauge the size of this division’s share without some indication of unit sales or other metrics to help us estimate the growth of the Company’s robotics business. If possible, please tell us about that as well.

Saito: I believe it was probably about 2,500 units in the previous fiscal year. However, there are some aspects of the specific breakdown that even I myself am not fully aware of.

One reason for the strong sales in China is that our desktop robots are already being used in the smartphone assembly process in the Chinese market.

In smartphone assembly, where precise and complex adhesive dispensing and bonding operations are required, our robots have been highly regarded for their user-friendly software and have gained strong support from end users in China.

While the price is certainly higher than that of Chinese products, they are still chosen for their ease of use and high performance. They are also widely used in smartphone lenses and speakers, as well as in wearable products.

Q&A: Growth of desktop robots and the relationship with the die-cast business

Questioner: Regarding desktop robots, the figures are presented together with the die-cast business in the industrial equipment business, which makes it difficult to get a clear picture of the actual situation.

As for desktop robots, I believe they are currently sold on a one-time sales basis. For example, assuming a useful life of seven years, could you tell us whether there is a possibility of shifting to a recurring business model in the future, whether there is potential to expand sales overseas, and what kind of growth you anticipate?

Also, while this business is included in the same segment as the die-cast business, could you please share your vision regarding how closely the two businesses are linked and how they are likely to grow in the future?

Saito: I will answer your question on how our desktop robots will grow. At this stage of development, our desktop robots are not yet capable of performing any tasks as a standalone product when made available to the public.

Customers will need to customize the product to match their needs. In addition, we generally wholesale the products to manufacturers of soldering equipment and adhesive dispensers, while trading companies and distributors handle these sales.

As for screw-tightening equipment, we do not manufacture the screwdrivers ourselves. For this reason, we install the screw-tightening device on the desktop robots in-house and sell them.

Regarding the relationship with the die-cast business, there is no direct relationship between the two. The die-cast business is strictly a standalone business.

Die-cast products are classified as industrial equipment because it is positioned as a BtoB product. It is currently classified under the industrial equipment business category, and the same applies to servo presses. Die-cast products, servo presses, and desktop robots are all positioned as independent products.

Q&A: Current status of the die-cast business and progress in price increase negotiations

Moderator: "Regarding the die-cast business, which posted a significant loss in the previous fiscal year, you are projecting a return to profitability this fiscal year. How confident are you in that projection? Also, when do you expect to start achieving monthly profits?" is the question.

Doi: Regarding the die-cast business, we took drastic measures last fiscal year in response to the sharp rise in raw material costs and the impact of clearing out past inventory. More recently, we have continued price increase negotiations since around the fourth quarter of the previous fiscal year, and in some cases, price increases were implemented from as early as the first quarter of the current fiscal year.

The die-cast business operates factories in Tsuru City, Yamanashi Prefecture, and Thailand. While price increase negotiations at the Thailand plant are running slightly behind schedule in some areas, both plants are aiming to return to profitability in the second half of the year and are proceeding with the goal of concluding all price increase negotiations by the end of the first half.

The vast majority of our customers have accepted the price increase. In addition, we are reviewing orders for projects that do not generate adequate profits, and at this point, we expect to return to profitability from the second half of the fiscal year.

Q&A: Unit sales and unit price of robots

Questioner: You mentioned that robot unit sales totaled approximately 2,500 units. If the unit price were 1 million yen, the total would be 2,500 million yen, and if it were 2 million yen, it would be 5,000 million yen, so I believe this is likely a cumulative figure. What were the unit sales figures in the previous fiscal year?

Saito: I believe it was somewhere between 2,000 to 2,500 units for the full year.

Questioner: Earlier, you mentioned that the unit price ranges from 1 million to 2 million yen.

Saito: Smaller ones sell in higher volumes.

Q&A: Major shareholder MM Investments

Questioner: MM Investments, which is a major shareholder of the Company, appears to be a subsidiary of Mitsui Matsushima Holdings. Is this investment based on some kind of business partnership with the Company?

Doi: As a matter of policy, we do not comment on individual shareholders.