Results Presentation Fiscal Year Ended March 2026

Hideumi Akizawa (“Akizawa”): Thank you very much for attending WIN-Partners Co., Ltd.’s results presentation today. I am Hideumi Akizawa, Chief Executive Officer.

As you are all aware, uncertainty continues around the world, including in Japan. In our industry, we carry out our daily operations based on the premise that patients must be able to receive medical care safely and with peace of mind. We have now finalized our results amid this environment, and I will report them to you today.

Highlights

Keiji Matsumoto: I am Keiji Matsumoto, Director, Executive Officer and General Manager of Administration Division. I will explain the results for fiscal year ended March 2026. First, I will cover the highlights.

In the fiscal year under review, both sales and profits increased year on year. Sales exceeded ¥90 billion and reached an all-time high. As a result, gross profit also marked an all-time high. Sales and profits also exceeded the initial forecast.

Business environment

I will explain the business environment in the fiscal year under review. As you know, Japan’s economy has shifted into an inflationary phase, and prices continue to rise. Labor shortages also persist across industries, not only in the medical industry, and have become a major risk for business operations.

In addition, toward the second half of the fiscal year, crude oil prices rose substantially amid rising tensions in the Middle East triggered by the military attack carried out by the United States against Iran in February. This impact has also spread to prices of many petroleum-related products, becoming a factor that could accelerate inflation and disrupt supply chains.

WIN’s initiatives ①

Under this business environment, the Company implemented the initiatives shown on the slide. First, as in the past, we focused on support for patient acquisition and management support. Based on issues raised by customers over the year, we conducted 31 medical service area surveys and made 233 strategic purchasing proposals.

As support for enhancing the technical capabilities of healthcare professionals, we assisted in planning and operating 81 workshops and research meetings. We also provided young doctors and clinical engineers with opportunities to observe clinical procedures handled by experienced doctors.

As support for workstyle reforms, we also assisted with the introduction of AI-powered image interpretation support, facility criteria management systems, and systems for remote monitoring of Holter electrocardiographs.

As a result of actively allocating management resources to growing markets, the number of CDR-certified employees, including those awaiting certification, reached 128 at the end of March. We also focused on sales of Pulsed Field Ablation (PFA)-related devices, a rapidly growing area, and sales in the CRS division increased 22% year on year.

In addition, during the fiscal year, we gained a large new customer in the CRS field, which contributed significantly to sales growth.

WIN’s initiatives ②

In logistics reform, where we are currently focusing our efforts, we expanded direct deliveries from WIN Heart Gate, our logistics base, to customer hospitals and further promoted the separation of delivery and sales activities. At WIN Heart Gate, we also utilized RFID in inventory check at several major medical facilities in the Kanto region, achieving a substantial improvement in efficiency.

We also introduced generative AI in several internal departments and are working to improve operational efficiency in day-to-day operations, including contract reviews and document preparation.

Furthermore, as announced at the end of last year, Plusten Medical, based in Hakodate, Hokkaido, joined the Group in January this year as a wholly owned subsidiary of WIN INTERNATIONAL.

Plusten Medical is a medical equipment trading company that mainly handles medical equipment in the cardiovascular and cardiac surgery fields. Through this transaction, we can strengthen our customer base and expand the scale of our business in Hokkaido.

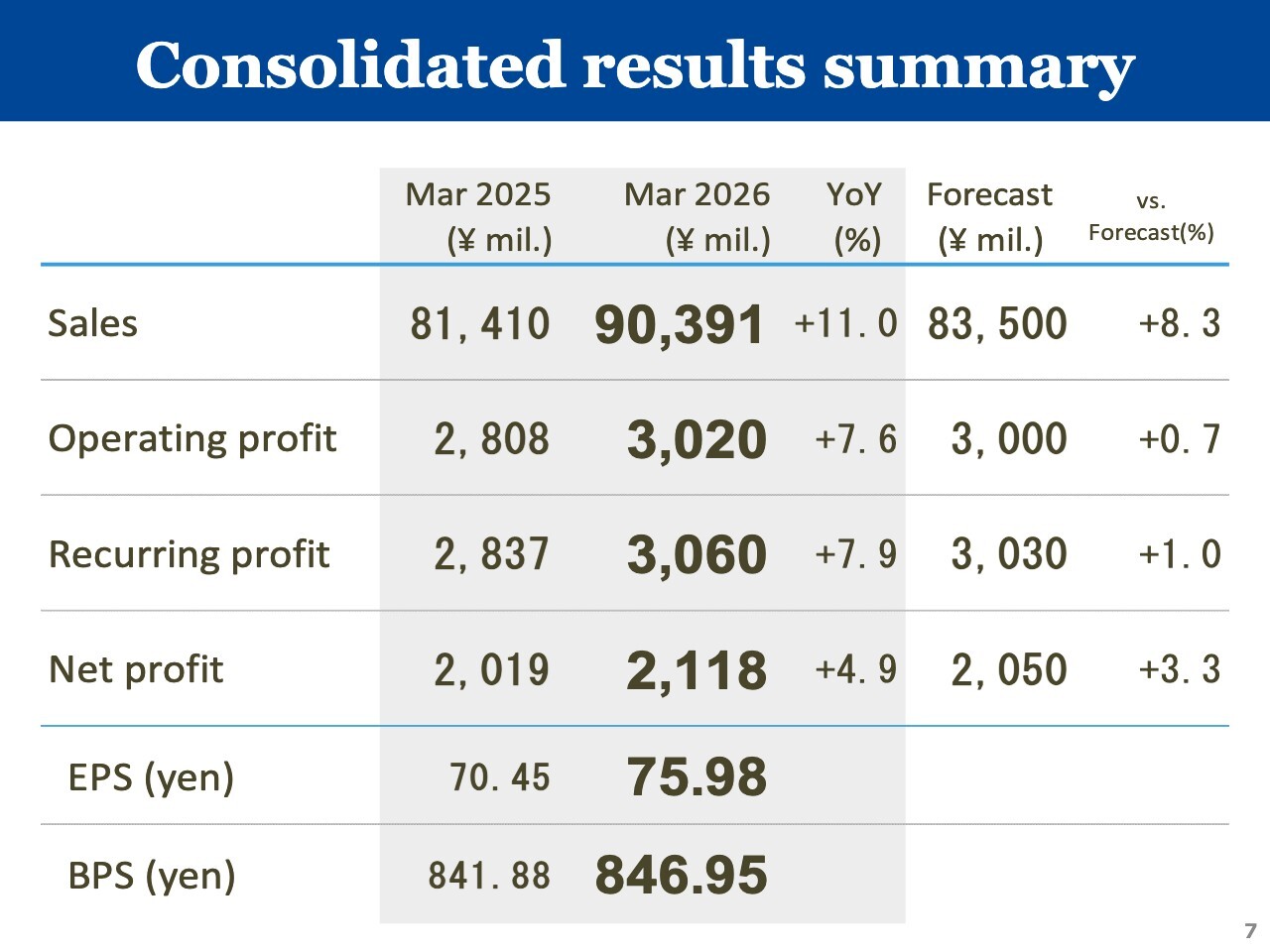

Consolidated results summary

As a result of these initiatives, sales for fiscal year ended March 2026 increased 11.0% year on year to ¥90,391 million, and operating profit rose 7.6% year on year to ¥3,020 million.

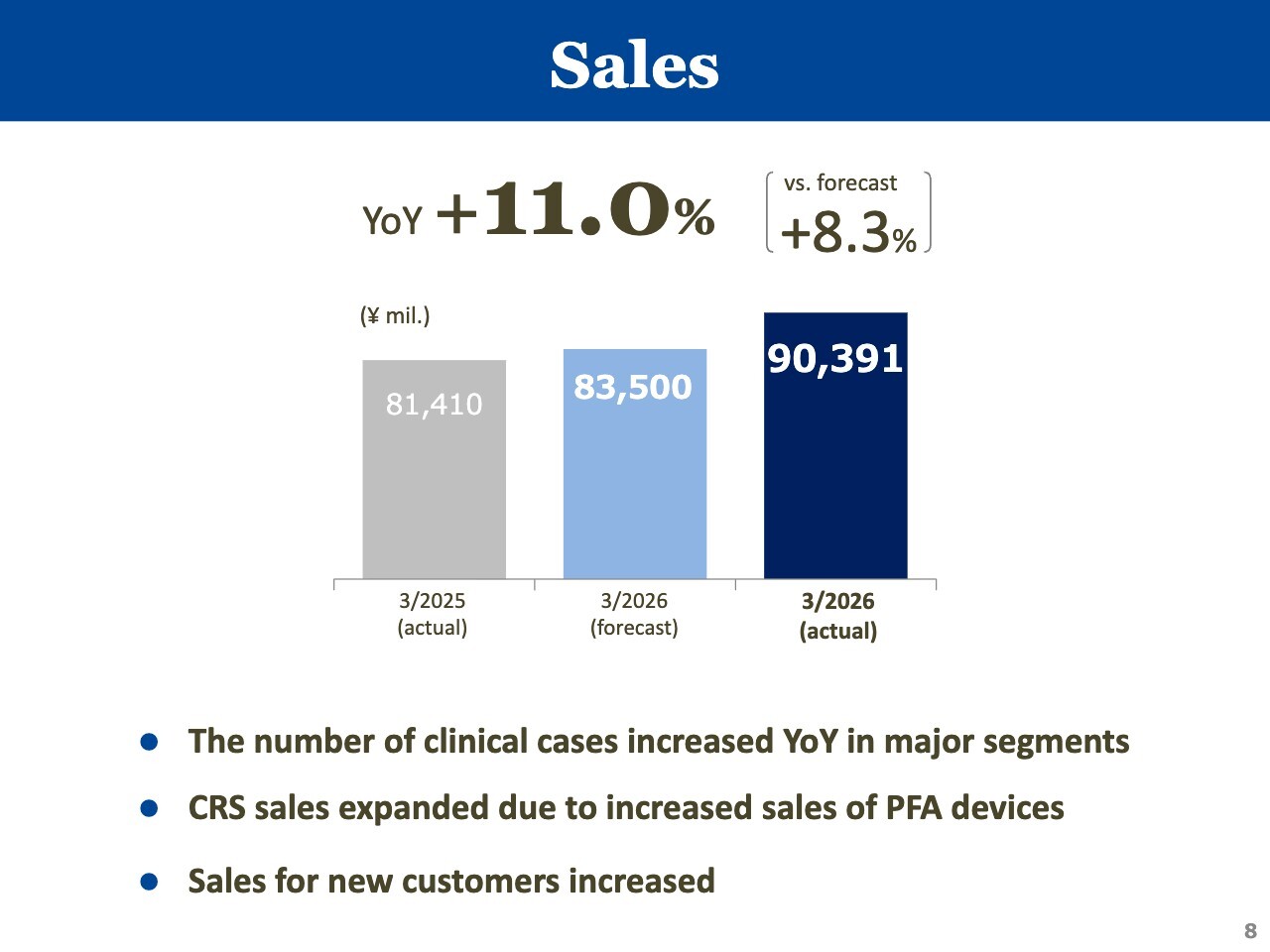

Sales

Sales expanded, supported by an increase in clinical cases in major segments. As noted at the beginning, sales exceeded ¥90 billion and marked an all-time high.

Plusten Medical has been included in consolidation from Q4, but its impact on the results was limited. In particular, sales of PFA devices, which are being adopted rapidly, started in earnest this fiscal year and contributed significantly to the increase in overall CRS sales.

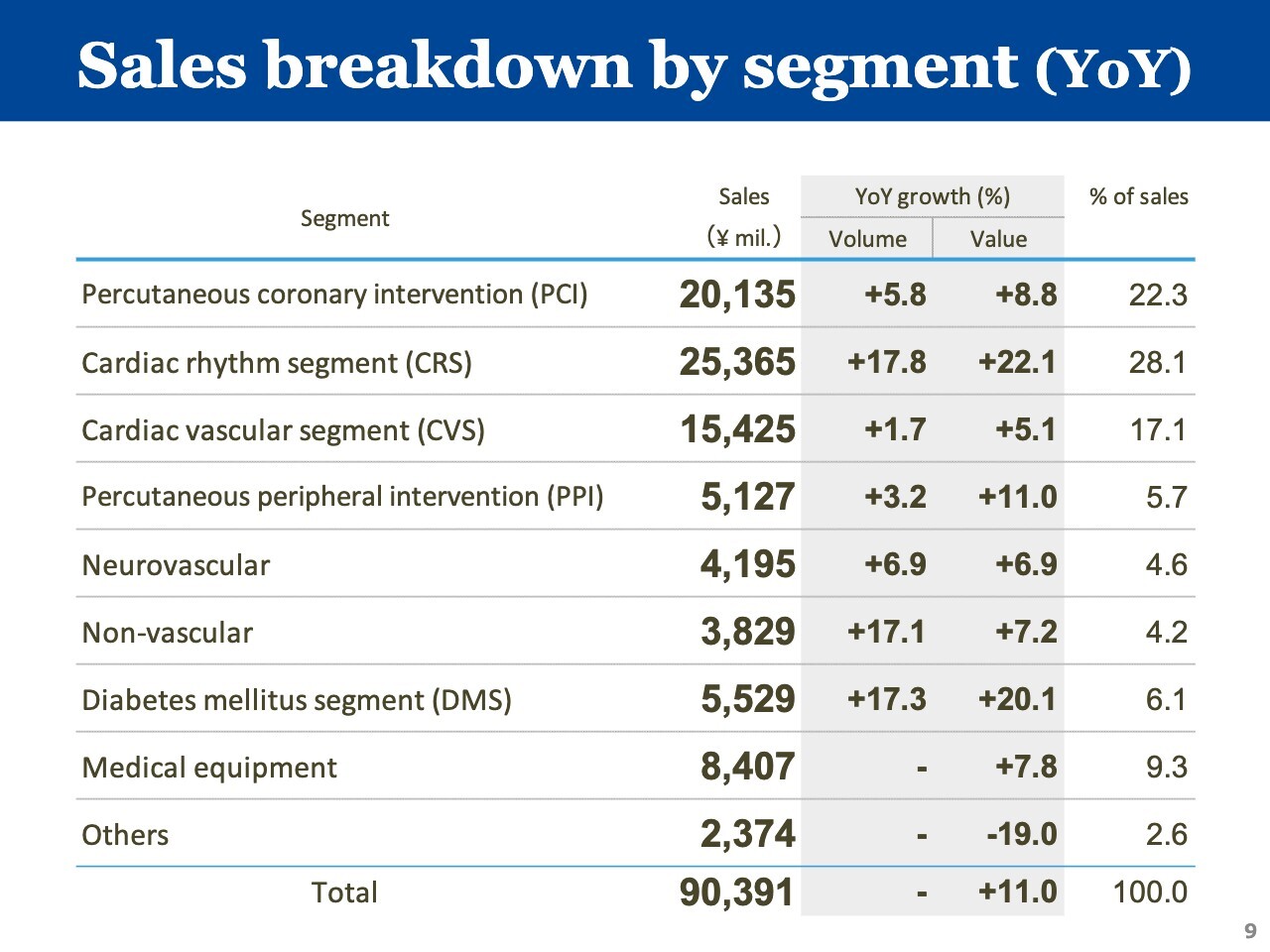

Sales breakdown by segment (YoY)

I will now explain the sales breakdown by segment. All segments except Others posted higher sales than in the previous fiscal year. In particular, CRS, a focus segment, showed a substantial increase, with sales up 22.1% year on year.

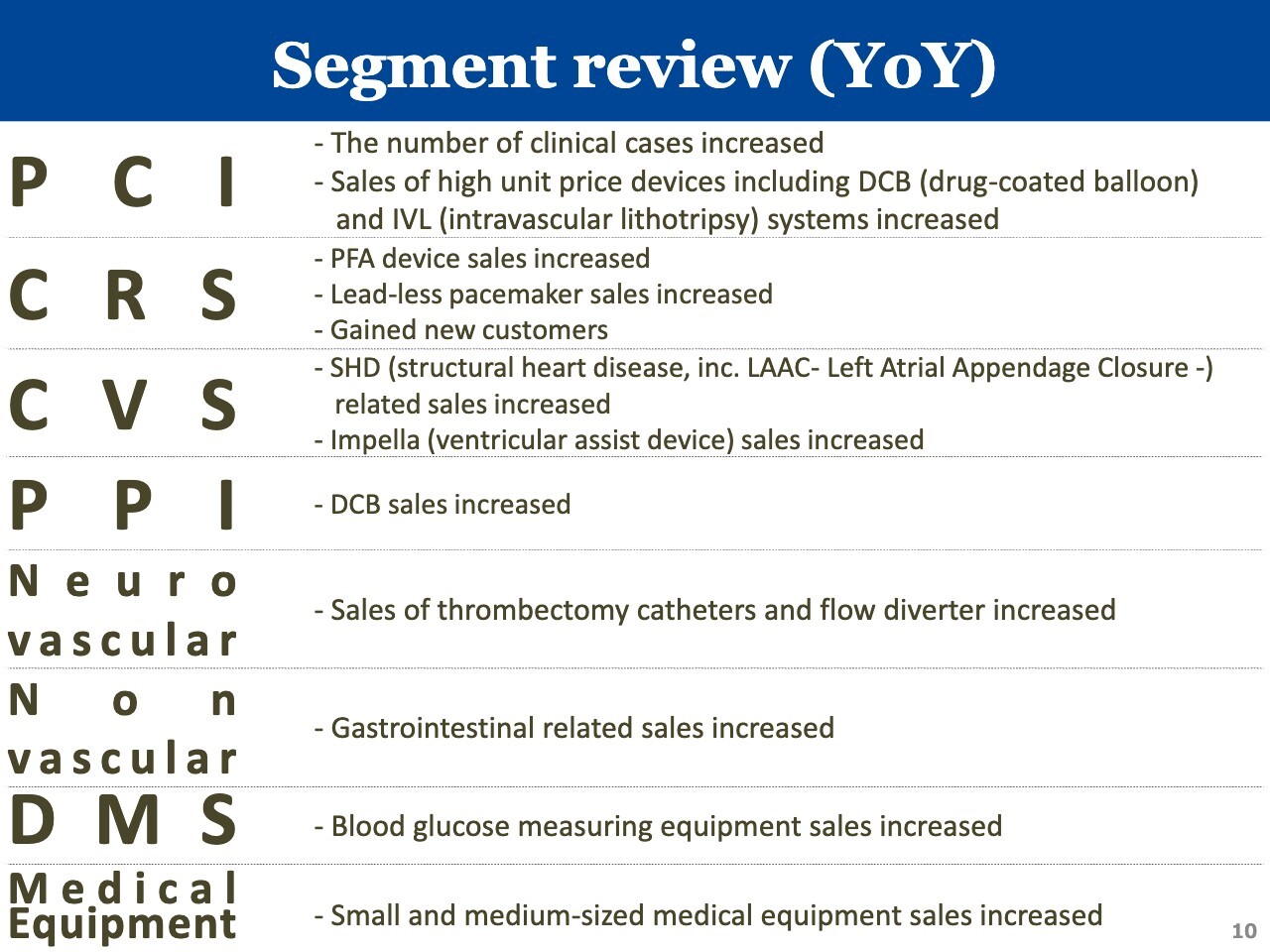

Segment review (YoY)

I will now explain the main points of the year-on-year changes in the sales breakdown by segment.

In PCI, sales growth was supported by an increase in the number of clinical cases and increased sales of relatively high unit price devices, such as DCB and IVL.

In CRS, sales of PFA devices increased substantially. Pacemaker sales also expanded, driven by growth in lead-less pacemakers. In addition, we gained new customers, which contributed to the sales increase.

In CVS, sales of SHD-related products, including left atrial appendage closure (LAAC) systems, continued to increase, and sales of Impella (ventricular assist device) also increased.

In PPI, sales of DCB increased for both peripheral vessels and shunts, which contributed to growth.

In Neurovascular, sales of thrombectomy catheters and flow diverters increased.

In Non vascular, gastrointestinal related sales increased.

In DMS, blood glucose measuring equipment sales increased.

In Medical equipment, increased sales of small and medium-sized medical equipment contributed.

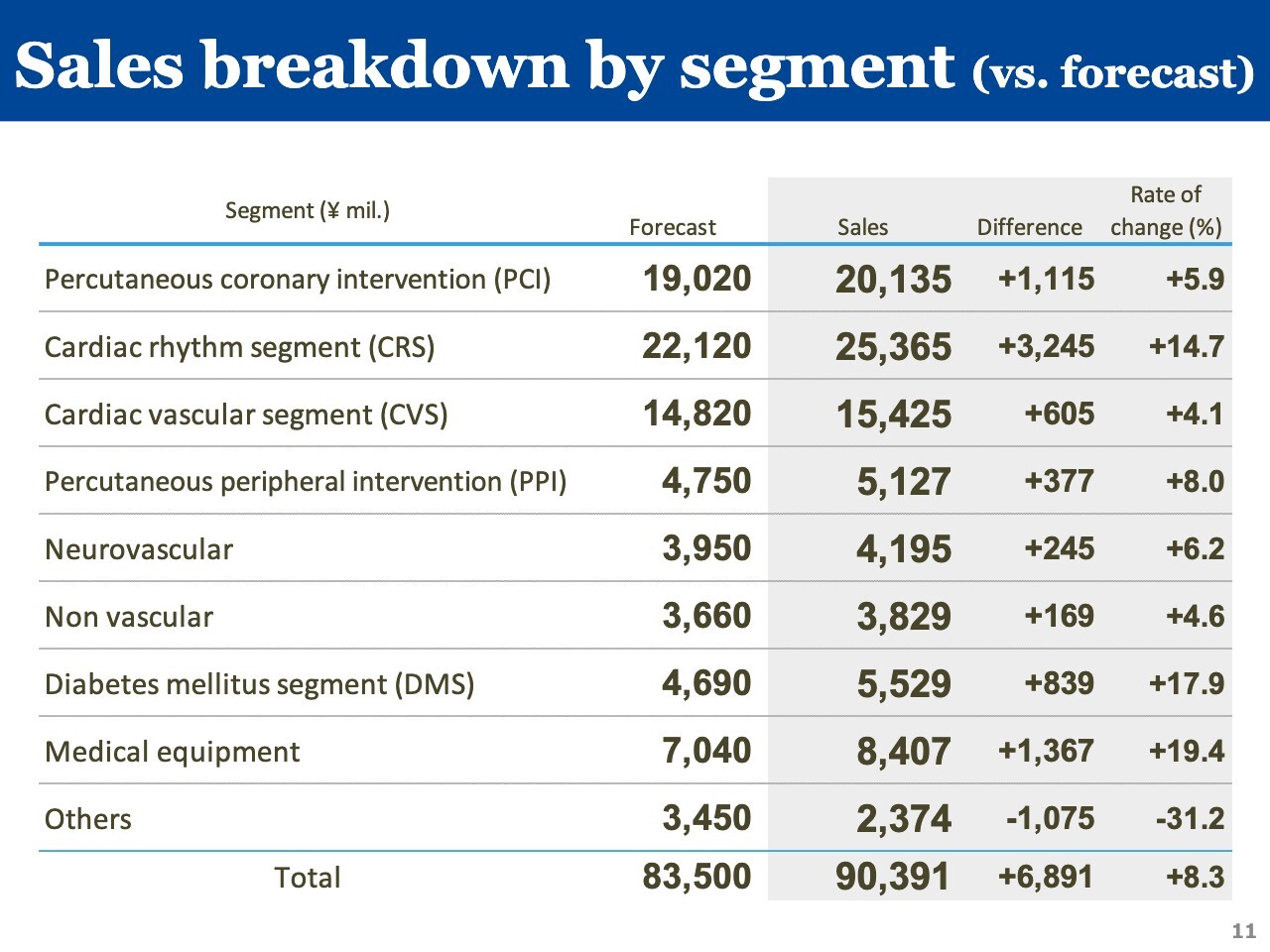

Sales breakdown by segment (vs. forecast)

I will explain the sales breakdown by segment against the forecast. Here too, all segments except Others exceeded the forecast.

In PCI, in addition to the increase in the number of clinical cases, sales of high unit price devices such as DCB and IVL exceeded the forecast.

In CRS, ablation-related sales exceeded the forecast, driven by expanded sales of PFA devices.

In CVS, sales exceeded the forecast due to increased sales of SHD-related products and Impella.

In PPI, increased DCB sales contributed, and sales exceeded the forecast.

In Neurovascular, sales of thrombectomy devices and flow diverters increased and exceeded the forecast.

In Non vascular, sales exceeded the forecast due to increased gastrointestinal related sales.

In DMS, sales exceeded the forecast due to higher sales of blood glucose measuring equipment and other factors.

In Medical equipment, sales exceeded the forecast as projects were steadily converted into contracts.

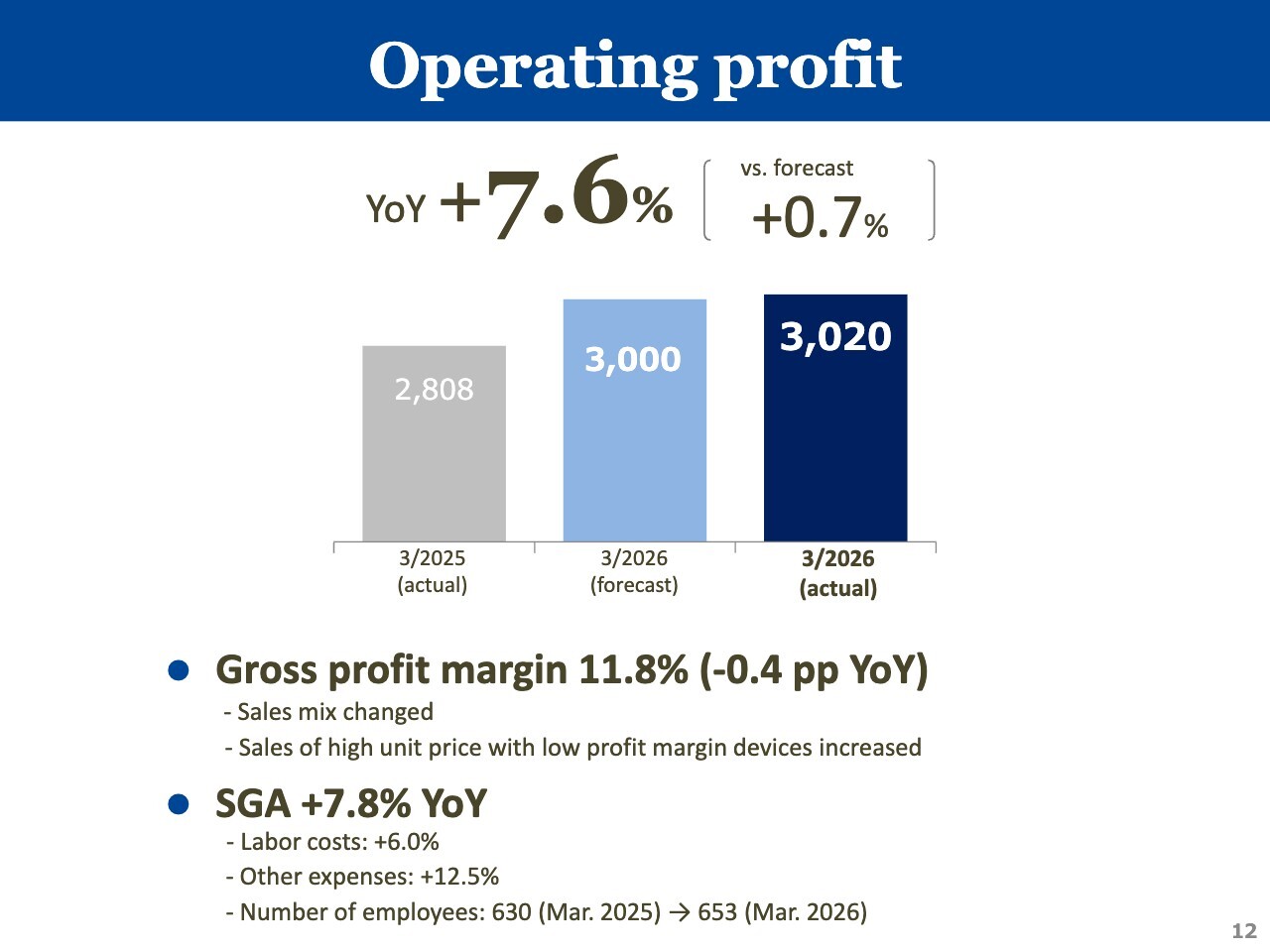

Operating profit

I will explain operating profit. In line with the increase in sales, gross profit for the fiscal year under review marked an all-time high.

On the other hand, gross profit margin decreased 0.4 percentage points from 12.2% in the previous fiscal year to 11.8%. This was mainly due to changes in the overall sales mix and a higher sales mix of high unit price, low profit margin devices.

On the cost side, labor costs increased 6.0% year on year, partly because the number of employees across the Group increased by 23 from the end of the previous fiscal year. Other expenses increased 12.5% year on year due to expenses related to the acquisition of Plusten Medical and higher depreciation. However, overall SG&A expenses rose 7.8%, a moderate increase compared with the growth in sales.

As a result, operating profit increased 7.6% year on year to ¥3,020 million. Operating profit also exceeded the forecast by 0.7%, reflecting higher gross profit and labor costs below the forecast, among other factors.

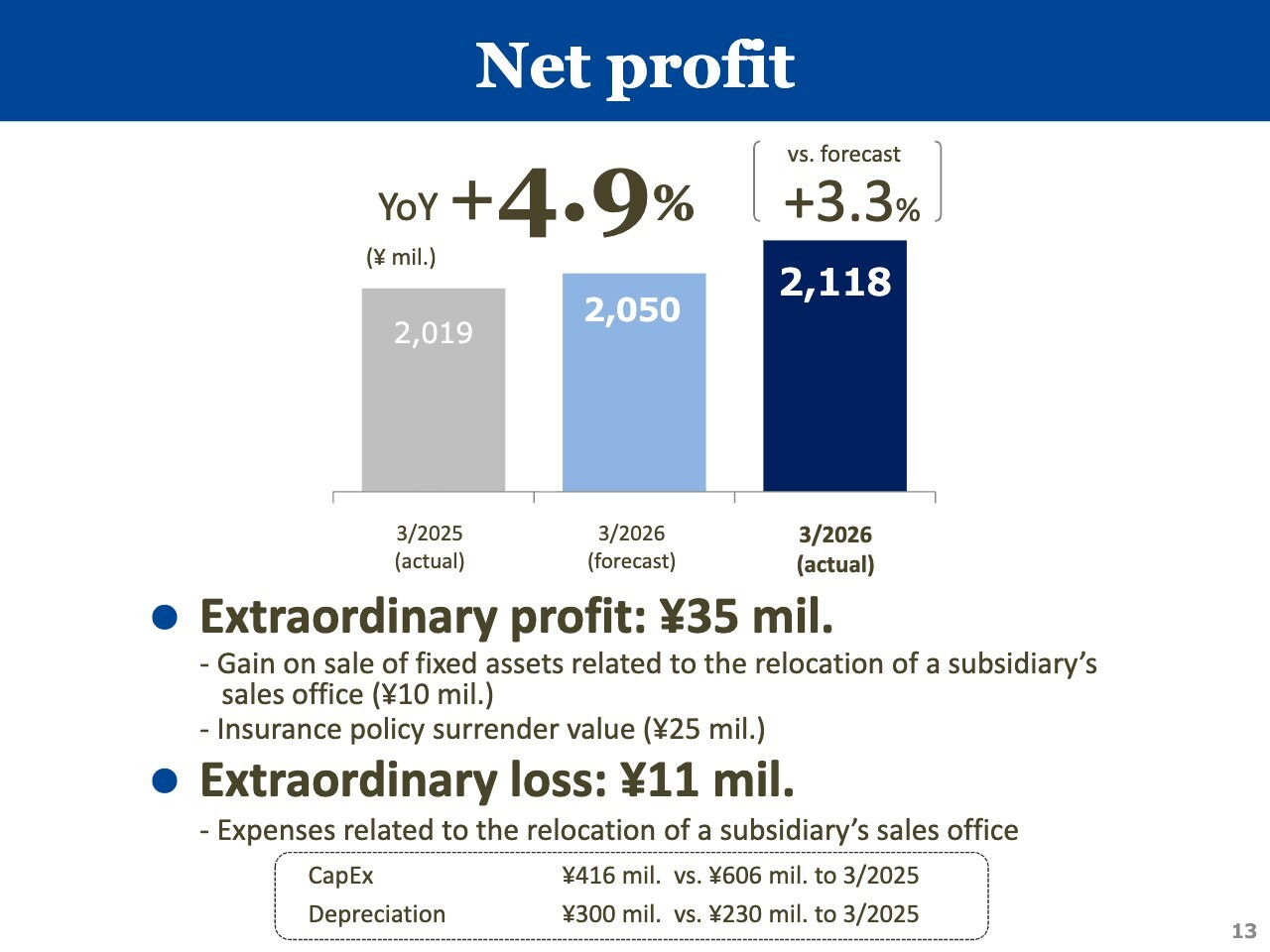

Net profit

Net profit increased 4.9% year on year to ¥2,118 million.

Extraordinary profit included ¥10 million in gain on sale of fixed assets related to the relocation of a subsidiary’s sales office and ¥25 million in insurance policy surrender value at Plusten Medical, for a total of ¥35 million.

Extraordinary loss included ¥11 million in expenses related to the relocation of a subsidiary’s sales office.

As a result, ROE at the end of the fiscal year was 8.9%, up from 8.5% in the previous fiscal year.

Capital expenditure for the fiscal year was ¥410 million, mainly for the development of the new logistics and sales management system and investments in rental medical equipment. Depreciation was ¥300 million, mainly for rental medical equipment.

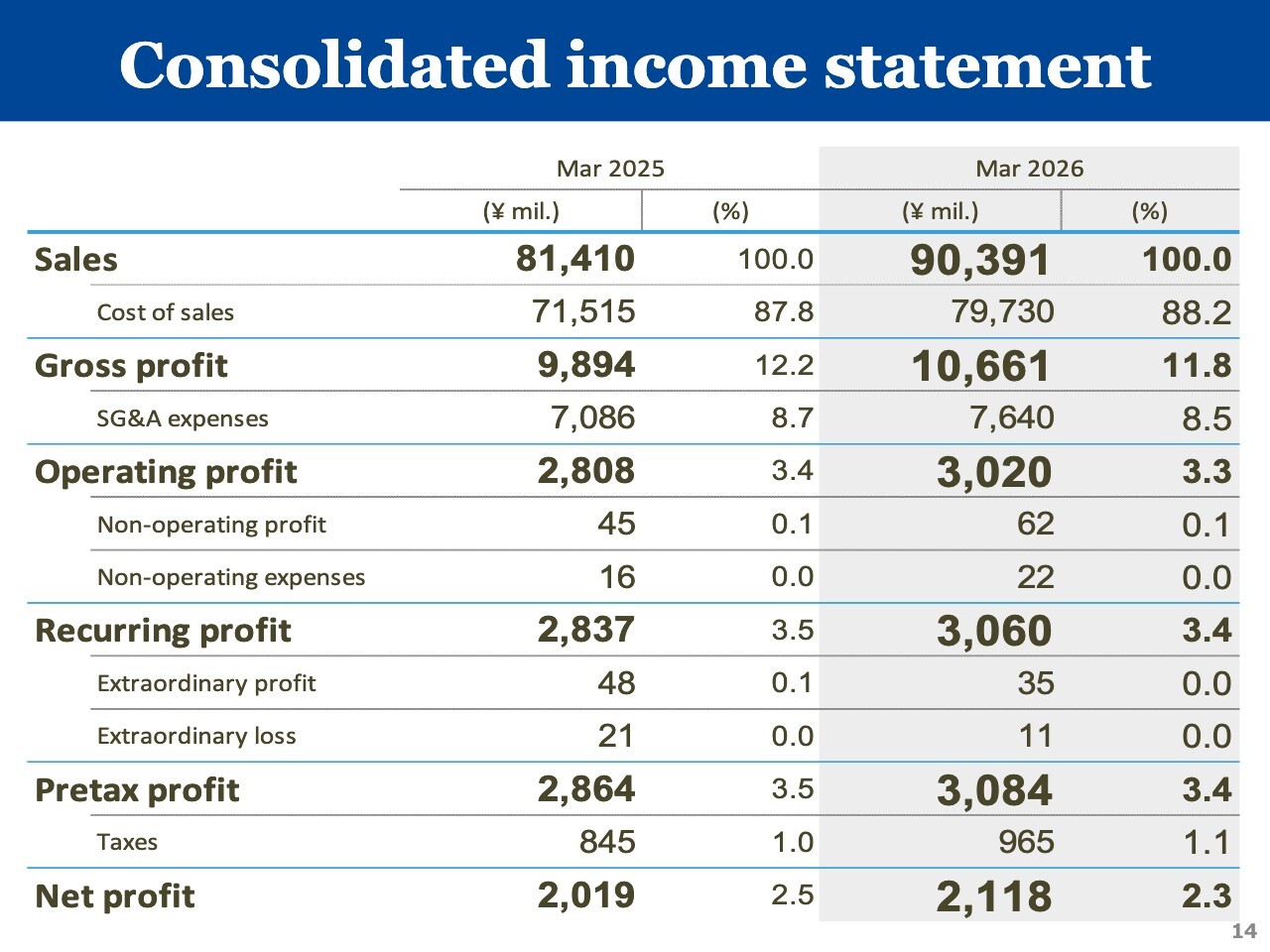

Consolidated income statement

The outline of the income statement is as shown on the slide. Sales and gross profit both marked all-time highs.

Non-operating profit increased due to higher interest income from investment securities. The main details of extraordinary profit and extraordinary loss are as I explained earlier.

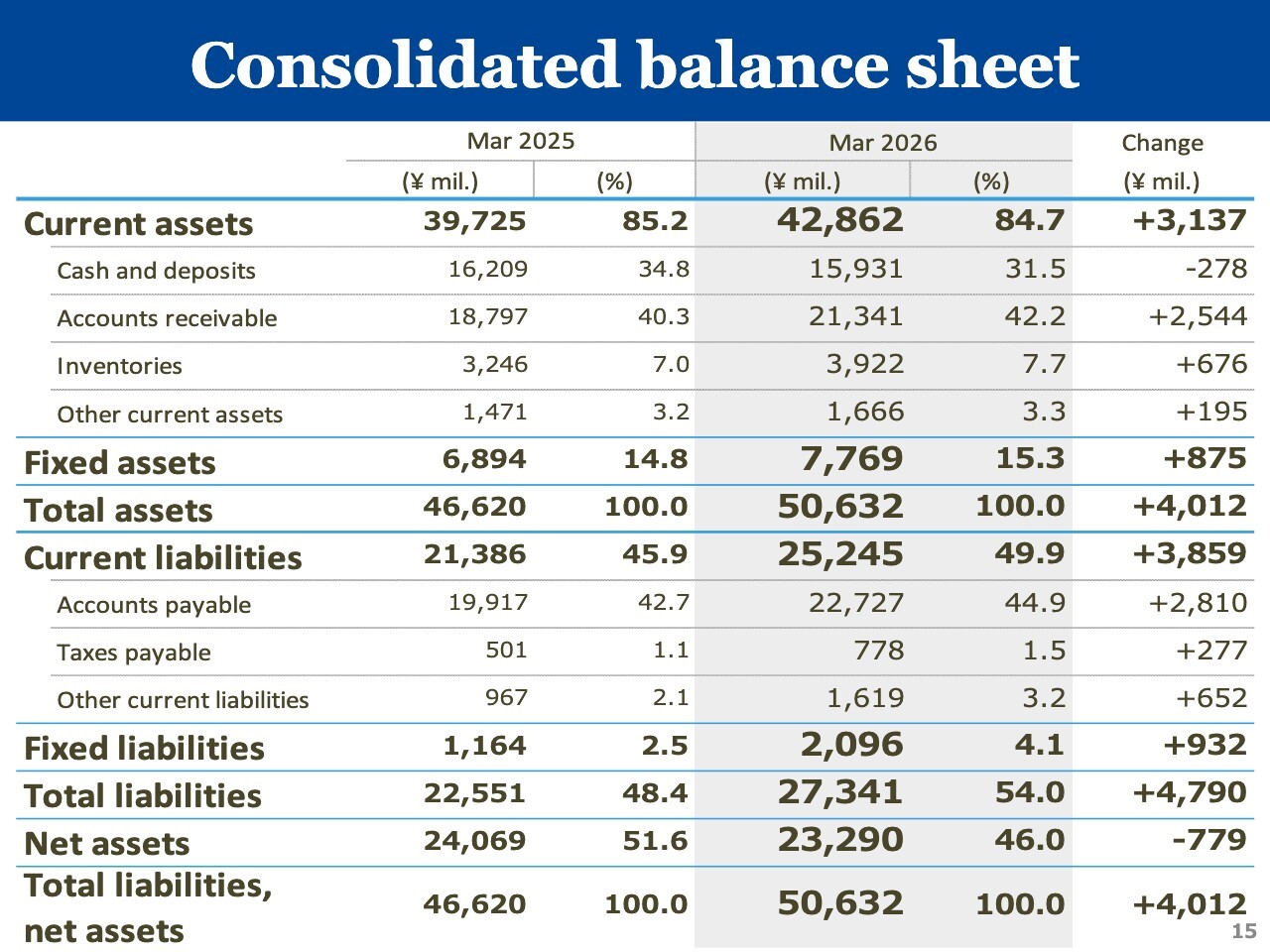

Consolidated balance sheet

I will explain the main changes in the balance sheet. Under assets, accounts receivable increased in line with sales growth. The increase in inventories was due to medical device consumables purchased in bulk. Fixed assets increased mainly due to goodwill recorded in connection with the acquisition of Plusten Medical.

Under liabilities, as with accounts receivable, accounts payable increased due to sales growth. The increase in fixed liabilities was mainly attributable to higher lease liabilities.

Under net assets, retained earnings increased, while net assets were reduced due to the purchase of treasury shares. As a result, total assets increased ¥4,012 million from the end of March 2025 to ¥50,632 million.

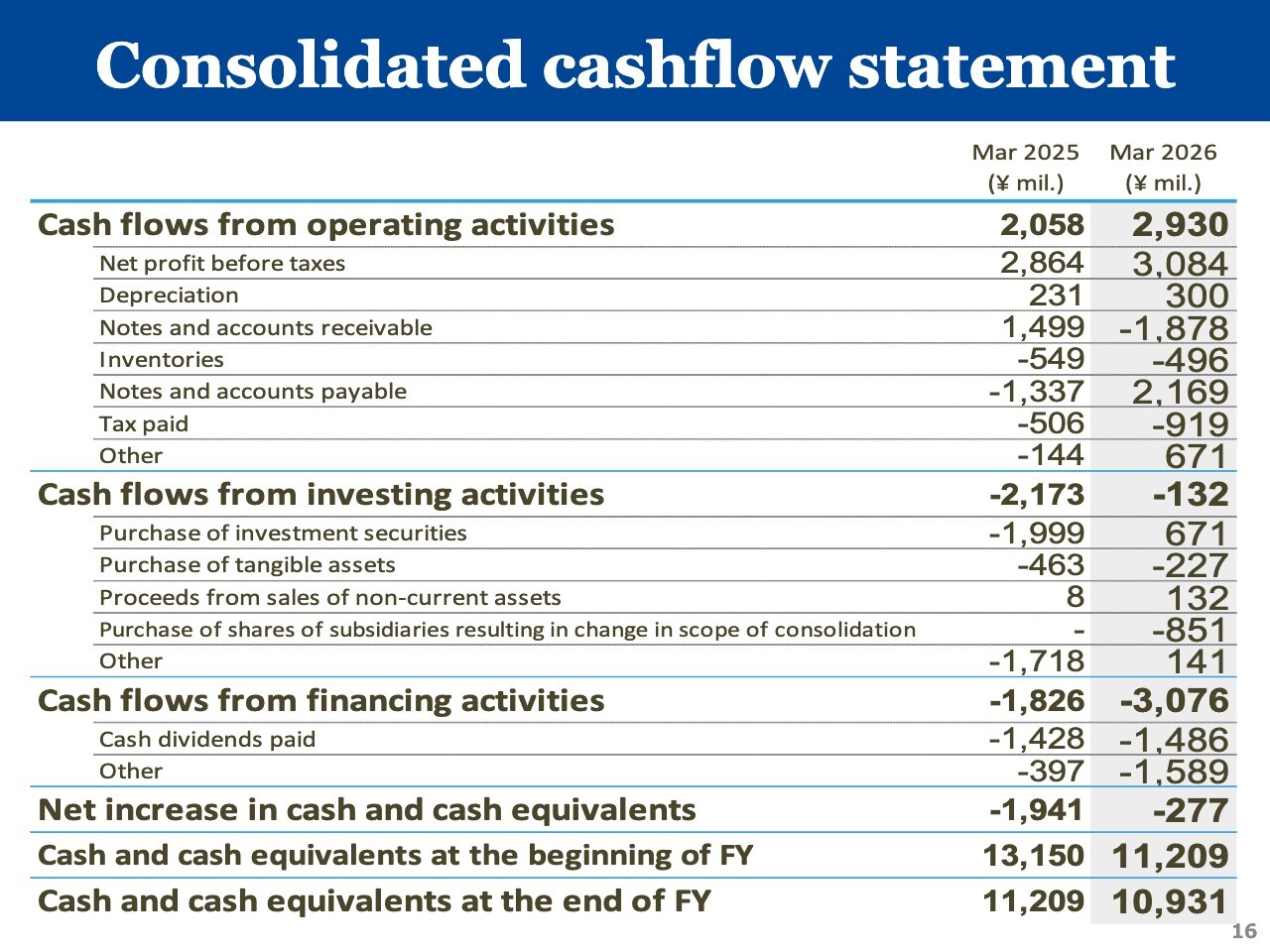

Consolidated cashflow statement

I will explain the consolidated cashflow statement. Cash flows from operating activities were positive ¥2,930 million.

Cash flows from investing activities were negative ¥132 million, mainly due to the acquisition of Plusten Medical. Negative cash flows from financing activities were mainly due to cash dividends paid and the purchase of treasury shares.

As a result, cash and cash equivalents at the end of the fiscal year were ¥10,931 million. Including time deposits, cash and deposits at the end of the fiscal year were ¥15,931 million, as shown on the balance sheet.

This concludes the overview of results for the fiscal year under review.

Business environment

Akizawa: I will explain the outlook for fiscal year ending March 2027.

First, I will cover the business environment. Since the conflict between the United States and Iran began, crude oil prices have remained elevated. In addition, supply chain disruptions have led to frequent price increases for related products, adding further pressure to inflation.

Medical institutions continue to face shortages of healthcare professionals, including doctors and nurses, which has become a burden on hospital management. Against this backdrop, the medical fee revision scheduled for June 2026 will be at the highest level in around 30 years, which can be regarded as positive news for medical institutions.

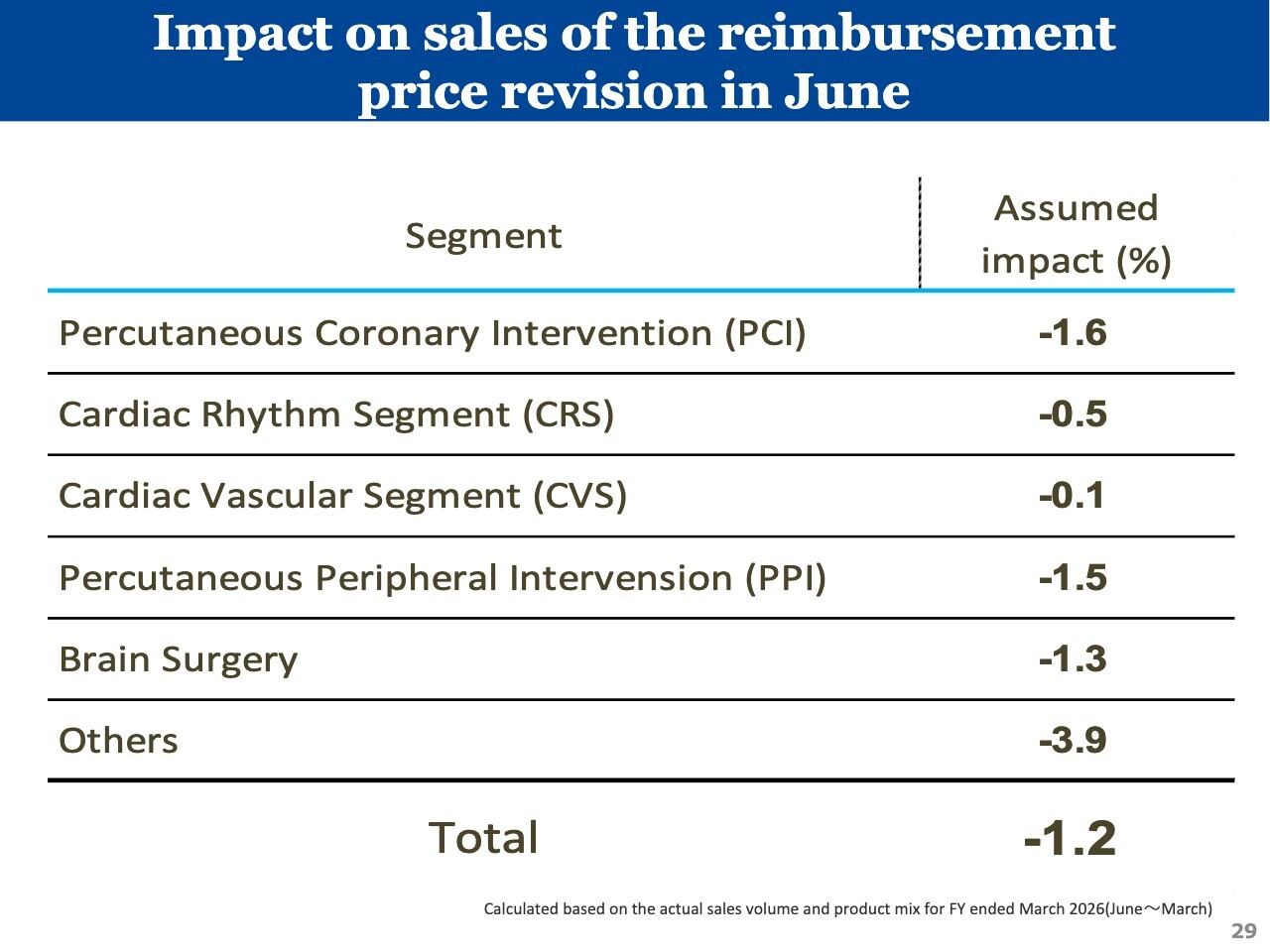

In addition, the revision of reimbursement prices for medical devices will be down 0.1% overall, with no sharp decline of the kind initially feared. As a result, the impact on the Company’s sales is expected to be negative 1.2%, and we do not expect it to be a major negative factor.

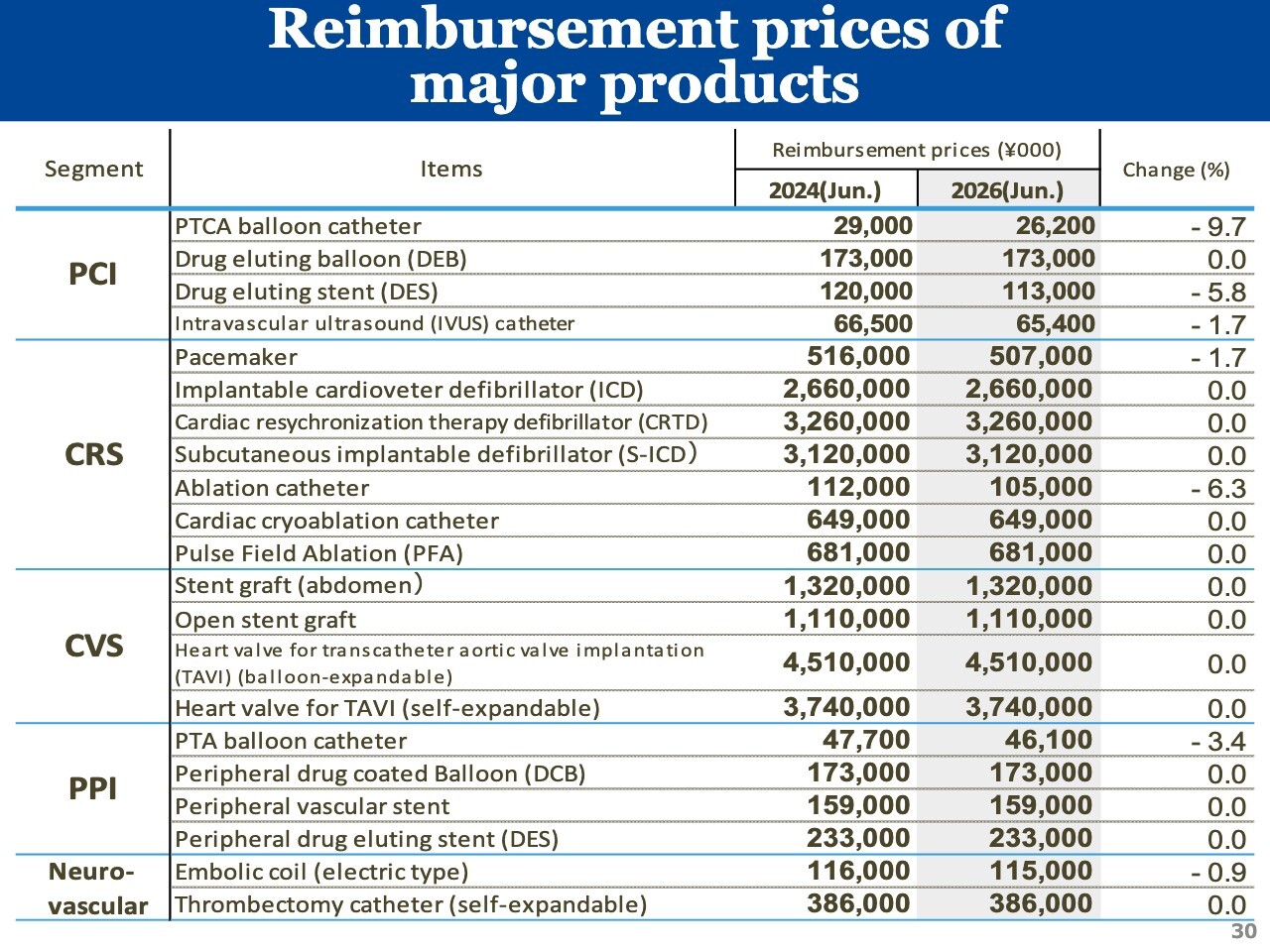

The impact by product segment and reimbursement prices for products are shown in the references on slides 29 and 30.

On the other hand, uncertainty over the outlook is also increasing due to the situation in the Middle East, the course of the war between Russia and Ukraine, and the policies that the Trump administration may introduce going forward.

In this environment, there is a strong need to both operate hospitals efficiently and maintain a system for delivering safe and secure medical care. Through various proposals and support, we aim to contribute to achieving these objectives.

WIN’s initiatives ①

Our main initiatives for this fiscal year are as follows. First, we are prioritizing support for customers to grow. The supplementary budget at the end of FY2025 and the recent medical fee revision are positive factors for medical institutions. However, we believe many medical institutions will continue to face difficult management conditions due to inflation and rising labor costs.

The recent medical fee revision also appears to reflect an intention to encourage the reorganization of acute-care hospitals in anticipation of the new regional healthcare vision to be formulated from FY2026 onward. While this is likely to lead to a shift in functions at some acute-care hospitals, we believe it may also benefit the Company, as our primary customers are core regional hospitals.

We regard this as an opportunity to support the growth of leading hospitals.

Through a range of proposals, we will support customer hospitals in strengthening their business foundations and operating more efficiently.

To this end, we will further promote separation of delivery and sales activities, with WIN Heart Gate, our logistics base, as the starting point. First, by around June, we plan to transfer nearly all major customers at major facilities handled by our Kanto business site, our largest business site, to the WIN Heart Gate-based logistics model.

After that, we will sequentially transfer facilities handled by the nine business sites in the Kanto region by January 2028. Through these transfers, we will improve the efficiency of on-site operations through inventory-taking using RFID and other measures. We will use the freed-up time to enhance proposal-based sales activity and improve the quality and quantity of sales activities, further expanding support for customer growth.

Next, I will explain WIN Asset, a service we launched in April. WIN Asset is a SaaS service that centrally manages all medical equipment and assets held by medical facilities on the cloud. It has a very simple and easy-to-use design, and in one case it reduced the working hours of clinical engineers responsible for managing medical equipment by approximately 60%.

In addition, appropriate management of medical equipment in use helps maximize equipment life and curb unnecessary replacement, leading to long-term cost reductions. WIN Asset uses a monthly flat-rate pricing system based on the number of beds, making the fee structure easy for hospitals to understand. It has currently been introduced at around 50 facilities, and we plan to expand this to around 150 facilities during the fiscal year.

Starting this fiscal year, we will introduce a new system for daily sales reports used by sales personnel. This will allow all sales personnel to share information from other departments across departmental and company boundaries and use it in their own sales activities.

In addition, we will further promote human interaction within the Group, which we have been advancing since FY2025, and provide support for customer growth across regions through Group-wide sales activities. We will also regularly analyze the information collected daily from more than 400 sales personnel using AI, so that we can identify customer issues and necessary sales activities without missing anything and provide timely support for proposals.

WIN’s initiatives ②

Another initiative is to improve the gross profit margin. In recent years, the Company’s gross profit margin has been on a downward trend, and we have been unable to achieve the gross profit margin set as our initial target. Factors include reimbursement price revisions and changes in product mix, but we cannot use these as excuses or overlook the situation.

To improve this situation, we will implement several measures. Current inflation is also affecting medical equipment manufacturers, and even as reimbursement prices are being reduced, we are receiving requests for price increases for some products due to rising material prices. For these products, we will work to curb price increases while seeking customer understanding, and proceed with price negotiations to secure appropriate profit.

As a leading dealer in cardiac-related products, we believe our sales capabilities are also significant for manufacturers. For general-purpose products, by appropriately managing product share, we can provide customers with cost benefits through volume discounts and manufacturers with the benefits of expanded share.

For this reason, we will negotiate with manufacturers in liaison with customer hospitals and strive to ensure that each party can secure appropriate profit.

In addition, by expanding WIN Asset, which I explained earlier, and Shinzo-kun, our proprietary system for managing major medical materials and devices, we plan to expand a recurring revenue business model that does not rely on transaction-based medical equipment sales.

Shinzo-kun has currently been introduced at around 90 facilities. All of these facilities are equipped for cloud connection, and one-quarter of them have automated master data updates for medical materials that were previously performed manually.

This improves operational efficiency. At the same time, we will expand installations of Shinzo-kun to 150 facilities during the fiscal year and increase recurring revenue.

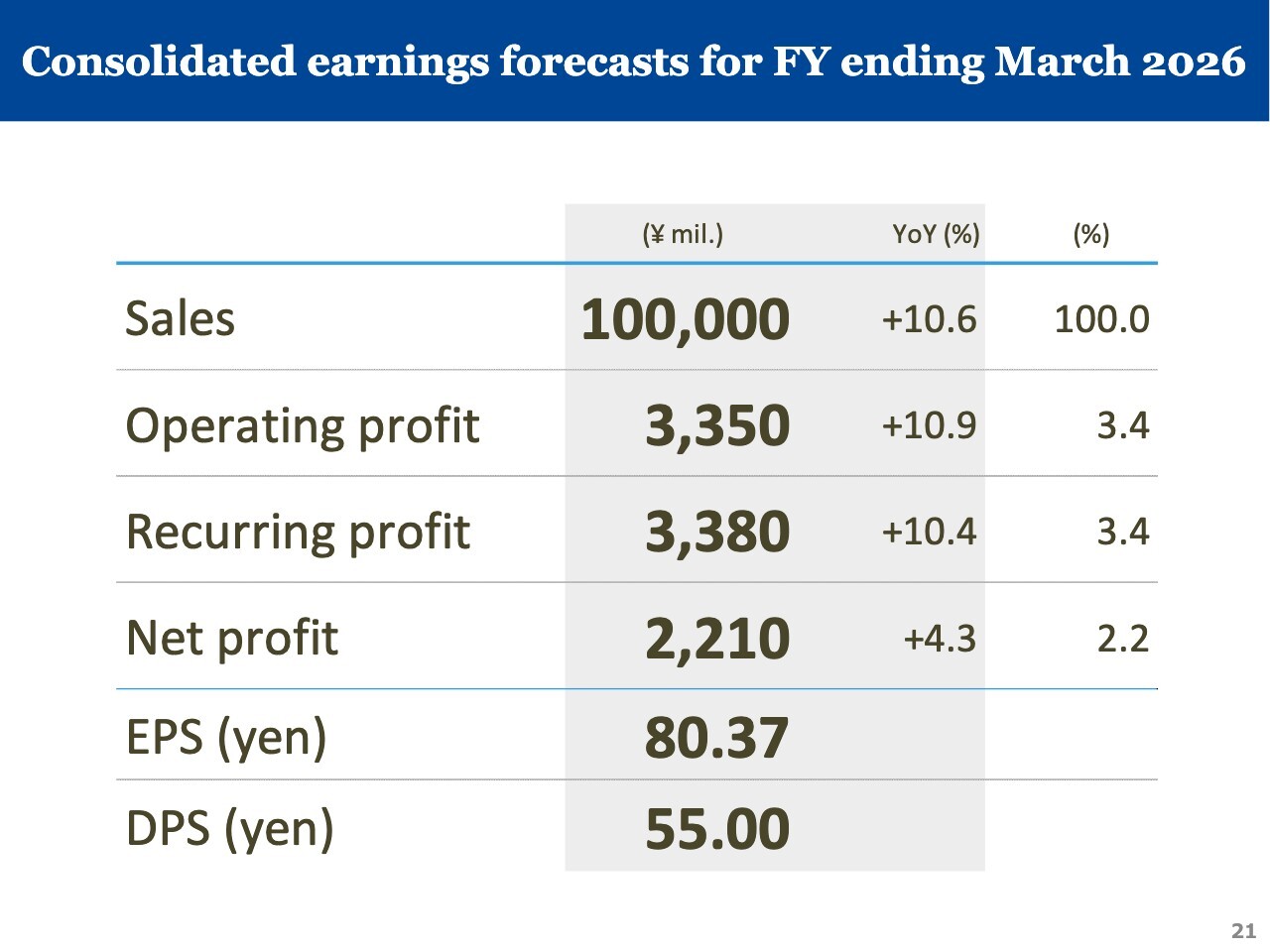

Consolidated earnings forecasts for FY ending March 2027

Based on these initiatives, here is our earnings forecasts for this fiscal year. We forecast sales at the ¥100,000 million level.

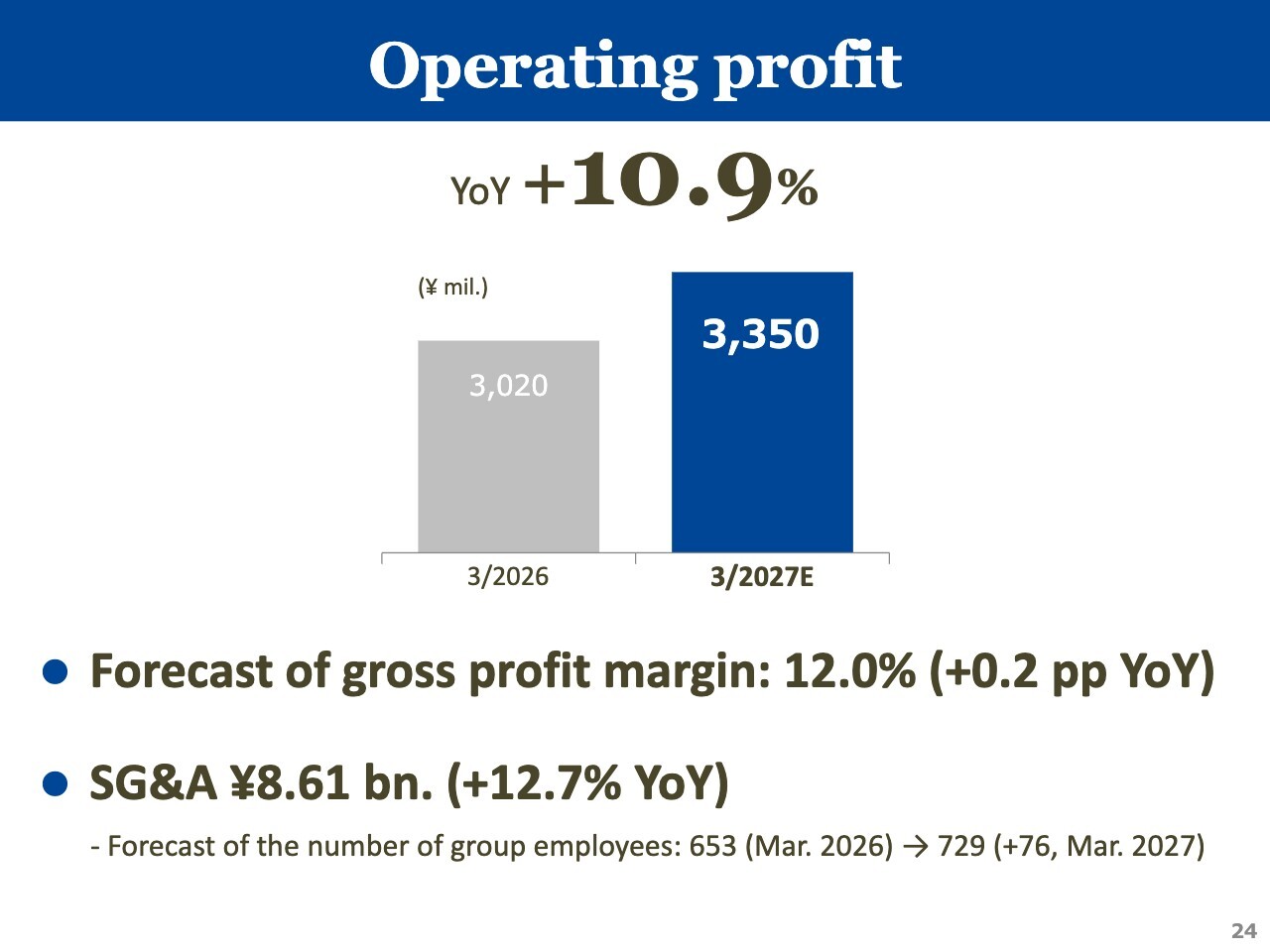

Supported by the profit increase from sales growth and an improvement in gross profit margin, operating profit is expected to increase 10.9% year on year to ¥3,350 million. If achieved, this would mark a new record high in operating profit for the first time in eight years, surpassing the previous record of ¥3,260 million in the fiscal year ended March 2019.

Sales

For sales, we forecast a 10.6% year-on-year increase to ¥100,000 million.

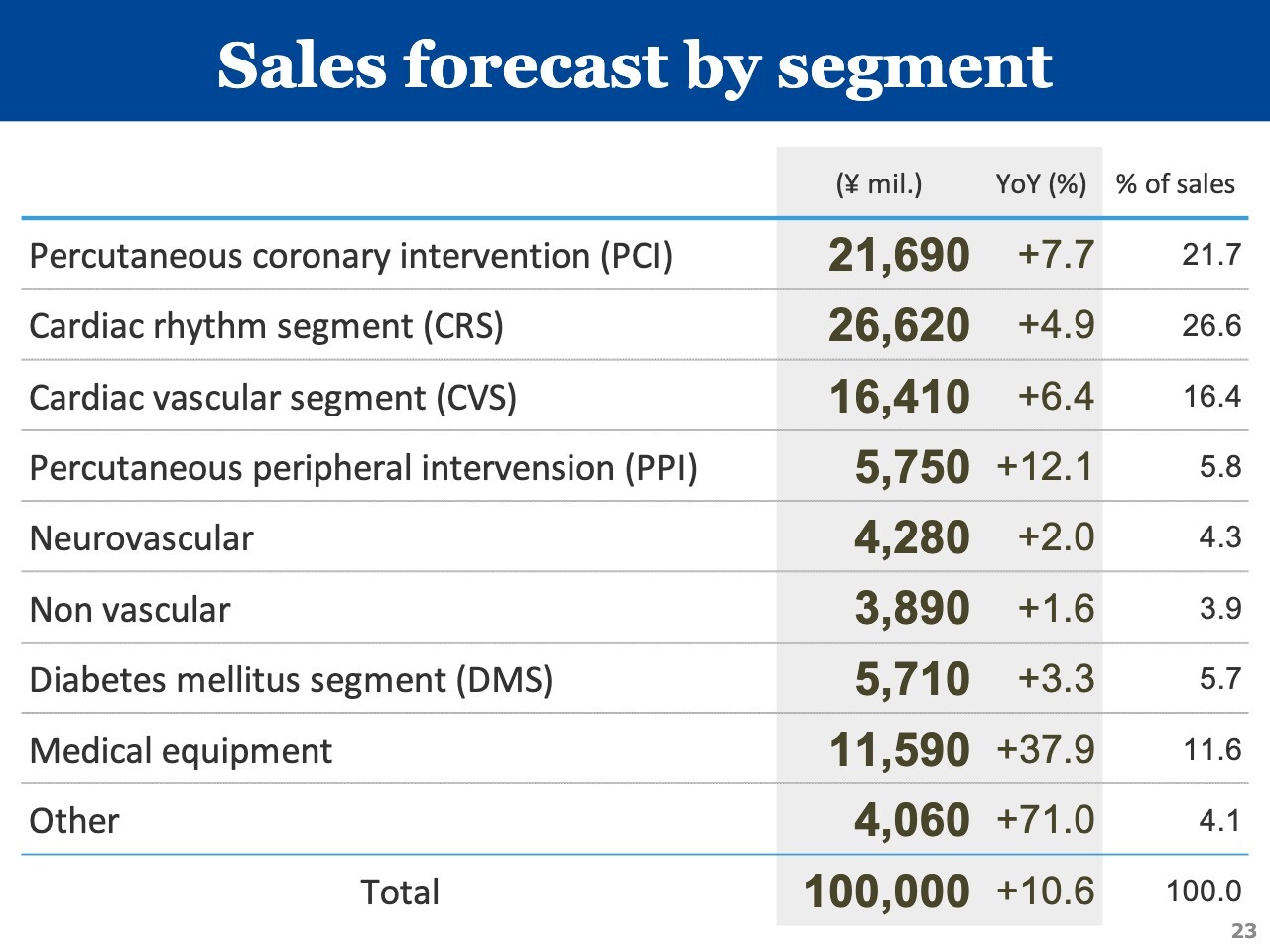

Sales forecast by segment

This is the sales forecast by segment.

In PCI, we will further strengthen support for patient acquisition at leading facilities and work to increase the number of clinical cases. We also expect sales growth in high unit price devices such as DCB and IVL to continue.

In CRS, we aim to expand sales by steadily capturing market growth in areas such as PFA, where further adoption at new facilities is expected to continue.

In CVS, we plan sales growth from SHD-related products, including TAVI, and Impella again this fiscal year, as well as from gaining new customers.

In PPI, we expect sales of DCB to increase again this fiscal year, supported by an expanded number of manufacturers handling DCB and a broader product lineup. We also expect increased use of renal denervation devices that were listed for insurance reimbursement in March 2026.

In Neurovascular, we expect demand for thrombectomy devices and flow diverters to continue growing.

In Non vascular, gastrointestinal related sales are expected to continue increasing.

In DMS, we plan to actively hold product briefings in cooperation with manufacturers and expand sales of insulin pumps and blood glucose measuring equipment.

For Medical equipment, in addition to projects carried over from the previous fiscal year, we will use information obtained from WIN Asset to capture equipment purchasing and replacement information earlier than before and work to secure projects steadily.

Operating profit

We forecast operating profit of ¥3,350 million, up 10.9% year on year. Gross profit margin is expected to rise 0.2 percentage points year on year to 12.0%, reflecting the effects of the measures I described earlier.

In terms of personnel, 23 new employees joined the Group in April, including nine new graduates and career hires. Although the hiring environment remains difficult, we will continue to focus on career hiring and plan to have 729 employees at the end of the fiscal year.

Operating expenses are also expected to increase due to the expansion of the Group’s business scale and continued active sales activities. As a result, SG&A expenses are planned to increase 12.7% from ¥7.64 billion in FY2025 to ¥8.61 billion.

Although the increase in SG&A expenses will be higher than sales growth, we plan to secure an increase in operating profit through sales expansion and an improvement in gross profit margin.

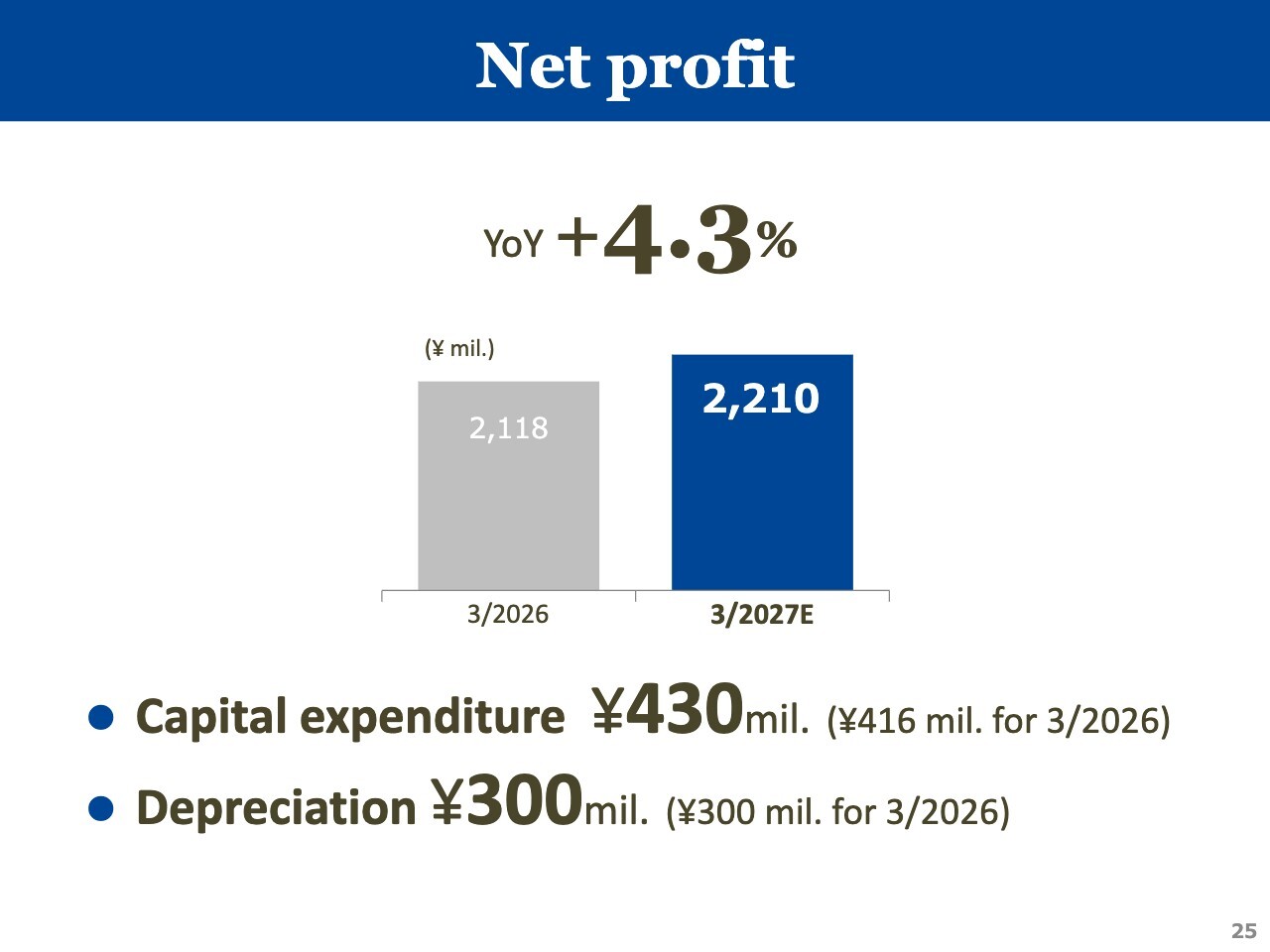

Net profit

We forecast net profit of ¥2,210 million, up 4.3% year on year. We do not expect to record extraordinary profit or extraordinary loss.

Capital expenditure for this fiscal year is planned at ¥430 million, mainly for the new logistics and sales management system and WIN Asset. Depreciation is planned at ¥300 million, mainly for rental medical equipment and the new logistics and sales management system.

Shareholder return

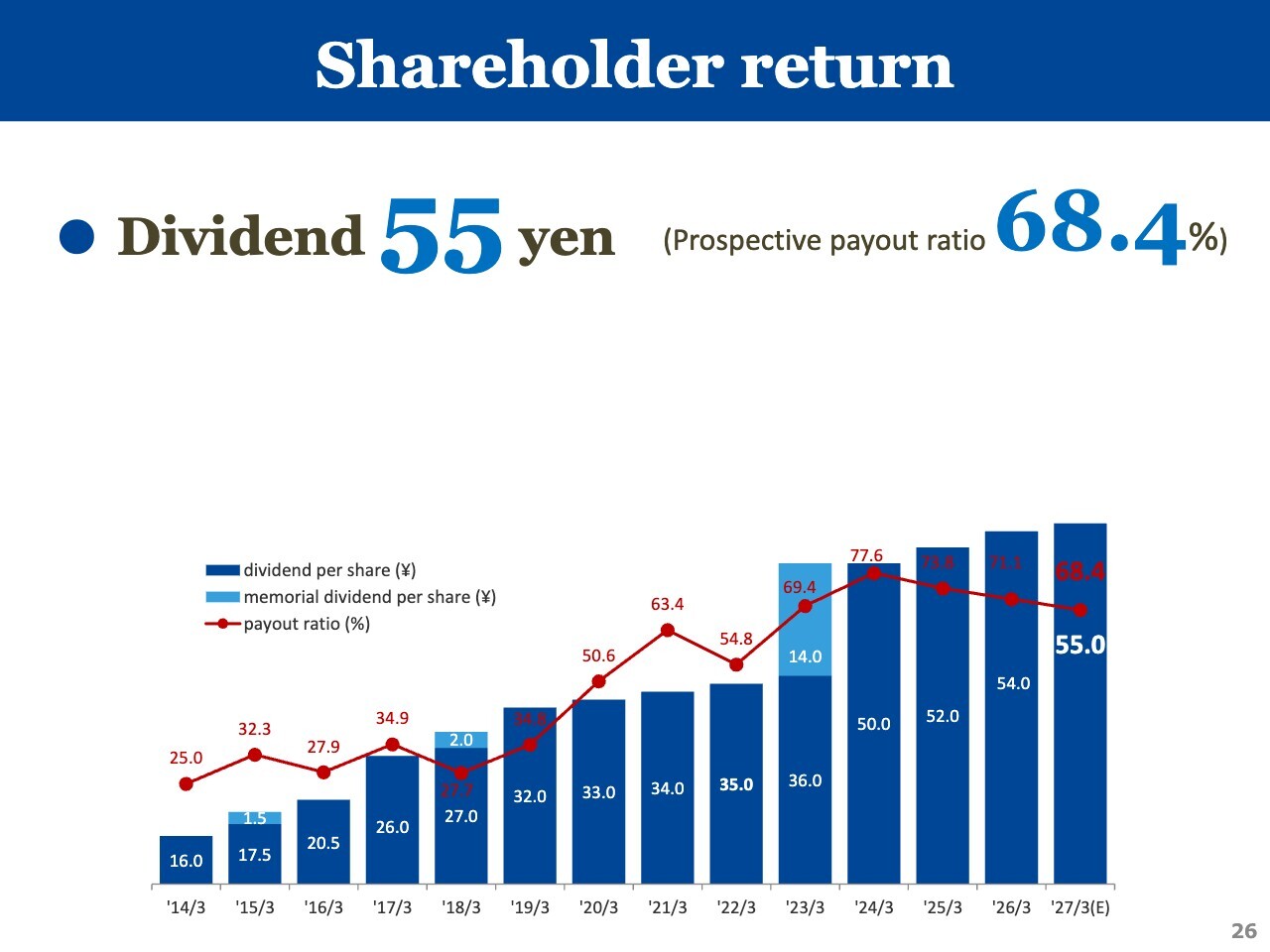

I will explain shareholder return. We plan to pay a year-end dividend for the fiscal year ended March 2026 of ¥54 per share, an increase of ¥2. For the fiscal year ending March 2027, we plan to raise the year-end dividend by another ¥1 to ¥55 per share. As a result, the prospective payout ratio will be 68.4%.

Strategy for future growth

Finally, I will discuss our strategy for future growth. The common thread among WIN Heart Gate, WIN Asset, and Shinzo-kun is digital.

Going forward, we will use RFID at WIN Heart Gate to promote separation of delivery and sales activities, while expanding new digital-driven services, including digital management of hospital assets through WIN Asset and digital management of medical materials and devices through Shinzo-kun. Through these initiatives, we aim to evolve and grow beyond our conventional business model.

Under this new growth trajectory, we will support customers’ growth and pursue the establishment of a more profitable business foundation.

Impact on sales of the reimbursement price revision in June

This reference shows the impact on sales of the reimbursement price revision.

Reimbursement prices of major products

This reference shows the reimbursement prices of major products.

This concludes my presentation. Thank you for your attention.