Website:https://www.toa-const.co.jp/eng/

IR Information:https://www.toa-const.co.jp/eng/ir/

IR Information: https://www.toa-const.co.jp/eng/ir/

FY2025 Financial Results Briefing Material

Takeshi Hayakawa (hereafter, “Hayakawa”): I am Takeshi Hayakawa, President and Representative Director. On April 7 of this year, a serious accident occurred during the demolition of an unloader crane—a project we were conducting—at the Keihin site of JFE Steel Corporation’s East Japan Works. As a result of this accident, three workers lost their lives, and one worker remains missing.

In addition, one person sustained serious injuries and remains hospitalized. We offer our heartfelt prayers for the repose of the souls of those who have passed away and extend our deepest condolences to their families. We also pray for the swift recovery of the injured person.

Furthermore, we fully recognize the profound anxiety and grief that the families of the missing are experiencing. We offer our sincere apologies and are working tirelessly every day to locate them as soon as possible.

We are currently cooperating fully with the relevant authorities in their investigation and are making every effort to determine the cause under the guidance of law enforcement and other relevant agencies. We take this matter extremely seriously and have established an internal accident investigation committee that includes external experts. We will verify and analyze the facts, formulate measures to prevent a recurrence, and ensure that they are thoroughly implemented.

On behalf of our company, we would like to express our deepest apologies for the immense distress and concern this devastating disaster has caused to the bereaved families, their loved ones, all those affected, and the wider community.

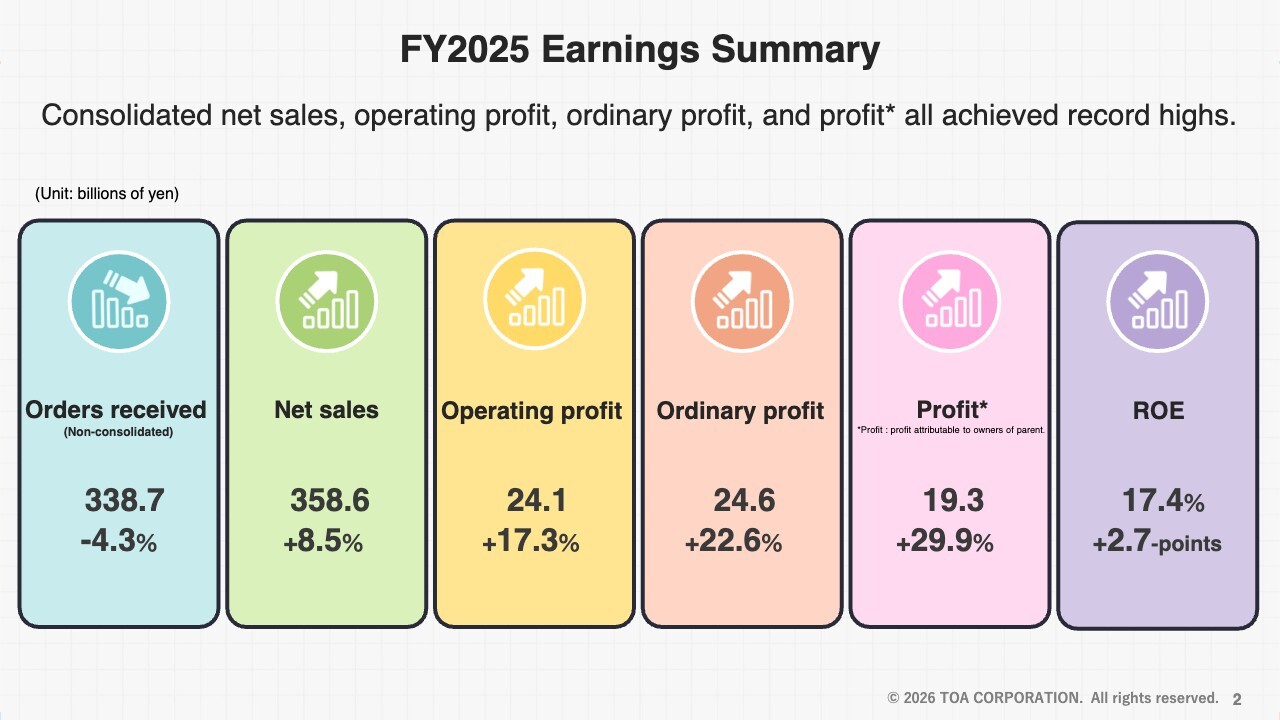

FY2025 Earnings Summary

Takeshi Nakao (hereinafter “Nakao”): Let me begin with the FY2025 earnings summary. During this fiscal year, we achieved record highs for all consolidated financial metrics, including net sales, operating profit, ordinary profit, and profit.

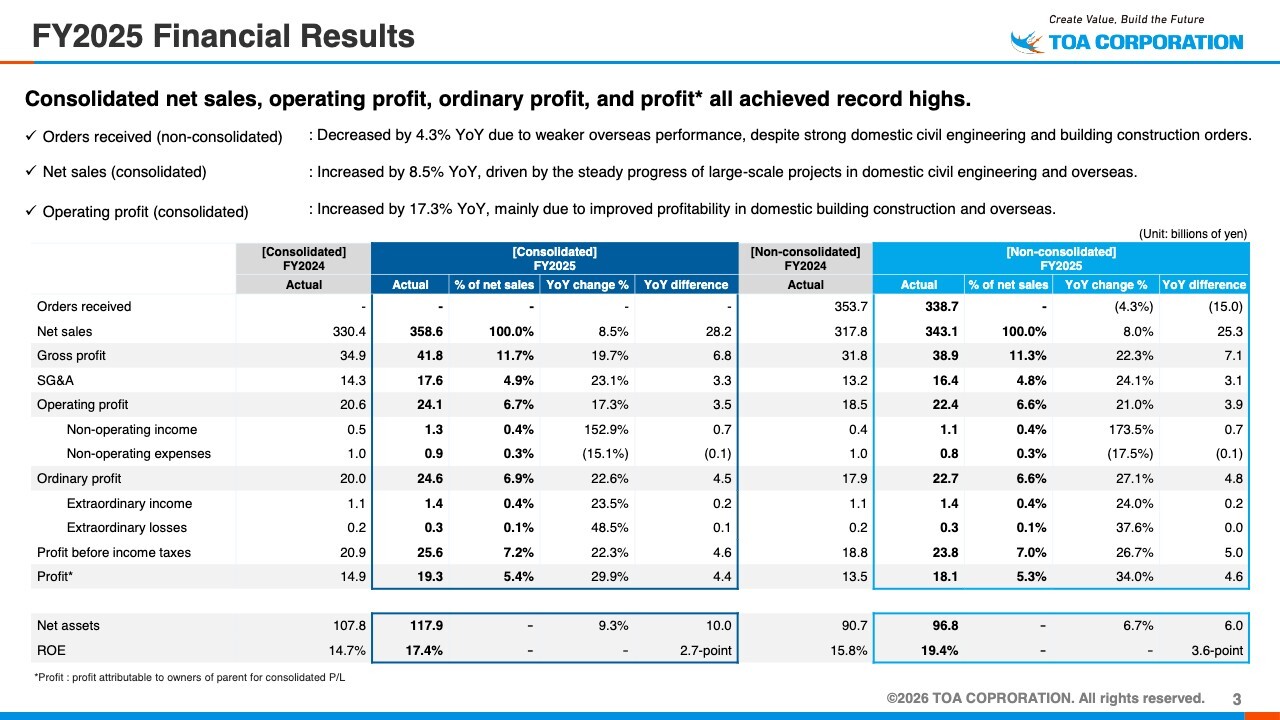

FY2025 Financial Results

Here are the FY2025 financial results. Non-consolidated orders received decreased by 4.3% YoY to ¥338.7 billion. While Domestic Civil Engineering and Domestic Building Construction steadily progressed in both public and private sector orders, Overseas fell below the previous year’s level. On the other hand, consolidated net sales increased by 8.5% YoY to ¥358.6 billion, due to the steady progress of large-scale projects in Domestic Civil Engineering and Overseas.

Consolidated operating profit increased by 17.3% YoY to ¥24.1 billion, driven primarily by improved profitability on large-scale projects in Domestic Building Construction and Overseas. Consolidated profit increased by 29.9% YoY to ¥19.3 billion.

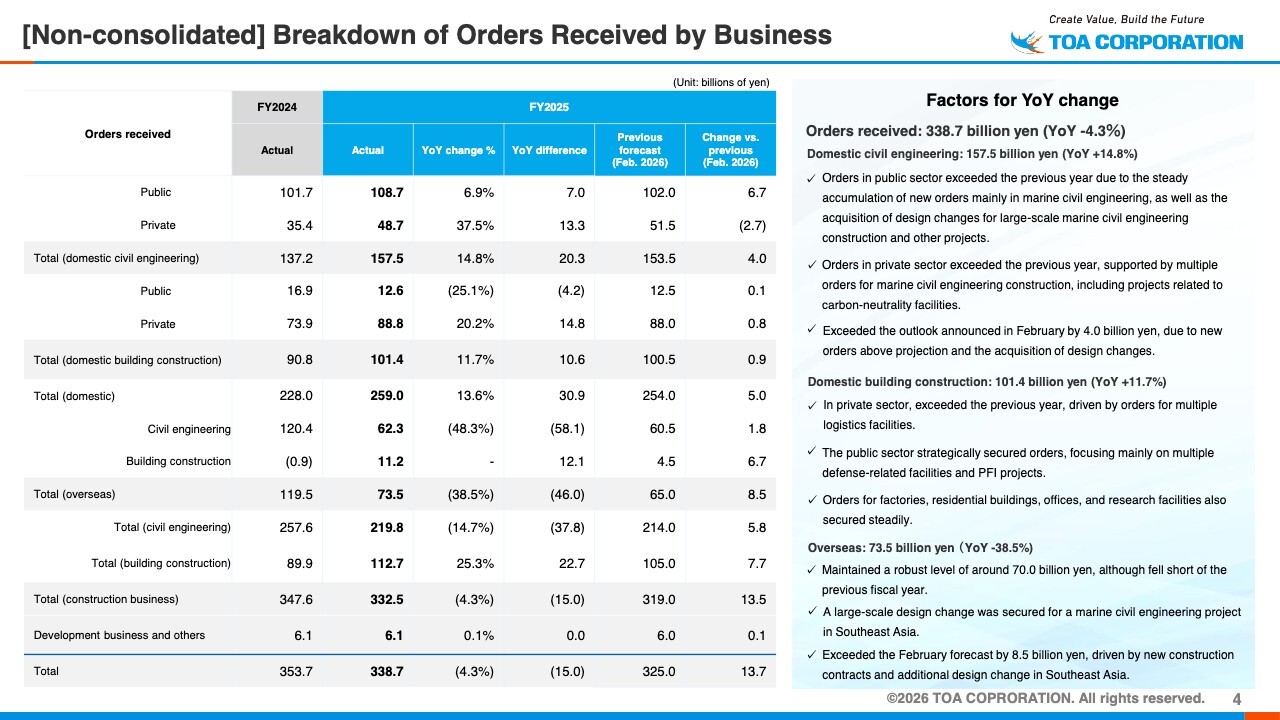

[Non-consolidated] Breakdown of Orders Received by Business

Here is the breakdown of orders received by business. Domestic Civil Engineering reached ¥157.5 billion, a 14.8% increase YoY, significantly surpassing the previous year’s figure thanks to contributions from private-sector marine civil engineering projects related to carbon-neutrality facilities. Orders in the public sector also remained at a high level.

Domestic Building Construction increased 11.7% YoY to ¥101.4 billion, with orders for multiple logistics facilities driving a significant YoY increase. Orders for factories, residential buildings, offices, and research facilities were also secured steadily.

Meanwhile, Overseas decreased by 38.5% YoY to ¥73.5 billion, with us being able to secure building construction contracts in South and Southeast Asia.

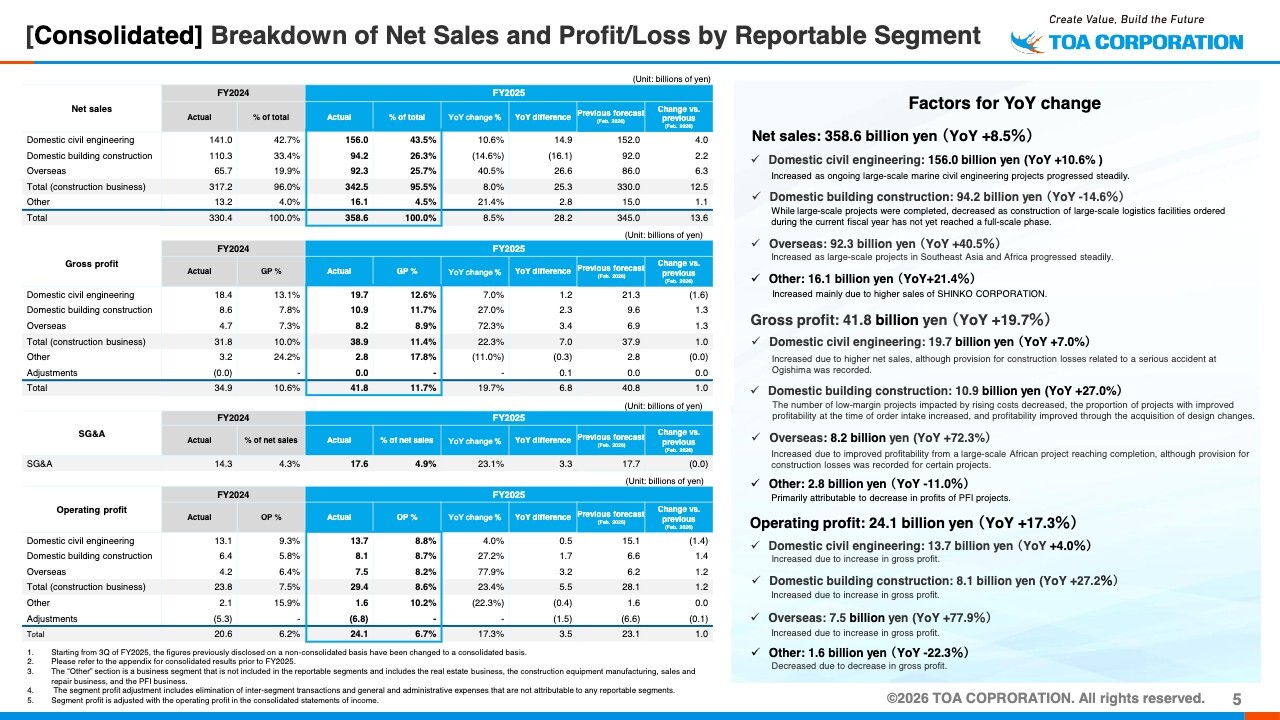

[Consolidated] Breakdown of Net Sales and Profit/Loss by Reportable Segment

Here is the breakdown of net sales and profit/loss by reportable segment. Net sales increased by 8.5% YoY to ¥358.6 billion. Net sales for Domestic Civil Engineering increased by 10.6% YoY to ¥156.0 billion, as ongoing large-scale marine civil engineering projects progressed steadily.

Net sales in Domestic Building Construction decreased by 14.6% YoY to ¥94.2 billion yen, as construction of large-scale logistics facilities ordered during the current fiscal year has not yet reached a full-scale phase while large-scale projects were completed. Overseas increased by 40.5% YoY to ¥92.3 billion yen, as large-scale projects in Southeast Asia and Africa progressed steadily.

Next, gross profit increased by 19.7% YoY to ¥41.8 billion overall. Gross profit in Domestic Civil Engineering increased by 7.0% YoY to ¥19.7 billion due to higher net sales, although provision for construction losses related to a serious accident at Ogishima was recorded.

Gross profit in Domestic Building Construction increased by 27.0% YoY to ¥10.9 billion, as low-margin projects impacted by rising costs decreased and the proportion of projects with improved profitability at the time of order intake increased.

Gross profit in Overseas increased by 72.3% YoY to ¥8.2 billion, due to improved profitability from a large-scale project reaching completion, although provision for construction losses was recorded for certain projects.

Let me briefly explain the current situation. The provision for construction losses related to the Ogishima accident in Domestic Civil Engineering was recorded in FY2025, and we believe it will not affect the profit outlook for FY2026.

In Domestic Building Construction, selective order intake has progressed and profitability at the time of order intake has improved, as rising costs have been successfully passed on through pricing. We expect this trend to continue going forward.

Regarding the provision for construction losses in Overseas, we intend to improve profitability through cost reviews and discussions with clients.

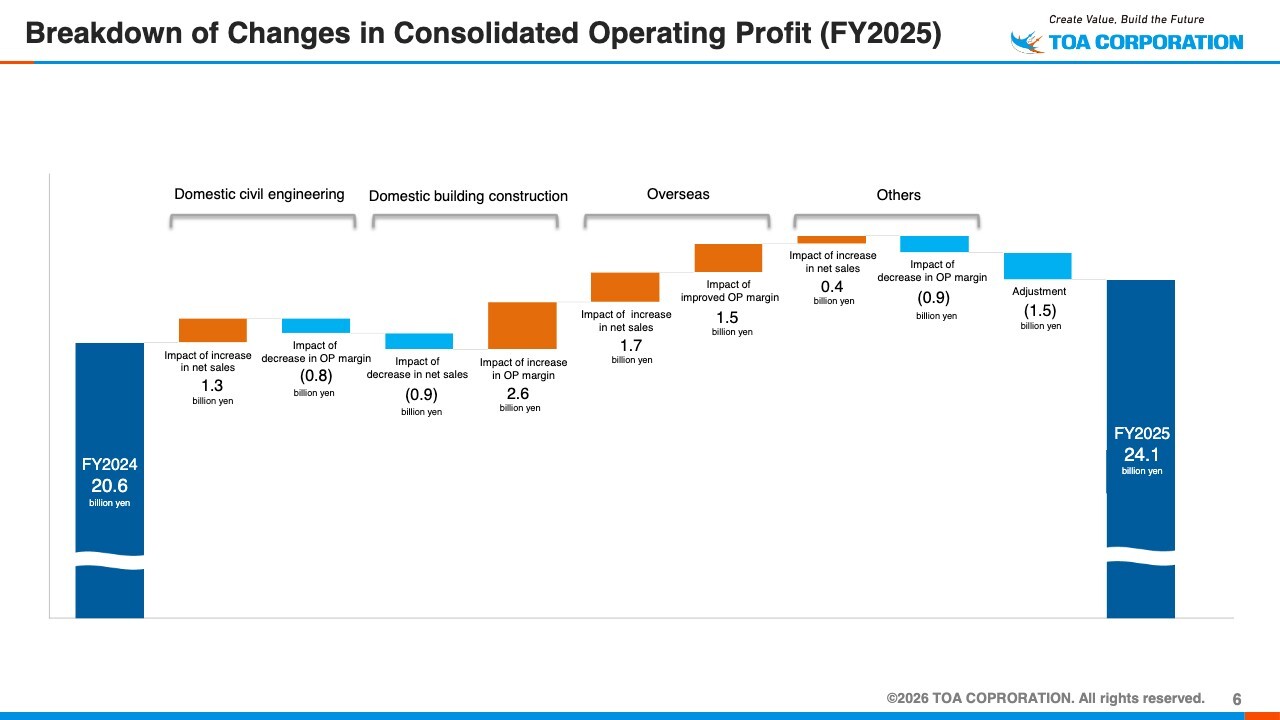

Breakdown of Changes in Consolidated Operating Profit (FY2025)

This slide shows the breakdown of changes in consolidated operating profit. In Domestic Civil Engineering, operating profit increased by ¥0.5 billion YoY, with a positive impact of ¥1.3 billion increase in net sales and a negative impact of ¥0.8 billion decrease in OP margin.

Domestic Building Construction increased by ¥1.7 billion YoY, reflecting a negative impact of ¥0.9 billion from a decrease in net sales and a positive impact of ¥2.6 billion from an increase in OP margin.

Overseas increased by ¥3.2 billion YoY, reflecting a positive impact of ¥1.7 billion from an increase in net sales and a positive impact of ¥1.5 billion from improved OP margin.

Consolidated operating profit was ¥20.6 billion in the previous fiscal year and increased by ¥3.5 billion to ¥24.1 billion in FY2025.

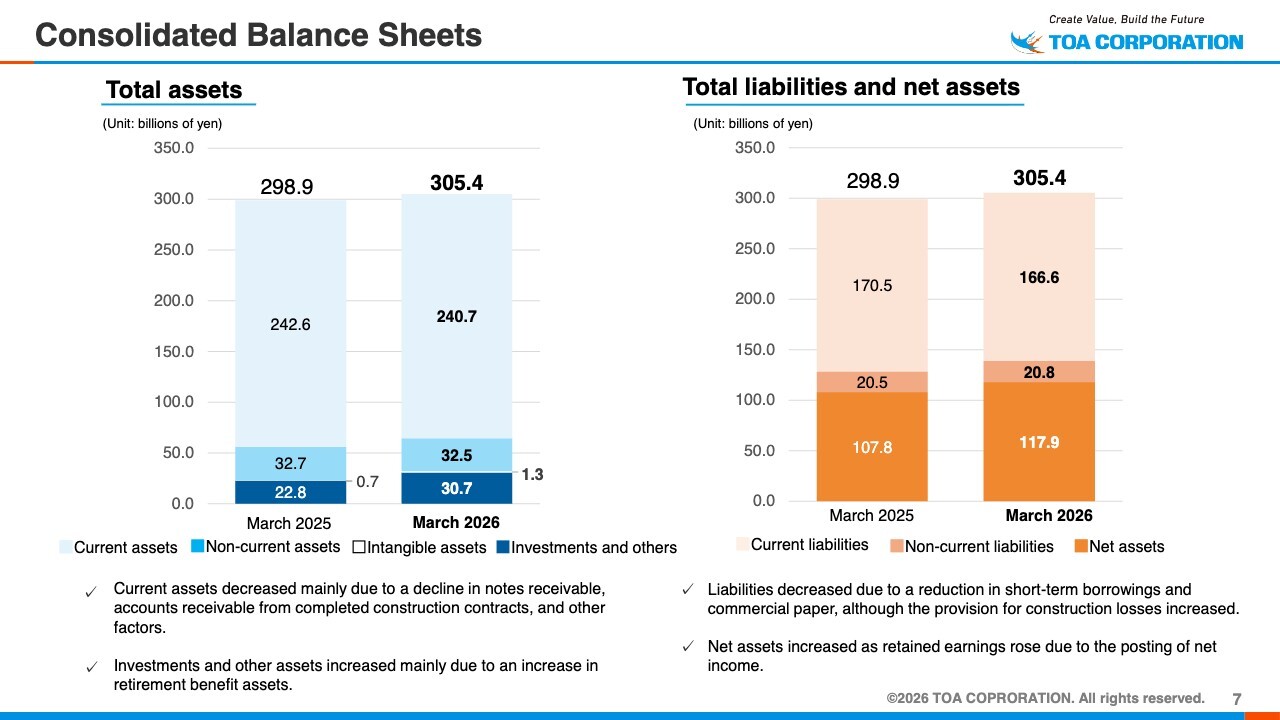

Consolidated Balance Sheets

This is the status of the consolidated balance sheets. Total assets increased to ¥305.4 billion. In current assets, notes receivable, accounts receivable from completed construction contracts and other items decreased thanks to progress in collecting payments for large-scale construction projects.

Investments and other assets increased mainly due to an increase in retirement benefit assets.

Liabilities decreased due to a reduction in short-term borrowings and commercial paper, although the provision for construction losses increased.

Net assets increased as retained earnings rose due to the posting of profit attributable to owners of parent.

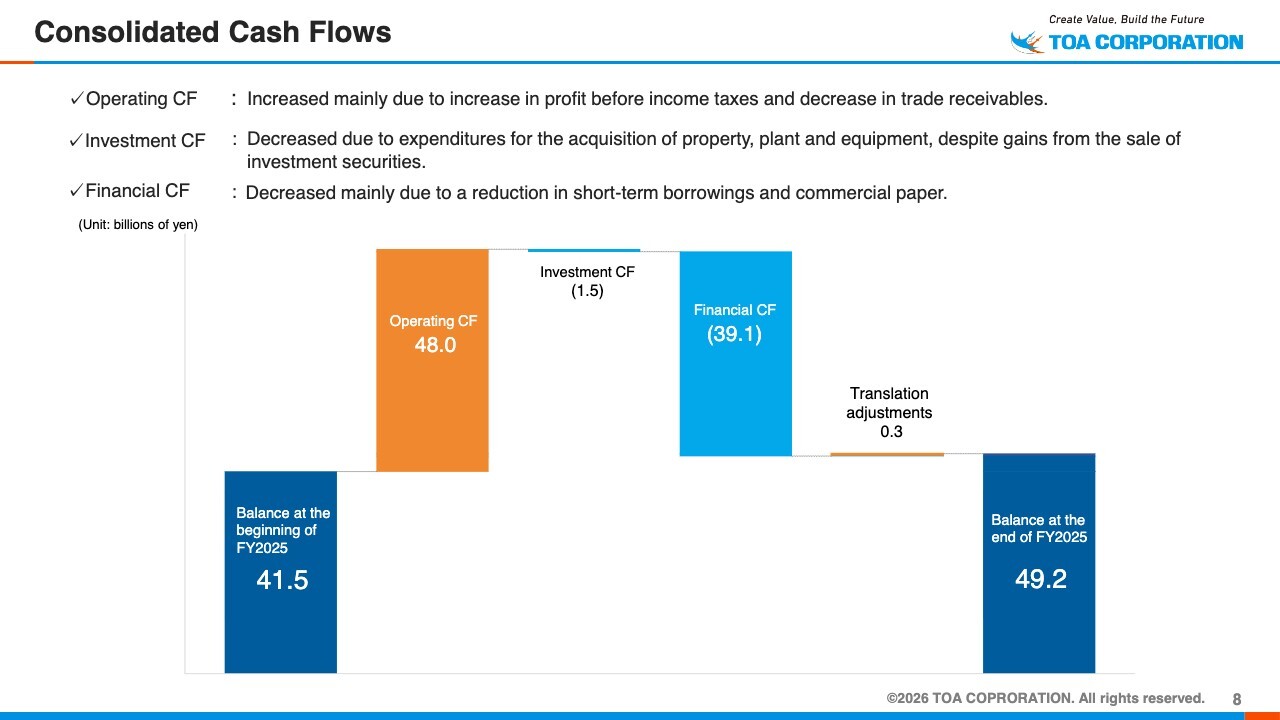

Consolidated Cash Flows

Let me now explain the consolidated cash flows. Operating CF increased by ¥48.0 billion chiefly due to progress in the collection of construction payments, including a decrease in trade receivables and an increase in advances received on uncompleted construction contracts in progress.

Meanwhile, investment CF decreased by ¥1.5 billion, primarily due to expenditures for the acquisition of property, plant and equipment.

Financial CF decreased by ¥39.1 billion due to factors such as repayment of borrowings, dividend payments, and the purchase of treasury shares.

As a result, the balance of cash and cash equivalents increased to ¥49.2 billion at the end of FY2025.

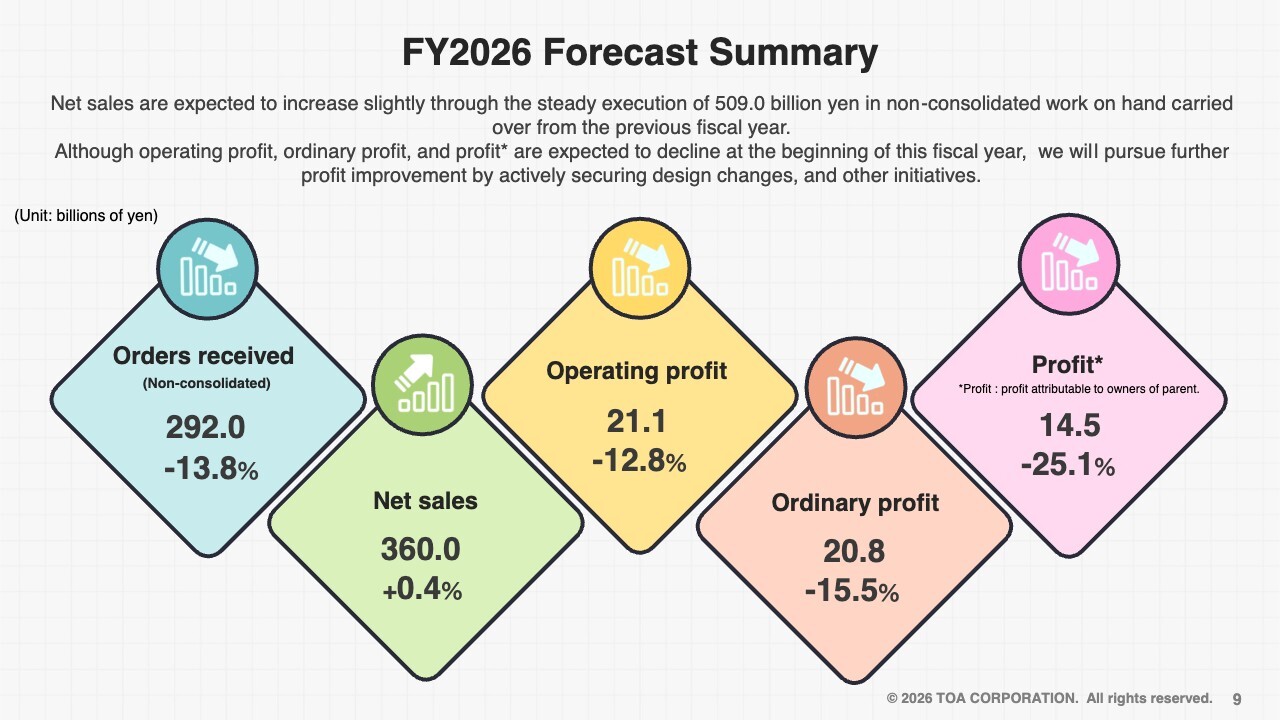

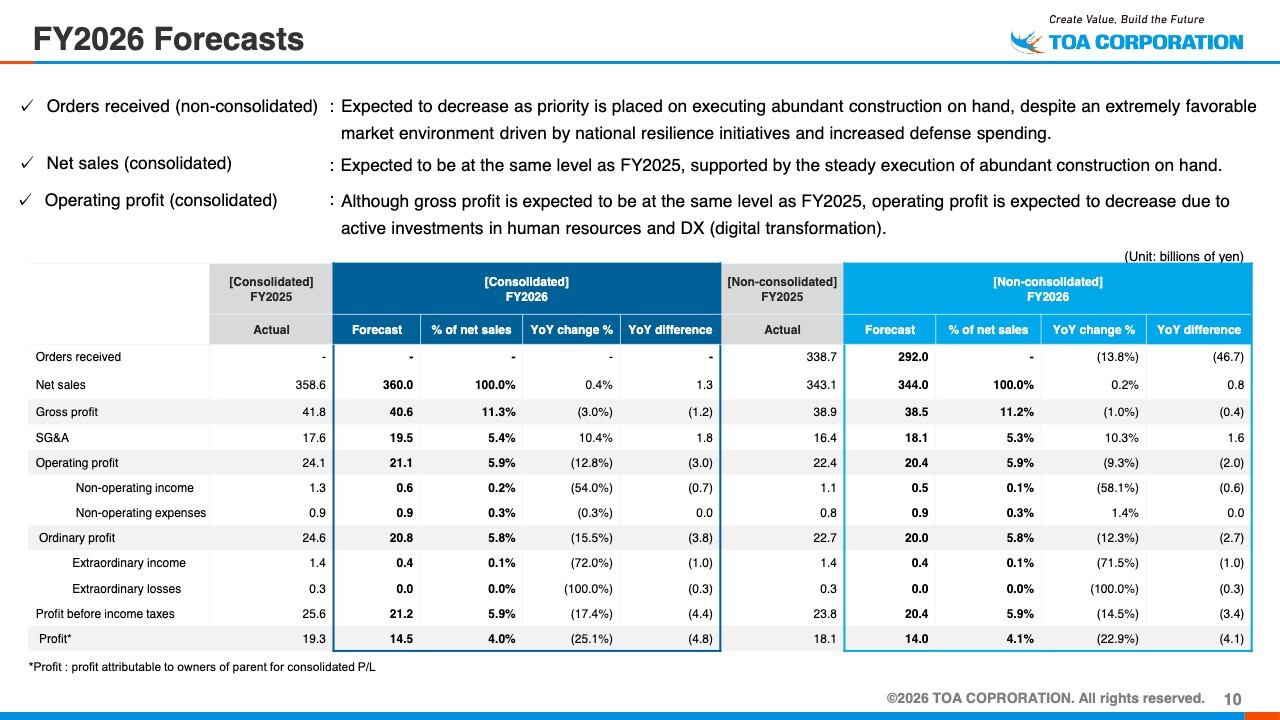

FY2026 Forecast Summary

This is a summary of the full-year FY2026 forecast. Net sales are expected to increase slightly through the steady execution of 509.0 billion yen in work on hand carried over from the previous fiscal year.

Although lower profits are expected at the beginning of this fiscal year, we will work together across the Group to further improve profitability by actively securing design changes and other initiatives.

FY2026 Forecasts

I will now explain the FY2026 forecast. First, non-consolidated orders received are expected to decrease to ¥292.0 billion, as priority will be placed on executing construction on hand.

Consolidated net sales are expected to increase slightly to ¥360.0 billion. Consolidated gross profit is expected to be at the same level as FY2025 at ¥40.6 billion, while consolidated operating profit is expected to decrease to ¥21.1 billion due to active investments in human resources and DX (digital transformation), which are essential for long-term growth.

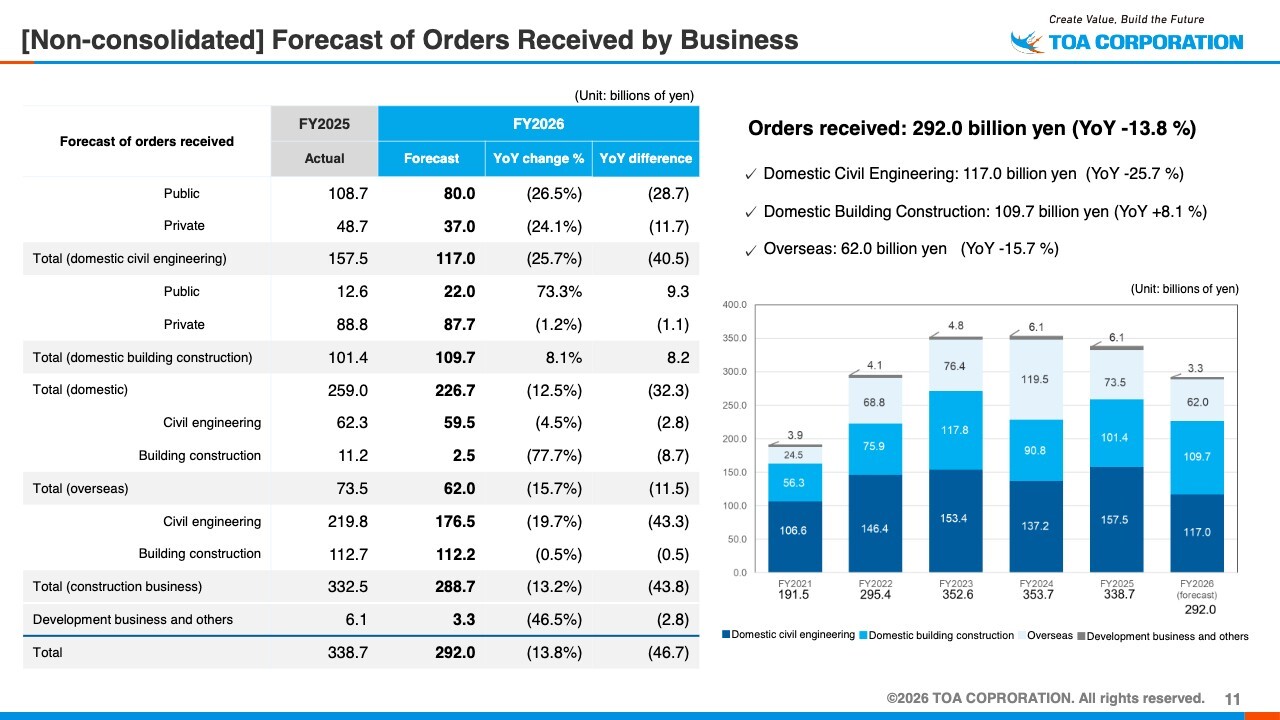

[Non-consolidated] Forecast of Orders Received by Business

Let me now explain the non-consolidated forecast of orders received by business. Although the order environment remains favorable, priority will be placed on executing the abundant construction on hand. With a work on hand carried over from the previous fiscal year totaling ¥509.0 billion, orders received for the current fiscal year are forecast at ¥292.0 billion.

The breakdown consists of ¥117.0 billion in Domestic Civil Engineering, ¥109.7 billion in Domestic Building Construction, and ¥62.0 billion in Overseas.

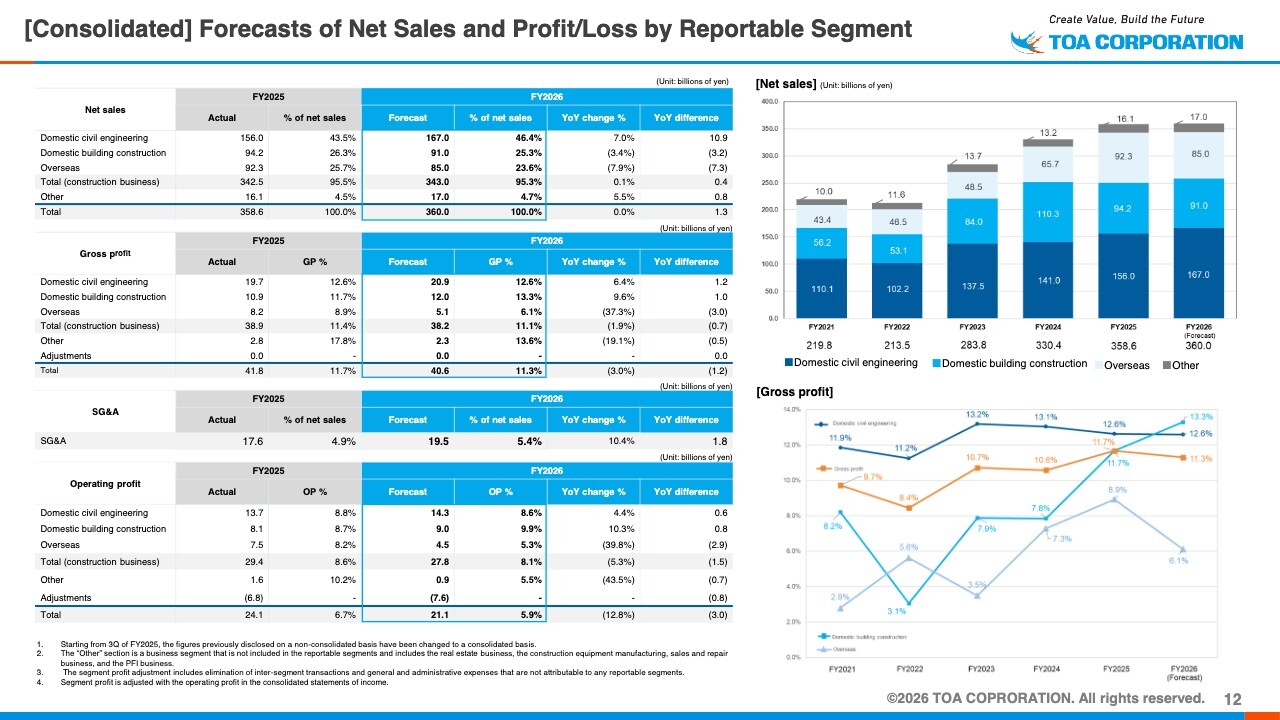

[Consolidated] Forecasts of Net Sales and Profit/Loss by Reportable Segment

Let me now explain the forecasts of net sales and profit/loss by reportable segment. Net sales are expected to total ¥360.0 billion overall, remaining slightly above the previous fiscal year’s level.

Domestic Civil Engineering is expected to increase by 7.0% YoY to ¥167.0 billion, supported by the steady progress of abundant construction on hand.

Domestic Building Construction is expected to decrease by 3.4% YoY to ¥91.0 billion, remaining slightly below the previous fiscal year’s level.

Overseas is expected to decrease by 7.9% YoY to ¥85.0 billion, mainly due to the decline following strong sales from a large-scale port construction project in Africa completed in the previous fiscal year.

Gross profit is expected to total ¥40.6 billion, slightly below the previous fiscal year’s level.

Domestic Civil Engineering is expected to increase by 6.4% YoY to ¥20.9 billion, mainly due to higher net sales.

Domestic Building Construction is expected to increase by 9.6% YoY to ¥12.0 billion, supported by construction projects on hand with favorable profitability at the time of order intake.

Overseas is expected to decrease by 37.3% YoY to ¥5.1 billion, mainly due to the decline following the completion of a large-scale marine civil engineering project in Africa that recorded high profit margins in the previous fiscal year.

Going forward, we will work to further improve profitability in each business segment through the acquisition of design changes.

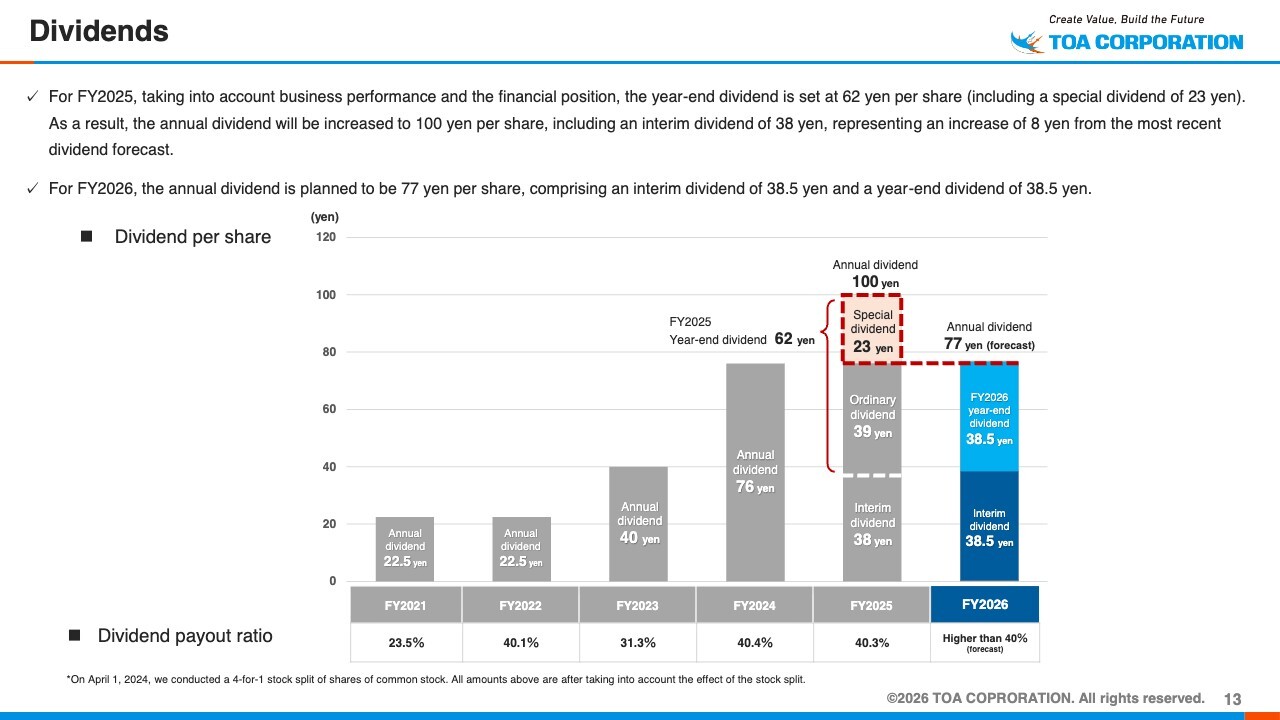

Dividends

Regarding dividends, the year-end dividend for FY2025 will be ¥62 per share, consisting of an ordinary dividend of ¥39 and a special dividend of ¥23, which includes an additional ¥8 over the latest dividend forecast. For FY2026, we plan to pay an annual dividend of ¥77 per share, comprising an interim dividend of ¥38.5 and a year-end dividend of ¥38.5.

To ensure stable dividends, we aim to maintain a payout ratio of 40% or higher, and intend to provide enhanced shareholder returns if profits improve.

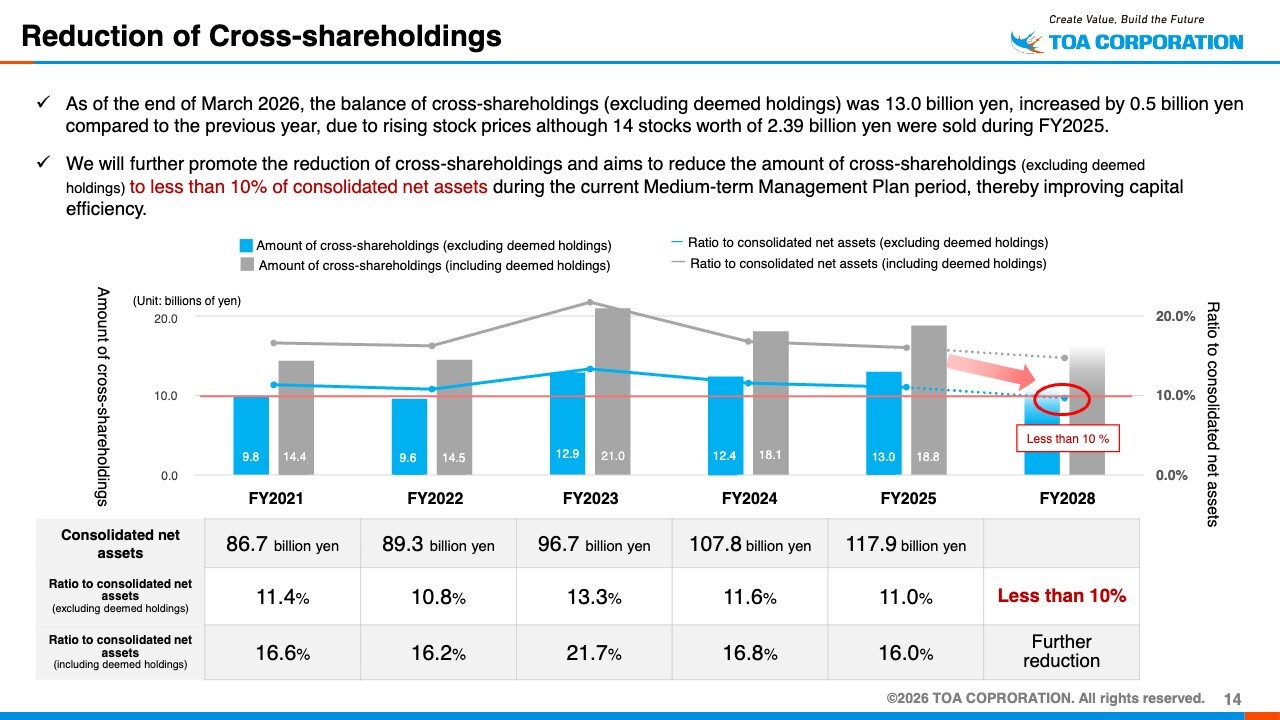

Reduction of Cross-shareholdings

Regarding cross-shareholdings, we have steadily reduced holdings in a planned manner. In the previous fiscal year, we fully sold 11 issues and partially sold three issues; however, due to factors such as rising stock prices, the balance increased by ¥0.5 billion YoY to ¥13.0 billion.

We will continue reducing cross-shareholdings and maintain our target of keeping the ratio to consolidated net assets below 10% during the current Medium-term Management Plan period.

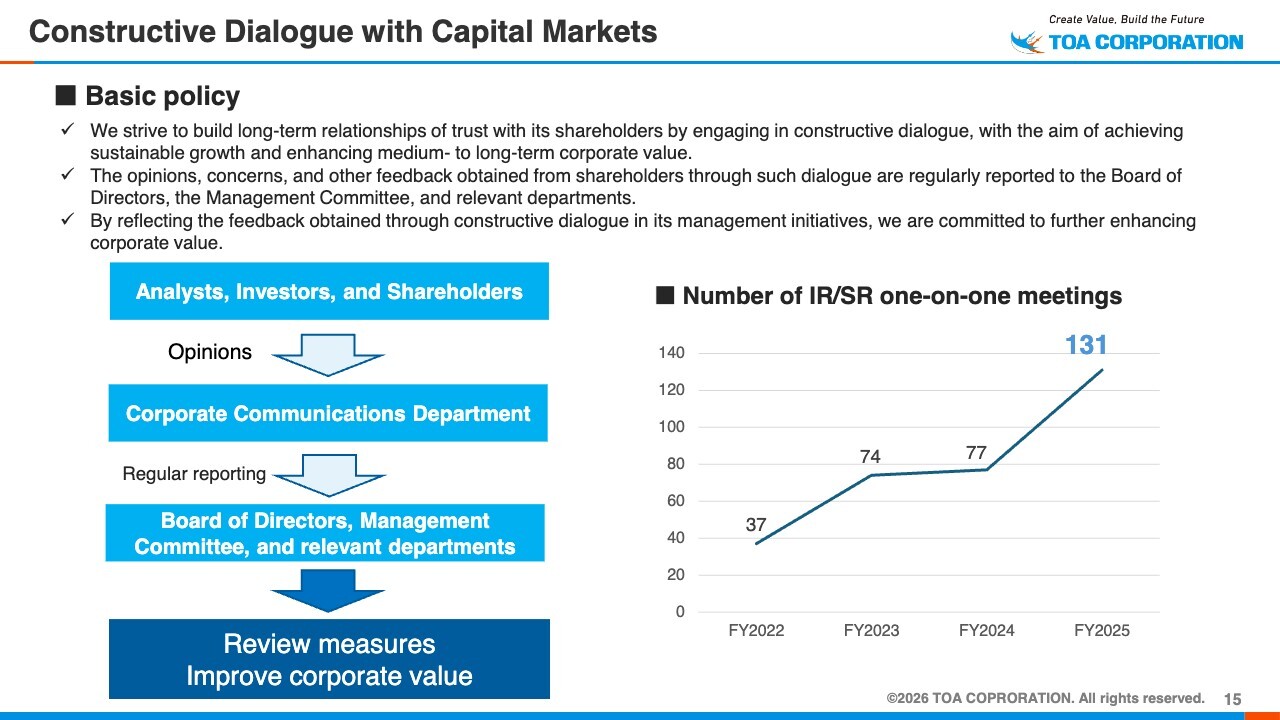

Constructive Dialogue with Capital Markets

Regarding dialogue with the market, we established the Corporate Communications Department with increased IR staffing in the previous fiscal year and conducted 131 meetings with shareholders and investors in FY2025.

We will continue working to enhance corporate value by reflecting opinions obtained through constructive dialogue with capital markets in our management policies.

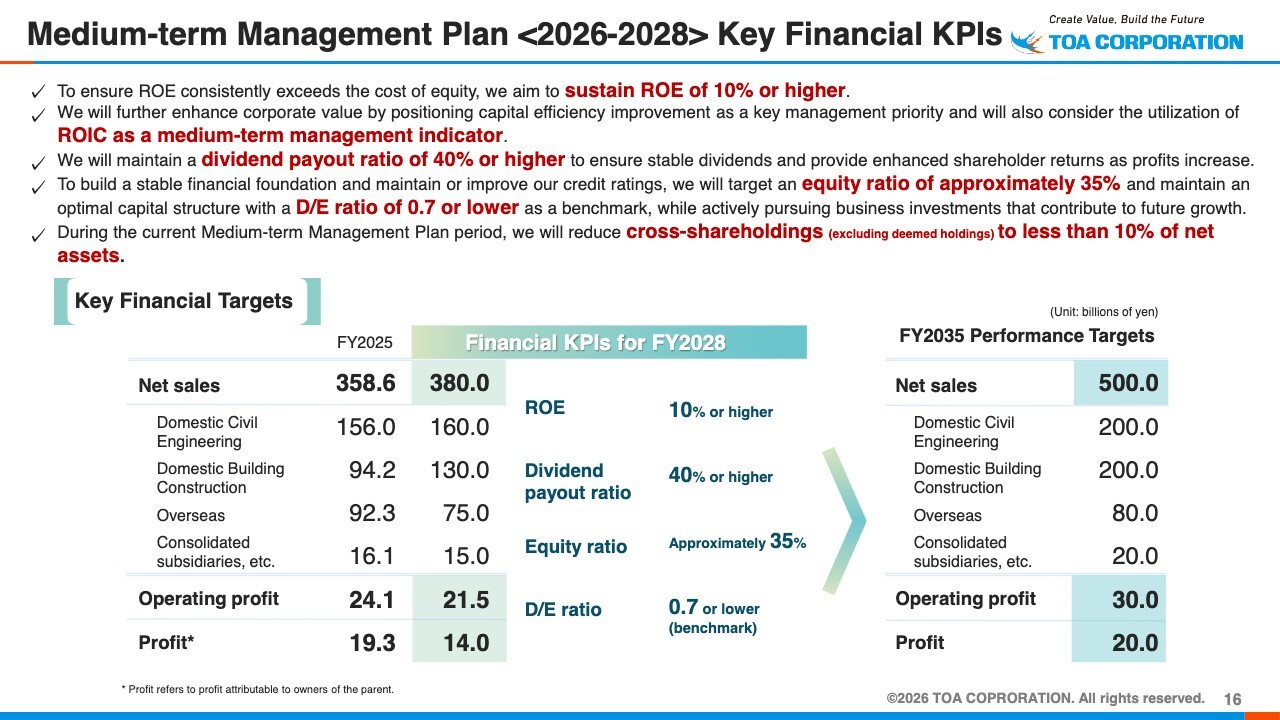

Medium-term Management Plan <2026-2028> Key Financial KPIs

This slide shows the key financial KPIs of the Medium-term Management Plan announced in March. We will maintain ROE at 10% or higher and continue shareholder returns with a payout ratio of 40% or higher.

Regarding share buybacks, we will consider implementing them flexibly as part of shareholder returns, taking into account future business conditions and financial circumstances.

As indicators of financial soundness, we have set a target equity ratio of approximately 35% and a D/E ratio of 0.7 or lower.

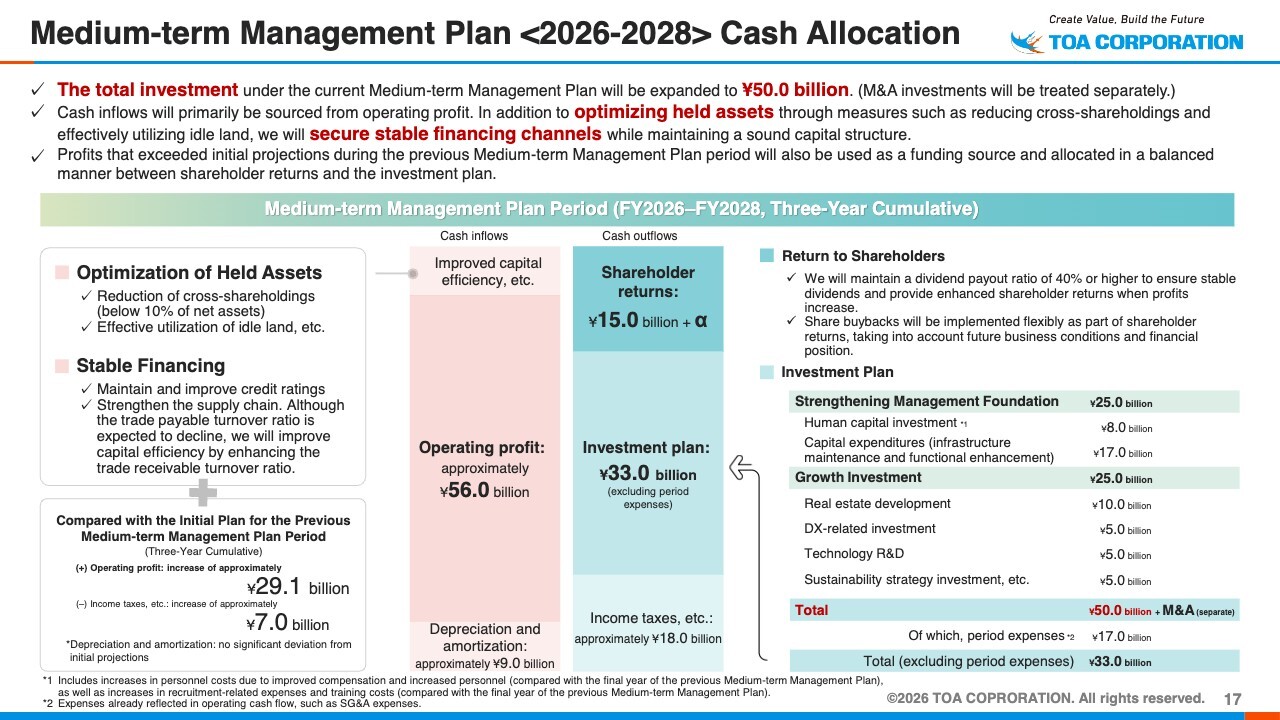

Medium-term Management Plan <2026-2028> Cash Allocation

This slide shows cash allocation under the current Medium-term Management Plan. The total planned investment during the plan period is ¥50.0 billion, consisting of ¥25.0 billion for strengthening the management foundation and ¥25.0 billion for growth investments. M&A investments are positioned separately from this framework.

Cash inflows will primarily be sourced from operating profit. In addition to optimizing held assets through measures such as reducing cross-shareholdings and effectively utilizing idle land, we will secure stable financing channels while maintaining a sound capital structure.

We will also use profits that exceeded initial projections during the previous Medium-term Management Plan period and allocate them in a balanced manner between shareholder returns and the investment plan.

That concludes my presentation.

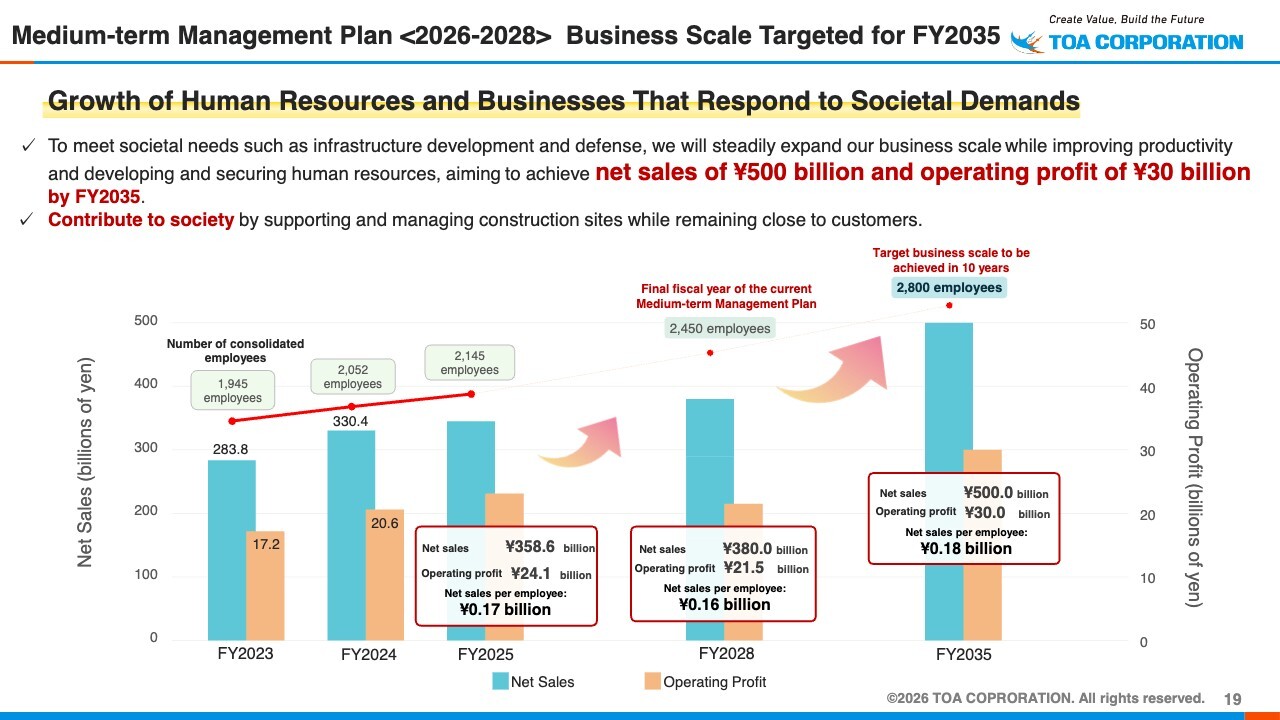

Medium-term Management Plan <2026-2028> Business Scale Targeted for FY2035

Hayakawa: I will now explain the business strategy for medium- to long-term growth. In the Medium-term Management Plan that has already been announced, we have set out the scale of business we aim to achieve by 2035. Although the business environment is such that even looking three years ahead is difficult, we nevertheless set these targets because we believe it is necessary to look ahead to the next 10 years.

We are targeting net sales of ¥500.0 billion and operating profit of ¥30.0 billion.

We are a company centered on construction management, so in order to achieve these targets, we need to steadily increase the number of employees. We aim to build a workforce of approximately 2,800 employees. The current Medium-term Management Plan represents the first three years of our 10-year plan, and in the final year of the plan, we target net sales of ¥380.0 billion, operating profit of ¥21.5 billion, and a workforce of 2,450 employees.

Toward Achieving Net Sales of 500 Billion Yen in FY2035

We have identified five pillars to achieve net sales of ¥500.0 billion.

The first is a focus on the construction business. As this is our core business, we will first work to strengthen it steadily. At the same time, we will expand into new business areas.

The second is talent acquisition and development. This will be a key priority. I will explain this in more detail later, including our workforce composition.

Third, we will enhance collaboration with partner companies to strengthen construction capabilities.

The fourth is strengthening pricing power. Amid growing labor shortages, we are now able to be more selective in accepting orders in certain areas, and we intend to leverage our strengths to further enhance pricing power.

The fifth is improving productivity and pursuing economies of scale. Although this is a continuation of our existing efforts, we intend to continue working on these initiatives steadily.

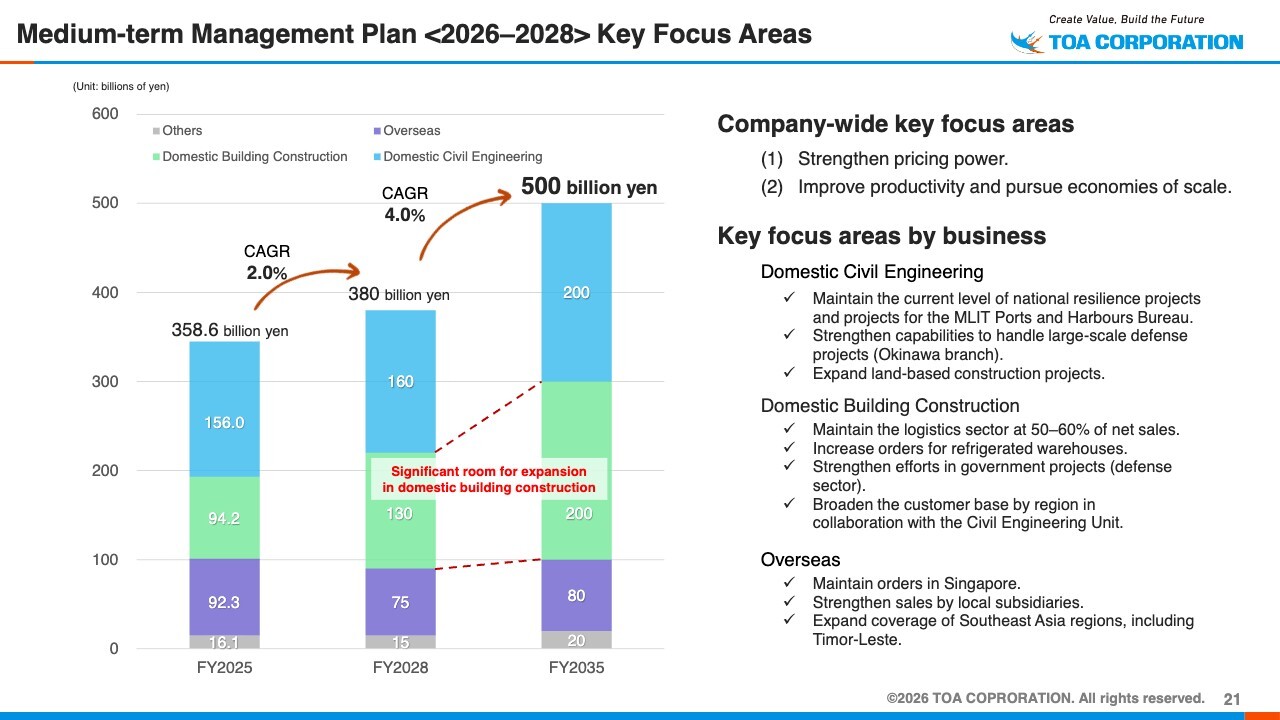

Medium-term Management Plan <2026-2028> Key Focus Areas

The graph on this slide illustrates the key areas to focus on in the Medium-term Management Plan covering the period from FY2026 to FY2028.

The far-right side of the graph shows the targets for FY2035. The breakdown of the ¥500.0 billion net sales target consists of ¥200.0 billion in Domestic Civil Engineering, ¥200.0 billion in Domestic Building Construction, and ¥80.0 billion in Overseas.

Compared with the FY2025 level, we plan to significantly increase Domestic Building Construction to nearly double its current size. Achieving net sales of ¥130.0 billion in FY2028 is positioned as a key milestone on the way toward our FY2035 target of ¥200.0 billion.

On the right side of the slide, the key focus areas for Domestic Civil Engineering, Domestic Building Construction, and Overseas are summarized in bullet points, which I will explain later.

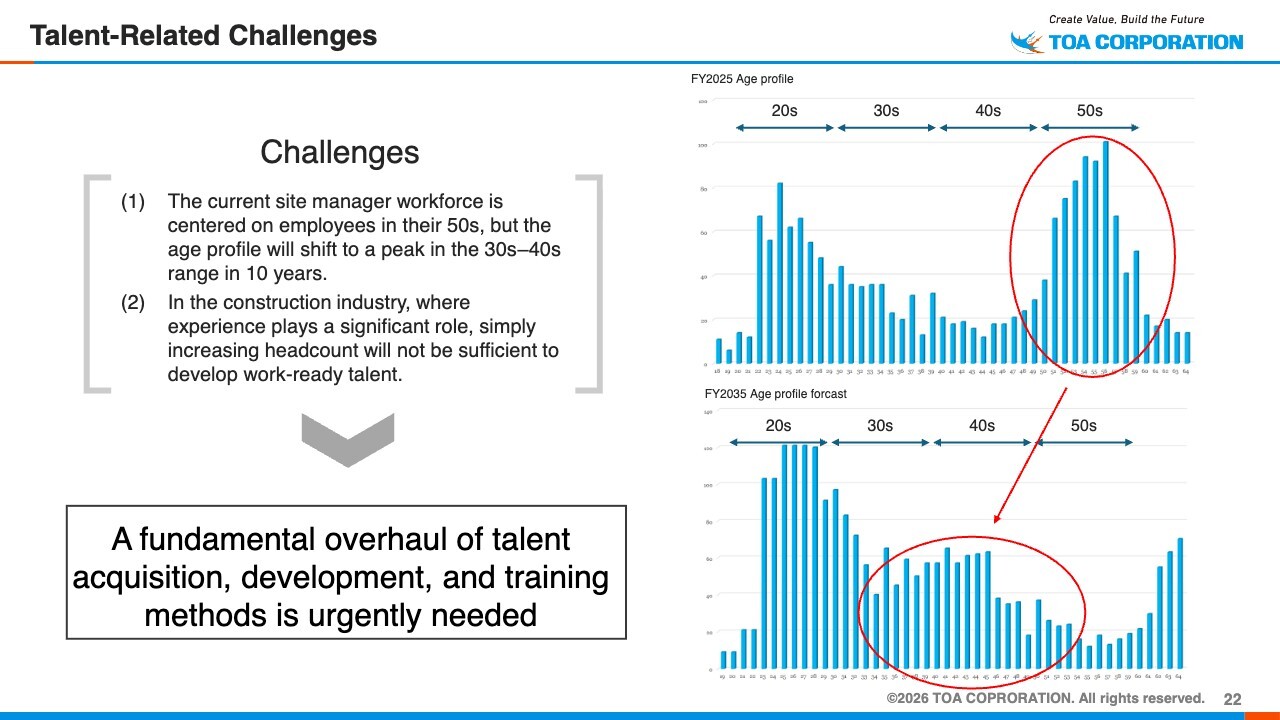

Talent-Related Challenges

This slide covers talent-related challenges. Our current workforce age profile is shown in the graph at the upper right of the slide.

The graph ranges from age 18 on the left to age 65 on the right, showing a workforce structure with a particularly large number of employees in their 50s and very few in their 40s. We believe this trend is common across many construction companies. In recent years, we have focused on recruiting employees in their 20s and 30s, and have been able to secure a certain level of personnel.

The graph at the lower right of the slide shows our workforce profile 10 years from now, assuming a certain level of hiring based on the current recruitment plan.

In this scenario, the number of employees in their 30s and 40s would increase, while the proportion of employees in their 20s would also become larger. In a sense, the workforce structure would become somewhat closer to a pyramid shape. One issue that would arise under such circumstances is that, as mentioned earlier, the age profile will shift to a peak in the 30s–40s range in 10 years.

Our construction business is often described as being highly dependent on experience-based expertise, making it difficult to develop employees into fully effective contributors simply by increasing hiring. Therefore, we believe it is urgently necessary not only to recruit talent, but also to fundamentally review our approaches to training and education thereafter.

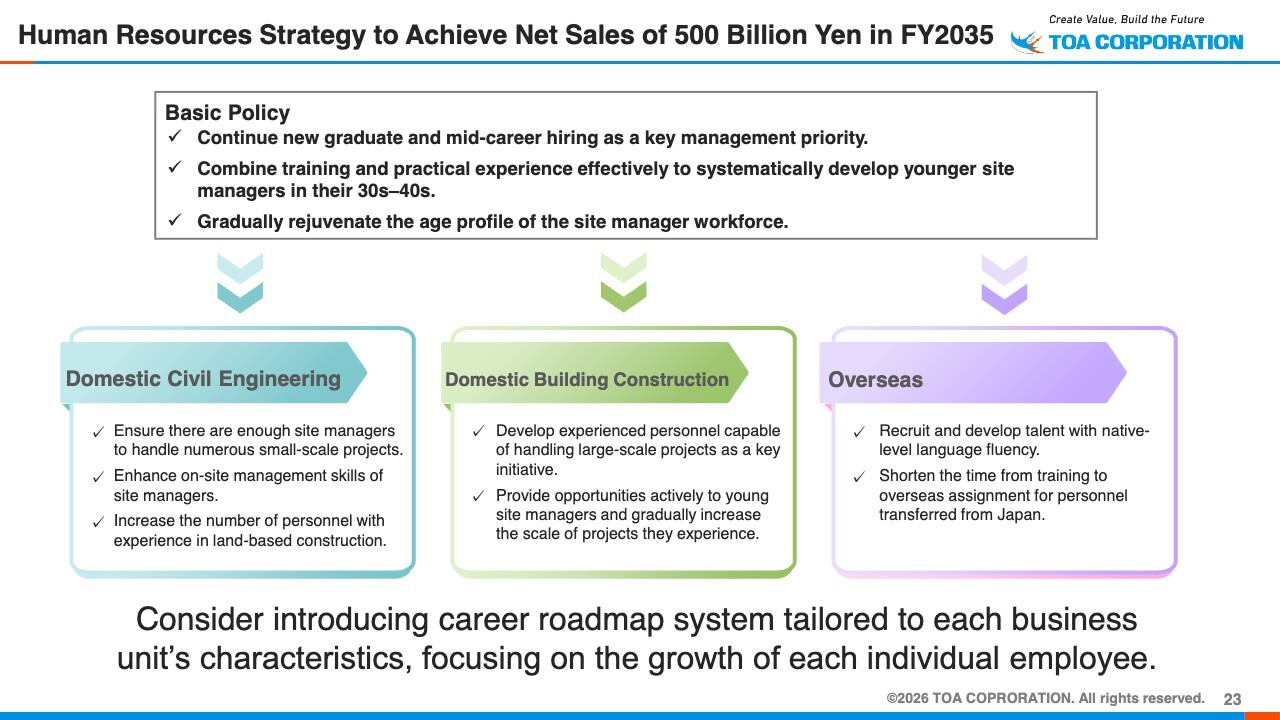

Human Resources Strategy to Achieve Net Sales of 500 Billion Yen in FY2035

We have established a human resources strategy to achieve net sales of ¥500.0 billion in FY2035. Our basic policies are to continue prioritizing new graduate and mid-career hiring as a key management priority, to combine training and practical experience effectively to systematically develop younger site managers in their 30s-40s, and to gradually rejuvenate the age profile of the site manager workforce.

We have three core business segments—Domestic Civil Engineering, Domestic Building Construction, and Overseas—but the background factors underlying the human resources strategy for each segment differ.

As a result, the strategies we adopt also differ, and I would like to briefly explain those differences.

First, regarding Domestic Civil Engineering, we specialize in public-sector construction projects, particularly marine civil engineering projects. On average, the scale of each project is in the ¥300 million range, so securing a sufficient number of site managers is essential in order to handle numerous small-scale projects. In addition, we aim to further enhance the on-site management skills of site managers while also increasing the number of personnel with experience in land-based construction projects.

Next, regarding Domestic Building Construction, in order to increase net sales to ¥200.0 billion over the next 10 years, we aim to maintain approximately a 50% share in logistics-related projects. To achieve this, we will need the capability to handle multiple large-scale projects exceeding ¥10.0 billion. Accordingly, the most important challenge will be developing experienced personnel capable of handling large-scale projects. We therefore plan to adopt a development approach that actively provides opportunities to young site managers while gradually increasing the scale of projects they experience.

Meanwhile, in Overseas, our traditional approach has been to dispatch personnel from Japan to overseas operations, and we will continue this approach. However, developing personnel under this approach requires time, and working with approximately 10 local national staff members at overseas sites also requires a certain level of experience. As a countermeasure, we believe that recruiting and developing talent with native-level language fluency will become an important challenge going forward.

In addition, we aim to shorten the time from training to overseas assignment for personnel transferred from Japan, while also considering training programs conducted locally at overseas sites.

In this way, taking into account the characteristics of each business segment, we plan to introduce a career roadmap system to support the growth of each individual employee, as shown at the bottom of the slide.

As a company, we consider the path through which we would like our employees to grow, while at the same time recognizing that each employee also has their own individual aspirations and perspectives. By aligning these perspectives, we aim to support each employee in proactively building their own career and encourage their continued growth.

Strengthening Collaboration with Partner Companies

The schematic on the left side of the slide illustrates the strengthening of collaboration with partner companies. We will promote collaboration in recruitment activities, training and education, and support to reduce management burden; however, we believe that the most important issue will be education.

In terms of collaboration in training and education, we believe that we should provide sufficient opportunities at our own expense not only to our employees but also to personnel at partner companies within our supply chain. In addition, we would like to work together on technical exchanges, sharing of know-how, and various compliance-related training programs.

In the collaboration in recruitment activities described below, we will work to address challenges across the entire supply chain. For example, when visiting schools, our company and partner companies will conduct visits together in order to help students understand the diverse roles within the construction industry, including both construction management roles and people involved in construction. Through these efforts, we plan to promote joint recruitment activities with partner companies while helping students recognize both the diversity of the construction industry and its broad scope.

Finally, regarding the support to reduce management burden shown at the lower right of the slide, we plan to shift all payments for new outsourcing contracts to full cash settlement during 1H FY2026.

Through these initiatives, we aim to support the reduction of management burdens.

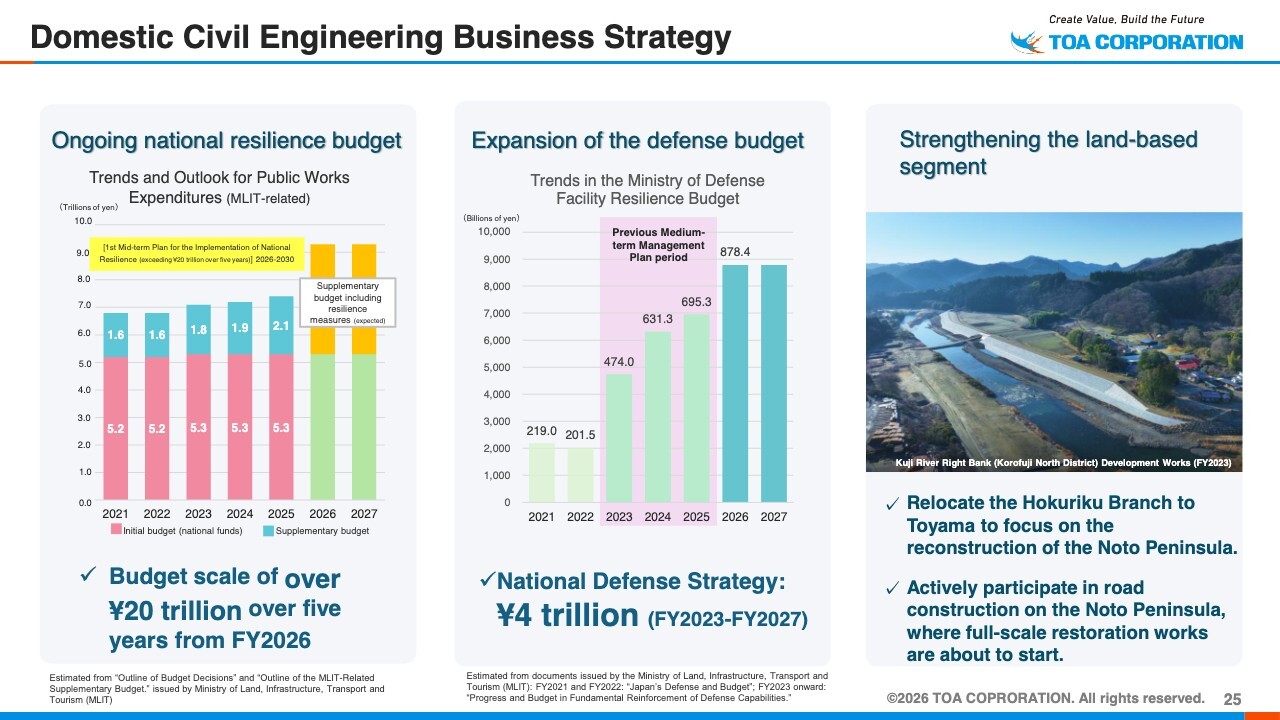

Domestic Civil Engineering Business Strategy

Next, I will explain the strategies for each business segment. First, regarding Domestic Civil Engineering, the national resilience budget shown on the left side of the slide has continued for the past several years. As indicated at the lower left of the slide, the budget scale for the five years beginning in FY2026 is expected to exceed ¥20 trillion.

Disaster prevention and mitigation are extremely important national issues, and budgets for national resilience have been allocated accordingly. As in the past, we intend to continue making steady efforts to secure projects and win orders.

Next, regarding the expansion of the defense budget shown in the center of the slide, the defense budget covers a wide range of uses. Among these, one area related to our business is the Ministry of Defense’s budget for strengthening facility resilience.

Currently, under the National Defense Strategy, budget allocations totaling ¥4 trillion are planned for the period from FY2023 to FY2027. These include projects such as the optimization of military bases, and we intend to actively pursue these opportunities as well.

Regarding the strengthening of the land-based segment shown on the right side of the slide, our growth has historically focused on marine civil engineering projects, but we recognize the need to actively engage in land-based construction as well. The photo shows the riverbank protection work at the Kuji River.

Regarding the reconstruction of the Noto Peninsula, we are currently involved in port restoration work. As for road construction, full-scale restoration work is expected to begin in the future, and in preparation for this, we relocated our Hokuriku Branch to Toyama.

We intend to actively participate in road construction projects as well, supporting sites from locations close to the Noto Peninsula in order to ensure the steady execution and completion of construction work.

Domestic Building Construction Business Strategy

Next, regarding the Domestic Building Construction Business Strategy, I will first explain the continued focus on the logistics sector shown on the left side of the slide.

Amid increasingly diverse needs, we are also seeing inquiries for large-scale multi-tenant projects. Even as net sales ultimately expand to the ¥200.0 billion level, we aim to maintain the logistics sector at 50% to 60% of total sales and maximize economies of scale to contribute to profitability.

Next, as shown in the center of the slide, we are promoting efforts to capture the replacement demand for refrigerated warehouses. We have strong expertise in this field. Among the various types of demand, there are also requests for the conversion of some existing dry warehouses into refrigerated warehouses.

Last fiscal year, we established a Group company specializing in renovation projects. By collaborating with this company, we aim to respond to replacement demand for refrigerated warehouses.

Regarding the strengthening of capabilities for government and public-sector construction projects shown on the right side of the slide, our business has historically focused primarily on the private sector. Within this area, we have also built a track record of engaging in projects such as PFIs from a relatively early stage.

We have established a new Social and Public Business Development Department as part of our public infrastructure functions. We intend to further strengthen our efforts in government and public-sector construction projects. We also aim to secure orders for optimization projects at Japan Self-Defense Forces bases mentioned earlier.

Overseas Business Strategy

Next, I will explain the overseas business strategy. First is maintaining order intake in Singapore.

Our company first expanded overseas in 1963. Singapore was the first country we entered, and we have continuously built a track record in large-scale projects there. Leveraging the design-build expertise we have cultivated over the years, we will continue working to secure a steady pipeline of projects on an ongoing basis.

I would also like to discuss strengthening order acquisition through local subsidiaries, as shown in the center of the slide. Until now, our business has primarily focused on Official Development Assistance (ODA) projects. However, as Southeast Asian countries have continued to develop, the number of ODA projects has been decreasing. Accordingly, we believe it is important to establish local subsidiaries and build a framework capable of securing projects directly from local governments.

As part of these efforts, following Indonesia, we also established a local subsidiary in the Philippines. Although operations will begin on a relatively small scale, we will work to strengthen order acquisition and construction frameworks for non-ODA projects as well.

Let me introduce emerging opportunities shown on the right side of the slide. There is a country in Southeast Asia called Timor-Leste. It gained independence from Indonesia and joined ASEAN in 2025.

We secured an international airport development project in this country. With the ASEAN Summit scheduled to be held there in 2029, we believe it is highly significant that we were able to win the contract for the airport project, which will serve as the gateway to the country.

Using this project as a foothold, we also aim to secure orders for marine port construction projects , which are one of our core strengths.

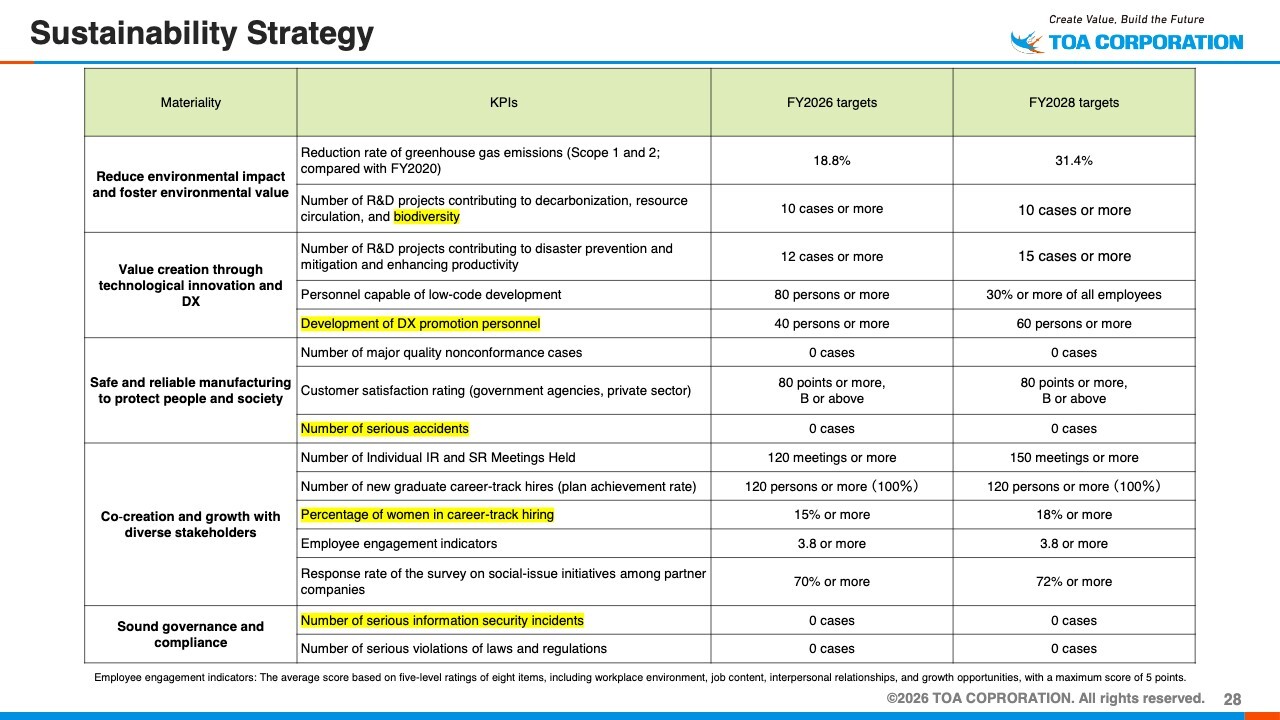

Sustainability Strategy

Let me now explain our sustainability strategy. We have established a very large number of KPIs; however, going forward, we intend to narrow them down to some extent and address them with clearer priorities and focus.

Regarding the materiality shown on the far left of the slide, the first item is “reducing environmental impact and fostering environmental value.” We have established a variety of targets within this category, and we believe biodiversity will become an especially important keyword going forward.

Regarding “value creation through technological innovation and DX,” although DX will not progress all at once, it has been steadily gaining traction. To further accelerate this trend, we intend to focus on developing personnel capable of driving DX initiatives.

As for “safe and reliable manufacturing to protect people and society,” preventing serious accidents is our highest priority above all else. We will position this as our top management focus and work toward achieving zero serious accidents.

As for “co-creation and growth with diverse stakeholders,” we have established a variety of initiatives. We would like to further promote the active participation of women. Currently, women account for only around 10% of new hires, and we intend to increase this ratio while creating an environment in which women can play a more active role.

“Sound governance and compliance” are essential to corporate management. In light of the various information security incidents that have occurred in recent years, we are committed to implementing a range of measures to ensure that such incidents never occur within our company.

That concludes my presentation.

Q&A Session: Order Plan for Domestic Civil Engineering

Questioner: I have a question about the order plan. In Domestic Civil Engineering, orders received are expected to decline YoY in the current fiscal year. Should this be viewed as the minimum level? Also, if there are projects with exceptionally high profitability, could orders received potentially exceed the current forecast?

Hayakawa: As noted in the comments in the financial results presentation materials, the decline in orders reflects our priority on steadily executing projects already on hand, taking into account our current construction capabilities.

At present, from the standpoint that orders should not be expanded excessively, the figure is projected to decline; however, construction volume is expected to exceed the previous fiscal year’s level. In addition, because individual projects tend to be large in scale, please understand that orders received will not necessarily remain consistent every year.

Q&A Session: Profitability at Order Intake in Domestic Building Construction and the Impact of the Situation in the Middle East

Questioner: I have a question about Domestic Building Construction. Profit margins have been improving. First, could you comment on recent trends in profitability at the time of order intake?

In addition, I would appreciate it if you could explain the extent to which the impact of the situation in the Middle East has been factored into the plan, as well as how much of the expected benefits from design changes have been incorporated into the initial plan for the fiscal year.

Hayakawa: Turning to profitability at the time of order intake in Domestic Building Construction, amid the current labor shortages, we are now in a position to be more selective in order intake to a certain extent. In private-sector projects as well, we have steadily explained the need for price pass-through to clients, and this has gradually led to greater acceptance of such measures. As a result, profitability at the time of order intake has been improving year by year.

Regarding the situation in the Middle East, there are concerns that the supply of petroleum-related products could be disrupted; however, we currently do not expect any impact on construction projects in this fiscal year.

However, as prices for petroleum-related products have been gradually rising, we expect costs for construction projects in the next fiscal year to increase. In that context, we believe the key challenge will be the extent to which clients accept price revisions.

Specifically, we expect prices to increase by approximately 3% for large-scale logistics facilities, around 4% for housing projects, and about 5% for refrigerated warehouses, where the proportion of equipment-related work is higher and which is one of our core strengths.

Q&A Session: Plan for Gross Profit Margin

Questioner: My question concerns the plan for the gross profit margin in Domestic Civil Engineering remaining flat. Considering the impact of the provision, my understanding is that the margin is declining in substance. Should this be interpreted as being due to differences in project mix, or because no additional design changes have been factored in at the beginning of the fiscal year? I would like to understand how we should view the actual situation.

Hayakawa: In Domestic Civil Engineering, our projections are based on the initial profit assumptions. In some cases, issues related to design changes arise due to discrepancies in conditions at individual construction sites, and we believe these could contribute some additional profit.

However, since each project has different characteristics, the reality is that we cannot determine the exact outcome until construction begins. Basically, we believe it is necessary to aim for profit margins in line with the usual annual level.

Q&A Session: M&A Strategies

Questioner: My question concerns M&A. At present, marine civil engineering companies are becoming involved in M&A activities in various ways as acquisition targets. I would like to ask how your company intends to respond to this situation.

Improving performance and increasing market capitalization would be the best approach. However, at present, the plan appears somewhat conservative, and market capitalization has also declined, which gives the impression of moving in the opposite direction. Could you explain how you view the risk of your company itself becoming an acquisition target?

Hayakawa: Turning to M&A, there have certainly been various cases involving marine civil engineering contractors. Regarding the risk of becoming an acquisition target, we believe that taking an aggressive stance by steadily expanding our business scale is itself the strongest form of defense.

The question then becomes which areas represent growth opportunities, and for us, the building construction business is particularly important. Rather than focusing solely on the marine civil engineering contracting business or overseas business, we intend to achieve corporate growth by maintaining a well-balanced business portfolio.

We believe this approach will help reduce the risk of becoming an acquisition target. We would like you to understand that these considerations have been incorporated into our Medium-term Management Plan, which has been formulated with a view toward the next 10 years.

Questioner: How about from the perspective of being an acquirer?

Hayakawa: From the perspective of being an acquirer, there are various potential targets. Currently, labor shortages are becoming increasingly severe; however, the reality is that it is difficult to find companies willing to respond in a way that directly addresses the objective of securing personnel. Nevertheless, we intend to continue gathering information and keep a close watch on potential opportunities at all times.

We are a company with a nationwide presence. Therefore, we are considering multiple options, such as finding companies that are capable of operating nationwide or pursuing M&A with suitable companies in each region. We will carefully move forward while thoroughly considering these options. We are not ruling out any possibilities. That is all.

Q&A Session: Construction Cost Increases Due to the Situation in the Middle East and the Possibility of Price Pass-Through

Questioner: I would like to confirm one point regarding your earlier response. You mentioned that the situation in the Middle East could lead to increases of approximately 3% for warehouses and 4% for housing projects in the next fiscal year. Does this mean that you expect overall construction costs to rise by those amounts?

If costs rise to that extent, I would expect a corresponding impact on profit margins as well. Could you elaborate, including with reference to the slide and other materials, on whether you believe it will be possible to pass through these cost increases?

Hayakawa: The factors driving these increases include finishing work, exterior work, electrical work, and, particularly for refrigerated warehouses, thermal insulation work, all of which are highly affected by rising prices. Accordingly, these figures were calculated by applying estimated increase rates based on the composition of construction work in past projects.

We believe it is essential for us to carefully explain these cost increases to clients so that they can be appropriately reflected in prices. If we are unable to do so, those additional costs will naturally have to be absorbed, resulting in lower profits. Therefore, we believe this ultimately depends on our own efforts.