Full-Year Results for FY2026/3 and Future Management Policies

Motoaki Tanigo (hereinafter “Tanigo”): I am Motoaki Tanigo, President and CEO. Thank you for taking the time today to join our financial results briefing.

Today, I will begin with an overview of our full-year business performance for FY2026/3, then discuss the current status of our efforts to strengthen our growth foundations, and finally cover the progress of structural reforms to our management foundation.

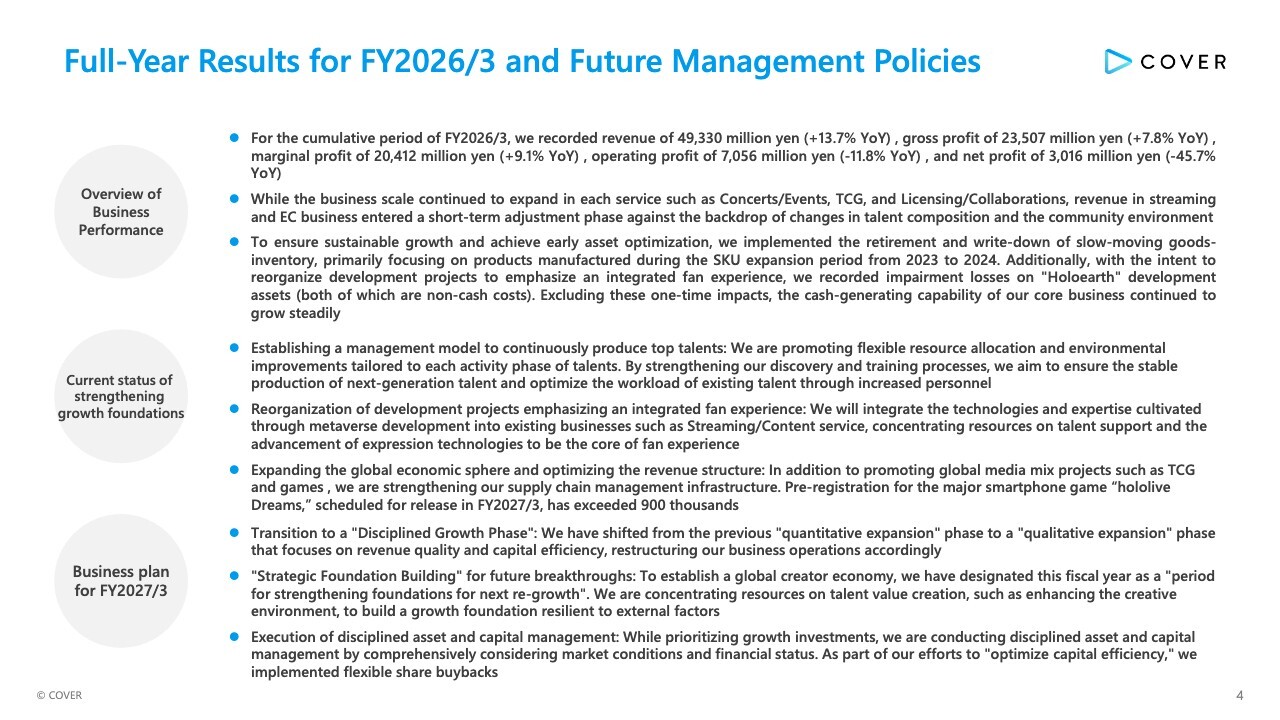

For the full year of FY2026/3, we recorded revenue of approximately 49.3 billion yen, operating profit of approximately 7.0 billion yen, and net profit of approximately 3.0 billion yen. While revenue increased 13.7% YoY, the results fell short of the initial forecast set at the beginning of the fiscal year.

While the business scale continued to expand in each service such as Concerts/Events, Trading Card Games (TCG), and Licensing/Collaborations, revenues from streaming and e-commerce have entered a short-term adjustment phase against the backdrop of changes in talent composition, the community environment, and the impact of tariffs in North America.

Profits declined YoY as we recorded one-time non-cash costs, such as the retirement and write-down of slow-moving inventory and impairment losses on “Holoearth” development assets. However, excluding these items, the cash-generating capability of our core business continues to grow steadily.

Next, I will explain the current status of our efforts to strengthen the growth foundation, as shown in the middle section of the slide. First, we are establishing a management model to continuously produce top talents. We are promoting flexible resource allocation and environmental improvements tailored to each talent’s activity phase. By strengthening our discovery and training processes, we aim to ensure the stable development of next-generation talents and optimize the workload of existing talents through increased personnel.

Second, we are working on the reorganization of development projects emphasizing an integrated fan experience. We will integrate the technologies and expertise cultivated through metaverse development into existing businesses such as Streaming/Content service, concentrating resources on talent support and the advancement of expression technologies, which form the core of the fan experience.

Third, we are expanding the global economic sphere and optimizing the revenue structure. Through the promotion of global media mix projects via TCG and game expansion, we aim to increase brand touchpoints for potential fans. Pre-registrations for the major smartphone game “hololive Dreams,” scheduled for release in this fiscal year, have exceeded 900,000, and we expect it to become a new pillar of revenue.

At the same time, we will optimize supply chain management to improve procurement and other costs, and enhance services for fans both at home and abroad.

Finally, I will discuss our business plan for FY2027/3. We have shifted from the previous quantitative expansion phase to a disciplined growth phase aiming for qualitative expansion focused on revenue quality and capital efficiency, restructuring our business operations accordingly.

We position this fiscal year as a period of strategic foundation building for future breakthroughs. We are concentrating resources on talent value creation, such as enhancing the creative environment, to build a robust growth foundation resilient to external factors.

At the same time, while prioritizing growth investments, we are conducting disciplined asset and capital management by comprehensively considering market conditions and financial status. Against this backdrop, today on May 14, we announced the implementation of a flexible share buyback program.

We take our current challenges seriously and will continue to strive to rebuild our business foundation and enhance sustainable corporate value.

Financial Highlights |Summary for FY2026/3

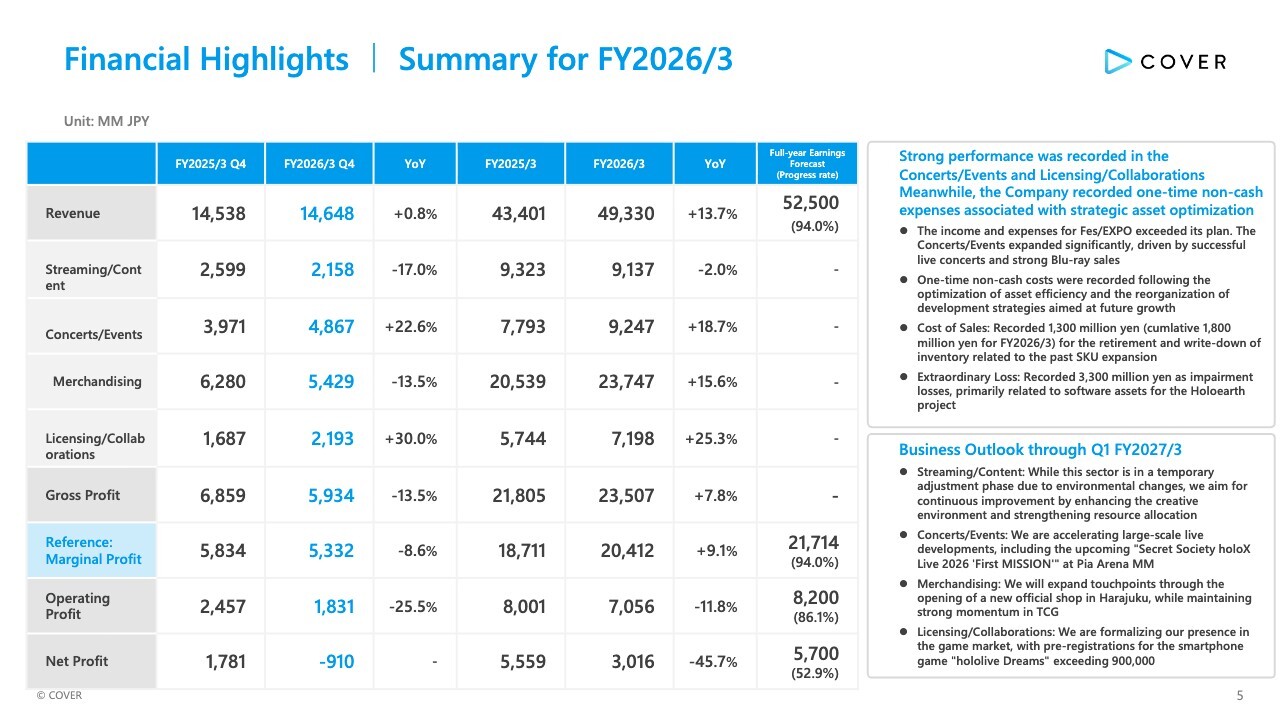

Here are the financial highlights. Our full-year results are as I outlined earlier and shown in the table on the left side of the slide.

For Q4, the results for the large-scale Fes/EXPO exceeded the plan. The Concerts/Events sector expanded steadily, driven partly by strong Blu-ray sales. The Licensing/Collaborations sector has also continued to perform well.

On the other hand, we recorded one-time non-cash costs in Q4 as a result of strategic asset rationalization and the reorganization of our development strategy aimed at future growth. Specifically, we recorded 1,300 million yen for the retirement and write-down of inventory related to the past SKU expansion, and an additional 3,300 million yen in extraordinary losses as impairment losses, primarily related to software assets for the Holoearth project.

Now I will explain the business outlook through Q1 FY2027/3, which is shown in the bottom right of the slide. While the Streaming/Content sector is in a temporary adjustment phase due to environmental changes, we aim for continuous improvement by enhancing the creative environment and strengthening resource allocation.

In the Concerts/Events sector, we are accelerating large-scale live developments, including “Secret Society holoX Live 2026 ‘First MISSION’” at Pia Arena MM.

In the Merchandising sector, we will expand touchpoints with fans through the opening of a new official shop in Harajuku, while maintaining strong momentum in TCG.

Finally, in the Licensing/Collaborations sector, we will fully establish our presence in the game market by advancing preparations for major projects in the pipeline, such as the smartphone game “hololive Dreams” whose pre-registrations have exceeded 900,000.

Historical Trends in Revenue and Gross Profit

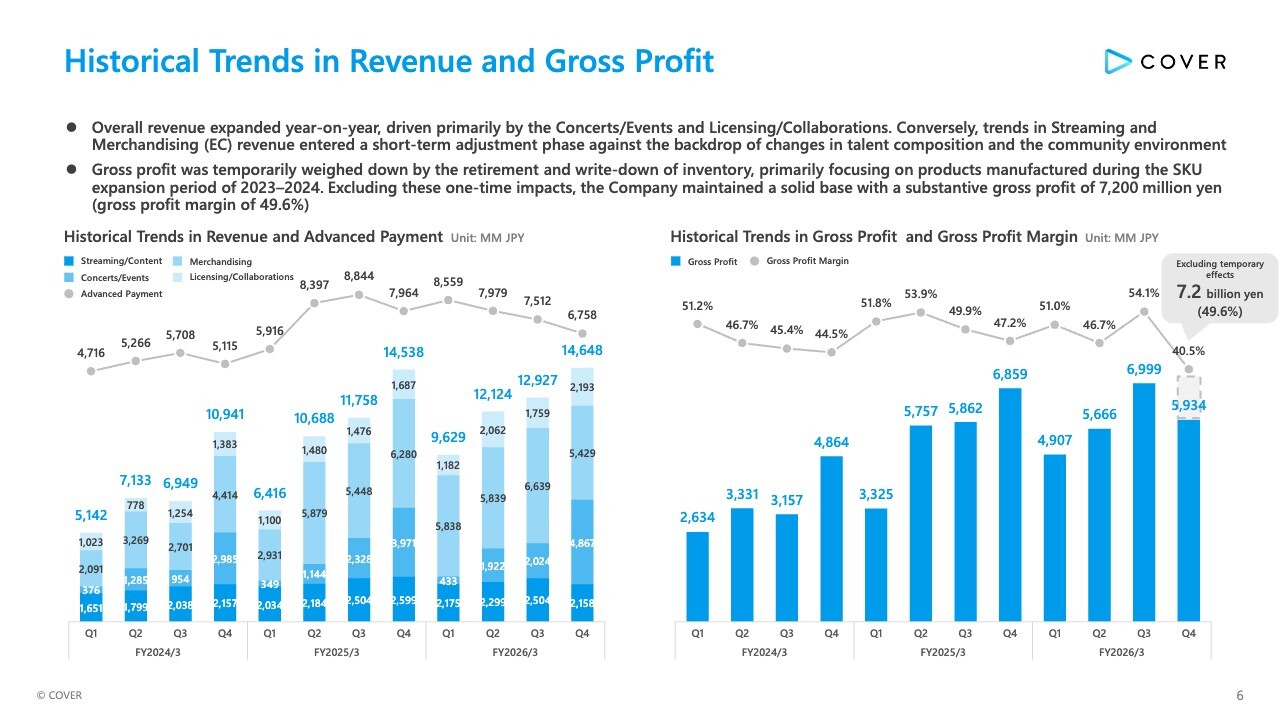

Here is the quarterly trend in revenue and gross profit. Revenue for Q4 was 14.6 billion yen. Overall, revenue continued to grow YoY, driven by the Concerts/Events and Licensing/Collaborations sectors.

Conversely, trends in Streaming and Merchandising (EC) revenue entered a short-term adjustment phase against the backdrop of changes in talent composition and the community environment.

Gross profit for Q4 was 5.9 billion yen, with a gross profit margin of 40.5%, temporarily weighed down relative to the recent trend. This was due to the recognition of the retirement and write-down of inventory, primarily for products manufactured during the SKU expansion period of 2023 and 2024, as cost of sales.

However, excluding this one-time impact, as represented by the dotted line in the graph on the right side of the slide, gross profit for Q4 was 7.2 billion yen, with a gross profit margin of 49.6%.

Although we recorded a temporary write-down this time, excluding this impact, our core business profitability continues to maintain a solid foundation with a gross profit margin of nearly 50%.

Historical Trends in Cost of Sales and SG&A Expenses

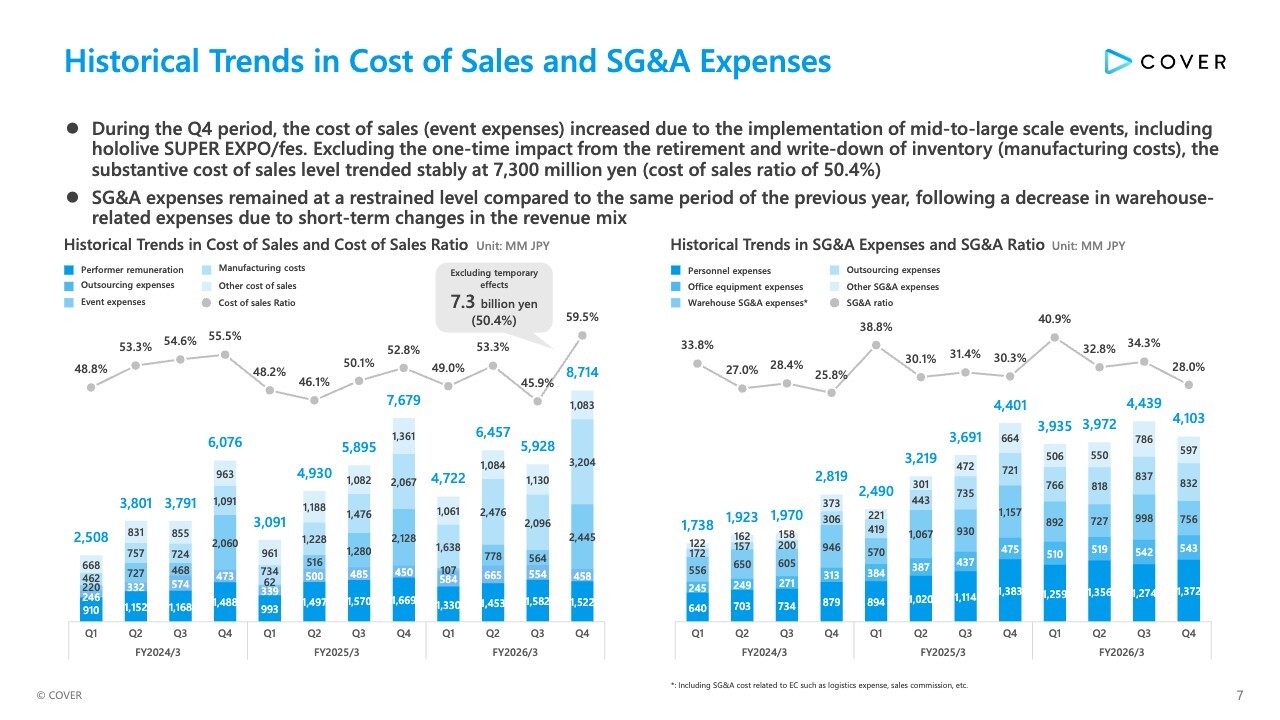

Here is the trend in cost of sales and SG&A expenses. In Q4, cost of sales amounted to 8.7 billion yen, with a cost of sales ratio of 59.5%. This reflects an increase in event expenses due to the implementation of mid-to-large-scale events, including Fes and EXPO, as well as the one-time impact of the retirement and write-down of inventory explained earlier.

However, excluding this one-time impact, as represented by the dotted line in the graph on the left side of the slide, the substantive cost of sales for Q4 was 7.3 billion yen, with a cost of sales ratio of 50.4%. This indicates that the underlying cost level remains stable.

SG&A expenses for Q4 were 4.1 billion yen, with an SG&A ratio of 28.0%. Against the backdrop of short-term changes in the revenue mix, such as adjustments to EC revenue, warehouse-related SG&A expenses decreased, resulting in overall SG&A expenses remaining at a restrained level compared with the same period of the previous year.

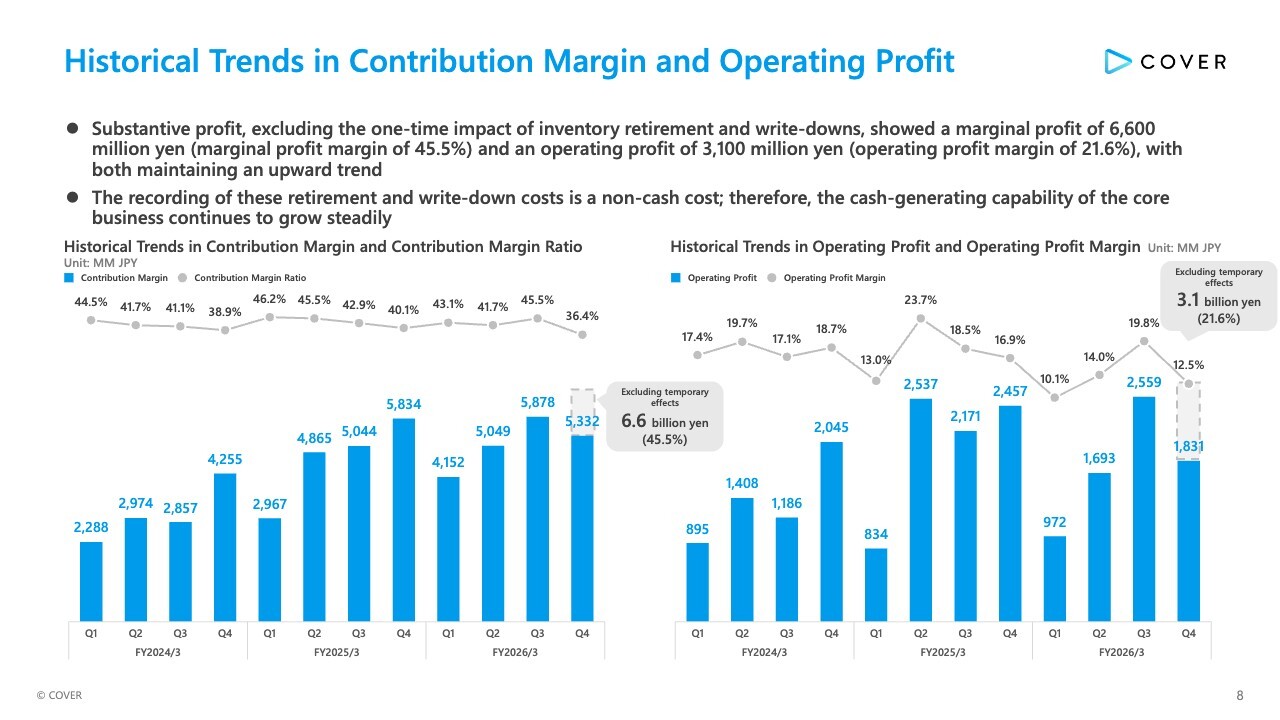

Historical Trends in Contribution Margin and Operating Profit

Here is the trend in contribution margin and operating profit. In Q4, the contribution margin was 5.3 billion yen, and operating profit was approximately 1.8 billion yen. These figures also include the one-time impact of the inventory retirement and write-downs, which I explained earlier.

Excluding this one-time impact, as represented by the dotted line on the graphs in the slide, the substantive contribution margin was 6.6 billion yen, with a contribution margin ratio of 45.5%, and operating profit was 3.1 billion yen, with an operating profit margin of 21.6%. Both figures maintained an upward trend.

Please note that the retirement and write-downs of inventory assets, which were recorded as costs of sales this time, are non-cash expenses. Therefore, the cash-generating capability of our core business continues to grow steadily.

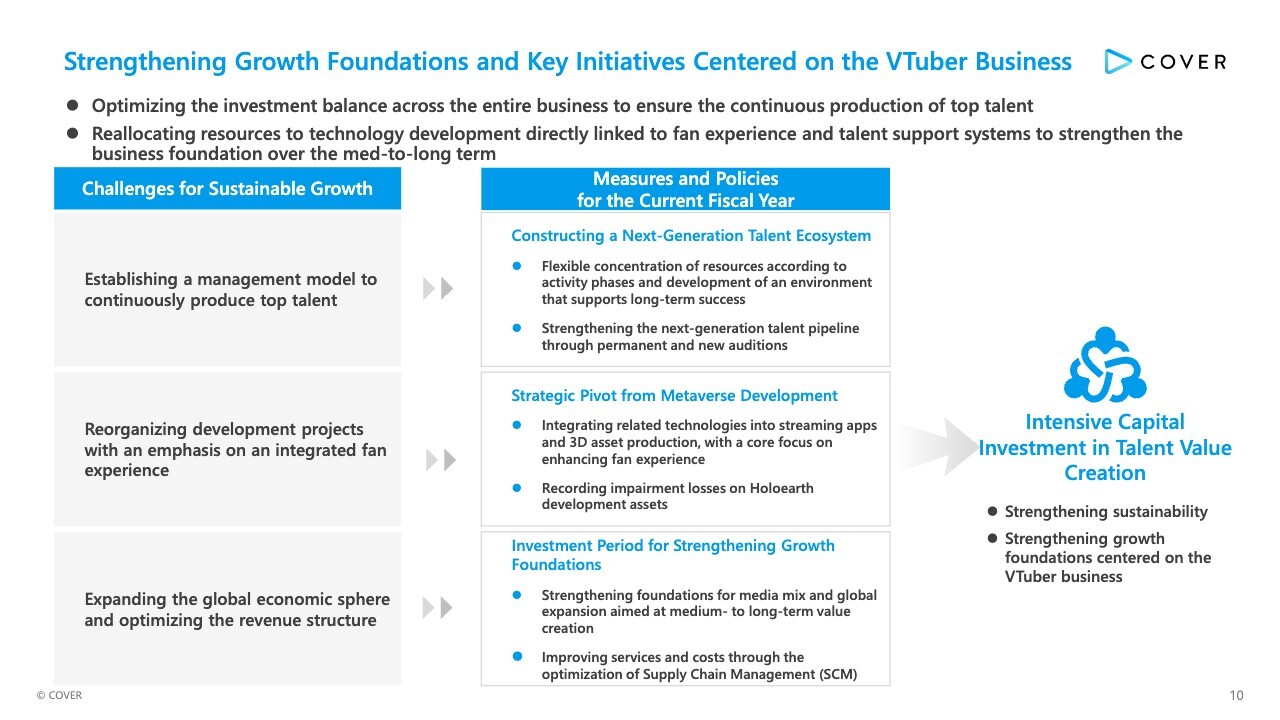

Strengthening Growth Foundations and Key Initiatives Centered on the VTuber Business

Turning to the current status of strengthening our growth foundation, we will optimize the balance of investments across our entire business to ensure we continue to produce top talents in the future. Specifically, we are reallocating resources to technology development directly linked to the fan experience and to talent support systems, thereby strengthening our business foundation over the medium to long term.

As key initiatives, we have identified three major challenges and measures to address them. The first is the establishment of a management model to continuously produce top talents.

To construct a next-generation talent ecosystem, we will promote the flexible concentration of resources according to each talent’s activity phase and the development of an environment that supports their long-term success. At the same time, we will work to strengthen our talent pipeline through both permanent and new auditions.

Second, we are reorganizing our development projects with an emphasis on an integrated fan experience. We are strategically pivoting away from metaverse development, and integrating the related technologies we have cultivated into streaming apps and 3D asset production, with a core focus on enhancing fan experiences. In line with this strategic shift, we have recorded impairment losses on “Holoearth” development assets, as I explained earlier.

Third, we aim to expand our global economic sphere and optimize our revenue structure. Viewing this fiscal year as a period for investing in strengthening our foundation, we will solidify the foundation for media mix and global expansion aimed at creating value over the medium to long term. At the same time, we will improve our services and reduce costs through the optimization of the supply chain.

Through these measures, we will intensively invest capital in talent value creation, as shown on the right side of the slide. We will further enhance the sustainability of our business and establish a solid growth foundation centered on the VTuber business.

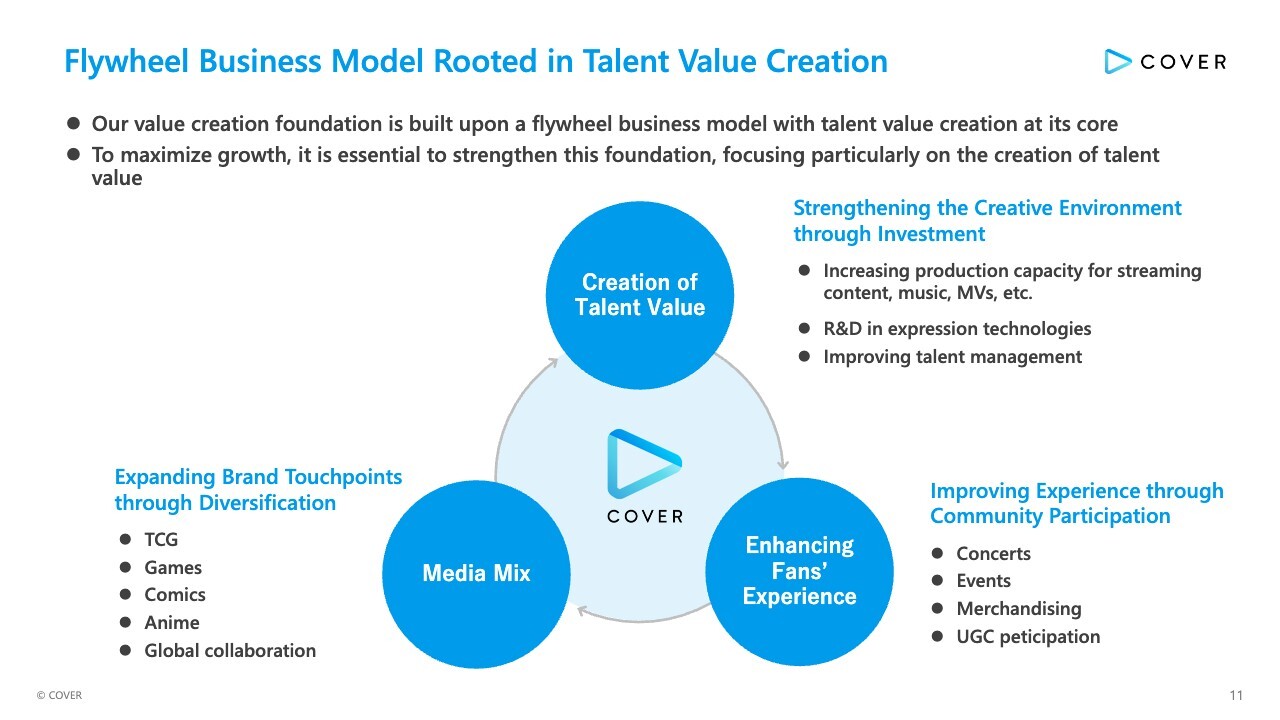

Flywheel Business Model Rooted in Talent Value Creation

To maximize growth, it is essential that we strengthen the three cycles illustrated on the slide. Among these, we are currently focusing our investments on the “creation of talent value”—the top cycle in the diagram, which serves as the core of the entire framework.

Specifically, we are working to strengthen our creative environment by increasing production capacity for streaming content, music, and music videos; conducting R&D in expression technologies; and improving talent management.

The talent value generated here leads to “enhancing fan experience” in the bottom right of the diagram. We will enhance experience value through community activities such as concerts, events, merchandising, and participation in UGC.

Then, there is “media mix” in the bottom left of the diagram. Building on the increased fan enthusiasm, we will significantly expand brand touchpoints through multifaceted initiatives such as trading card games, games, comics, anime, as well as global collaborations.

Moving forward, starting with our investment in the core “creation of talent value,” we will vigorously circulate these three elements to drive medium- to long-term growth.

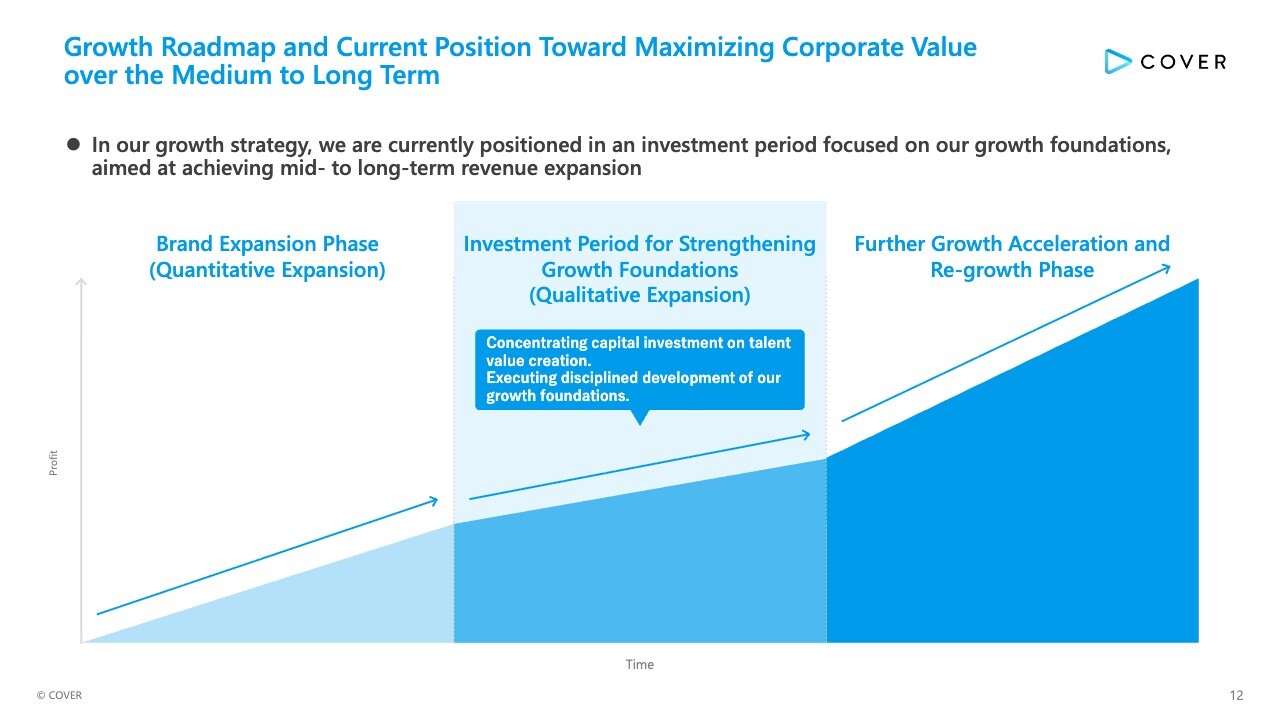

Growth Roadmap and Current Position Toward Maximizing Corporate Value over the Medium to Long Term

Here is the growth roadmap and our current position toward maximizing corporate value over the medium to long term. The graph on this slide shows the timeline on the horizontal axis and profit on the vertical axis.

To date, we have expanded our business scale during the brand expansion phase on the left side of the graph—that is, the phase of quantitative expansion.

Currently, as highlighted in the center of the slide, we have transitioned into an investment period for strengthening our growth foundation. During this period, we are prioritizing qualitative expansion and working to reorganize our business structure, aiming to achieve medium- to long-term revenue expansion.

As I have explained earlier, we will intensively allocate capital to the “creation of talent value"—the core of all our initiatives—and work to develop a disciplined foundation for growth.

By building a solid foundation during this critical investment period, we will seamlessly transition to the phase of further growth acceleration and re-growth shown on the right side of the slide, thereby achieving sustainable enhancement of corporate value.

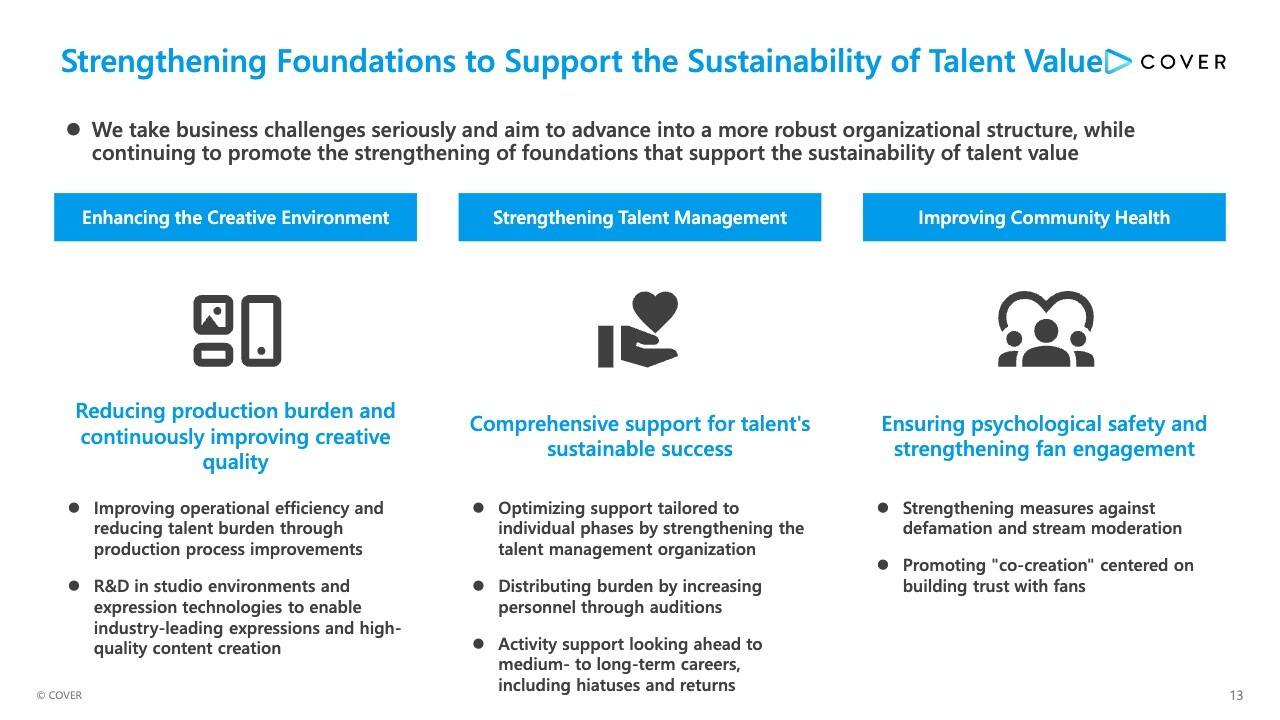

Strengthening Foundations to Support the Sustainability of Talent Value

Let me explain our efforts to strengthen the foundations to support the sustainability of talent value. As a concrete initiative in the investment toward qualitative expansion as outlined earlier, we take our current business challenges seriously and will work to build a more robust organizational structure.

Specifically, we will focus on the three areas listed on the slide. First is enhancing the creative environment. We will improve operational efficiency and reduce the production burden on talent by improving the production process.

Furthermore, to enable the creation of industry-leading, high-quality content, we will continue R&D on studio environments and expression technologies, aiming to enhance creative quality.

Second is the strengthening of talent management. We will strengthen our management organization and build an optimal support system tailored to each talent’s activity phase.

Additionally, we will comprehensively support talents’ sustained success by distributing workloads through increased personnel, and by looking ahead to their medium-to-long-term careers, including periods of hiatuses and returns.

The third is improving community health. We will ensure psychological safety for both talents and fans by strengthening measures against defamation and improving stream moderation. Building on this foundation, we will further promote “co-creation” centered on building strong, trusting relationships with fans.

By concurrently pursuing these structural enhancements, we will solidify the sustainability of talent value, which forms the core of our business.

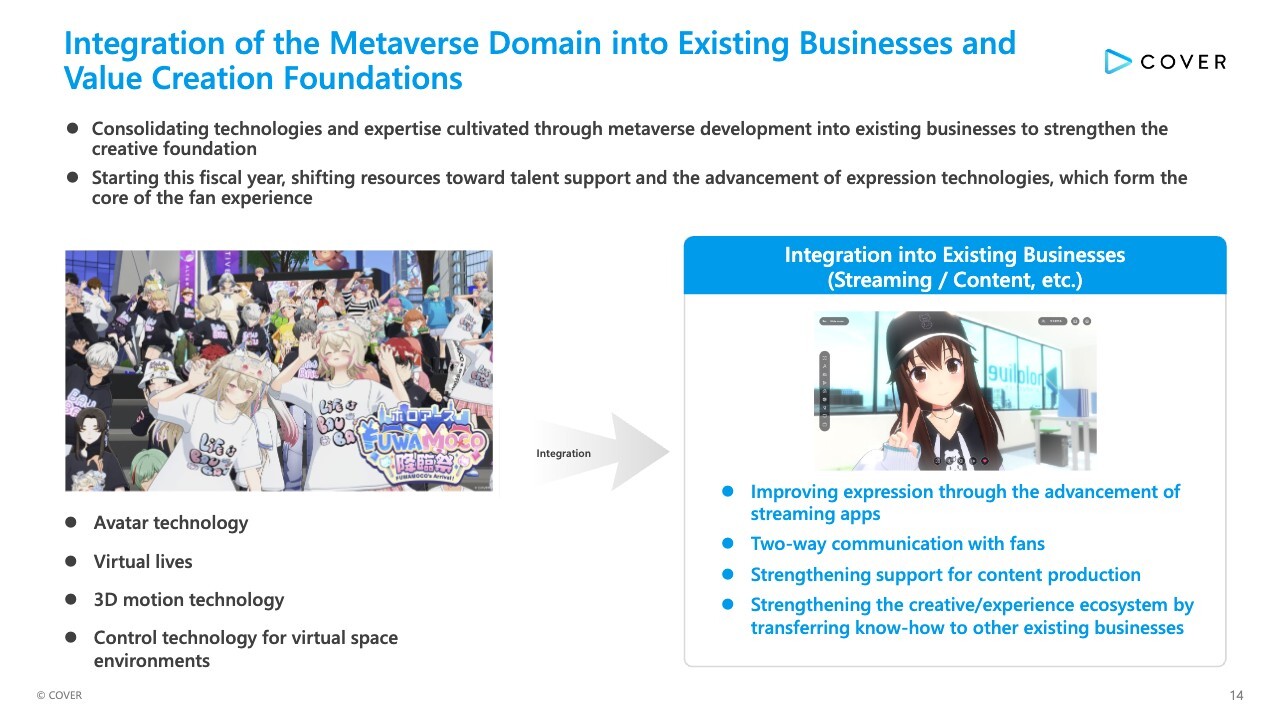

Integration of the Metaverse Domain into Existing Businesses and Value Creation Foundations

I will discuss the integration of metaverse technologies into our existing businesses and value creation foundations. Through our metaverse development efforts to date, we have cultivated advanced technologies and expertise in areas shown on the left side of the slide, such as avatar technology, virtual lives, 3D motion technology, and control technology for virtual space environments.

Starting this fiscal year, we are consolidating and integrating these technologies into our core existing businesses, such as Streaming/Content, rather than managing them as independent projects.

We will directly transfer this know-how to areas shown on the right side of the slide, such as improving expression through the advancement of streaming apps, strengthening two-way communication with fans and support for talent content production. This will enable richer expressions in streaming and 3D live events featuring a diverse range of talents both in Japan and overseas.

In this way, by strategically shifting resources toward talent support and the advancement of expression technologies—which form the core of the fan experience—we will further elevate the experience value in our existing businesses.

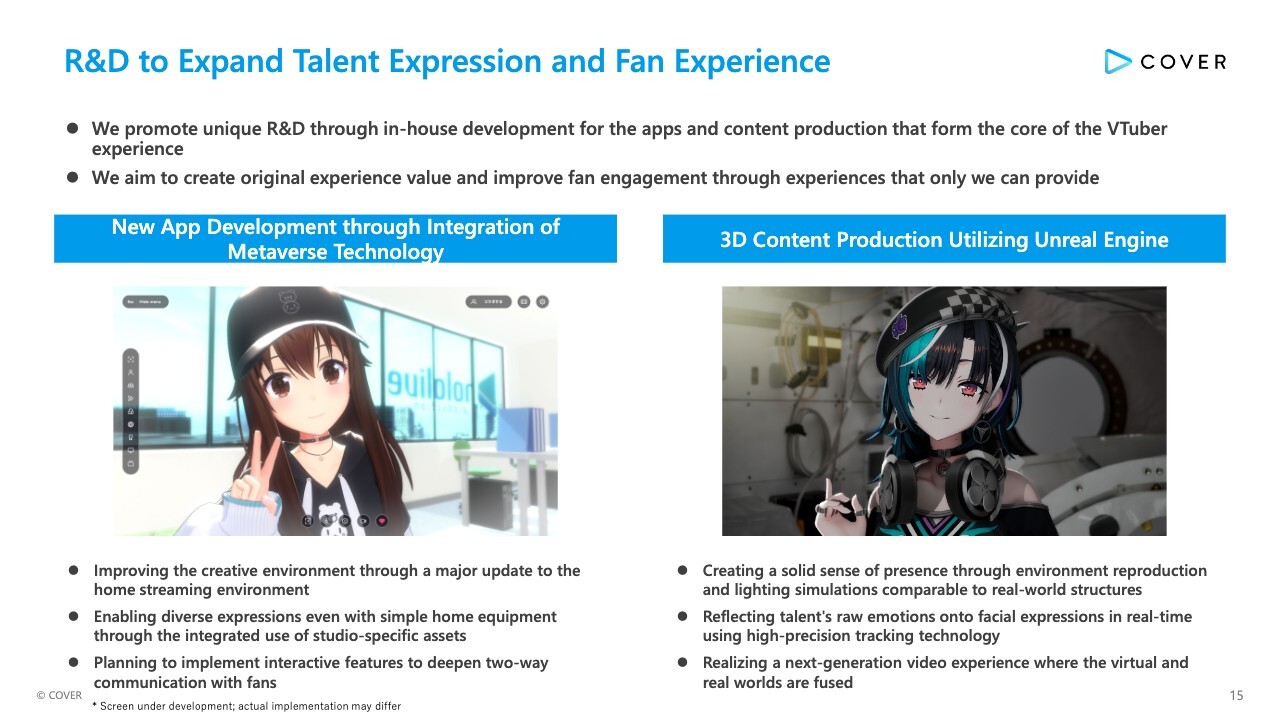

R&D to Expand Talent Expression and Fan Experience

I will talk about our R&D to expand talent expression and fan experience. We promote unique R&D through in-house development for the apps and content production that form the core of the VTuber experience.

Through this, we aim to create original experience value that only we can provide, and further improve fan engagement.

One specific initiative, as shown on the left side of the slide, is new app development through the integration of metaverse technology. By upgrading talents’ home streaming environments and making assets, which were previously reserved for studios, accessible even with simple home equipment, we enable diverse expressions in daily streams.

Additionally, we aim to deepen two-way communication with fans through the implementation of interactive features.

The right side of the slide shows 3D content production utilizing Unreal Engine. In addition to environment reproduction and lighting simulations comparable to real-world spaces, we use high-precision tracking technology to reflect the talents’ raw emotions onto their facial expressions in real time. This allows us to provide a next-generation video experience that seamlessly fuses the virtual and the real world.

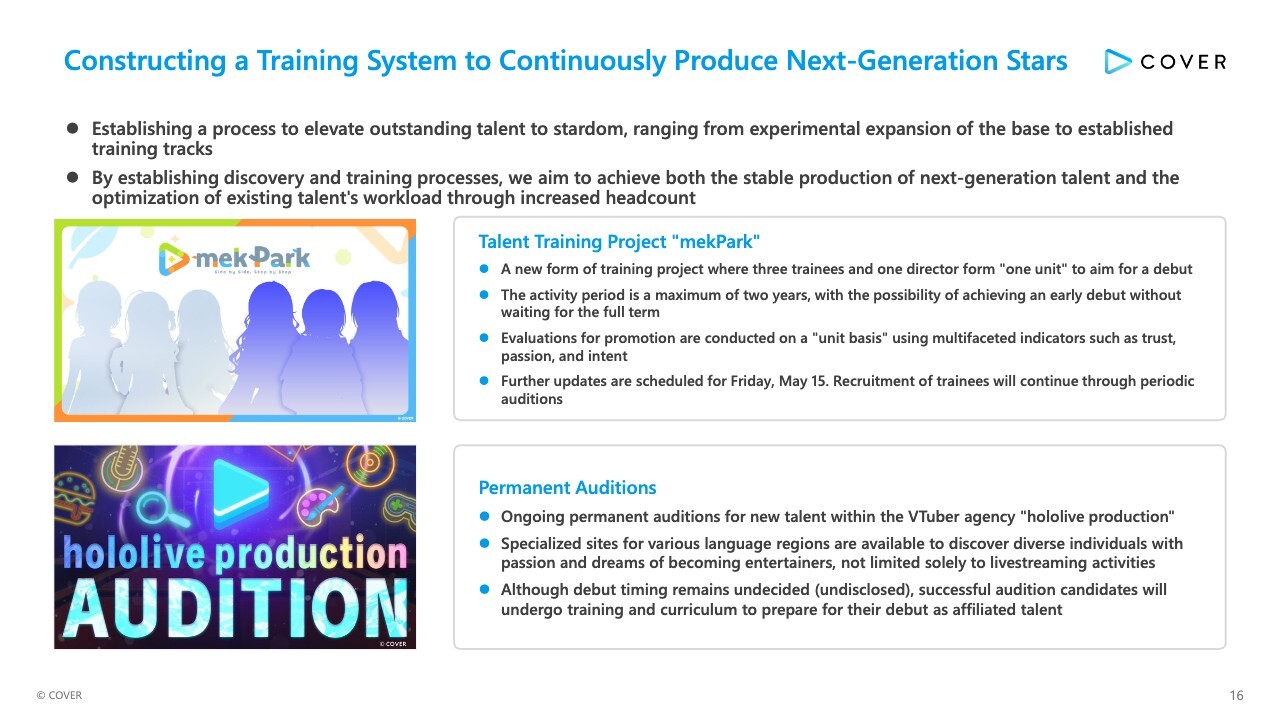

Constructing a Training System to Continuously Produce Next-Generation Stars

Moving on to the construction of a training system to continuously produce next-generation stars. We are working to establish a process to elevate outstanding talent to stardom, ranging from experimental expansion of our talent base to established training tracks.

By establishing this discovery and training process, we aim to achieve both the stable production of next-generation talents and the optimization of the workload of existing talents through increased headcount.

The first specific initiative is the talent training project “mekPark,” shown at the top of the slide. In this new form of training project, three trainees and one director form one unit, aiming to debut.

Over an activity period of up to two years, evaluations will be conducted using multifaceted indicators, with the unit aiming for promotion. Follow-up information on this project is scheduled to be announced on May 15.

The second initiative is the permanent audition shown at the bottom of the slide. We have set up specialized sites for various language regions and are continuously discovering individuals globally who possess diverse talent and passion, not limited solely to livestreaming activities. Successful candidates are provided with training based on our unique curriculum and undergo intensive preparation for their debut.

By constructing this training system, we will continuously produce the next generation of top talents and strongly drive our medium- to long-term growth.

Expanding Brand Touchpoints through Media Mix

Next, I will discuss the initiatives for expanding brand touchpoints through media mix. As a pioneer in the industry, we are promoting media mix development to cultivate new markets and build a robust business foundation.

Moving forward, we will continue to develop multifaceted businesses, focusing on areas with high synergy with our VTuber business. The left side of the slide shows our track record and outlook for trading card games. In FY2026/3, we achieved approximately 7.2 billion yen in revenue and sold over 20 million packs cumulatively.

We have captured approximately a 2% share of the domestic market. Going forward, we will prioritize player base growth to solidify our position in the domestic market while pursuing full-scale global expansion.

The right side of the slide covers the area of game development. For FY2027/3, we plan to release our first major smartphone game, “hololive Dreams.” Pre-registrations have already exceeded 900,000, and we expect this title to enhance our presence in the gaming market.

In FY2026/3, we released four small-to-medium-sized titles through joint development with external companies, recording sales of over 160,000 units. As such, we are steadily building a track record in the gaming sector.

Strengthening Foundations for Global Expansion and Optimizing Supply Chain Management

Let me explain our initiatives for strengthening our foundation for global expansion and optimizing supply chain management. We are vigorously promoting the development of our business foundation toward establishing a global creator economy.

Please take a look at the left side of the slide, which shows the expansion of fan touchpoints in the global market. As the graph indicates, both overseas sales and the number of partners have continued to grow steadily.

As a specific example, our large-scale collaboration with the Wei Chuan Dragons in Taipei drew a total of approximately 100,000 people over three days, achieving one of the highest turnout records in the history of the Taipei Dome, thereby demonstrating our significant presence in the Asian region.

In the North American market, we held a 24-hour collaboration event with Twitch titled “holoday: Twitch × hololive,” achieving significant results, including 500,000 impressions across related social media platforms and a total of 250,000 followers. Moving forward, we aim to further strengthen brand awareness in the gaming sector in North America.

Turning to the right side of the slide, we will discuss optimizing procurement and logistics costs and improving services. As the foundation to support our global expansion, we are advancing the optimization of the entire supply chain.

In addition to enhancing the ordering process and improving logistics efficiency from overseas production sites, we have consolidated our warehouses. Furthermore, as mentioned in the overview of business performance at the beginning of this presentation, we have implemented the retirement and write-down of slow-moving inventory as part of our efforts to improve overall warehouse and asset efficiency.

At the same time, we are working to improve the user experience (UX) by expanding our cross-border EC sales regions and implementing flat shipping rates, while also expanding our pop-up shop initiatives both domestically and internationally. Through these efforts to strengthen our foundation, we will ensure sustainable service improvements in the global market and the expansion of the creator economy.

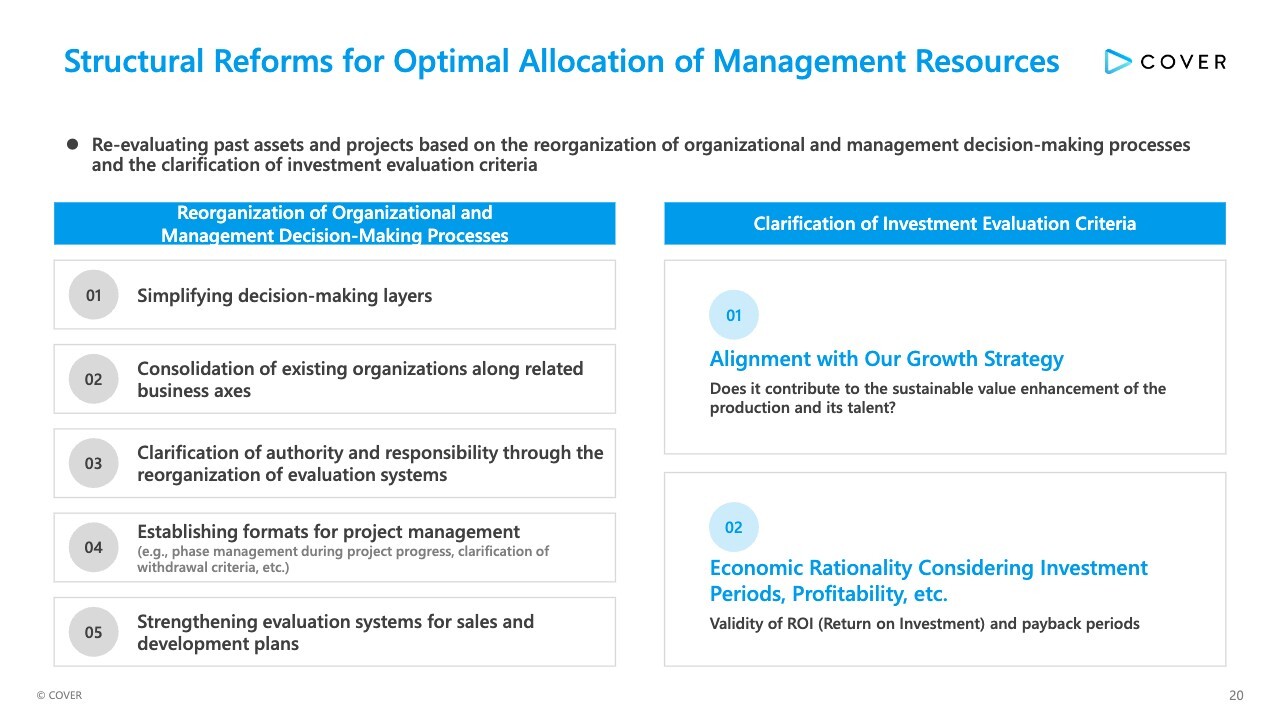

Structural Reforms for Optimal Allocation of Management Resources

Yosuke Kaneko (hereinafter “Kaneko”): I am Yosuke Kaneko, Director and CFO. I will now explain the progress in our structural reforms to the management foundation. To achieve disciplined growth going forward, we have reorganized the organizational and management decision-making processes and clarified our investment evaluation criteria. Based on this, we have reevaluated our past assets and projects.

First, let’s look at the reorganization of organizational and management decision-making processes shown on the left side of the slide. We will improve management speed by simplifying decision-making layers and consolidating organizations along related business axes.

Concurrently, we will clarify authority and responsibility through the reorganization of evaluation systems and establish formats for project management, including withdrawal criteria, to build a more disciplined business management framework.

Moving to the right side of the slide, we have clarified our investment evaluation criteria. For future investment decisions, we will set two clear criteria. The first is alignment with our growth strategy. We place the highest priority on whether an investment contributes to the sustainable value enhancement of the production and its talents.

The second is economic rationality. We will assess the validity of ROI (Return on Investment) and payback periods. Through these structural reforms, we will optimally allocate our limited management resources to areas that truly drive growth and establish a solid earnings base.

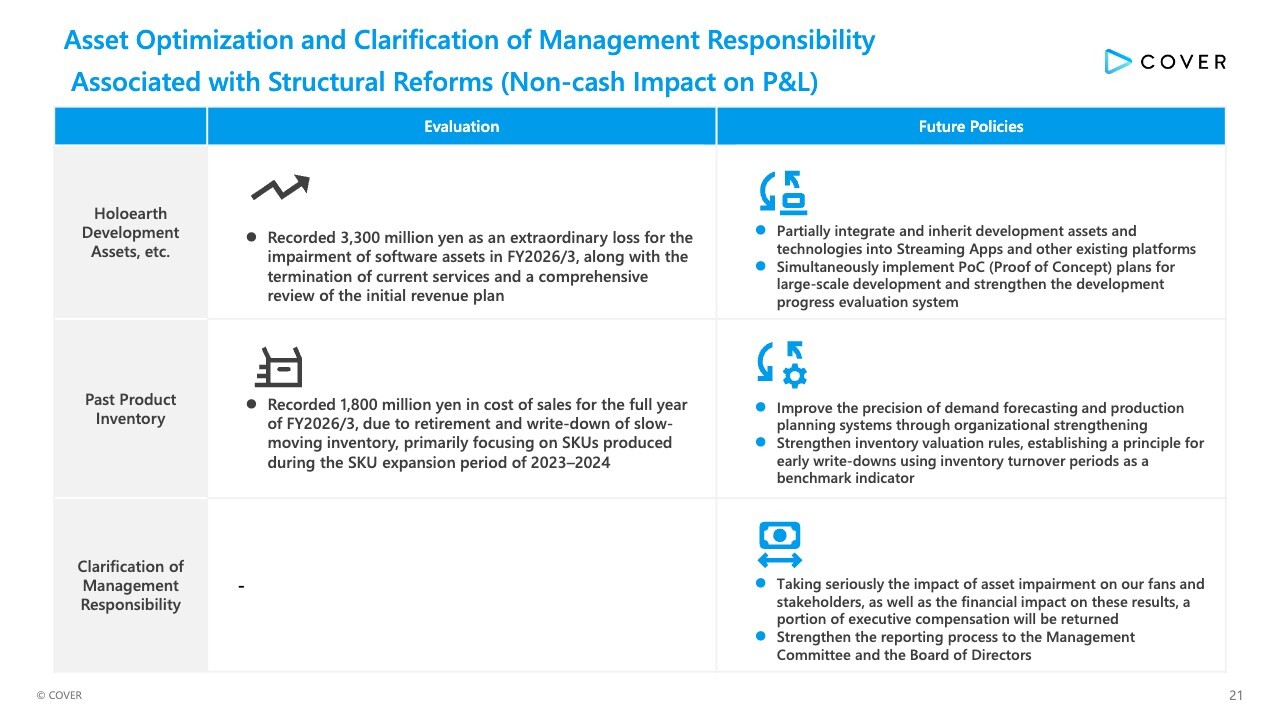

Asset Optimization and Clarification of Management Responsibility Associated with Structural Reforms (Non-cash Impact on P&L)

Here is the asset optimization and clarification of management responsibility. The purpose of this asset optimization is to eliminate future uncertainties at an early stage and establish a sound financial structure. Note that these are all non-cash expenses and do not involve any cash outflow.

First, regarding the “Holoearth” development assets, etc. shown at the top of the slide, we recorded 3,300 million yen as an extraordinary loss for the impairment of software assets in FY2026/3, along with the termination of current services and a comprehensive review of the initial revenue plan.

Going forward, we will integrate and inherit technologies and expertise cultivated through our business into existing businesses, while strengthening our management structure for large-scale development projects.

Next, regarding past product inventory. We recorded 1,800 million yen in cost of sales for the full year of FY2026/3, due to the retirement and write-down of slow-moving inventory, primarily focusing on items produced during the expansion period of 2023–2024.

To prevent recurrence, we will improve the precision of demand forecasting and production planning systems through organizational strengthening and strengthen inventory valuation rules, establishing a principle for early write-downs using inventory turnover periods as a benchmark indicator.

Lastly, I will discuss clarification of management responsibility. While we have optimized our assets associated with the structural reforms aimed at future sustainable growth, we take seriously the impact of asset impairment on our fans and stakeholders, as well as the financial impact on these results, and have accepted the return of a portion of executive compensation.

We will clarify management responsibility and pave the way for sustainable and disciplined growth through this series of structural reforms.

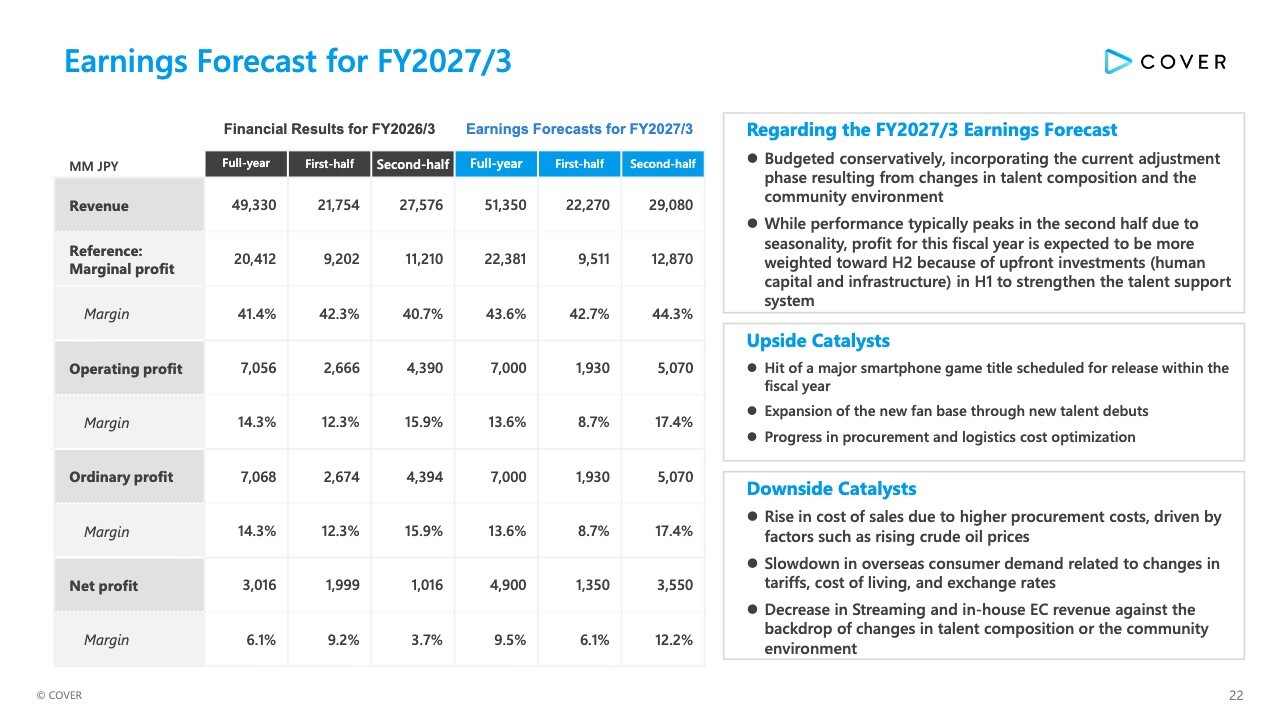

Earnings Forecast for FY2027/3

The slide covers our earnings forecast for FY2027/3. The specific figures for each item are listed in the table on the left side of the slide.

First, as a premise for the earnings forecast, we have budgeted conservatively, incorporating the temporary adjustment phase resulting from changes in talent composition and the community environment.

Additionally, while performance typically peaks in the second half due to seasonality, this fiscal year will see a concentration of upfront investments (human capital and infrastructure) in the first half to strengthen the talent support system. Therefore, profit for this fiscal year is expected to be more weighted toward the second half.

Next, let’s look at upside catalysts that could drive earnings above forecasts. Our upside catalysts include a hit for a major smartphone game title scheduled for release within the fiscal year, expansion of the new fan base through new talent debuts, and better-than-expected progress in procurement and logistics cost optimization.

On the other hand, we recognize some risks as downside catalysts that could lead to lower-than-expected performance. Those include a rise in cost of sales due to higher procurement costs driven by factors such as rising crude oil prices; a slowdown in overseas consumer demand related to changes in exchange rates and cost of living; and a decrease in Streaming and in-house EC revenue against the backdrop of environmental changes.

This fiscal year, we will ensure the execution of upfront investments aimed at future growth while appropriately managing these risks.

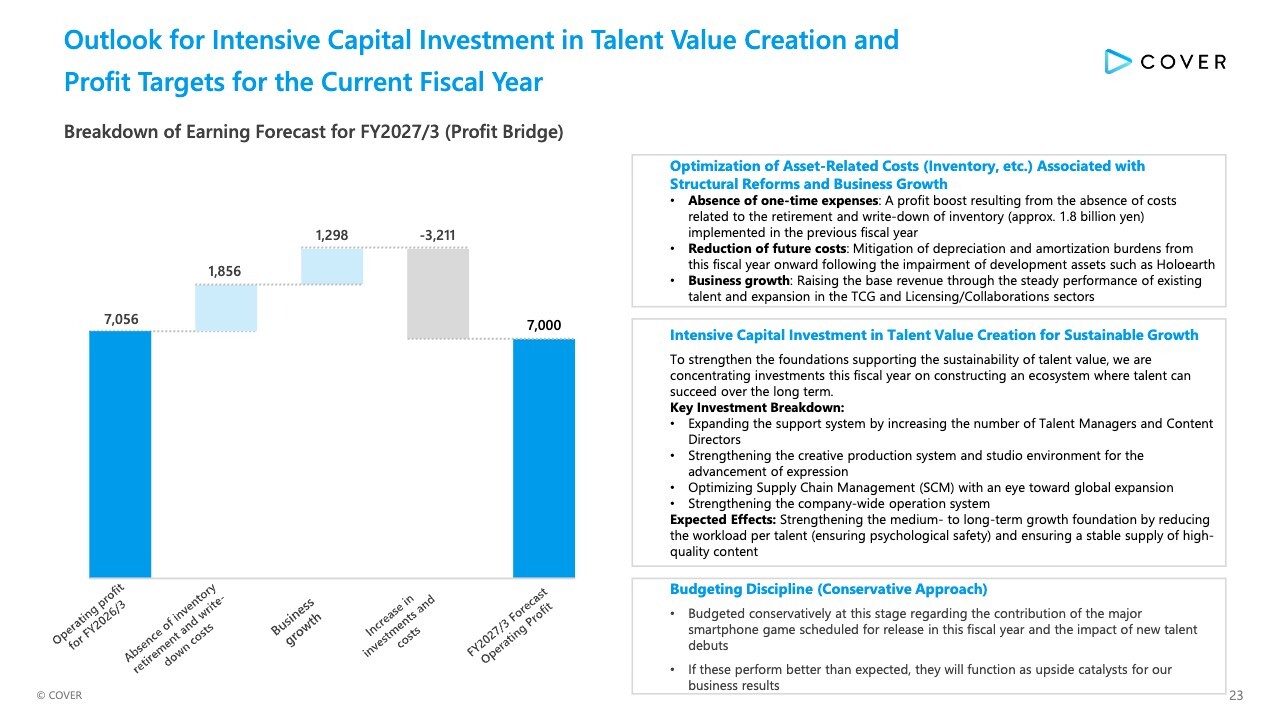

Outlook for Intensive Capital Investment in Talent Value Creation and Profit Targets for the Current Fiscal Year

This section covers our profit target for the current fiscal year and the profit bridge that breaks it down. Please refer to the graph on the left side of the slide.

For the current fiscal year, we have set a projected operating profit of 7,000 million yen, which is on par with the previous fiscal year’s level. I will explain the breakdown of this figure based on the three points on the right side of the slide.

First, the factors driving profit growth in the top section include optimization of costs resulting from the structural reforms. This includes the absence of costs related to the write-down of inventory (approx. 1.8 billion yen) implemented in the previous fiscal year and mitigation of depreciation and amortization burdens from this fiscal year onward following the impairment of development assets.

In addition, steady performance of existing talents and the expansion of our core businesses—such as TCG and licensing—have steadily boosted our base revenue.

Next, I will explain the approximately 3,200 million yen increase in investment costs, shown in the middle section as a factor weighing on profit. This represents intensive capital investment in talent value creation for sustainable growth.

Specifically, we will make concentrated investments in expanding the support system by increasing the number of Talent Managers and Content Directors, enhancing our studio environment for the advancement of expression, and optimizing our global SCM.

By reducing the workload on our talents and ensuring psychological safety, we will build a solid growth foundation that ensures a stable supply of high-quality content.

Finally, I will discuss the assumptions underlying the budget outlined below. At this stage, we have conservatively factored into the budget the introduction of the major smartphone game scheduled for release in this fiscal year and the impact of new talent debuts. If these perform better than expected, they will function as upside catalysts for our business results.

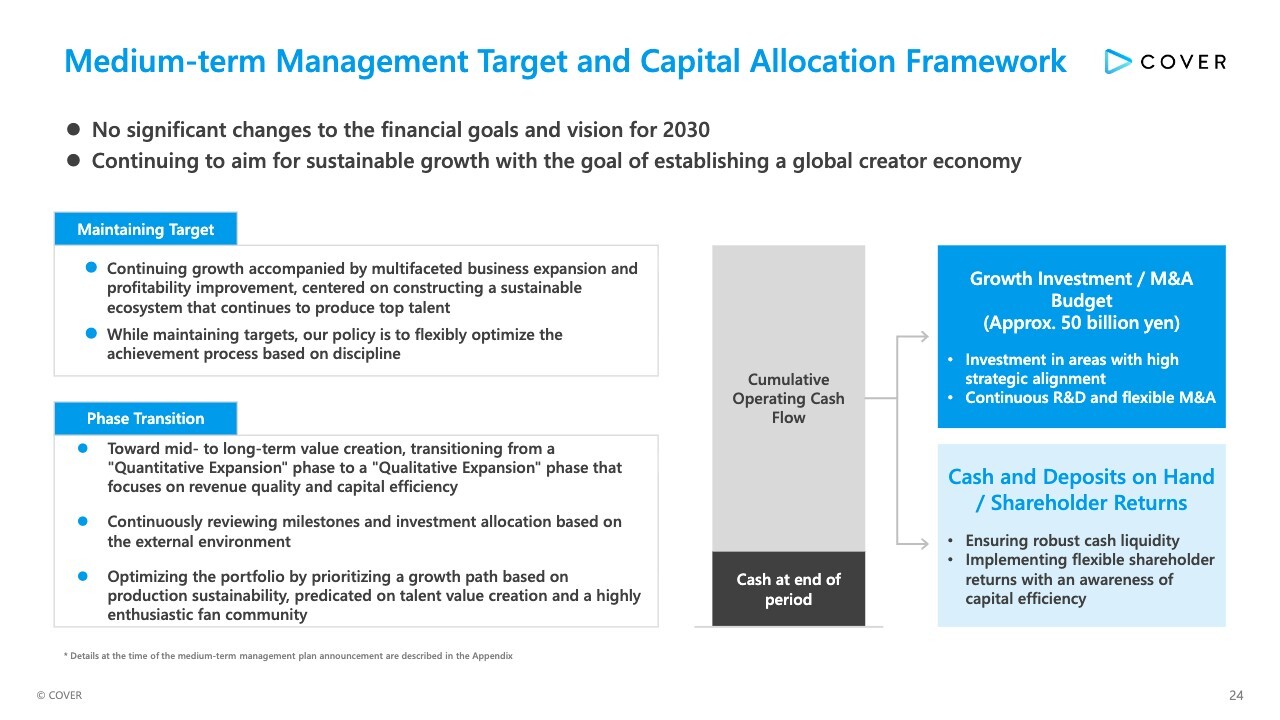

Medium-term Management Target and Capital Allocation Framework

Our medium-term management target and capital allocation framework are as follows. To begin with, we have no significant changes to the financial goals and vision for 2030. We continue to aim for sustainable growth with the goal of establishing a global creator economy.

As shown on the left side of the slide, while maintaining our ultimate targets, our policy is to flexibly optimize the achievement process based on discipline. As explained earlier, we will transition from a quantitative expansion phase to a qualitative expansion phase that focuses on revenue quality and capital efficiency.

With talent value creation as our fundamental premise, we will proceed with portfolio optimization that prioritizes the sustainability of the production. With this in mind, I will now explain the capital allocation outlined on the right side of the slide.

We plan to allocate approximately 50 billion yen in cumulative funds from the operating cash flow generated during the Medium-term Management Target period (starting from the past fiscal year) toward growth investments in areas with high strategic alignment, such as organizational strengthening for sustainable production growth, continuous R&D and flexible M&A.

At the same time, we will implement flexible shareholder returns with an awareness of capital efficiency while ensuring robust cash liquidity. We will work to achieve the optimal balance between disciplined growth investments and returns to maximize corporate value over the medium to long term.

We are currently in a phase of growth investment aimed at achieving our mission, and our basic policy is to continue prioritizing this proactive investment stance moving forward.

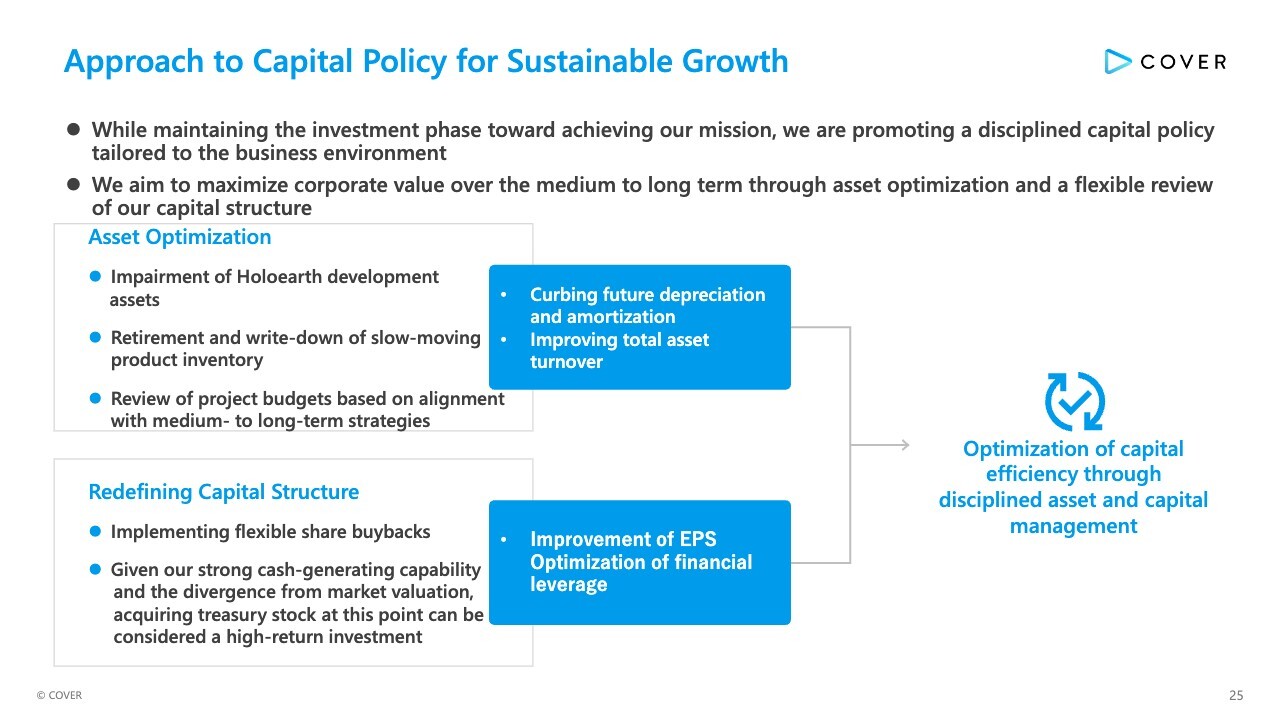

Approach to Capital Policy for Sustainable Growth

Concurrently, rather than simply pursuing scale expansion, we will implement a disciplined capital policy considering appropriate capital efficiency in line with each business phase.

As part of this approach, we are proceeding with asset optimization. The impairment of Holoearth development assets disclosed in these financial results, as well as the retirement and write-down of slow-moving product inventory, are concrete examples of this policy in action.

Through these measures, we are reducing future cost burdens and improving our total asset turnover, thereby establishing a foundation that allows us to make investments aligned with our medium- to long-term growth strategy more efficiently. Furthermore, while prioritizing investments for growth, we will flexibly review our capital structure accordingly.

As a concrete example of this, we have decided to implement a flexible share buyback program. Given the gap between our strong cash-generating capability and our current market valuation, we believe that share buybacks conducted in parallel with growth investments represent a high-return investment at this time.

Moving forward, we will continue to prioritize growth investments while combining this with disciplined asset and capital management to maximize corporate value over the medium to long term.

Q&A: Revenue projections for FY2027/3 and trends in the Merchandising service

Question: The revenue projection for FY2027/3 is only a 4% increase, which appears to be weaker guidance than usual. Does this mean growth in specific segments is slowing down?

For example, the Merchandising service saw a double-digit decline in revenue during the January-March quarter. Is it difficult to anticipate high growth due to changes in product demand trends, or is this simply a more conservative plan than usual? Can you elaborate on the planned revenue level and trends in the Merchandising service?

Kaneko: First, overall, as you mentioned, we are indeed taking a conservative view. While the factors are complex, regarding EC revenue within the Merchandising service, we have adopted a slightly conservative outlook in our planning, considering changes in talent composition and community environment, and the impact of exchange rates and tariffs in light of the global situation.

On the other hand, we continue to anticipate steady growth in retail operations and card games within Merchandising; we believe these two areas will complement each other. Additionally, we believe continued growth can also be expected in B-to-B licensing tie-ups outside the games.

Furthermore, factors that could drive growth this fiscal year include the addition of new talents and the release of “hololive Dreams,” a major smartphone game.

Given the current situation and the fact that this is our first experience releasing a major smartphone game, it is difficult to incorporate these factors into our budget. We believe this is one reason why our estimates for these major growth drivers remain conservative.

While we plan to focus on improvements based on intensive capital investment in talent community and operational reforms, we are currently factoring these efforts conservatively into our numerical projections.

Q&A: Expense plan and the impact of one-off and recurring investments on earnings

Question: I have a question regarding the expense plan. As mentioned on Slide 23, you've allocated 3,200 million yen as an upfront investment this year, following last year's approach. Could you break down these expenses into one-time costs and those that will continue into the next fiscal year and beyond?

In particular, you mentioned that the workforce will grow, but I recall you previously stating that the pace of employee growth would be relatively gradual. Does this mean that the current situation has changed, perhaps due to measures such as strengthening the support system for talents?

Kaneko: Taking a longer-term perspective, we expect the ratio of fixed costs to steadily decline as we improve our profitability through the diversification of our business driven by media mix initiatives. In fact, excluding the impact of impairment losses and asset disposals, our operating profit margin for the fourth quarter exceeded 20 percent.

At the same time, while media mix and business development are growing significantly, I believe substantial expansion over the medium to long term will be difficult without the sustained engagement of our core talent activities and the continued influx of fans.

At this inflection point, our management decision for the period spanning the second half of last fiscal year through the first half of the current fiscal year is to put that sustained engagement back on a solid footing—even if it requires short-term costs.

I will now discuss the extent to which these costs are temporary. We recognize that, by their nature, items such as CAPEX (capital expenditures) that do not place a significant direct burden on the statement of income (P&L) are not particularly substantial. However, in connection with the advancement of our production systems and creative environment, we anticipate that some CAPEX will be incurred for software development and the enhancement of streaming apps.

That said, personnel expenses—including costs associated with organizational restructuring that will continue as fixed costs in the next fiscal year—are expected to be the main driver. As shown in the slide, we anticipate increased spending on expanding our workforce with additional talent managers and content directors and organizational restructuring for our supply chain management infrastructure to support global expansion.

As a result, while these are ongoing investments that will have a direct short-term impact on the P&L or increase fixed costs, as I mentioned at the beginning, we believe that in the medium term, the ratio of fixed costs will decrease, allowing us to manage these costs effectively.

Q&A: “Holoearth” summary and new app development

Question: Regarding “Holoearth,” you mentioned that the technology cultivated through this service will be applied elsewhere. Could you please provide a summary of “Holoearth” at this time? Please share what went well, the challenges that emerged, and the lessons learned for the future.

Also, you mentioned plans to develop a new app. Given what you said earlier, the development costs don’t seem particularly high. Could you also tell us whether this requires the same level of investment as “Holoearth”?

Tanigo: Presently, in the so-called metaverse market, VRChat—a VR community platform—and Roblox—a game-based UGC platform—are the two dominant players, both experiencing significant growth in the number of users.

Our “Holoearth” platform incorporated games and communication features in addition to virtual lives, allowing us to expand our content offerings broadly. We believe, however, a major challenge was that we expanded our scope too broadly, making it difficult to maintain adequate focus.

Since last fiscal year, we have shifted our focus to virtual live performances aimed specifically at fostering interaction between talents and fans, as well as initiatives utilizing talent Arrival Festivals; however, we recognize that we still were not sufficiently focused.

Furthermore, while talents use the app daily for their regular streams, they were also required to use the separate “Holoearth” app, which we believe created unnecessary duplication of effort.

Therefore, moving forward, our policy is to repurpose the technology developed for “Holoearth” into an app that can be used for regular streams on “hololive.”

One of the key factors in our success was the positive reception of the experience that allowed talents and fans to interact in the same virtual space. The second factor was the experience of virtual lives. Typically, when watching live streams on platforms like YouTube, viewers were watching through a screen with fixed camera angles. However, we believe that the ability to watch their favorite talent’s performance from any angle they preferred during virtual lives was extremely well-received by our audience.

Third, the avatar system. While it was originally introduced as a system allowing users to change their avatars’ outfits, development last year enabled us to implement it as a costume-change system for talents as well. We believe this mechanism is a technology that can be repurposed when we roll out the “hololive” streaming apps in the future. Kaneko will explain the cost aspects.

Kaneko: First, cases where such development projects incur massive costs typically involve very long development cycles or situations where we continuously create large volumes of assets, such as 3D assets for the game portion of “Holoearth.”

In contrast, for the development of this new app, experimental validation is constantly being conducted while talents themselves continue to stream. Thus, we plan to streamline and refine development by relying on a small, elite development team and integrating existing studio assets into the home streaming environments that talents use most frequently.

Accordingly, while there is a possibility that we will continue to improve the development through iterative testing in certain areas, we do not currently anticipate that the capitalized development expenses will accumulate to billions of yen, as was the case with “Holoearth.”

Q&A: Strategy for acquiring new fans following the integration of existing businesses

Question: You mentioned that, following the suspension of “Holoearth” development, you are proceeding with the integration of existing businesses, such as streaming content. Regarding this, is it correct to understand that streaming will continue to be the primary focus for acquiring new fans in the medium to long term?

What are your current thoughts on the necessity and potential of acquiring a new fan base that does not necessarily watch daily streams—such as those drawn through video games or trading card games?

Tanigo: As mentioned in this presentation, we believe our media mix strategy is more extensive than that of our competitors. While peers in the industry have announced plans to launch card games in the future, we have already taken the lead in this area, and we aim to be the first in the industry to release smartphone games as well.

Through these media mix initiatives, we plan to continue actively working to attract new fan segments.

Meanwhile, many of our talents regularly stream three to seven times a week, and they have a large viewership. Therefore, we consider technical investments in the streaming content sector to be a high-priority initiative.

While YouTube currently facilitates interactive communication through the chat box off-screen, we believe leveraging “Holoearth” technology could enable initiatives where talents and fans can interact during live streams in the future.

Such initiatives will become feasible by integrating the “Holoearth” team into the “hololive” streaming apps development team.

Q&A: Future inventory valuation policy and its impact on the cost of sales ratio

Question: I need to confirm your future inventory valuation policy. You previously explained that your general policy is to implement early write-downs based on inventory turnover periods. In that regard, it would be helpful if you could share your current thoughts on the extent to which you anticipate additional impacts on the cost of sales ratio or additional costs to cost of sales—compared to the level excluding this fiscal year’s temporary write-downs.

Kaneko: In Q4, we recorded approximately 1,300 million yen in manufacturing costs related to retirement and write-down, bringing the cumulative total for the full fiscal year to approximately 1,800 million yen. This breakdown is the result of actively clearing out slow-moving inventory: products that are not unsellable but are hindering efficient operations.

Consequently, we believe we can significantly mitigate these write-offs and impairment effects in FY2027/3 and beyond. We believe the figure will comfortably remain in the low hundreds of millions of yen range.

Question: Does this mean you're projecting the figure to be in the low hundreds of millions of yen for the full year?

Kaneko: Depending on the circumstances, the figure could be even lower.

Q&A: Current status of fan communities and improvement measures

Question: I believe there has recently been a slight downturn regarding fan communities, “hololive,” and IP value. Can you please explain this situation again?

Tanigo: As a result of establishing many departments in line with our business expansion up until last fiscal year, even if a single error occurred within a specific department, it appeared to talents and fans as if multiple errors had occurred. In this regard, we recognize that, as a company, we did not manage that area sufficiently.

Moreover, regarding defamation on social media, while we had been taking measures against attacks on our talents through information disclosure and other means, our countermeasures against those directed at the company itself were insufficient. We have come to recognize that these issues, primarily related to governance, have created an unfavorable environment within the current fan community.

As immediate countermeasures, first, we have been streamlining our organization since April, consolidating our departments from 19 to approximately 10. Additionally, we have established a system where the corporate division strictly monitors and addresses errors that occur in individual departments, aiming to minimize such errors and prevent the recurrence of similar issues.

Second, as I have already begun this effort, I am personally communicating directly with fans.

Currently, while we have provided some explanation to our talents, we have not been sufficiently conveying the company’s policies to our fans. As a result, there are instances where the information is misinterpreted. For this reason, I believe it will remain crucial to clearly communicate the company’s initiatives to our fans going forward.

Third, we are reassigning talented personnel from our metaverse business to improve not only the application of technology but also areas such as art direction and the management of live events. This allows us to leverage the capabilities of the talented individuals we have hired and transform our organization into one capable of producing high-quality content in-house.

Q&A: Impact of Hoshimachi Suisei’s establishment of a private office on financial performance

Question: Regarding Hoshimachi Suisei’s establishment of a private office, can you please explain how the impact on financial performance has been factored into this fiscal year’s plans, and whether there are any anticipated negative effects?

Kaneko: Regarding the impact on financial performance, we expect to factor in an impact of several hundred million yen. For example, we believe that income from live concerts and similar events, which our company previously organized primarily on its own, will be replaced by other top talents utilizing our limited resources to hold concerts. Therefore, we expect the net decrease in revenue to be mitigated to some extent.

While she has announced her independence, as stated in the press release, we will adopt a hybrid structure in which she will continue her activities as an artist through her office while continuing her activities as a “hololive” member with our company as before.

Furthermore, we believe that aspects of her artist activities involving IP owned and managed by our company, as well as contractual and rights-related matters, will continue to present profit opportunities for our business to a certain extent. Therefore, we will not lose all revenue. Additionally, we expect to maintain a certain level of engagement with the fan community that has grown through her activities.

Q&A: Optimism in management decisions and future actions

Question: This may sound a bit harsh, but I’d like to ask about the comments made by the talents who have left the company and the accounting issues that have come to light. From your perspective as president, was there an underlying optimism that led to this outcome? If you were indeed too optimistic and have reflected on that, could you please tell us what steps you intend to take in the future?

Tanigo: As you pointed out, we acknowledge that there were aspects in which our outlook may have been overly optimistic. We also recognize that, in line with market growth, we prioritized the allocation of resources more toward offensive initiatives than defensive measures.

Simultaneously, in preparation for the measures we announced here, we have been reviewing our inventory management since last fiscal year. We are taking the current situation seriously and have been working since last fiscal year to strengthen our foundation so that we can become a company capable of achieving steady growth once again. This fiscal year, building on that foundation, we plan to take steps such as hiring new talent. We intend to move forward with this approach.