Business Briefing on April 20, 2026

Shiro Tomiyasu (hereafter, Tomiyasu): I am Shiro Tomiyasu, Representative Director, Chairman & Executive Officer. Thank you for taking the time to join our business briefing today.

This is the first time we’ve held a meeting like this, and I’m very pleased that so many of you are able to attend. I would like to express my sincere appreciation for your continued guidance and support toward our IR activities.

Today’s topics are European business and domestic large-sized machinery. Each holds a material position in our medium- to long-term growth strategy and represents areas of particular interest in our discussions with institutional investors and analysts.

We would like to use this briefing as an opportunity to share our vision and direction for our medium- to long-term growth.

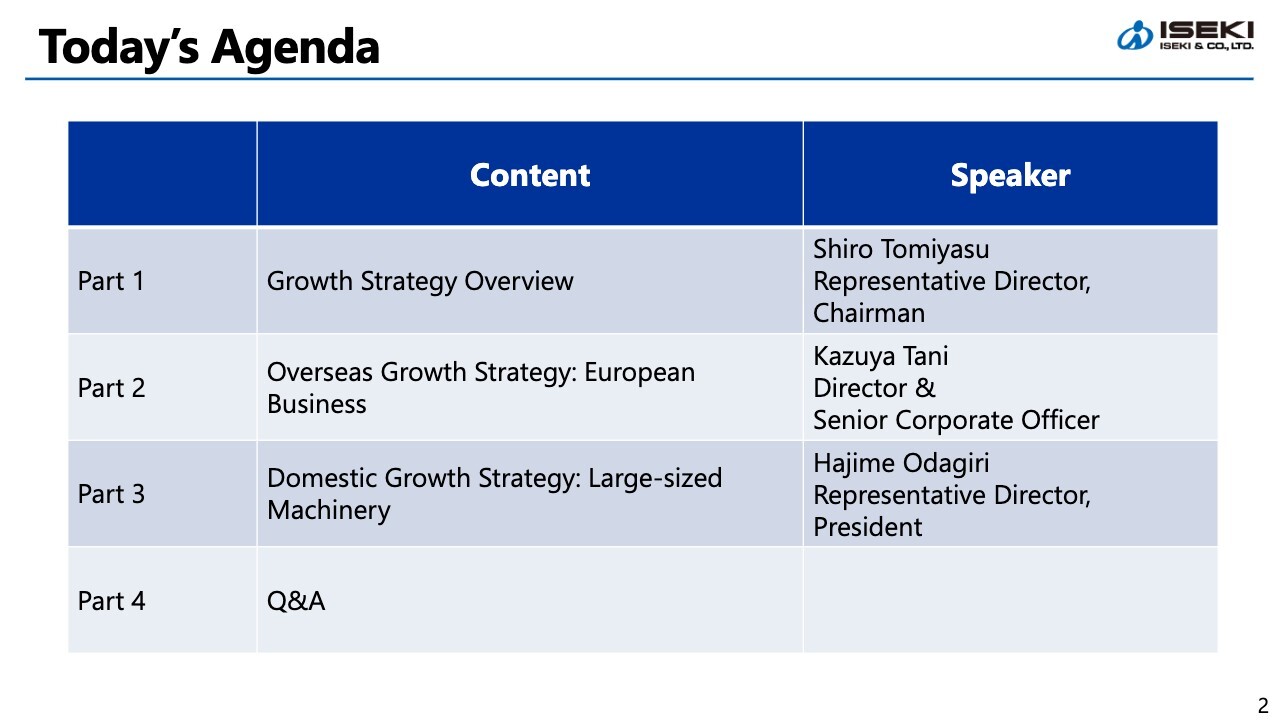

Today’s Agenda

Here is today’s agenda. First, in Part 1, I will provide an overview of the company. Next, in Part 2, Tani, Director & Senior Corporate Officer, will give a detailed presentation on our overseas growth strategy, with a particular focus on European business. Tani is in charge of Corporate Planning, Investor Relations, and Finance and previously served as General Division Manager, Overseas Business Division.

In Part 3, Odagiri, Representative Director and President, will discuss our domestic growth strategy, focusing on the large-sized machinery strategy. As you know, he assumed the role of President at the end of March, continuing to lead Project Z.

I hope this will serve as a valuable opportunity for dialogue regarding ISEKI’s next phase of growth. While time is limited today, please join our discussion.

Introduction

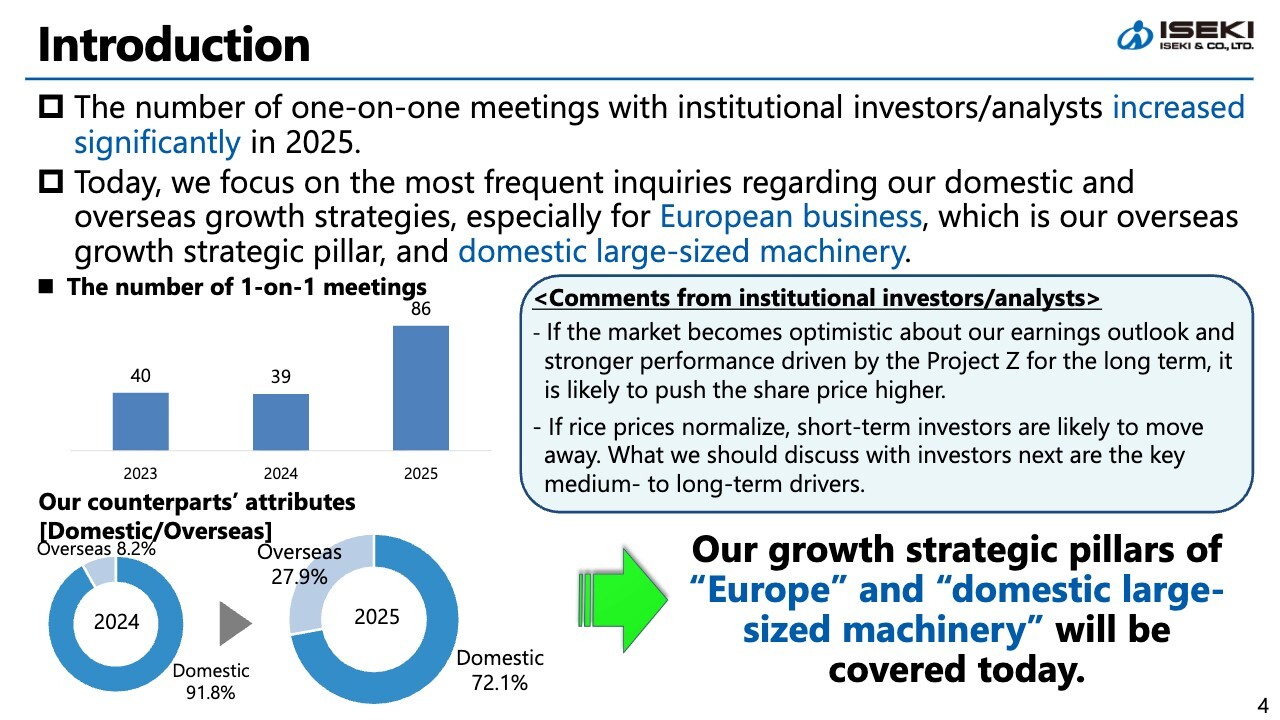

Let’s now move on to the overview of Part 1. First, I’d like to explain where we should place this briefing in our IR activities. Compared to previous years, the number of one-on-one meetings with institutional investors/analysts increased significantly in 2025.

While we appreciate that you have a certain level of understanding regarding our recent performance improvements and structural reforms, we have received a lot of feedback: what we should discuss with investors next are the key medium- to long-term drivers, and how we see growth evolving beyond Project Z.

Today, based on these discussions, I will discuss two key pillars of our growth strategy. Specifically, these are our European business—the core of our overseas growth strategy, and our large-sized machinery strategy, the cornerstone of our domestic growth strategy.

We aim to convey not only short-term changes in the market environment but also our plan to enhance corporate value from a medium- to long-term perspective.

ISEKI’s Growth Story –Project Z–

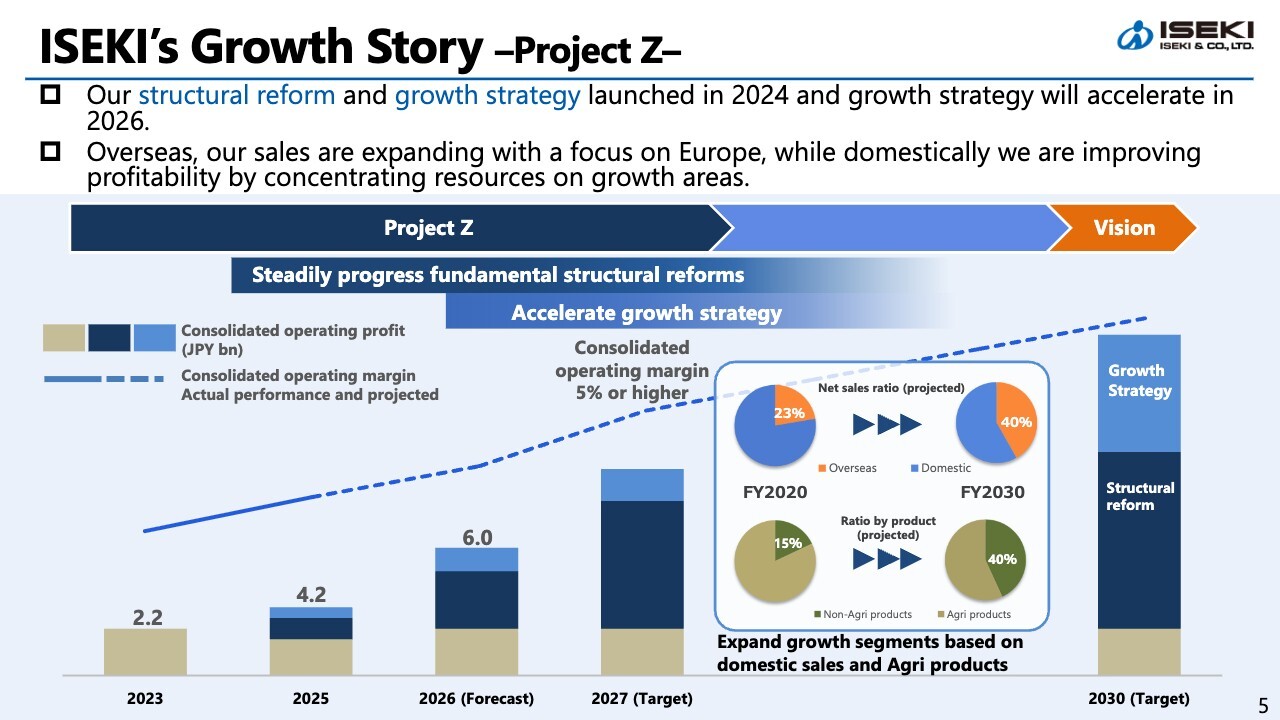

I would like to explain Project Z, our growth story. Project Z is an initiative to simultaneously advance fundamental structural reforms and execute growth strategies from 2024 through 2027 and toward 2030.

Starting in 2024, we are prioritizing structural reforms through a short-term, high-intensity approach. We are reviewing the company’s foundational areas, including production, development, sales, and human resources, to transform into a robust corporate structure. In this project, I am advocating for a complete overhaul of every aspect of our operations: design, production, sales, service, and administration.

Building on the results of these reforms, we will transition to a phase where our growth strategy is fully implemented starting in 2026. We will lay the groundwork from 2024 to 2025, and from 2026 onward, we will shift our focus to growth.

We will expand sales overseas, primarily in Europe, and improve profitability domestically by focusing on growth sectors. This is the growth direction outlined by Project Z.

Progress of Project Z

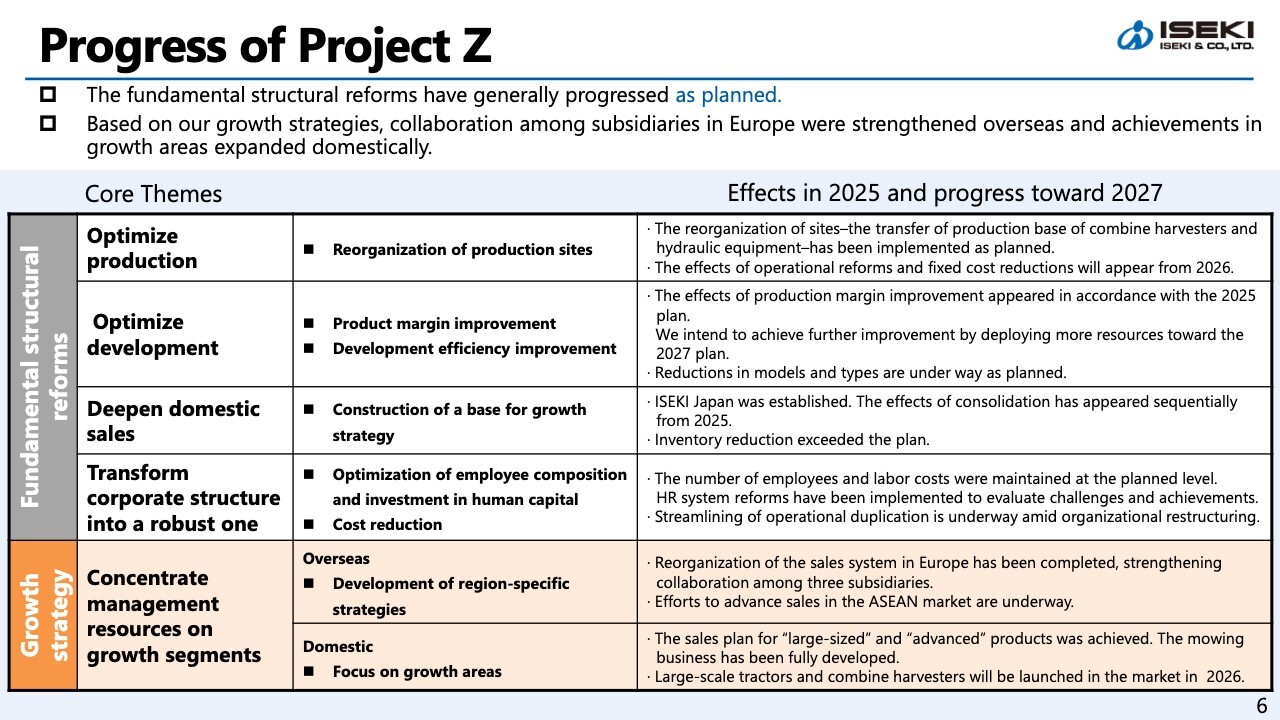

I would like to report on the progress of Project Z. First, the fundamental structural reforms have generally progressed as planned.

On the production front, we steadily consolidated and transferred production sites for combine harvesters and key components. We gradually began combine harvester production in Matsuyama starting last month (March). We expect the benefits of this improvement in our profit structure to appear progressively from 2026 by simultaneously increasing production efficiency and reducing fixed costs.

On the development front, while there have been some delays in product margin improvement, we are working to make improvements by expanding the scope of our initiatives. The benefits of these improvements began to emerge gradually in 2H of 2025, and we will continue our efforts toward achieving our 2027 target.

In terms of development efficiency improvement, we are proceeding as planned with the consolidation of models and types and the promotion of common design, while allocating development resources more intensively to growth areas.

To deepen domestic sales, we established ISEKI Japan in January 2025 and integrated our sales structure. As a result, we were able to reduce inventories more than planned, which has significantly contributed to improved cash flow. We are also proceeding with a shift in personnel to support growth.

Through these reforms, we are positioning ourselves to shift from a defensive to a more proactive stance. Let me now walk you through an overview of our growth strategy on the next page.

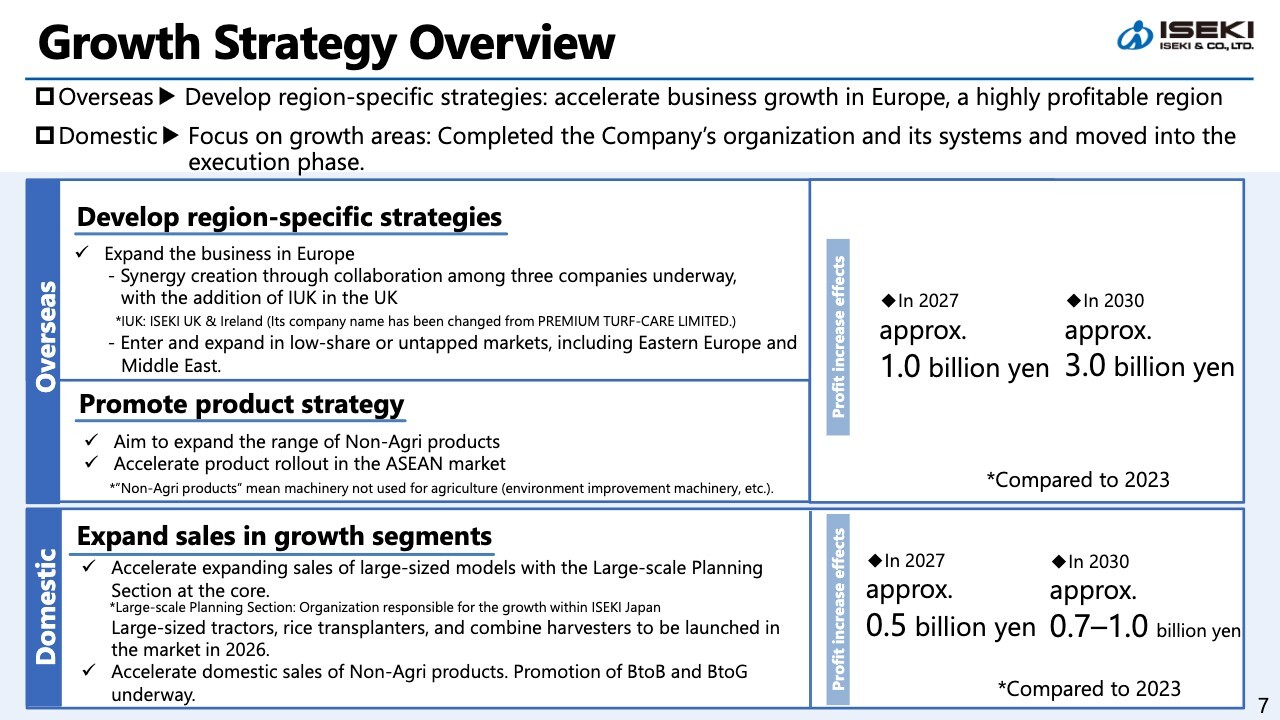

Growth Strategy Overview

Overseas, we will expand our highly profitable business in Europe while also advancing business expansion in emerging markets, particularly in ASEAN, where long-term growth is anticipated.

In Europe, in particular, ISEKI France and ISEKI Germany, together with ISEKI UK & Ireland (ISEKI UK), which was consolidated in 2025, are collaborating to promote integrated sales and inventory management, broadening the product range, and expanding the sales territory. We are currently advancing initiatives aimed at the second stage of growth in Europe.

In the domestic business, we are concentrating management resources on growth areas of large-sized products, advanced products, dry field farming, and environmentally friendly products as well as Non-Agri (non-agricultural) products. The Large-scale Planning Section, established within ISEKI Japan, serves as the central hub for our product and sales strategies, and we are steadily expanding our business results. Based on this, we have designed a strategy to incrementally build earnings through 2027 and toward 2030.

Crucially, our goal is not excessive pursuit of sales volume, but rather growth that enhances profit margins and cash generation capabilities.

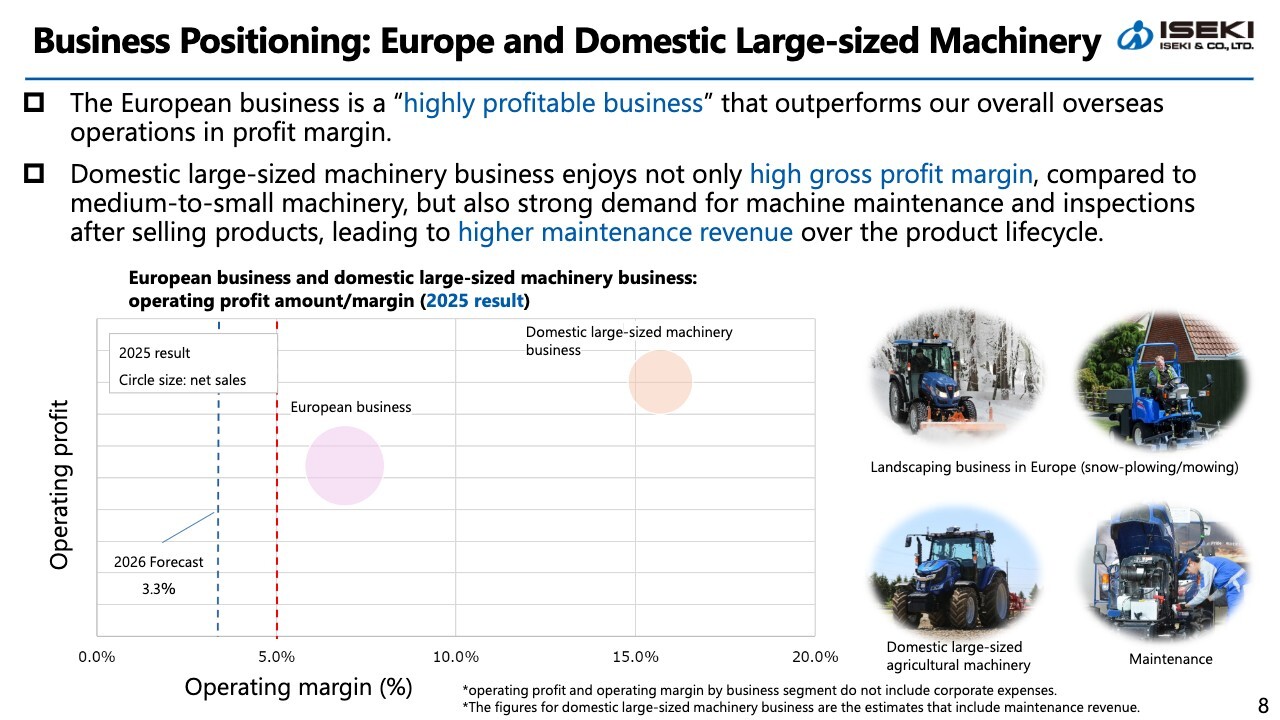

Business Positioning: Europe and Domestic Large-sized Machinery

Now, let me clarify the positioning of the two businesses we will discuss today. The European business is a highly profitable business with the highest operating margin across our overseas operations. Furthermore, its growth over the past few years has been exceptionally strong.

On the other hand, domestic large-sized machinery business enjoys not only high product gross profit margin, but also strong demand for machine maintenance and inspections after selling products, generating revenue over the product lifecycle. This domain can be considered a growth area within the domestic market.

What both businesses have in common is that they have high profit margins and will continue to generate cash while sustaining growth. Today, I will explain these two businesses in detail as ISEKI’s medium- to long-term growth drivers.

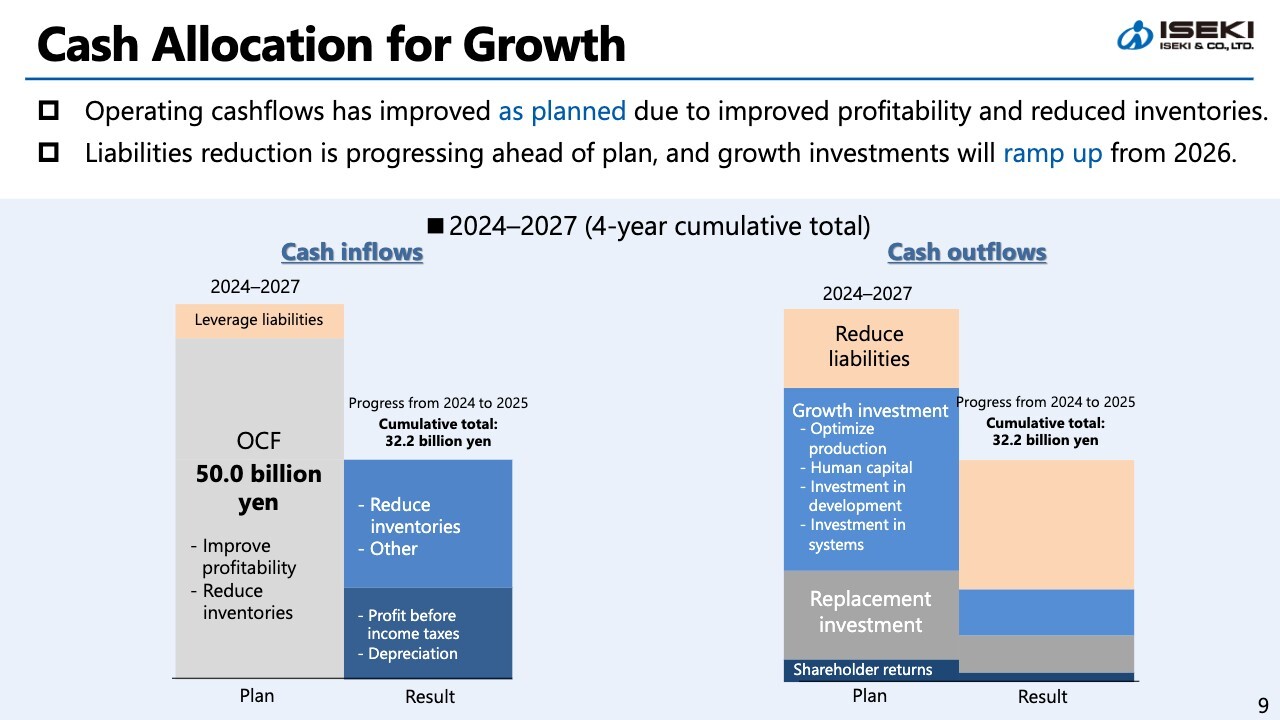

Cash Allocation for Growth

My final point concerns cash allocation. Operating cash flow has improved as planned due to improved profitability and reduced inventories. Additionally, liabilities reduction is progressing at a pace exceeding our plan. As a result, we are establishing a financial structure that will allow us to fully ramp up growth investments from 2026.

Growth investments centered on optimizing production are scheduled to peak in 2026 and 2028. We believe that the crux lies in continuing to improve operating cash flow and reduce inventory to keep liability growth in check.

In addition, we will also be mindful of maintaining a balance with returns to our shareholders, while allocating funds to growth investments.

That concludes the overview of Part 1. Next, we will provide detailed explanations on European business in Part 2 and on our domestic large-sized machinery in Part 3.

Today’s Key Point(1)

Kazuya Tani (hereafter, Tani): Good afternoon, everyone. I am Tani, Director & Senior Corporate Officer. Thank you for taking the time to join us today despite your busy schedules. I would also like to take this opportunity to once again express my deep gratitude for your continued understanding and support of our Group’s business activities from a long-term perspective.

Now, let me explain our European business, which forms the core of our overseas growth strategy. Your attention is appreciated.

To start with the conclusion, the European business represents a business area where we can achieve both sales expansion and profit margin increase simultaneously. It will serve as a growth driver that boosts the overall profitability and shareholder value of our Group over the medium to long term.

There are three key drivers that will support our future growth. Currently, one of our primary markets is Western Europe. While we aim to further deepen our business presence there, we also intend to expand our geographic sales territory to include regions such as North Africa and the Middle East.

The second is our product strategy. In growth areas such as electric/robotic products —which the market demands— we will strive to enrich our product portfolio by introducing new offerings in a timely manner, regardless of whether they are manufactured in-house or by third parties.

The third is non-organic growth. In many cases, European companies often have an edge, particularly in areas such as the design know-how for electric products. We believe that building partnerships, including establishing new sales offices and making equity investments, is crucial for accelerating the expansion into these growth sectors.

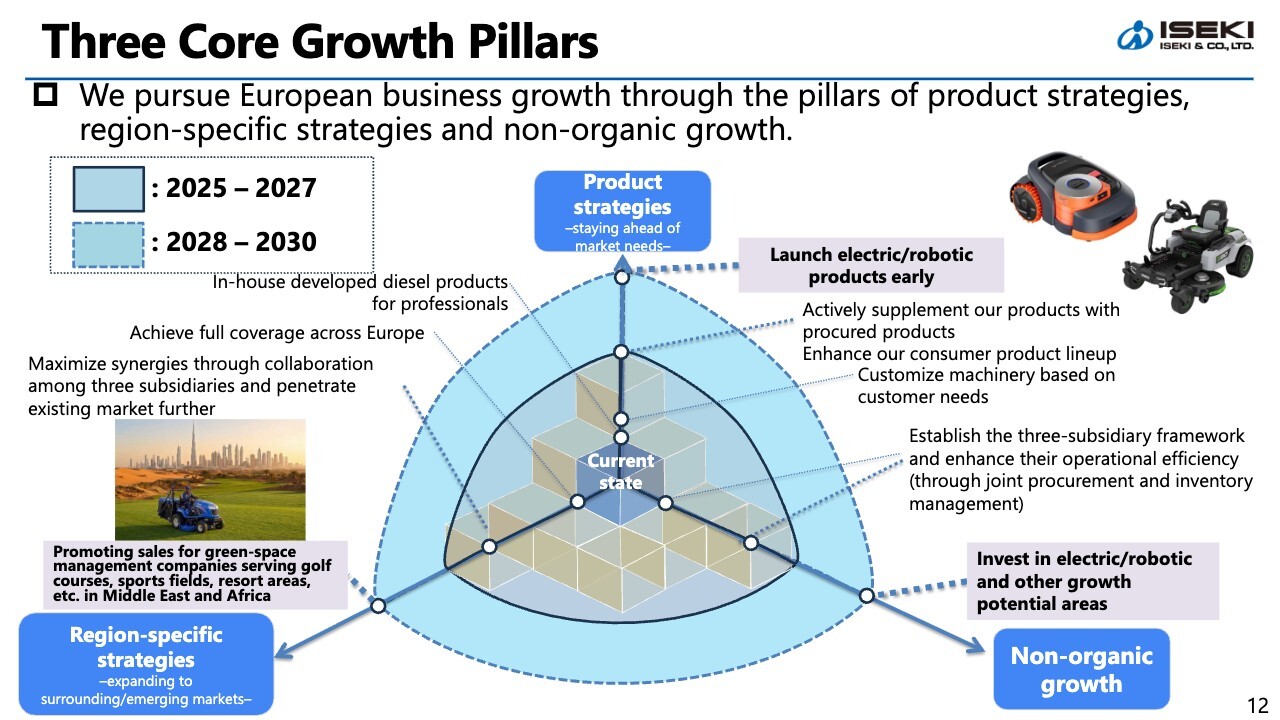

Three Core Growth Pillars

The diagram shown on the slide illustrates the three pillars supporting the growth of our European business, as I mentioned earlier. By advancing each of these growth pillars in a chronological sequence, we will solidify our presence in the European market and achieve sustainable growth in corporate value.

The first growth pillar is our region-specific strategies. After more than 50 years of operations, our sales network now achieves full coverage across Europe. Since 2014, we have acquired wholesale distributors in key markets through M&A, making them consolidated subsidiaries. Moving forward, building on our track record in Europe, we are expanding our reach to include golf courses and resort areas in the Middle East and Africa by 2030.

The second growth pillar is product strategies. Beyond selling our core, in-house developed diesel products and enhancing value through local customization, we have complemented our product lineup by actively utilizing sourced products. We will continue to pursue this direction while striving to expand our product lineup of electric/robotic products.

The third growth pillar is non-organic growth, namely our investment strategy. We are currently advancing the integration of the three sales companies we acquired to further enhance efficiency. Going forward, we will make strategic investments not only in distribution subsidiaries but also in areas with future growth potential, considering collaborations with local companies possessing technical expertise and capital alliances as needed.

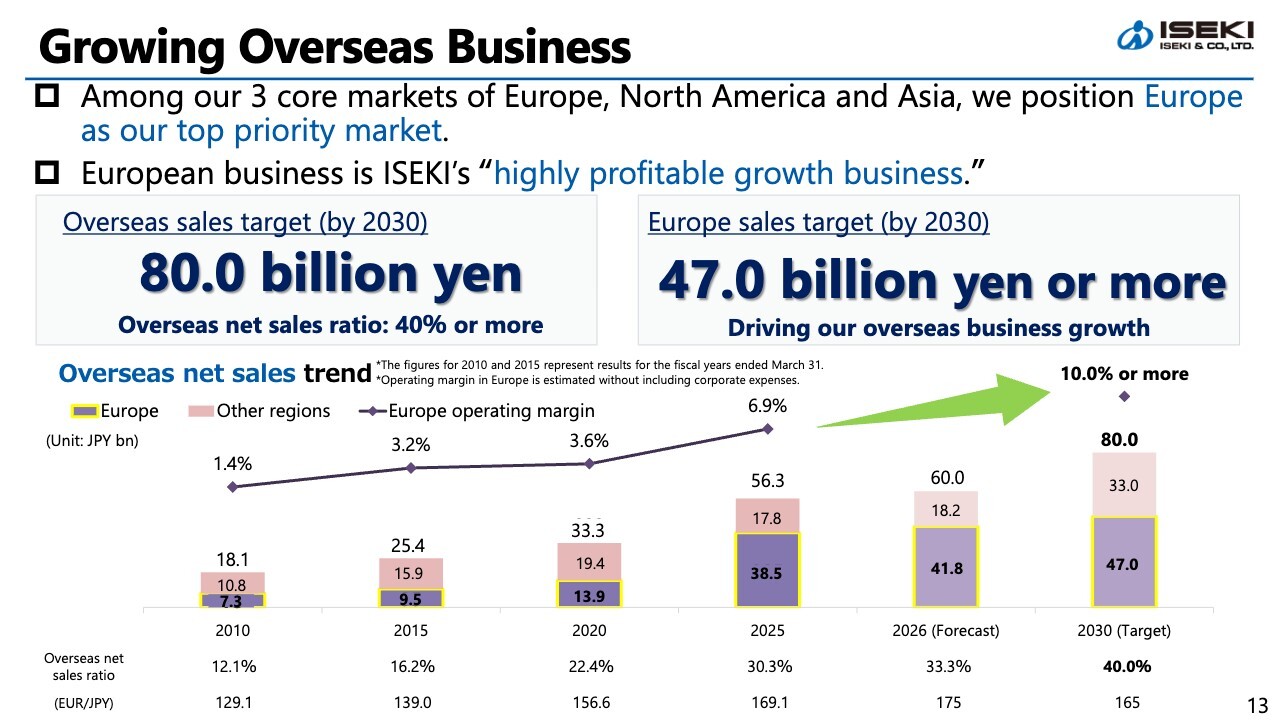

Growing Overseas Business

Here is the trend in overseas net sales. As shown on the slide, overseas net sales, which stood at 18.1 billion yen in 2010, are projected to reach 56.3 billion yen in 2025 and 80.0 billion yen in 2030.

We develop our overseas business in three regions: Europe, North America, and Asia. Among these, we position Europe as our top priority market. As shown on the slide, European business is not only expanding in net sales but also continuously improving its operating margin, and has now grown into a business capable of targeting an operating margin exceeding 10%.

Looking ahead to 2030, our targets are 80 billion yen in overseas net sales, an overseas net sales ratio of 40% or more, and at least 47 billion yen of that in Europe. We hope you understand that Europe is the core driver that will lead the growth of our entire overseas business going forward.

European Business: Its History and Landscaping Market

Here is a brief overview of the history of our European business. Our European business began in the 1960s with the sale of tillers. True to our name, our goal was to expand our agricultural machinery business. However, the average farm size in Europe was vastly different from that in Japan ; consequently, we were unable to capture significant demand for agricultural machinery.

Nevertheless, our products were well-regarded for their high durability and performance. In particular, we found that they were well-suited for tasks requiring daily use, such as cleaning, snow plowing, and mowing in parks.

Since then, our reputation has continued to grow, and the ISEKI brand has become established among local governments and the contractors working with them. A few years ago, the Japan Times featured an article about us, noting that their machines showcased their own strength, leading to business expansion.

Please note that we translate the term “landscape” in the fields known as municipal business, park business, and landscape business literally as landscaping business.

European Business is ISEKI’s “Highly Profitable Growth Business”

We have gained strong trust in the landscaping market in Europe and established our European business as a robust core business that generates high profits and holds a top-class market share (estimated at 20–30%).

Our European business has three key strengths. The first is our sales and management structure, supported by three consolidated subsidiaries. This structure enables us not only to swiftly implement our sales strategies but also to advance efficient operations.

The second is our strong sales network. ISEKI France, ISEKI Germany, and ISEKI UK have each built extensive, high-performing dealer networks based on long-standing relationships of trust with local dealers.

The number of dealers stands at 200 or more for ISEKI France; 150 or more for ISEKI Germany; and 100 or more for ISEKI UK. Furthermore, when including sub-dealers, ISEKI France and ISEKI Germany have sales networks of over 1,000 dealers.

The third is our customization capabilities. ISEKI Germany possesses customization functions based on sophisticated technical expertise, and has earned strong trust from professional users through customizations tailored to country- and region-specific needs.

As you can see in the photo on the right side of the slide, the parts that attach implements to the front of the tractor, as well as the cabins, are customized by ISEKI Germany based on its advanced technical expertise.

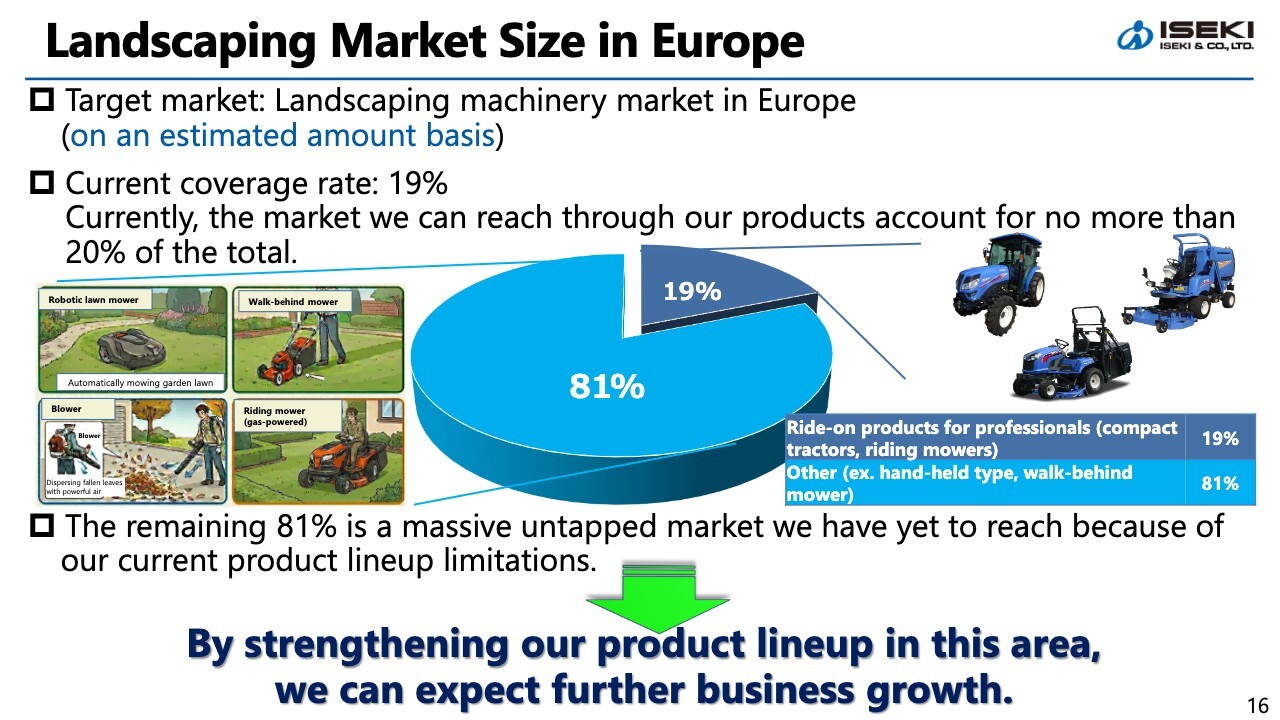

Landscaping Market Size in Europe

The pie chart in the slide illustrates the overall European landscaping market and the scope covered by our products. This is an illustration based on industry figures from various countries.

Currently, our in-house designed and manufactured products cover only about 19% of the total market. The remaining approximately 81% consists of areas not covered by our product lineup such as hand-held type and walk-behind machines.

This means the existing market still has significant room for growth. We plan to supplement the remaining areas through externally sourced products and joint development, and leverage our strong dealer network to expand our business.

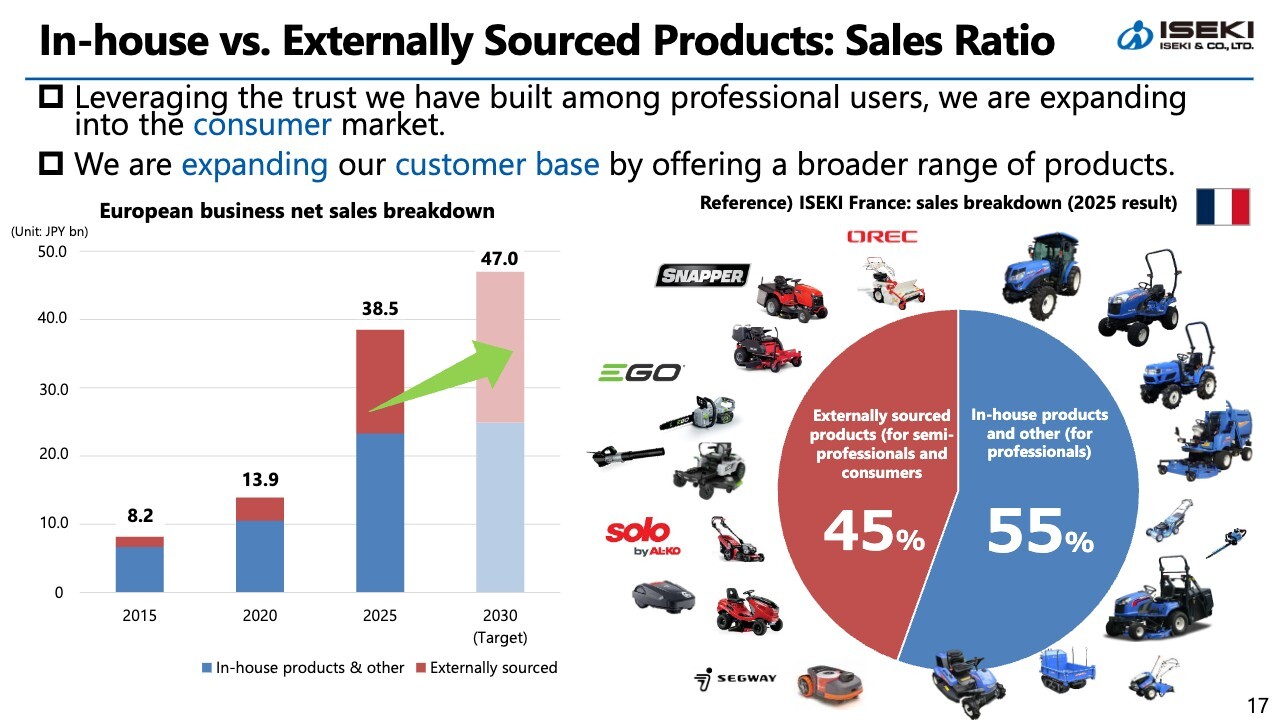

In-house vs. Externally Sourced Products: Sales Ratio

This chart shows the sales ratio of in-house products versus externally sourced products. The pie chart on the right side of the slide illustrates the sales breakdown for ISEKI France.

As you can see, while focusing on in-house products, we combine them with externally sourced products to target not only professional users but also semi-professional users and consumers. Wholesale companies are expanding their customer base by leveraging brand recognition of ISEKI as a subsidiary.

Furthermore, we have achieved stable revenue growth by enriching our product portfolio. Going forward, we will promote joint purchasing among our three European subsidiaries while simultaneously advancing the development of successful models across Europe.

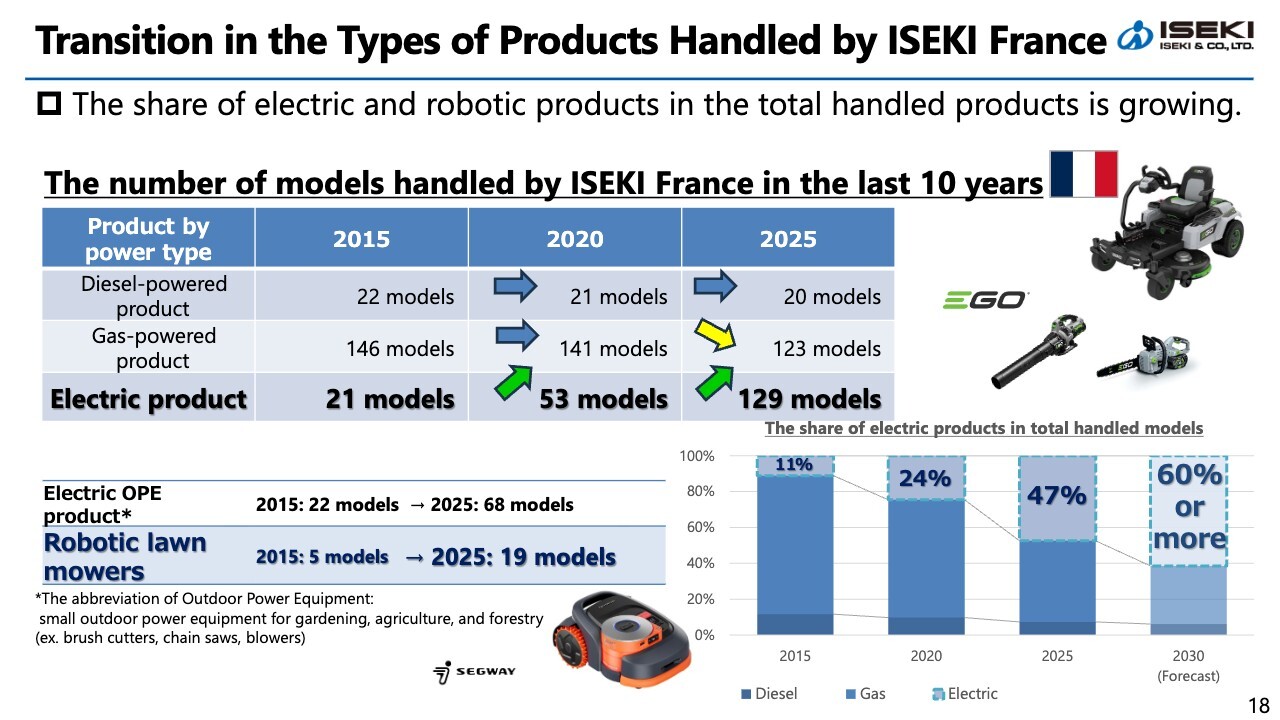

Transition in the Types of Products Handled by ISEKI France

This is about the expansion of electric and robotic products. We highlight ISEKI France as an example. Over the past decade, the number of models handled by ISEKI France has increased significantly. While diesel-powered products have remained largely flat and gas-powered products have declined slightly, the number of electric product models expanded from 21 to 129.

Electrification is gaining recognition not only for its compliance with environmental regulations but also for its noise reduction and labor-saving benefits. We anticipate that the electric and robotic fields will continue to expand further in the European market.

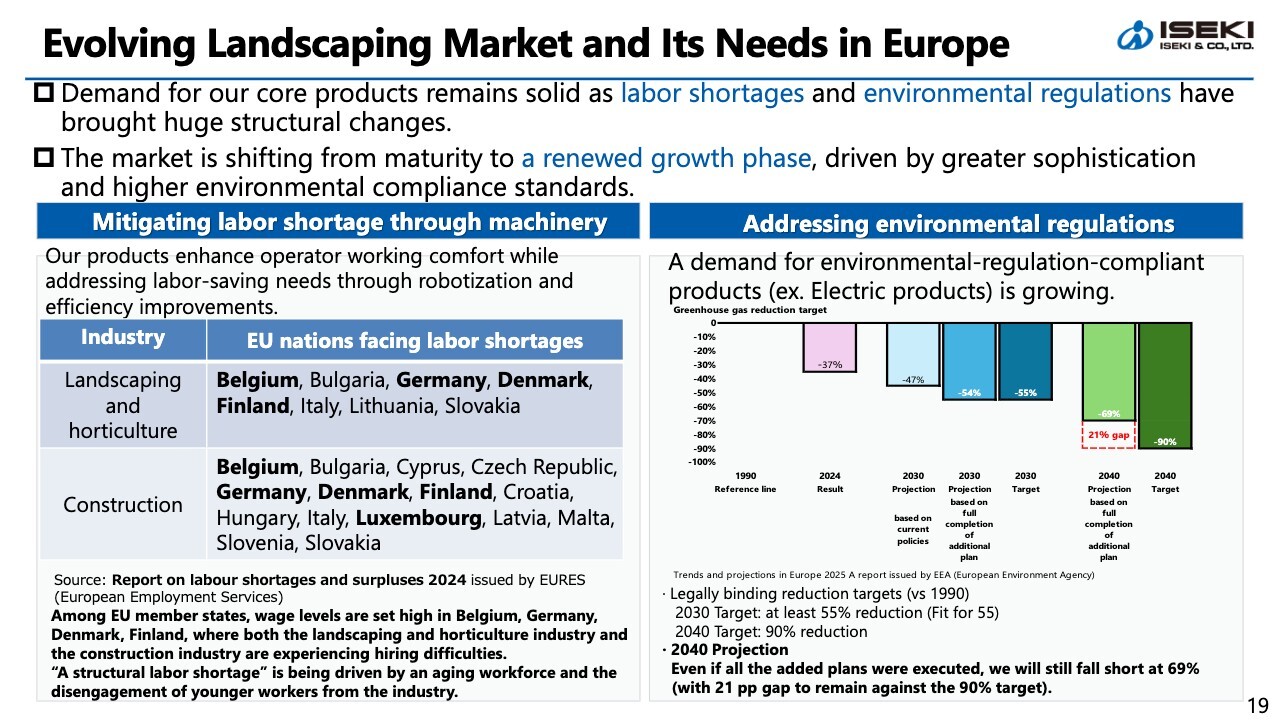

Evolving Landscaping Market and Its Needs in Europe

The European market is undergoing structural changes characterized by labor shortages and stricter environmental regulations. Countries with high labor costs, in particular, have a very strong demand for labor-saving measures and robotization. They are accelerating their shift toward electric products that are easier to comply with environmental regulations.

We view these changes not as temporary, but as a sign that the market is re-entering a growth phase. This environment directly translates our strengths into growth opportunities.

Growth Pillar (1) Region-specific Strategies: Deploying for Existing and New Markets

This is our region-specific strategy. In existing markets, we will promote efficiency and high value-added services through collaboration among the three companies to improve profitability.

Meanwhile, we are advancing into new markets in the Middle East and Africa. This region boasts a significant number of landscaping markets for professionals, such as golf courses in the Middle East and resort facilities around Agadir in western Morocco. This is a sector expected to continue growing in the future.

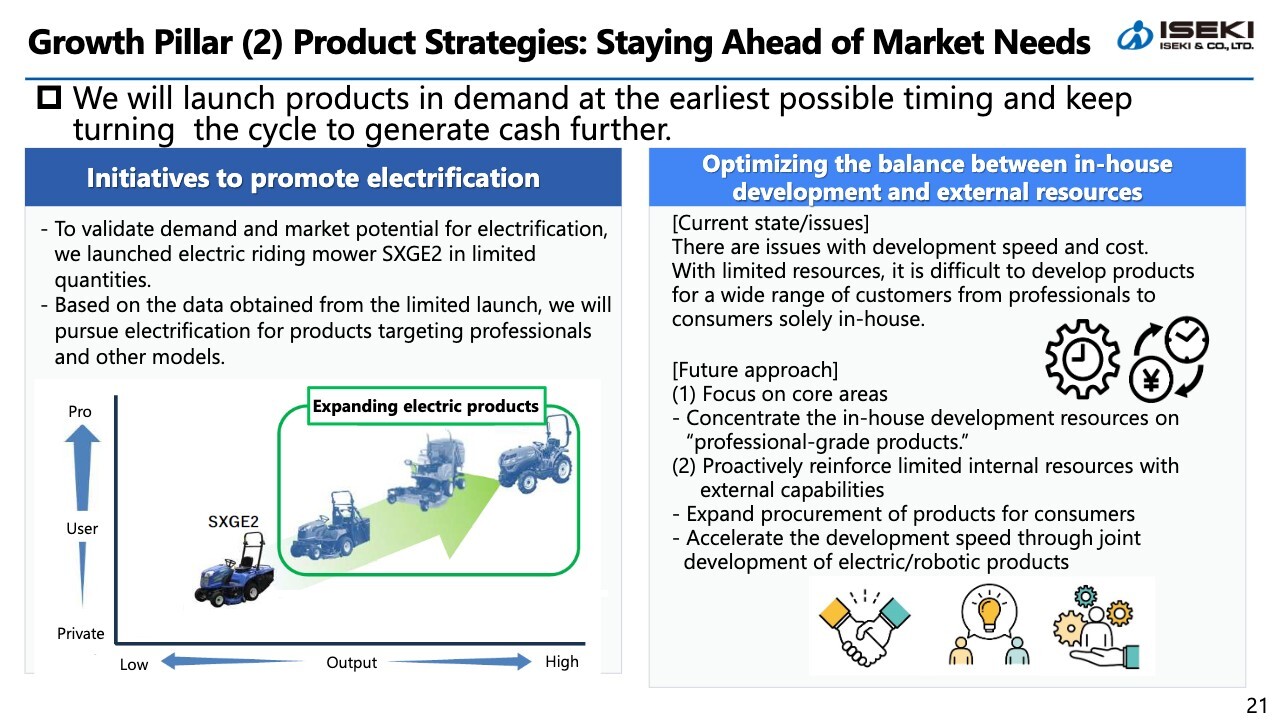

Growth Pillar (2) Product Strategies: Staying Ahead of Market Needs

This is about our product strategy. Rather than manufacturing everything in-house, we combine concentration on our core areas with the utilization of external resources. For professional-grade products, we will leverage our advanced technological capability to drive development that leads the industry.

In other areas, we will reinforce our capabilities with procurement and joint development, while also considering the use of external resources. To this end, we are also considering the possibility of forming capital alliances as needed. In any case, we aim for further growth in our core markets and will build a structure capable of addressing market needs in the fastest manner.

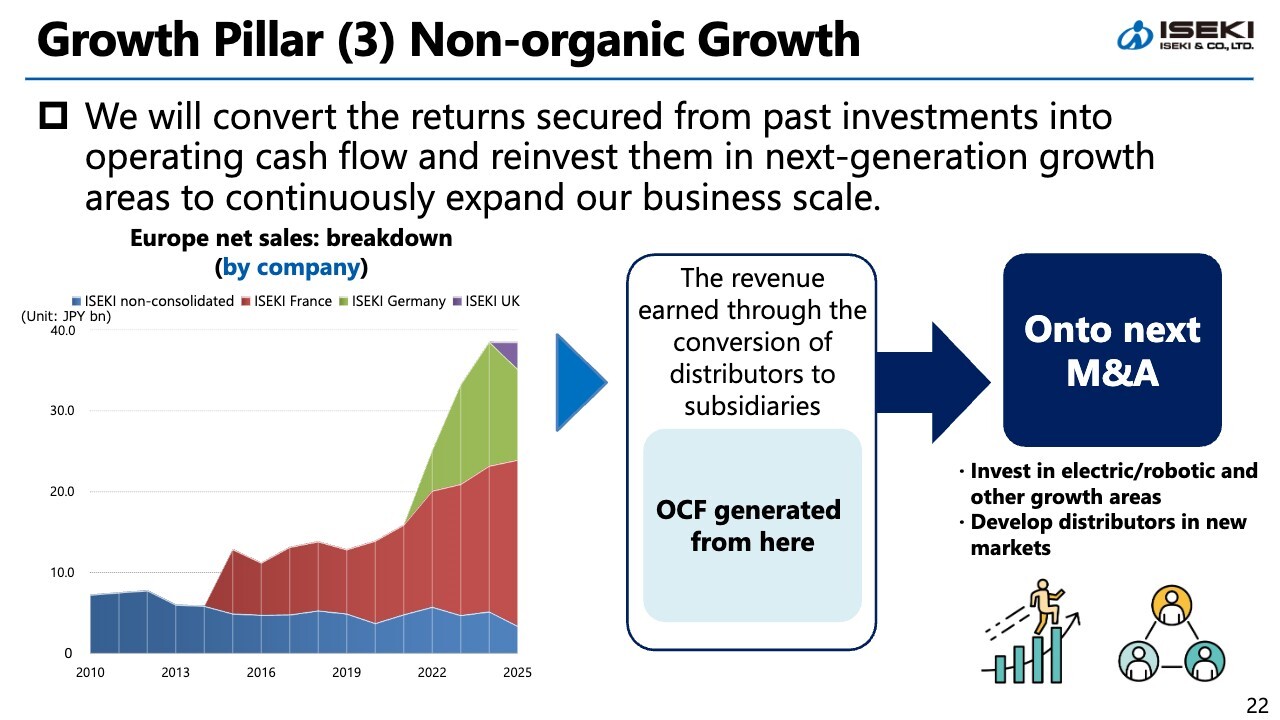

Growth Pillar (3) Non-organic Growth

Here is non-organic growth. To date, on the sales front, we have steadily and rapidly expanded our European net sales by converting distributors to subsidiaries through M&A. Furthermore, by incorporating local service revenue through these acquisitions, we have also improved groupwide profitability.

We will continue to steadily raise both our business scale and profitability by maintaining a cycle of reinvesting the cash generated from past investments into the next growth areas.

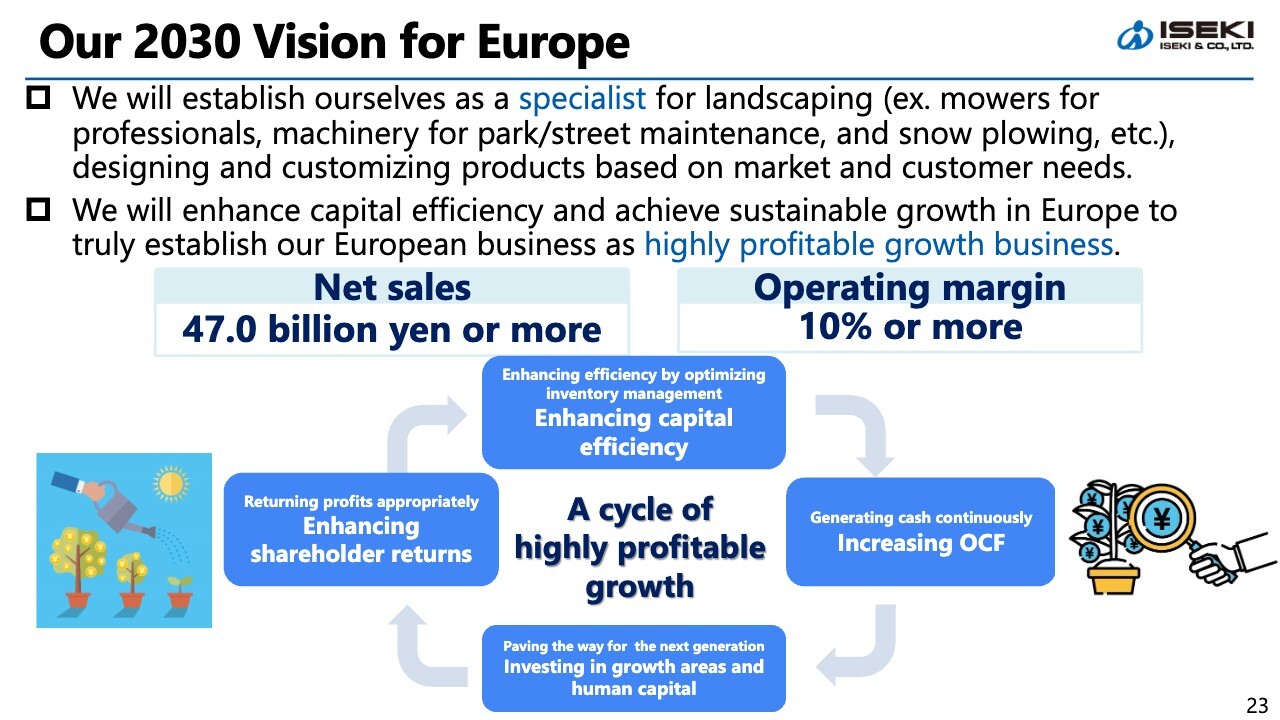

Our 2030 Vision for Europe

Here is our vision for our European business in 2030. We aim to achieve net sales of 47.0 billion yen or more and operating margin of 10% or more.

We will evolve our European business into a core business that generates a cycle of highly profitable growth, positioning it as a specialist in the landscaping field. By reinvesting the cash generated into next-generation growth areas and human capital, we will enhance the value of the entire ISEKI Group.

That concludes our presentation on our European business. Thank you for your attention.

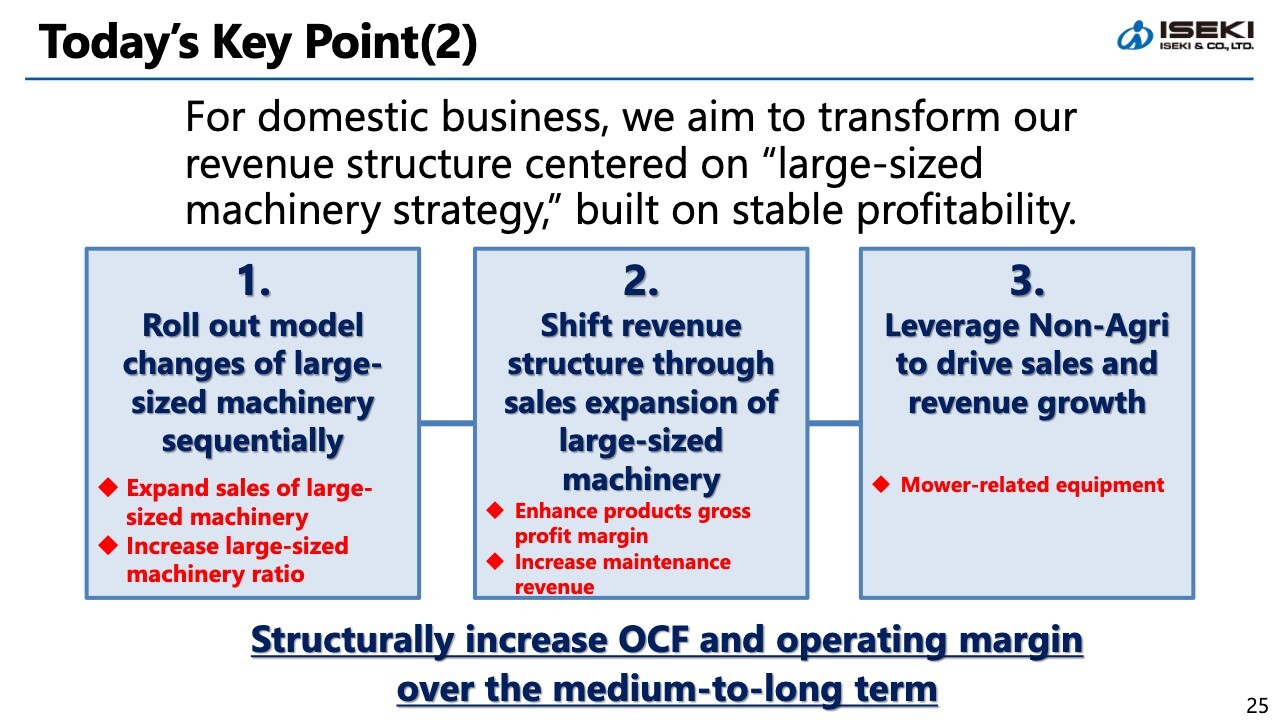

Today’s Key Point(2)

Hajime Odagiri (hereafter, Odagiri): Good afternoon, everyone. I am Odagiri, Representative Director and President. In Part 3, I will explain our domestic growth strategy, with a particular focus on our domestic large-sized machinery strategy.

At first glance, the domestic business appears to be a mature market where sales volume is difficult to predict. However, we believe that this is a sector where further growth and improved profit margins are possible by concentrating our management resources on growth areas and transforming our revenue structure. Today, I will explain our approach and initiatives in this regard.

Let me begin by highlighting three key points I would like to share today. The first is to roll out model changes of the large-sized machinery sequentially to enhance product competitiveness and expand sales of the large-sized machinery with our sales capabilities centered on the integration of our sales system as our foundation.

The second is to shift revenue structure of the domestic business through sales expansion of the large-sized machinery. The large-sized machinery not only has a high product gross profit margin but also generates revenue throughout its entire lifecycle, including post-sale maintenance revenue.

The third is to leverage Non-Agri to drive sales and revenue growth. We see this as an initiative to deploy products in the landscaping sector, which has already proven successful in Europe, to the domestic market, and develop it as another pillar of revenue over the medium to long term.

Centering on these three points and transforming our revenue structure built on stable profitability, we will structurally increase operating cash flow and operating margin over the medium to long term.

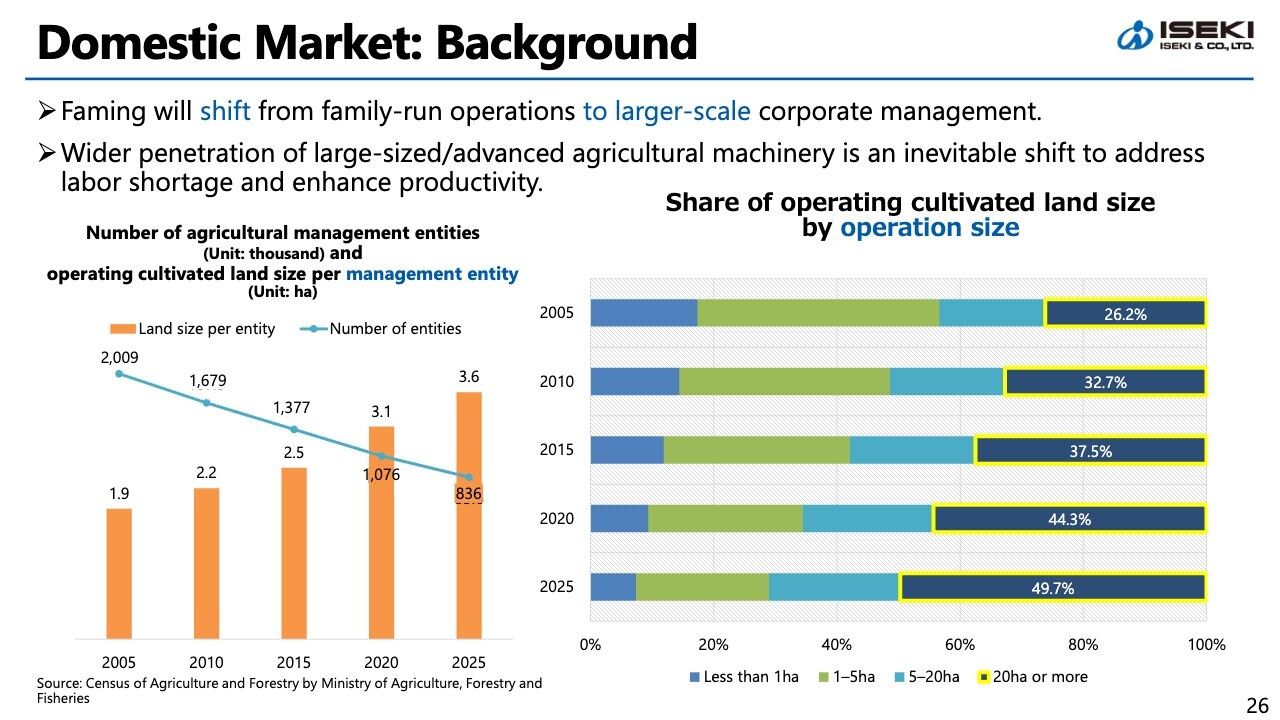

Domestic Market: Background

Here is some background on the domestic market. Japanese farming is undergoing a structural shift from family-run operations to large-scale operations managed by corporations or community-based farming groups. As shown in the graph on the left side of the slide, while the number of agricultural management entities is decreasing, the land size per entity is steadily increasing.

Given this situation, addressing labor shortages and enhancing productivity are unavoidable challenges from the perspective of food security. We believe that expanding the adoption of large-sized/advanced agricultural machinery is inevitable to resolve these issues.

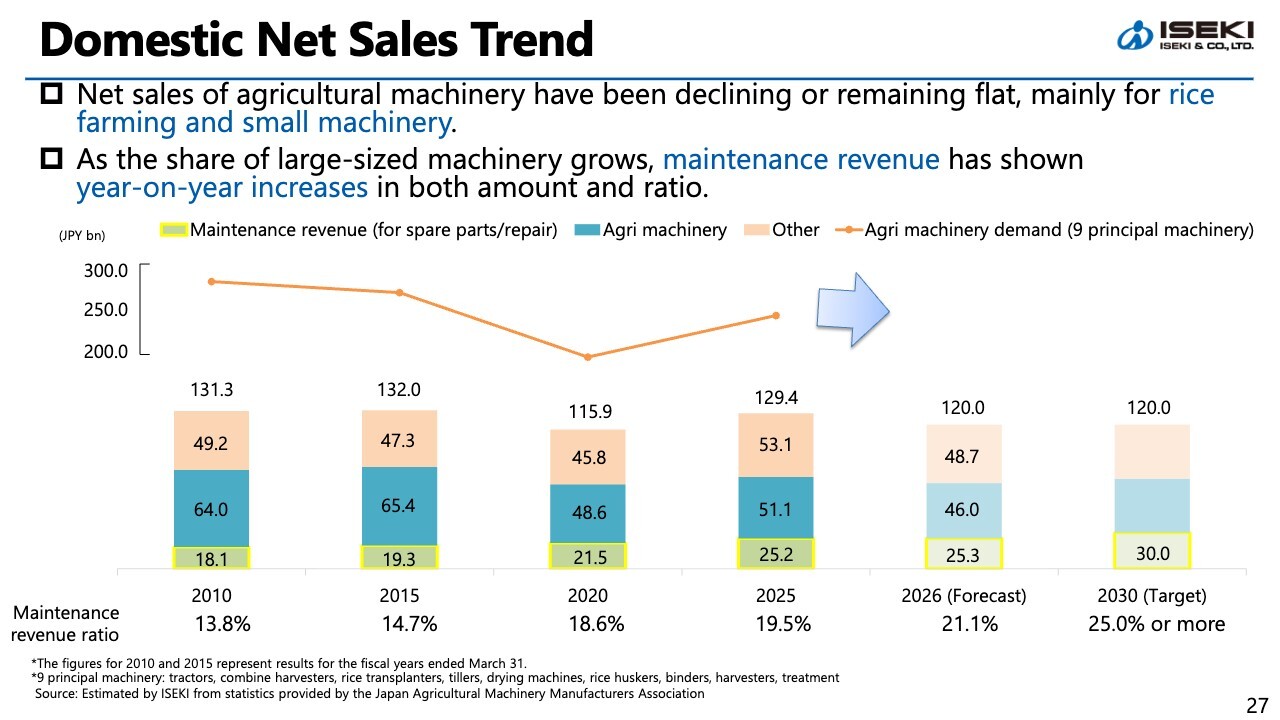

Domestic Net Sales Trend

Here is the domestic net sales trend. Net sales of agricultural machinery have been declining or remaining flat, mainly for rice farming and small machinery. On the other hand, a trend worth noting is that of maintenance revenue. As shown at the bottom of the graph on this slide, maintenance revenue has been steadily increasing in both amount and ratio.

The maintenance revenue ratio stood at 13.8% in 2010 and reached 19.5% in 2025. Our target is to exceed 25% by 2030. This trend forms the foundation for the transformation of our domestic business revenue structure.

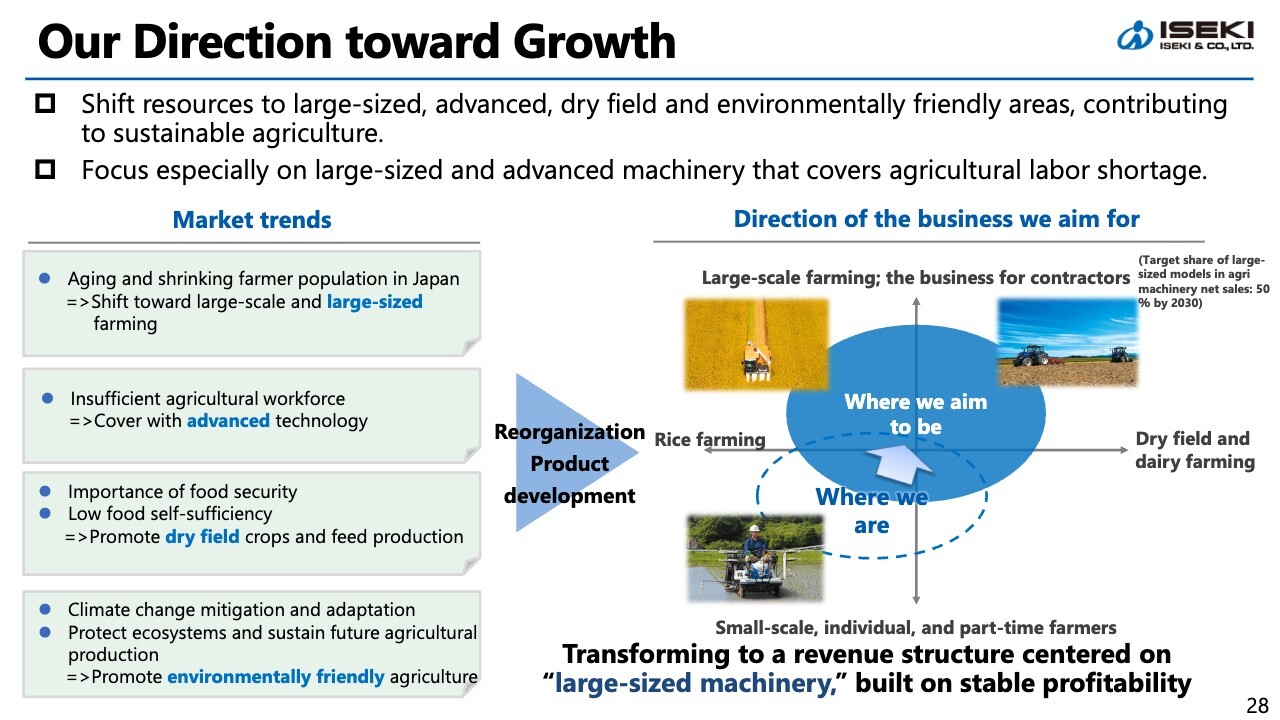

Our Direction toward Growth

Against this backdrop, we will initially shift our management resources toward growth areas: large-sized, advanced, dry field, and environmentally friendly. In particular, we will strive to transform to a revenue structure built on stable profitability by centering on large-sized farming.

We will also contribute to enhancing agricultural productivity by expanding sales of the large-sized machinery, while building a stable and sustainable revenue structure that includes maintenance revenue.

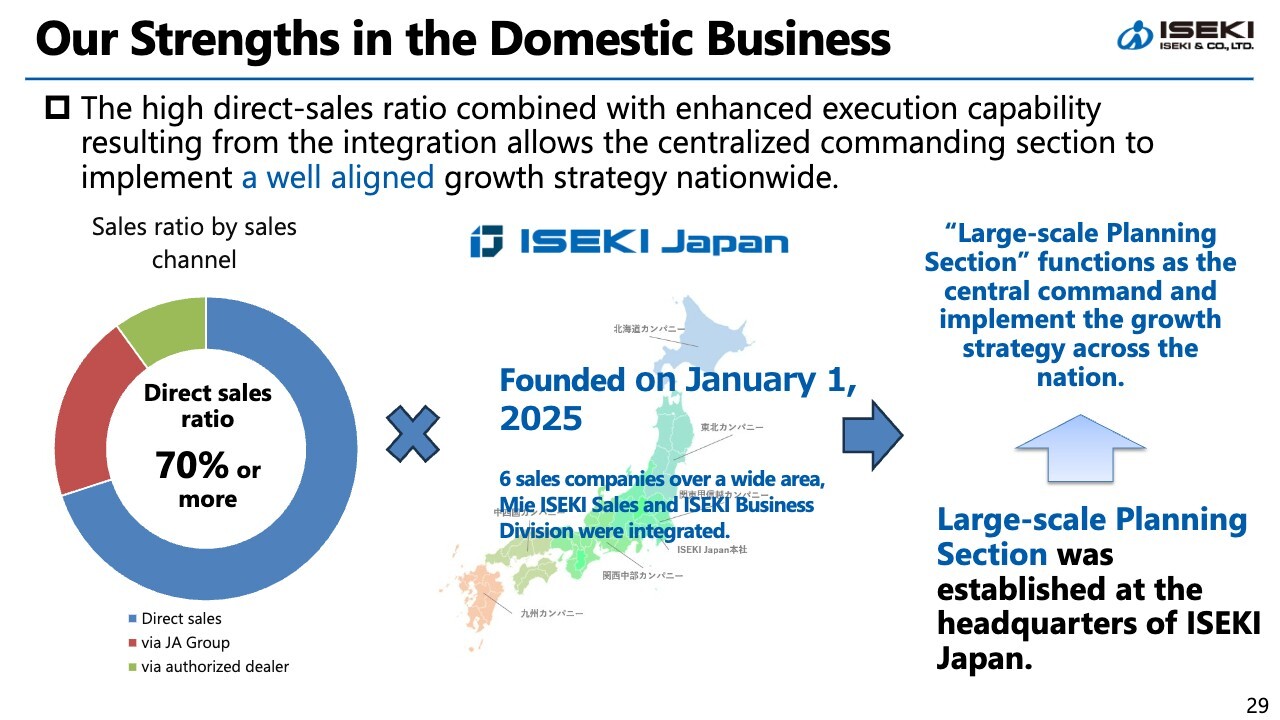

Our Strengths in the Domestic Business

Let me explain our strengths in the domestic business. Our greatest strengths lie in our high direct-sales ratio combined with enhanced execution capability resulting from the integration of sales companies. In 2025, we established ISEKI Japan, integrating six sales companies over a wide area, Mie ISEKI Sales, and ISEKI’s Business Division function.

Furthermore, we established a Large-scale Planning Section within ISEKI Japan to serve as the central command, building a structure capable of executing a disciplined growth strategy on a nationwide basis. With a direct sales ratio exceeding 70%, our ability to directly reflect customer needs in our products and initiatives is a major strength.

Approach to Large-scale Farmers

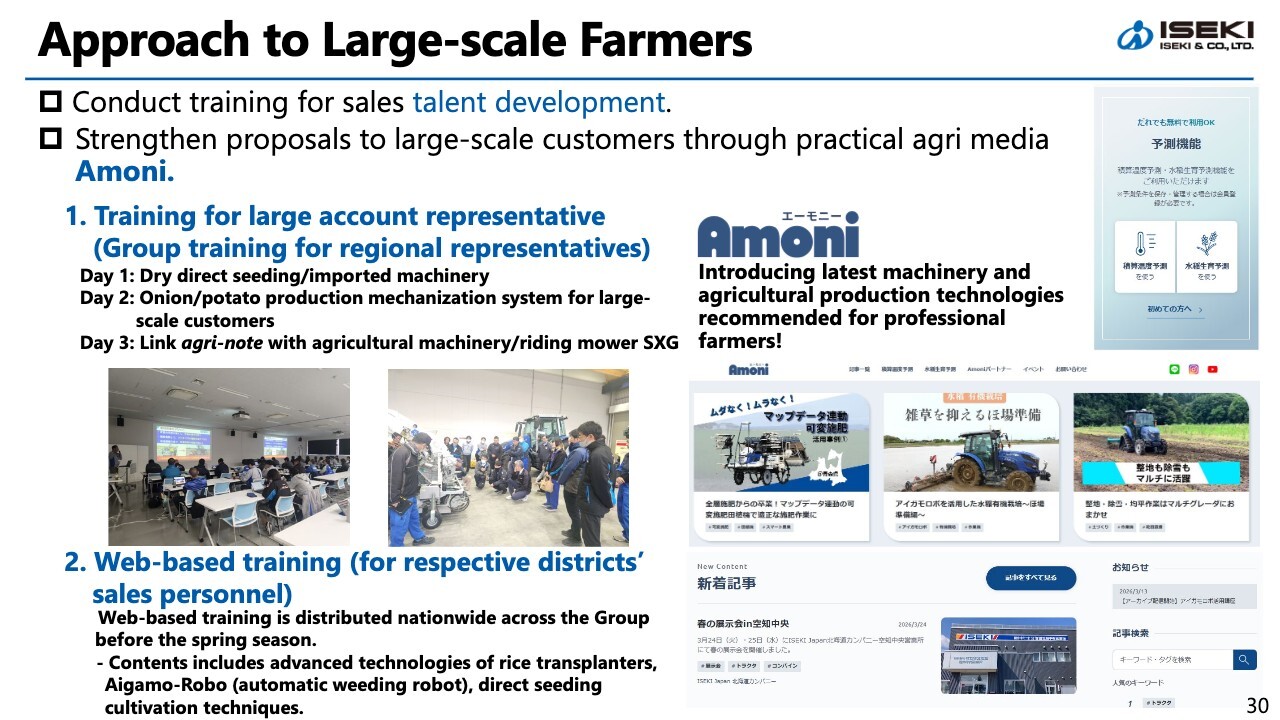

To expand sales of large-sized machinery, sales talent development and strengthening solution capabilities to customers are also critical. We are currently providing sales training for representatives serving large-scale farmers through group training or web-based training. Moreover, we are utilizing Amoni, a practical agricultural media platform, to enhance our solution capabilities combining latest machinery and agricultural production technologies.

Amoni is a website launched in 2021 with the aim of becoming a platform where large-scale farmers gather. Focusing on labor-saving and cost-reduction, we deliver content covering both hardware (such as agricultural machinery) and software (such as cultivation techniques), working to build a more user-friendly “space” that attracts people.

We aim to provide value not merely as a machinery seller, but as a partner supporting the entire farm business.

Large-sized Machinery Model Change

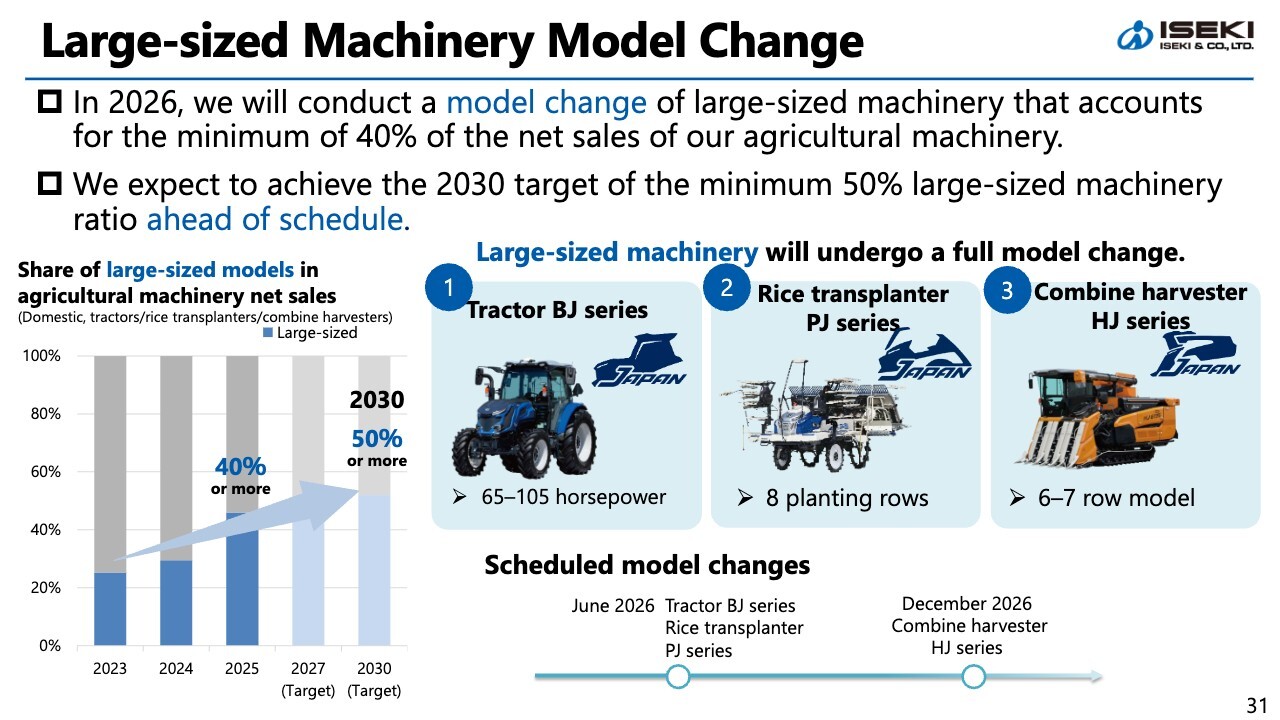

Here is the large-sized machinery model change. In 2026, we will conduct a full model change of large-sized machinery that accounts for the minimum of 40% of the net sales of our agricultural machinery. First, we plan to sequentially introduce new models of the three main product lines : Tractor BJ series in JAPAN Series; Rice transplanter PJ series; and Combine harvester HJ series.

As a result, we expect to achieve the 2030 target of the minimum 50% large-sized machinery ratio ahead of schedule. Additionally, while we anticipate a YoY decline in domestic net sales for 2026 due to production capacity issues, we expect higher net sales in the next fiscal year (2027) compared to 2026, driven by the impact of new products.

Product Portfolio

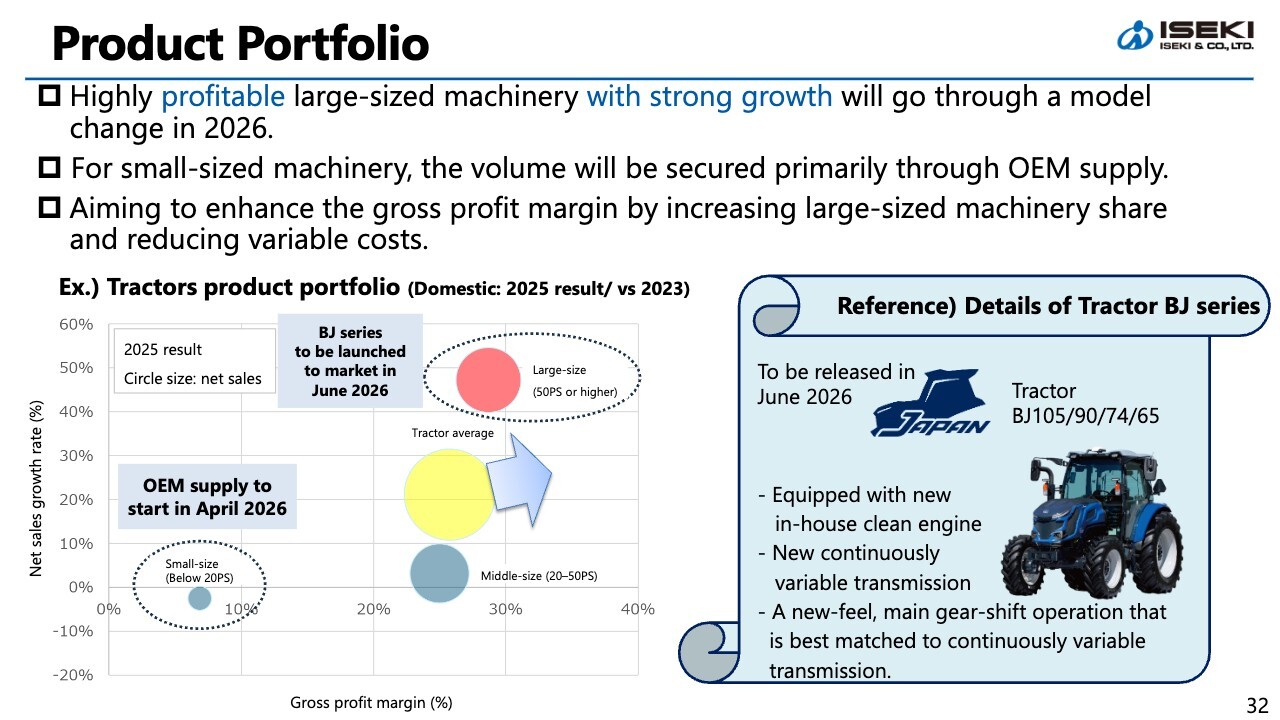

Here is our approach to the product portfolio. The diagram in the lower left corner of the slide shows profitability on the horizontal axis and growth potential on the vertical axis. We will enhance our competitiveness by manufacturing highly profitable large-sized machinery with growth potential in-house, while leveraging OEM supply to secure volume and efficiency for small-sized machinery.

Through this combination, we will simultaneously increase large-sized machinery share and reduce variable costs, the latter under the Project Z structural reforms, to enhance the gross profit margin of the entire domestic business.

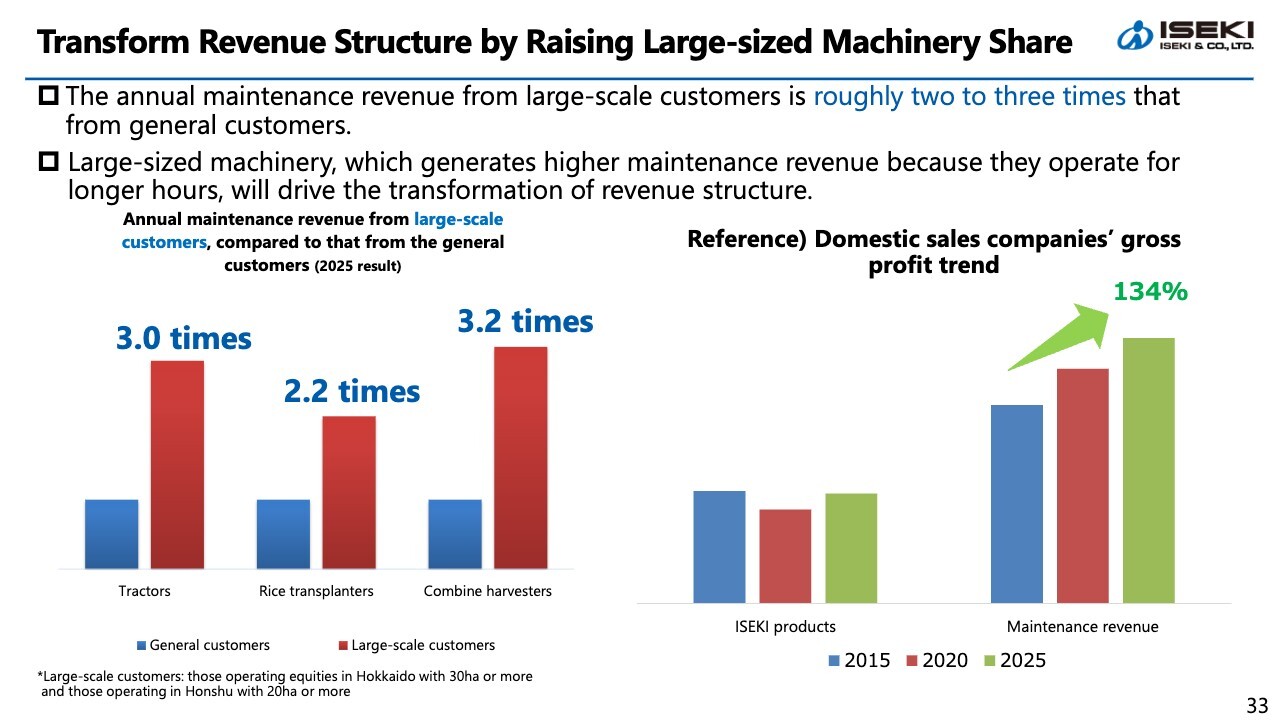

Transform Revenue Structure by Raising Large-sized Machinery Share

This is about transforming revenue structure by raising large-sized machinery share. The annual maintenance revenue from large-scale farmers is roughly three times higher for tractors, more than double for rice transplanters, and more than three times higher for combine harvesters compared to that from general farmers.

The large-sized machinery operates for longer hours and generates stable revenue even after sales. We will further expand this structure to transform our domestic business into a revenue structure based on stable profitability.

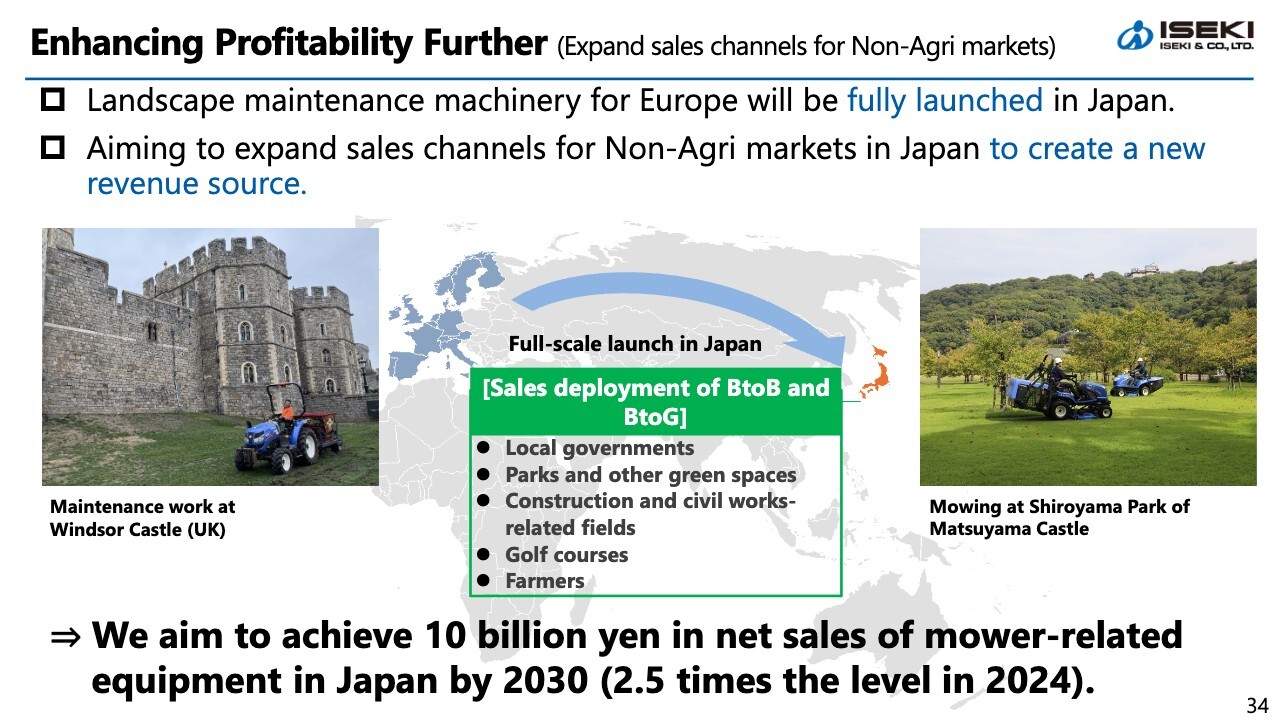

Enhancing Profitability Further (Expand sales channels for Non‐Agri markets)

Furthermore, we will focus on the Non-Agri area. Landscape maintenance machinery will be fully launched in Japan. It has a proven track record in Europe as explained earlier in Part 2.

Specifically, we will cultivate it as a new revenue source, focusing primarily on the BtoB and BtoG sectors, including local governments, parks, golf courses, and construction and civil works. We aim to achieve 10 billion yen in net sales of mower-related equipment in Japan by 2030.

Expanding Market Reach of Mower-related Equipment in Japan

Here is an example of our specific sales activities for mower-related equipment. We are actively participating in trade shows to strengthen our BtoB sales.

Most recently, through our participation in Manufacturing World 2026 Nagoya we presented proposals to customers in sectors such as maintenance work for corporate green spaces and parks. On the day of the event, we were able to establish concrete connections with approximately 150 companies through business card scanning. We aim to expand sales further through on-site demonstration of the machine going forward.

We plan to continue participating in trade shows and similar events on an ongoing basis. In this way, we will continue to develop the market in the domestic Non-Agri sector by leveraging our strength: once customers use our products, they recognize the quality.

In addition to our domestic large-sized machinery strategy, we aim to cultivate mower-related equipment as a new growth driver to ensure stable growth in our domestic business.

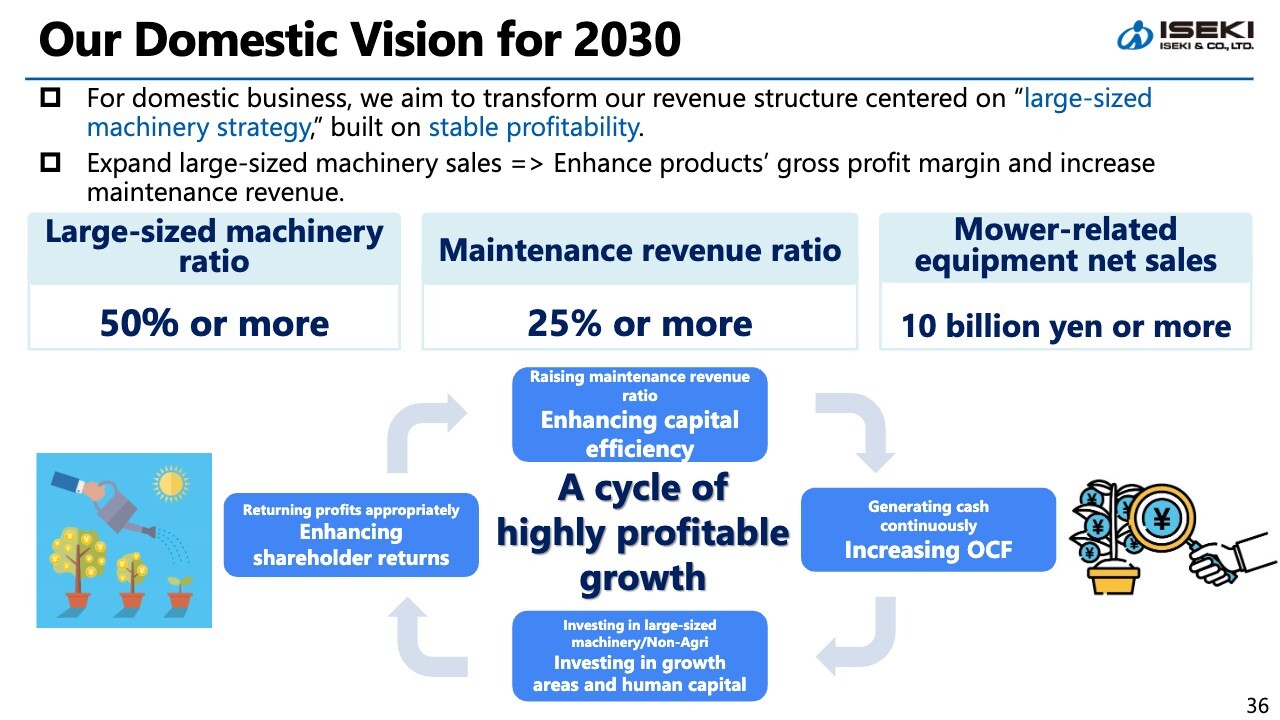

Our Domestic Vision for 2030

Finally, I would like to discuss our vision for the domestic business in 2030. Our targets are to achieve a large-sized machinery ratio of 50% or more, a maintenance revenue ratio of 25% or more, and mower-related equipment net sales of 10 billion yen or more. Through these initiatives, we will establish a cycle of highly profitable growth in our domestic business as well.

By enhancing product gross profit margins and increasing maintenance revenue owing to expanding large-sized machinery sales, we will generate cash continuously and invest it in our next phase of growth. That concludes my explanation of our domestic growth strategy, particularly our strategy for large-sized machinery.

This concludes the presentation covering Parts 1 through 3. Thank you for your attention.

Q&A: Impact of the situation in the Middle East and our response

Participant: Could you please explain the impact of the situation in the Middle East? You mentioned medium- to long-term growth. Given that you expect to achieve your 2030 target for large-sized machinery ahead of schedule, I wondered if this might be slightly affected by the situation in the Middle East. Please tell us the impact.

Tani: As you noted, there is a possibility that procurement costs—particularly those derived from crude oil, such as tires, rubber, and resin products for our machinery—could increase by approximately 20% to 30%.

The same applies to transport costs; shipping companies have indicated that they would like to raise ocean freight rates by about 10%. Furthermore, we are concerned about the impact of rising costs on energy sources such as electricity and gas, which are essential for operating our factories.

Currently, we are managing to maintain production without disruption by ordering parts and other materials on a longer lead time than usual.

However, we are currently scrutinizing our costs. We believe that cost increases from this year through next are unavoidable. In addition to our own efforts, we may need to consider price pass-through to the market, if necessary.

Q&A: Order status for new models and growth outlook for 2027

Participant: On the domestic business front, you mentioned that a new model will be launched this year and that growth will begin in 2027. Could you please provide details on inquiries and order status for the new model? I would also appreciate a bit more explanation of the background for solid growth in 2027.

Noriaki Ishimoto (hereafter, Ishimoto): I am Ishimoto, Corporate Officer, General Division Manager, Business Division, responsible for our domestic business. We have already received orders for the new products. As shown on the slide, since shipments are scheduled for June and December, we expect the new products to start contributing meaningfully to sales in 2027.

Among others, we plan to begin shipping the Combine harvester HJ series which we have already announced as a new product, starting in December 2026. From January through March, we have received stronger-than-expected orders for this product from customers.

Furthermore, since we are seeing solid sales figures for the new Tractors BJ series as well, we believe the impact of these new products is already becoming evident.

Q&A: Prospects for maintenance revenue ratio

Participant: You have a policy to increase the maintenance revenue ratio in Japan, and this ratio has indeed been gradually rising. You have set a target of 25% or more by 2030. If you could give us a rough estimate, could you please explain what level of growth potential you see for the maintenance revenue ratio and what specific level you are aiming for?

Ishimoto: The current maintenance revenue ratio is hovering around 20%. Looking ahead, we aim to achieve a large-sized machinery ratio of over 50% in domestic sales; therefore, we expect the maintenance revenue ratio to increase accordingly. At this stage, we intend to proceed with the goal of exceeding 25%.

Q&A: Factors contributing to higher operating profit in overseas business from 2027 to 2030

Participant: You expect the profit increase effects from your overseas business to reach approximately 1.0 billion yen in 2027 and approximately 3.0 billion yen in 2030. The left side of the slide lists various factors behind the greater profit increase effect from 2027 to 2030. Could you please tell us which factors, in particular, you believe will drive this profit growth?

Tani: While we have various initiatives in place for this, it is primarily associated with sales growth in Europe. Europe net sales were 38.5 billion yen in 2025, and we aim to increase this to 47.0 billion yen or more. We anticipate top-line growth of approximately 10.0 billion yen and plan to achieve an operating margin of 10% or higher.

We are also gradually raising prices. Furthermore, as mentioned earlier, we will continue initiatives to improve profitability per unit through customization and other measures. Through these efforts, we have set a target of a profit increase of approximately 2.0 billion yen.

Q&A: Ratio of in-house products vs. externally sourced products in our European business

Participant: The European business net sales breakdown is shown on the left side of Slide 17. Looking at this graph, the plan indicates a decrease in the ratio of in-house products through 2030; however, you also mentioned that you still have room to expand in-house product offerings and strengthen our product lineup. Could you please elaborate on the planned ratio of in-house products to externally sourced products toward 2030?

Tani: Kindly refer to the pie chart on the right side of the slide. This shows ISEKI France's sales breakdown, with in-house products accounting for 55% and externally sourced products for 45%.

While the ratio of in-house products has decreased compared to the past, the absolute amount has increased. Therefore, when comparing the growth driven by in-house products versus that driven by externally sourced products, externally sourced products are increasing at a faster rate.

Incidentally, in the UK and Germany, which we have made into subsidiaries, the percentage of consumer products is not as high as in France, indicating further room for growth. Overall, as you pointed out, the growth in externally sourced products will be greater while we increase in-house products.

In terms of profit margins, a difference exists because manufacturing profit is added to in-house products; however, we see no significant difference in profitability from sales between in-house products and externally sourced products at present.

Participant: When looking at profitability based on a combination of selling profit and manufacturing profit, your in-house products are more profitable. Under the current plan, however, I think the overall profitability of the product mix will deteriorate if the ratio of products purchased from other companies increases toward 2030.

On the other hand, is it correct to say that your policy is to improve overall profit margins by increasing sales volume?

Tani: You are correct; increasing sales volume is one factor. Additionally, our policy is to improve the overall profitability of the business by expanding our lineup of profitable products such as electric/robotic products with advanced technology, rather than simply purchasing products from other companies, thereby reducing profitability.

Q&A: Possibility of achieving maintenance revenue targets ahead of schedule

Participant: I have a question about maintenance revenue in Japan. Looking at the graph on Slide 27, the growth rates from 2020 to 2025 and from 2025 to 2030 show almost the same trend, so I believe the projection is reasonably valid.

Meanwhile, since you expect to achieve the target for the share of large-sized machinery ahead of schedule, I wonder if the 2030 maintenance revenue target of 30 billion yen might also be attained ahead of schedule. How should I interpret this?

Ishimoto: As we accelerate progress toward our target share of large-sized machinery, we expect the maintenance revenue will also increase.

I would like to follow up on the earlier response to your question regarding maintenance revenue. Although we have long provided after-sales service, in recent years, we have increased the maintenance revenue by working on pre-sales support, including preventive inspections, particularly for large-scale farmers.

As you pointed out, if front-loaded demand emerges across the board, it is highly likely that additional revenue from parts and maintenance services will be generated.

Q&A: Potential market size, expected profitability, and competitors in overseas business

Moderator: The question is: What are the potential market sizes and expected profitability in Northern Europe, Eastern Europe, North Africa, and the Middle East? What will drive demand? Also, what competitors exist, and what risks do you foresee?

Yoshiaki Kimata: I am Kimata, Senior Corporate Officer, General Division Manager, Overseas Business Division.

Although the market size is not very large, there are still regions we have yet to tap into, and we intend to promote sales of landscape maintenance machinery, particularly in Northern Europe, Eastern Europe, North Africa, and the Middle East.

Since these are niche markets and accurate data is not readily available, giving specific figures on market size is difficult.

Generally speaking, while Northern Europe consists of many small countries, they have a very high level of environmental awareness and correspondingly large markets. We see Eastern Europe as a market with promising future growth potential. As you are all aware, the current situation in the Middle East, including North Africa, makes it somewhat difficult to expand sales in these regions. As Tani explained earlier, while the landscape maintenance machinery in which we specialize is a niche market, we believe there is definite demand in resort areas and similar locations.

Furthermore, unlike the agricultural machinery market, we believe that machinery for the landscaping market can be reasonably profitable. We are pursuing highly profitable business development in Europe, and expect to secure a certain level of profitability in other regions as well, albeit in niche markets.

However, there are competitors. Among the major players, we consider Japanese manufacturer Kubota Corporation (Kubota), the even larger American company Deere & Company, and, particularly in the golf course sector, The Toro Company to be very strong.

At the same time, relatively low-cost and competitive manufacturers from India and China are emerging on the global stage, and we anticipate competition from them.

Consequently, we intend to compete in high-value-added segments by leveraging our established brand recognition and superior product quality.

We also intend to offer products in the low-price segment in some way, while exploring partnerships with other companies. I apologize for not being able to provide specific figures at this time, but this is the general direction we are envisioning.

Q&A: Differentiation and strengths in domestic business

Moderator: The question is: I believe Kubota and YANMAR HOLDINGS CO., LTD. are strong players in the domestic agricultural machinery market. How are you positioning yourself against competitors?

Ishimoto: When it comes to product differentiation, factors such as product strength, sales capabilities, and development capabilities come into play.

We feature our “Only i” logo on our products, which represents our proprietary technologies. We promote and encourage them as an aspect that allows us to offer customers advantages that our competitors do not possess.

Additionally, as I mentioned earlier, direct-sales ratio accounts for 70% or more of our business. We position ourselves as “the closest partner to farmers” and promote this as another key strength.

Furthermore, the Amoni website was refreshed last October. With the goal of making it easy for customers to view, we are actively disseminating information. We are also seeing positive trends, such as increased view counts, on social media.

Moreover, we organize events in various prefectures to create opportunities to meet customers. Depending on the prefecture, we hold these events about two to three times a year, and we consider this activity to establish connections with many customers to be one of our strengths.

Greetings from Mr. Odagiri

Odagiri: Thank you very much for your active participation and questions today. Project Z is an initiative that ISEKI has resolved to achieve in full as we look toward our next 100 years. To ensure the plan’s successful completion, I will work to thoroughly instill and implement it among our employees to further strengthen our execution capabilities.

We are already beginning to see steady results in terms of our revenue structure and financial performance. Moving forward, we are entering a phase where we will translate these results into growth. We would appreciate your continued support as we pursue our initiatives from a medium- to long-term perspective.

Thank you very much for your time today.