Review of 26 Medium-Term Management Plan and Next Direction

Hideaki Asakura: Hello, everyone. I am Hideaki Asakura, Vice President and Representative Director of Taiheiyo Cement Corporation. Thank you very much for your continued support of Taiheiyo Cement.

Every day, we hear a variety of reports, such as “It’s unclear how the conflict between Iran and the U.S. will unfold” and “How many vessels have passed through the Strait of Hormuz?” Even amid the extreme volatility in energy prices, we believe it is important to keep moving forward while overcoming various challenges.

With two of the three years of our 26 Medium-Term Management Plan now complete, today I would like to look back on these past two years, discuss the events that have unfolded, and explain what we’re considering and how we intend to proceed in the final year of the plan.

Furthermore, since we typically formulate our medium-term management plans on a roughly three-year cycle, I will also discuss the key focus areas for our next medium-term management plan. Following my presentation, we will hold a Q&A session, and I hope this will deepen your understanding of our company.

Katsuya Kawata: Hello, everyone. I am Kawata, Managing Executive Officer, and I will be presenting today. I have been serving as the executive in charge of Corporate Planning since April of this year.

I will be discussing the topic “Review of 26 Medium-Term Management Plan and Next Direction,” with the subtitle “Initiatives for Early Realization of PBR of Over 1X.”

Contents

Contents. The presentation is broadly divided into two sections. First, we will cover the progress of the 26 Medium-Term Management Plan, as well as deviations from the plan and the results achieved. Focusing on cash allocation, we will explain the areas where results deviated from the plan and the outcomes.

Next, to achieve a PBR of over 1 as soon as possible, I will explain our future initiatives by breaking down the PBR into ROE and PER. Finally, I will discuss the challenges and initiatives related to the formulation of our next medium-term management plan.

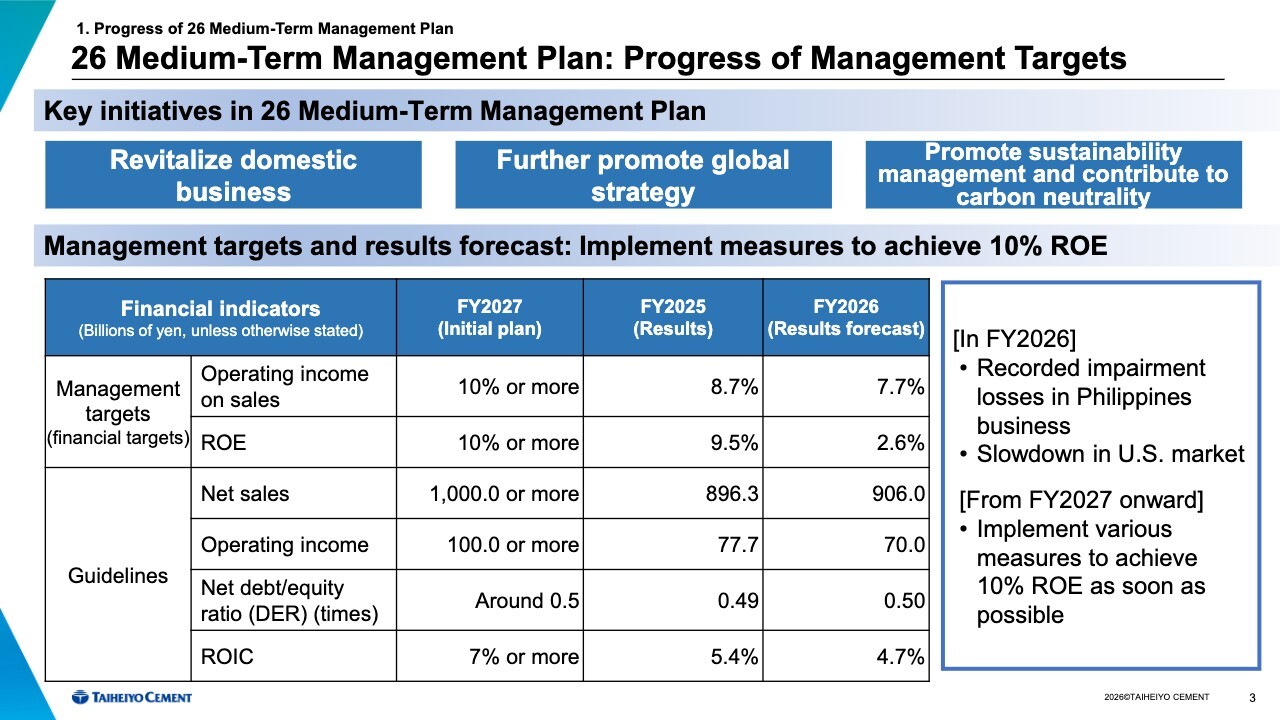

1. Progress of 26 Medium-Term Management Plan: 26 Medium-Term Management Plan: Progress of Management Targets

This is the progress of the 26 Medium-Term Management Plan. Under the 26 Medium-Term Management Plan, we have set out three key initiatives: “Revitalize domestic business,” “Further promote global strategy,” and “Promote sustainability management and contribute to carbon neutrality.”

The table on this slide shows our management targets and guidelines for the initial plan for FY2027, the final fiscal year, the results for FY2025 and the results forecast for FY2026.

In particular, for FY2026, as shown on the right side of the slide, we expect results to fall short of the initial plan due to factors such as the recognition of an impairment loss in the Philippine business, a slowdown in the U.S. market, and sluggish domestic demand in Japan. The target figures for FY2027, the final year, are deviating from actual performance.

Despite this situation, we will implement various measures from FY2027 onward with the aim of achieving a 10% ROE as soon as possible.

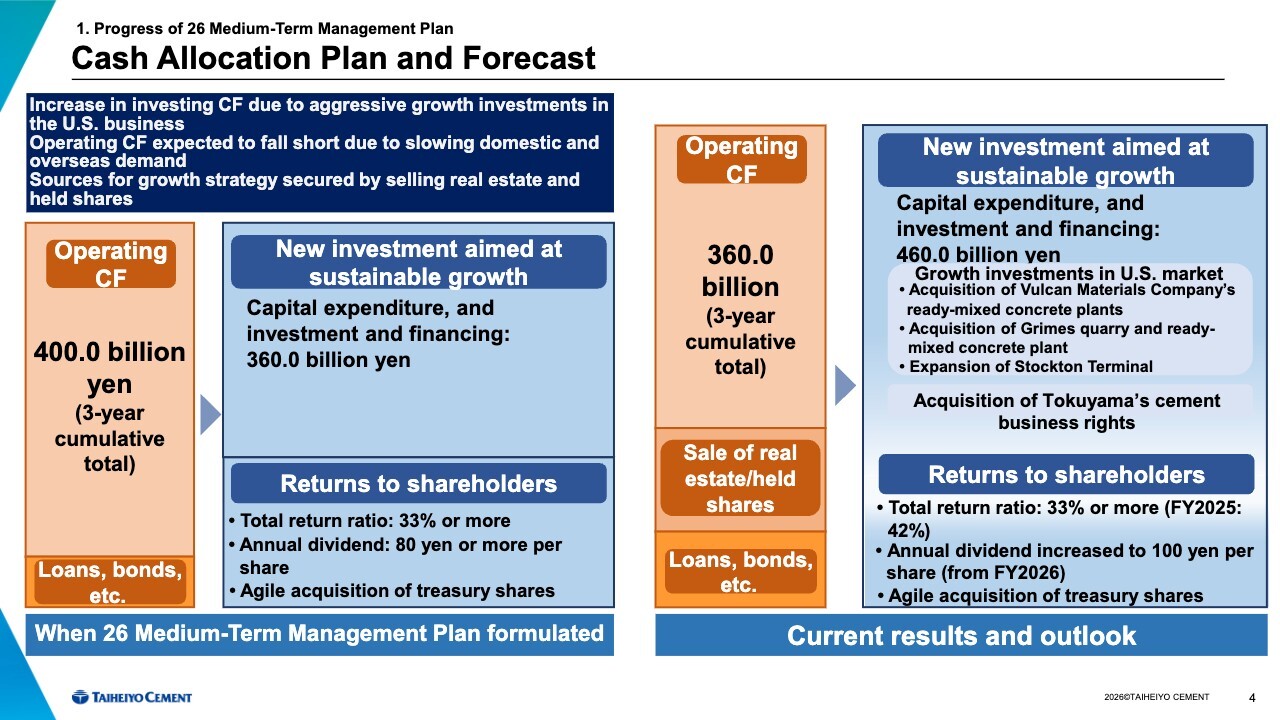

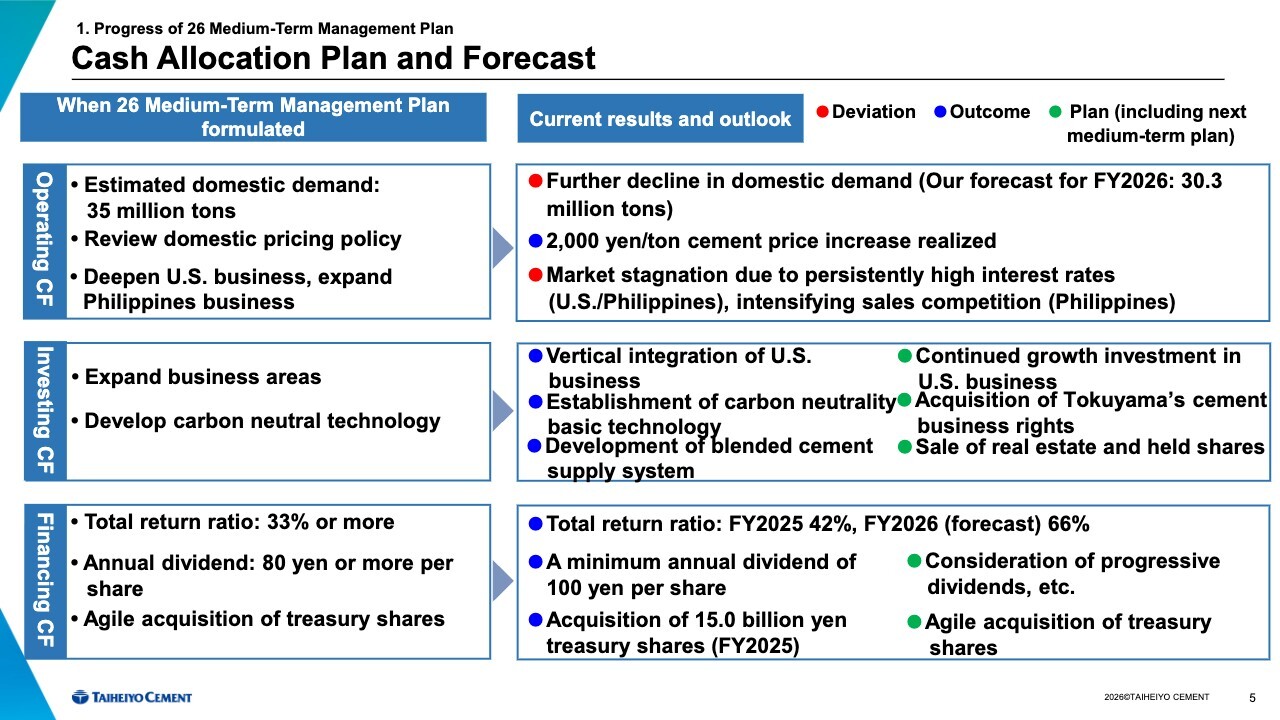

1. Progress of 26 Medium-Term Management Plan: Cash Allocation Plan and Forecast

This slide outlines the cash allocation plan and forecast. The left side shows the initial plan, while the right side shows the current status.

We originally expected operating cash flow of 400 billion yen over the three-year period, but we now expect it to be 360 billion yen. Growth investments were initially planned at 360 billion yen, but are now expected to reach 460 billion yen. As a result, investment cash flow exceeds the plan by approximately 100 billion yen, while operating cash flow falls short by approximately 40 billion yen.

Growth investments, in particular, are progressing ahead of plan. This reflects the importance of timing in investment decisions and our ability to act without missing opportunities. Major investments include the acquisition of ready-mix concrete plants from Vulcan Materials and acquisition of quarries operated by Grimes Rock as part of our growth strategy in the U.S. market.

In addition, we issued a press release on March 25 regarding the acquisition of Tokuyama’s cement business rights. This was not included in the initial plan and has been newly added.

On the other hand, operating cash flow is short by 40 billion. This is mainly due to factors such as the slowdown in the U.S. market and the recognition of an impairment loss in the Philippine business mentioned earlier, resulting in a gap of approximately 140 billion yen.

In this context, we are proceeding with the sale of real estate and equity holdings to secure funds for growth investments. For the portion that cannot be covered, we plan to raise funds through borrowings and corporate bonds.

1. Progress of 26 Medium-Term Management Plan: Cash Allocation Plan and Forecast

This is a summary of the execution items at the time of formulating the 26 Medium-Term Management Plan, along with the current results and outlook. As shown on the slide, red dots indicate deviations, blue dots indicate outcomes, and green dots indicate plans, including those for the next medium-term management plan. I will explain each item individually.

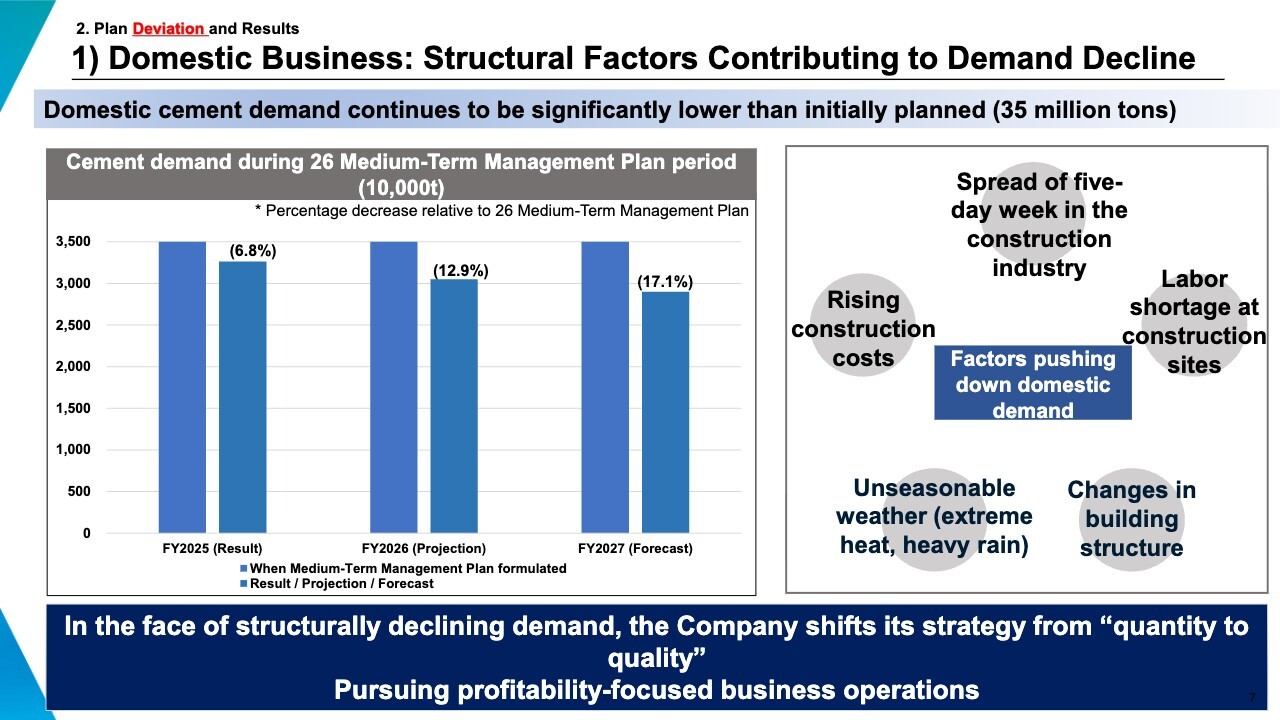

2. Plan Deviation and Results 1) Domestic Business: Structural Factors Contributing to Demand Decline

Demand in the domestic business has fallen significantly short of our initial assumptions. We had originally expected demand to remain at around 35 million tons per year over the three-year period.

However, in reality, demand has been declining by approximately 6% annually. As a result, in FY2027, demand is expected to be around 30.3 million tons per year, representing a deviation of approximately 17.1% from the initial assumption of 35 million tons per year.

As shown on the right side of the slide, several factors are contributing to this situation. The construction industry is facing challenges such as the spread of five-day week in the construction industry, labor shortage at construction sites , which have led to unsuccessful bids and project delays.

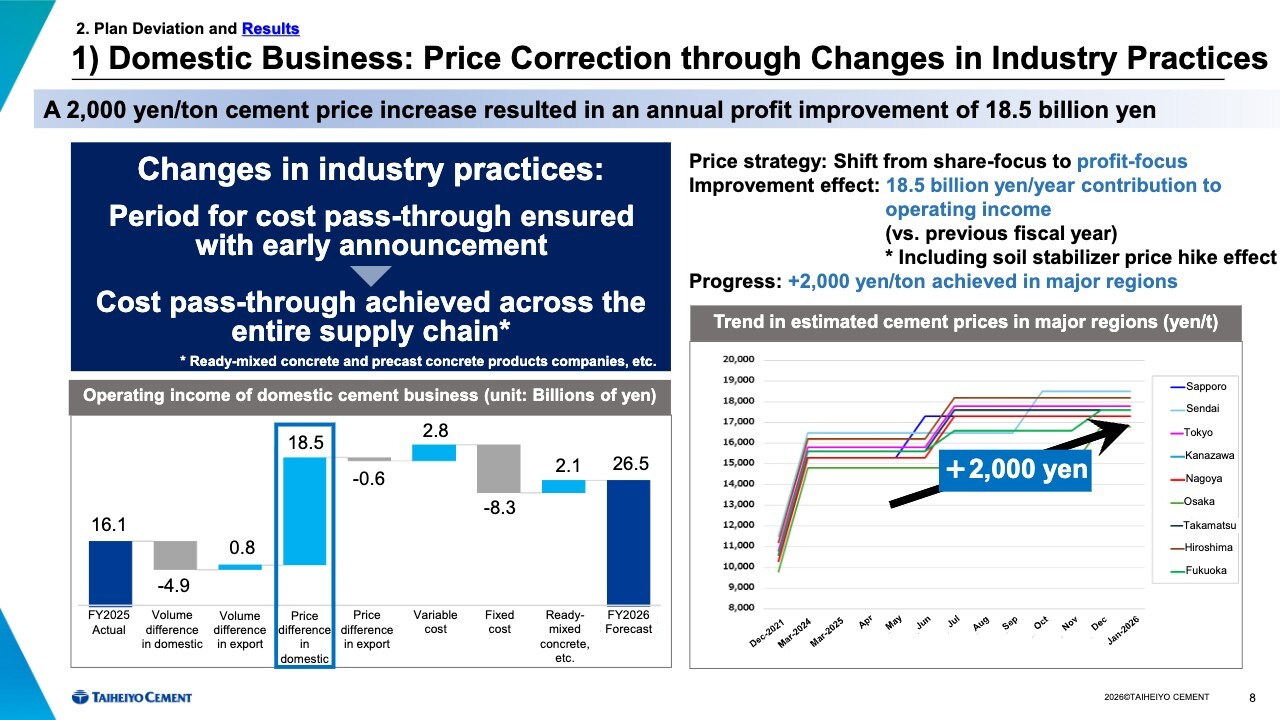

2. Plan Deviation and Results 1) Domestic Business: Price Correction through Changes in Industry Practices

I omitted this at the beginning, but today I will explain five key points that we consider important, highlighting each one as we go.

First, the first key point. As mentioned earlier, domestic demand is on a gradual decline, but we announced a price increase of 2,000 yen per ton last spring and have nearly achieved it. As a full-year effect, this resulted in an annual profit improvement of 18.5 billion yen in FY2026.

As shown in the lower-left graph, the decline in domestic demand led to a decrease in profit of 4.9 billion yen. However, the successful implementation of the price increase, resulted in a profit increase of 18.5 billion yen increase in profits, leading to a significant overall improvement compared to the previous fiscal year.

This is not merely about achieving a 2,000-yen per ton price increase. What I would like to emphasize is that we were able to significantly transform industry practices.

Prior to this 2,000-yen per ton price increase, coal prices surged significantly during the Russia’s invasion of Ukraine , leading to a 5,000-yen per ton price increase. Since there was a clear and understandable factor—the rise in coal prices—customers were able to accept it.

For the recent 2,000-yen per ton price increase, we announced it one year in advance. As a result, we believe we were able to implement the increase not only with our direct customers but across the entire supply chain, including downstream customers.

In this sense, we recognize this price increase as a significant achievement, distinct from past increases.

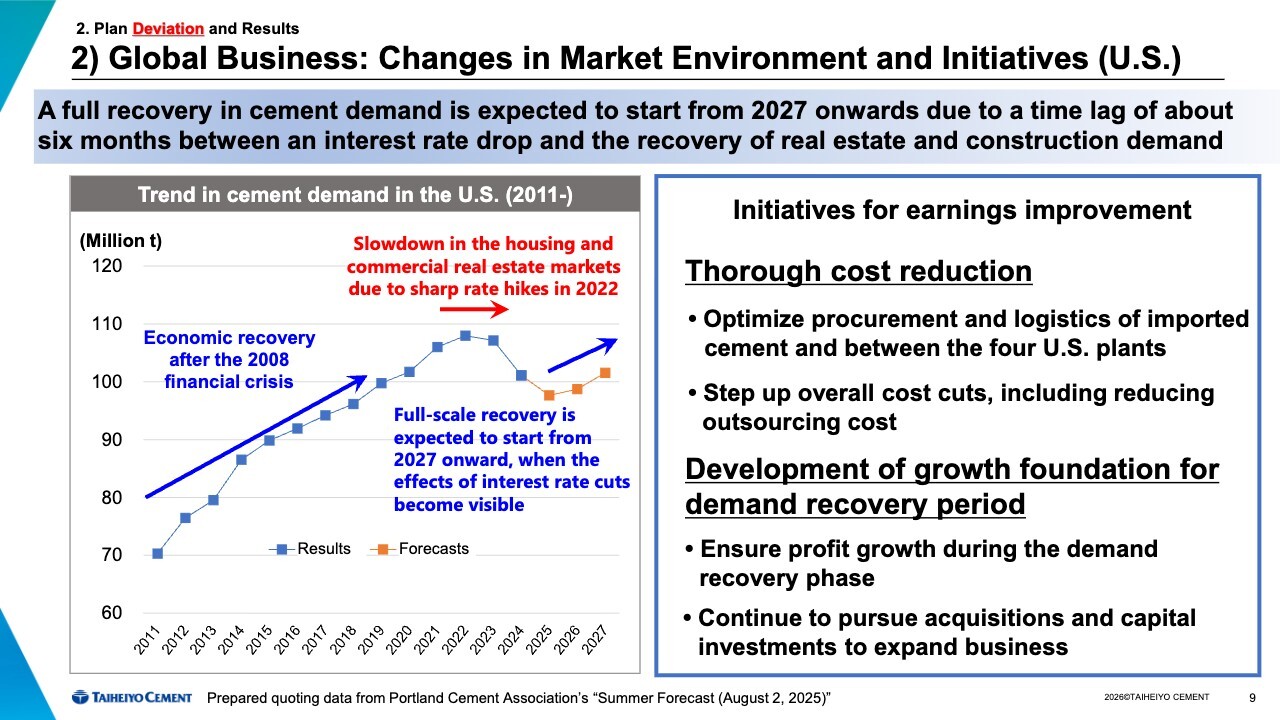

2. Plan Deviation and Results 2) Global Business: Changes in Market Environment and Initiatives (U.S.)

This section covers the status of our U.S. business. As indicated in the top-left corner of the slide, the title reads “Plan Deviation and Results,” but here I will focus specifically on the deviation shown in red.

As you can see from the graph on the left side of the slide, following the recovery in demand after the 2008 financial crisis, the housing and commercial real estate sectors have been sluggish since 2022 due to the impact of rapid interest rate hikes, and cement demand has slowed accordingly.

The situation remains highly uncertain due to factors such as last year’s tariffs introduced by the Trump administration and ongoing developments in Iran. However, we expect cement demand to recover with some time lag following the shift to a rate-cut cycle.

Against this backdrop, we are rigorously implementing cost reductions, as shown on the right side of the slide, while also investing in a growth foundation for the upcoming recovery phase, as I will explain on the next page.

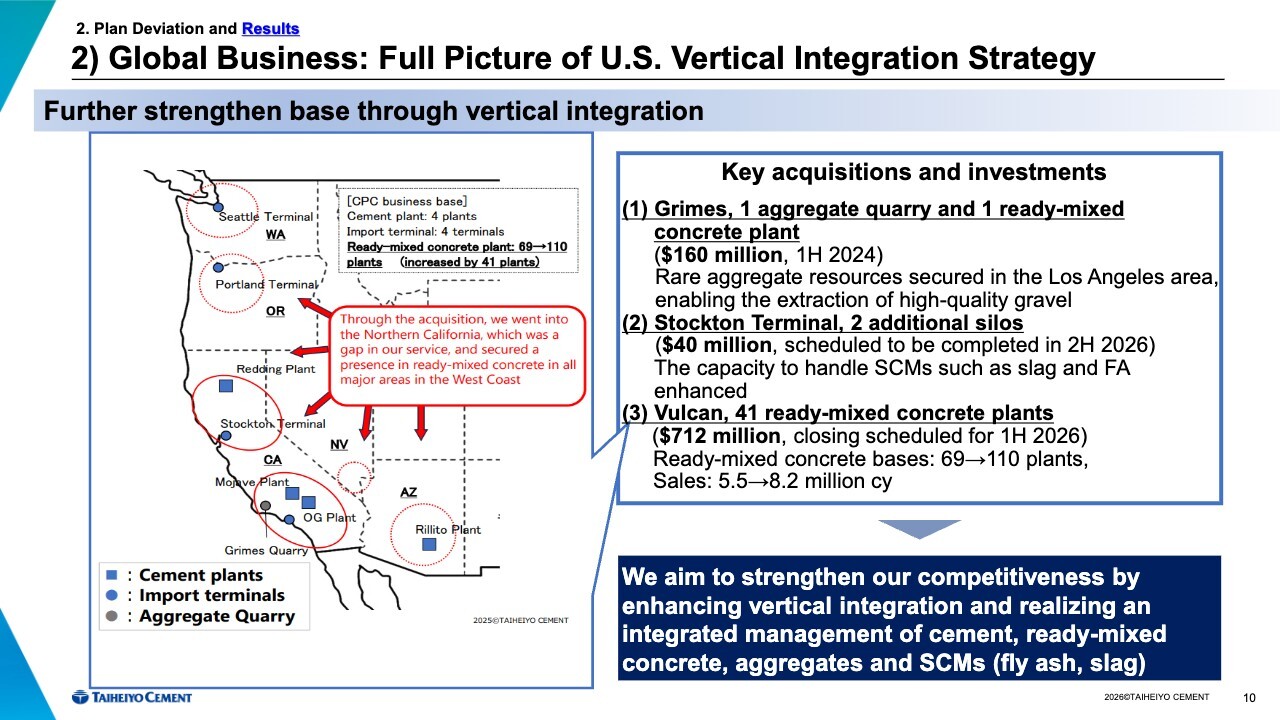

2. Plan Deviation and Results 2) Global Business: Full Picture of U.S. Vertical Integration Strategy

These are the major investment projects in the U.S., which we also explained at the U.S. business briefing last December.

On the left, you can see the benefits resulting from our acquisition of Vulcan Materials’ ready-mix concrete business. We have now achieved near-complete vertical integration in key regions of Northern California and the West Coast, areas where we previously had no presence.

Additionally, the decision to add two silos to the Stockton terminal was made about two years ago. These silos are designed to handle cementitious materials such as slag and fly ash. Construction is progressing steadily, and we expect it to be completed and begin operations in the second half of this fiscal year.

Regarding Vulcan Materials Company’s ready-mix concrete plants, the HSR (Hart-Scott-Rodino) review is currently underway. We expect closing to be completed during the first half of this fiscal year.

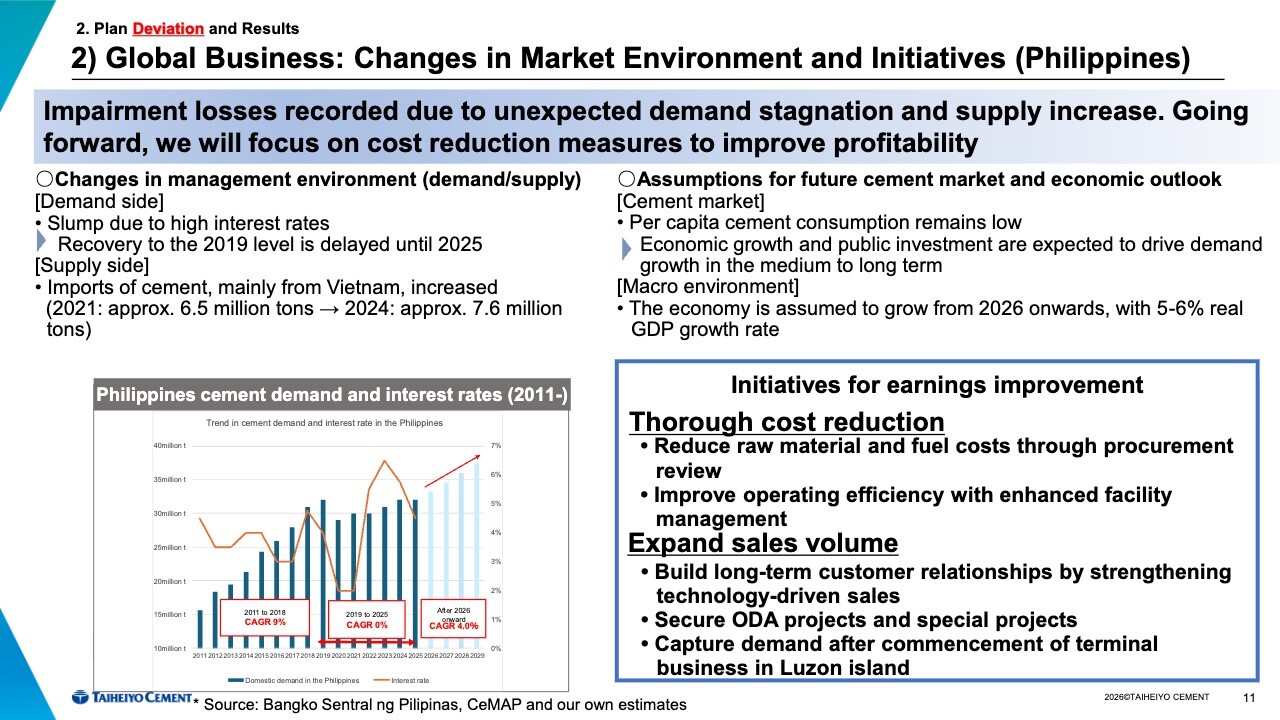

2. Plan Deviation and Results 2) Global Business: Changes in Market Environment and Initiatives (Philippines)

Now, let’s look at the situation regarding the Philippines business, where a significant deviation from the plan can be seen. The top left of the slide reads “Demand Side.” Due to the impact of high interest rates, demand has been in a severe slump since 2019. It took approximately six years to recover, and it finally returned to 2019 levels in 2025.

On the supply side, large volumes of low-cost Vietnamese products are entering the market. Vietnam has a domestic demand of 60 to just under 70 million tons yet possesses a supply capacity of approximately twice that amount, and this surplus is flowing into the geographically close Philippine market.

In 2024, imports from Vietnam increased to approximately 7.6 million tons, accounting for about 25 percent of the overall market. However, more recently, a three-year safeguard measure was implemented starting last year, and import volumes have since declined.

Given this situation, we view the Philippine cement market as a developing market. Per capita cement consumption remains low, and we expect demand to expand over the medium to long term, driven by economic growth and public investment.

As an immediate measure, we will focus on reducing raw material and fuel costs by reviewing our procurement processes to thoroughly cut costs, while also aiming to expand sales volume. Since ODA projects have very strict quality requirements, we will focus on supplying the high-quality cement we specialize in.

In addition, we will pursue specific projects, such as terminal operations on Luzon Island, to secure demand.

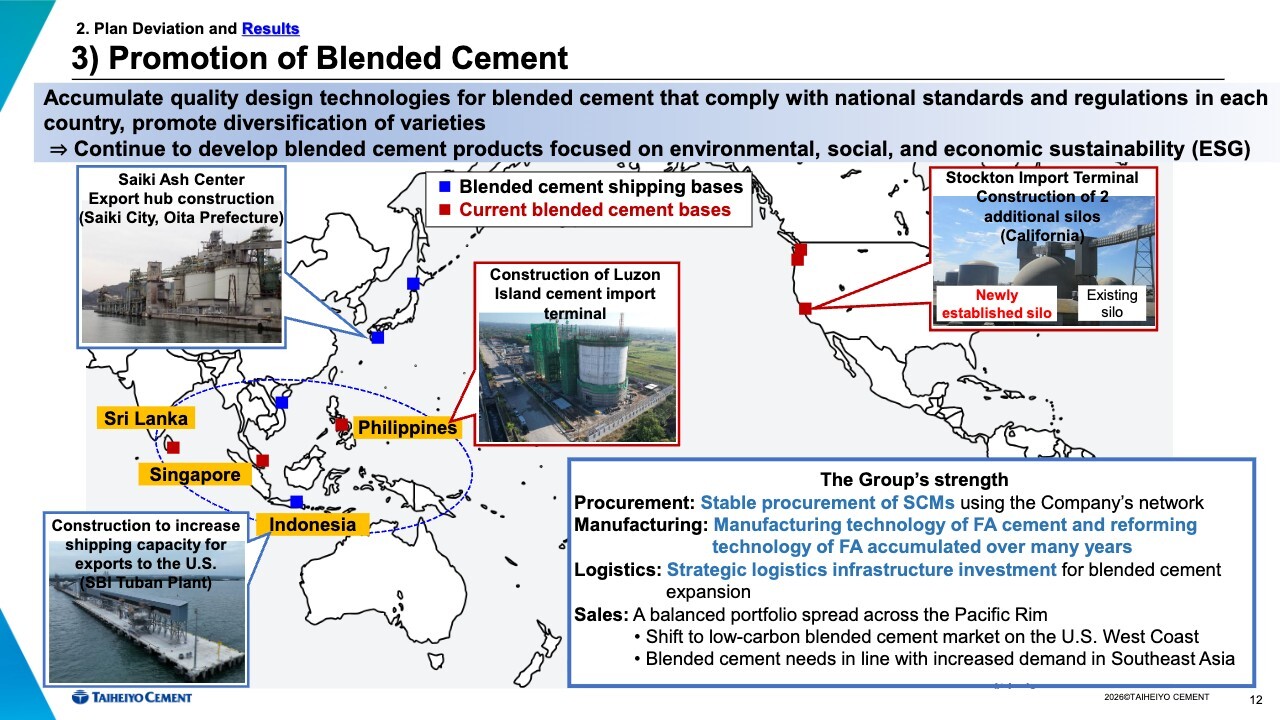

2. Plan Deviation and Results 3) Promotion of Blended Cement

This is the second point I would like to emphasize. To promote blended cement, we have spent the past several years building a supply chain that spans the Pacific Rim and U.S. markets.

As shown in the lower right corner of the slide, let me start with procurement. We have long maintained strong business relationships with steel manufacturers and electric power companies in Japan. Building on this, we have developed strong procurement capabilities for cementitious materials— materials used in blended cement—primarily in Japan, giving us a competitive advantage over our competitors..

For example, fly ash—a byproduct of coal-fired power generation—requires processing before it can be used in cement. We process and blend fly ash to make it suitable for use in cement, leveraging our technical and production expertise. We have extensive experience in this field.

Furthermore, we have secured supply bases in the Pacific Rim region and established a transit hub in the United States. Thus, on the U.S. West Coast—a region with promising future growth—we have already established a supply chain that encompasses everything from raw material supply to customer service in the Pacific region by leveraging the robust sales and distribution network of CalPortland Company (hereinafter “CPC”). This is a major strength.

We believe it would be extremely difficult for competitors to replicate this system even if they attempted to follow suit.

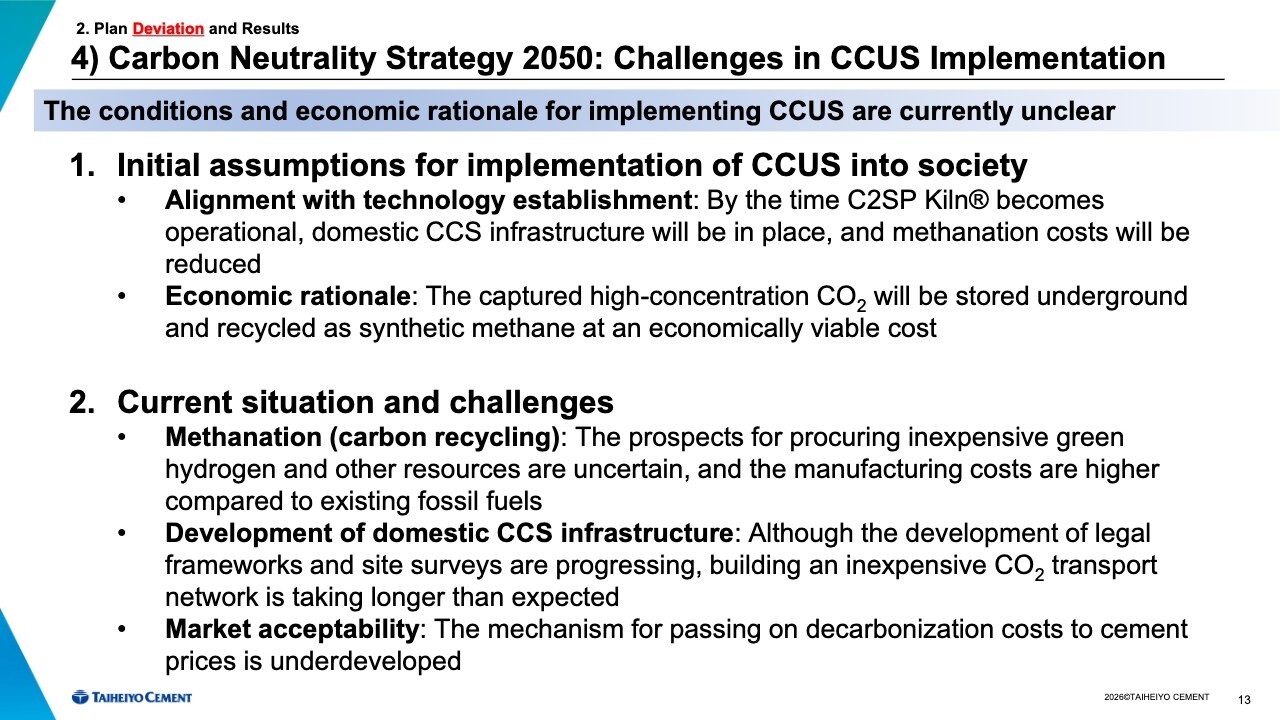

2. Plan Deviation and Results 4) Carbon Neutrality Strategy 2050: Challenges in CCUS Implementation

I would like to explain the carbon-neutrality strategy. The initial assumptions regarding the social implementation of CCUS were that, by the time the C2SP Kiln becomes operational, domestic CCS infrastructure would be in place and methanation costs would have reduced. I will explain the C2SP Kiln later.

From the perspective of economic viability, we initially envisioned a roadmap through 2030 in which captured CO2 could be stored underground or recycled into synthetic methane at economically viable costs.

However, the current reality and challenges indicate that securing affordable green hydrogen and other resources for methanation is extremely difficult. Given these circumstances, we recognize that achieving the social implementation of CCUS will still take time.

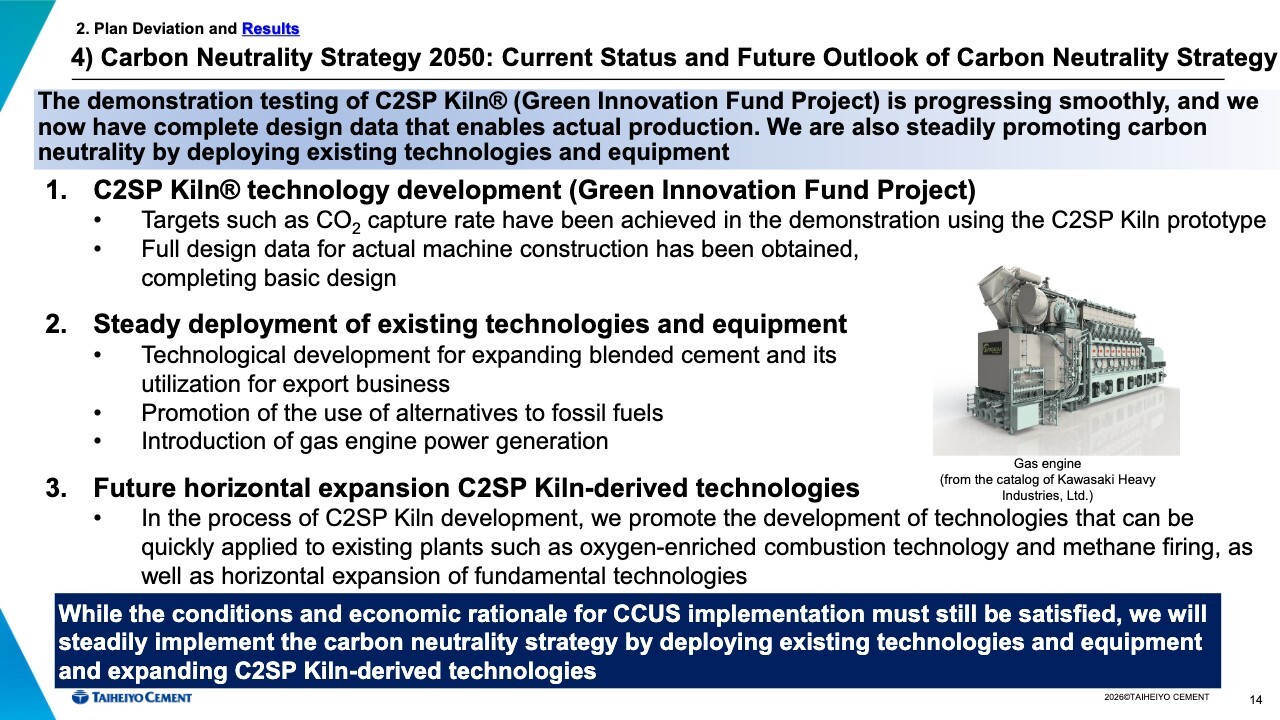

2. Plan Deviation and Results 4) Carbon Neutrality Strategy 2050: Current Status and Future Outlook of Carbon Neutrality Strategy

Amid an uncertain external environment, we are steadily implementing what needs to be done at present. Details on the C2SP Kiln are provided in the supplementary materials. The C2SP Kiln is a technology developed by the Company to capture CO2 during the calcination process.

We have achieved our CO2 capture rate targets. Furthermore, we have completed the collection of data required for actual plant construction and finalized the basic design.

In addition, we are steadily deploying proven technologies and equipment. As mentioned earlier, we are advancing initiatives such as building the technological foundation for expanding the use of blended cement and introducing gas engine power generation at the Fujiwara Plant.

Though our carbon neutrality initiatives, as initially envisioned, have not progressed as planned due to various factors, we have now established the foundational technologies. We plan to first apply these technologies to existing businesses.

We will advance efforts to horizontally deploy technologies acquired through the development of the C2SP Kiln, such as oxygen-enriched combustion and methane firing, across existing operations.

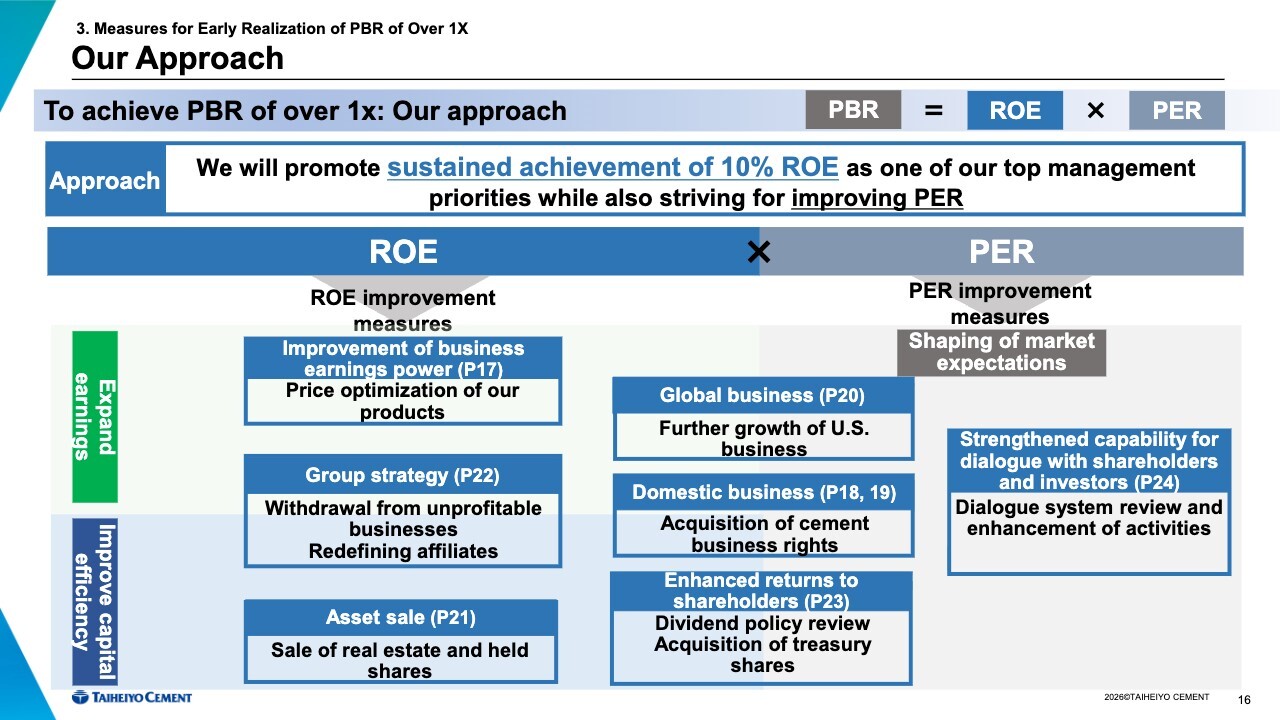

3. Measures for Early Realization of PBR of Over 1X: Our Approach

This slide outlines initiatives aimed at achieving a PBR of over 1x. Here, PBR is broken down into ROE and PER, and the vertical axis categorizes the initiatives into “expand earnings” and “improve capital efficiency.” I will explain each of them in turn.

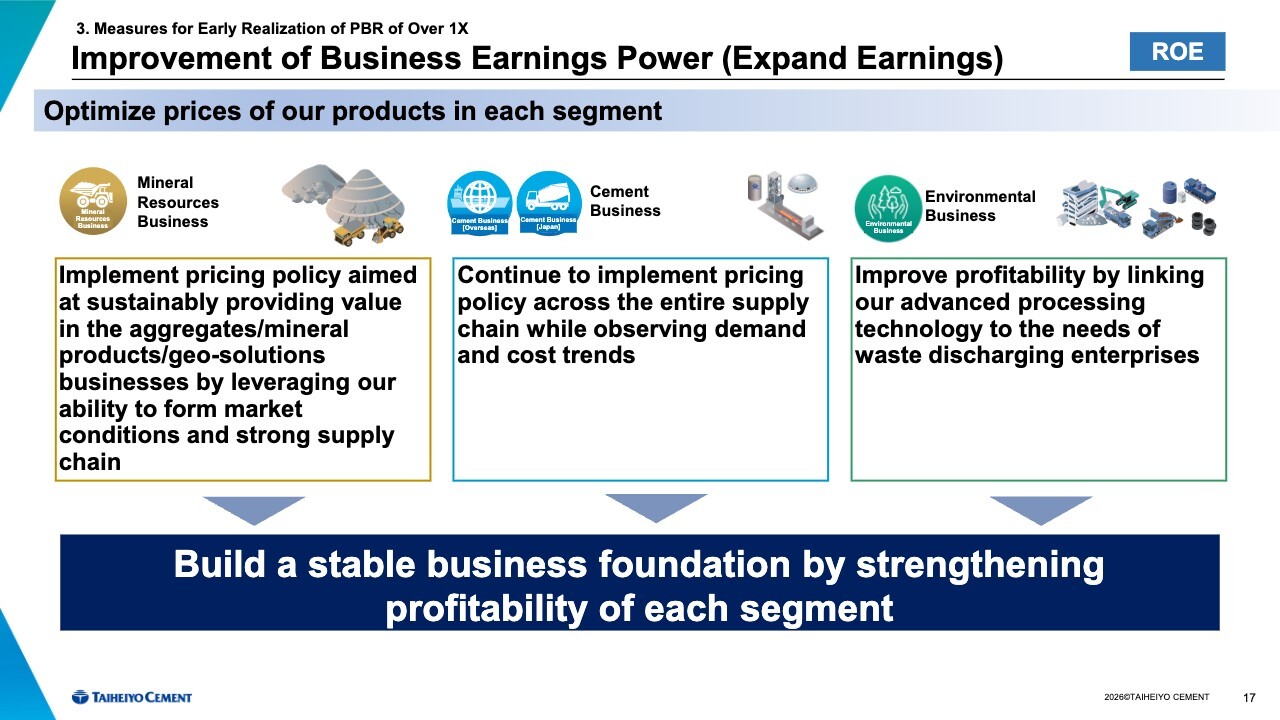

3. Measures for Early Realization of PBR of Over 1X: Improvement of Business Earnings Power (Expand Earnings)

I would like to explain ROE in relation to achieving a PBR of over 1x. As for the Cement Business, the situation is as I have explained so far.

Regarding the Mineral Resource Business, which is our core domestic operation, we are implementing pricing policy aimed at sustainably enhancing value in the aggregates/mineral products/geo-solutions businesses by leveraging our ability to form market conditions and strong supply chain.

In our Environmental Business, we are working to optimize waste processing fees for waste treated at cement plants. By improving profitability across all segments, we are building a stable revenue base.

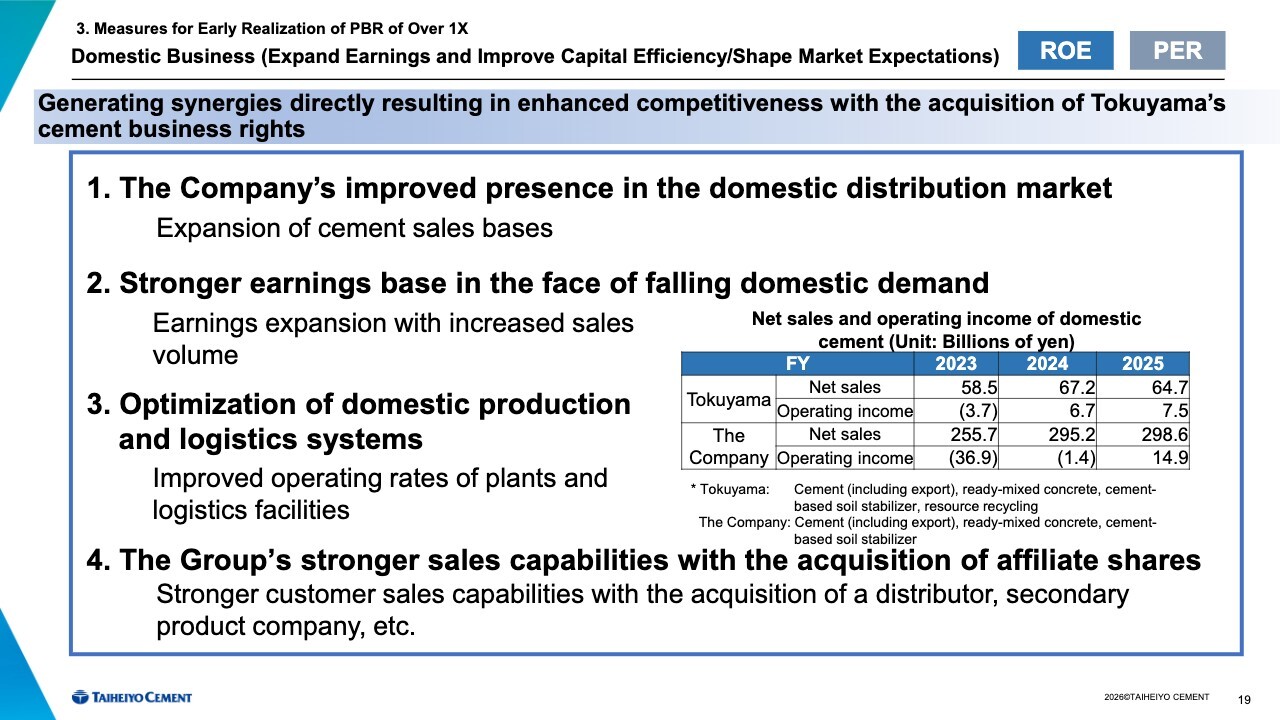

3. Measures for Early Realization of PBR of Over 1X: Domestic Business (Expand Earnings and Improve Capital Efficiency/Shape Market Expectations)

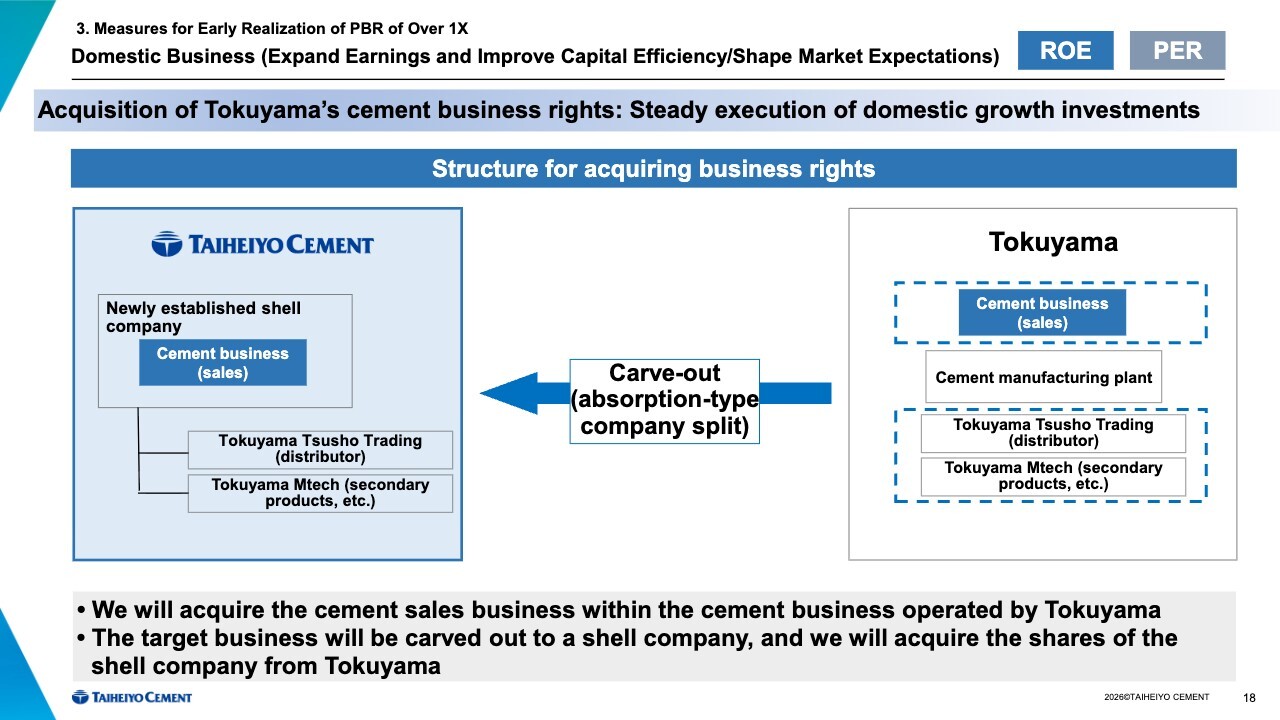

This is the content of the press release issued on March 25, and it is the third point to highlight. As shown on the slide, the scheme is that we will acquire Tokuyama’s cement business rights.

This transaction will be structured as a carve-out (absorption-type company split), with the target business carved out to a shell company to be established in October this year, and we will acquire the shares of that shell company from Tokuyama.

At present, we are awaiting clearance from the Japan Fair Trade Commission. We are preparing to take over Tokuyama’s cement business over a two-year transition period starting in the second half of this fiscal year.

3. Measures for Early Realization of PBR of Over 1X: Domestic Business (Expand Earnings and Improve Capital Efficiency/Shape Market Expectations)

This offers significant benefits, as it allows us to acquire a customer base in Western Japan, an area where we have had limited presence. Furthermore, securing a transshipment hub will enable us to optimize our supply chain. We also believe this will contribute significantly to improving the operating rates of our production facilities in the long run, and we expect to realize synergies.

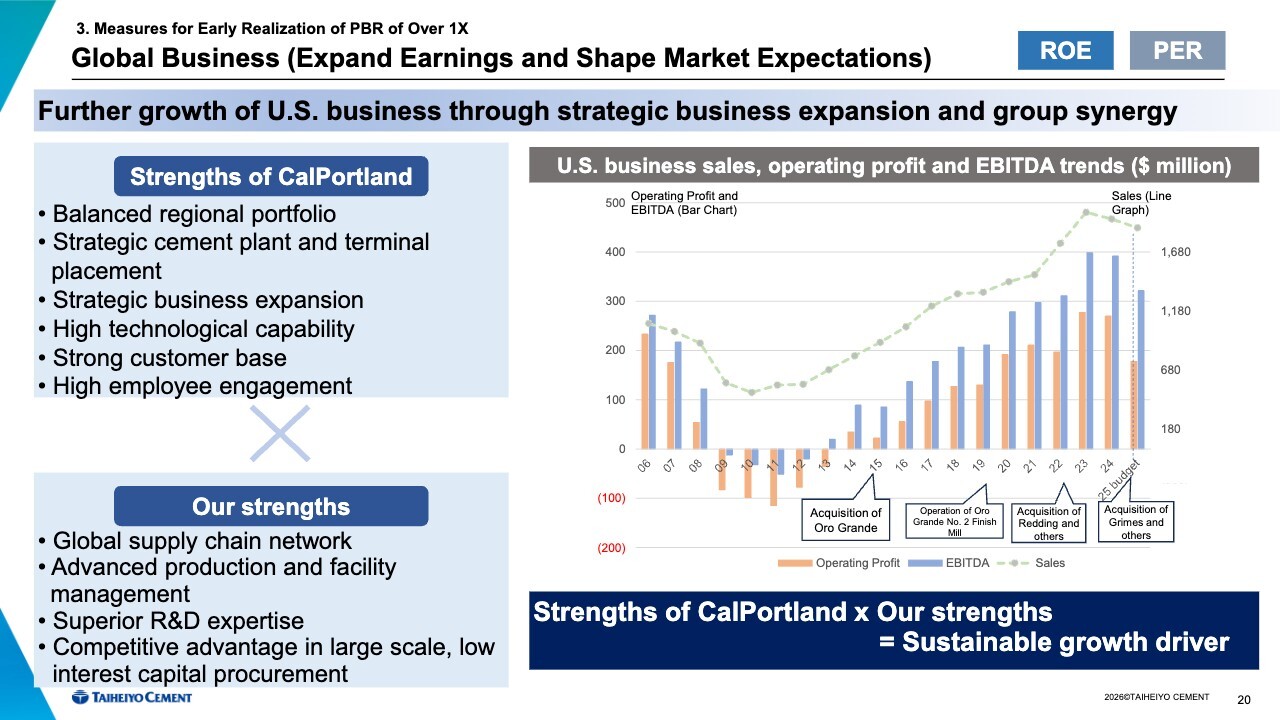

3. Measures for Early Realization of PBR of Over 1X: Global Business (Expand Earnings and Shape Market Expectations)

Now, let me explain the global business. In the U.S. business, we aim to maximize synergies by combining the strengths of our Company and CPC.

In the U.S. market, where the shift toward blended cement is progressing rapidly, sources of fly ash and slag on the West Coast are almost nonexistent, and even where they do exist, they are very limited and are expected to decline further.

Therefore, to achieve sustainable growth, collaboration between CPC and our Company is a critical factor, as we can supply cementitious materials.

We recognize that this point has not been sufficiently communicated in the past. Therefore, in order to help shareholders better understand the value of the U.S. business, we will expand opportunities to provide information and enhance the content of our disclosures.

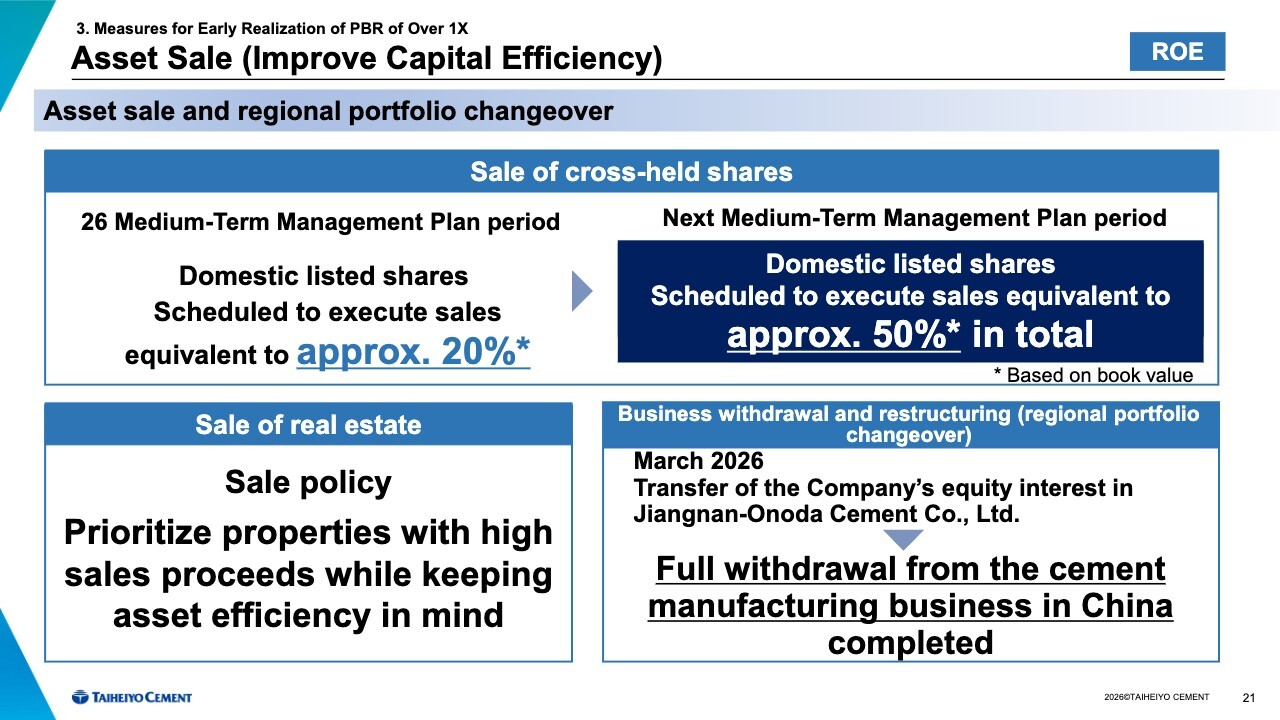

3. Measures for Early Realization of PBR of Over 1X: Asset Sale (Improve Capital Efficiency)

Shifting gears, I would now like to discuss asset sales and improvements in capital efficiency.

First, regarding the sale of cross-held shares, we plan to execute sales equivalent to approximately 20% of domestic listed shares during the 26 Medium-Term Management Plan period, based on book value as of the end of March 2025. Including the next medium-term management plan period, we plan to execute sales equivalent to approximately 50% in total.

Regarding real estate sales, we will prioritize projects that generate cash flow while keeping asset efficiency in mind.

As for business withdrawals and restructuring (regional portfolio changeover), as announced in the March 2026 press release, we have transferred the Company’s equity interest in Jiangnan-Onoda Cement Co., Ltd. and have fully withdrawn from the cement manufacturing business in China.

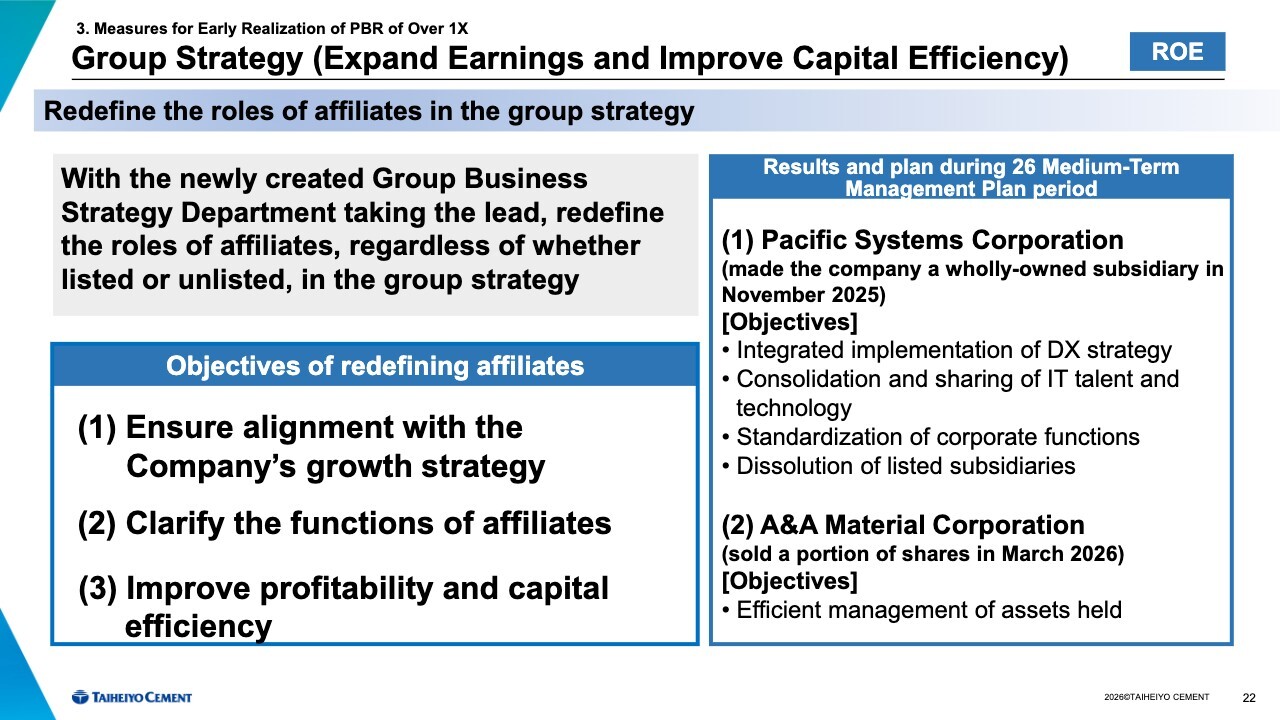

3. Measures for Early Realization of PBR of Over 1X: Group Strategy (Expand Earnings and Improve Capital Efficiency)

Now, turning to our group strategy. Centered on the newly established Group Business Strategy Department, we are redefining the roles of affiliated companies in the group strategy, regardless of whether they are listed or unlisted. Specifically, this is being pursued with the aim of ensuring alignment with the Company’s growth strategy, clarifying the functions of affiliated companies, and improving profitability and capital efficiency.

A concrete example of this is the acquisition of Pacific Systems Corporation last November, making it a wholly owned subsidiary. More recently, at the end of March, a portion of the shares in A&A Material Corporation was sold.

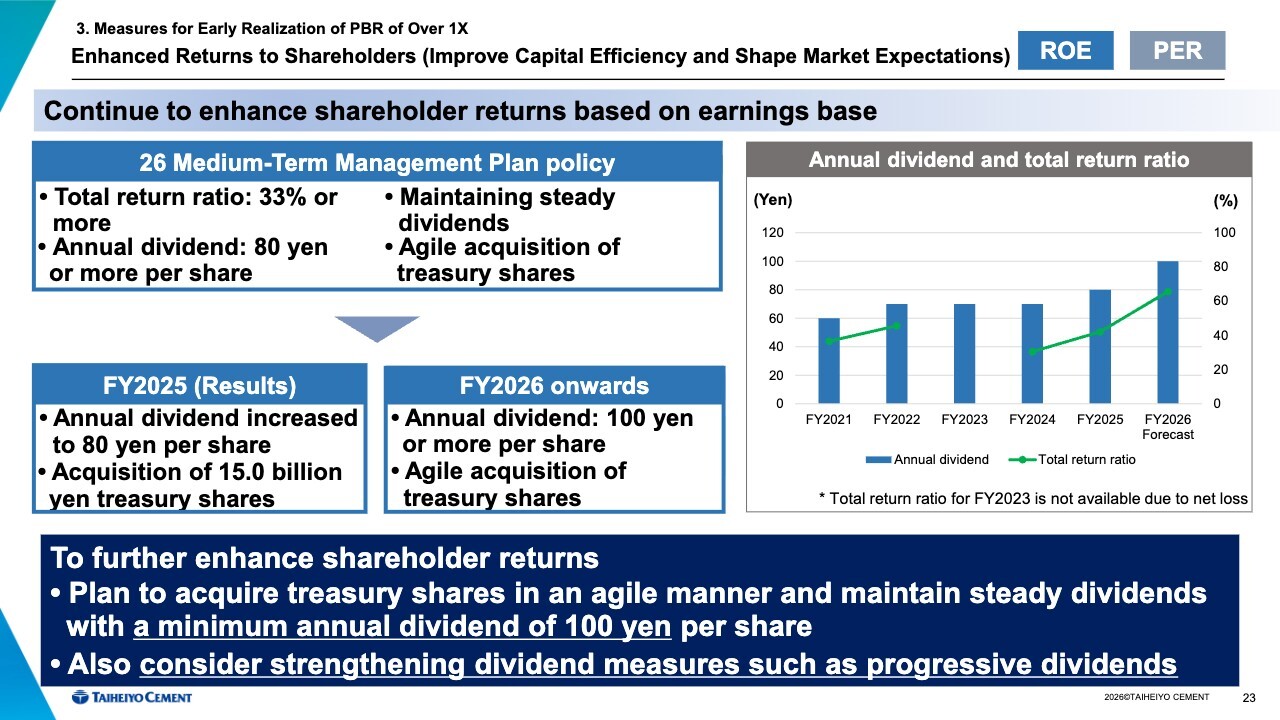

3. Measures for Early Realization of PBR of Over 1X: Enhanced Returns to Shareholders (Improve Capital Efficiency and Shape Market Expectations)

Next, regarding enhanced shareholder returns. For FY2026, we increased the annual dividend per share from the originally planned 80 yen to 100 yen.

Going forward, to further enhance shareholder returns, we plan to acquire treasury shares in an agile manner and maintain steady dividends with a minimum annual dividend of 100 yen per share. We will also consider strengthening dividend measures such as progressive dividends.

3. Measures for Early Realization of PBR of Over 1X: Strengthened Capability for Dialogue with Shareholders and Investors (Improve Market Value)

This concerns strengthened capability for dialogue with shareholders and investors. As part of our efforts, we held a briefing on our U.S. business last December.

Furthermore, as indicated in blue on the slide, while we had previously only disclosed the medium-term management plan, this was the first time we provided an opportunity to review the plan and explain our future policy.

Moreover, we plan to continue holding briefings led by top management from this fiscal year onward.

In addition, while the IR Group previously belonged to the General Affairs Department, it was transferred to the Corporate Planning Department in April in order to enhance responsiveness and ensure that the opinions of shareholders and investors are reflected in management strategy at an early stage. Through this change, we plan to promptly share opinions from the capital markets with the Board of Directors and incorporate them into management strategy.

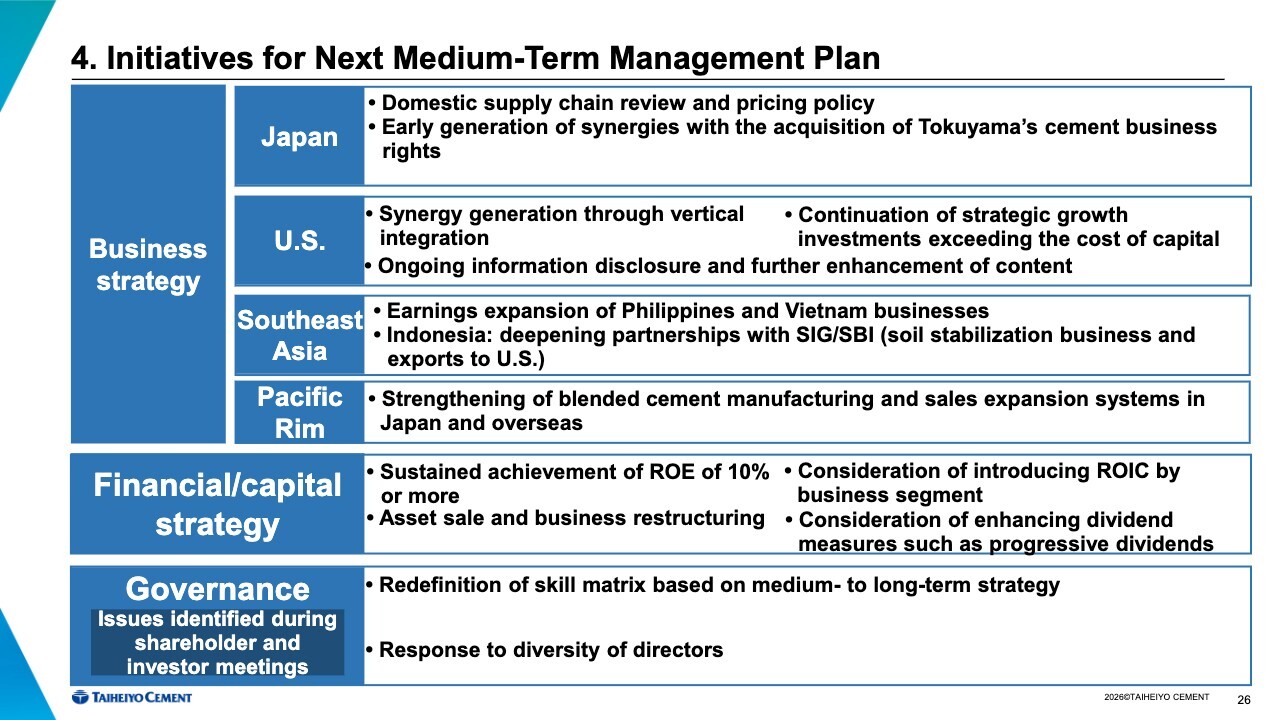

4. Initiatives for Next Medium-Term Management Plan

In conclusion, I will explain our initiatives for the next Medium-Term Management Plan, focusing on the issues and challenges identified. Domestically, a key driver is considered to be the early realization of synergies from the Tokuyama’s cement business rights, as discussed earlier.

Pricing policy is another key area. Currently, coal prices are rising somewhat in tandem with oil prices, and many other costs, including labor costs, are also increasing. We intend to steadily advance the establishment of a system to achieve cost pass-through, ensuring that customers fully understand the situation.

For the U.S. business, although approval for vertical integration has not yet been obtained, we aim to realize the benefits of the acquisition of Vulcan Materials Company’s ready-mixed concrete business as early as possible, from the second half of this fiscal year onward.

Another challenge is that the value of the U.S. business is not yet fully understood by shareholders. To address this, we plan to enhance communication by holding business briefings and providing more detailed information.

In Southeast Asia, a major focus for this fiscal year is to achieve positive operating income for the Philippines business on a single-year basis.

Regarding financial and capital strategy, we are considering introducing ROIC by business segment. While the domestic business presents particularly significant challenges, the cement, mineral resources, and environmental businesses are interconnected as a single supply chain when viewed from a broader perspective.

Therefore, it is considered easier to understand if these segments are explained as an integrated unit rather than individually. For this reason, we are considering introducing ROIC by business segment and incorporating a system in the next Medium-Term Management Plan to evaluate ROIC from an efficiency perspective.

Lastly, on governance. Since the end of last year, shareholder relations activities have been strengthened, increasing the number of meetings with shareholders and investors. Among the points raised, the skill matrix will be appropriately redefined and refined based on the medium- to long-term strategy.

Additionally, suggestions regarding board diversity have been received, and the voice of the stock market will be taken seriously and addressed promptly.

This concludes the presentation. Thank you very much.

Q&A: Projected supply volume and improvements in plant utilization and profit margins achieved through the acquisition of cement business rights

Questioner: I’m asking about the acquisition of Tokuyama’s business rights, which you have recently announced. I understand that this relates to the domestic sales business, and I would like to know the expected supply volume and how much you expect this to improve your facility utilization rate.

Respondent 1: Currently, Tokuyama supplies just under 3 million tons for the domestic market. Although demand has been declining in the near term, we aim to acquire close to 100% of this volume.

Exports are not included in this transfer. However, we will consult with Tokuyama and, if necessary, proceed with taking over their customers.

Regarding facility utilization rates, we expect an increase of approximately 10% based on a rough estimate.

Questioner: I would like to ask about the impact on profit improvement if the utilization rate increases by 10%. Would it be appropriate to consider this in terms of the contribution margin rather than the operating margin relative to net sales?

Respondent 1: That is correct. Since this transaction does not involve any significant additional investment, we expect the currently assumed contribution margin to be reflected as an improvement in profitability on the volume side.

Questioner: So, are you expecting this to improve profits to a level similar to Tokuyama’s performance, as shown on Slide 19?

Respondent 1: Exactly. In that sense, how to secure the volume has become a very significant task. We intend to work closely with Tokuyama and carefully take over the business rights that Tokuyama has cultivated over many years.

Q&A: Plans for the sale of cross-held shares

Questioner: You plan to sell approximately 20% of your cross-held shares during the current Medium-Term Management Plan period and around 50% in total by the end of the next Medium-Term Management Plan period. Please tell us your estimated value in monetary terms for each of these sales.

Additionally, please explain how you calculated the 50% target to be executed during the next Medium-Term Management Plan period, and what your policy would be regarding the remaining holdings.

Respondent 1: Regarding the figures of 20% and 50%, we established a subcommittee to examine which shares could be sold over the next year or so and which could be sold during the next Medium-Term Management Plan period, taking into account our relationships with the respective issuers. While negotiations with the other parties will be necessary, we believe it is feasible to sell shares at these levels.

In terms of the actual value, while this will depend on stock price trends, we estimate that 50% will be equivalent to approximately ¥27.0 billion of the amount recorded on the balance sheet as of the end of March 2025.

Q&A: Plans for the sales of real estate

Questioner: You mentioned sale of real estate. What is the approximate value of the real estate available for sale, and how much of it do you plan to sell?

Respondent 1: We still own a significant amount of land. However, given the various businesses conducted on these properties, the challenge is whether we can generate gains by selling that land as-is. Under these circumstances, our policy is to prioritize selling properties that will yield gains in the near term.

Questioner: Setting aside the question of whether it will yield gains, what level of proceeds are you expecting from the sale?

Respondent 1: Since negotiations are ongoing, it is difficult to provide specific figures at this point. However, we intend to sell a property of significant value by tender sometime in the near future.

Q&A: Target operating margin for the Domestic Cement Business and the barriers to price increases

Questioner: I have a question regarding your Domestic Cement Business. Yesterday, your competitor announced a price increase. Under the Medium-Term Management Plan through fiscal year 2027, your company targets an operating margin of 10%. How do you view this 10% target in the changing external environment?

Additionally, given your awareness that industry practices are changing, please tell us whether you anticipate any potential barriers or risks arising within the industry or the supply chain as a whole in connection with the next price increase.

Respondent 1: We have not given up on our target of achieving a 10% operating margin. However, the reality is that due to increases in various fixed costs, we have not yet reached that 10% mark.

Considering the current rising costs of coal and other materials, we naturally need to gain customers’ understanding and pass these costs on to prices.

Although it is difficult to take concrete action immediately due to the ongoing Tokuyama project, we recognize that we face a similar challenge. Once the review process is successfully completed, we intend to make preparations in a timely manner to announce our pricing policy.

Regarding the barriers to raising prices, in the ready-mixed concrete industry—our primary customer base accounting for 70% of our business—we have been unable to increase prices easily because it has been difficult to pass costs through to general contractors.

However, as mentioned earlier, we have recently successfully implemented price increases by making early announcements—more than a year in advance—and enabling our customers to systematically pass the costs to their downstream customers. We believe we can take this approach for the next round of price increases.

Respondent 2: To add a few points, while I’m sure you are all well aware of the situation regarding the Ready-Mixed Concrete Cooperative Association, I believe a major contributing factor is that the Cooperative Association of Tokyo District has started to raise prices on a shipment basis.

Previously, contracts signed in spring would remain unchanged for one, two, or even three years, not reflecting shipment-based prices at all. Consequently, in the ready-mixed concrete industry, there was little room to absorb increases in aggregate, labor, or cement costs even when they rose during the contract period.

However, as almost all cooperative associations have become able to raise prices on a shipment basis, I understand that this has created more room for them to absorb rising costs.

Q&A: Estimated date for completion of clearances for the Tokuyama transaction

Questioner: When do you expect the clearance process for Tokuyama transaction to be completed?

Respondent 2: I refrain from providing specific comments as we are currently in the application process with the Fair Trade Commission. While this is purely my personal opinion, I believe there are only minor factors that could hinder competition, given the current state of the industry. For example, in Kyushu, there are currently six brands, and this transaction would only reduce that number to five.

Q&A: Investment strategy and profitability improvement for the global business

Questioner: As you operate primarily in the U.S. and the Philippines, the business environment in those markets has been slow to improve. From what we’ve heard today, you seem to be prioritizing cost reductions over expansion strategies as you head into the next Medium-Term Management Plan.

While large-scale investments, including M&A in the U.S., were made under the current Medium-Term Management Plan, are you shifting your policy under the next Medium-Term Management Plan to slightly curbing overseas investments and improving profitability?

Respondent 1: Amid ongoing large-scale investments, we can look to the net debt/equity ratio as a benchmark to assess our progress. Under our initial plan, we are considering a ratio of around 0.5x as a guideline figure.

We anticipate the net debt/equity ratio will rise to approximately 0.7x after this investment in the U.S. However, using the profits generated from the acquisition of Vulcan Materials Company, we aim to ultimately reduce it to our target level of 0.5x.

Therefore, while the ratio may temporarily rise to around 0.7x, we intend to quickly lower it to our target level of around 0.5x by generating cash flow as soon as possible.

Q&A: Scheme for the acquisition of cement business rights

Questioner: Regarding the acquisition of Tokuyama’s cement business rights, is it correct to understand that the scheme used this time is similar to the one previously employed in the acquisition from Denka Company Limited?

Additionally, what are your plans for the facilities going forward? If the facilities are to be scrapped under certain circumstances, it could potentially affect the overall utilization rate of cement plants and pricing strategy given that your company will continue to produce cement at your plant. Please provide your insights on this matter within the scope you are able to disclose.

Respondent 1: As you correctly noted, it will be a scheme where we procure and sell products through an OEM arrangement. We believe there are significant advantages to shipping products from our own factory at the end of the process.

Q&A: Disposal of waste

Questioner: If Tokuyama first processes waste at its factory and subsequently processes it at a different facility two years later, will your company’s factory be the one that handles the disposal?

Respondent 1: Tokuyama has been processing coal ash from its on-site coal-fired power plants, as well as by-products and waste generated during the manufacture of chemical products, at the cement kilns within its cement plants. Naturally, if cement plant operations are suspended, processing of these materials becomes difficult; therefore, we anticipate a scheme under which our company would assume the responsibility for processing them in such cases.

Questioner: Will your company receive some disposal fees, or will this allow you to slightly reduce those costs within the cement cost structure?

Respondent 1: We are also processing waste as much as possible at each of our plants. However, with the acquisition of Tokuyama’s cement business, our production volume will increase. Accordingly we plan to accept waste generated by Tokuyama to the fullest extent possible.

Questioner: Doesn’t this mean that disposal fees will increase?

Respondent 1: As a result of acquiring Tokuyama’s cement business, Taiheiyo Cement’s overall disposal fees will increase

Q&A: Initiatives for achieving targets in the Medium-Term Management Plan

Questioner: I would like to ask about the figures in the current Medium-Term Management Plan and the vision for the next Medium-Term Management Plan. The initial plan targeted an operating income of ¥100.0 billion or more. However, the results stand at approximately ¥70.0 billion. Given the rising crude oil prices, I think it will be necessary to advance pricing strategies.

From an external perspective, the target of ¥100.0 billion appears to be quite challenging to achieve. While I assume the next Medium-Term Management Plan will also be structured with this ¥100.0 billion figure as a benchmark, could you please explain specifically what steps you plan to take during the remaining year of the current Medium-Term Management Plan to bridge the ¥30.0 billion gap?

Respondent 1: Considering Mitsubishi UBE Cement Corporation’s recent announcement of a price increase, we intend to thoroughly analyze our current cost structure and future trends in order to implement an appropriate pricing policy.

The increase in base revenue through capturing Tokuyama’s volume will be achieved mainly after the transition period ends.

If we assume the transition period will last two years, I expect the synergies to fully materialize from around the second half of FY2029. We believe we can achieve the ¥100.0 billion target set in our current Medium-Term Management Plan by steadily capturing these synergy benefits.

Questioner: Overseas, the Philippine business is currently running at a loss. However, would it be correct to understand that by recording an impairment loss to reduce costs, and assuming the U.S. business improves—though this depends on demand—the Global Business segment as a whole will make a certain level of contribution?

Respondent 1: That is our understanding.

Q&A: The relationship between the acquisition of cement business rights and price increases

Questioner: What makes it difficult to separate the acquisition of Tokuyama’s cement business rights from the price increases?

Respondent 1: The business acquisition is currently under review by the Fair Trade Commission. Under these circumstances, our top priority is to ensure we complete clearance successfully.

Questioner: Put another way, does that mean your company might be the last to announce a price increase this time?

Respondent 1: It largely depends on the moves of peer companies . We recognize that each company has a different cost structure, but energy costs have been rising recently, and labor costs and subcontracting expenses are also trending upward across the board. Therefore, we anticipate that they will take similar courses of action.

Given the upward trend in various costs, we are considering announcing our pricing policy at an appropriate time.

Q&A: The significance of the Construction Materials Business and its future direction

Questioner: Your company still operates the Construction Materials Business segment. However, this segment was not mentioned in the pricing optimization section of today’s presentation. Additionally, according to the news release, you will partially sell your stake in A&A Material Corporation and retain it as an equity-method affiliate. What is the significance of the Construction Materials Business in your company?

Respondent 1: The Construction Materials Business encompasses many different areas. For example, it includes companies like Onoda Chemico, which uses cement raw materials in powder form, as well as companies such as A&A Material Corporation and Clion, which shape cement into construction panels. As such, the Construction Materials Business covers a wide range of categories.

Among these, affiliated companies closely related to the cement business and connected to the Cement, Mineral Resources, or Environment Business segment were transferred to their respective segments in April 2025. The companies that remain under the Group Business Strategy Department are those that manufacture products such as building panels and cement admixtures.

We need to determine our approach for these companies going forward, assessing whether they generate synergies for our group and whether Taiheiyo Cement is the best possible owner for them.

We plan to explore this matter to a certain extent during this fiscal year, aiming to reach a conclusion during the next Medium-Term Management Plan period regarding whether to retain the Construction Materials Business as a single segment.

Q&A: Possibilities for vertical integration in the Japanese and Asian markets

Questioner: I would like to ask about your view on vertical integration. Building on the previous question, I believe CRH and Holcim are examples of benchmark companies in Europe and the United States. They have increased the rate of vertical integration to a very high level, and I get the impression that your company is aiming for a similar direction, particularly regarding your U.S. business.

Do you think it is possible to achieve the kind of vertical integration in Japan and Asia that leads to the pricing advantages these companies enjoy in European and U.S. markets? Furthermore, in European and U.S. markets—particularly in Europe—companies with high ratios of blended cement are leveraging the EU ETS (European Union Emissions Trading System) to gain further momentum.

I think it would be truly impressive if your company could achieve similar results in Japan. Please share your perspective on the timing for moving in this direction in the Japanese market.

Respondent 2: Frankly speaking, in Europe and the United States, market players in sectors such as cement, aggregates, and ready-mixed concrete are quite limited, making it difficult for new companies to enter the market. As a result, it is possible to achieve some degree of oligopoly in the aggregates sector. Furthermore, vertical integration in the cement sector significantly increases the proportion of ready-mixed concrete sales at plant-linked outlets.

Even if demand is dispersed across various regions, demand can be captured consistently as long as ready-mixed concrete outlets can supply a certain volume. Therefore, in countries where market entry is difficult, improving profitability through vertical integration is highly effective.

On the other hand, the situation is different in Asia. In many countries, it is easy to enter the cement plant sector, and a new ready-mixed concrete plant can be built in a short period of time; furthermore, permits for aggregates are relatively easy to obtain. We believe it will be difficult to achieve a fully integrated vertical structure in the near future.

Q&A: Structural differences and strategies in the U.S. and Asian markets

Questioner: Given the numerous measures being implemented for organizational restructuring both at home and abroad, and considering the timing discrepancies involved, I believe the resulting timing lag is unavoidable in terms of when these efforts are reflected in earnings. On the other hand, the U.S. business, for example, still has some areas that remain unclear, as was pointed out earlier today.

As was explained earlier by the company, there are structural differences between Japan and the U.S. For example, in Japan, fly ash and slag are treated as industrial waste, and the Company generates revenue from the disposal fees. In contrast, on the East Coast of the U.S., these materials are treated as resources, and the company pays to purchase them.

Because of these fundamentally different underlying structures, the proportion of blended cement is very high on the East Coast, but its adoption has not yet progressed on the West Coast. I imagine you are implementing various strategies within this complex and intricate structure. However, the challenge is that these strategies are not clearly visible on the surface.

I would like to hear not just about what you are buying or working on, but also how you perceive the strategies based on these underlying structural differences. I understand it would be difficult to discuss everything here, but could you please share one or two key points, such as what you anticipate for the market?

Respondent 2: It is true that in Japan, the market has a unique structure characterized by the high quality of slag and fly ash, as well as the practice of charging fees for their disposal.

By leveraging the Company’s strengths and CPC’s network on the U.S. West Coast, we have built a robust revenue base there. We have been earnestly considering ways to ensure that our shareholders fairly evaluate and gain a deeper understanding of this situation.

Due to the unique properties of the soil on the West Coast, which contains high levels of sulfate minerals typical of the California region, it is necessary to use sulfate-resistant cement. We are working to improve sulfate resistance by blending limestone and pozzolans into the cement.

Similarly, in the San Francisco area, we are improving sulfate resistance by blending slag into the cement. We intend to more effectively communicate that our future strategies have a competitive advantage.

In addition to these structural characteristics of the market, we operate businesses in the Philippines and Vietnam in Asia. For regions outside the U.S., including Japan, we intend to analyze how the supply and demand of so-called supplementary cementitious materials, such as slag and fly ash, will evolve in the market structure 10 or 20 years from now, and formulate our strategies accordingly.