Presentation Video https://youtu.be/OTDDJS94VGM

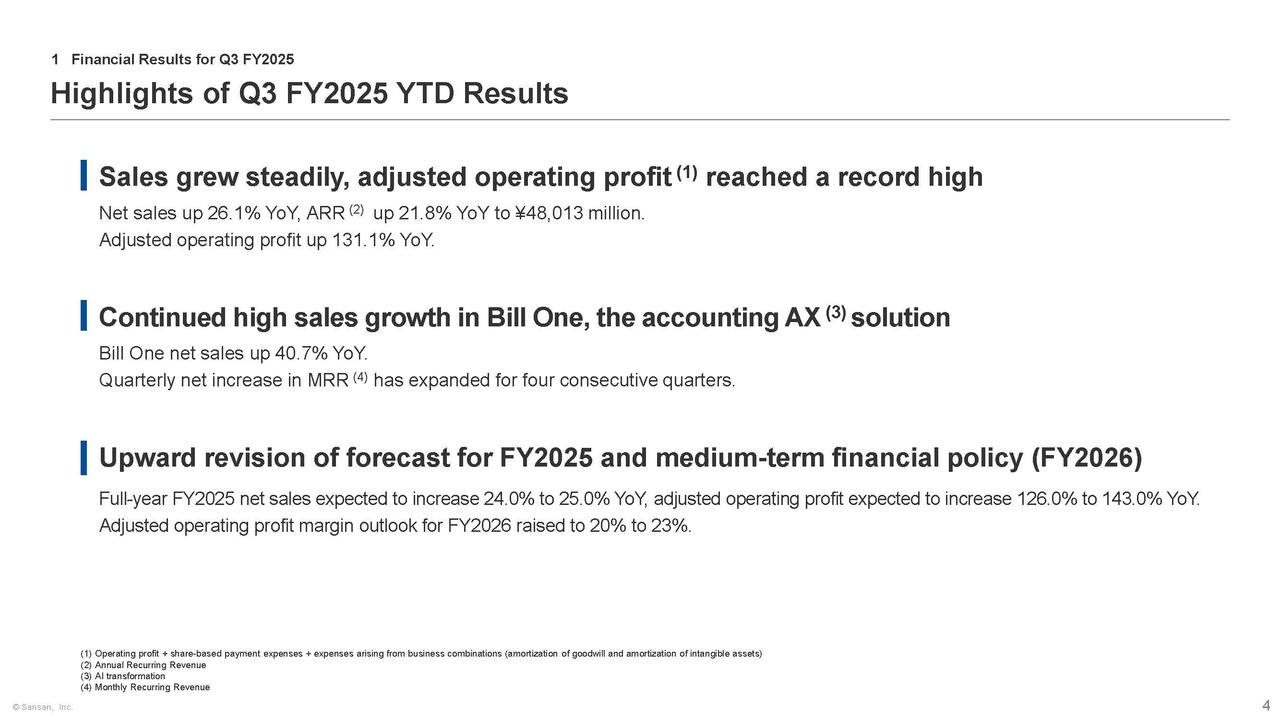

Highlights of Q3 FY2025 YTD Results

Muneyuki Hashimoto (“Hashimoto”): Thank you for joining our earnings presentation today. I am Hashimoto, the CFO of Sansan, Inc. I will present our Q3 results for the fiscal year ending May 31, 2026 (FY2025).

Please turn to page 4. Here are the highlights of our Q3 YTD of FY2025. First, net sales increased by 26.1% YoY, maintaining steady growth. Adjusted operating profit rose by 131.1% YoY, reaching a record high, driven in part by a reduction in losses from our accounting AX solution Bill One.

Second, Bill One continued its high sales growth, with the net increase in Monthly Recurring Revenue (MRR) expanding for four consecutive quarters.

Third, in light of our solid performance through Q3, we have revised upward our full-year earnings forecast for FY2025 and medium-term financial policy (FY2026).

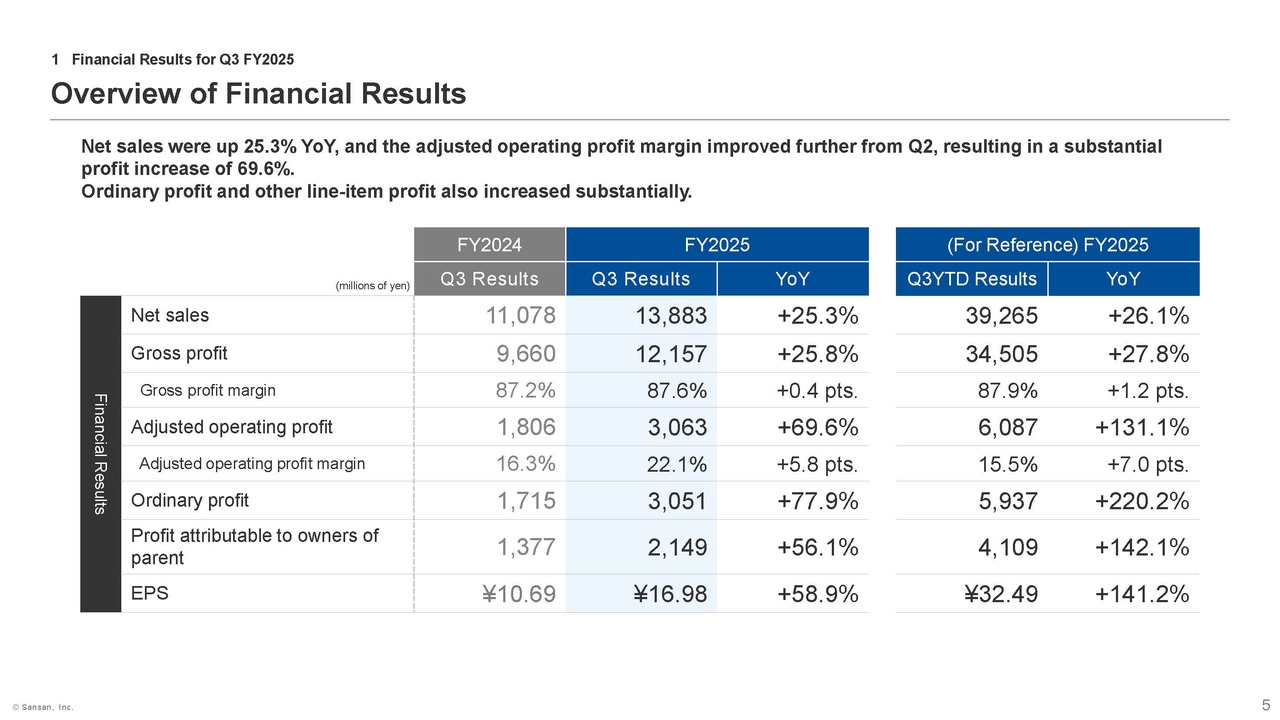

Overview of Financial Results

I will move on to the results for the 3 months of Q3. Net sales grew steadily, up 25.3% YoY, while gross profit margin improved by 0.4 percentage points YoY.

Adjusted operating profit rose sharply by 69.6% YoY, driven by both sales expansion and a decline in the SG&A ratio, marking a record high for a single quarter.

Against this backdrop, both ordinary profit and profit attributable to owners of parent saw significant increases.

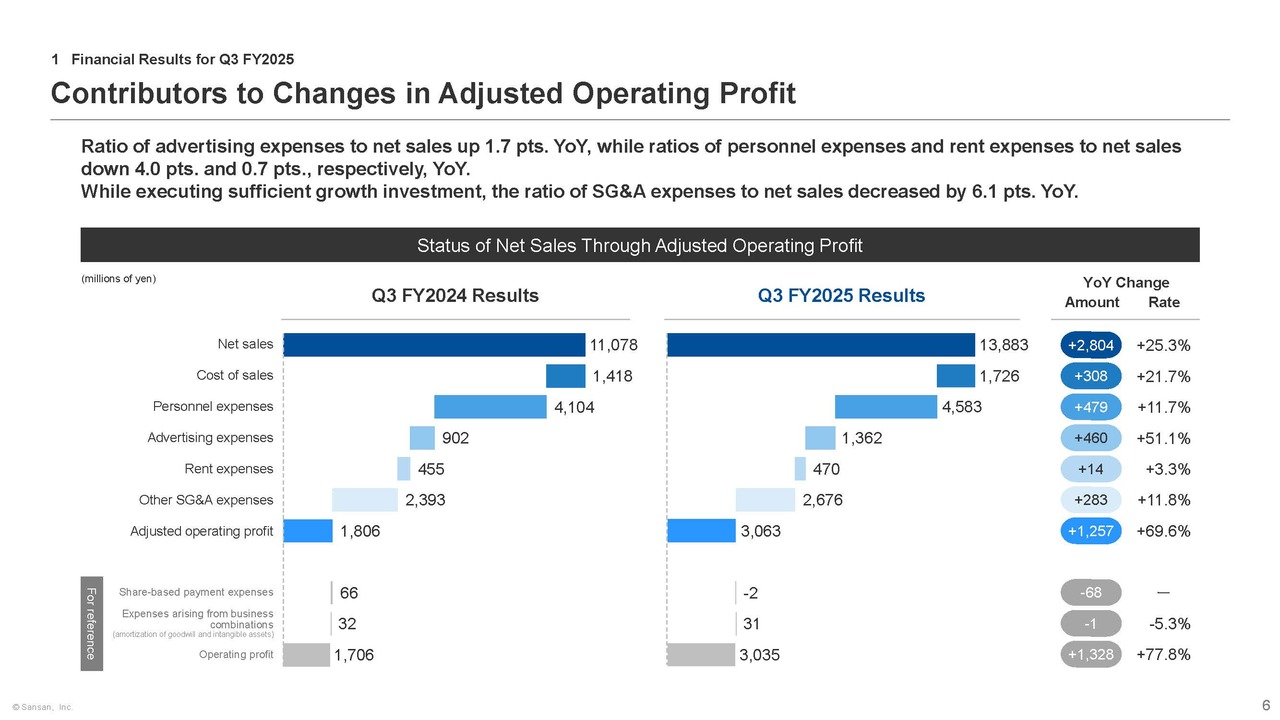

Contributors to Changes in Adjusted Operating Profit

I will now explain the details of adjusted operating profit. Net sales increased steadily by 25.3% YoY, and the cost of sales ratio decreased by 0.4 percentage points YoY.

Advertising expenses increased by 51.1% YoY due to intensified promotional activities, such as television commercials, driven by strong order intake for Bill One, and the ratio of advertising expenses to net sales rose by 1.7 percentage points. Meanwhile, the increase in personnel expenses was limited to 11.7% YoY, and the ratio of personnel expenses to net sales fell by 4.0 percentage points.

As a result, the SG&A ratio decreased by 6.1 percentage points YoY, and while continuing to make the investments necessary for growth, adjusted operating profit saw a significant increase of 69.6% YoY.

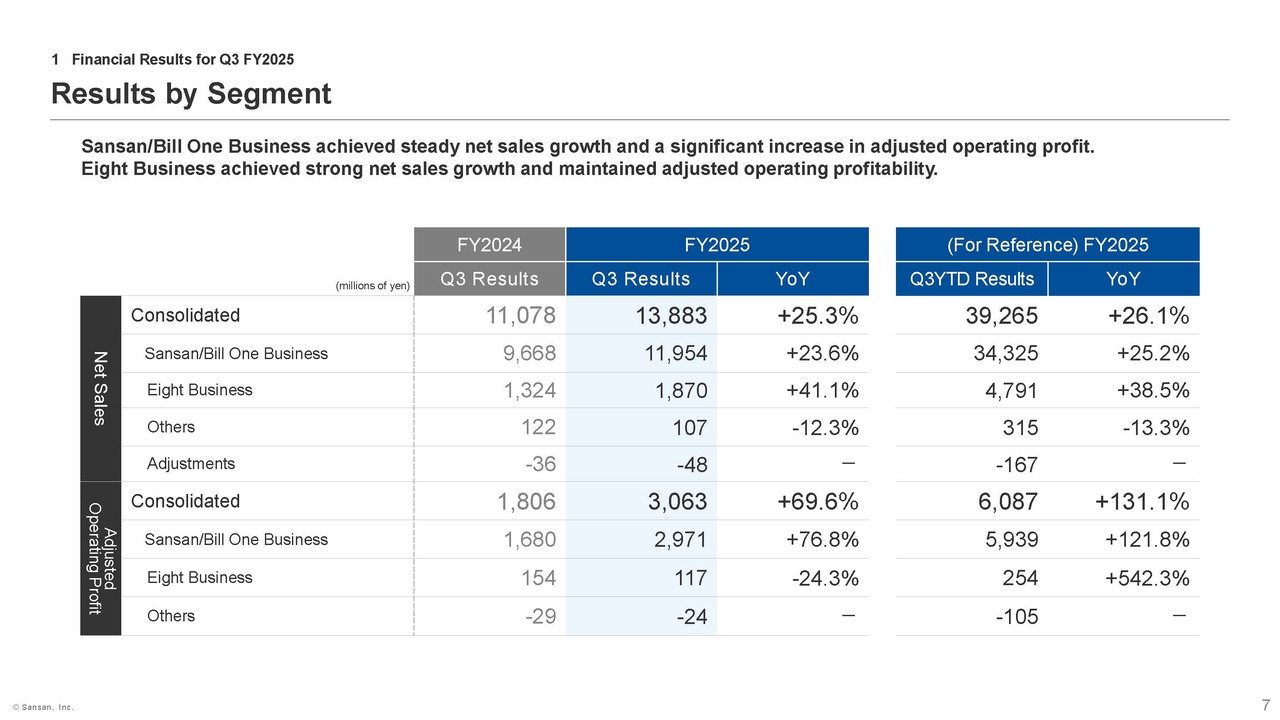

Results by Segment

Next, I will talk about the overview by segment. The Sansan/Bill One business continued to report steady net sales growth and a significant increase in adjusted operating profit.

Although the Eight business continued to report strong net sales growth, it reported a decrease in adjusted operating profit 24.3% YoY. Nevertheless, it remained profitable.

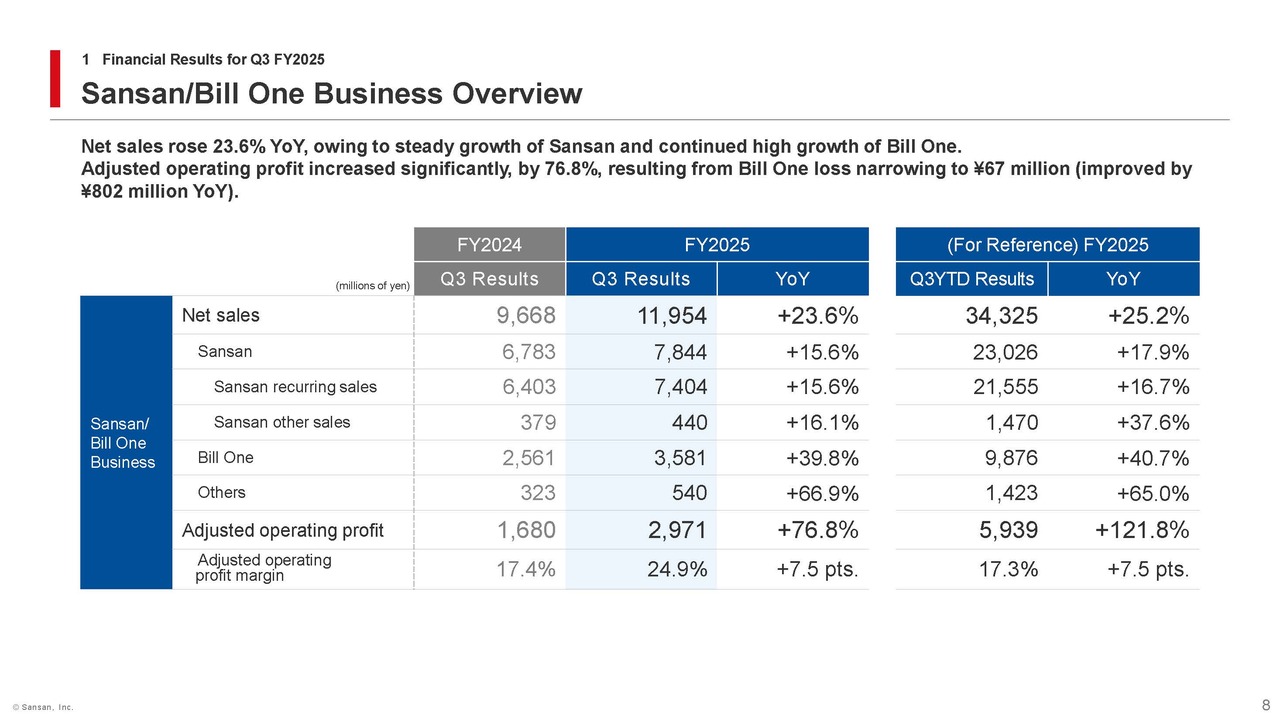

Sansan/Bill One Business Overview

Next, starting on page 8, I will explain the details by segment. Net sales for the Sansan/Bill One business increased by 23.6% YoY, driven by steady growth in Sansan and continued high growth in Bill One.

In addition, “Others,” which includes the performance of Contract One and Ninout Inc., a group company, also performed well and contributed to sales growth. Of which, Contract One sales increased by 101.9% YoY, and the number of subscriptions reached 653, a 102.2% increase YoY. Furthermore, Annual Recurring Revenue (ARR) has been expanding steadily, exceeding ¥1.0 billion as of the end of March 2026.

Adjusted operating profit rose sharply, up 76.8% YoY. By solution, improved profitability in Bill One contributed significantly; it turned a profit in a single month in certain months during Q3, and the net loss was reduced to approximately ¥60 million, improving about ¥800 million YoY. Additionally, Sansan reported a 19.2% YoY increase in adjusted operating profit.

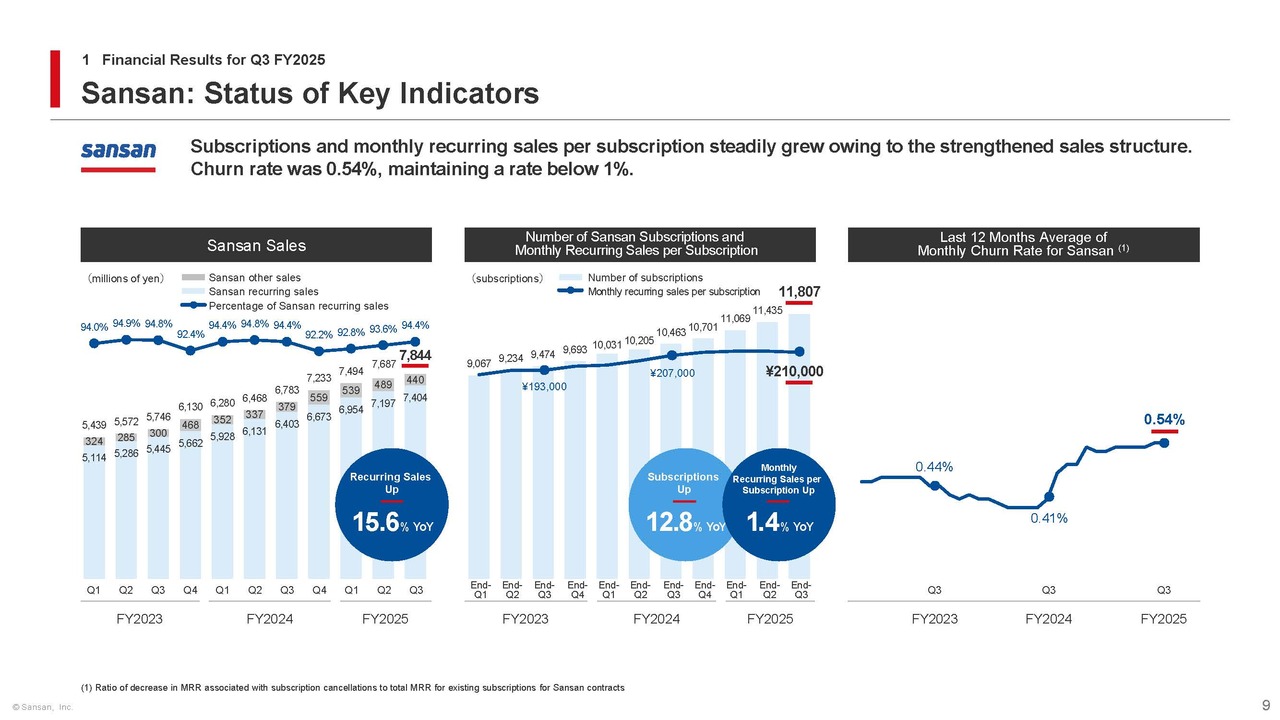

Sansan: Status of Key Indicators

Here is an explanation of KPIs for Sansan. The left side of the slide shows recurring sales with a solid 15.6% YoY growth.

As shown in the graph in the center of the slide, the number of Sansan subscriptions increased by 12.8% YoY on a period-end basis, with a net quarterly increase of 372 subscriptions, accelerating growth from Q2. The monthly recurring sales per subscription rose by 1.4% YoY and showing a high level-performance.

The graph on the right side of the slide shows the last 12 months average of monthly churn rate. In Q3, it stood at 0.54%, which is roughly the same level as in Q2, maintaining at a stable, low rate below 1%.

Furthermore, the reasons for cancellation remain unchanged and are based on circumstances specific to each company. For example, we are not aware of any cancellations resulting from companies developing in-house systems to replace Sansan by using generative AI.

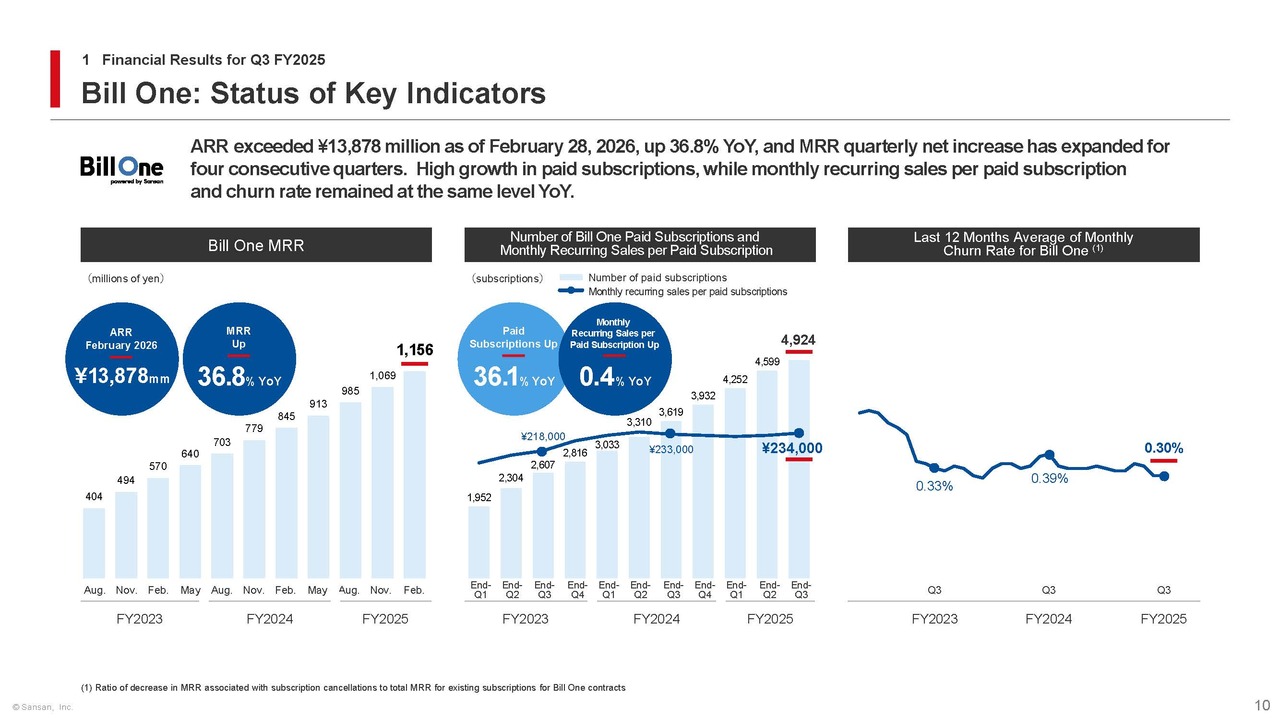

Bill One: Status of Key Indicators

Next, please turn to page 10 for the KPIs of Bill One. On the left side of the slide, MRR reached approximately ¥1,156 million, up 36.8% YoY. This represents a net increase of approximately ¥86 million from the end of Q2, marking the fourth consecutive quarter of growth in quarterly net increase.

Next, in the center of the slide, the number of paid subscriptions increased by 36.1% YoY, with a net quarterly increase of 325 subscriptions. This also continues the stable growth of exceeding 300 subscriptions per quarter since Q3 of the previous fiscal year. Both monthly recurring sales per paid subscription and the last 12 months average of monthly churn rate improved slightly YoY and remained at healthy levels.

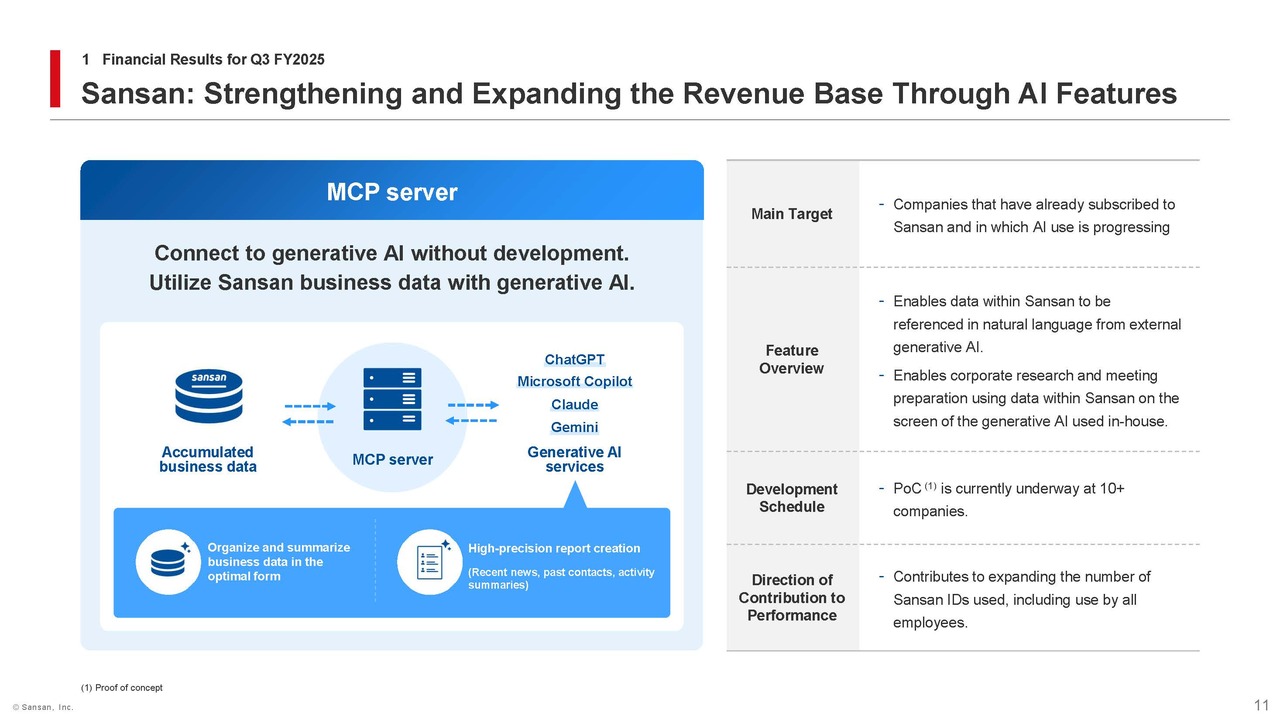

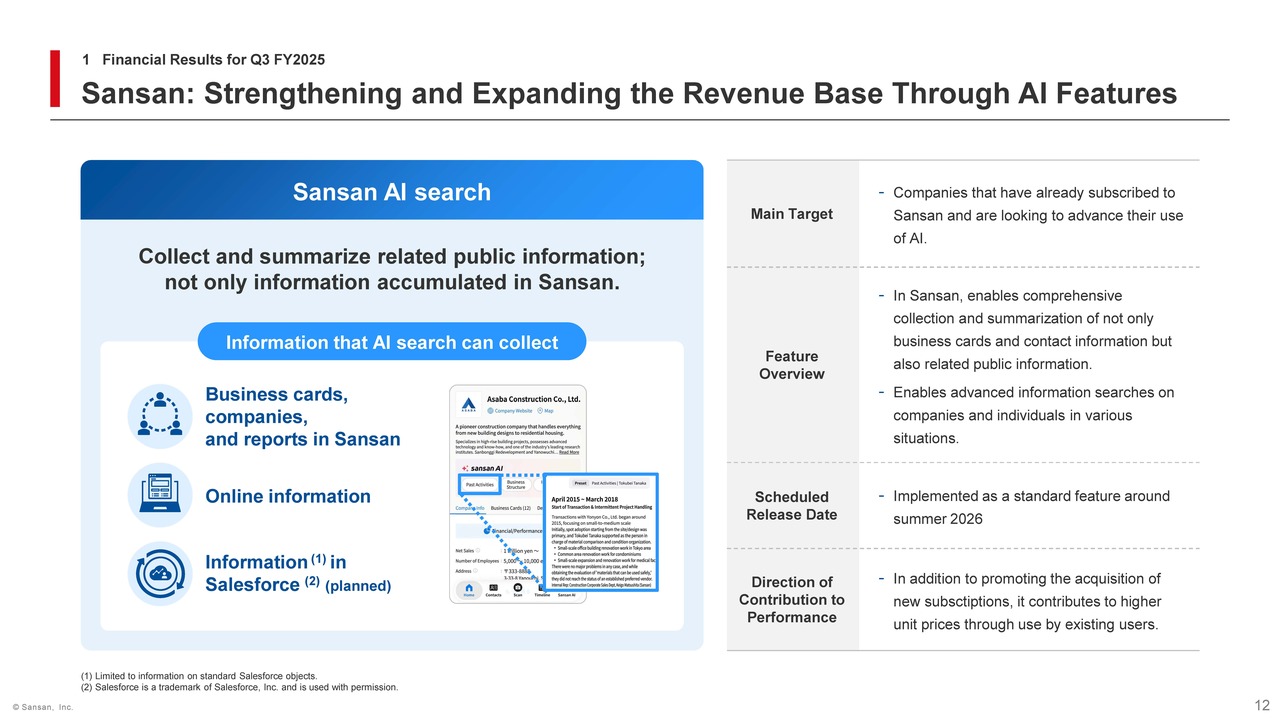

Sansan: Strengthening and Expanding the Revenue Base Through AI Features

Next, I will explain the development status of AI-powered features for Sansan, Bill One, and Contract One, as well as how these are expected to contribute to our future performance.

First, let me introduce the Sansan MCP Server, which we announced in our financial results for FY2024. This feature enables users to directly retrieve business card-based contact data and contact history stored in Sansan from generative AI tools such as Microsoft Copilot that they use within their own organizations. In essence, it serves as a bridge connecting Sansan with external generative AI.

Since launching PoC last November, we have conducted extensive testing with more than 10 early adopters, primarily large companies, and have identified a key challenge. Specifically, we found that simply feeding data from Sansan to external AI system results in variations in the quality of the output. This is because the accuracy of the responses and the way they are summarized depend on the performance of the AI models used by each company and the instructions provided by users.

To address this issue, we are currently updating our system at Sansan to incorporate AI, so that data is organized and processed into the optimal format for each specific use case before being passed on to external AI systems. This will enable Sansan to generate highly accurate reports covering, for example, recent news, past interactions and summaries of activities, which external AI systems can then utilize directly.

As a result, users will be able to easily elicit accurate responses from generative AI without having to deal with complex settings or advanced prompt design.

Sansan: Strengthening and Expanding the Revenue Base Through AI Features

Launched last November, Sansan AI Agent differs from the Sansan MCP Server mentioned earlier. It is an AI feature that operates entirely within Sansan. With Sansan AI Agent, users can use natural language to access and utilize data within Sansan as well as data from sales tools integrated with Sansan, all directly within the platform.

This Sansan AI Agent was a fairly large-scale feature, essentially a fully customized solution. However, we were able to confirm a clear customer need for it, as evidenced by our success in securing several major contracts.

That said, if we were to keep this fully customized version as is, the number of companies able to adopt it would inevitably be limited. Therefore, in order to attract more users going forward, we have decided to reorganize the key features of Sansan AI Agent into Sansan AI search and make it easier to use within the Sansan platform.

For example, using Sansan AI search, users can instantly generate highly accurate lists by cross-referencing business cards, contact history, and relevant publicly available online information. So, it can even respond to highly abstract instructions such as identifying “companies with which we already have a relationship” and “companies with which we have no relationship” among those in the manufacturing sector that are advancing digital transformation.

We plan to roll out these features in phases, with a view to fully implementing them around this summer. We believe that expanding our AI capabilities will not only help us acquire and retain new customers but also increase unit price per existing customer.

We believe that as we develop these features and increase the utilization of the data accumulated in Sansan, the value of the database itself will also grow. The source of this value lies in primary information, such as business cards and contact histories, that generative AI cannot obtain from publicly available information.

Because Sansan is structured to continuously collect and accumulate this primary information through the use of its services, we expect that as AI adoption advances, this structural strength will be further reinforced, leading to increased competitive advantage and enhanced value with the generative AI evolution.

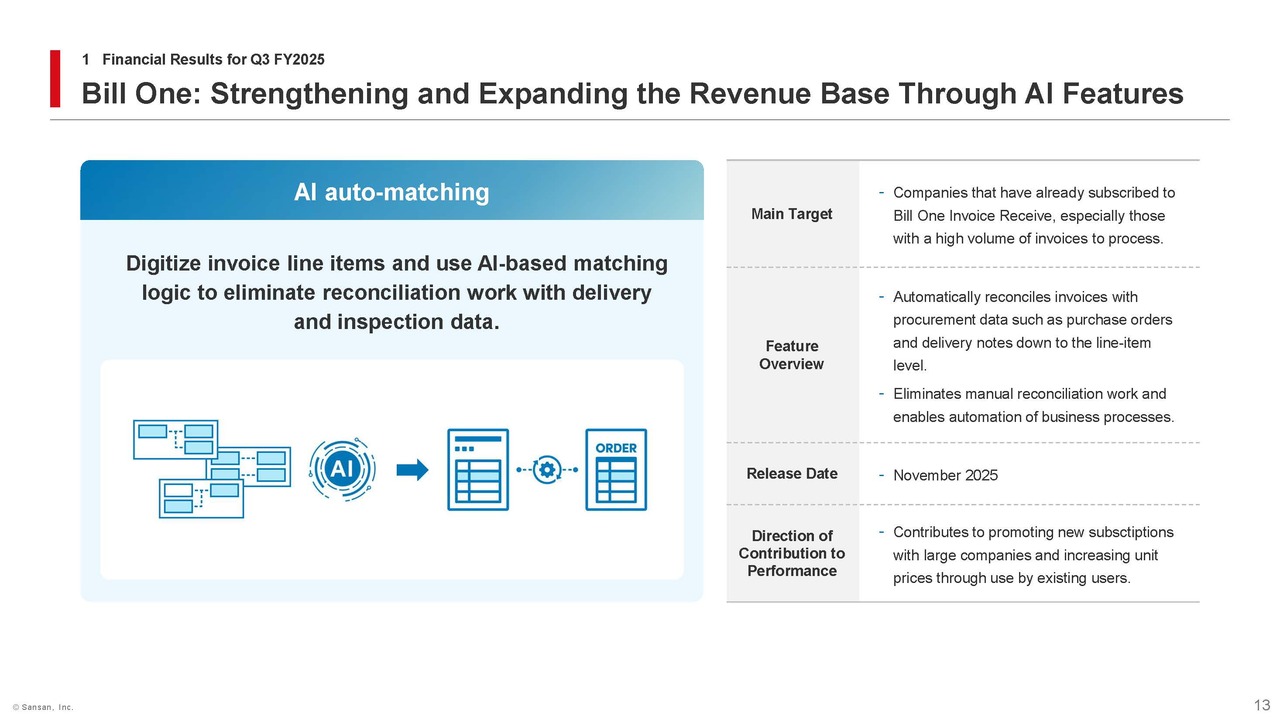

Bill One: Strengthening and Expanding the Revenue Base Through AI Features

Next, I would like to explain the current status of AI-powered features in Bill One and their contribution to our performance. First, in November of last year, we launched AI auto-matching as an optional feature. This feature matches the details of invoices and delivery notes received by a company with the details of purchase-related documents, such as purchase orders and acceptance certificates, at both the total amount and line-item levels.

Companies conduct these reconciliation processes to prevent overpayments and other issues. But in many cases, this work is performed manually by staff, resulting in a significant operational burden. This is an area where both the workload and costs are particularly high, especially in cases where statements contain thousands of lines or where companies must allocate dozens of staff at the end and beginning of each month. Under such circumstances, there is a very high demand for this feature, making it a key priority for improving operational efficiency within companies.

Since this feature enables significant reductions in man-hours and costs, we have received a great deal of positive feedback since its announcement. Even before the feature was officially launched, we secured a deal worth approximately ¥42 million in ARR from a single client that included the auto-matching option. Furthermore, in Q3 when the feature was launched, we secured another deal worth approximately ¥28 million in ARR from a single client, indicating a strong start.

We anticipate that as this feature becomes more widely adopted, it will not only increase the average revenue per user for Bill One but also accelerate the adoption of Bill One Invoice Receipt and lead to the acquisition of high unit price projects, including those from enterprise clients.

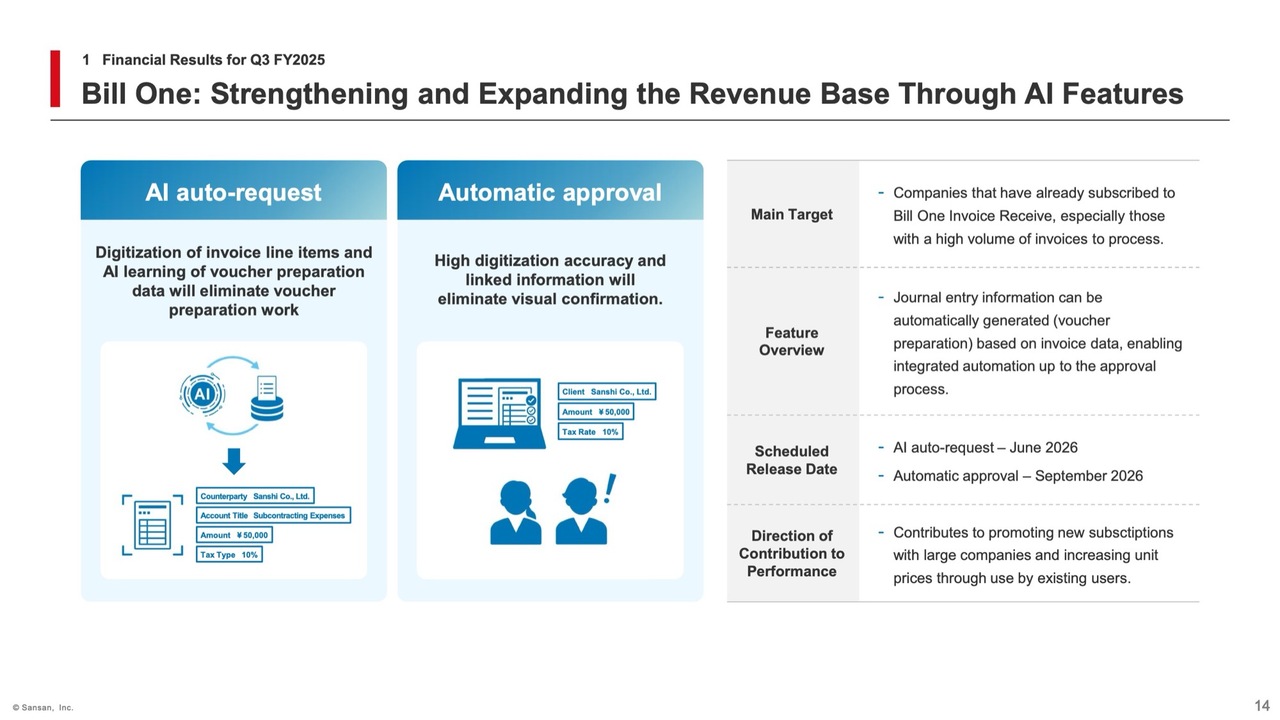

Bill One: Strengthening and Expanding the Revenue Base Through AI Features

Next, let me touch on our AI auto-request, feature, which is scheduled to launch around summer 2026. First, in accounting, voucher preparation work refers to the process of entering accounting items, amounts, and other details based on invoice information to generate vouchers for internal approval.

AI auto-request is a feature that automates the voucher preparation work by using AI to automatically input and suggest accounting items, tax rates, and other details based on the line-item data from received invoices and historical invoice data. As staff members create vouchers daily in Bill One, processing information is accumulated in the learning database, automatically improving the AI's processing accuracy and significantly reducing the workload.

In addition, we are exploring a new feature called Automatic approval, which uses AI to automatically verify the details of submitted vouchers against the invoice data, thereby streamlining the approval process. Although this feature has not yet been released, we have already received a great deal of positive feedback, including new orders placed in Q3 based on the expectation that this feature will be available. Therefore, we expect it to contribute to the future growth of Bill One.

The ability to offer features such as AI auto-matching, AI auto-request, and Automatic approval is made possible by the fact that Bill One is designed to capture primary information, specifically invoices, and digitize it with high precision down to the line-item level.

Invoice processing is a process comprising multiple closely linked stages, ranging from receipt to matching, voucher preparation, approval, and journal entry. To truly achieve business automation through AI, both accurately digitized primary information and a system that consistently supports the entire business process are essential. By capturing the process from the very start of invoice processing, Bill One offers the advantage of being able to automate subsequent business processes as a unified whole, which also creates opportunities to expand the value it provides.

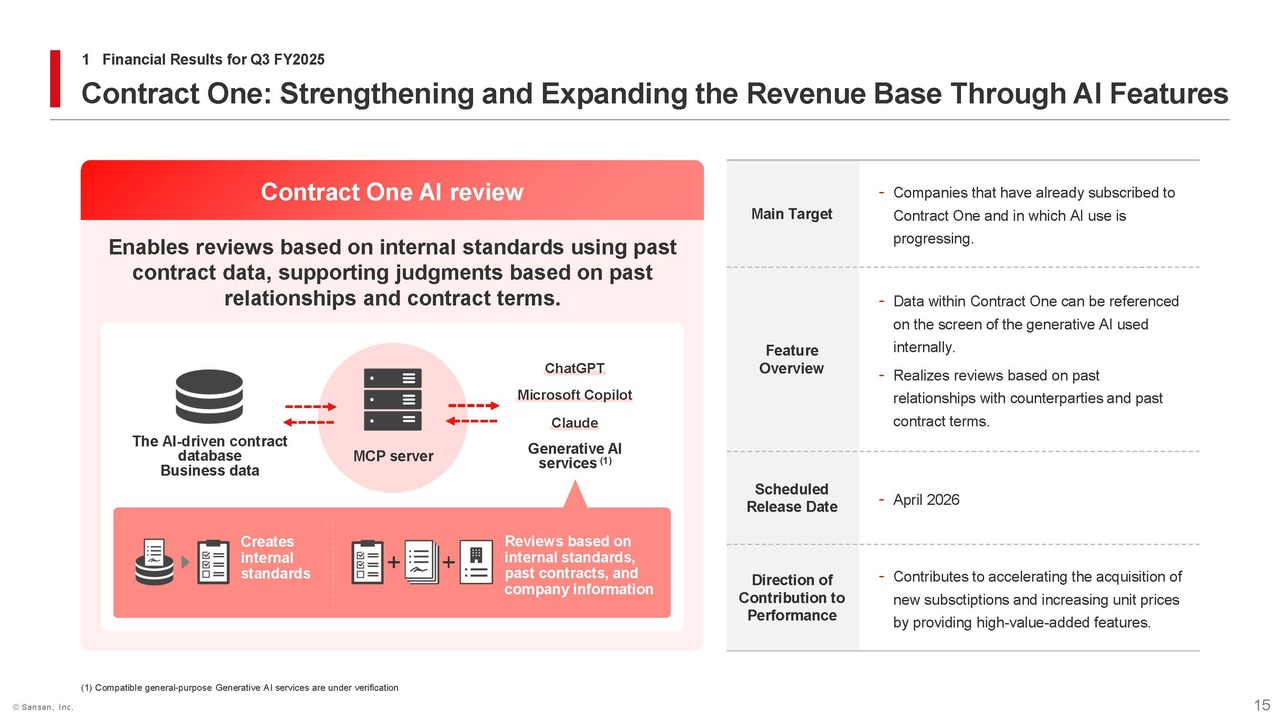

Contract One: Strengthening and Expanding the Revenue Base Through AI Features

Finally, I would like to explain the current status of development regarding AI-powered features in Contract One. While there are currently AI-powered contract review services available on the market, our understanding is that most of them primarily focus on verifying compliance with laws and general review criteria, or comparing contracts against the company’s own templates.

On the other hand, what is required in the business world are practical decisions that take into account relationships with business partners and past contract terms. To meet these needs, Contract One is launching an AI review feature that enables users to make judgments based on internal standards using historical contract data.

Contract One leverages the data digitization and data integration technology developed through Sansan to accurately identify and link contract information for each counterparty—ranging from past contracts to the latest memorandums of understanding—and organize it into a structured database. This enables users to utilize generative AI to review contracts based on their company’s unique criteria, such as assessing whether terms are favorable or unfavorable, while taking into account past similar cases and the contractual history with the relevant party.

In terms of implementation, we will build an environment that allows users to access the Contract One database via the MCP server from the generative AI tools they normally use, such as Claude. As a result, users will be able to obtain responses based on past contractual decisions and review contracts according to the terms specific to each counterparty, all from within their familiar AI environment.

Contract One AI review is scheduled to launch in April 2026. By further enhancing the value proposition of Contract One, we aim to drive further business growth, including the acquisition of new contracts.

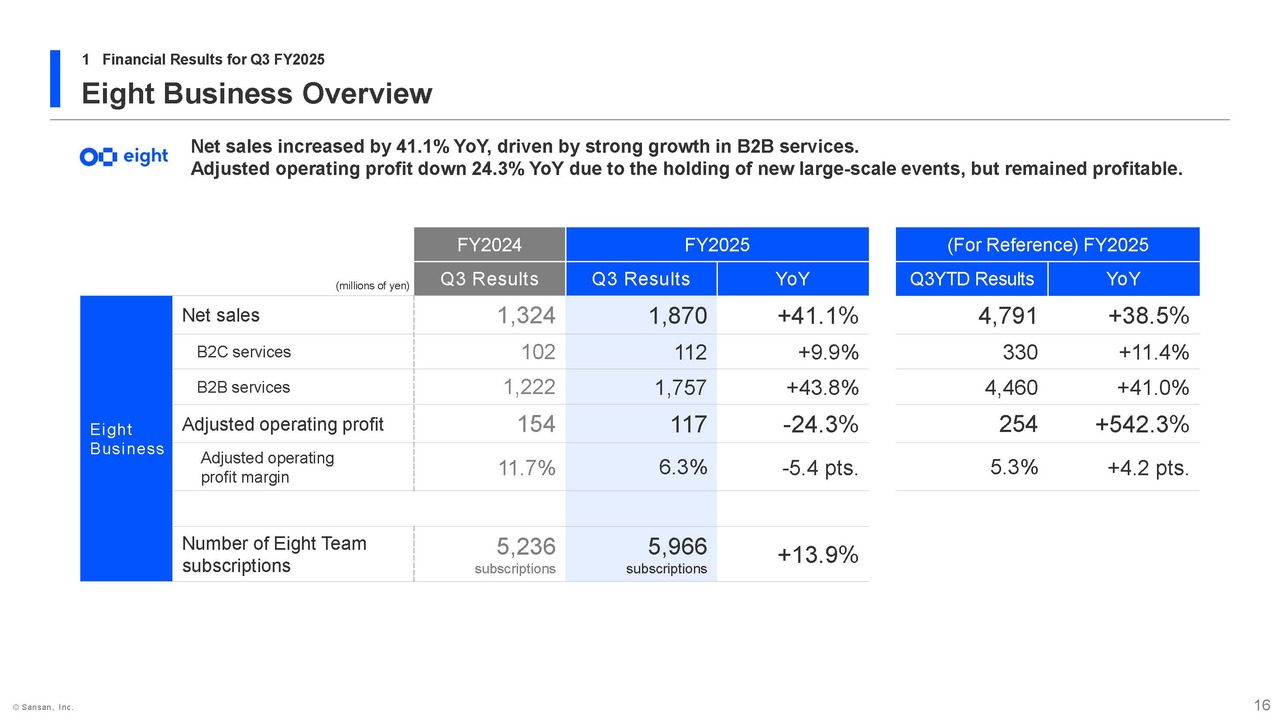

Eight Business Overview

I will now explain the Eight business on page 16. Net sales from B2C services increased 9.9% YoY. Net sales from B2B services increased by 43.8% YoY, driven by steady growth in business events and strong growth of recruiting platform. As a result, net sales for the Eight business increased by 41.1% YoY.

Adjusted operating profit decreased by 24.3% YoY due to a slight decline in profitability resulting from our efforts to commence new large-scale events aimed at sustaining robust growth in the coming fiscal year and beyond. However, we remain in the black. We have achieved a significant increase in profit for the Q3 YTD, so there are absolutely no concerns.

Upward Revision of Forecast for FY2025 and Medium-Term Financial Policy (FY2026)

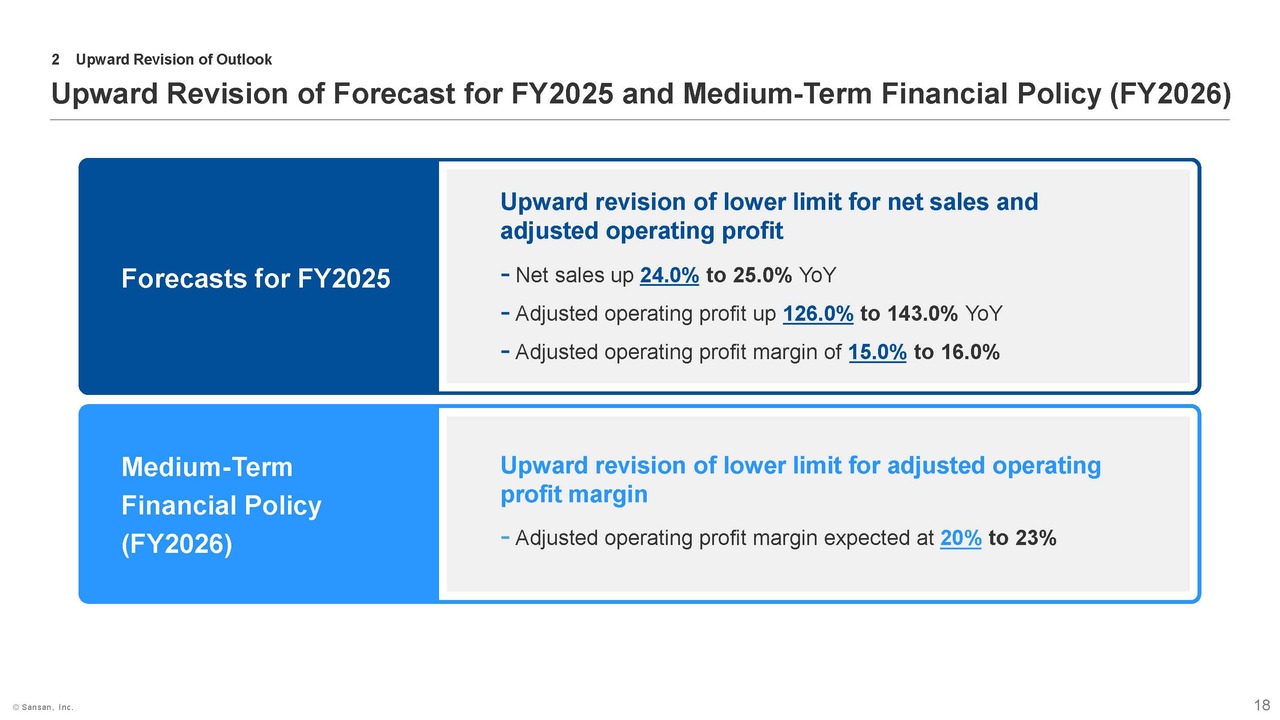

Next, let me explain the upward revision to our earnings forecast on page 18. In light of our performance through Q3, we have revised upward our full-year earnings forecast for FY2025 and our medium-term financial policy, so I will explain these in order.

Upward Revision of Forecasts for FY2025

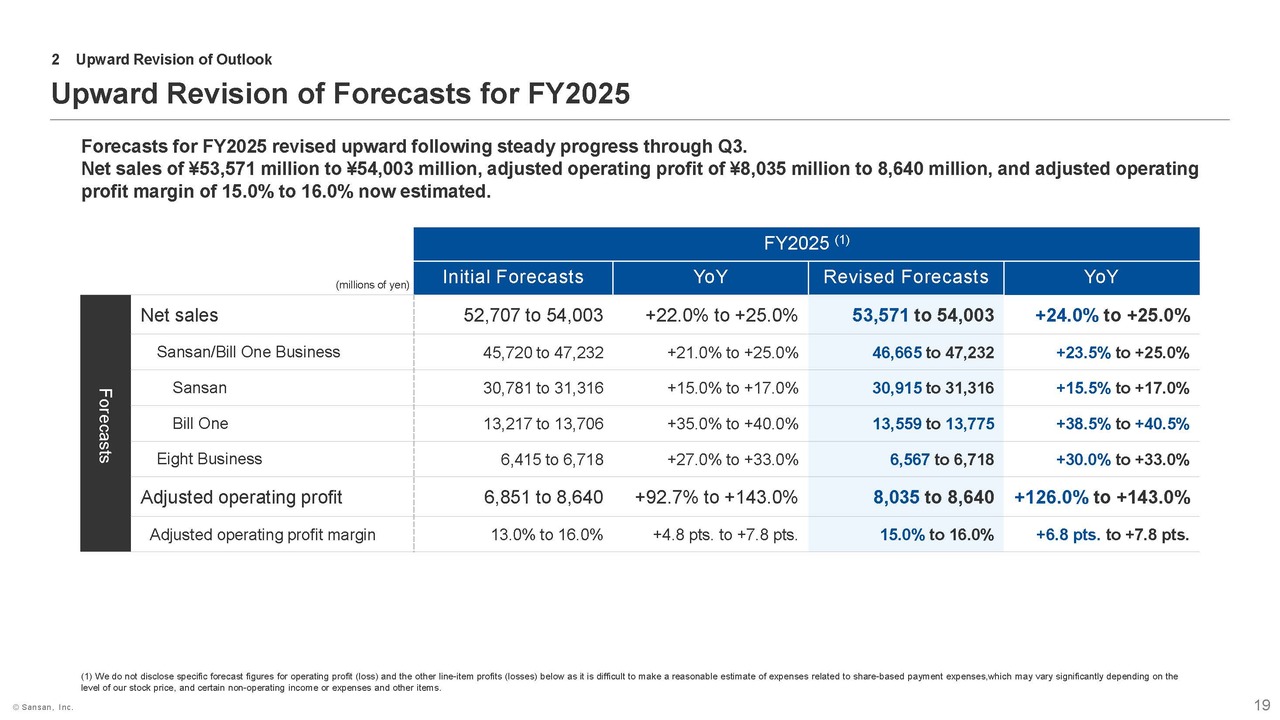

First, please turn to page 19 for details on the upward revision to our forecast for FY2025. Against the backdrop of steady growth across all our solutions, we have raised the lower end of our net sales range and now expect a YoY increase of 25.0%, up from the previous forecast of 24.0%.

In addition, we have raised the lower end of the range for adjusted operating profit, projecting a YoY increase of 143.0% (up from 126.0%), and expect the adjusted operating profit margin to be 16.0% (up from 15.0%).

Upward Revision of Medium-Term Financial Policy (FY2026)

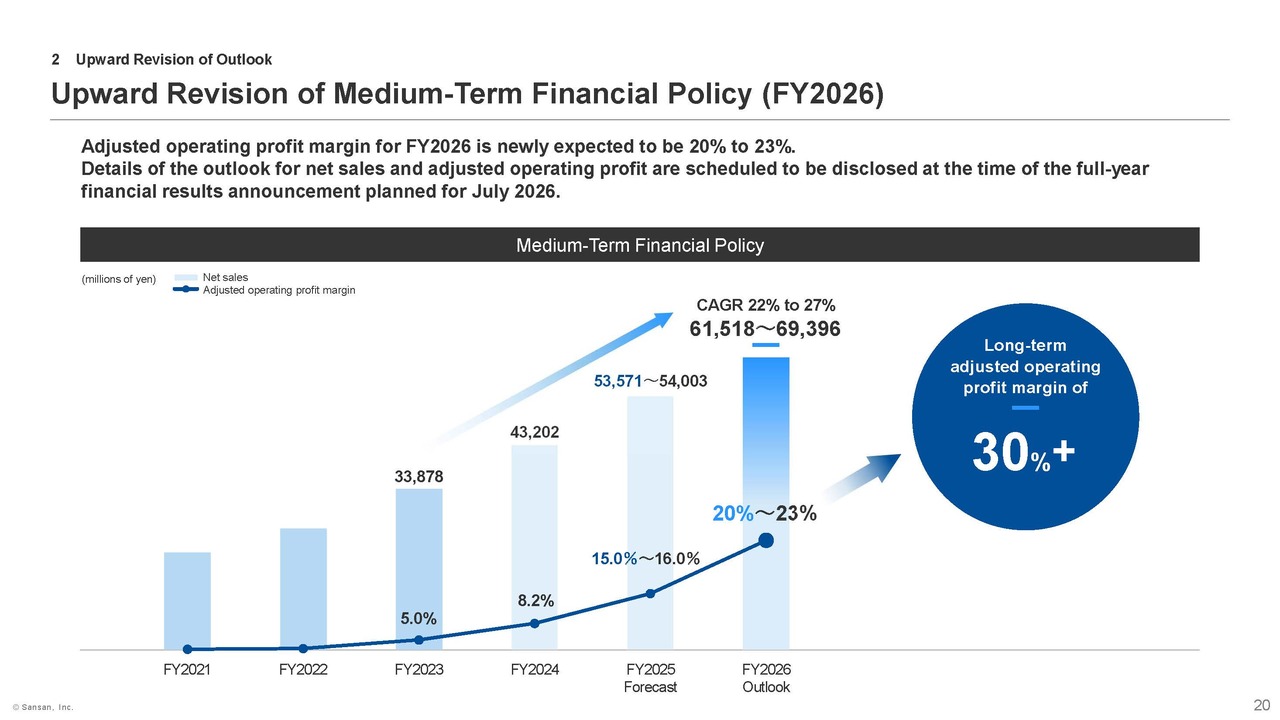

Next, please turn to page 20 for our medium-term financial policy. Previously, our medium-term financial policy set the target range for next fiscal year’s adjusted operating profit margin at 18% to 23%. However, in light of the strong profit performance this fiscal year, we are raising the lower limit and revising the target range upward to 20% to 23%. Please note that at this time, we have only revised the adjusted operating profit margin outlook; details regarding net sales, adjusted operating profit, and other metrics will be disclosed during the full-year financial results announcement planned for July 2026.

Looking back at our performance to date, both net sales and profits have been trending steadily, with profits in particular growing at a pace that exceeds our expectations. This is largely due to the significant reduction in losses at Bill One, which continues to experience high growth, as well as the fact that Sansan, our major revenue source, has entered a phase where it is consistently generating profits.

We recognize that, amid the rapid development of generative AI, there remains a sense of caution regarding the medium- to long-term growth prospects of SaaS companies in the current stock market. As we have explained, we view the advancement of generative AI not as a risk, but as a business opportunity.

By building on this strong current performance into the next fiscal year and the year after, we will achieve further sales growth and improved profit margins.

That concludes my presentation. Thank you very much.

Q&A: Trends in order volume

Questioner: You have mentioned there have been no adverse effects, such as cancellations, resulting from customers’ decision to develop an in-house system using generative AI as an alternative to Sansan. Additionally, regarding order trends, I have confirmed in the materials that new orders for Bill One are performing well. In light of this, I would like to ask whether there are any signs of a slight weakening in order trends, including those for Sansan.

Hashimoto: As you mentioned, new order intake for Bill One is going very well. On the other hand, regarding Sansan, unfortunately, orders declined slightly in Q3 YoY.

One contributing factor is that we adjusted our service prices during the same period last year. Now that this process has run its course, the increase in unit price per existing customer has slowed somewhat.

Another factor is that, across the market, we are seeing that for many companies, determining how to leverage generative AI within their organizations has become a top priority. There is also a tendency to prioritize investment in generative AI, which means that Sansan may not yet be at the top of their list of priorities.

We will continue to emphasize that leveraging Sansan services to organize data is essential for effectively utilizing generative AI. We plan to implement measures to this end in Q4, and we expect orders to recover going forward.

Questioner: I think it is virtually impossible to build something on par with Bill One or Sansan from scratch. On the other hand, have you noticed a trend toward small companies developing and selling similar services that follow the “you get what you pay for” principle?

Hashimoto: To the best of our knowledge, we are completely unaware of any such situation. Of course, when it comes to managing business cards on an individual basis, I believe it is certainly true that developing apps using tools like Claude has become easier than ever before.

However, if that’s the case, then Eight can also be used for free. Of course, developing an app on your own may be worthwhile, but our experience suggests that for most companies, there isn’t much point in building a similar service in-house as part of their regular operations.

Q&A: Trend in the number of employees and recruiting policy

Questioner: I have a question on the trend in the number of employees. While the ratio of personnel expenses to net sales has decreased and the adjusted operating profit margin has improved significantly, the number of insured employees appears to be declining considerably each month.

Is this net decrease the result of difficulties in recruiting staff and a certain level of turnover? Or is the company intentionally adjusting its headcount downward? What is the rationale behind your approach to staffing levels?

Hashimoto: While our headcount has decreased from Q1 to Q2 and from Q2 to Q3, this trend is in line with our expectations. During the previous fiscal year, the entire company experimented with and evaluated “how to utilize AI.” Furthermore, during H1 of this fiscal year, we actively worked internally to improve operational efficiency through the use of AI. As a result, we recognize that we have increased individual productivity in both front-office and back-office operations and are beginning to be able to handle the same workload with fewer staff members.

On the other hand, there are many tasks that can be handled by only humans. Therefore, while not to the same extent as in the past, we have resumed our proactive hiring efforts starting in Q3 and are strengthening our policy to ensure we have sufficient staff. New graduates are scheduled to join the company in April of Q4, and we expect our headcount to increase as we approach the end of the fiscal year.

Therefore, to answer your question, while we significantly curtailed hiring during H1 of the year due in part to improvements in productivity. However, we are now expanding our hiring again looking ahead to H2 of the year.

Q&A: Relationship between hiring controls and profit growth trends

Questioner: While the revenue growth trend continues, it is impressive that the company has managed to achieve solid revenue growth without significantly increasing its workforce. I believe your company made a significant investment in advertising from Q2 through Q3. Considering the lead time involved, I personally feel that the effects of that investment continued through Q3.

Are you suggesting that, even without these measures, you can continue to operate while maintaining the current level of revenue growth with this number of staff?

Hashimoto: That’s right. While the drivers of growth and new orders do depend in part on the number of high-quality sales force we have, new hires don’t immediately contribute to our performance.

Therefore, we will grow the company by expanding our workforce and strengthening our capabilities. In the process, we will undertake new initiatives while also ensuring that sufficient resources are allocated to our existing operations. While staff turnover is inevitable, we will make sure to fill those positions effectively. We feel confident that we can keep the business running smoothly even as we adopt a more restrained approach to hiring than in the past.

Q&A: Interpretation of the upward revision to the full-year earnings forecast for FY2025 and the medium-term financial policy

Questioner: Should these upward revisions be interpreted as “you don’t need to increase you workforce as much as originally planned because productivity has improved”? Or should it be interpreted as “costs were lower than expected”?

Hashimoto: From management’s perspective, as is often said, we believe that certain tasks performed by junior staff can now be entrusted to AI to a certain extent. I believe this applies not only to engineering but also to front-line roles such as sales.

Therefore, while we must continue to prioritize the recruitment of senior-level talent, there is no longer a need to hire as many junior-level staff to handle day-to-day operations.

Q&A: Outlook for adjusted operating profit in Q4

Questioner: I would like to ask the financial results for FY2025. If back out Q4 from the cumulative figures, adjusted operating profit is estimated to be between approximately ¥1.95 billion and ¥2.55 billion, and a slight decrease is anticipated compared to Q3. How should I make of this?

Hashimoto: While we invested in TV commercials and other initiatives during Q3, we plan to increase our marketing investments, including TV commercials, even further in Q4 compared to Q3.

In addition, as I mentioned earlier regarding personnel expenses, a large number of new graduates will be joining the company in April. While the recruitment of new graduates is similar to that of junior employees, we view them as key personnel who will eventually lead the company, and we have hired 105 employees. Including mid-career hires, the number of employees is expected to increase by approximately 190, and the associated costs are expected to be reflected in Q4.

Q&A: Advertising expenses for FY2025

Questioner: What level of advertising expenses should we anticipate for FY2025?

Hashimoto: Although the initial plan estimated the cost at approximately ¥6.5 billion, we expect it to exceed that figure slightly. We anticipate the cost will be between approximately ¥6.6 billion and ¥6.9 billion.

Questioner: Are you accelerating advertising efforts for Bill One?

Hashimoto: We are considering branding campaigns for the entire company, including Bill One.

Q&A: Factors behind the decline in orders for Sansan

Questioner: Looking back at the results for the period from late January through February, were there any changes in the business environment for the Sansan/Bill One business?

Hashimoto: As far as areas within our control, such as sales and development, are concerned, I don’t have the impression that there have been any specific changes.

Questioner: Is it correct to understand that the decline in orders for Sansan was not related to changes in the industry that began in mid-January?

Hashimoto: I don't think it has anything to do with it at all.

Q&A: Factors contributing to the increase in the proportion of recurring sales from Bill One for enterprise

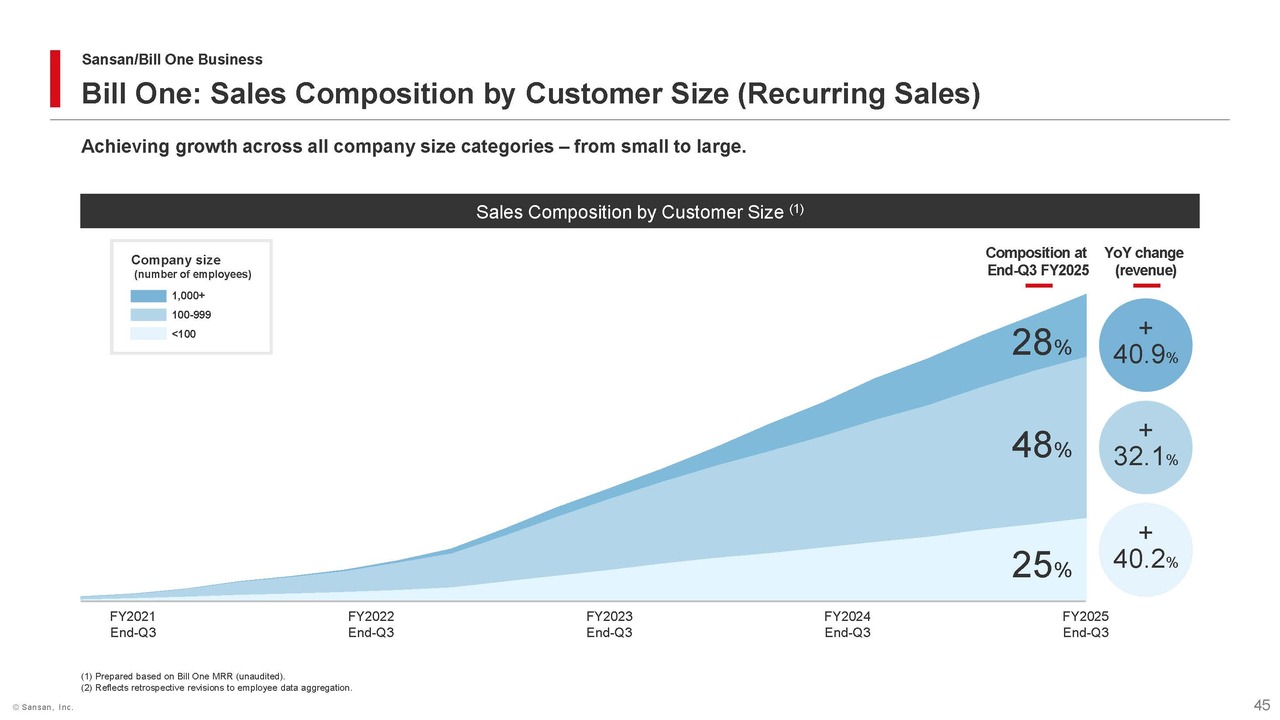

Questioner: I have a question about the percentage of recurring sales for Bill One. I believe the figure was in the 31% range in your previous presentation materials, but this time it stands in the 40% range, which leads us to believe that the momentum of recurring sales from the user base of over 1,000 has increased.

I believe you mentioned in your presentation two quarters ago that you were expanding your customer base among mid-sized and large companies. What changes have been made to your sales approach or organizational structure?

Hashimoto: As you say, sales to the enterprise sector, that is, to larger companies, are currently on the rise. We believe this is due largely to internal factors rather than external ones. One reason is that, as a result of rapidly expanding our organization over the past four years, we have finally established a robust sales structure for the enterprise sector.

Furthermore, Bill One is a relatively small-scale business, and within that context, the proportion of revenue derived from the enterprise sector, that is, large corporations, is not yet particularly significant. Given this situation, securing a single major contract can lead to a sharp increase in sales, which is another contributing factor.

We believe that these two factors, when combined, are driving the high growth rate.

Q&A: Factors contributing to the decline in the proportion of recurring sales from Sansan for mid-sized and large companies

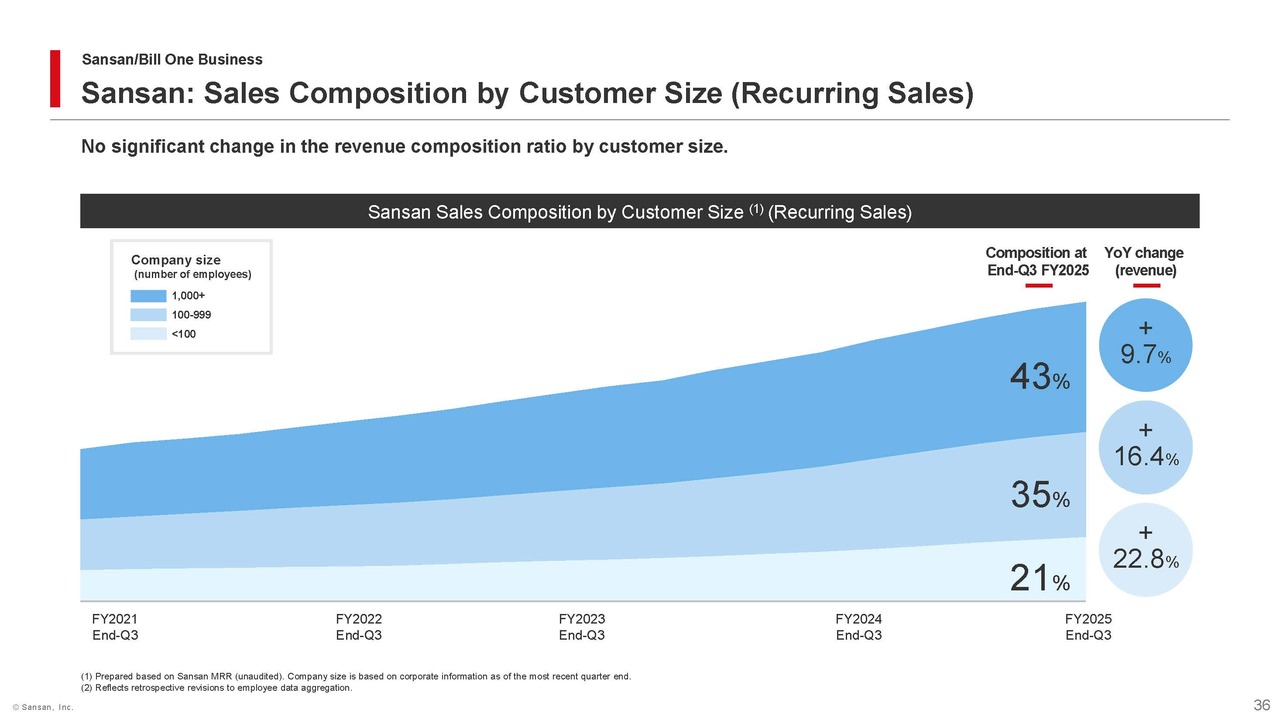

Questioner: I believe the sale composition of Sansan’s recurring sales coming from companies with 100 to 999 employees has decreased since the last briefing. Based on the composition, I estimate that while the figure was just over ¥2.8 billion in Q2 briefing, it is now approximately ¥2.6 billion. What changes have led to this?

Hashimoto: I don’t think the change in that area is particularly significant in terms of sales composition. Unfortunately, the growth rate of mid-sized and large companies has slowed slightly, which has led to a decrease in the sales composition.

As I mentioned earlier, one factor contributing to the decline in growth is that the previous quarter saw the positive effects of price adjustments for existing customers. That effect has now run its course this quarter.

Q&A: The balance between R&D expenditures in generative AI and profit growth

Questioner: Generative AI is constantly evolving, and I imagine your company feels it must continue its research and development efforts to enhance its capabilities. For this reason, I anticipate that R&D expenditure may increase in the future. At the same time, I believe profit growth is also essential. How should I approach this balance?

Hashimoto: For example, while we utilize general-purpose generative AI across all departments, not just the engineering department, the expenses associated with it have not yet reached a level that would impact our profit margins.

We do not anticipate that costs related to generative AI will become significantly higher in the future. I feel confident that we can continue to utilize it while maintaining appropriate control.

Q&A: Competitive environment and market segmentation using generative AI

Questioner: Your company’s Bill One offers invoicing-related features, and I believe leveraging generative AI could make it even more convenient to use. On the other hand, I imagine you may be concerned that if competitors were to utilize generative AI to offer integrated functions, such as accounting, invoicing, and HR, all on a single platform, it could make it harder for your company to compete in the invoicing space. What are your thoughts on this?

Hashimoto: I imagine you are comparing us to accounting software or similar solutions, but we believe the value we provide to our customers is entirely different. We offer a service that combines software with BPO to receive and digitize invoices on their behalf.

In addition, with features such as AI auto-matching and AI auto-request, which I mentioned earlier, tasks that were previously performed in accounting software can now be completed entirely within Bill One. As a result, the two services are expected to become increasingly interconnected.

On the other hand, we are confident that we are the only company capable of providing high-quality services that capture the very moment data is generated.

I believe that, recently, the strengths and weaknesses of generative AI have become increasingly clear. I believe that the key to compensating for its weaknesses lies in accurately digitizing data and normalizing and structuring it into a format that is easy for AI to utilize. Therefore, I believe that by maintaining a certain degree of differentiation, we can continue to offer products based on our unique strategy.

Q&A: Slowdown in demand for Sansan’s core business

Questioner: I understand that the slowdown in demand for Sansan’s core business is attributed to factors such as the completion of price adjustments and shifts in customer priorities. In terms of changes by industry, which sectors are experiencing a decline? If there are any discernible patterns, please let me know.

Hashimoto: Frankly speaking, the answer is “none in particular.” Given that the net increase in the number of subscriptions for Q3 was the highest on record, we do not perceive any signs of slowing demand.

Q&A: Outlook for the churn rate following the price adjustments

Questioner: I would like to ask about the churn rate. I believe that once the price adjustments have run their course, the churn rate will also decline. Could you please elaborate on that point?

Hashimoto: Since the price adjustments have not led to a significant rise in the churn rate, I do not think the two are related.

Q&A: Handling of the upper limit in the upward revision of the full-year earnings forecasts

Questioner: In the upwardly revised full-year earnings forecast for FY2025, the lower limit has been raised while the upper limit remains unchanged. What are the reasons behind the decision to keep the upper limit unchanged?

Hashimoto: This is based solely on our performance through Q3 and our fair outlook for Q4, and we are doing this with the intention of providing information that is as useful as possible. Therefore, there is no particular “strategic” intention behind this.

By the way, we have also slightly revised the upper limit for Bill One upward, revising the growth forecast to 40.5%.

Q&A: Outlook for expenses in Q4

Questioner: I have a question on the approach to expenses, including advertising expenses, for Q4. I believe you mentioned earlier that these expenses are expected to be between approximately ¥6.6 billion and ¥6.9 billion.

On the other hand, I believe personnel expenses currently stand at approximately ¥19.6 billion. In that case, while this would represent an increase of about ¥1.0 billion from the previous quarter, I honestly don’t think the increase will be that significant, even when factoring in the 105 new graduates joining the company. Given the costs you currently anticipate, how should I approach Q4?

Hashimoto: I believe that the level of adjusted operating profit will fall within the range of our earnings forecast, taking into account other costs and various factors.

Q&A: Reasons for the rising churn rate for Sansan

Questioner: I am aware that the churn rate for Sansan remains at a low level. However, looking at the figures for FY2025, it appears to have risen compared to previous periods. Is there a specific reason for this?

Hashimoto: A single large-scale cancellation occurred in Q4 of FY2024. Since we calculate the 12 months average of monthly churn rate, we expect this trend to continue throughout the year and remain at this level through Q4.