Financial Results Briefing for the Fiscal Year Ended March 31, 2026

Yoshifumi Taura (hereinafter, “Taura”): My name is Yoshifumi Taura, President and Representative Director of Taiheiyo Cement Corporation. Thank you for taking time out of your busy schedule to join us today.

After I provide a brief review of the year 2025 and a few words on our Medium-Term Management Plan, Senior Managing Executive Officer Ban will give a brief presentation on our financial results. I will also discuss three points announced today.

Looking Back at 2025

First, let me take a look back at 2025. During the year, the world was shaken by the policies of the Trump administration. With no understanding of how tariff issues would play out, companies remained unable to set outlooks for budgeting. In the current year, the situation in the Middle East destabilized from February 28. There is a sense that the world has become increasingly uncertain and difficult to read.

In Japan, a particularly noteworthy incident for our industry was the road cave-in that occurred in the city of Yashio. 2025 was a year that spurred a renewed awareness of Japan’s aging infrastructure and the importance of preventive maintenance and preservation.

According to data from the Ministry of Land, Infrastructure, Transport and Tourism, Japan’s sewage system spans a total length of 500,000 kilometers. Of this, sections that have a useful life of 50 years or more cover 40,000 kilometers.

A nationwide special priority survey conducted by the Ministry of Land, Infrastructure, Transport and Tourism in April of this year confirmed that sections requiring urgent action total 748 kilometers. The situation is highly pressing, with a road collapse incident reported again in the news last week.

Another point of note is the great number of earthquake swarms that occurred during 2025. Earthquake swarms of Intensity 1 or higher doubled in number from 2024. The Noto Peninsula earthquake and earthquakes around the Nankai Trough, off the coast of Hyuga, in the Chishima Trench, and in the Tokyo metropolitan area increased the sense of caution over earthquakes and aging infrastructure during the year.

Japan enacted the Basic Act for National Resilience in 2013 after the Great East Japan Earthquake of 2011. However, resilience construction and infrastructure investment do not seem to have progressed well. While some degree of budget has been secured, little progress has been made on the ground.

The construction industry also faces the issue of a declining number of workers. The industry had 6.8 million workers at its peak, but that number has dropped by 2 million to 4.8 million.

I admire Hisakazu Oishi, a former technical director of the Ministry of Land, Infrastructure, Transport and Tourism, and often read his books and watch his YouTube channel. He states that reduced public investment will lead to regional construction companies going out of business and skilled workers leaving the workforce, resulting in reduced capacity for disaster recovery.

I can strongly relate to his point that a country that allows its construction industry to weaken during peacetime will not be able to maintain the functions of state in an emergency. Amid steadily declining demand, I hope to see investments in national resilience move forward solidly soon. In 2025, however, there was little sign of progress.

Looking back at the Medium-Term Management Plan

Next, as a look back at our Medium-Term Management Plan, I would like to talk about four points. The first of these is that our price increases in Japan have received considerable understanding and have been accepted.

A recent briefing on a review of the 26 Medium-Term Management Plan touched on the need to change industry practices. Under the shift “from price competition to value competition," different types of cement have appeared.

We have been able to gain understanding on prices amid our call for pricing policy that supports resilience. I have the impression that this understanding has become firmly rooted.

The second point I want to discuss is our acquisition of business rights from Tokuyama Corporation. While it is difficult to discuss directions and details on some points at this time as the review is still underway, the initiative will enhance our presence in the domestic distribution market and strengthen the revenue base of our domestic business.

The third point I want to note is that we have completed a portfolio shift in our overseas business. We completed our withdrawal from all three of our large bases in the Chinese market, which we originally entered in 1989. The withdrawal proceeded very successfully, as we were able to secure compensation and other costs without paying additional expenses.

In our portfolio, we are pursuing what we call a "South Down Shift" that involves investing human and financial resources in Southeast Asia. Specifically, a new kiln was completed two years ago in the Philippines. In addition, an import terminal is currently under construction south of Manila and is expected to be completed next year.

In Indonesia, a very large terminal has been completed in Surabaya in eastern Java. Exports to the U.S. will begin this month.

The U.S. imports roughly 2 million tons from Asia. We currently export through Nghi Son in Korea and Vietnam, but to hedge against risks in light of a number of circumstances, we have established Indonesia as a new supply source.

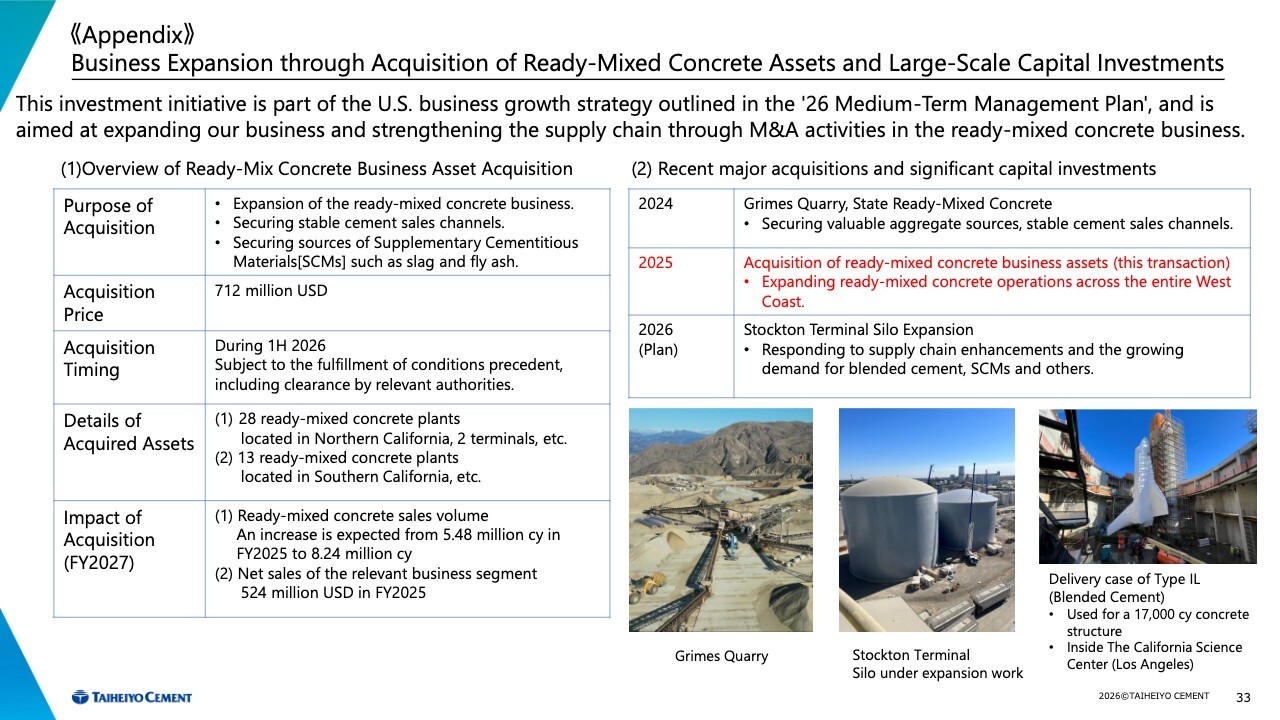

The fourth point I want to note is our business in the U.S. and other countries. In the U.S., we completed the acquisition of the aggregates business assets of Grimes Rock, Inc. The acquisition of Vulcan Materials' ready-mixed concrete plant is in the final stage, with completion scheduled for June. We are now making steady progress toward our long-held dream of vertical integration.

The U.S. interest rate on 10-year government bonds has risen to 4.46%. We do not believe that new housing units under construction will progress unless these interest rates fall. We have great hopes for that happening, and we believe it is likely to do so in 2027.

In the Philippines, imports from Vietnam had been increasing very rapidly. A safeguard of 349 pesos per ton has been applied for three years, which has reduced imports from Vietnam into the Philippines by 20% from 2024 levels. Prices are finally rising in line with this action, and growth can be seen in the Philippines.

In Vietnam, demand continues to grow steadily, with an expected 80 million tons per year this year, up 5 million tons per year from 2025.

In addition, the country’s north-south highway is coming quite close to completion, which we believe will spur a virtuous cycle for industrial parks and other investment-related activities. Accordingly, we are paying attention to Vietnam as a promising country.

Today's Announcements

We have three announcements today. First, we will implement a price increase of 3,000 yen per ton from next April. We have explained the reasons for this in a number of ways, but one point that has not been written about enough is that, as I noted earlier, infrastructure investment will increase and significant budget will be secured.

In resilience-related business, after the Great East Japan Earthquake we disposed of 1 million tons of debris at our plant in Ofunato, Iwate Prefecture. We subsequently supplied ready-mixed concrete and cement for restoration and reconstruction efforts. Compared to the pre-disaster level, cement demand has grown by 6 million tons per year.

Japan could face unprecedented crisis or disaster in the near future. Given that, the option of allowing the cement industry to weaken, with plants closing one after another, is not acceptable. We want to somehow keep plants running, even as fixed costs rise. We hope to receive the understanding of our customers as we pass costs on to prices. Logistics and other costs are also rising sharply.

In addition, our C2SP kiln is nearing completion and is attracting much attention as a carbon neutrality initiative. We intend to actively pursue investments related to carbon neutrality.

Against this background, we made an announcement asking for cooperation with our price increase of 3,000 yen.

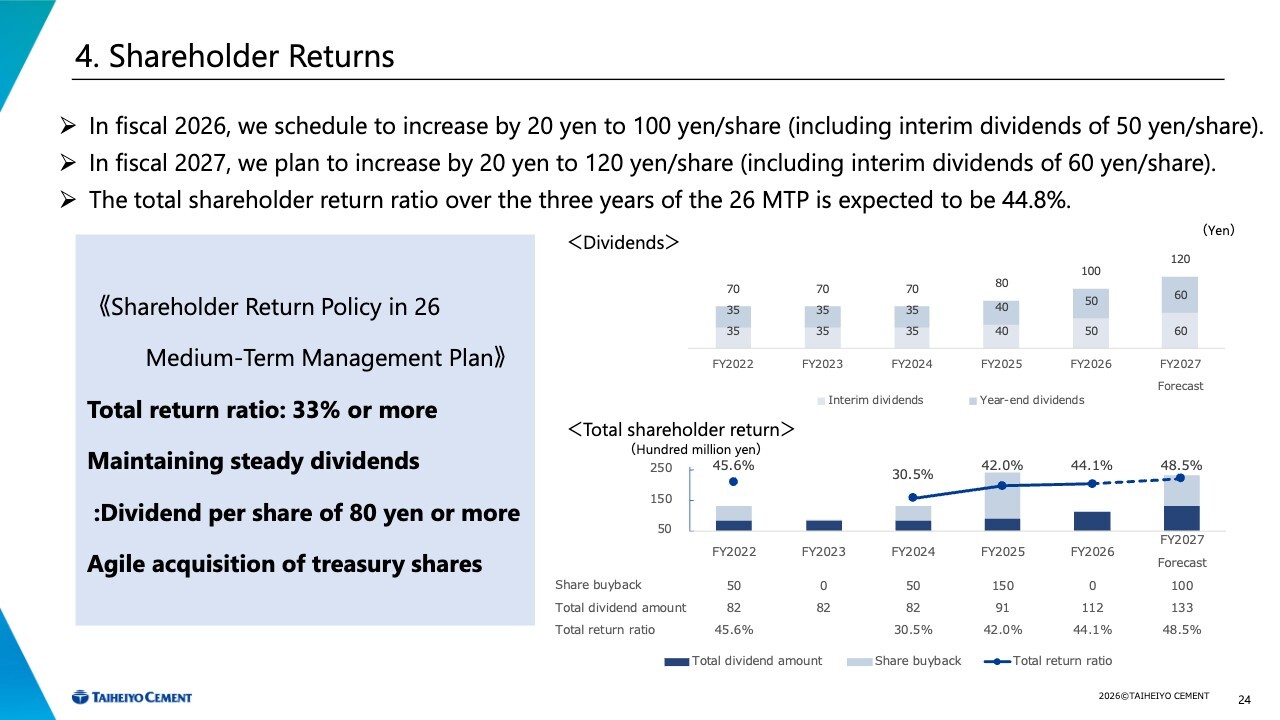

Our second announcement today concerns our intent to boost our dividend from 100 yen to 120 yen per share. Our third announcement is our plan to acquire treasury shares worth 10 billion yen. The company's shareholder returns policy stated in the 26 Medium-Term Management Plan specifies a total return ratio of 33% or higher, the maintenance of stable dividends, and agile acquisition of treasury shares.

Regarding the 26 Medium-Term Management Plan, we are making good progress toward its original budget and plans. We have also confirmed solid progress at our three global bases: Japan, the U.S., and Southeast Asia. With the company growing steadily, we believe that we must solidly move forward in returning profit to shareholders.

While we are carrying out shareholder returns in the form of dividends and acquisition of treasury shares from a short-term perspective, our medium-term growth strategy is also largely on track. After all, in the long run, it is the employees who support the company. Amid conditions that make the acquisition of human resources difficult, those human resources are extremely important from a long-term perspective. Accordingly, we will raise the starting salary to 320,000 yen from next year and will steadily increase the base salary. There is no change in our policy of returning profit while balancing short-, medium-, and long-term plans.

That concludes my brief explanation. Thank you very much.

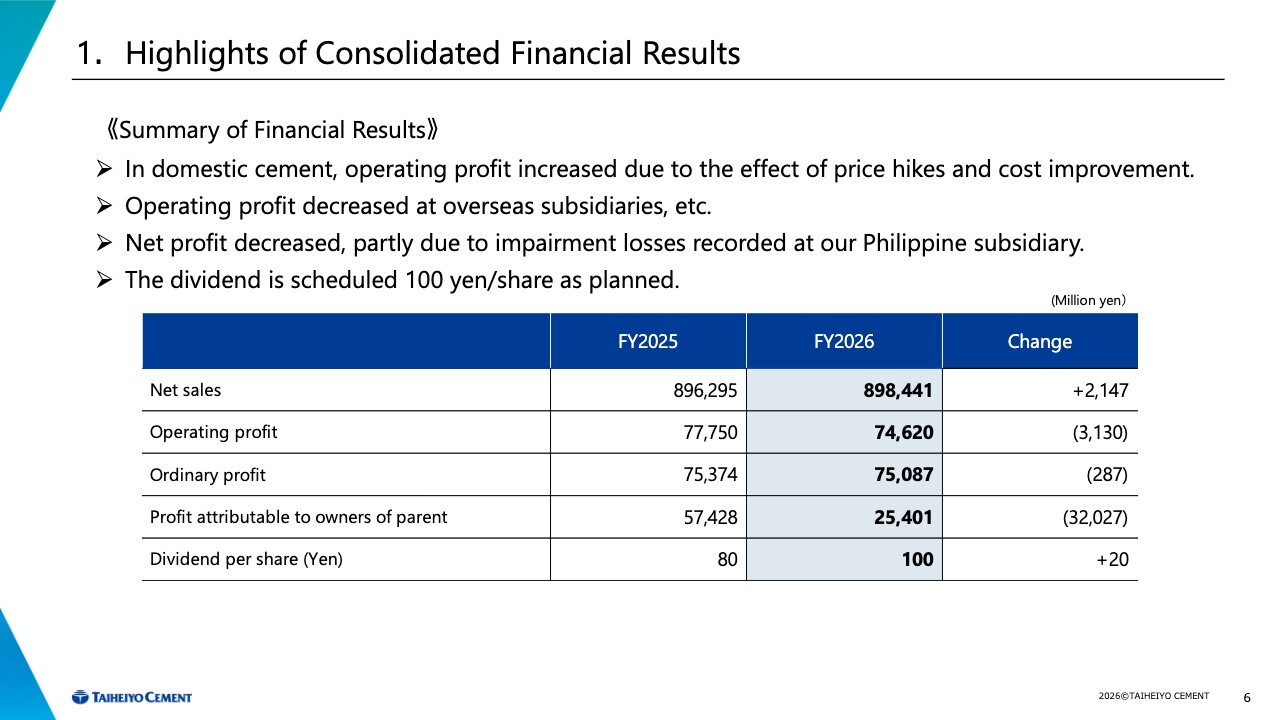

1. Highlights of Consolidated Financial Results

Masahiro Ban: My name is Masahiro Ban, Senior Managing Executive Officer. I would like to explain our financial results for fiscal 2026, with reference to explanatory materials. First, I will discuss our consolidated financial highlights.

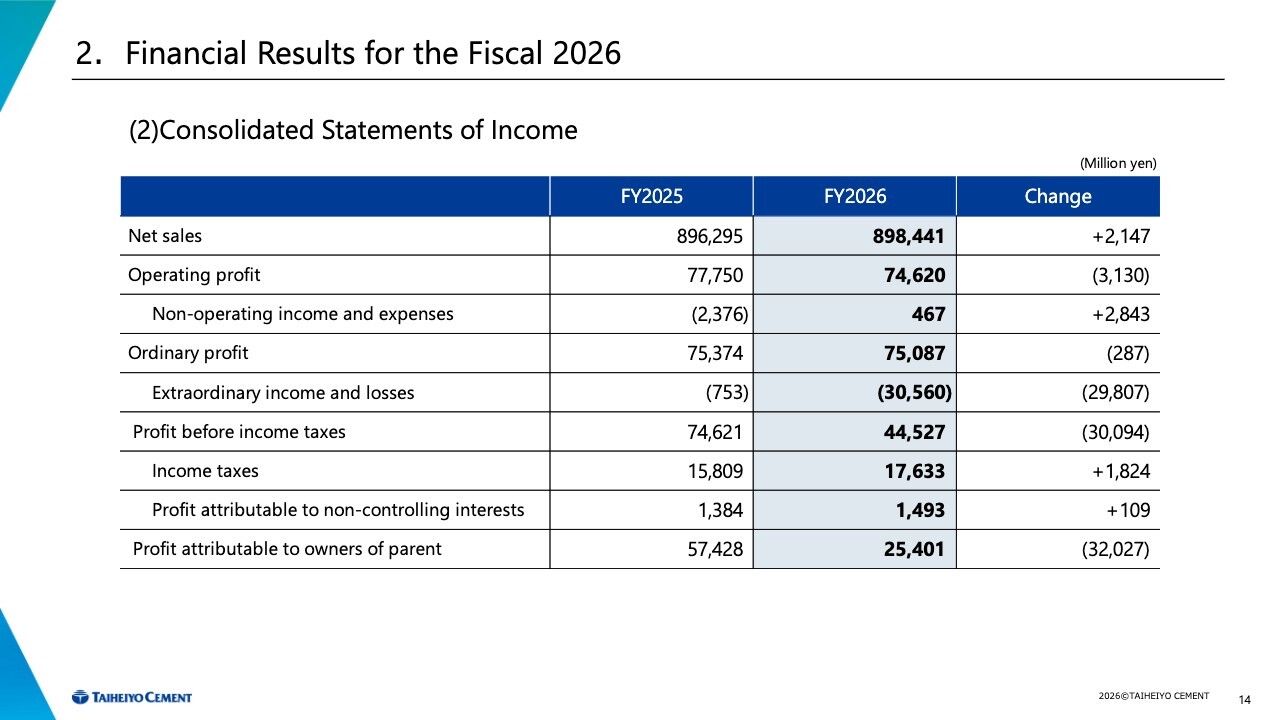

Net sales were 898,441 million yen, up 2,147 million yen YoY. Operating profit was 74,620 million yen, down 3,130 million yen YoY; ordinary profit was 75,087 million yen, down 287 million yen YoY; and profit attributable to owners of parent was 25,401 million yen, down 32,027 million yen YoY.

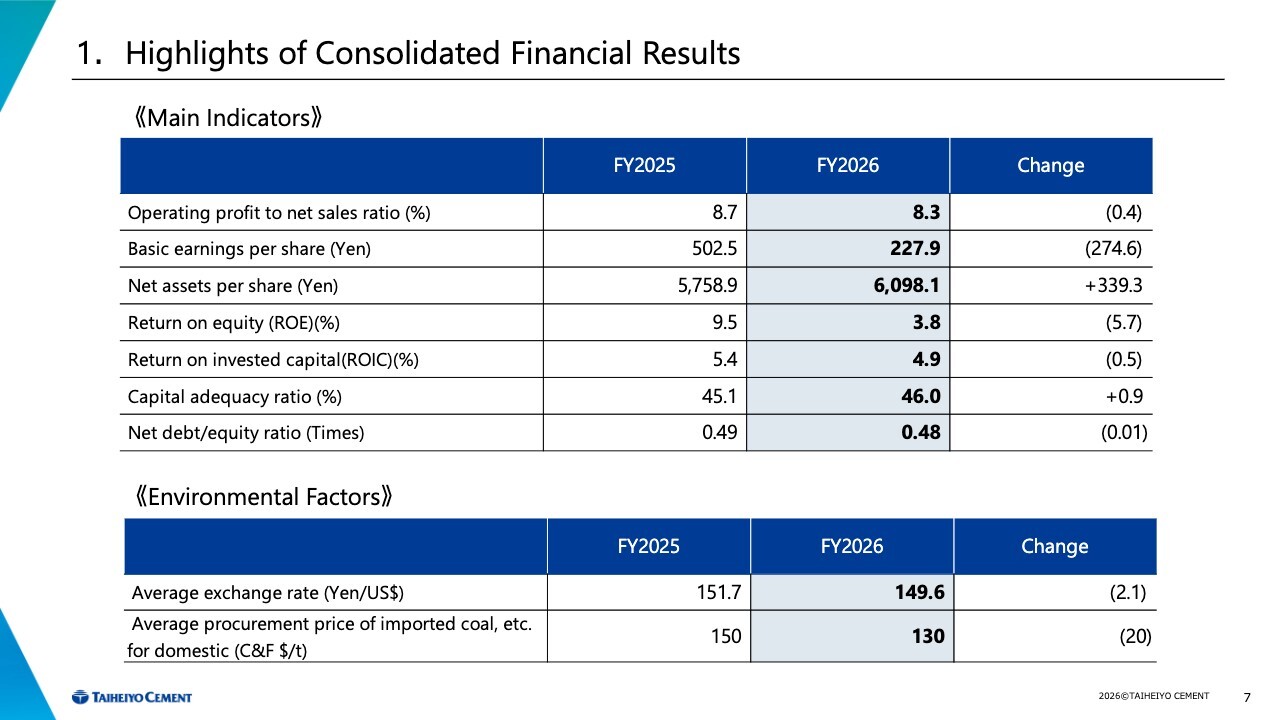

1. Highlights of Consolidated Financial Results

Key management indicators include an operating profit to net sales ratio of 8.3%, ROE of 3.8%, and a net debt/equity ratio of 0.48.

Environmental factors are also shown at the bottom of the slide. The average exchange rate was 149.6 yen to the U.S. dollar, a 2.1-yen appreciation of the yen YoY. The domestic average procurement price (C&F) of imported coal was $130 per ton, down $20 YoY.

2. Financial Results for Fiscal 2026

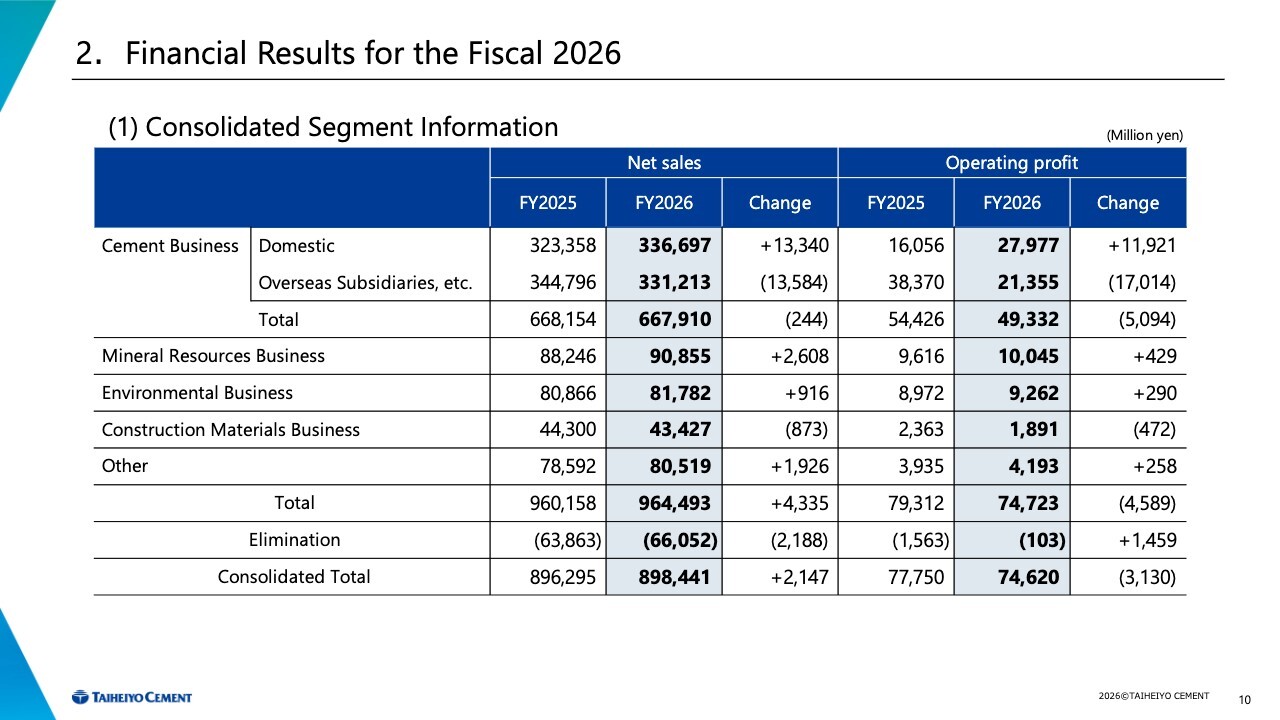

(1) Consolidated Segment Information

On the topic of performance, this slide contains information about our segments overall.

2. Financial Results for Fiscal 2026

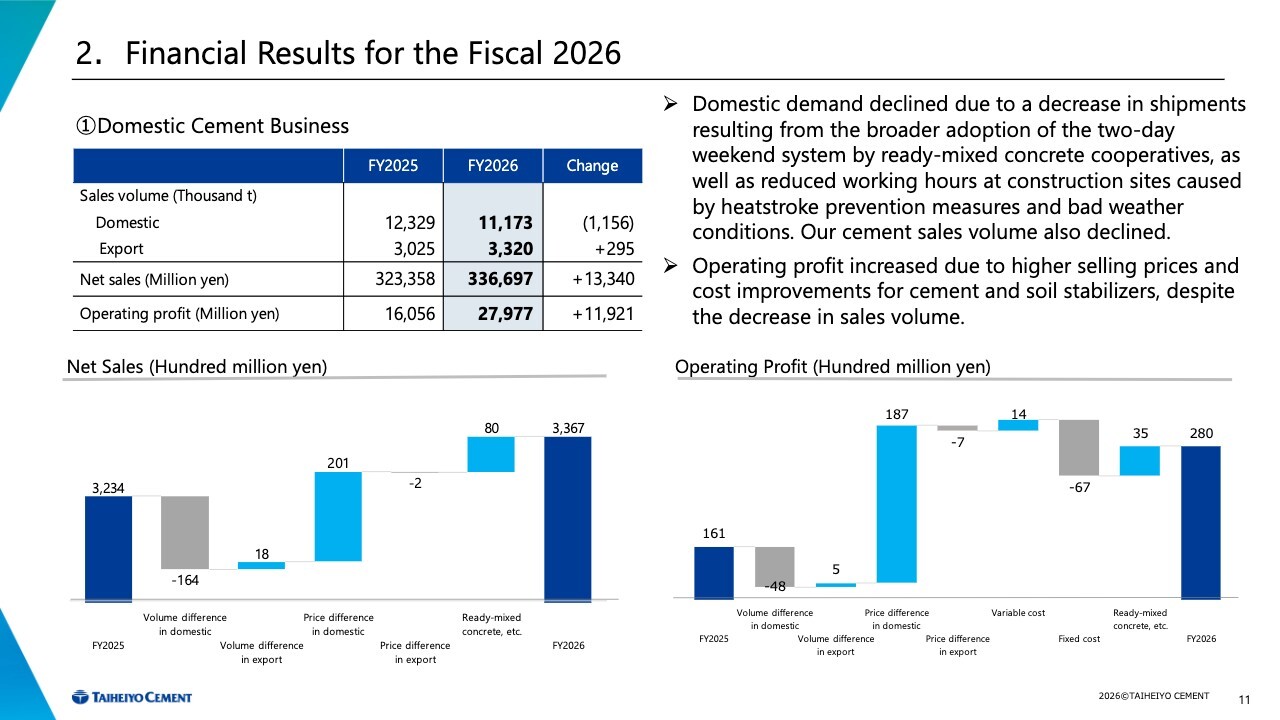

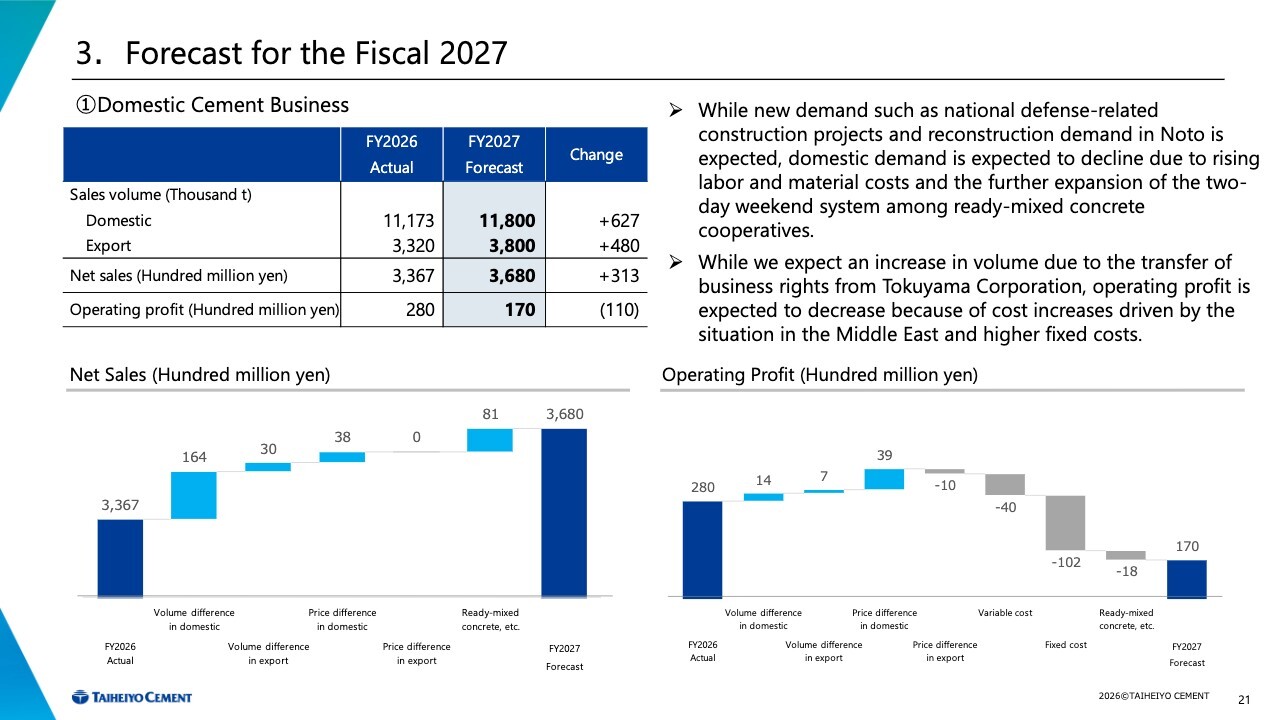

1) Domestic Cement Business

First, I will discuss the cement segment. Domestic cement sales volume totaled 11,173,000 tons, a decrease of 1,156,000 tons YoY. Export volume totaled 3,320,000 tons, an increase of 295,000 tons YoY.

Net sales increased by 13,340 million yen YoY to 336,697 million yen, while operating profit increased by 11,921 million yen to 27,977 million yen. Although sales volume decreased due to a decline in domestic demand, higher sales prices led to higher earnings.

Looking at variable costs, while the purchase prices of the raw materials limestone and cement rose, the price of coal fell by about $20 on a purchased basis, which reduced fuel and power costs and resulted in a slight decrease in total costs.

Looking at fixed costs, increases occurred in repairs, overheads, labor costs, and depreciation.

2. Financial Results for Fiscal 2026

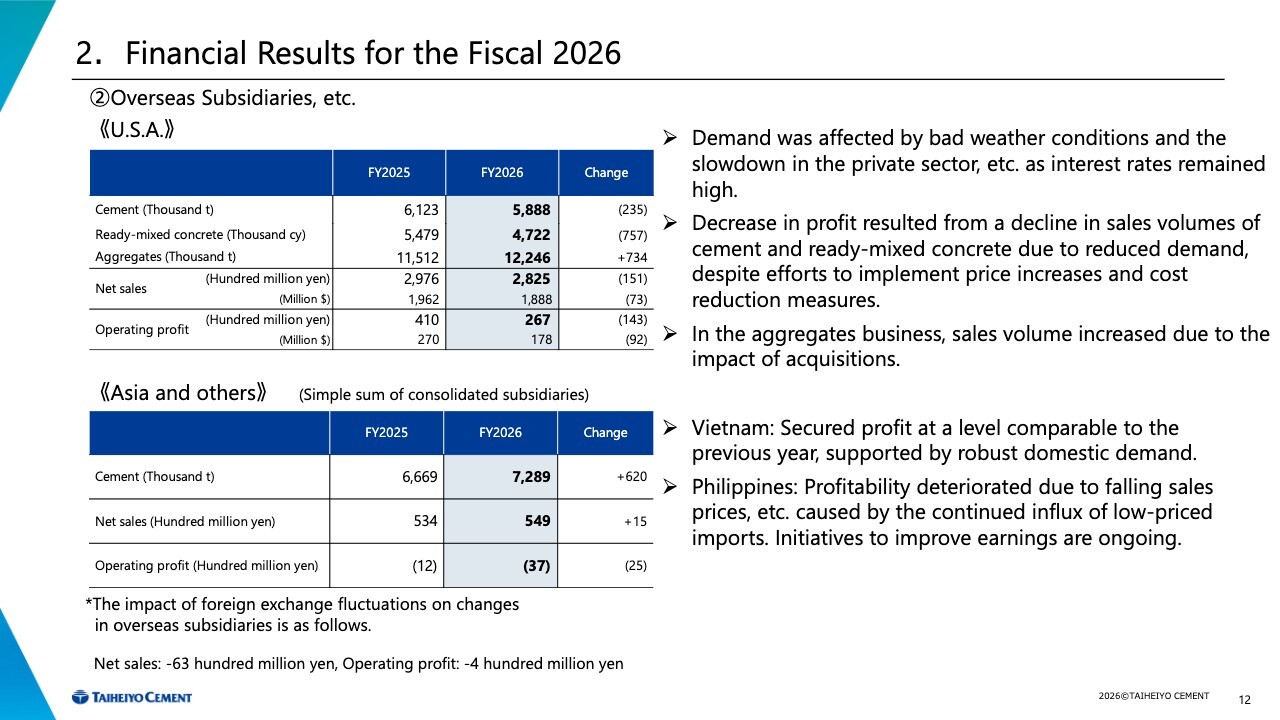

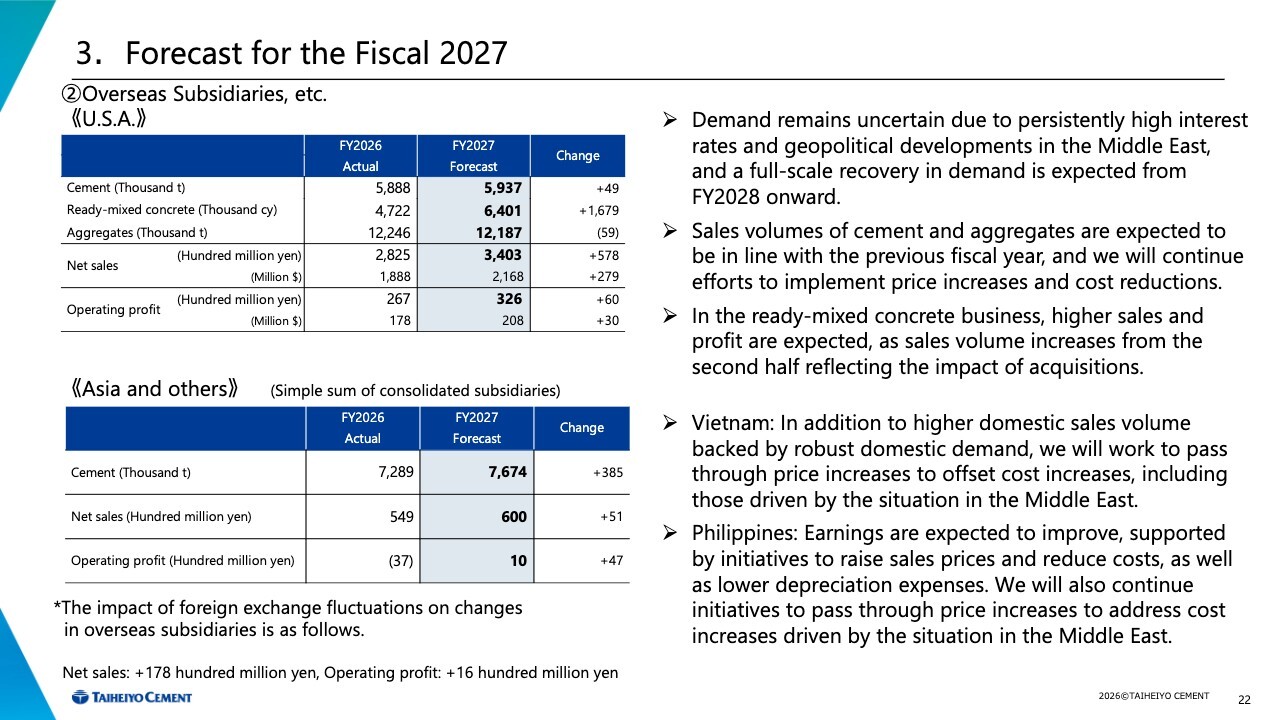

2) Overseas Subsidiaries, etc.

This slide addresses our overseas subsidiaries, with the U.S.A. and Asia and others shown separately. Please first note the U.S.A. table at top. Net sales were 282,500 million yen, a decline of 15,100 million yen YoY, while operating profit was 26,700 million yen, a decline of 14,300 million yen YoY.

In the aggregates business, the acquisition of the aggregates business of Grimes Rock, Inc. led to increased sales volume and profit. At the same time, the Cement Business and Ready-Mixed Concrete Business reported lower profit due to lower sales volumes and higher variable costs.

Next, please note Asia and others. In Vietnam, Nghi Son Cement Corporation reported a slight decrease in profit as higher domestic and export volumes were offset by lower selling prices and higher fixed costs.

In the Philippines, lower selling prices had an impact. We also recorded an impairment charge in the third quarter, and depreciation expenses decreased in the fourth quarter. However, overall fixed costs increased, resulting in a 2,200 million yen deterioration in profit/loss.

Foreign exchange fluctuations had negative YoY impacts of 6,300 million yen on net sales and 400 million yen on operating profit for overseas subsidiaries overall.

2. Financial Results for Fiscal 2026

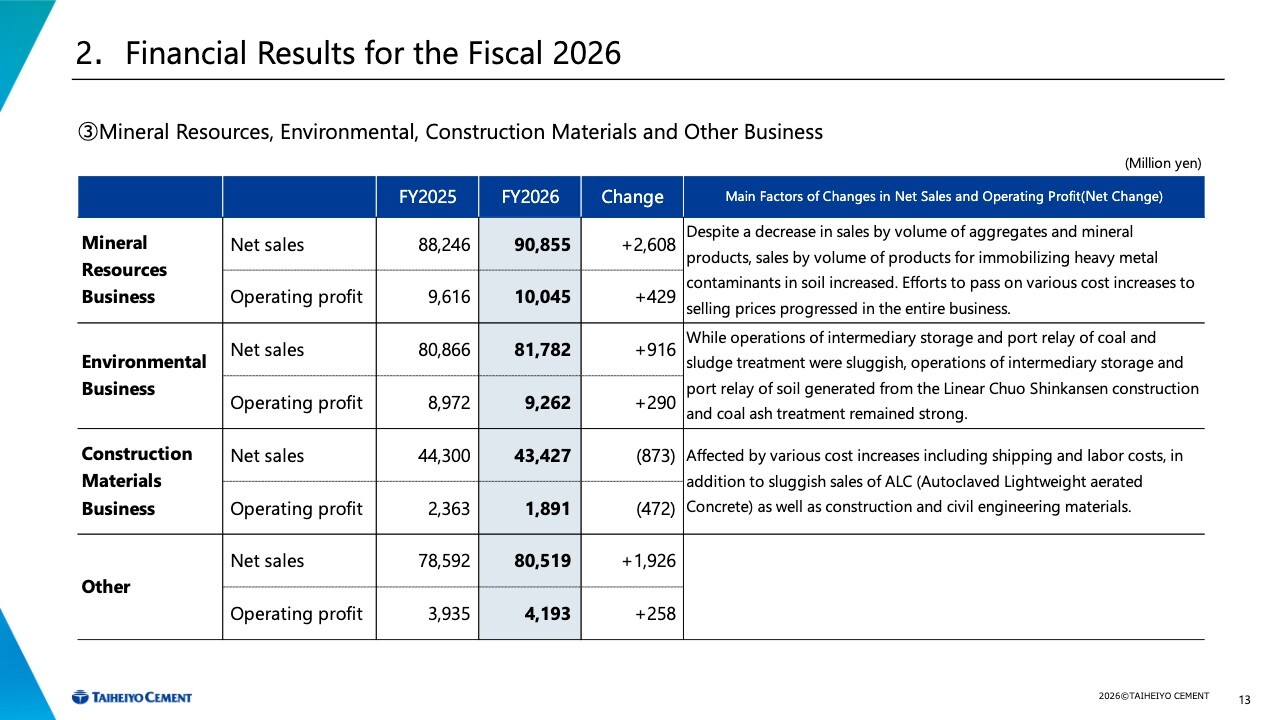

3) Mineral Resources, Environmental, Construction Materials and Other Business

This slide describes segments other than cement. Feel free to review the content later.

2. Financial Results for Fiscal 2026

(2) Consolidated Statements of Income

The slide presents our overall statement of income. Looking at the figures under operating profit, non-operating income and expenses improved by 2,843 million yen YoY to 467 million yen. This was due to the one-time amortization of goodwill of Solusi Bangun Indonesia (SBI) in the previous fiscal year as an equity-method gain.

Extraordinary profit/loss for the current fiscal year includes the 24,400 million yen impairment loss on Taiheiyo Cement Philippines, Inc. (TCPI) that was mentioned earlier. In the end, profit attributable to owners of parent decreased by 32,027 million yen YoY to 25,401 million yen.

2. Financial Results for Fiscal 2026

(3) Consolidated Balance Sheets

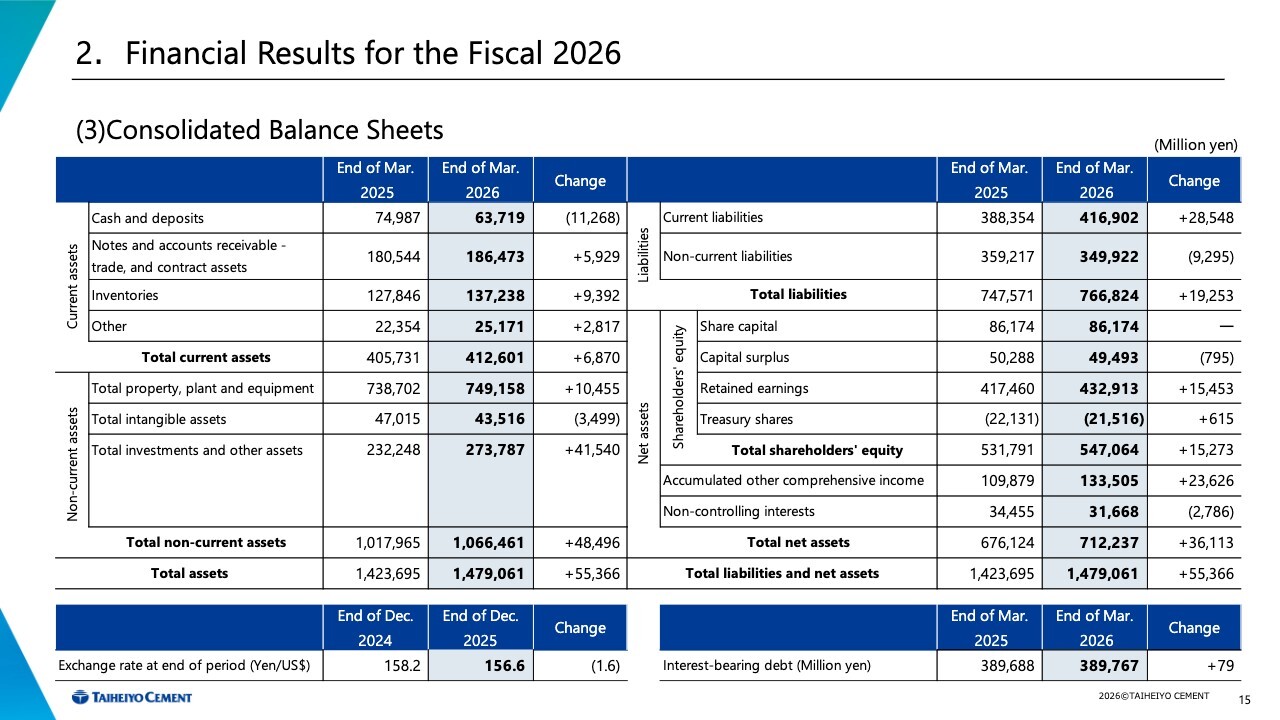

This slide presents our consolidated balance sheet. I will discuss major increases and decreases. Total assets are shown in the lower left. Total assets at year-end were 1,479,061 million yen, an increase of 55,366 million yen from the end of the previous year. This includes negative 8,500 million yen due to foreign exchange fluctuations.

The increase in assets was mainly due to increases in fixed assets and in investments and other assets. Among these, investment securities and assets related to retirement benefits, which are pension plan assets, increased significantly due to global stock market appreciation in the previous fiscal year. These totaled to an increase of 43,800 million yen.

There was also an increase of about 10,000 million yen in tangible fixed assets due to capital expenditures for domestic plants and an increase in construction in progress resulting from mine development.

Total liabilities are shown on the right. Total liabilities increased by 19,253 million yen from the previous year-end to 766,824 million yen. As interest-bearing debt was nearly unchanged from the end of the previous fiscal year, the main reason for the increase in liabilities was an increase in deferred tax liabilities due to an increase in investment securities, which was the cause of the increase in assets. The impact from this was 16,800 million yen.

The increase of 36,113 million yen in net assets includes increased net income and an increase of 17,900 million yen in unrealized gains on available-for-sale securities. This is also a counterpart account for investment securities, which is a factor in the increase in assets.

2. Financial Results for Fiscal 2026

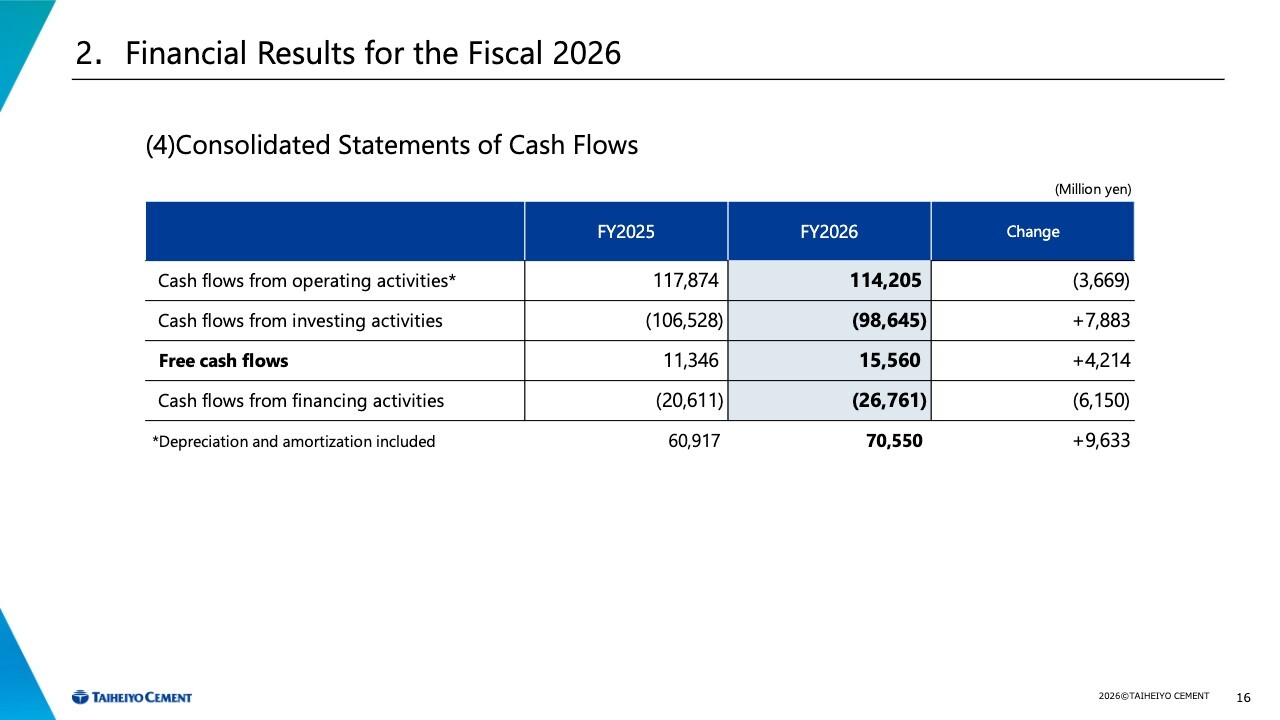

(4) Consolidated Statements of Cash Flows

This slide addresses our consolidated statements of cash flows. The decrease in cash flows from operating activities was due to a decrease in operating profit.

Cash flows from investing activities includes 24,700 million yen for the acquisition of the U.S. ready-mixed concrete aggregates business in FY2024. In fiscal 2026, the amount of cash outflow associated with mine development at Shin-Tsukumi and Mt. Kurohime is increasing.

3. Forecast for Fiscal 2027

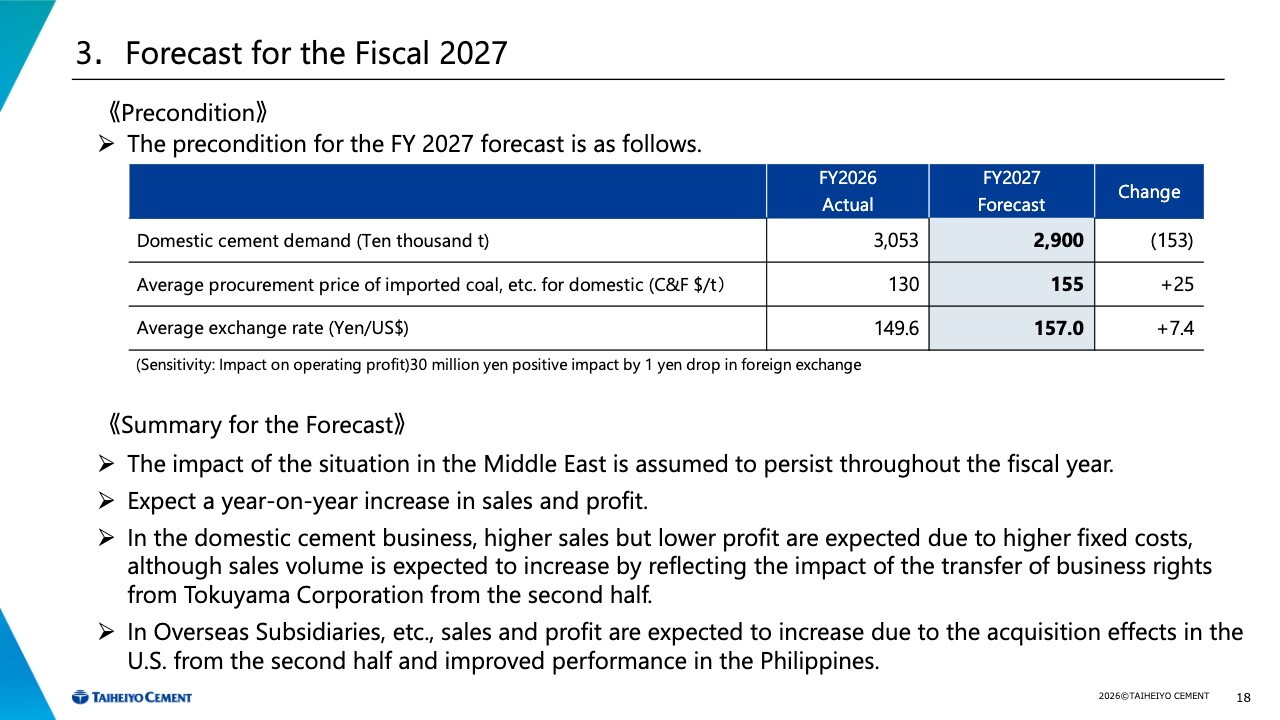

I would now like to talk about our forecast for fiscal 2027. Our assumptions are based on domestic cement demand of 29 million tons, a domestic average procurement price of $155 for imported coal, etc., and an average exchange rate of 157 yen. Exchange rate sensitivity is a positive 30 million yen impact on operating profit per 1 yen of depreciation.

Our forecast for fiscal 2027 anticipates impacts from the situation in the Middle East throughout the fiscal year. Domestically, we foresee higher coal prices and oil prices remaining at $100 per barrel.

Regarding our overseas subsidiaries, we have incorporated effects from the acquisition of the ready-mixed concrete business in the U.S. from the second half of the fiscal year, factoring in six months of effects.

3. Forecast for Fiscal 2027

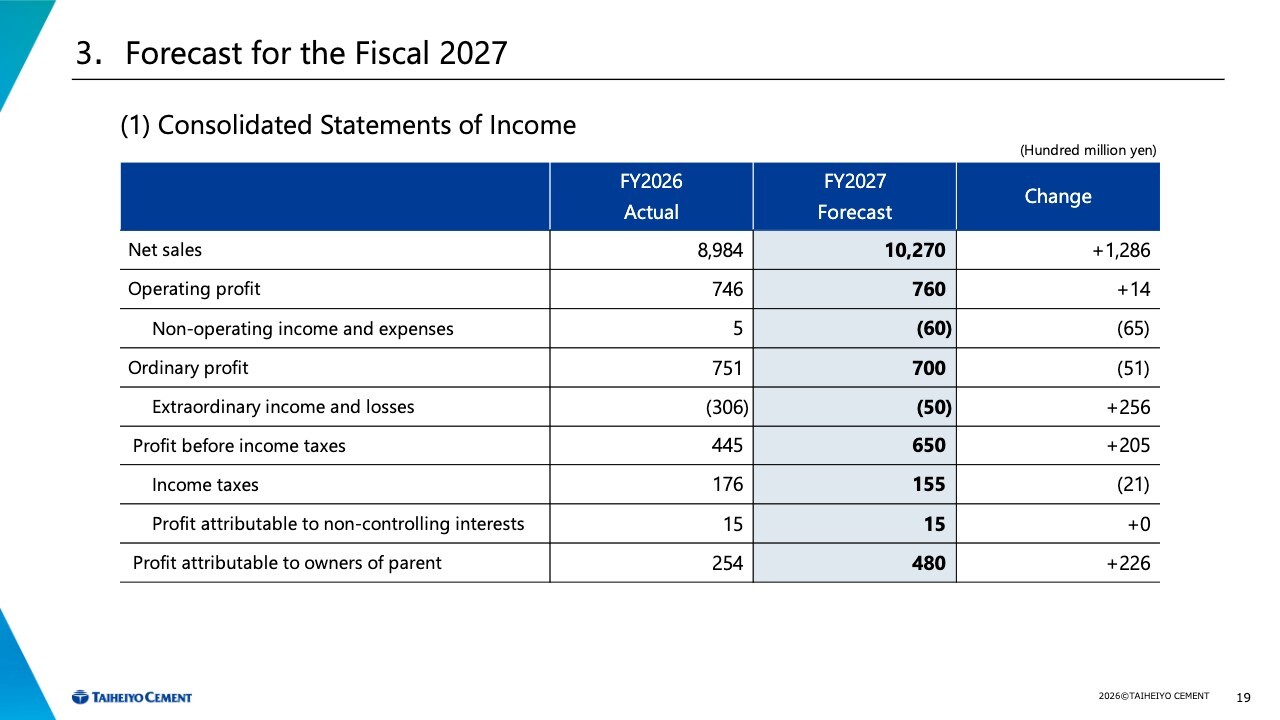

(1) Consolidated Statements of Income

This slide addresses consolidated statements of income. We forecast net sales of 1,027,000 million yen, up 128,600 million yen YoY; operating profit of 76,000 million yen, up 1,400 million yen YoY; ordinary profit of 70,000 million yen, down 5,100 million yen YoY; and profit attributable to owners of parent of 48,000 million yen, up 22,600 million yen YoY.

3. Forecast for Fiscal 2027

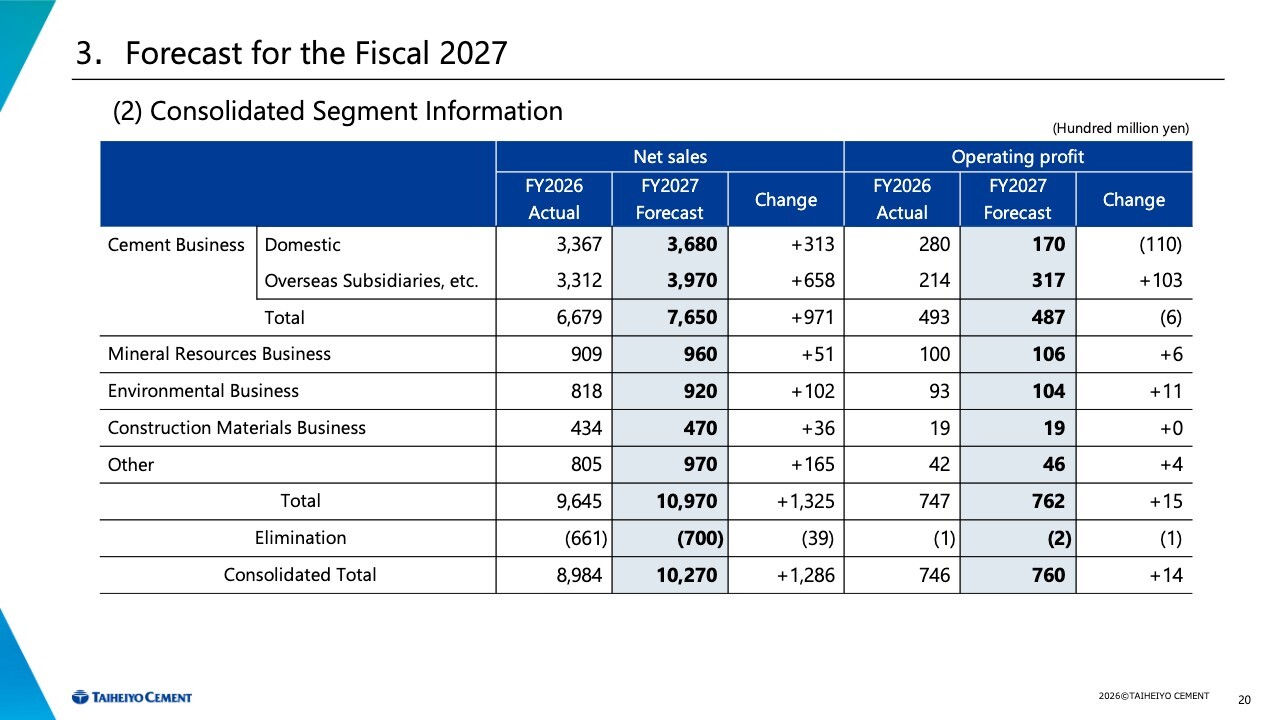

(2) Consolidated Segment Information

This slide contains information about our segments overall.

3. Forecast for Fiscal 2027

1) Domestic Cement Business

I would like to discuss the forecast in detail, starting with the cement segment. Domestic sales volume is forecast to increase by 627,000 tons to 11,800,000 tons, while export volume is forecast to increase by 480,000 tons to 3,800,000 tons. Net sales are forecast to increase by 31,300 million yen YoY to 368,000 million yen. Operating profit is forecast to decrease by 11,000 million yen to 17,000 million yen.

The increase in sales volume incorporates purchases and sales from the transfer of business rights from Tokuyama Corporation. Without this, domestic cement sales volume would decline in real terms.

For variable and fixed costs, we forecast a total increase of 14,200 million yen, which incorporates higher fuel costs and other impacts of the situation in the Middle East. We also expect personnel costs, overheads, repairs, depreciation, and other fixed costs to increase.

3. Forecast for Fiscal 2027

2) Overseas Subsidiaries, etc.

This slide looks at our overseas subsidiaries. In the U.S., we forecast increased sales and profit. We expect the stagnant cement volumes of fiscal 2026 to continue in fiscal 2027. Some areas of some U.S. states will see increased volume accompanying the construction of data centers, but we expect volume to remain nearly flat overall.

In ready-mixed concrete, profit/loss from the ready-mixed concrete business to be acquired from Vulcan Materials has been factored in for a period of six months.

Looking at Asia and others, we expect an increase in domestic sales volume in Vietnam in line with growing domestic demand, but we also expect profit to decrease due to higher fuel and power costs. In the Philippines, we expect to post an operating surplus due to factors including improved selling prices, the use of domestic coal, and reduced power costs.

4. Shareholder Returns

As President Taura mentioned, we plan to acquire 10 billion yen’s worth of treasury stock and pay a dividend of 120 yen per share in fiscal 2027.

Q&A: Domestic private sector demand and reactions to price increases

Questioner: My question concerns the domestic demand environment and the announced price increases. You talked about public sector demand, but what are your thoughts on the risk of shrinking private sector demand in the construction market overall amid soaring construction costs?

Also, you announced a 3,000 yen price increase in response to rising costs. How do users view this, and what is their level of tolerance?

Respondent 3: Regarding construction costs in the context of private demand, you may be taking the view that overall construction costs, including ready-mixed concrete, will rise in line with cement price increases. However, as far as we can see from figures on general contractors' on-hand construction work (order backlog), we do not believe that we are heading into a situation of constrained construction work due to cement price hikes that result in higher construction costs.

Naturally, we believe that clients may consider design changes and so on, but at present, we hope and expect that there will not be a great impact.

We intend to make requests concerning the 3,000 yen price increase toward the entire supply chain, including general contractors, based on the same cycle as in the past. We want to firmly request a 3,000 yen increase based on the announcement we made a year ago regarding changes to industry practices, and we intend to proceed with passing on costs.

Respondent 1: For years, there has been talk about a cost of over 100 million yen for 70 square meters of floor space in the 23 wards of Tokyo. Recent news stories indicate that demand is leveling off considerably.

To answer why costs are going up, this has to do less with cement and more with labor costs and dry construction method materials. I believe that labor costs in particular are a very significant issue.

In the past, approximately 100 tons of cement were used for every 100 million yen invested in construction. The correlation can be seen over the long history of the market, but the situation has changed in recent years. Today, the amount is less than 50 tons per 100 million yen.

A similar trend can be seen in the U.S. Factors behind this include the shift to the dry construction method, as well as the fact that skyscrapers in Singapore and Japan are increasingly built with glass sides.

However, cement is used in the 3- to 4-meter thick foundations technically known as mat slabs. There is no substitute for cement in these. Accordingly, cement will continue to see use even under a price increase.

With regard to demand for use in private construction, the amount of cement used in general housing is very low. The use of cement in housing is limited to foundations, and overall usage volume is not very high.

As an example, when a 100-million-yen house is built, the amount of cement used is at most 20 tons. Assuming a unit cost of 20,000 yen, the total amount will be 400,000 yen. If that price were to rise by 20%, the increase would still be only about 100,000 yen.

As such, a price increase does not necessarily have a significant impact on the construction of the house itself. While impacts do exist, we believe that these are more the direct result of increased costs stemming from labor costs and extended construction periods, and that the impact from cement is not so significant.

We feel that customers will continue to recognize that cement prices have long been very inexpensive, and will gradually come to understand the various costs involved in cement and ready-mixed concrete. For those reasons, we believe that the increase of 3,000 yen per ton from next year will be met with sufficient understanding.

Q&A: About the outlook for cement business exports and for the recycling-related business

Questioner: My question concerns your domestic business. Regarding the export cement business and the recycling-related business that you have been discussing, what are your outlook for the new fiscal year and your current thoughts on whether the businesses can be viewed as medium- to long-term earnings drivers in terms other than volume and price?

Respondent 4: Regarding exports, I believe you are referring to exports of blended cement, which we have talked about for some time. This year, too, we are exporting to Singapore, the Philippines, and Sri Lanka.

Customers understand the benefits of blended cement, including its heat generation properties and its usefulness in preventing cracking. In Singapore, we are actively introducing and promoting the use of technical sales and marketing expertise from Japan, right up to the stage of local concrete production.

We intend to further strengthen these efforts to further grow exports of blended cement from Japan. Of course, while there is the matter of balancing exports with domestic conditions, we understand that exports overall contribute greatly to the company in terms of profits, partly due to exchange rate effects.

We will continue to monitor the situation in Japan, but in the meantime, we have received high acclaim from our export customers. For that reason, we aim to strengthen our efforts in this area.

Respondent 3: Regarding your question concerning the recycling-related business, which I take to mean our environmental business, it could be said that the domestic cement business is in fact an integral part of our environmental business and would not function without the environmental business.

In addition to the large volume of waste disposal-related requests, we also have contracts with local governments, and as President Taura mentioned in his remarks, we cannot readily shut down plants. For these reasons, the environmental business is needed, as is blended cement.

Also in connection with your question concerning performance drivers, the environmental business is an inseparable business for us, like a runner in a three-legged race. This business has recently made considerable contributions and is a great help for us.

Respondent 2: As we continue to operate with the Middle East situation in mind, I think a major reason why operating profit is growing even under rising fixed costs is the robust performance of our overseas business. I believe that the increase in recycling-related processing fees in Japan is also an important factor.

Q&A: Demand composition and future trends in the U.S.

Questioner: My question concerns the U.S. You forecast a full recovery in the business environment in fiscal 2028. You also noted some demand related to data centers. To the extent that the company can currently see, how do you view the composition of demand in the U.S. in the new fiscal year, in terms of the ratios of private sector-, residential-, industrial-, and infrastructure-related demand?

Respondent 4: The composition of demand in the U.S. varies by area, but 30% to 40% comes under residential, another 30% to 40% commercial (commercial properties), and the remaining 30% public sector construction. This composition is commonplace.

Regarding the outlook for this year and next, there was a lot of talk this morning, too, about interest rates and the rekindling of inflation. The housing business in particular is very sensitive to interest rates and is still somewhat weak, I hear. We do not expect a full-fledged recovery until next year or later.

In the commercial area, there is data center- and semiconductor-related-demand, just as you noted. It is difficult to discuss specific properties due to confidentiality obligations, but looking at data centers, according to reports from the field, there are about 10 projects under construction or bidding in both California and Arizona.

Under these circumstances, we feel that demand is reasonably strong. We believe that this sort of demand is providing a foundation at present.

Depending on location, public sector infrastructure works are affected by interest rates and other factors, but there are examples such as the southern Arizona border wall with Mexico, which has been much talked about by the Trump administration. We have heard that about 600,000 tons of blended cement were ordered over the course of two years, and understand that this is providing support for the infrastructure side of demand as well.

Conversely, we expect housing to remain somewhat difficult for the rest of the year. However, we believe that the local backlog in commercial and infrastructure properties will provide support.

Respondent 1: First, as was explained many times regarding the private sector, there is a strong correlation between housing units under construction and mortgage rates. Mortgage rates have effects on 10-year government bonds and other securities.

As reported on television this morning, the yield on the 10-year government bond is up to 4.46%. Unless that rate falls quickly and mortgage rates drop below 5% or 6%, new housing units under construction will not ramp up to address inadequate housing conditions.

Next, the public sector business is very different from that in Japan. The Infrastructure Investment and Jobs Act (IIJA) was passed during the Biden administration. It was passed on a bipartisan basis with a budget of $1.2 trillion, or more than 150 trillion yen at the exchange rate at the time. The Republicans did not oppose it, and the process was readily passed under a shared understanding that it definitely should be implemented.

This legislation is a major bipartisan policy measure recognizing that the country cannot grow as a nation unless it moves forward on initiatives including rebuilding aging infrastructure, transitioning to decarbonized energy, strengthening supply chains, and making road-related improvements.

The measures are finally getting underway, albeit with time lags. The data centers mentioned earlier are an example. As the foundation is solid, we believe that recovery will occur as interest rates further fall and stabilize. However, this is an area that is not going well.

Q&A: Effects of the consolidation of Vulcan Materials

Questioner: Regarding the consolidation of Vulcan Materials, will effects simply be add-ons to data for the second half of fiscal 2027, or is there a prospect of synergies emerging to some extent and contributing to earnings?

Respondent 4: As was mentioned, we plan to close the Vulcan Materials transaction in June of this year.

The contract was signed last October and is currently in the preliminary antitrust review phase. We have already submitted materials and information requested by the authorities during the additional investigation period that began at the end of last year, although we cannot discuss detailed matters and preliminary details as they are currently under review by the authorities.

Procedures are moving forward as originally envisioned, and at present we expect to obtain antitrust approval and close the transaction by the end of June.

We expect this to contribute to profit/loss in the second half of the fiscal year. As it is an existing business, we understand that it will contribute to our business promptly and without delay from the date of closing.

Respondent 1: Regarding Vulcan Materials, the question was about synergies. The end products of our business are concrete and ready-mixed concrete, for which we provide cement. Currently, 20% to 30% is for in-house use, with all the rest sold externally.

With products like low-carbon blended cement and low-carbon concrete being requested by GAFA and others, it is the role of ready-mixed concrete companies to talk with the customer and plan what sorts of products to release.

Until now, we have only provided cements specified by ready-mixed concrete companies, and have not been able to directly meet with customers to discuss proposals concerning what sort of products we have or suggestions for ways of doing things.

By acquiring Vulcan Materials, though, we will be able to talk directly with customers and offer a variety of proposals. We have a wide variety of products that we intend to leverage to offer total solutions.

However, we believe that such discussions will not move forward until June, and that it will be next year before any full-fledged talks. I believe that a certain amount of time lag is unavoidable.

Q&A: Incorporation of acquired businesses into the fiscal 2026 performance plan

Questioner: I would like to discuss the incorporation of acquired businesses in the new fiscal year performance plan. How many months have you factored in regarding Vulcan Materials Company's ready-mixed concrete business and the acquisition of Tokuyama Corporation's business rights in Japan, and how much of that is reflected in sales and profit?

Respondent 4: Let me first talk about the aspects of your question relating to the United States. The acquisition of Vulcan Materials is expected to be concluded in June and has been factored into income. Based on the assumption that this will make a contribution—for example, through synergies—from July, we estimate that 4 to 5 billion yen will be contributed to income as operating profit.

Respondent 2: Regarding the impact of Tokuyama, as stated in the domestic cement part of the forecast, normal purchasing and sales have already been determined. Since there are unknown factors regarding subsequent costs, they are factored into the domestic volume difference as normal purchasing and sales. We expect the amount to be in the range of 2 to 3 billion yen.

Therefore, the domestic volume difference portion would have been negative without the impact of Tokuyama.

Questioner: Tokuyama told us that production will be transferred to your company in two years. I thought that its contribution to profits would occur after production is shifted to your company, but rather than that, has the procurement price been contracted so that it will contribute from the beginning of the acquisition?

Respondent 5: As you say, the full effect will not be demonstrated until the second half of 2028 according to the current schedule. The transition period is scheduled to begin in October 2026, with shipments from our plants scheduled to begin in the second half of 2028. Therefore, full synergistic effects are not expected until the second half of 2028 or later.

Until then, our scheme is to purchase cement manufactured by Tokuyama. During this period, there will be no effect from increasing the operating rate of our facilities, so synergistic effects will be somewhat limited. For this reason, we estimate the effect this year to be between 2 and 3 billion yen.

Questioner: Am I correct in understanding that with Tokuyama, six months’ worth of cement is expected?

Respondent 5: That is correct.

Q&A: Acquisition of Vulcan Materials

Questioner: With respect to Vulcan Materials, do you expect to incur amortization or depreciation of intangibles? Since the acquisition is not yet concluded, there may be some unclear aspects, but what are your thoughts at this point?

Respondent 4: At this time, we do not anticipate incurring significant amortization, etc. However, we are in the process of working with experts to examine this matter closely, including the allocation of assets, etc.

Q&A: Business environment in the Philippines and Vietnam and outlook for FY2026

Questioner: This question is about the overseas cement business. You explained that business in the Philippines struggled considerably last year, but is expected to improve and be profitable this fiscal year.

Please update us on the situation in the Philippines and Vietnam, including the business environment, what kind of progress you expect in terms of volume and prices, and how much improvement in income you expect compared to the previous year.

Respondent 4: Regarding the situation in Asia, as you mentioned, the Philippines was in a difficult situation last year. In particular, inexpensive imports from Vietnam did not decrease. In addition, major earthquakes and typhoons have occurred since October, and this has been very tough on our results.

However, with regard to the external environment, safeguards were put into effect and temporary measures were implemented in March of last year, and from October, a more permanent measure of 349 pesos per ton—about 900 yen—was imposed for three years.

As a result, import volumes decreased by approximately 20% last year. In addition, the volume of imports from Vietnam from January to April of this year dropped by almost half. In this sense, we believe that the competitive environment is moving in the right direction.

As countermeasures for Taiheiyo Cement Philippines, Inc. (TCPI), while volume and selling price are important, the most significant point is to focus on the cost aspect, which we can control. Therefore, we are reviewing our overall procurement, including that of electricity, coal, and other raw materials.

This has allowed us to obtain competitive prices. Regarding actual cost reduction in the production process on the new production line, we are taking measures with full cooperation not only locally but also at head office production facilities, and the results became apparent from January to March.

With sales, figures for January to March were higher than last year, and remained steady until March. However, since mid-March, sales have been slightly affected by the situation in the Middle East, which is a cause for concern, but as a base, sales have been recovering considerably compared to last year.

Selling prices are affected by the situation in the Middle East, not only for our company but also for our competitors. Many of you may be aware of the situation in the Philippines through newspapers and other media, and there has been a move toward price pass-through.

TCPI has also been notifying its customers of the price increase in three to four phases starting in March, and we hear that some of the increases have already been accepted.

The Philippines is still being affected by the situation in the Middle East, but it is unclear how prolonged this impact will be. However, the situation steadily improved from January to March. Our policy is to first ensure that the controllable cost aspect is addressed and that results are achieved.

Regarding the situation in the Middle East and gasoline prices, we are also considering improving our income while asking customers for a price pass-through.

Questioner: In terms of amounts, how much improvement do you expect in the Philippines and Vietnam?

Respondent 4: A significant portion of the improvement in the other figures from Asia presented here is due to the Philippines. As for Vietnam, demand was consistently higher year on year until around mid-2024, followed by very strong figures of 75 million tons last year and 80 million tons this year.

In addition, the cost reduction and export initiatives that we have been working on for the past few years are certainly generating results. However, to a certain extent, the figures shown here factor in the impact of the situation in the Middle East on logistics and other costs.

In the mid- to long-term, I believe that growth can still be expected in the Philippines and Vietnam once we are clear of the situation in the Middle East. We intend to operate them as important bases by ensuring that we can reduce costs and realize synergies where feasible.

Respondent 1: Currently, the population of Vietnam is about the same as that of the Philippines, with both at about 100 million. Demand in Vietnam is expected to be about 80 million tons, while demand in the Philippines is expected to be between 32 and 33 million tons.

In view of these circumstances, we believe that the Philippine government intends to continue promoting investment. Originally, President Rodrigo Duterte and President Bongbong Marcos won their election campaigns with the slogans "Build, Build, Build" and "Build Better More," respectively.

My theory is that a combination of improvements in three areas—infrastructure development, port development, and electricity supply—will lead to rapid economic growth.

Currently, political instability is an issue for the Philippines and Vietnam, and such factors are the reason why ODA and public investment have not progressed well, but we believe that once these factors settle down, both countries will surely achieve growth.

Another factor is that it is not only per capita but also so-called accumulation that is important. Various infrastructures have been built using cement, and I believe that the degree of accumulation is a very important integral factor.

For example, Japan has a per capita cement accumulation of 30 tons. In the U.S., it is 20 tons per capita. The populations of the Philippines and Vietnam are growing, so we believe accumulation will grow further in the future. On the other hand, the accumulation of social capital is still insufficient at 7 to 8 tons in Vietnam and 5 to 6 tons in the Philippines.

We believe that political instability is a major factor in the lack of significant, steady growth. However, we are confident that once this begins to resolve itself, growth will be quite rapid.

We are currently at an inflection point, or rather, the situation is rather frustrating, but we expect to make significant progress, probably next year. The Philippines also believes the situation will improve as Vietnam develops, as there will no longer be an influx of inexpensive cement from there.

Therefore, we believe that as Vietnam improves, so will the Philippines. Accordingly, we expect that next year will be much better.

It is difficult to provide specific figures, but the highest profit generated until now by our plant in Cebu, Philippines is 4 billion yen. Even if we do not reach that level immediately, we believe that it is fully possible to expect around that level of profit as an ultimate goal.

Q&A: Impact on business of the situation in the Middle East

Questioner: I would like to ask about the impact of the situation in the Middle East on your business. I seem to recall that at one time there were reports of a shortage of fuel oil for transportation in the ready-mixed concrete and aggregate industries. What is your current view on the risk of operations being affected by the inability to procure such raw fuel?

Respondent 2: We have factored in price increases in relation to the current situation in the Middle East. However, we have not factored in the risk of supply disruptions, as we do not see any such risk in the current fiscal year.

Questioner: Are you saying there is no problem? Or do you mean that we don't know?

Respondent 2: I think it probably won't be a problem. If supply had not been possible, we would not have been able to provide the forecast on this occasion. For this briefing, price increases are factored in conditionally and with the assumption that there is no such risk. In some respects we are not sure what will actually happen, but we do not think there will be a problem.

Respondent 1: First and foremost, as far as gasoline, etc. is concerned, the situation is completely different from that with naphtha. In the case of naphtha, the stockpile is said to be enough to last about three weeks, but as for gasoline and other items, Prime Minister Takaichi has said that everything is okay. We believe that a major impact will only be felt if the situation becomes very protracted and serious.

At this point, it is also difficult to predict things like whether the UAE will withdraw from OPEC and begin to increase oil production, but our view at the moment is that such an impact is unlikely.

Q&A: Performance plan for fiscal 2026

Questioner: I would like to ask about your performance plan for this fiscal year. M&A effects are approximately 4 to 5 billion yen from Vulcan Materials, 2 to 3 billion yen from Tokuyama, and 3 to 4 billion yen from improvements in the Philippines and Asia.

Based on this, I imagine that results will improve by about 10 billion yen. However, your company's plan for the current fiscal year is for a slight increase in profit, which appears to be limited to a levelling off of additional profit. With M&A effects alone increasing revenue by 10 billion yen, please tell us about the factors that offset this increase. Are you concerned about the negative impact of the situation in the Middle East?

From $130 in the previous fiscal year's financial results, the coal price has increased by $25 to $155 this fiscal year, which will have an impact of about 5 billion yen in terms of sensitivity. Do you think that with the addition of further logistics and other costs, M&A effects will be canceled out by the situation in the Middle East?

Respondent 1: As you mentioned, we expect the impact of the situation in the Middle East on our domestic business to be about 10 billion yen. Therefore, the M&A effects mentioned earlier will be almost canceled out.

In addition, besides the situation in the Middle East, recent inflation and rising labor costs have also had an impact. This is reflected not only in labor costs, but also in repair and capital expenditures and depreciation, and is a major factor in the increase in fixed costs, inhibiting profits in the current fiscal year.

Questioner: Is it correct to say that on an actual basis, excluding M&A effects, the situation this fiscal year is either stable or rather difficult?

Respondent 1: In addition to the impact of reduced volumes in Japan, there will be no price increases this year. Therefore, to put it simply, I think your perception is correct.

Questioner: Since the assumption is that domestic demand for cement is 29 million tons, am I correct in understanding that unless overall demand recovers a little more, the reality is that this will be a rather difficult year?

Respondent 1: If nothing else happens, that would be the situation, but in fact, price increases have had an effect of about 75% last year and about 25% this year, so there is of course a positive effect. However, I think you are correct for the most part.

Q&A: Backdrop to the decision to raise prices

Questioner: This is about domestic price increases. At the briefing held in April of this year to reflect on the Medium-Term Management Plan, I believe there was a statement to the effect that your company plans to wait and see about the situation with Tokuyama until it can obtain clearance from the Fair Trade Commission.

What is the background to the announcement of a 3,000 yen per ton price increase on this occasion, which comes approximately two months after that briefing? Can you please explain in detail why your attitude toward price increases has changed over the past two months, for example, in relation to the impact of the situation in the Middle East?

Respondent 1: My explanation at the briefing for reviewing the 26 Medium-Term Management Plan was due to the time at which the Fair Trade Commission's examination of Tokuyama began, and to the fact that it is a very sensitive issue.

In fact, we are always considering price increases, and information was included in an industry publication last December. The backdrop to the reason for this price increase is that it is not a sudden occurrence and has been under consideration for some time. Therefore, it has nothing to do with Tokuyama or the current situation in the Middle East.

We have been discussing internally when it would be appropriate to announce this price increase, with consideration for deferring the timing for our customers. As a result, we have determined that since this price increase is a separate issue unrelated to clearance, etc., it is necessary to explain the current situation to customers separately. Against this backdrop, we made the official announcement yesterday.

Q&A: Customer response to price increase implementation

Questioner: I believe that the last two price increases were easily understood due to effects from the external environment, such as rising coal prices and the problem in 2024 related to logistics. Of course, I fully understand that costs continue to rise today, but the situation has calmed down somewhat compared to the previous two price increases.

In this context, what are your thoughts on how to achieve this 3,000 yen price increase?

Respondent 1: After April 2027, as in the past, we will proceed with passing on the increased costs of ready-mixed concrete products to coincide with announcements, and we intend to work on this on a year-round basis, including in the general contractor supply chain.

Announcement dates coincide with those for financial results, and the previous announcement was on May 9. This is also being implemented at the same time this year, and we are proceeding without regard for the situation in the Middle East. Therefore, we have no intention of changing the amount from 3,000 to 4,000 or 5,000 yen simply because of the situation in the Middle East.

We accept the obligation based on the idea of valuing a year-long cycle. We may take the next price pass-through into account, but we are always willing to work together with our customers.

Most importantly, we have assumed that domestic demand for cement will be 29 million tons this time around, and the decline in volume is a particularly significant factor. The numbers did not fall because of price increases.

Currently, the adoption rate for the two-day weekend is 100% in Kanto 1, Shikoku, Hokkaido, Osaka, and Hyogo. However, since this system has not yet been introduced in Nagoya in Tokai, Fukuoka in Kyushu, Hiroshima in Chugoku, and Sendai in Tohoku, it appears that the numbers may drop further in the future.

Thus, the decrease in volume can be attributed to manpower. With general contractors, current order backlog and nominal construction investment have reached similar levels to the time of the so-called bubble economy. Therefore, even if the decline in volume continues, we believe it will pick up as general contractors' construction techniques progress and change, and we are working from the perspective that the decline will not be permanent.

Respondent 1: We have also been telling our customers for the past two years that not only coal but also the various environments surrounding us are leading to increased costs. In addition, the Integrated Report includes the term "7R+1T," meaning seven risks (R) and one threat (T).

The seven risks include demand continuing to decline, CO2 emissions trading beginning under the Emissions Trading System (ETS), and coal remaining vulnerable with no way of telling how it will fare.

In addition, there are serious issues with the Mineral Resources Business. The Buko mine in Saitama Prefecture is said to have only 50 years left as its resources continue to decline. There are two ways of looking at this: "We still have 50 more years" and "We only have 50 more years," but in the cement industry, the attitude is that "we only have 50 more years."

For this reason, we are currently developing the Tsukumi mine and have secured 500,000 tons of yard space in the Kanto area as a whole. In southern Kanto, we supply from the Tsukumi mine, and in northern Kanto, we are pursuing a very long-term plan and investment using the resources of the Buko mine.

Regarding production facilities, we have 17 kilns, although the newest of these is the T3 in Tsukumi, which was installed in 1982. Forty years have passed since then, repair costs are increasing as the kiln continues to deteriorate, and more major breakdowns are occurring. Things like this cost money.

Next is the issue of labor costs. We have told our customers that the industry will not be viable unless we think carefully about the issue of labor costs, including those relating to our logistics employees, and respond to cost increases. Finally, there are geopolitical risks. There is uncertainty in not knowing what will happen at any given time.

In this way, we are explaining that compounding factors are involved in increased costs. We continue to carefully explain to our customers so they understand to some extent that just because coal is settling down, it does not necessarily mean that everything is okay.

In addition, although price pass-throughs have been difficult in the industry for many years, we now have the understanding of everyone in the ready-mixed concrete industry and of general contractors. With each general contractor company also making a profit, some of the business practices and sensibilities of the past are changing. Therefore, I do not believe that the current situation is particularly tough.

Then there is the demand that was mentioned earlier, and some people are saying that it is getting lower and lower. Just a few days ago, a budget was announced of "more than 20 trillion yen over five years" for national resilience, but I feel that this is not at all sufficient.

The recent House of Representatives election campaign was all about the sales tax, but the reality is that there was no discussion about how to respond to a Nankai Trough earthquake, an earthquake directly under the capital, or a major earthquake in Hokkaido. The topic of a Mt. Fuji eruption has also been covered on TV, but no budget for these eventualities has been secured.

The government does not appear to be tackling these issues very proactively. However, compared to the time of the 2011 Great East Japan Earthquake, cement demand increased by 7 million tons in 2013.

There was a demand for 7 million tons in that region alone, plus other regions responded, but Japan is a country that would need a substantial budget to tackle these issues in earnest. With this as a starting point, it is our contention that the nation will not be able to maintain itself unless it increases domestic demand for cement—which is currently less than 30 million tons—to 35 or 40 million tons.

We believe that demand will surely increase if infrastructure investment is properly made at some point. We see this as a transitional period and a situation in which we must stand firm.

Message from Mr. Taura

Taura: I would like to take some time at a later date to give a full management briefing. As this will also constitute our policy for the next Medium-Term Management Plan, we hope you will participate and we appreciate your continued understanding.

Thank you very much for your time today.