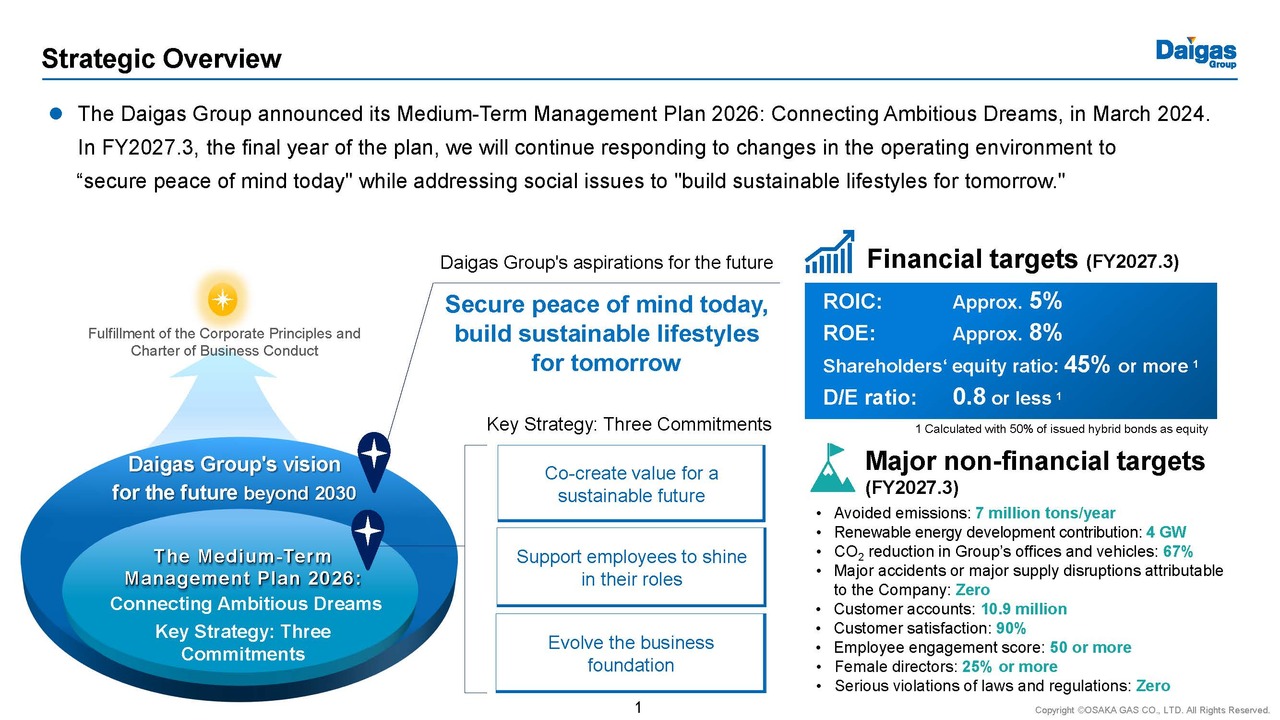

Strategic Overview

Tadasu Yano (“Yano”): I am Tadasu Yano, Executive Officer and Senior General Manager of Corporate Strategy Department at Osaka Gas Co., Ltd. Today, I will walk you through the Daigas Group FY2027.3 Management Plan. Let me begin with our overall direction. Under our Medium-Term Management Plan 2026, we are guided by our vision: "Secure peace of mind today, build sustainable lifestyles for tomorrow." We provide a safe and stable energy supply to ensure customer peace of mind, even amid geopolitical uncertainty while addressing long-term social challenges.

FY2027.3 marks the final year of the current plan. In this final year, we will focus on executing our key initiatives and delivering on our targets.

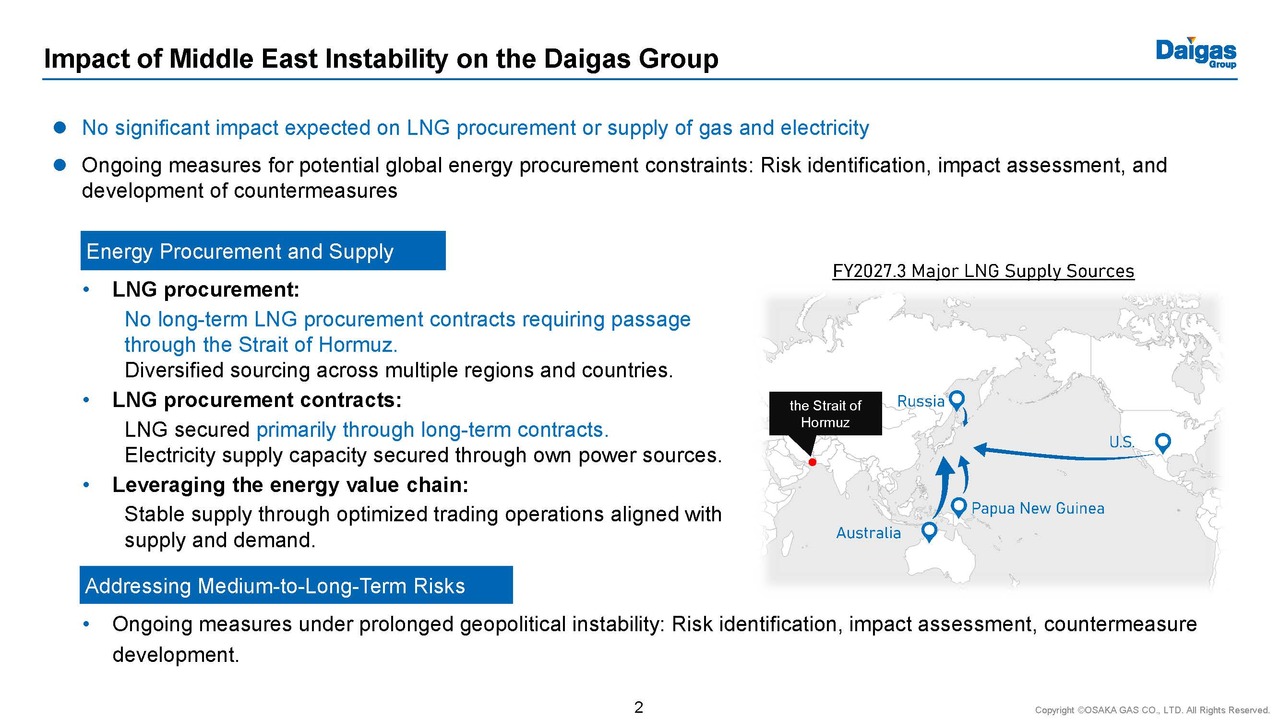

Impact of Middle East Instability on the Daigas Group

Before turning to the details of the plan, let me briefly comment on recent developments in the Middle East, including the Strait of Hormuz. At present, we see no immediate impact on our LNG procurement or overall energy supply. We do not source LNG via the Strait of Hormuz and maintain a well-diversified procurement portfolio. In addition, our long-term contracts and owned power sources provide a stable supply base. That said, the situation remains uncertain. Should instability persist, global energy procurement conditions could tighten. We will continue to closely monitor developments and take appropriate measures to mitigate risks.

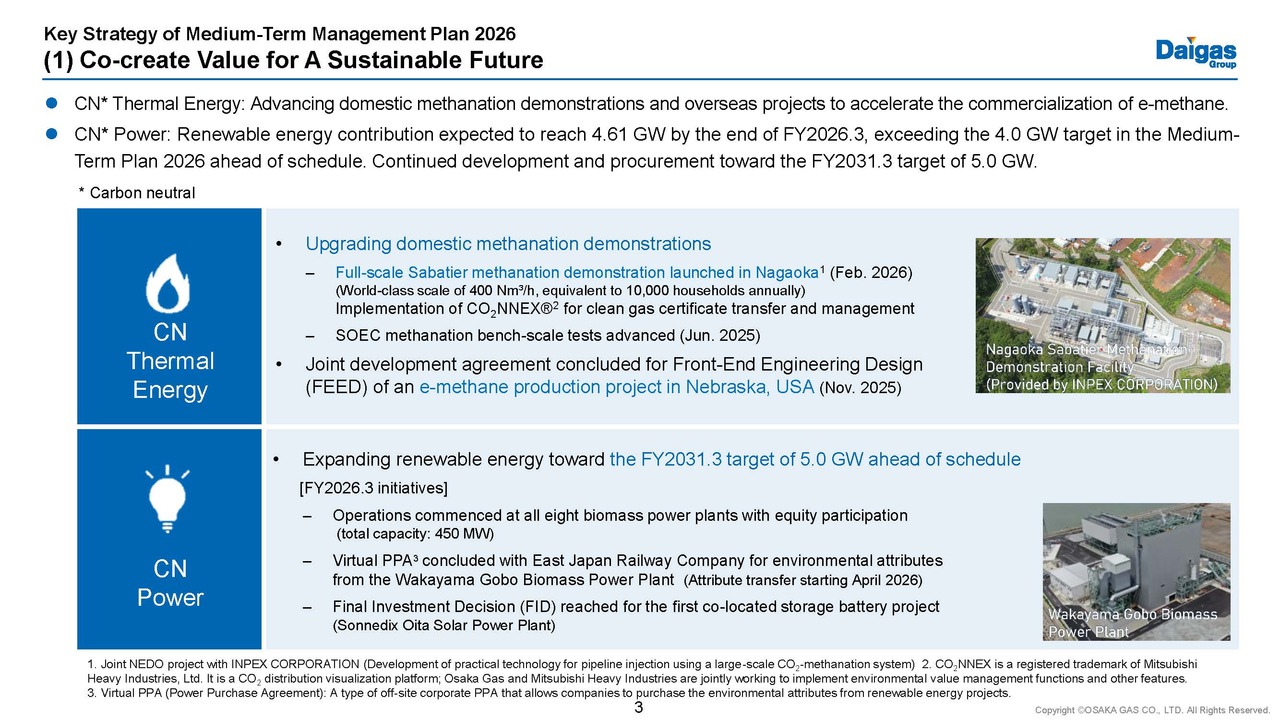

Key Strategy of Medium-Term Management Plan 2026 (1) Co-create Value for A Sustainable Future

Let me now turn to the key initiatives of our plan. I will begin with our carbon neutrality strategy. Under our priority of "Cocreate value for a sustainable future," we are making steady progress.

In thermal energy, we are working toward introducing more than 1% e-methane by FY2031.3. We commenced full-scale Sabatier methanation trials in Nagaoka in February and are also advancing bench-scale testing of SOEC methanation technologies. Overseas, we are progressing FEED for an e-methane production joint project in Nebraska, U.S.

In electricity, all of our eight biomass power plants are now operational, and our renewable energy development contribution is expected to reach 4.61 GW in FY2026.3. We remain on track to achieve 5 GW by FY2031.3, while also expanding storage battery capacity.

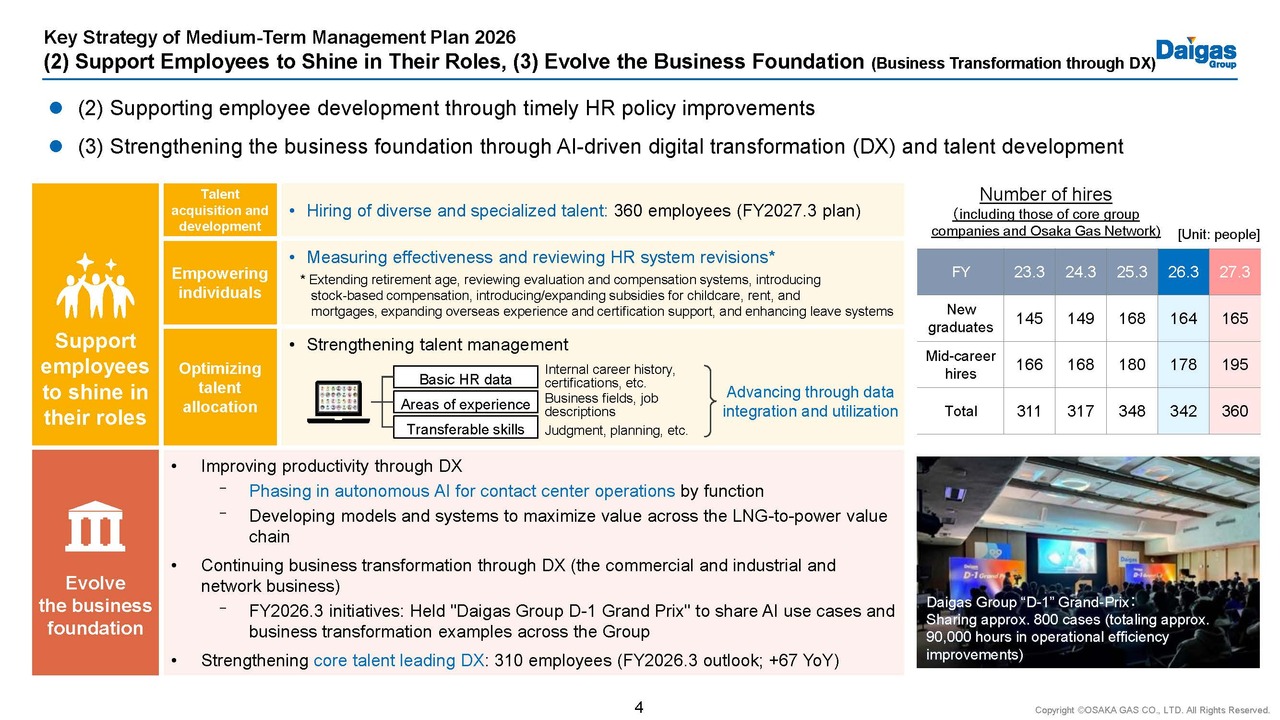

Key Strategy of Medium-Term Management Plan 2026 (2) Support Employees to Shine in Their Roles, (3) Evolve the Business Foundation (Business Transformation through DX)

Next, let me move on to other key initiatives, " Support employees to shine in their roles" and “Evolve the business foundation.” We are strengthening both human capital and digital transformation.

On the human capital side, we are enhancing talent acquisition, targeting 360 hires in FY2027.3, including core companies and Osaka Gas Network. At the same time, we are accelerating DX across our operations. This includes scaling the use of AI in customer service and optimizing the LNG and electricity value chain to improve productivity and efficiency. We are also fostering a culture that promotes DX and strengthening core talent to accelerate these initiatives.

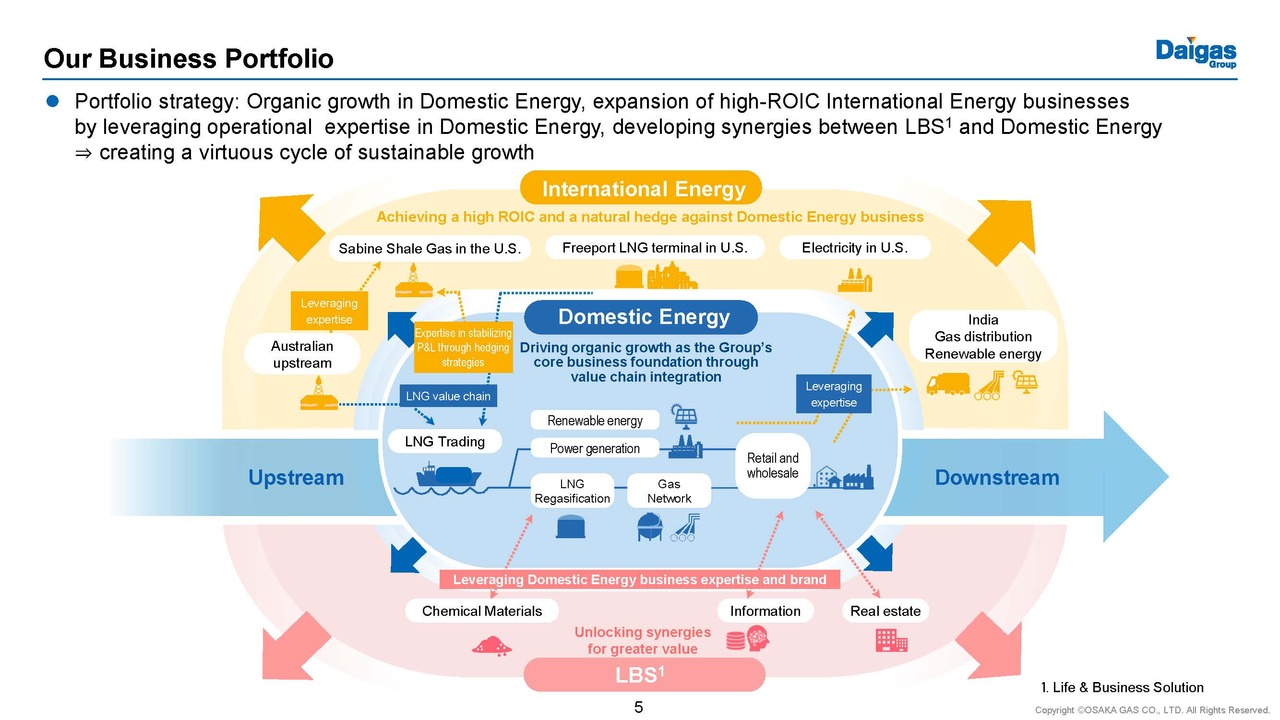

Our Business Portfolio

As shown on this slide, we leverage our Domestic Energy business as our core, capturing synergies to drive growth in International Energy and Life & Business Solutions (LBS).

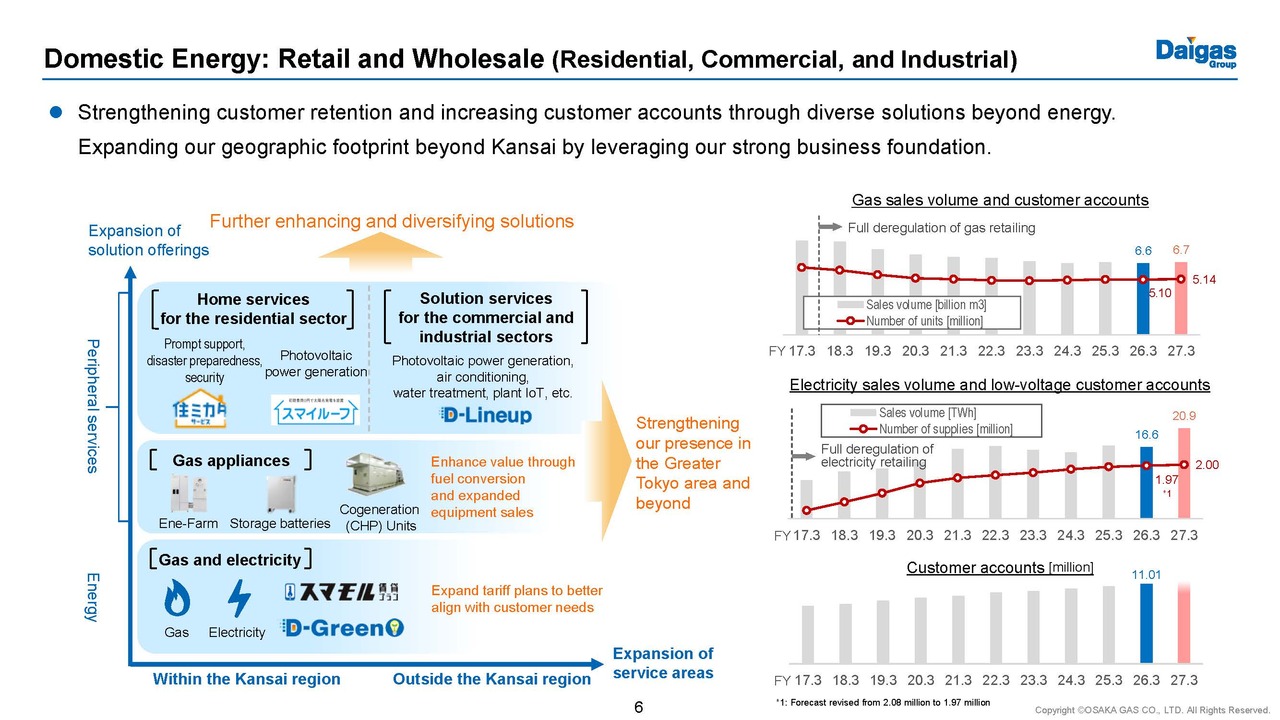

Domestic Energy: Retail and Wholesale (Residential, Commercial, and Industrial)

In the Domestic Energy Business, we are accelerating cross-selling and nationwide expansion by leveraging our strong customer base and broad product portfolio.

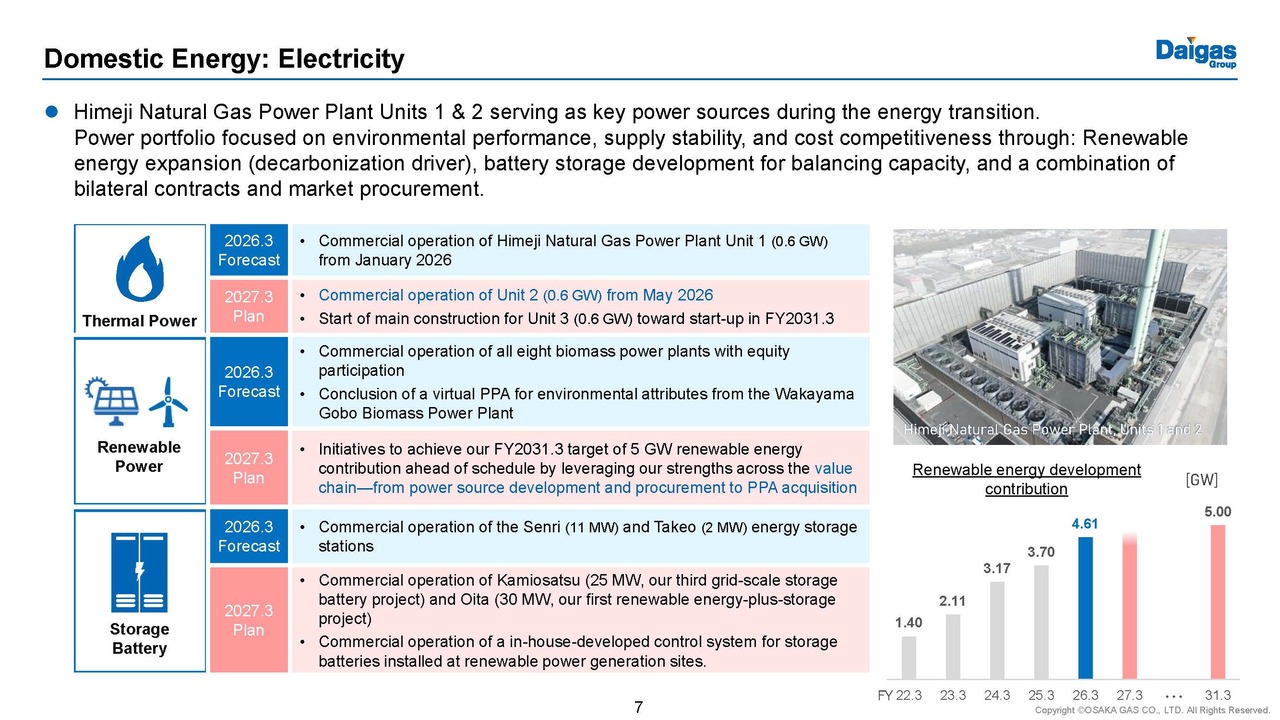

Domestic Energy: Electricity

Turning to the power and renewable energy business. In the domestic thermal power, Unit 1 of the Himeji Power Plant began operations in January 2026, with Unit 2 scheduled for May. These additions will increase our capacity by 1.2 GW to 3.2 GW, enabling us to respond promptly to rising electricity demand from data centers and AI. We have also started construction of Unit 3, targeted for operation in FY2031.3.

In renewable energy, we will continue to expand development and procurement while leveraging our integrated value chain to provide added value to customers, including through virtual PPAs. Through these initiatives, we will further grow our renewable energy business. Details on storage batteries will be covered on the next slide.

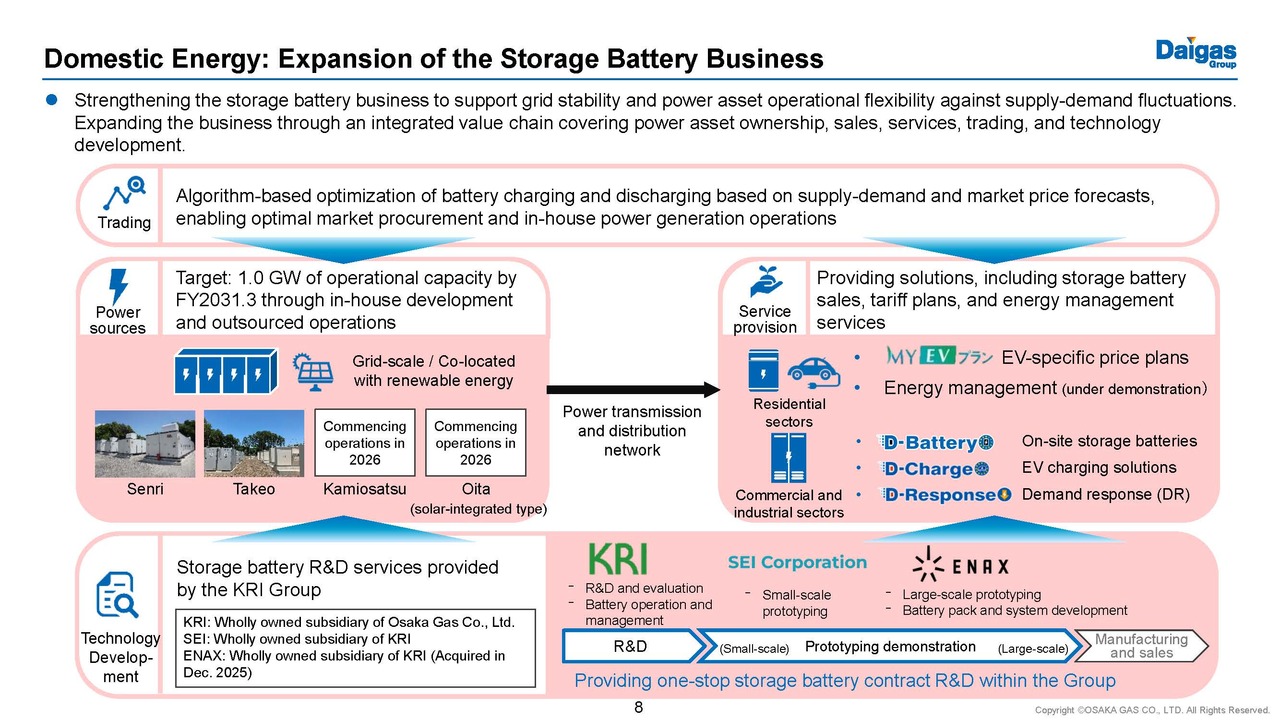

Domestic Energy: Expansion of the Storage Battery Business

The rapid expansion of renewable energy has significantly increased demand for storage batteries. We are building our battery business across the entire value chain, from grid-scale and co-located systems to on-site installations for customers. Our competitive advantage lies in the integration of trading capabilities to monetize batteries in power markets, DX-driven automated operations, and advanced technical expertise accumulated at KRI, our R&D subsidiary. In addition, KRI’s recent acquisition of ENAX shares enables a one-stop platform from R&D through large-scale prototyping. By leveraging these strengths, we aim to establish ourselves as a fully integrated battery business operator.

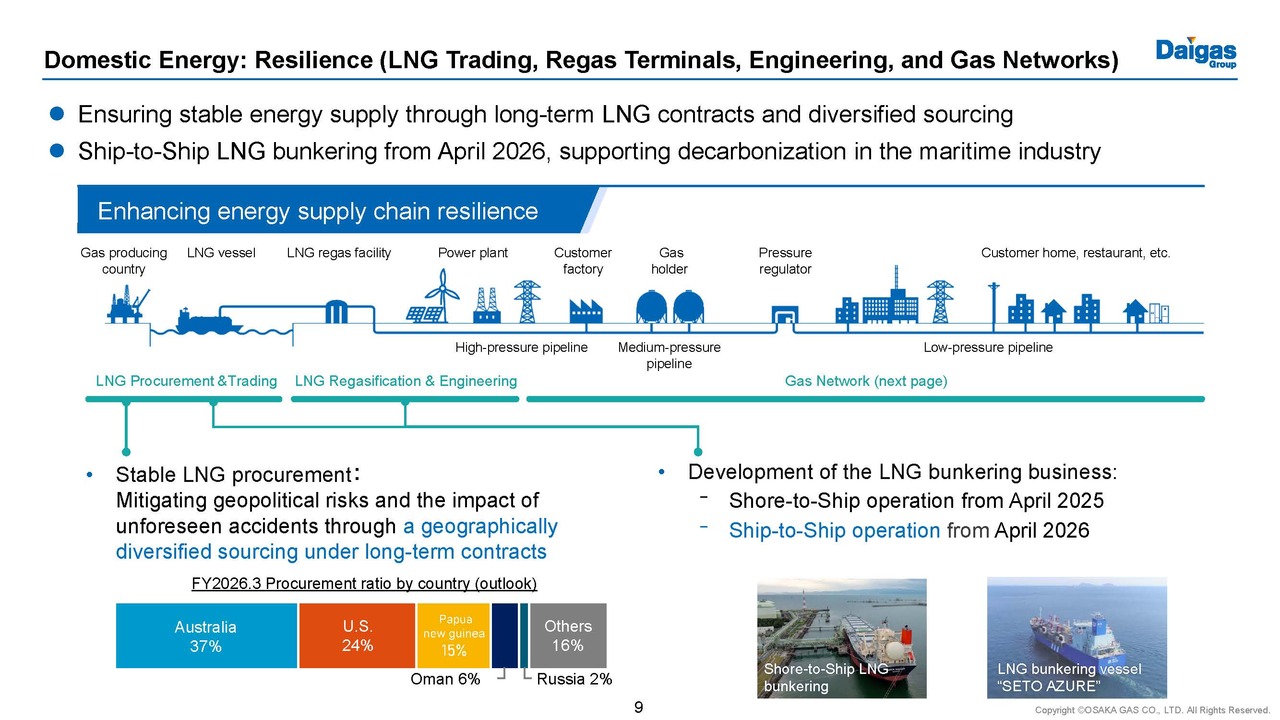

Domestic Energy: Resilience (LNG Trading, Regas Terminals, Engineering, and Gas Networks)

Next, let me turn to our efforts to enhance energy supply chain resilience. As previously mentioned, we will maintain stable LNG procurement through long-term contracts and geographic diversification. Meanwhile, demand for LNG as marine fuel is growing alongside the global shift toward carbon neutrality. Leveraging our experience in truck-to-ship and terminal-toship bunkering, we will expand into ship-to-ship bunkering using dedicated vessels starting this April. With the number of LNG-fueled vessels expected to rise, we are targeting an annual supply volume of approximately 70,000 tons by 2030.

Domestic Energy: Gas Supply Safety and Reliability

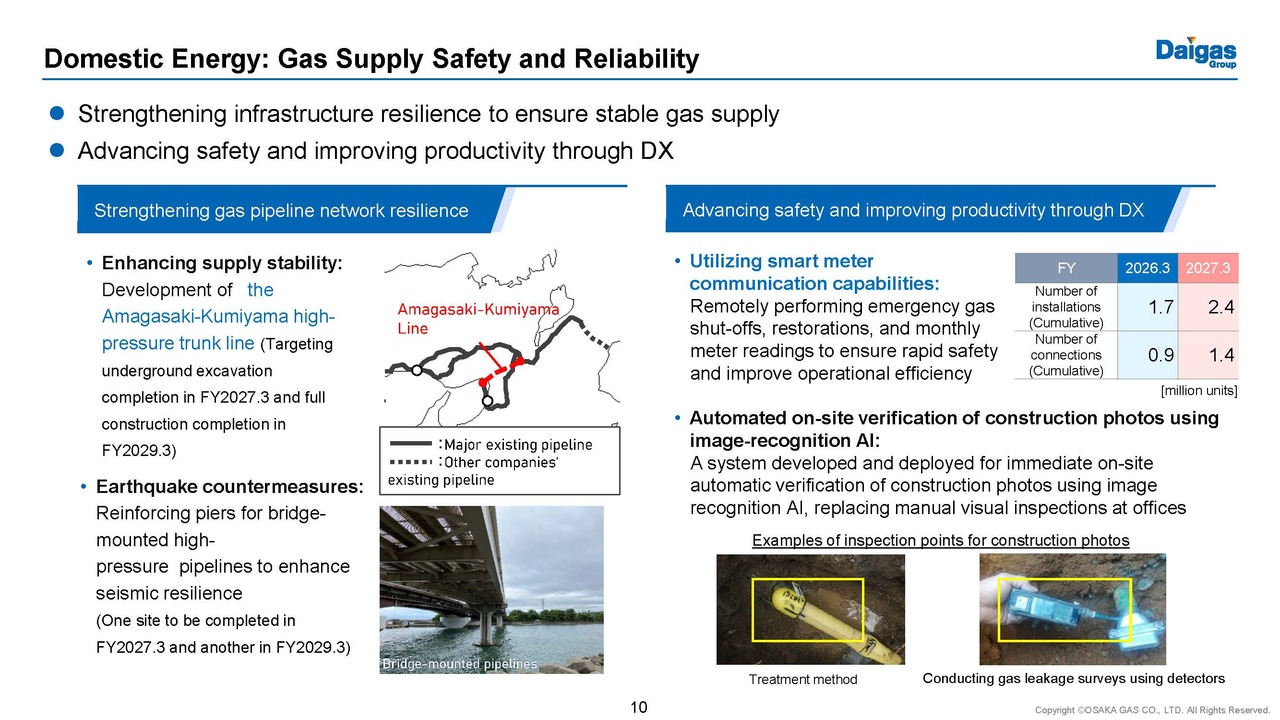

Next, let me turn to our network business. To strengthen supply stability, we are constructing the Amagasaki-Kumiyama highpressure pipeline, scheduled for commissioning in FY2029.3. In parallel, we are rolling out smart meters across all customers. Since FY2026.3, we have begun utilizing their communication capabilities to enable faster safety confirmation and improve operational efficiency, with full deployment targeted by FY2034.3.

International Energy: United States

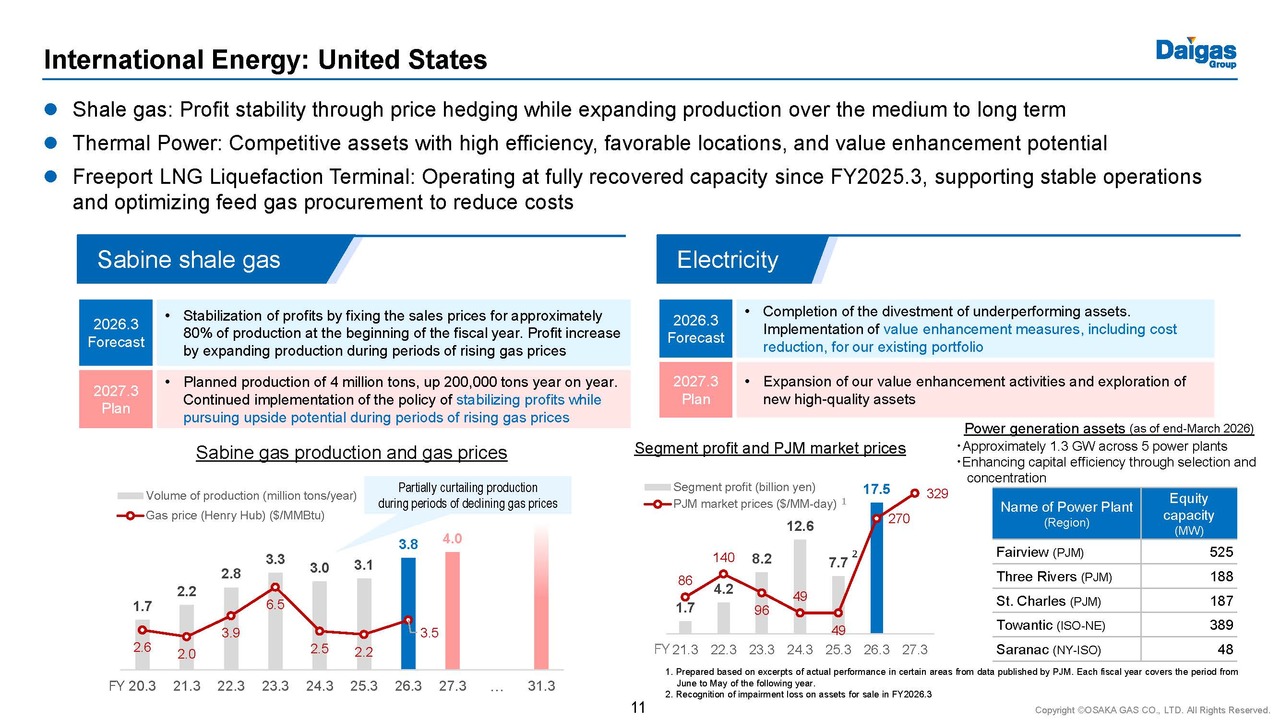

Next, let me turn to our International Energy Business. In upstream, our shale gas subsidiary Sabine dynamically adjusts production in line with market prices, increasing output during price upswings to capture upside. In the U.S. thermal power business, we provide timely supply from competitive power sources to meet growing demand driven by the expansion of AI and data centers. We will continue to enhance asset value while selectively pursuing high-quality investment opportunities to drive medium- to long-term earnings growth.

International Energy: India

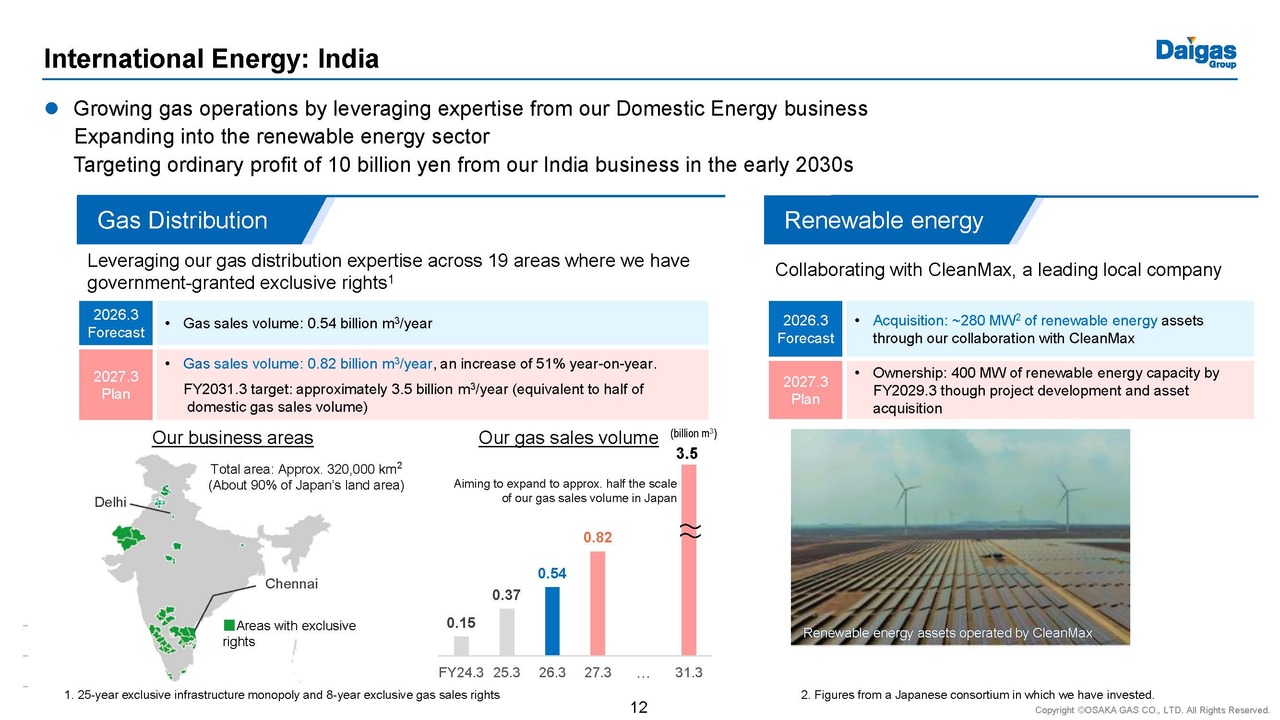

In Asia, we are expanding gas infrastructure in India. We target gas sales of 820 million cubic meters in FY2027.3 and 3.5 billion cubic meters in FY2031.3, equivalent to roughly half of our current domestic volume. At the same time, we are advancing renewable energy projects and asset acquisitions with local partners. By leveraging the expertise developed in Japan, we aim to generate approximately 10 billion yen in profit from the Indian market in the early 2030s.

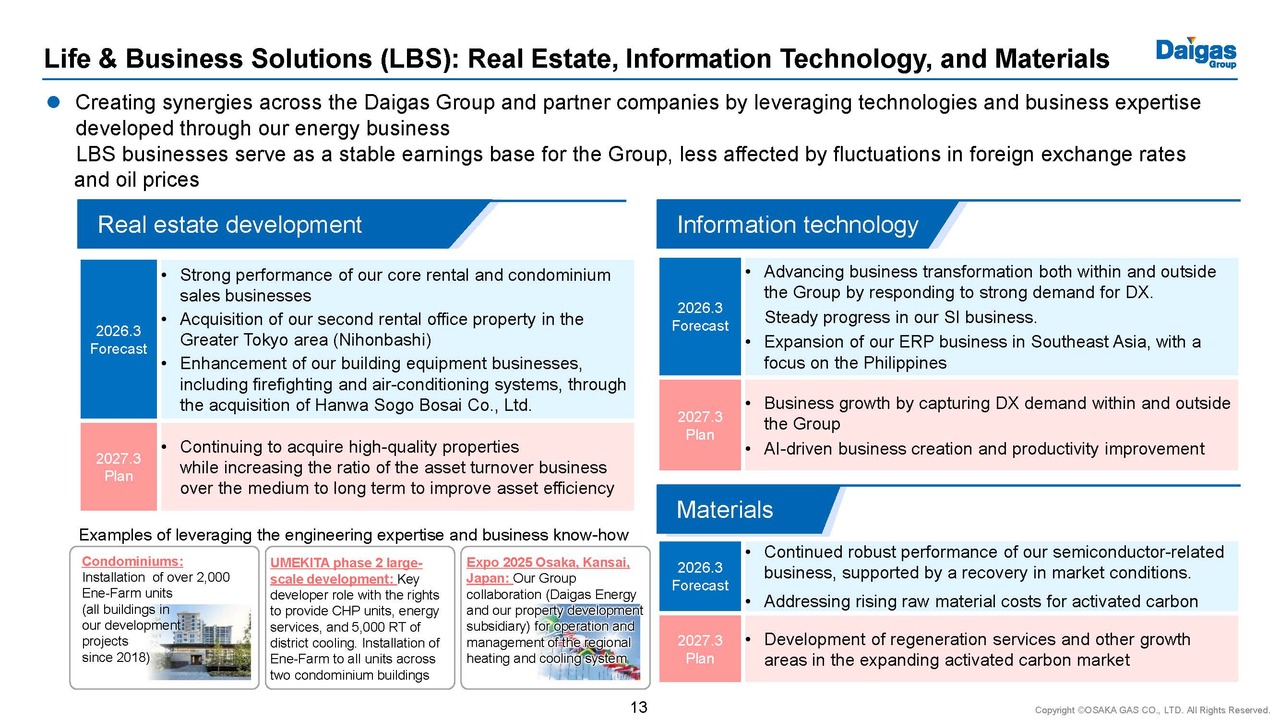

Life & Business Solutions (LBS): Real Estate, Information Technology, and Materials

Next, let me turn to the Life & Business Solutions (LBS) segment. Each of these businesses has evolved from our core gas operations, achieving steady and sustainable earnings growth by leveraging synergies within the Daigas Group.

In the real estate business, apartment leasing and condominium development and sales, our core operations, remain solid, and we are expanding into new areas such as offices in the Greater Tokyo area and logistics facilities. Over the medium to long term, we aim to increase the proportion of turnover-type businesses to improve asset efficiency while expanding profit scale.

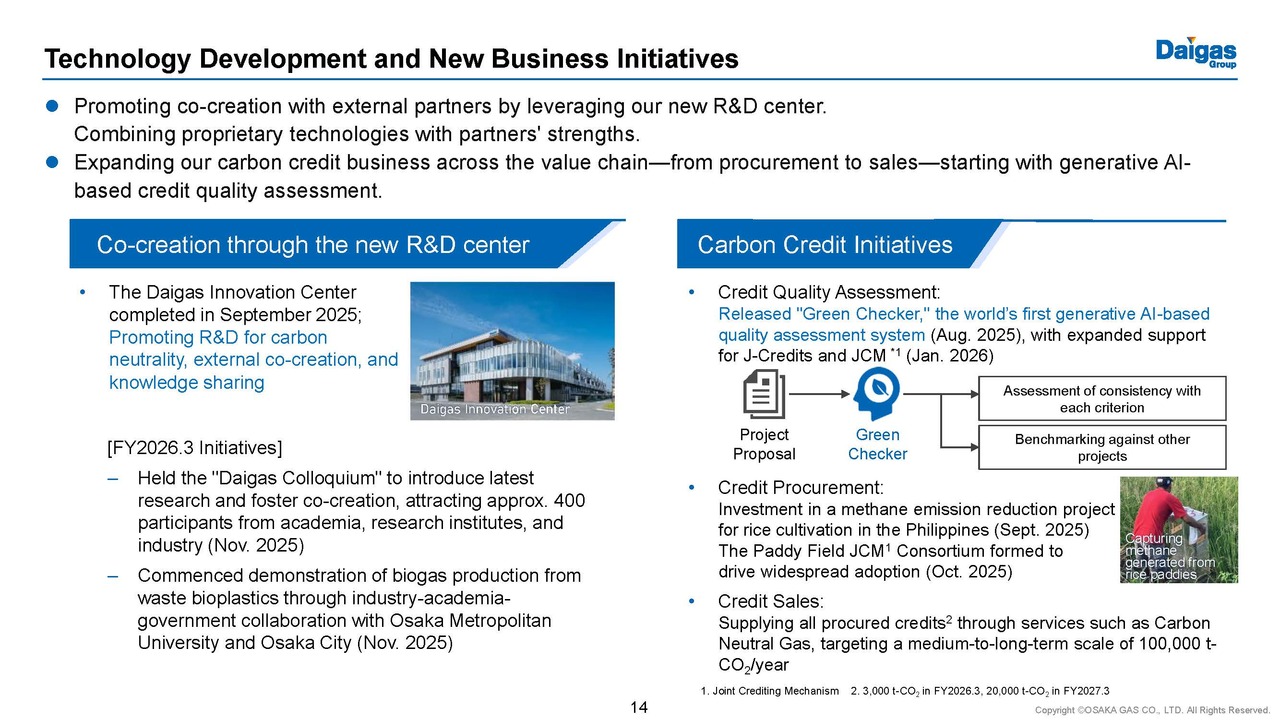

Technology Development and New Business Initiatives

Next, let me discuss our technology development and new business initiatives. We have completed the Daigas Innovation Center, a new R&D hub that will strengthen our research capabilities and accelerate value creation through enhanced facilities and open innovation with external partners.

In new business areas, we are focusing on carbon credits. Leveraging "Green Checker," our generative AI-based quality evaluation system, we are expanding our business across the entire carbon credit value chain, from procurement to trading and sales.

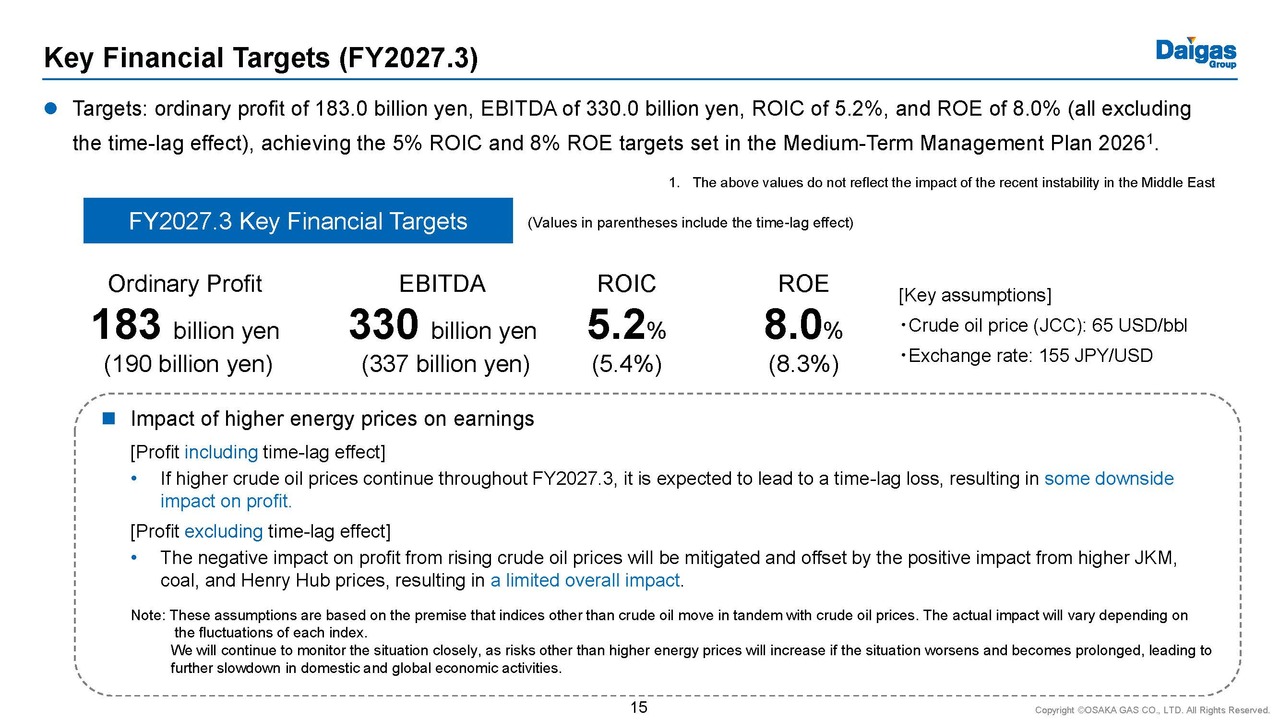

Key Financial Targets (FY2027.3)

Now, let me turn to our financial targets. For FY2027.3, we are targeting: ordinary profit (excluding time-lag effect) of 183.0 billion yen, EBITDA of 330.0 billion yen, ROIC of 5.2%, and ROE of 8.0%. These targets are in line with the goals set in our Medium-Term Management Plan. While these figures do not reflect the recent instability in the Middle East, we expect the negative impact from higher crude oil prices to be partially offset by positive effects from increases in other energy prices. Specifically, we assume a crude oil price of $65/bbl for FY2027.3. If crude oil prices were to increase by $30 to $95 per barrel and remain at that level for one year, ordinary profit would decline by 36.0 billion yen, including the time-lag effect. Excluding the time-lag effect, the negative impact on profit would be limited to 6.0 billion yen. This sensitivity analysis reflects only changes in crude oil prices; in practice, fluctuations in JKM and coal prices would also have an impact.

As mentioned at the outset, the situation remains highly uncertain. If economic activity in Japan and overseas were to slow further, these assumptions could be affected. We will continue to monitor developments closely and take appropriate measures as necessary.

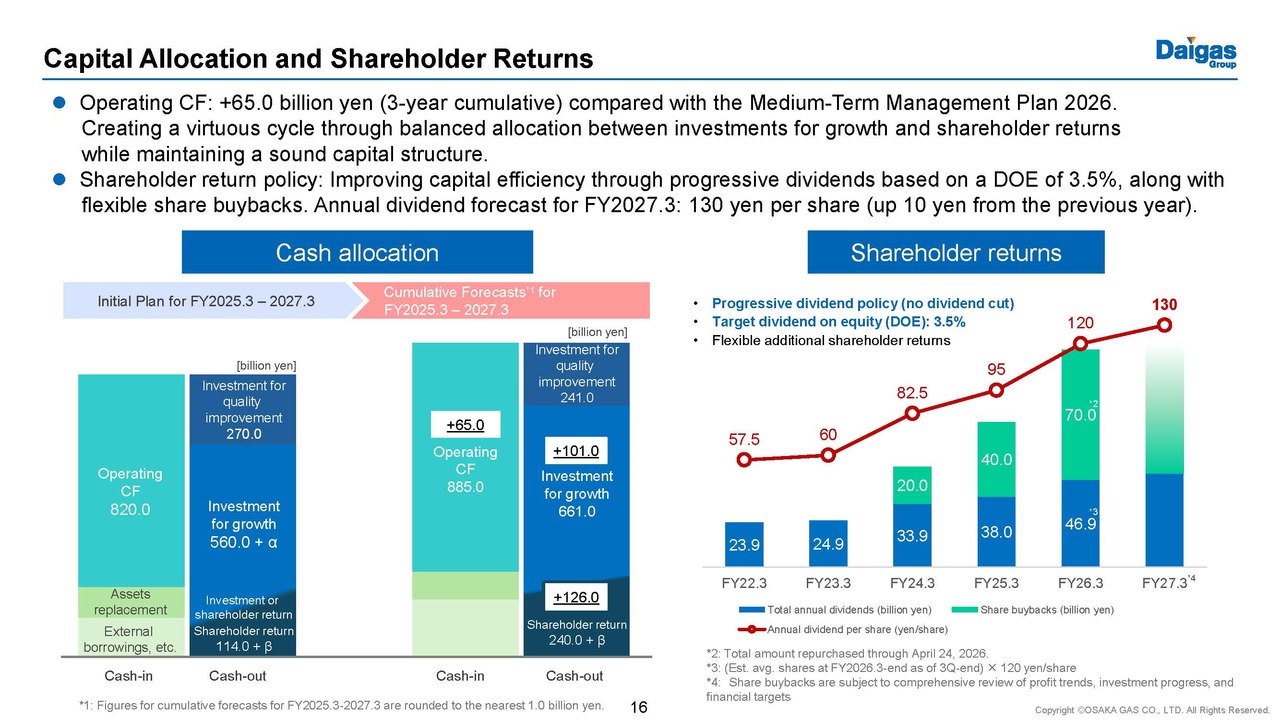

Capital Allocation and Shareholder Returns

Finally, let me turn to our capital allocation. We expect three-year cumulative operating cash flow to exceed the original plan by 65 billion yen. This increase will be allocated in a balanced manner between investments for growth and shareholder returns to support a virtuous cycle of long-term growth.

For shareholder returns, following the increase of our DOE target to 3.5%, we plan an annual dividend of 130 yen per share, representing a 10 yen increase. In addition, we will implement flexible additional return measures in line with business performance to ensure appropriate shareholder returns.

This concludes my presentation on the Daigas Group FY2027.3 Management Plan. Thank you.

Q&A at the Analysts' Meeting held on March 13, 2026, on the Business Plan for fiscal year ending March 31, 2027 (FY27.3)

Q1: Is the 8% ROE target for FY2027.3 based on profit excluding the time-lag effect? If the FY2027.3 profit falls short—for example, due to a higher-than-expected increase in shareholders' equity—would the target be achieved through capital control?

A1:The ROE target is based on profit excluding the time-lag effect. To achieve this target, both earnings growth and capital control are being pursued, with capital control considered one of the available measures.

Q2: How is shareholders' equity, the denominator for ROE, calculated?

A2: There has been no change from the forecast presented in our third-quarter financial results. While a share repurchase of 70 billion yen currently being executed, no additional measures have been decided for FY2027.3, and therefore none are reflected in the ROE calculation.

Q3: What are the key factors driving changes in profit by segment for FY2027.3?

A3: In the Domestic Energy segment, profit is expected to decrease. This is based on a crude oil price assumption of $65/bbl for FY2027.3, under which the time-lag gains are expected to narrow. In addition, higher fixed costs are anticipated in the electricity business, including depreciation related to the Himeji Power Plant. In the International Energy segment, profit is expected to increase, driven by a rebound from valuation losses on U.S. renewable energy recorded in FY2026.3, as well as higher shale gas production in the U.S. upstream business. In the LBS segment, gains on sales are expected to increase, supported by favorable real estate market conditions.

Q4: What would be the impact of higher JKM and coal prices?

A4: Higher JKM prices would have a positive impact on profit. This is because retail gas prices are linked to JLC, and increases in JKM may be accompanied by higher JLC and retail prices. In addition, our LNG procurement is primarily based on long-term contracts, with a relatively low share of spot purchases compared to peers. Similarly, higher coal prices would also have a positive impact on profit, primarily because retail electricity prices are adjusted in line with Kansai Electric Power’s fuel cost adjustment system. Given the relatively low share of coal-fired power in our portfolio, the increase in fuel costs is limited. That said, the overall impact will depend on the specific scenario, as prices may move independently, for example our LNG procurement costs or coal prices may rise on their own.

Q5: What are the ROIC levels by business within the Domestic Energy segment?

A5: As an indicative breakdown, using the segment's planned FY2027.3 ROIC of 3.3% as a benchmark, gas retail and production are above this level, while the electricity and network businesses are below it. The electricity business is below the benchmark due to higher fixed costs associated with the Himeji Power Plant. The network business is also below the benchmark, reflecting the delay in passing on inflationary costs.

At the segment level, ROIC remains below our medium-term target. One factor is that the FY2027.3 plan was formulated before the deterioration in the Middle East situation, when JKM was trending below the assumptions used in our Medium-Term Management Plan. As a result, the plan reflects a relative decline in the competitiveness of our long-term contracted LNG linked to JLC. ROIC is expected to improve gradually, supported in part by a steady reduction in fixed costs at the Himeji Power Plant.

Q6: What are your Henry Hub price assumptions and hedged levels for the U.S. upstream business in FY2027.3?

A6: Our Henry Hub price assumptions are not disclosed; however, they are broadly in line with market levels. In addition, approximately 80% of our production volume has been hedged.

Q7: The sensitivity to crude oil, excluding the time-lag effect, is negative 200 million yen per $1/bbl increase. What drives this?

A7: Higher oil prices have a positive impact on our upstream business in Australia, but a negative impact on the domestic electricity business. The net effect is a decrease of 200 million yen per $1/bbl increase.

Q8: Within the Domestic Energy segment, what is expected to drive the increase in profit from FY2026.3 to FY2027.3, excluding the time-lag effect?

A8: In LNG sales, profitability is expected to improve, driven by optimization of the sales portfolio.

Q9: What are your plans for LNG procurement from Oman and Russia?

A9: Our long-term contract with Oman expired in FY2026.3, and there will be no procurement from Oman from FY2027.3 onward. Procurement from Russia will continue, but it represents only a limited share of our total volume.

Q10: How do your long-term LNG procurement contracts work? Can volumes be adjusted during periods of low demand?

A10: In general, long-term contracts require us to off-take of fixed annual volumes in exchange for supply stability. When domestic demand declines and results in surplus LNG, the surplus is monetized through trading by reselling it to other regions.

Q11: The FY2026.3 forecast remains unchanged from the third-quarter financial results. Is progress in line with the plan?

A11: The forecast has been maintained as there have been no significant changes in the business environment. The current situation in the Middle East is not expected to affect our FY2026.3 results, as LNG prices for March have already been fixed.

Q12: Will fluctuations in electricity spot prices affect your financial performance?

A12: The impact of electricity spot price volatility on our overall results is expected to be limited. This is because our plan includes not only selling but also procuring a certain volume of electricity through JEPX. In addition, during actual operations, power generation is optimized, and therefore our performance does not necessarily move in line with market conditions.

Q13: What is the breakdown of investments for quality improvement and investments for growth for FY2027.3?

A13: Investments for quality improvement are broadly in line with previous years, with the largest allocation to pipeline-related construction, followed by maintenance of regasification facilities and commercial equipment. The overall amount is expected to decline year-on-year due to the absence of costs related to the rebuilding of our research facilities in FY2026.3. Regarding investments for growth, a significant portion in the Domestic Energy segment is allocated to the electricity business. Unit 1 of the Himeji Power Plant is already operational, and Unit 2 is scheduled for completion in May 2026; as a result, capital expenditure in this area is expected to decline compared with FY2026.3. In the International Energy segment, investment in the U.S. upstream business is increasing. In the LBS segment, real estate accounts for the majority of investments, with total investment rising, supported by favorable market conditions.

Q14: Growth in the domestic solutions business has historically been a focus. Going forward, will growth be driven by increased gas sales volume, or by profit from value-added services rather than gas sales?

A14: Our strategy is to grow profit through added value. For example, "Sumairoof" is a residential service under which we install and own solar panels on customers’ roofs, with customers paying a monthly fee equivalent to their electricity bill, eliminating the need for upfront investment. Similar services are offered for commercial and industrial customers. As these business models recover investment over several years, they do not generate significant profit initially; however, we expect profits to accumulate steadily over time as a stock-type business.

Q15: Regarding the expansion of the battery storage business, is it currently generating substantial profit, or is it still in an exploratory phase?

A15: Currently, with only two storage facilities in operation, profit remains limited. As profitability depends on electricity market conditions, this is not yet a business that guarantees substantial profit. While it still has elements of a development phase aimed at future expansion, we recognize its significant potential. Recently, battery prices have declined relative to historical levels, partly due to a slowdown in global EV market growth, creating an opportunity to install equipment at lower cost. Over the medium to long term, we believe that combining solar power with battery storage has the potential to provide a stable and affordable decarbonized power. Reflecting this potential as a future growth driver, we have set a target of 1 GW in operating capacity (on an investment decision basis) by FY2031.3.

Q16: What are your initiatives for the India business in FY2027.3?

A16: We will continue to expand gas sales volume through the construction of CNG stations and the extension of pipelines. We aim to steadily grow volume to 3.5 billion cubic meters by FY2031.3, equivalent to half of our domestic gas sales volume.

Q17: Is the solutions business expected to undergo structural changes relative to the conventional ESCO business, including through AI-driven initiatives?

A17: While no fundamentally new technologies have emerged compared with the past, we are now targeting a nationwide market. For example, there are approximately 10,000 designated energy management factories, representing a significant market opportunity. We provide tailored solutions to meet individual customer needs, including solar power, air conditioning, water treatment, and demand response. In addition, as the number of personnel capable of engineering design at these factories declines, we are promoting implementation proposals positioned as factory automation focused on energy management and carbon neutrality.