Contents

Takashi Kuramoto (“Kuramoto”): Good afternoon, everyone. Thank you for joining MEDIA DO Co., Ltd.’s financial results briefing for Q4 and the full-year FYE 2/26. I am Kuramoto from the Corporate Planning Department.

Today, I will explain our financial highlights and earnings trends, while Fujita will discuss our growth strategy and the full-year earnings forecast for FYE 2/27.

Executive Summary

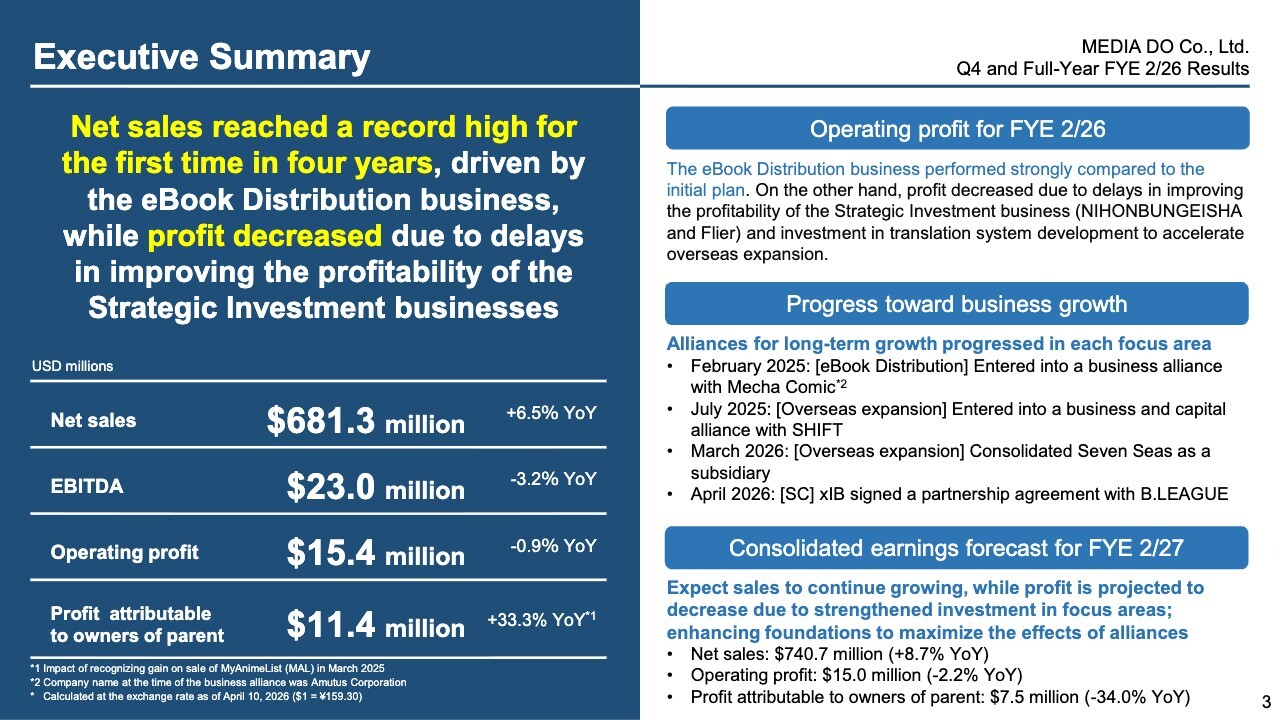

Please refer to the Executive Summary after the presentation.

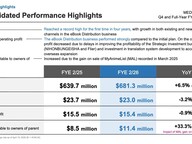

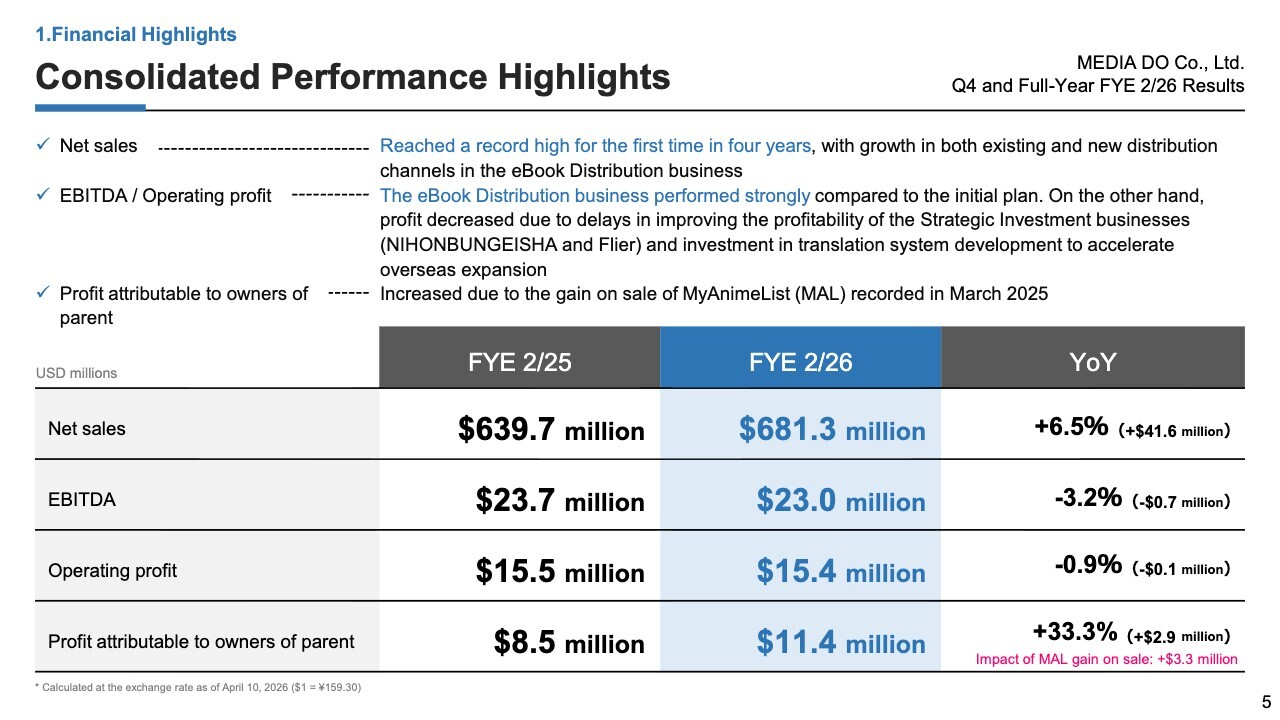

Consolidated Performance Highlights

Let me begin with our financial highlights. First, here are the consolidated performance highlights.

For the full-year FYE 2/26, net sales were $681.3 million, up 6.5% YoY; EBITDA was $23.0 million, down 3.2% YoY; operating profit was $15.4 million, down 0.9% YoY; and profit attributable to owners of parent was $11.4 million, up 33.3% YoY.

Net sales reached a record high for the first time in four years as both existing and new distribution channels grew in the eBook Distribution business.

On the other hand, EBITDA and operating profit declined due to delays in improving the profitability of the Strategic Investment businesses, particularly in H2,and investment in translation system development to accelerate overseas expansion although the eBook Distribution business performed strongly compared to the initial plan.

Profit attributable to owners of parent increased 33.3% YoY. This was mainly due to the gain on sale of MyAnimeList (MAL) recorded in March 2025. Although extraordinary losses were recorded in Q4 due to the recognition of an impairment loss on goodwill at NIHONBUNGEISHA, this was offset by extraordinary income associated with the sale or liquidation of subsidiaries and affiliates.

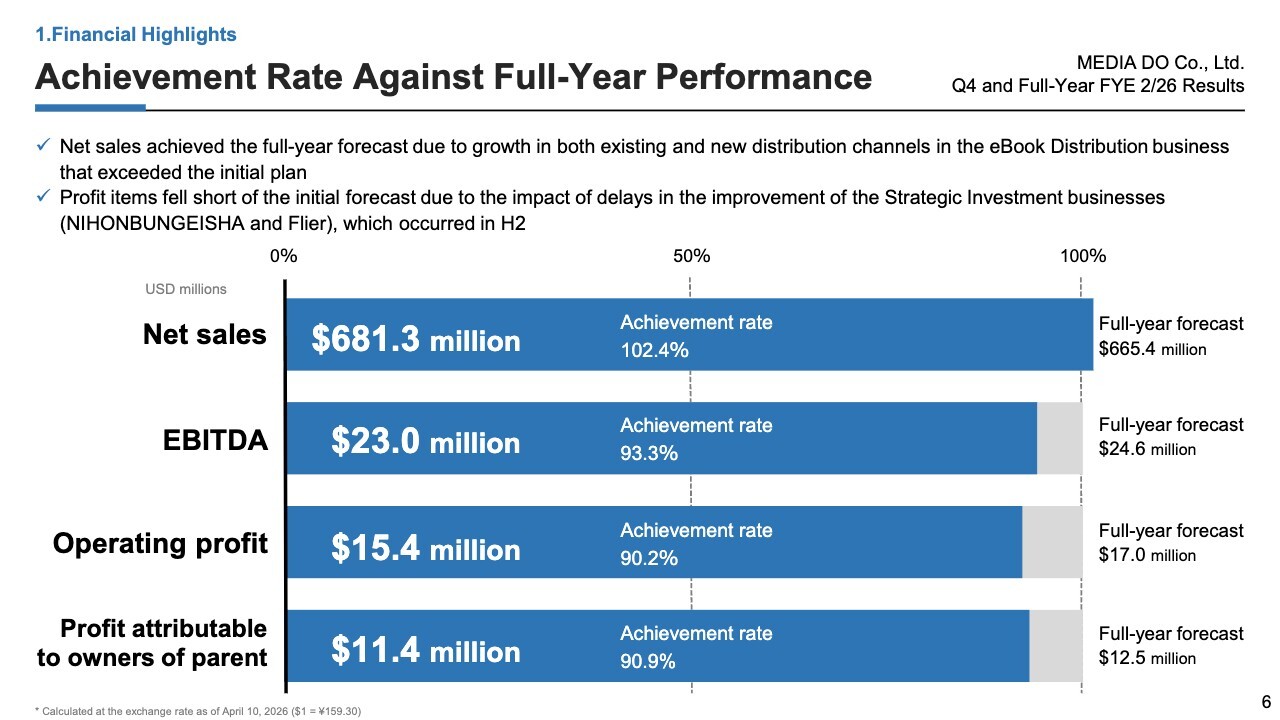

Achievement Rate Against Full-Year Performance

Let me move on to the achievement rate against the full-year performance. Net sales achieved the full-year forecast, with an achievement rate of 102.4%, due to growth in both existing and new distribution channels in our eBook Distribution business that exceeded the initial plan.

On the other hand, the achievement rates for EBITDA, operating profit, and profit attributable to owners of parent were 93.3%, 90.2%, and 90.9% of the initial forecasts, respectively, each falling short by slightly less than 10%.

The reasons for the shortfall in profit items will be explained on the next slide.

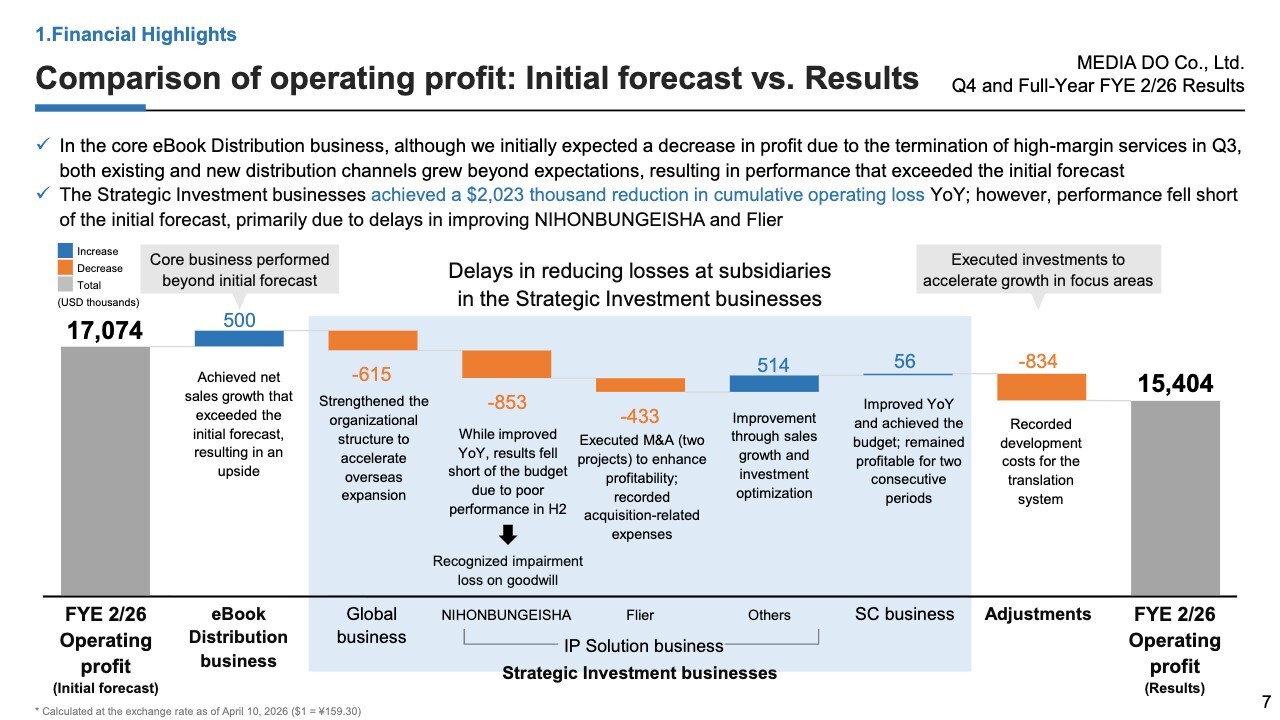

Comparison of operating profit: Initial forecast vs. Results

This slide compares the initial forecast and results for operating profit. As you can see on the left end of the slide, we initially forecast operating profit for FYE 2/26 at $17,074 thousand.

In our core eBook Distribution business, we initially expected a decrease in profit due to the termination of high-margin services in Q3. However, both existing and new distribution channels grew beyond expectations, resulting in performance that exceeded the initial forecast, with an increase of $500 thousand.

On the other hand, the Strategic Investment businesses achieved a $2,023 thousand reduction in cumulative operating loss YoY, demonstrating steady improvement. However, performance fell short of the initial forecast, mainly due to delays in improving NIHONBUNGEISHA and Flier from Q3 onward.

Here, let me explain the breakdown of the Strategic Investment businesses. In the Global business, our efforts to strengthen our organizational structure to accelerate overseas expansion resulted in a decrease of $615 thousand. Although we achieved an improvement of $564 thousand YoY for NIHONBUNGEISHA in the IP Solution business, poor performance in H2 led to a shortfall of $853 thousand against our plan.

Based on that result, we recognized an impairment loss on goodwill for NIHONBUNGEISHA. By writing down half of the goodwill at the end of FYE 2/25 and the remaining half at the end of FYE 2/26, goodwill related to NIHONBUNGEISHA has been fully written off as of the end of FYE 2/26.

Flier in the IP Solution business saw a shortfall of $433 thousand against our plan due to the recording of temporary acquisition-related expenses resulting from the execution of M&A to enhance profitability, despite an improvement of $131 thousand YoY.

Operating profit of Others and the SC business in the IP Solution business improved YoY, exceeding our initial forecasts. Steady sales growth and cost improvements led to higher sales and profits.

Adjustments reflect the execution of investments to accelerate growth in focus areas. The primary factor was the recording of development costs for the translation system, exceeding the initial estimate, to promote overseas expansion in our Global business. As a result, adjustments amounted to a negative $834 thousand, bringing our operating profit for FYE 2/26 to $15,404 thousand.

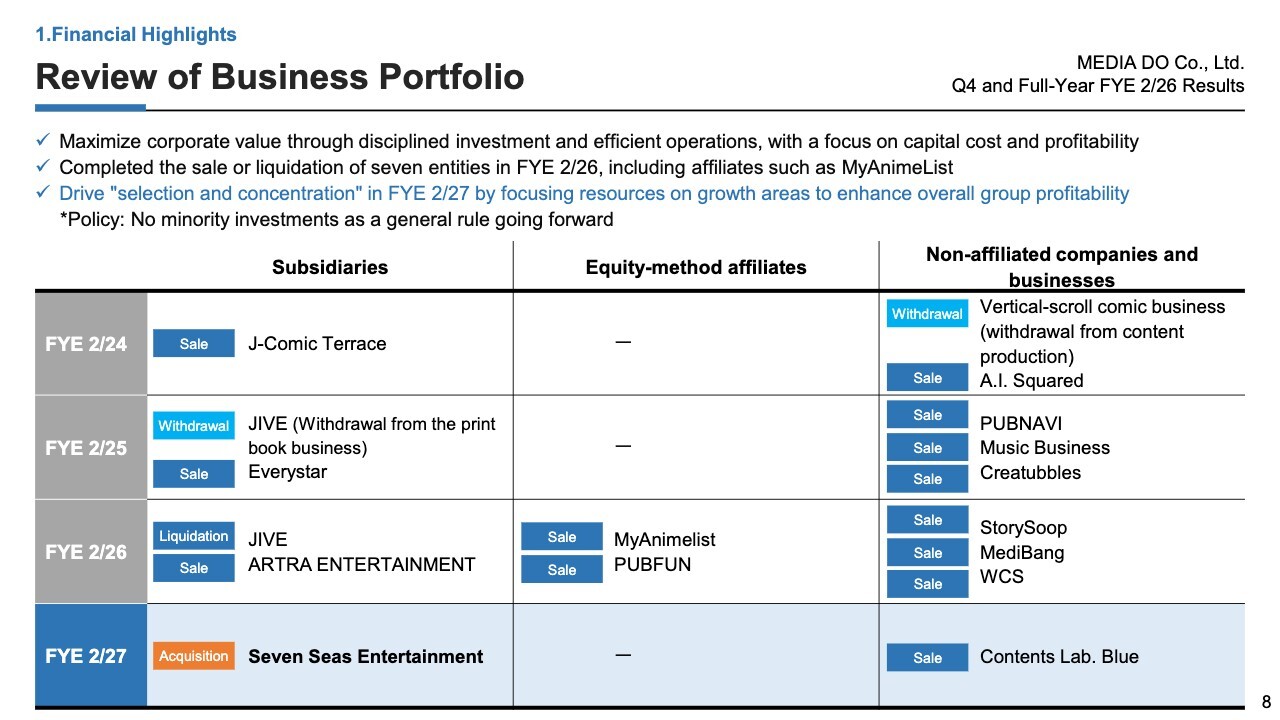

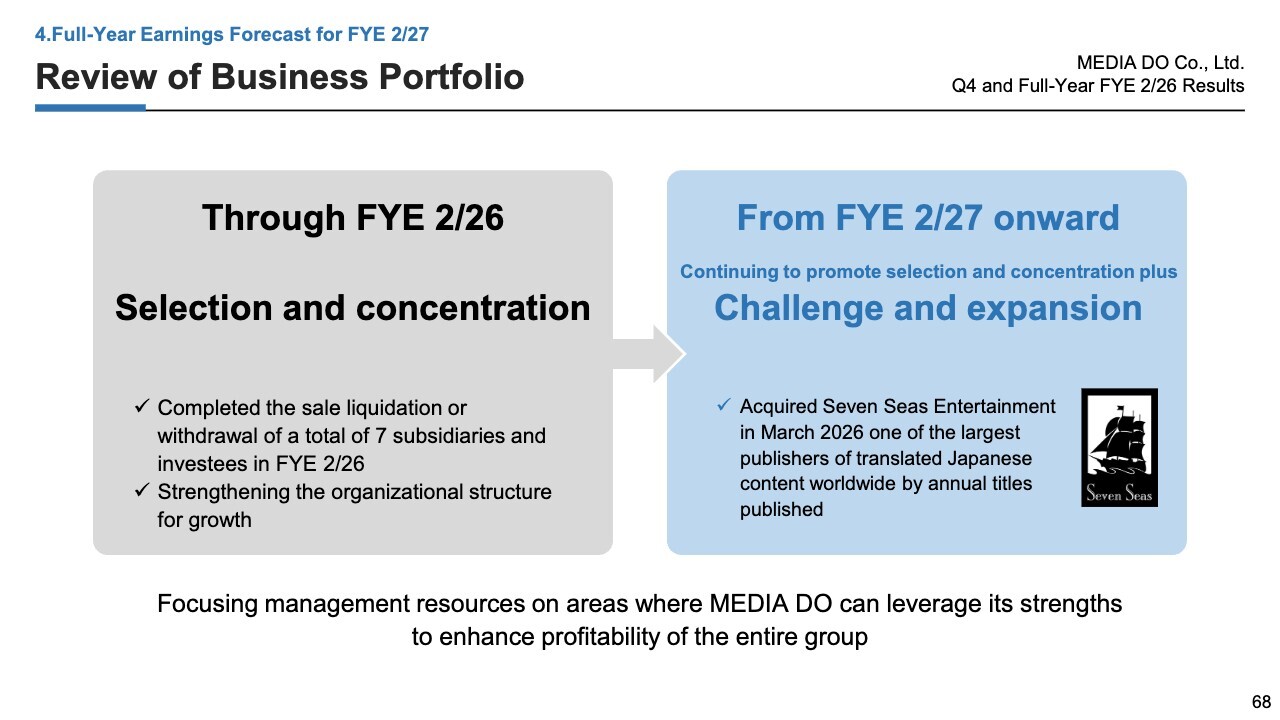

Review of Business Portfolio

Next, I will explain the review of our business portfolio. From FYE 2/24 to FYE 2/26, we have focused on reviewing our business portfolio.

In FYE 2/26 in particular, we liquidated JIVE and sold ARTRA ENTERTAINMENT, both of which were our subsidiaries, and also sold five other equity-method affiliates and minority investees, resulting in the sale or liquidation of seven entities. We intend to further drive selection and concentration in FYE 2/27 as well.

We have already completed the sale of a minority investee Contents Lab. Blue, a South Korean vertical-scroll manga production studio. Also, we are proactively reviewing our other businesses and minority investees.

Meanwhile, as shown in the lower left of the slide, we acquired Seven Seas Entertainment, LLC (“Seven Seas”) in March 2026.

This company is a U.S. publisher that boasts one of the world’s largest titles of translated Japanese content. We aim to enhance overall group profitability by focusing resources on such growth areas.

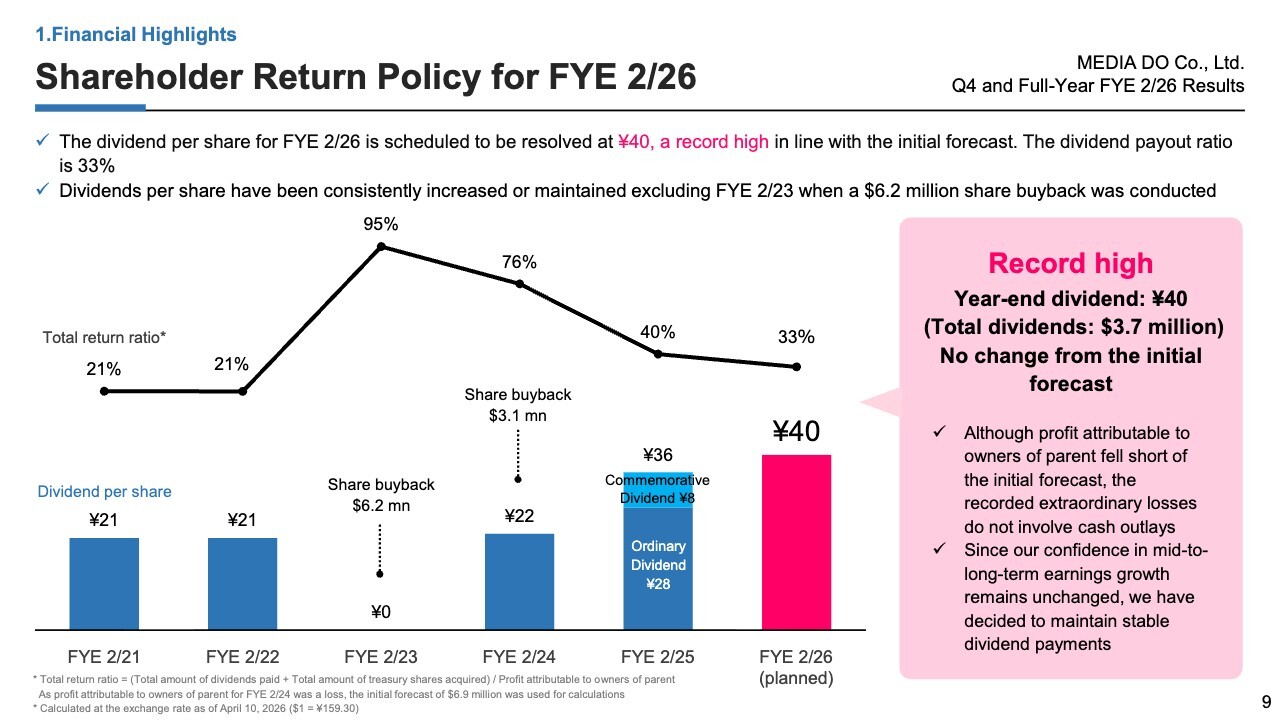

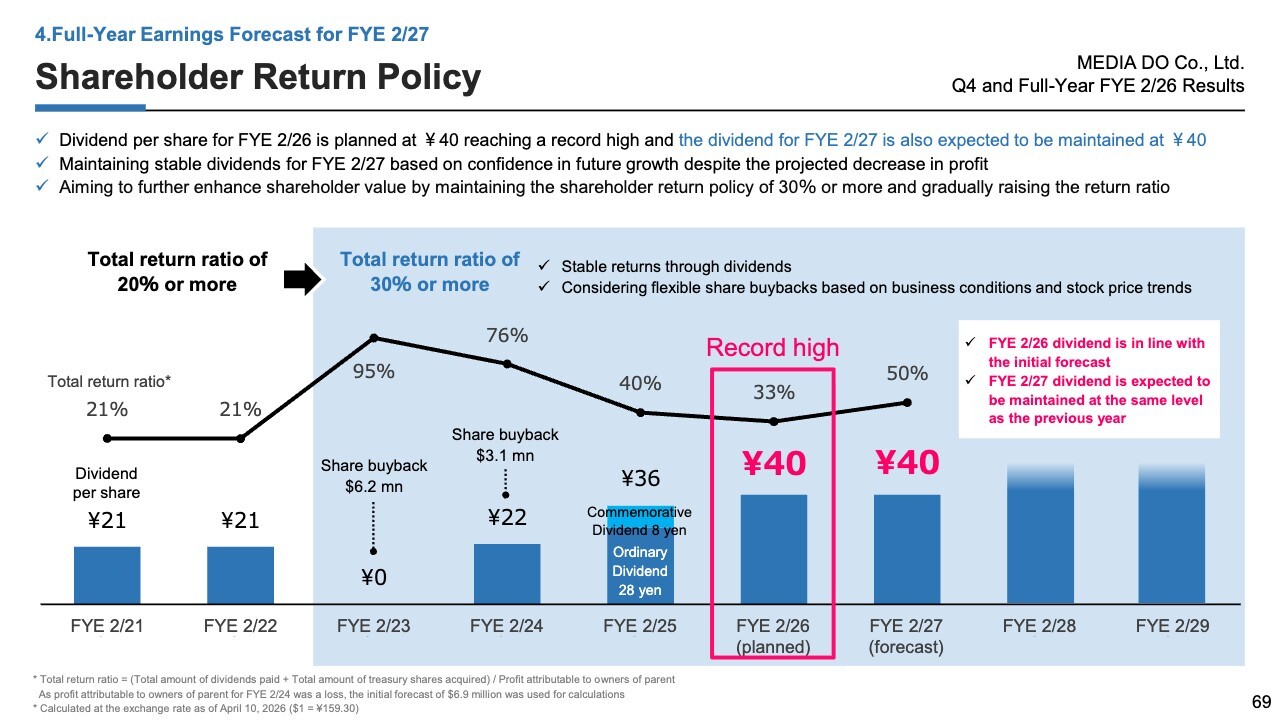

Shareholder Return Policy for FYE 2/26

Now, let me focus on our shareholder returns for FYE 2/26. Although profit attributable to owners of parent for FYE 2/26 fell short of our initial forecast, we plan to propose a record-high dividend of ¥40 per share, in line with our initial forecast.

We expect the dividend payout ratio to be 33%. Our shareholder return policy targets a total return ratio of 30% or higher. Specifically, since FYE 2/24, we have considered share buybacks to be an additional method of return, based on the assumption that a total return ratio of 30% is first achieved through dividends alone.

Except for FYE 2/23 when we conducted a $6.2 million of share buyback, dividend per share has generally increased since our listing or remained at the previous year’s level.

We will explain the details of our earnings and dividend forecasts for FYE 2/27 later, but in summary, we also plan to pay a dividend of ¥40 per share for FYE 2/27 and aim to continue delivering stable dividends in the future.

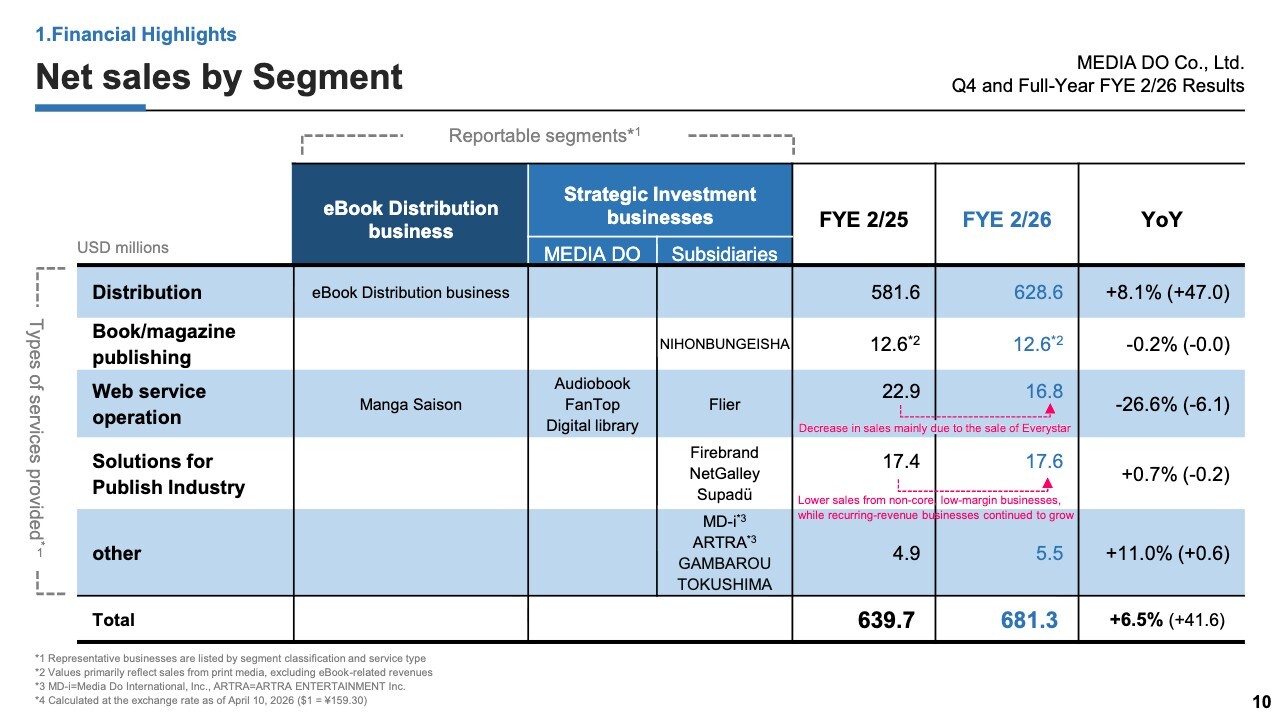

Net sales by Segment

Please refer to the slide for net sales by segment.

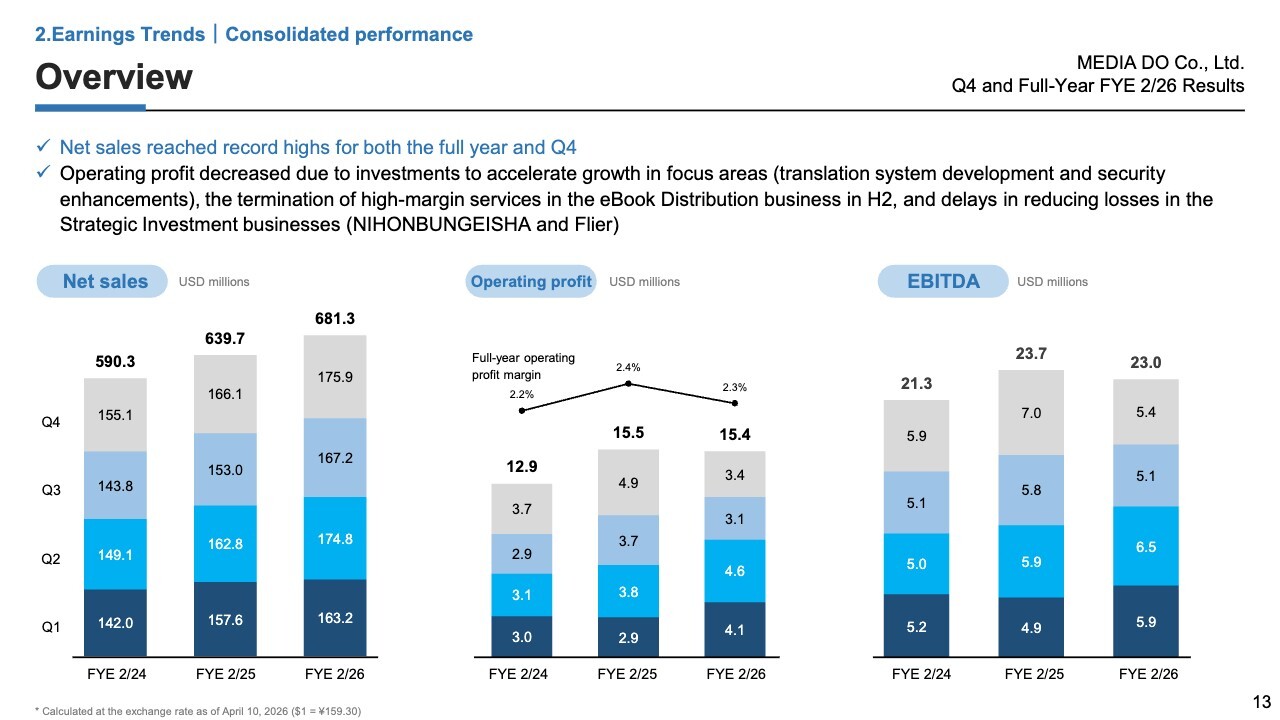

Overview

Now, I would like to talk about our earnings trends. First, let’s look at our consolidated performance. Net sales exceeded $175 million in Q4 alone, reaching record highs for both Q4 and the full year.

Operating profit decreased due to investments to accelerate growth in focus areas, such as translation system development and security enhancements; the termination of high-margin services in the eBook Distribution business in H2; and delays in reducing losses in the Strategic Investment businesses, also in H2.

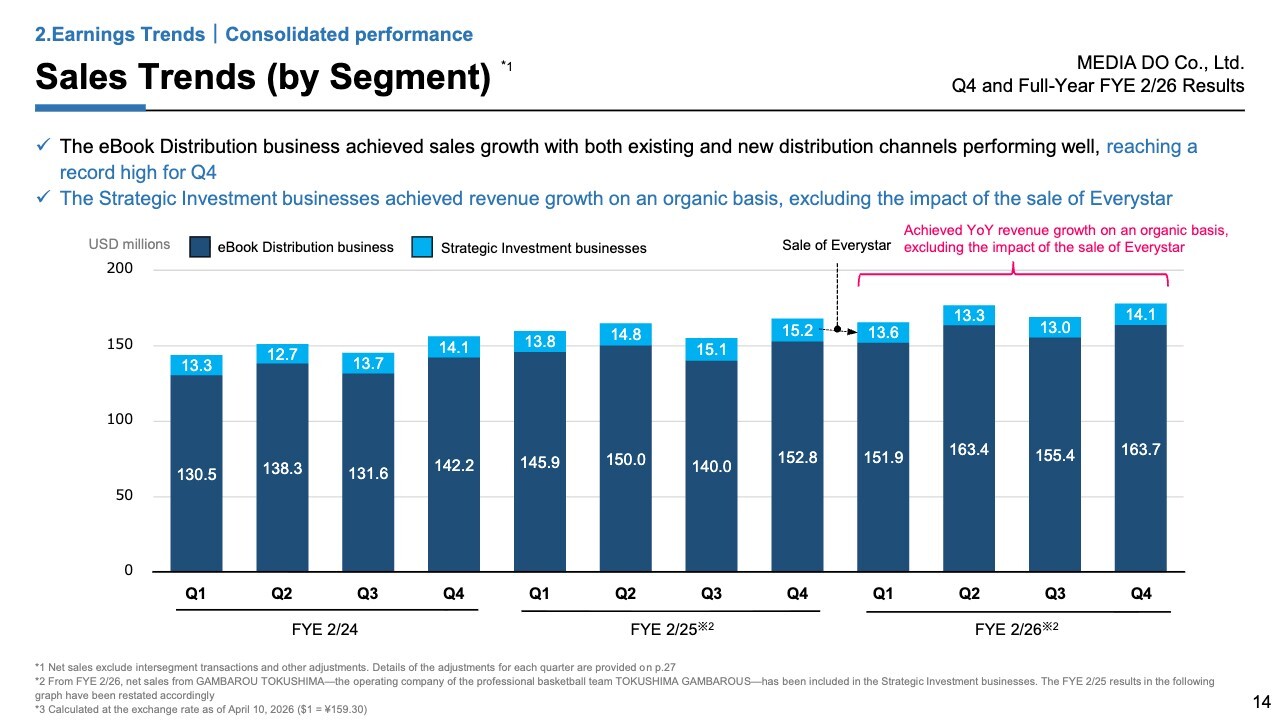

Sales Trends (by Segment)

Please refer to the slide for our sales trend.

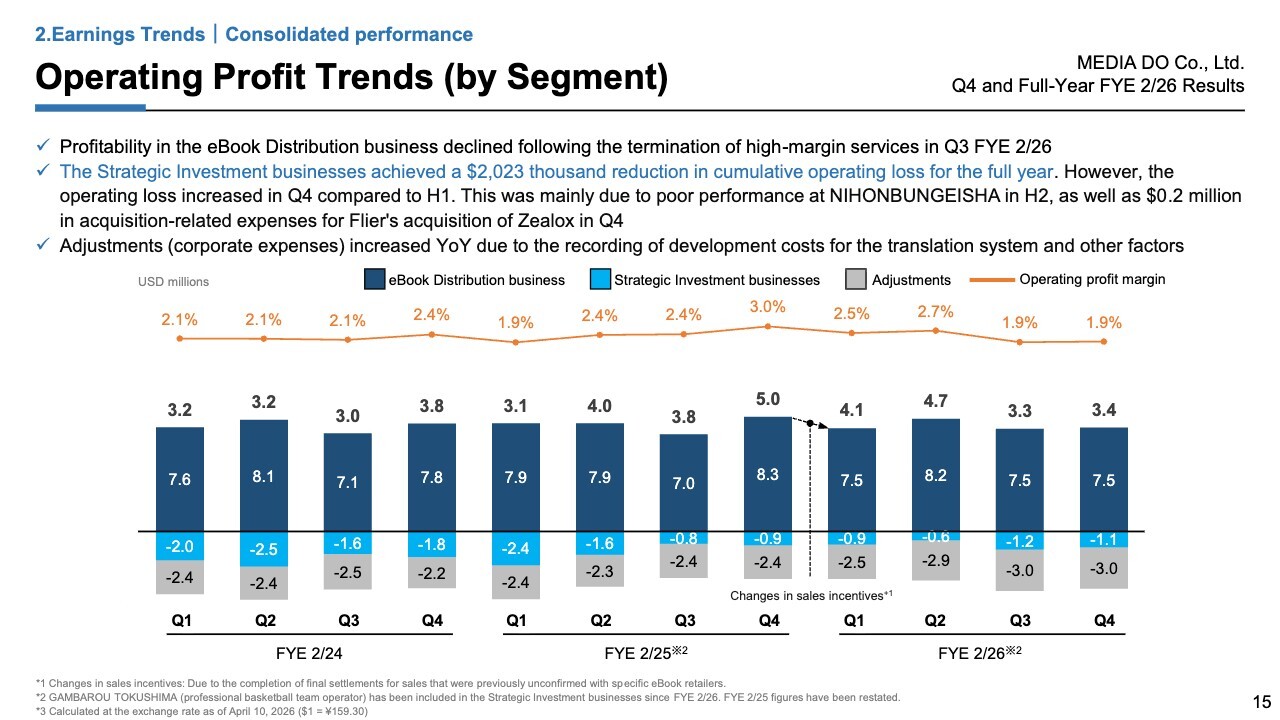

Operating Profit Trends (by Segment)

Now, turning to our operating profit trends. We will discuss the eBook Distribution business and the Strategic Investment businesses in more detail later in the presentation.

The gray portions at the bottom of the slide represent adjustments. Adjustments, including corporate expenses, increased YoY from Q2 onward due to the recording of development costs for the translation system and other factors.

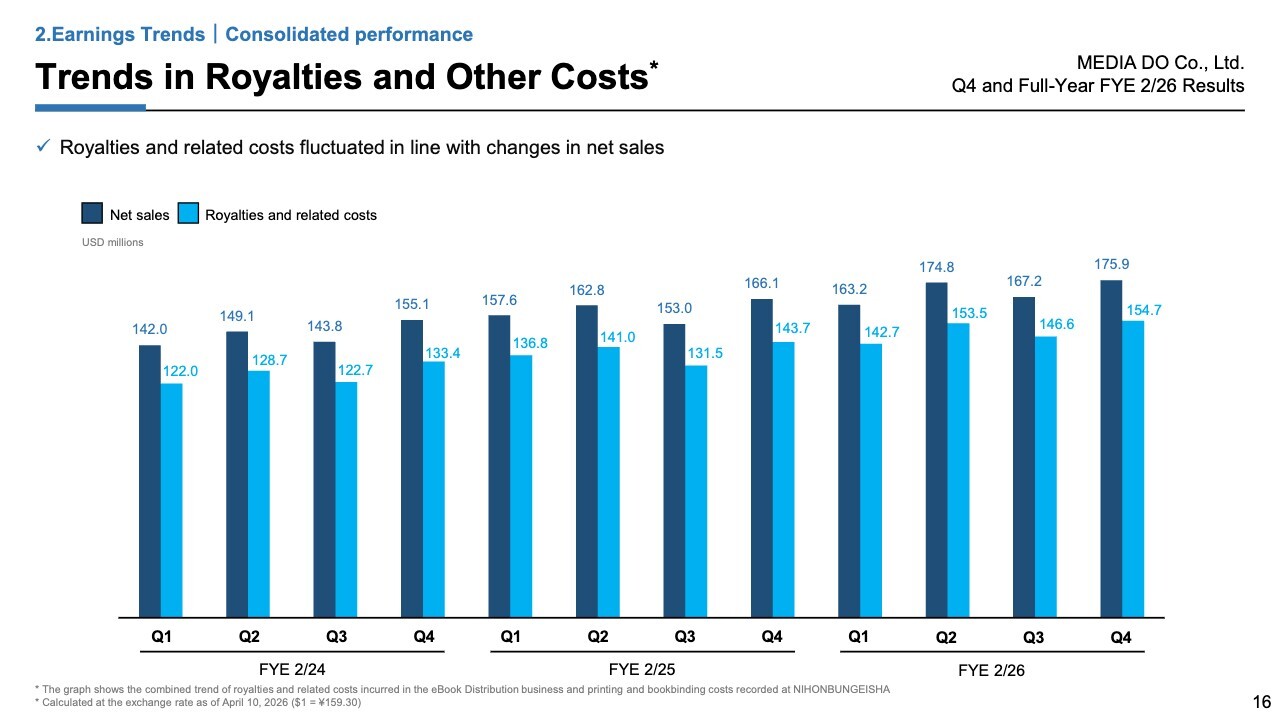

Trends in Royalties and Other Costs

Please refer to the slide for the trends in royalties and other costs.

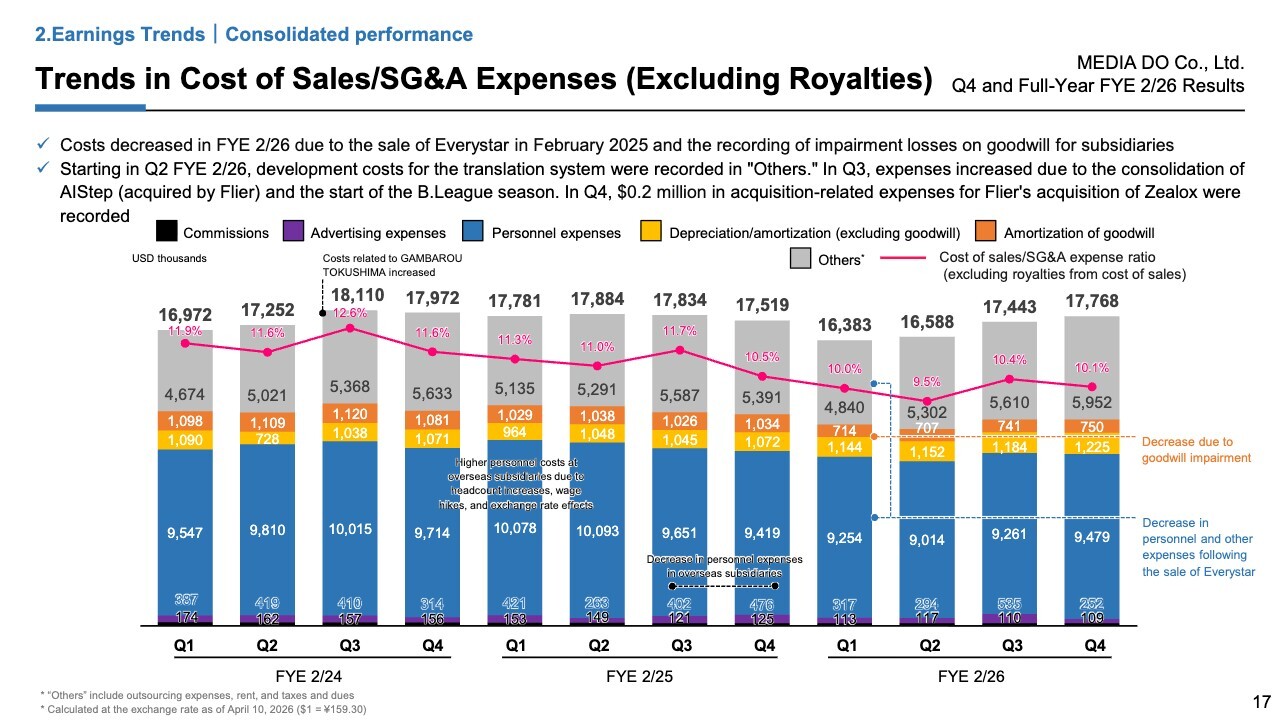

Trends in Cost of Sales/SG&A Expenses (Excluding Royalties)

Next, I would like to show you the trends in cost of sales and SG&A expenses. Costs decreased in Q1 FYE 2/26 due to the sale of Everystar in February 2025.

Starting in Q2 FYE 2/26, development costs for the translation system were recorded in “Others,” and in Q3, expenses increased due to the consolidation of AIStep, acquired by Flier, and the start of the B.League season.

In Q4, $0.2 million in acquisition-related expenses for our subsidiary Flier’s acquisition of Zealox were temporarily recorded, resulting in a YoY increase in expenses.

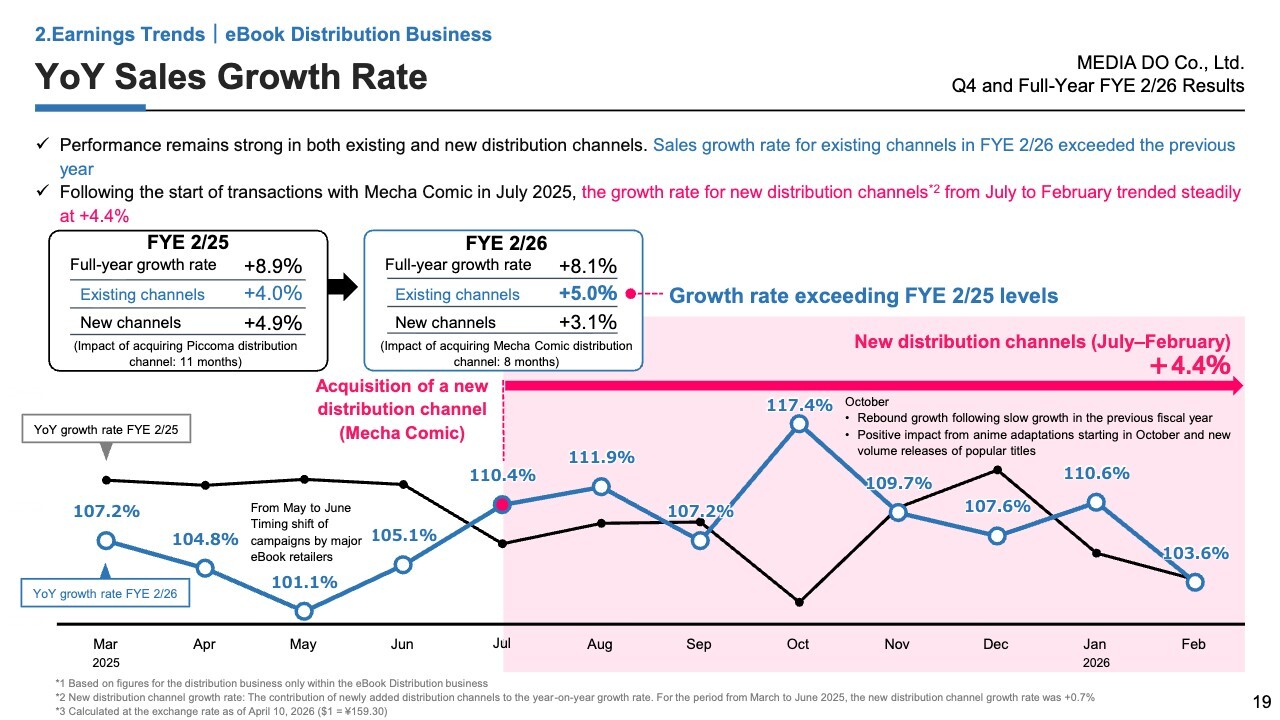

YoY Sales Growth Rate

Let me explain the YoY sales growth rate in our eBook Distribution business. The solid black line indicates the growth rate for FYE 2/25, and the solid blue line indicates the growth rate for FYE 2/26.

The full-year growth rate for FYE 2/26 is 8.1%, the breakdown of which is 5.0% for existing channels and 3.1% for new distribution channels. Especially in existing channels, growth accelerated from 4.0% in FYE 2/25 to 5.0% in FYE 2/26, achieving a growth rate exceeding that in FYE 2/25.

New distribution channels reflect the effect of new distribution channel of Mecha Comic acquired in July 2025. Incorporating the results for the eight-month period from July 2025 to February 2026 resulted in 3.1% growth.

At the start of FYE 2/26, we expected overall growth to be 4.0%, the breakdown of which is 3.0% for existing channels and 1.0% for new channels. Thankfully, both existing and new channels achieved growth exceeding our initial expectation.

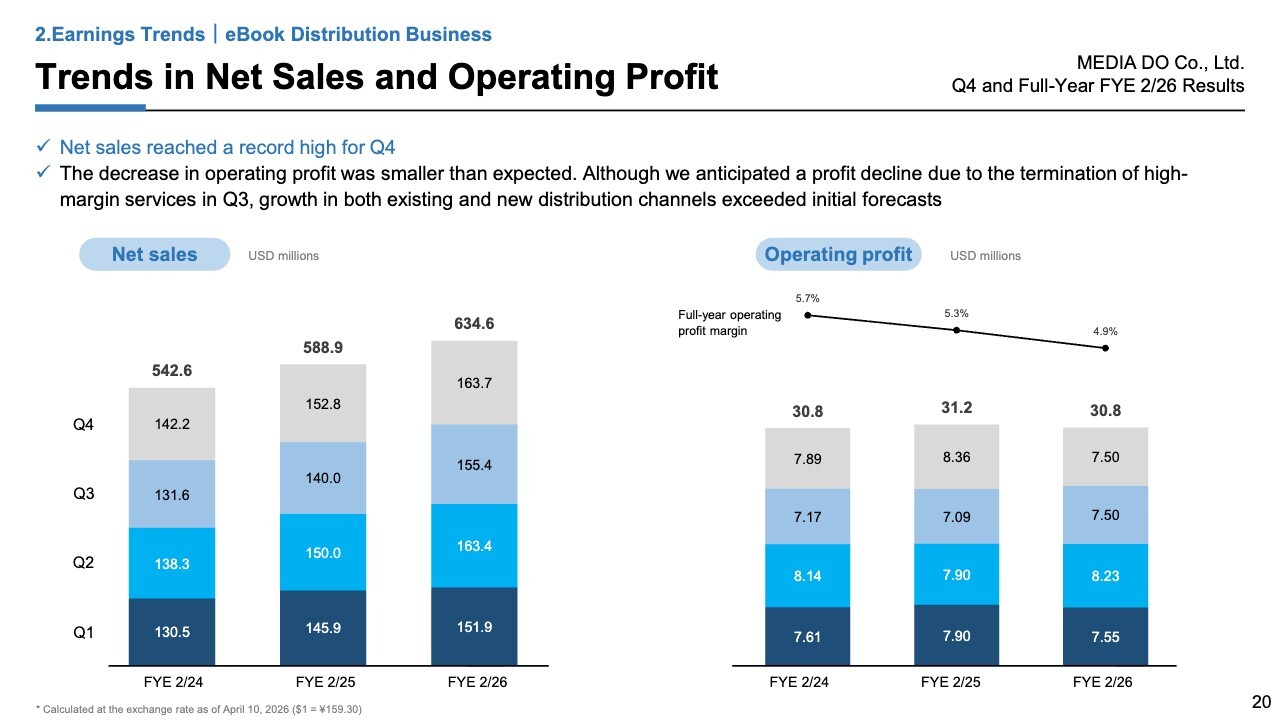

Trends in Net Sales and Operating Profit

As I mentioned earlier, net sales grew by 8%, but operating profit decreased. Nevertheless, the decrease in operating profit was smaller than expected since growth in both existing and new distribution channels exceeded initial forecasts, which initially assumed a profit decline.

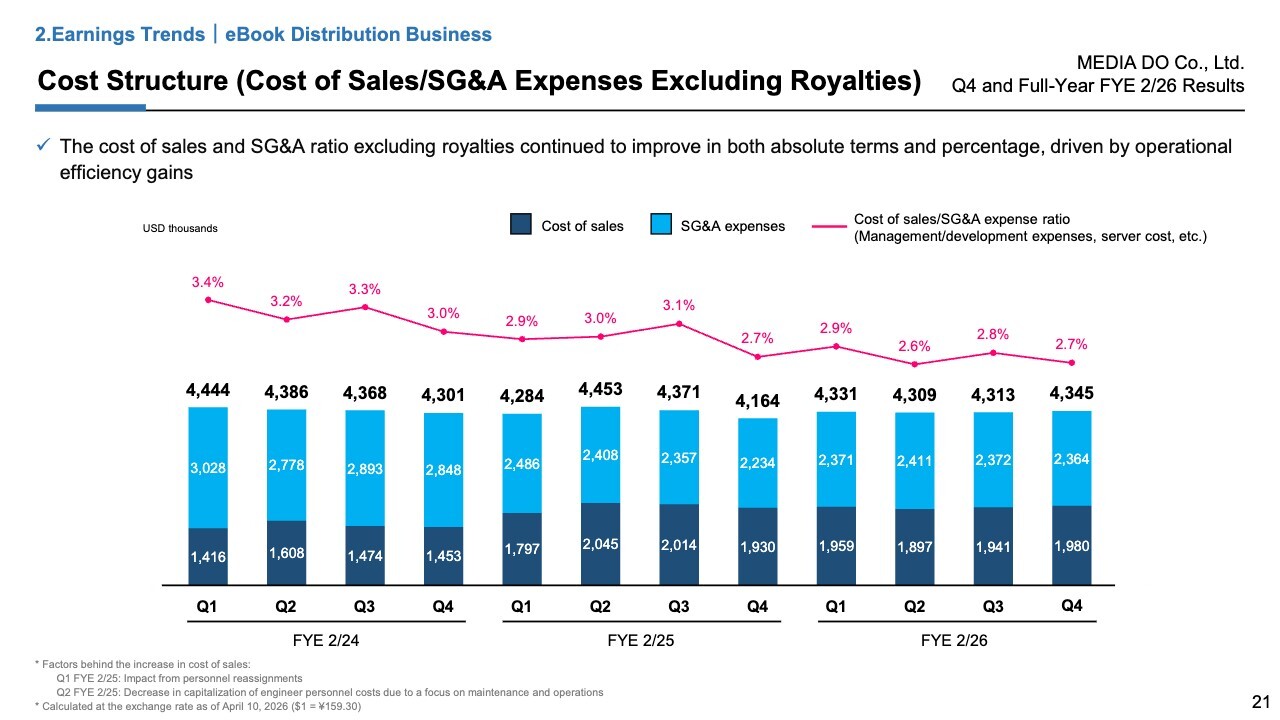

Cost Structure (Cost of Sales/SG&A Expenses Excluding Royalties)

Next, I will present our cost structure. Net sales are steadily increasing, and the number of titles in our catalog and the number of campaigns we handle have reached a massive scale.

At the same time, the cost of sales and SG&A expenses continued to improve in both absolute terms and percentage, driven by our continued efforts to achieve operational efficiency gains.

Overview of main service in the Strategic Investment Businesses

Now, I will explain our Strategic Investment businesses, which consists of three subsegments: Global business, IP Solution business, and SC business.

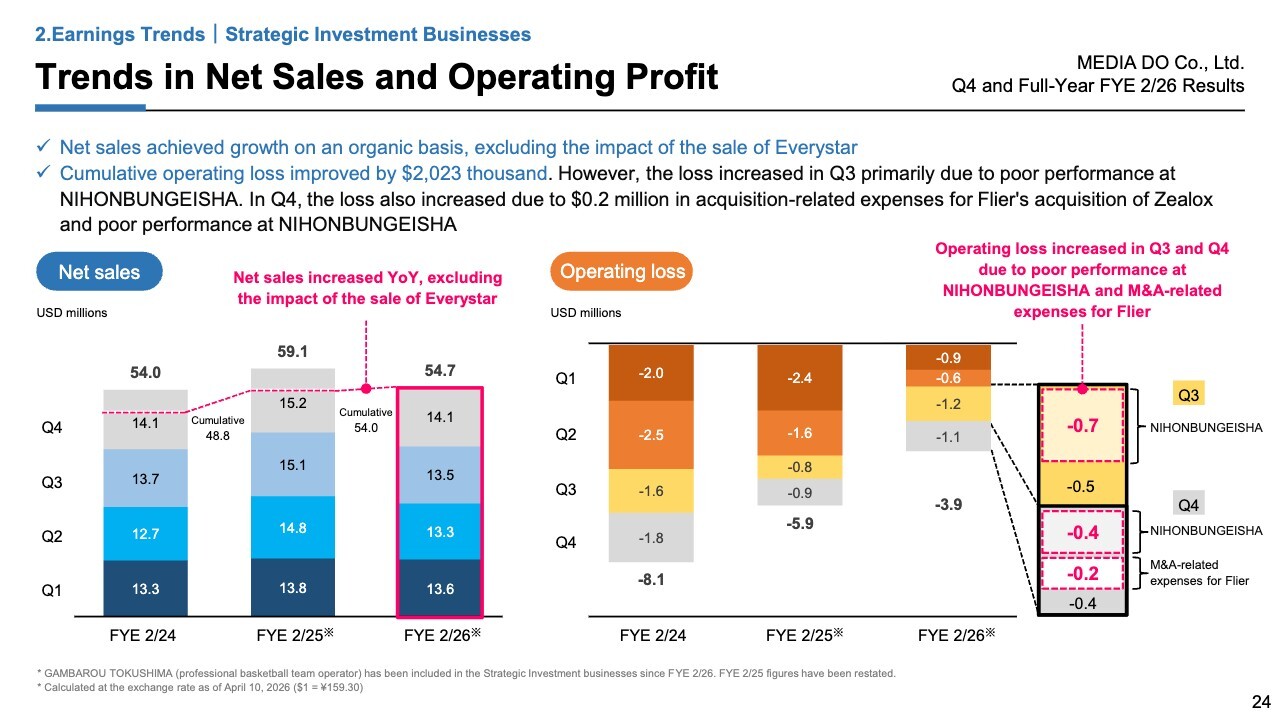

Trends in Net Sales and Operating Profit

Net sales achieved growth on an organic basis, excluding the impact of the sale of Everystar in February 2025, and cumulative operating loss improved by $2.0 million. Since we had projected an improvement in reducing operating loss of around $3.1 million at the start of the fiscal year, the actual result fell short of this projection.

Q1 and Q2 saw progress in improvements in the profitability of our Strategic Investment businesses. However, the loss increased in Q3 due to poor performance at NIHONBUNGEISHA. In Q4, the loss also increased due to a temporary recording of $0.2 million in acquisition expenses related to the Flier’s M&A, in addition to the poor performance at NIHONBUNGEISHA.

The right side of the slide provides a detailed breakdown of the losses for Q3 and Q4. In Q3, we recorded a loss of $1.2 million, of which NIHONBUNGEISHA accounted for $0.7 million.

In Q4, we recorded a loss of $1.1 million, of which NIHONBUNGEISHA accounted for $0.4 million, and Flier’s temporary acquisition expenses accounted for $0.2 million. Excluding these expenses, you can see that improvements in our other businesses are progressing steadily.

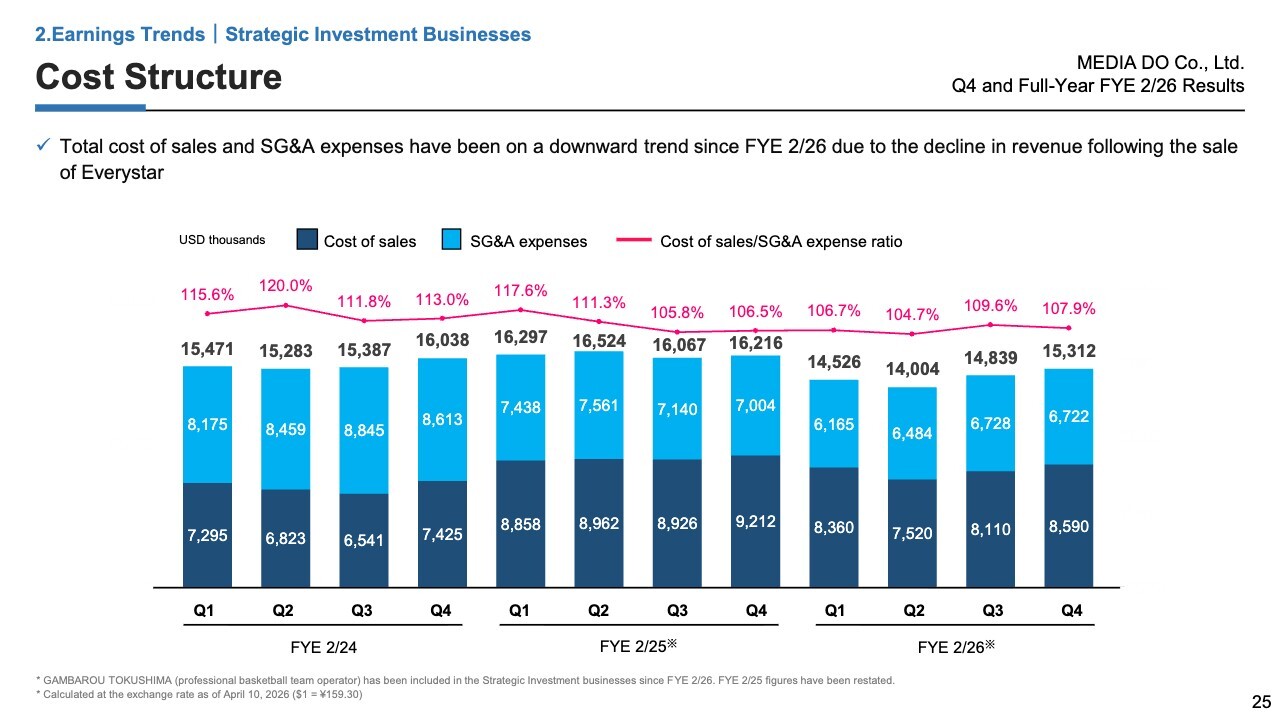

Cost Structure

Please refer to the slide for our cost structure.

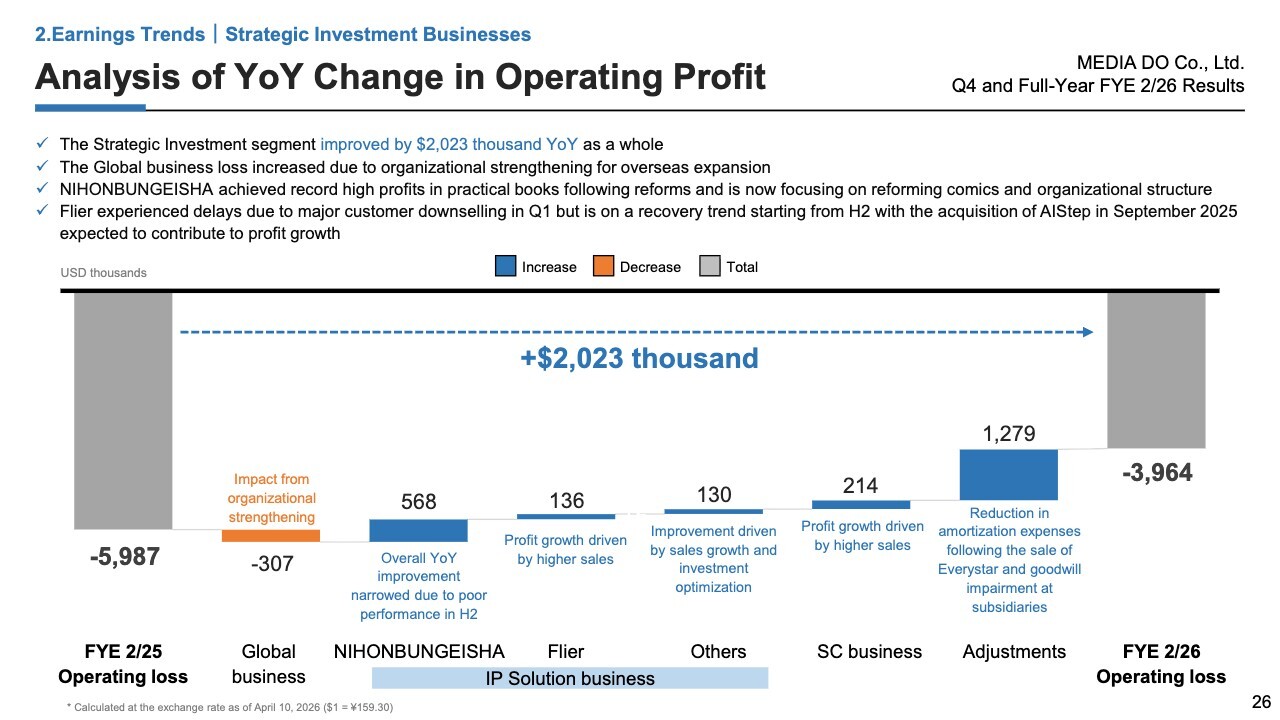

Analysis of YoY Change in Operating Profit

Now, let me address the analysis of YoY change in operating profit. Operating profit for the full-year FYE 2/25 was a loss of $5,987 thousand, whereas that for the full-year FYE 2/26 was a loss of $3,964 thousand, representing a YoY improvement of $2,023 thousand.

Looking at the breakdown by business segment, only the Global business saw a YoY decline due to organizational strengthening, while other businesses, including the IP Solution business, achieved steady improvements.

Operating profit of NIHONBUNGEISHA in the IP Solution business improved by $568 thousand YoY, but this improvement narrowed due to poor performance in H2. The reforms are progressing steadily, and profits in the practical books segment have reached a record-high level.

Since practical books are usually standalones, we can see the effect of improvement of measures relatively quickly; conversely, comics generally require multiple volumes to be published before the effect of measures become apparent. Hence, although we are focusing on improvements in the comics segment, some delays have occurred in certain areas.

For FYE 2/27, we intend to continue working on improvements in practical books as well as to further focus on reforming the comics department and organizational structure.

Flier experienced some delays due to major customer downselling in Q1 but achieved a YoY improvement of $136 thousand. Taking into account $257 thousand in M&A-related expenses mentioned earlier, we determine that we successfully improved operating profit by approximately $376 thousand for the full year on an organic basis.

Flier executed two M&A transactions in the previous fiscal year. In FYE 2/27, we will be able to reflect a full year of earnings from the acquired companies and are targeting a profit improvement of $439 thousand.

In the others of the IP Solution business and the SC business, operating profit improved YoY, driven by improved net sales and cost reforms, resulting in performance that exceeded the initial forecast.

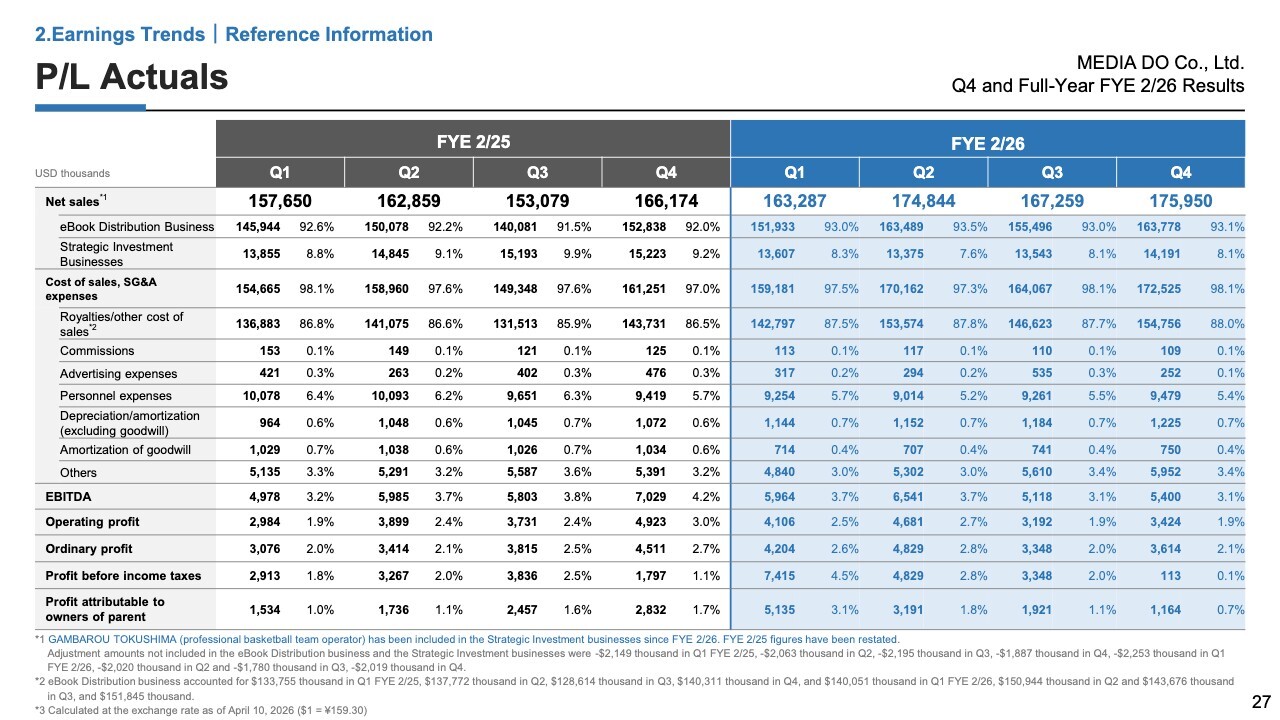

P/L Actuals

Please refer to the slide for the P/L actuals.

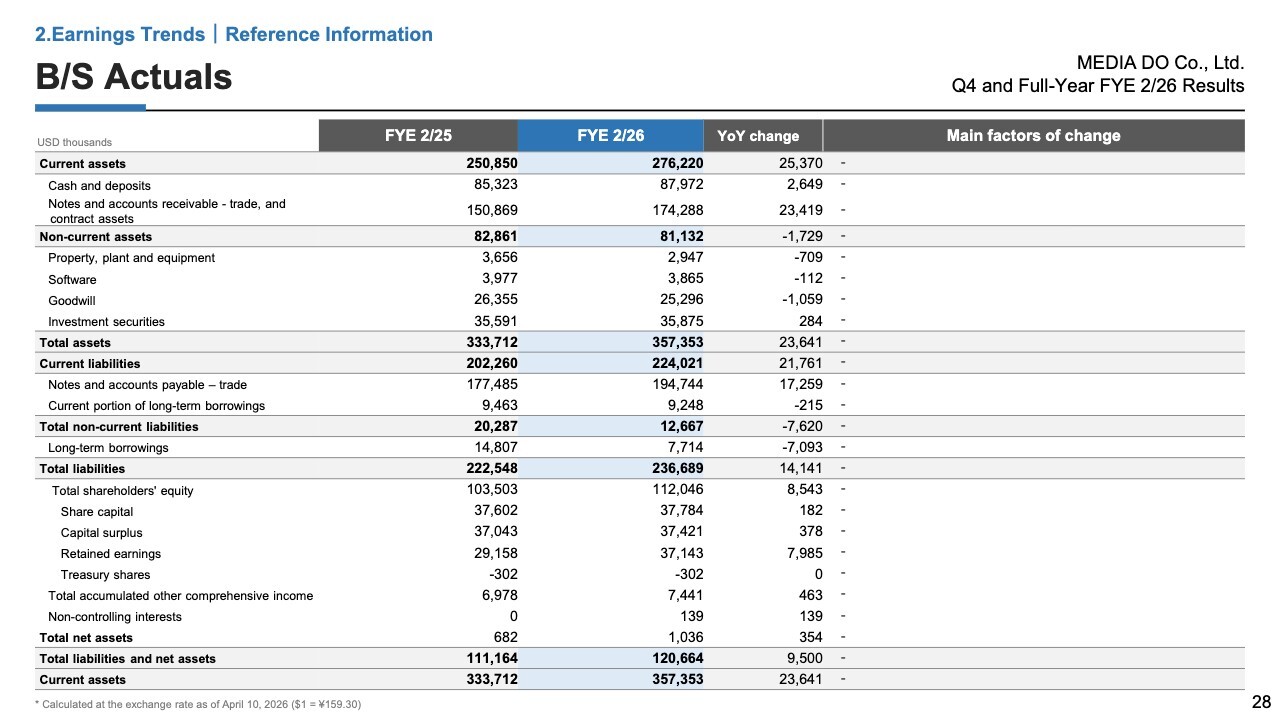

B/S Actuals

Please also refer to the slide for the B/S actuals.

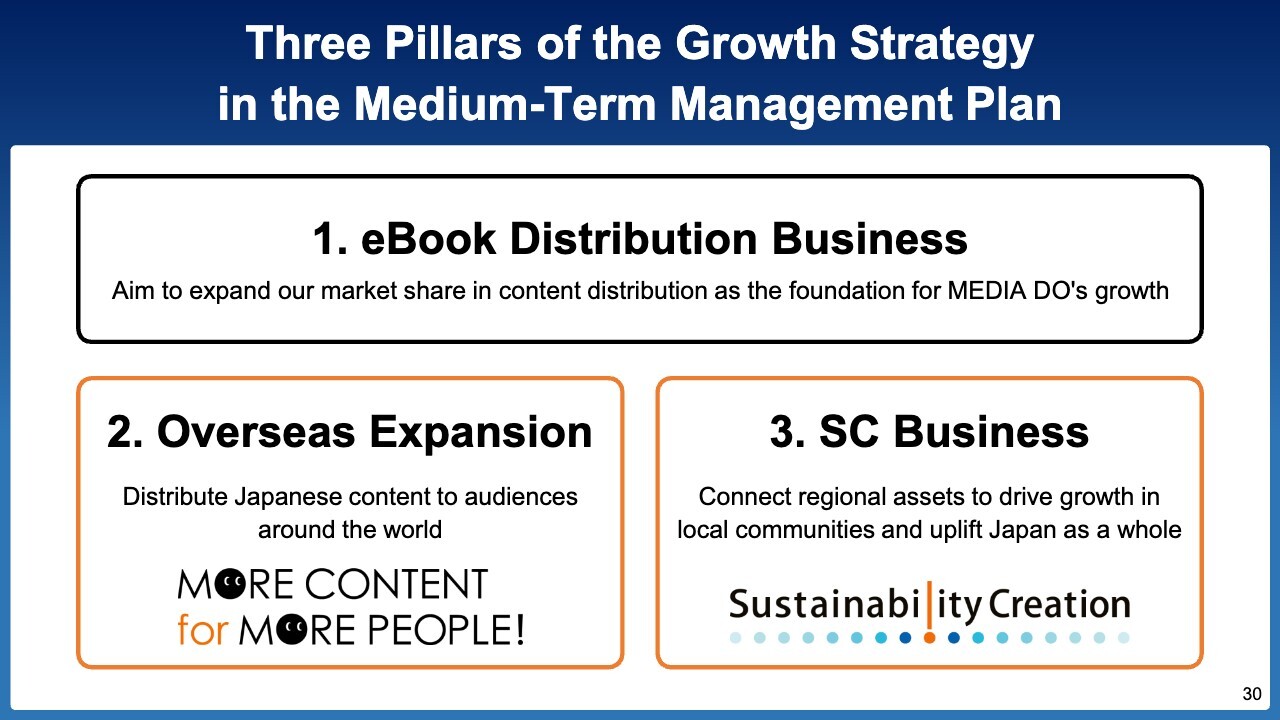

Three Pillars of the Growth Strategy in the Medium-Term Management Plan

I will now hand it over to Fujita, who will explain our growth strategy.

Yasushi Fujita (“Fujita”): Good afternoon, everyone. I am Fujita, President and CEO. I will explain our growth strategy. Last April, we announced our Medium-Term Management Plan. In the plan, we identified the three items shown on the slide as the pillars of our growth strategy.

First, to expand our position and market share in the domestic eBook Distribution business; second, how to expand Japanese content overseas in our overseas expansion; and third, to make a full-scale entry into the SC business, a regional revitalization business.

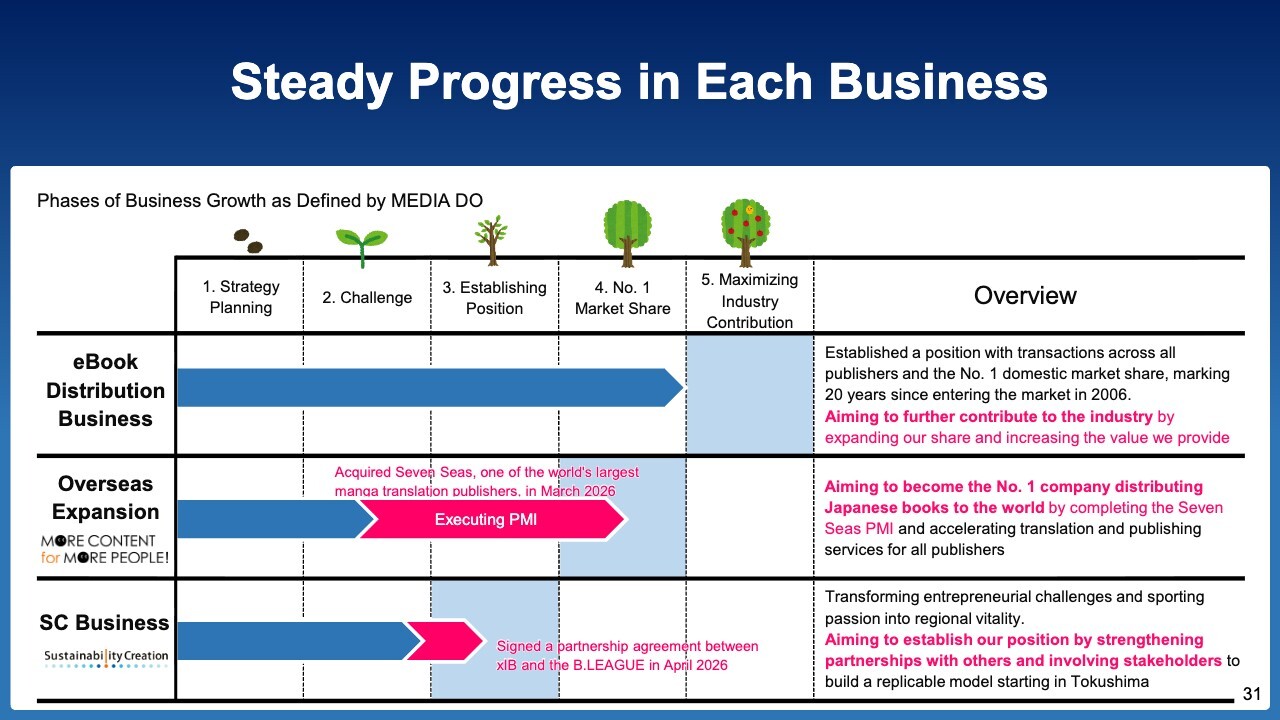

Steady Progress in Each Business

I believe we have made solid progress on each of these three pillars of our growth strategy over the past year.

In the eBook Distribution business, we believe we are moving closer to the “Maximizing Industry Contribution” phase by continuing to further solidify our No. 1 position. Our current challenge is determining how to move on to the next stage from our position as the market leader.

For overseas expansion, we will first strengthen the distribution of Japanese content in the U.S. As a company that handles eBooks, we will need expertise in distribution and printing as we expand into print books in addition to eBooks.

Efforts to publish Japanese books overseas have primarily been supported by the four major publishers. Other publishers had previously been unable to establish their own distribution networks, but our efforts to build a proprietary distribution network for print publications that non-major publishers can also use have expanded significantly.

We have acquired Seven Seas, the company that translates, distributes, and sells the largest number of Japanese books worldwide. We will advance PMI going forward, thereby aiming to establish the MEDIA DO Group’s solid position corresponding to that built by Seven Seas in the overseas manga market and expand our market share.

In the SC business, we are also steadily progressing in establishing our position.

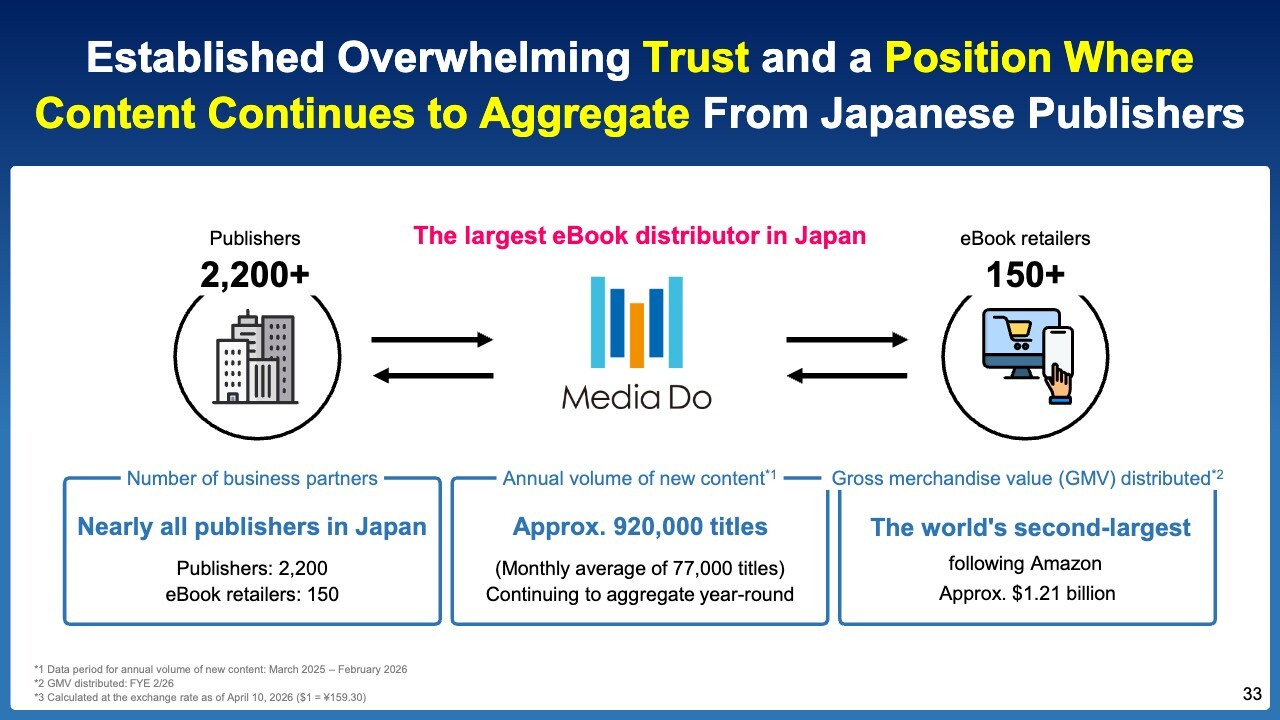

Established Overwhelming Trust and a Position Where Content Continues to Aggregate From Japanese Publishers

Then, let’s take a closer look at our first growth strategy related to the eBook Distribution business serving as the foundation of our operations. The actual value distributed in the previous fiscal year reached $1.21 billion.

We have been adding 77,000 new titles per month on average, and over the past year, we were entrusted with approximately 920,000 new titles from various publishers. We believe no other company can be entrusted with such a large volume of books in a single year. In this regard, we have proven ourselves to be No. 1 in both name and reality.

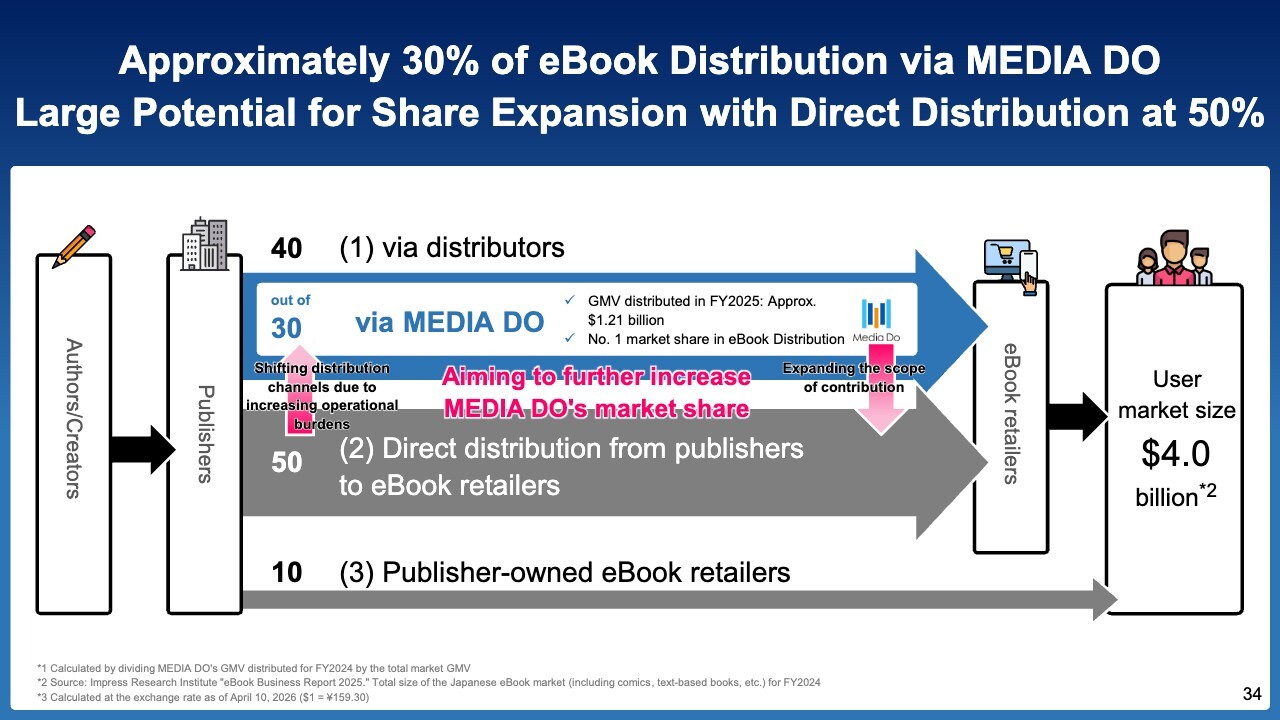

Approximately 30% of eBook Distribution via MEDIA DO Large Potential for Share Expansion with Direct Distribution at 50%

Having referred to our performance for the current fiscal year so far, you may feel that there are some areas where you have not yet seen significant growth.

Japan’s population is declining nationwide, and most people now read eBooks as approximately 20 years having passed since the dawn of the eBook distribution industry Amid this situation, we believe it is vital to leverage our current position and market share to expand Japanese books globally with the aim of finding a way to further drive our growth.

On the other hand, if MEDIA DO handles 100% of domestic eBook distribution, we can assume that our performance would move in perfect sync with declining population and eBook market trends. However, in reality, the distribution channels we manage account for only about 30% of the overall market. That is precisely why we must leverage our No. 1 position and develop distinctive strategies for the market leader.

Specifically, the key lies in how we can capture the remaining 70% of the market share. We believe there are two main directions we should pursue.

The first is to achieve this through our proposals. Essentially, we aim to create an environment where publishers and eBook retailers handling distribution directly will say, “We’ll entrust our content collectively to MEDIA DO.”

One point to note here is that we will fall behind if we set up the environment only after receiving an order. Therefore, we believe it is necessary for us to proactively build our operating structure.

On that basis, our challenge is to create an environment where clients feel, “Given that you have already established such a solid operating structure, we would like to entrust our content as a whole to you.” I believe this is the path to transitioning from the “No. 1 Market Share” phase, as mentioned at the beginning, to the “Maximizing Industry Contribution” phase.

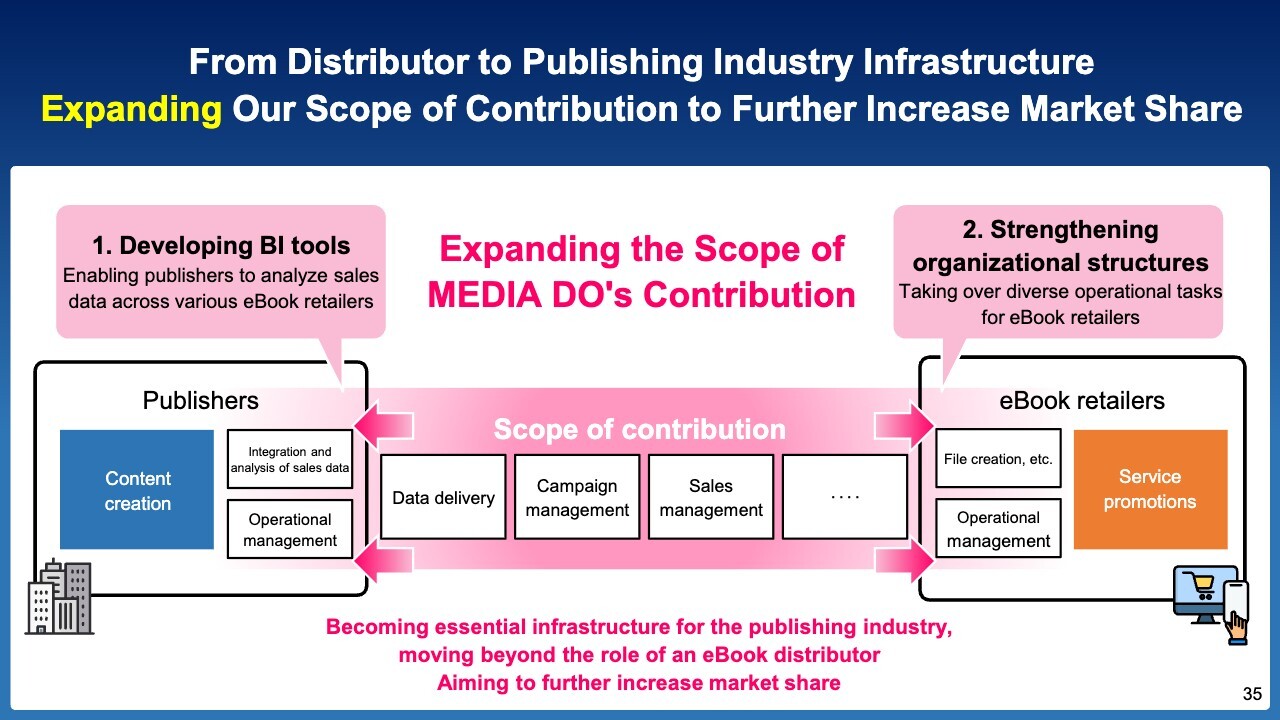

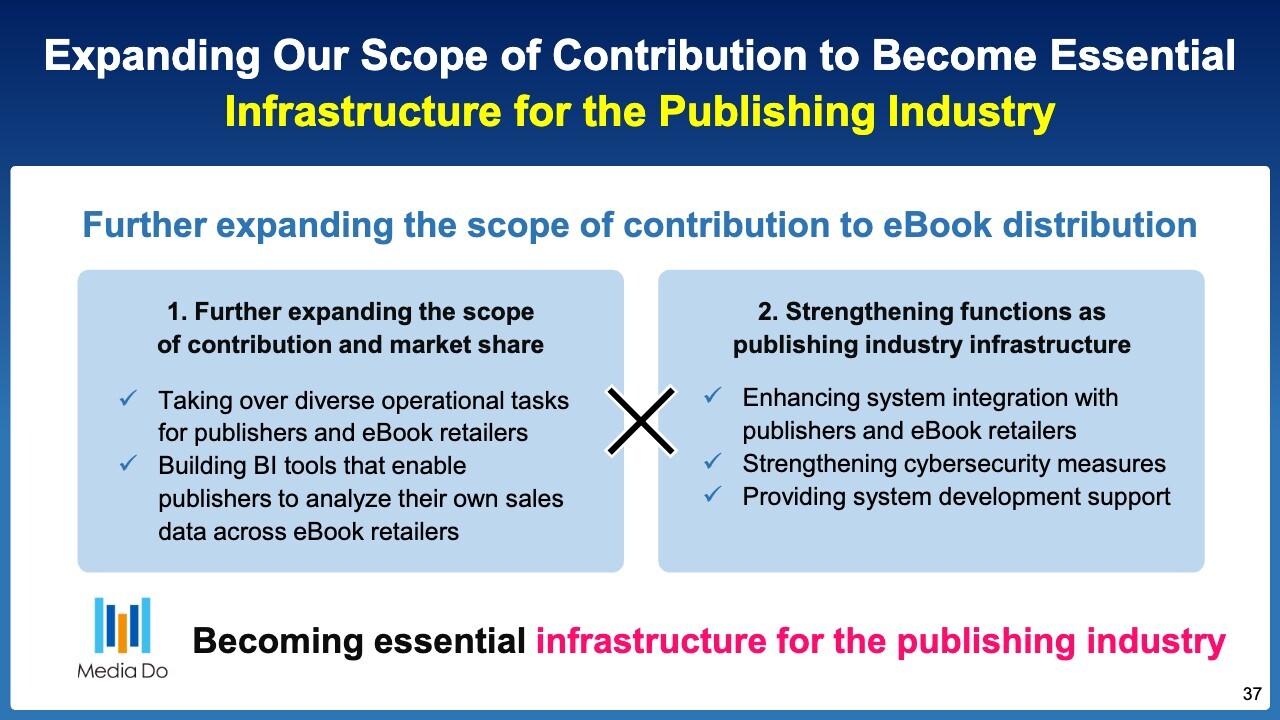

From Distributor to Publishing Industry Infrastructure Expanding Our Scope of Contribution to Further Increase Market Share

I understand that the structures we need to put in place differ slightly between publishers and eBook retailers.

I believe that providing BI tools for analyzing sales data at individual retailers is of the utmost importance for publishers.

When it comes to eBook retailers, annual and monthly promotions are becoming increasingly complicated. With print books, the number of events is relatively fixed.

For print books, Japan has a resale price maintenance system, which requires, for example, that a book priced at ¥1,000 be sold for ¥1,000 everywhere. For eBooks, however, various campaigns are available, such as selling a book that would normally be priced at ¥1,000 for ¥500 during a given month or offering three volumes for the price of one.

Since the number of such promotions at our company alone reaches 20,000 per year, the work involved is far more cumbersome and complex than with print books. Furthermore, it is difficult to organize structures for each eBook retailer. We will help them redirect the costs associated with building such systems toward marketing expenses, while we consolidate the necessary human resources for these promotions and establish a system to provide comprehensive support to publishers and eBook retailers.

Essentially, by strengthening our system investments and organizational structure, we aim to make clients feel confident enough to say, “Given that you have already established such a solid structure, we would like to leave the complicated details you.”

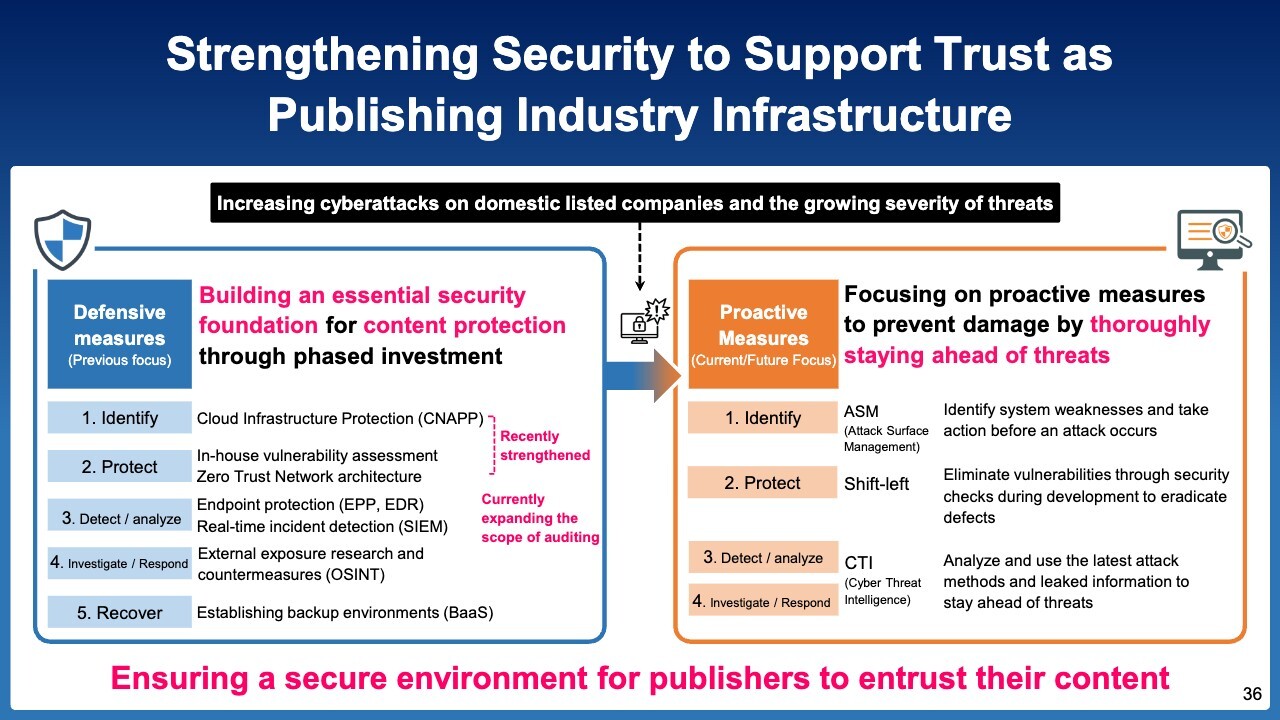

Strengthening Security to Support Trust as Publishing Industry Infrastructure

To maintain the trust placed in us as the backbone of the publishing industry, we must prioritize our efforts to prevent cyberattacks. While we have faced hacking attempts almost daily, we have responded effectively each time and have never experienced a single instance of content leakage.

However, we anticipate that various cyberattacks techniques, including the use of AI, will emerge in the future. In such a situation, we believe that if other companies implement 100 countermeasures, our clients will feel more confident entrusting us with their security if we can establish a system comprising around 200 measures, including those that address future threats.

Until now, we have focused primarily on defensive measures, but going forward, we will thoroughly implement proactive security measures to stay ahead of threats. In particular, we will address new cyberattacks techniques that have not yet been seen in Japan.

We will continue to contribute to the industry and expand our market share. Our current share is approximately 30%, and if we are able to exceed 50% in the future, we believe MEDIA DO will be widely recognized globally as the company that holds Japanese content.

We recognize that investing in measures to prevent a cyberattack before it occurs is our top priority. We intend to significantly increase our investment in these measures, particularly starting this fiscal year.

Expanding Our Scope of Contribution to Become Essential Infrastructure for the Publishing Industry

To further expand our market share, we will broaden the scope of our contribution and enhance our service offerings and staffing structure so that members of the publishing industry will feel confident entrusting their direct distribution to MEDIA DO.

At the same time, as we strengthen our functions as industry infrastructure, we believe it is important to take proactive measures in anticipation of increasingly sophisticated cyberattacks, thereby providing our customers with greater peace of mind.

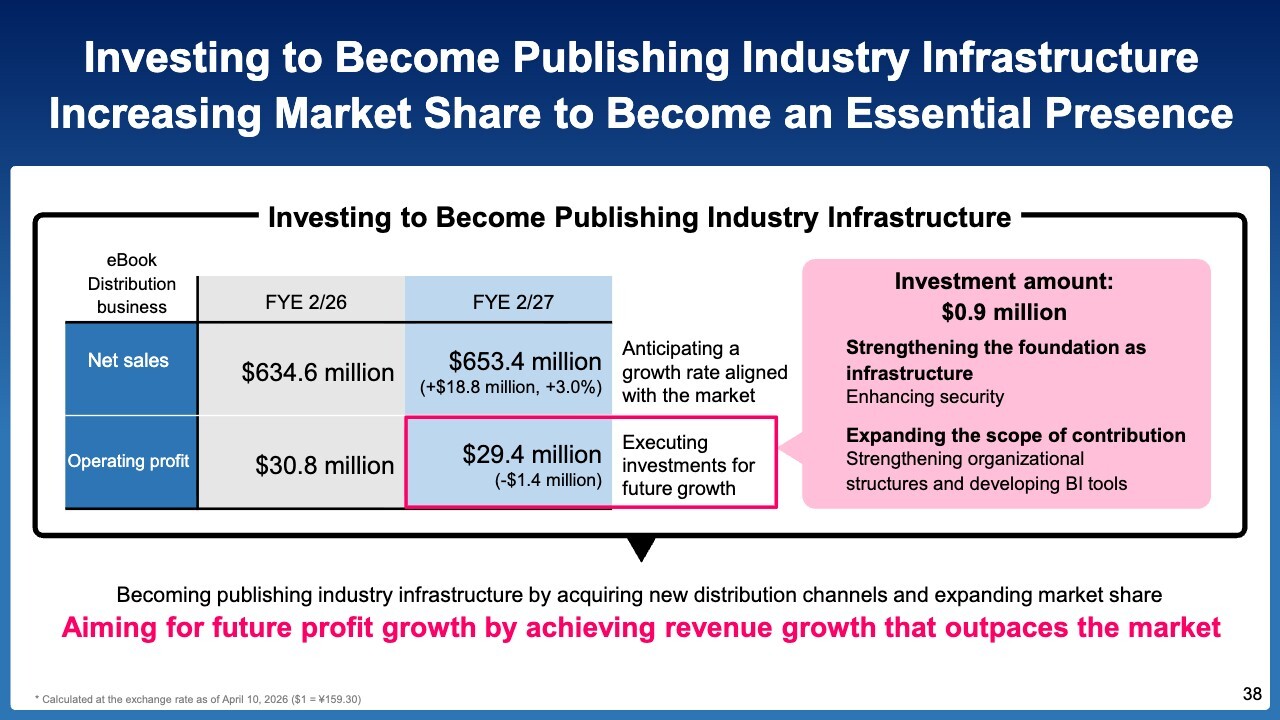

Investing to Become Publishing Industry Infrastructure Increasing Market Share to Become an Essential Presence

Operating profit for our eBook distribution business was $30.8 million last fiscal year, and we are projecting $29.4 million for this fiscal year, representing a decrease of $1.4 million. There are two factors contributing to this.

First, we will invest approximately $0.9 million in infrastructure to improve our operations. Second, contracts for high profit margin projects completed last year. As a result, our operating profits will decrease by a total of approximately $1.4 million.

However, our goal should not be to generate profits of $1 million, $2 million, or even $3 million, but rather to increase our current 30% market share to 51% or more. We believe this is the fundamental challenge we face.

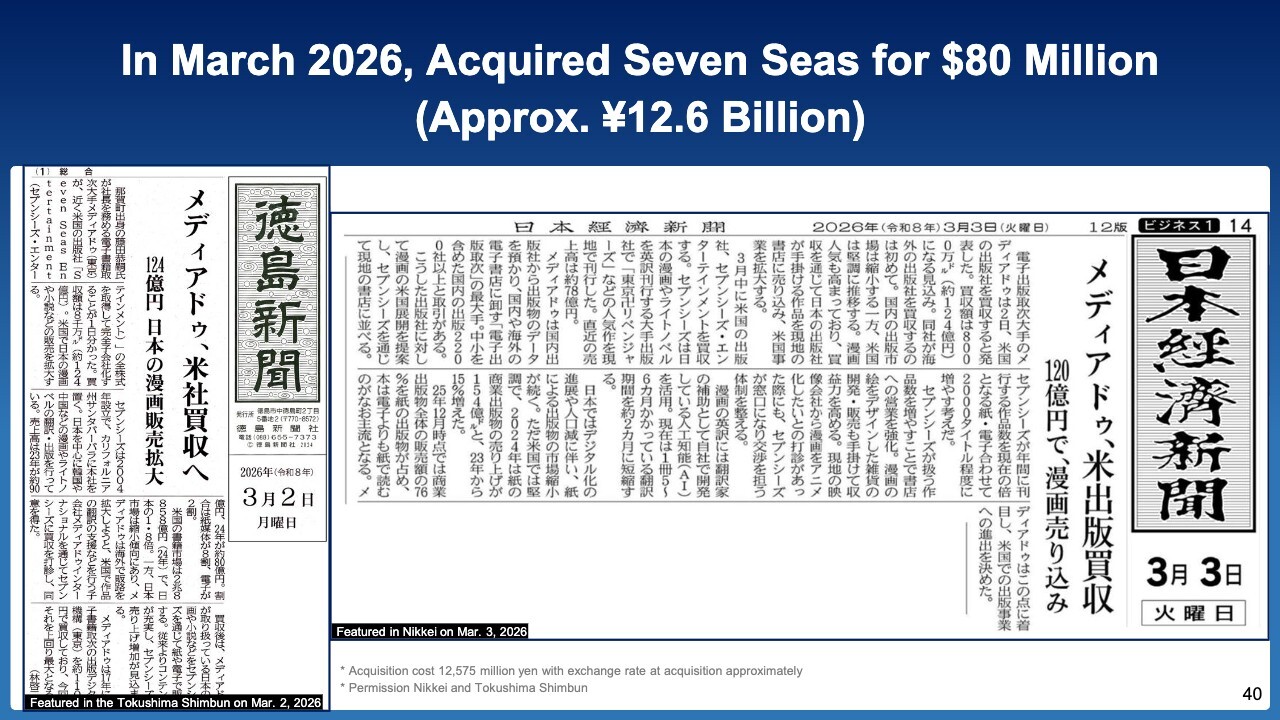

In March 2026, Acquired Seven Seas for $80 Million (Approx. ¥12.6 Billion)

I would like to talk about our global expansion. As I mentioned at the beginning, we acquired Seven Seas, a U.S.-based publisher that handles more Japanese manga than any other in the world, for $80 million (equivalent to approximately ¥12.6 billion)

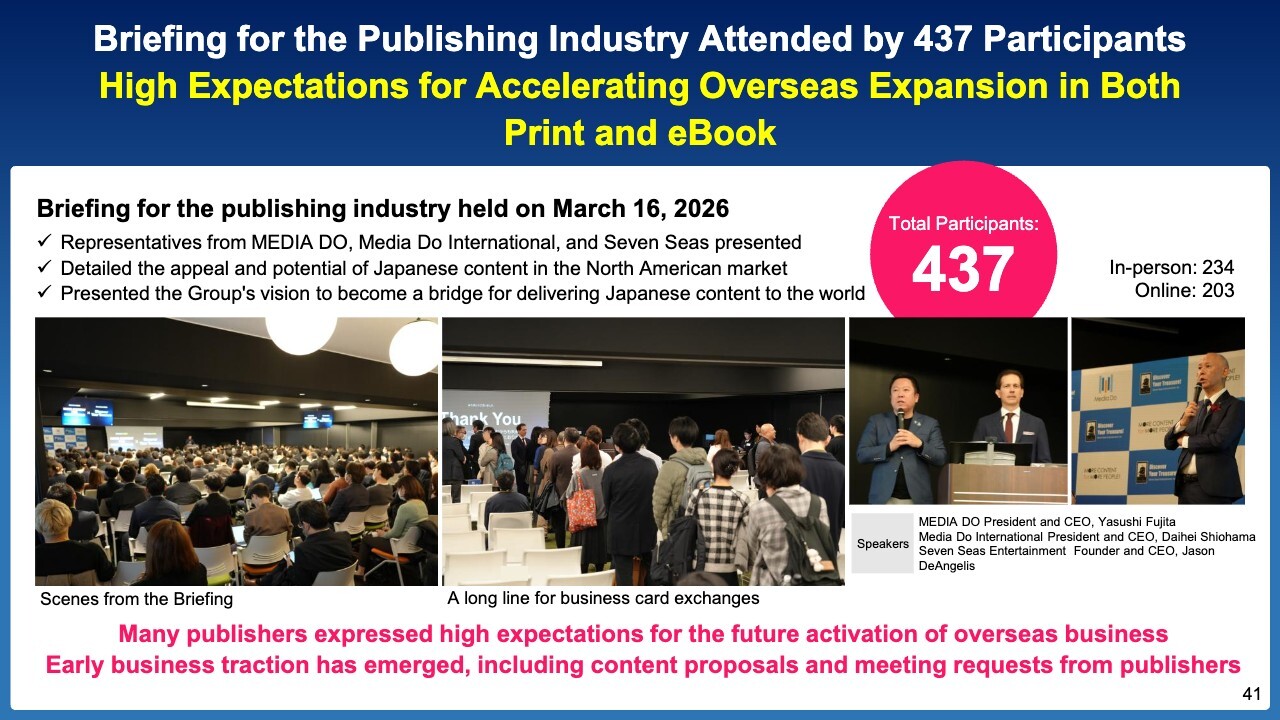

Briefing for the Publishing Industry Attended by 437 Participants High Expectations for Accelerating Overseas Expansion in Both Print and eBook

We announced the acquisition on March 2. Following the announcement, we received numerous inquiries from members of the publishing industry. As the response far exceeded our expectations, we quickly arranged for Jason, the former CEO and owner of Seven Seas, to come to Japan to hold a briefing session.

While representatives from financial institutions invited by our company were present at the briefing, 99% of the attendees were from the publishing industry. Since the venue could accommodate a maximum of approximately 230 people, the remaining attendees joined online. With over 200 participants joining online, a total of 437 people attended the session.

The photo on the left of the slide is the scene at that time. I would especially like you to take a look at the photo in the center, showing the line of people waiting to exchange business cards. So many people came to exchange cards that those at the back of the line had to wait for about an hour. As you can see, this acquisition had a significant impact on the publishing industry.

Currently, bookstores in Japan are facing tough times, and distribution and transportation costs for print books are on the rise. Against this backdrop, the question of how to expand the reach of Japanese books globally, beyond just eBooks, has become a challenge not just for individual publishers, but for the entire domestic publishing industry.

In this context, we believe that our acquisition of the world’s largest translation publisher specializing in Japanese books has garnered a great deal of interest from all.

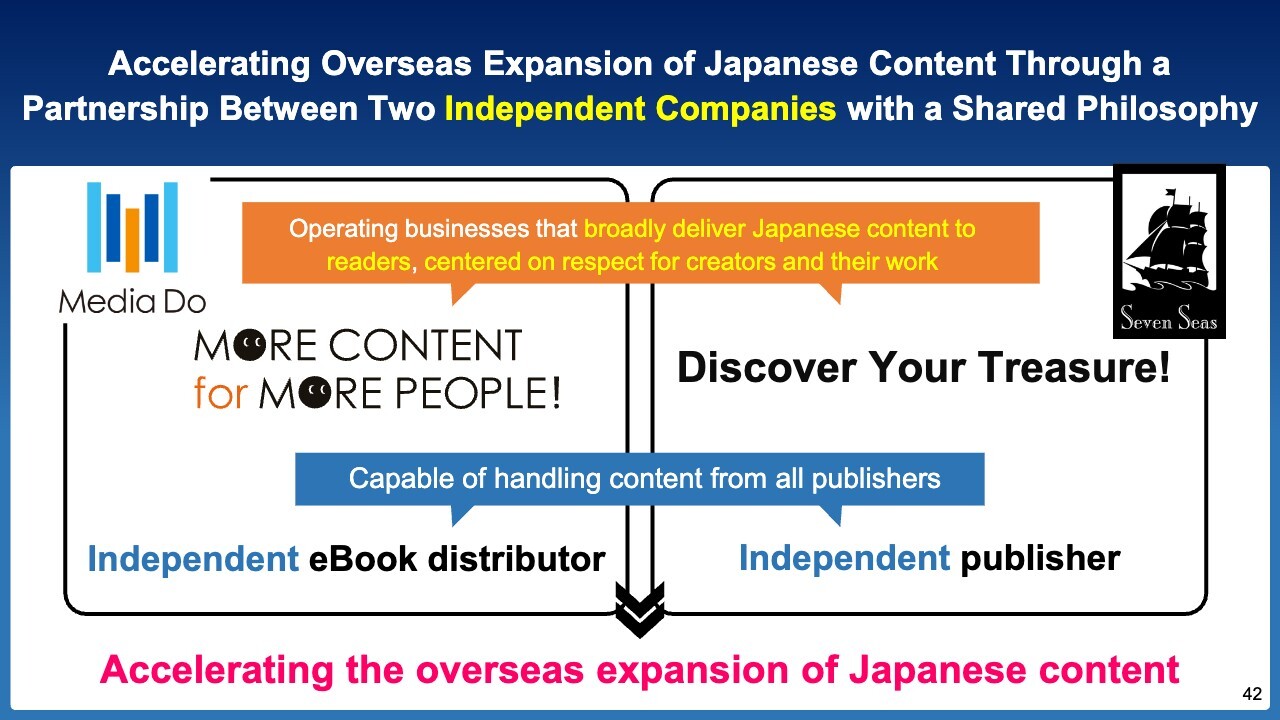

Accelerating Overseas Expansion of Japanese Content Through a Partnership Between Two Independent Companies with a Shared Philosophy

Let me explain why MEDIA DO was able to acquire this publisher. Given that it is a highly successful company generating approximately ¥1.6 billion in operating profit, it would seem there was no need to sell it.

However, from its perspective, it believed that forming a partnership with another company would be beneficial for future expansion, and several companies had made various proposals to Seven Seas.

One of the key reasons it chose our company is a phrase often used by the CEO, Jason: “MEDIA DO and Seven Seas are like Switzerland, perpetually neutral.” MEDIA DO is not a subsidiary of a major publishing house, and Seven Seas has also grown as a fully independent company, operating as a wholly owned entity.

The approaches to growing a business as an independent entity and growing it within a corporate group differ in every respect, starting with corporate culture. For this reason, even if it were to join a group, it apparently wanted to partner with a company that shares a similar corporate culture, rather than a major publishing house or trading company.

Furthermore, securing Japanese content will be crucial for its continued business growth. I first met with Jason last September, and we shook hands on the spot; in November, he visited Japan to negotiate the specific terms. Following approximately four months of negotiations between our respective legal teams, we reached an agreement and officially signed the contract on March 1.

I believe a key factor behind this extremely swift, lightning-fast acquisition was the fact that the two companies share very similar values.

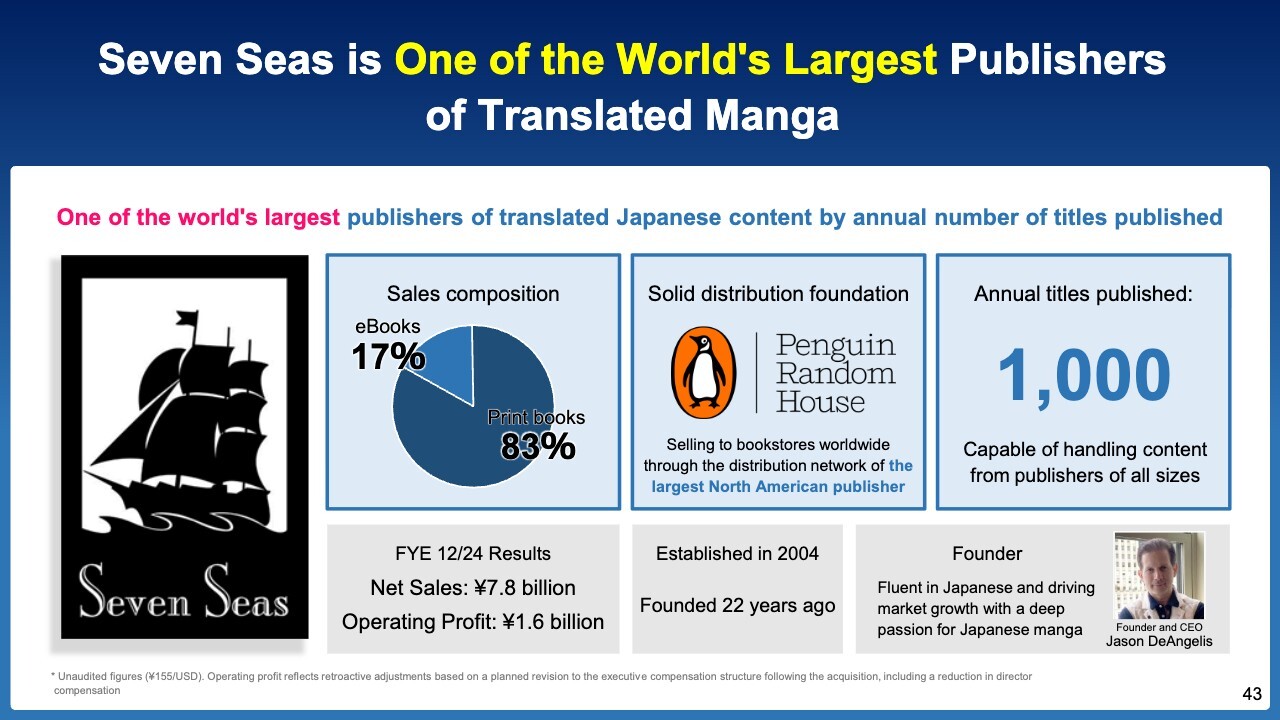

Seven Seas is One of the World’s Largest Publishers of Translated Manga

In FY24/12, Seven Seas reported net sales of ¥7.8 billion and operating profit of ¥1.6 billion. The company was founded in 2004 and has a 22-year track record.

The person in the bottom right corner of the slide is CEO Jason. He speaks Japanese fluently and has lived in Japan for six years. He has great respect for Japan and is a huge fan of Japanese works, including manga and novels.

The key point to note here is 1,000 titles on the far right of the slide. Seven Seas publishes 1,000 titles annually. Considering that even major publishers find it difficult to maintain a steady output of 1,000 titles each year, this is a truly remarkable achievement, and it demonstrates the company’s overwhelming publishing volume.

However, without readers and bookstores purchasing our books, neither sales nor publishing would be possible. Given the situation, the company’s ability to effectively distribute 1,000 titles with strong sales in the U.S. is, in my view, a major strength.

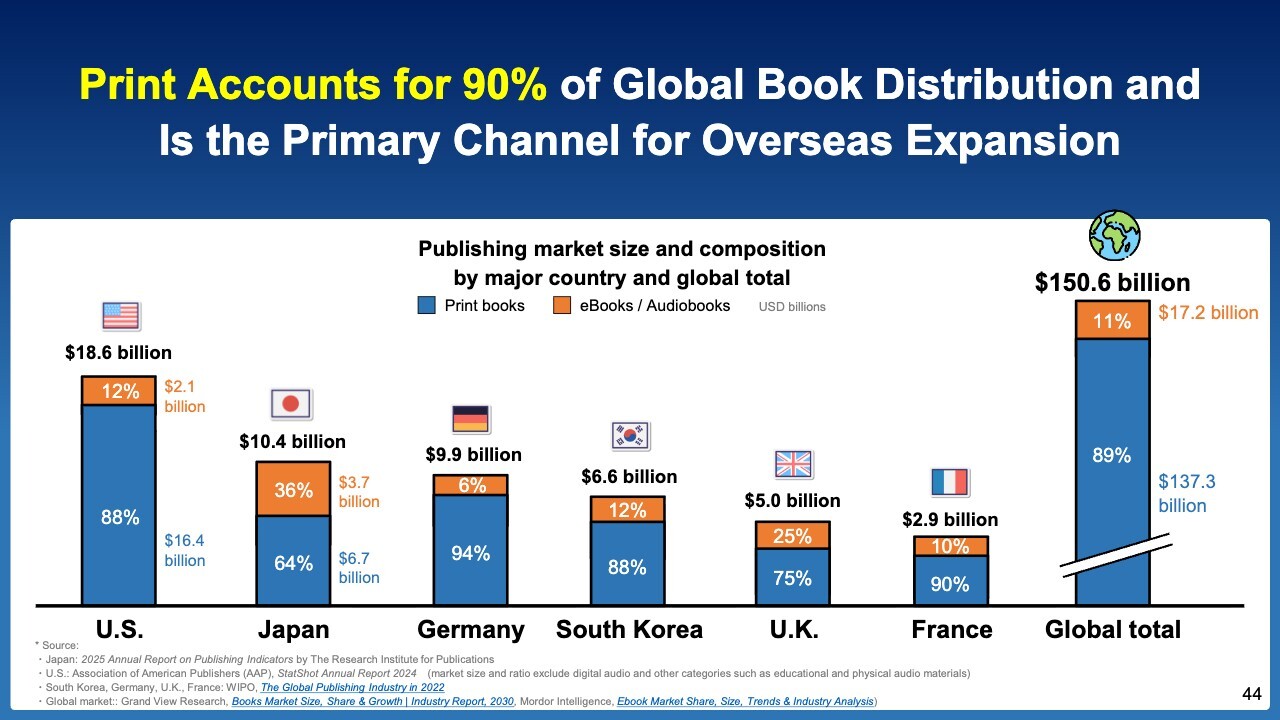

Print Accounts for 90% of Global Book Distribution and Is the Primary Channel for Overseas Expansion

There are two main channels for book distribution worldwide: print books and eBooks. In Japan, where manga accounts for a significant share of the market, eBooks make up 36% of the total.

However, in the U.S., eBooks, including audiobooks, account for only 12% of the market, with 88% still distributed in print. Globally, eBooks and audiobooks account for 11% of the market, while print accounts for 89%.

In other words, when bringing Japanese books to the global market, the key factor, aside from translation, of course, is whether they can be distributed in print.

Therefore, if our company were to launch Japanese books in the U.S. from scratch, acquiring a publisher with an established track record would be a far more rational strategy than starting a publisher from scratch and establishing new relationships with various bookstores.

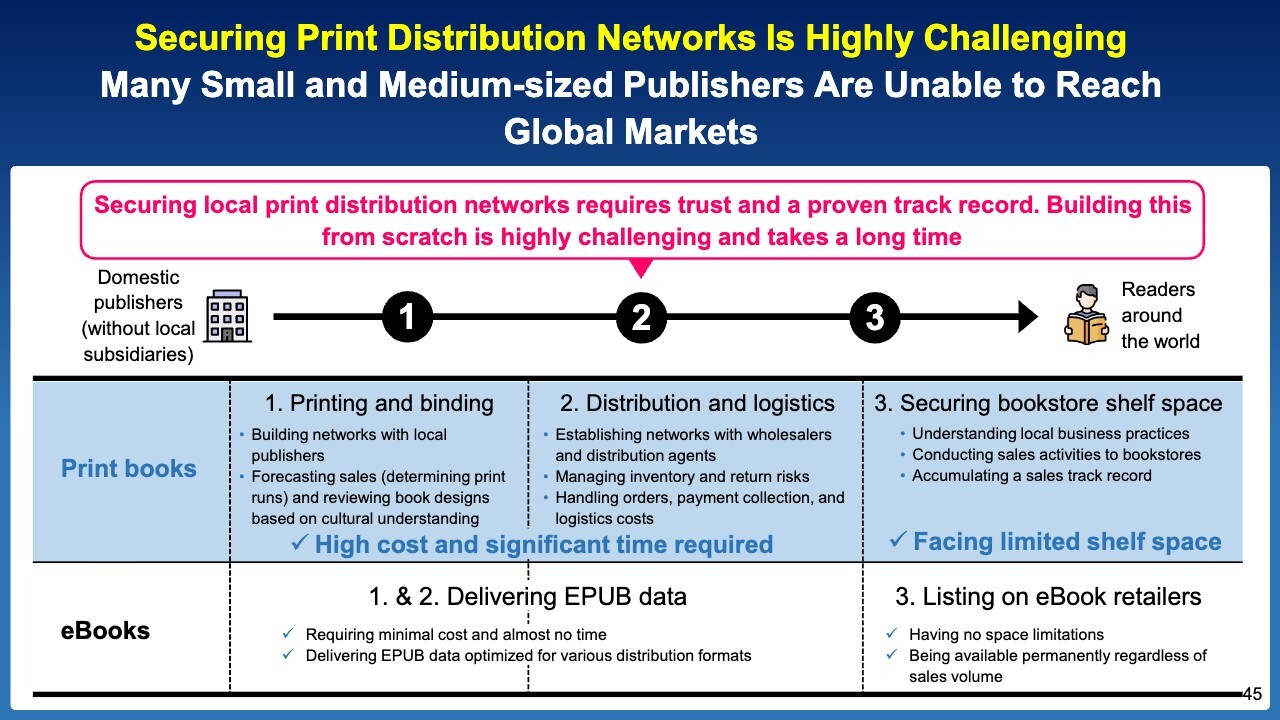

Securing Print Distribution Networks Is Highly Challenging Many Small and Medium-sized Publishers Are Unable to Reach Global Markets

This slide illustrates the distribution flow. The bottom section shows eBooks, while the top section shows print books. Compared to eBooks, the distribution of print books is significantly more complex and challenging.

For this reason, we believe that bringing Seven Seas, which already handles Japanese books and has an established distribution network, into the group was the best move to fulfill our mission of bringing Japanese content to the world.

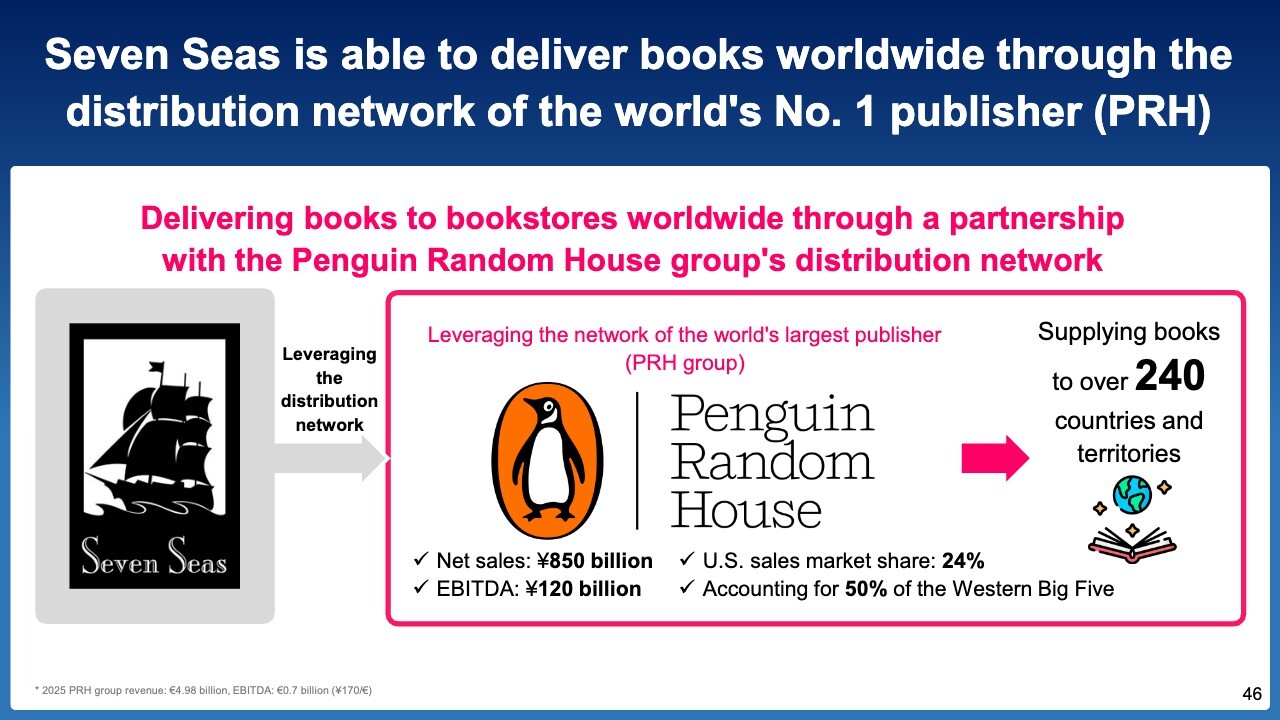

Seven Seas is able to deliver books worldwide through the distribution network of the world’s No. 1 publisher (PRH)

Seven Seas partners with Penguin Random House, the world’s largest publisher, to distribute books. Penguin Random House’s net sales stand at ¥850 billion, exceeding the combined sales of Japan’s big four publishers, while its EBITDA is ¥120 billion.

By publishing your book with Penguin Random House, you can distribute it not only in the U.S. but also in over 240 countries and territories worldwide.

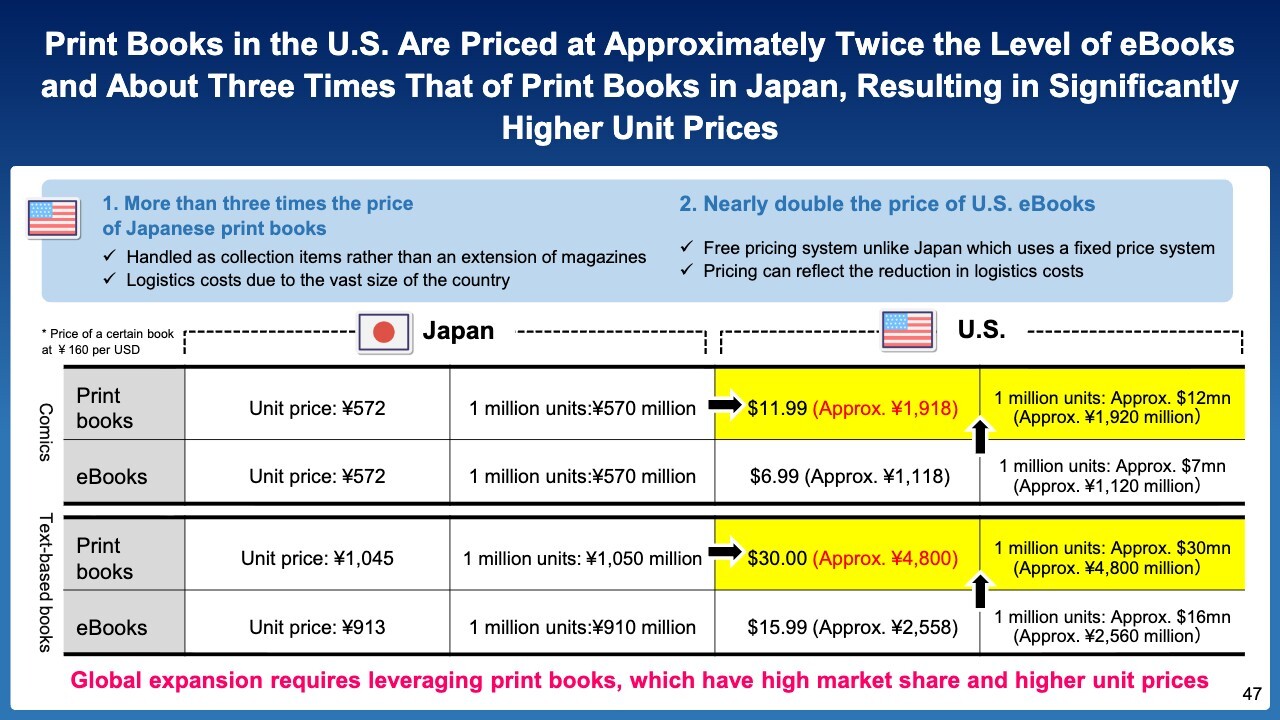

Print Books in the U.S. Are Priced at Approximately Twice the Level of eBooks and About Three Times That of Print Books in Japan, Resulting in Significantly Higher Unit Prices

As we work to bring Japanese content to the world, I imagine people might assume that, since we are an eBook company, we plan to compete internationally in the eBook market.

However, the purpose of this acquisition of Seven Seas is not to expand our eBook business. While we will certainly continue to develop our eBook offerings, we acquired the company specifically to expand our print book business. We carried out this acquisition with unwavering determination.

The reason isn’t just that 90% of the market consists of paper books or that it deals in Japanese books. It’s also because the unit prices of paper books and eBooks are vastly different, and because book prices in Japan and the U.S. are entirely different.

For example, the average price of a print comic book in Japan is about ¥572. If one million copies were sold, that would amount to approximately ¥570 million in sales.

In the U.S., the same book costs $11.99, or ¥1,918, so we can raise the price by about three times. If we sell one million copies, that amounts to ¥1.92 billion. Consequently, the amount we can return to the publisher will also be higher.

Prices for text-based books are even higher; while a print book in Japan costs 1,045 yen, the price in the U.S. is about 4.5 times that, $30, or ¥4,800. Therefore, if one million copies were sold, a title that would generate approximately ¥1 billion in Japan would generate about ¥5 billion in the U.S.

While we will certainly be focusing on the eBook market as well, we believe that print will be our main target overseas.

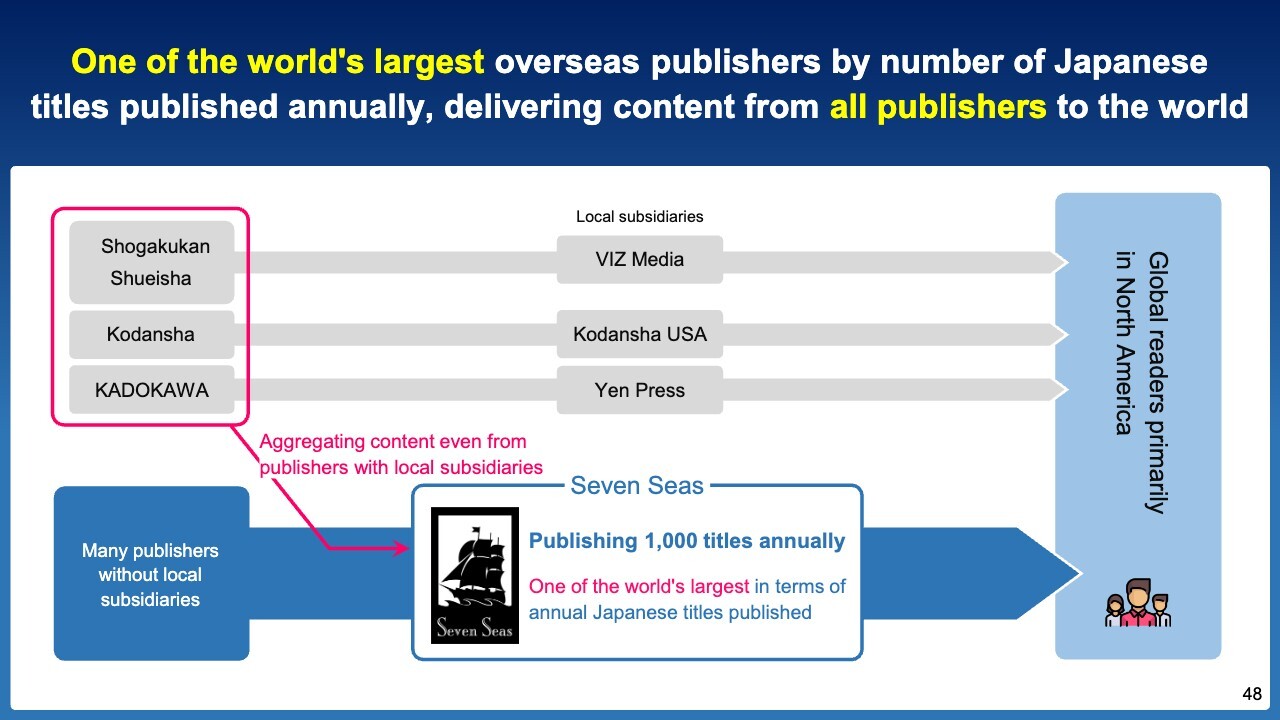

One of the world’s largest overseas publishers by number of Japanese titles published annually, delivering content from all publishers to the world

Major Japanese publishers such as Shogakukan, Shueisha, Kodansha, and KADOKAWA have their own subsidiaries in the U.S.

Shogakukan and Shueisha operate local publishers called VIZ Media, through which they distribute their titles. Kodansha has expanded into the U.S. by acquiring Kodansha USA, while KADOKAWA has done the same by acquiring Yen Press.

Seven Seas handles a wide variety of titles, including those from publishers that do not have local subsidiaries. Furthermore, big four publishers cannot handle the distribution of all their titles through their local subsidiaries alone.

For example, even if a publisher has 1,000 titles in its catalog, only a few hundred can actually be distributed. Depending on the nature of the work and the target audience, Seven Seas obtains licenses from publishers and handles everything from translation to publication.

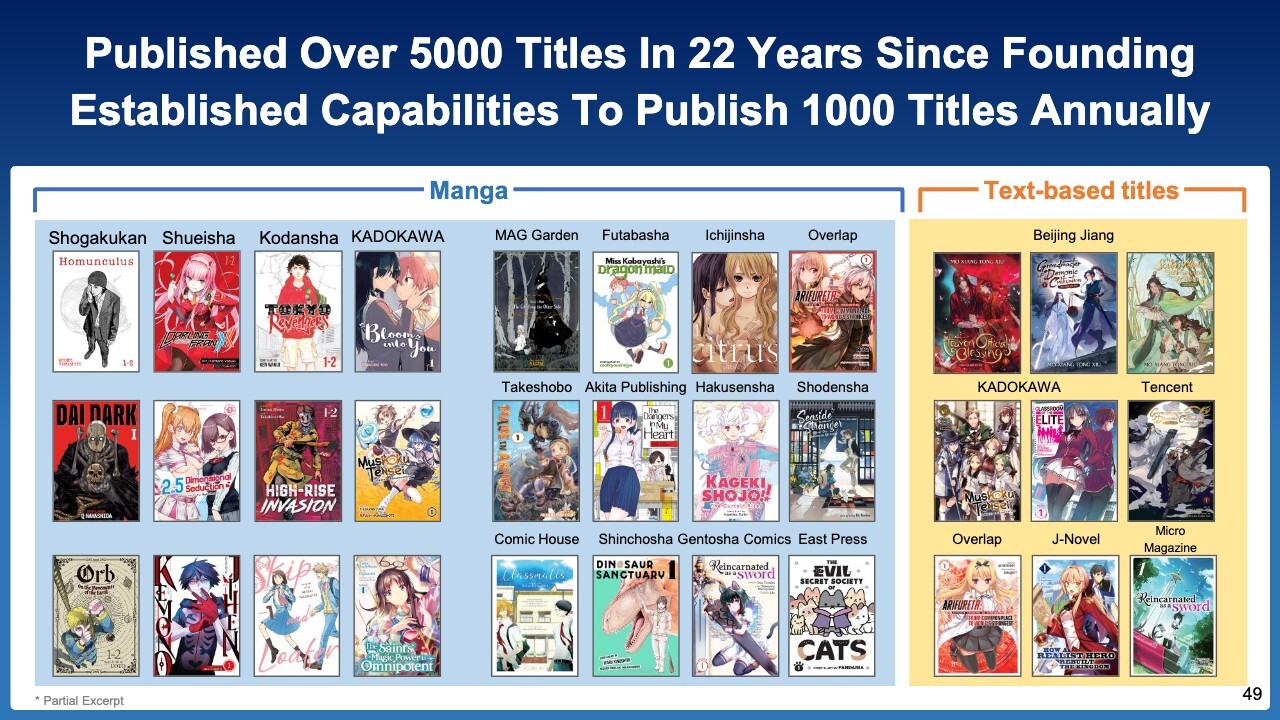

Published Over 5000 Titles In 22 Years Since Founding Established Capabilities to Publish 1000 Titles Annually

The slide serves as proof of this. Seven Seas handles not only manga content from publishers such as Shogakukan, Shueisha, Kodansha, KADOKAWA, and others, but also a wide range of text-based books. As I mentioned earlier, it is not merely a platform for publishers without local subsidiaries but also serves as a platform for major publishers.

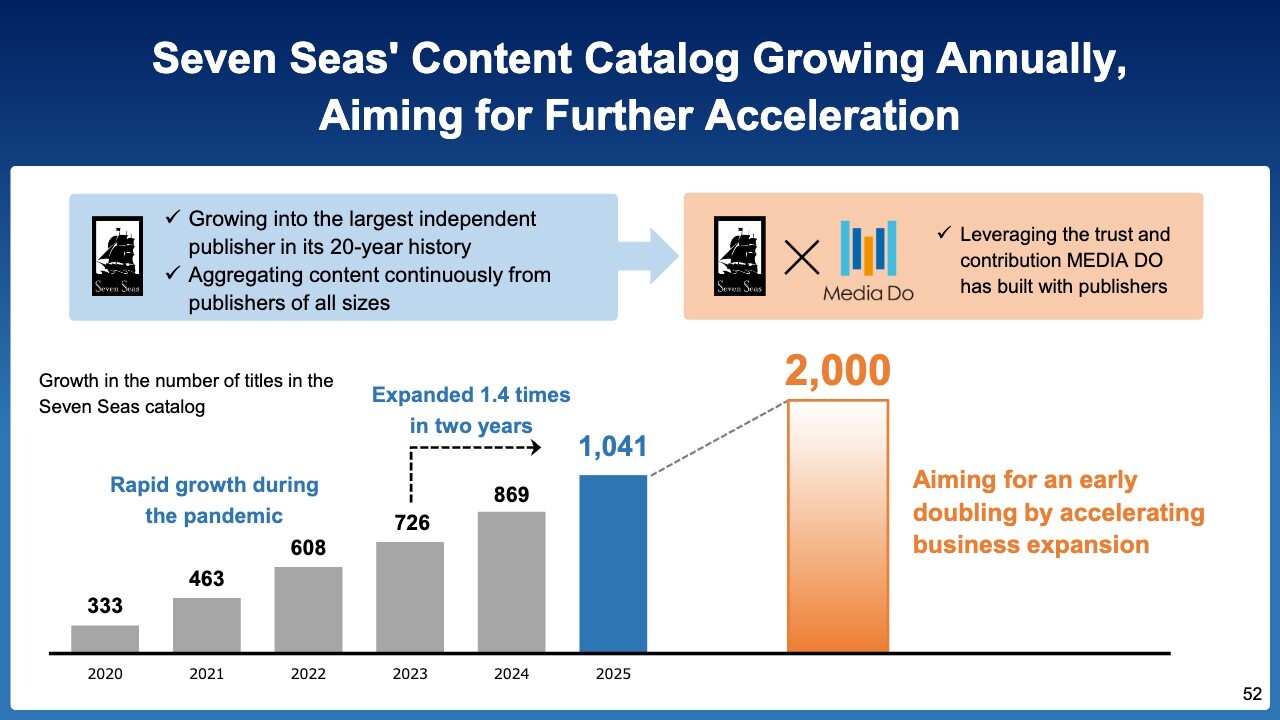

Seven Seas’s Content Catalog Growing Annually, Aiming for Further Acceleration

Since the COVID-19 pandemic, Japanese content has become increasingly visible on Netflix and other platforms.

This slide shows the trend in the number of titles distributed by Seven Seas since 2020. In 2020, it distributed 333 titles. Following the pandemic, Japanese content gained significant attention, and last year it exceeded 1,000 titles. We also intend to continue expanding this portfolio in the future.

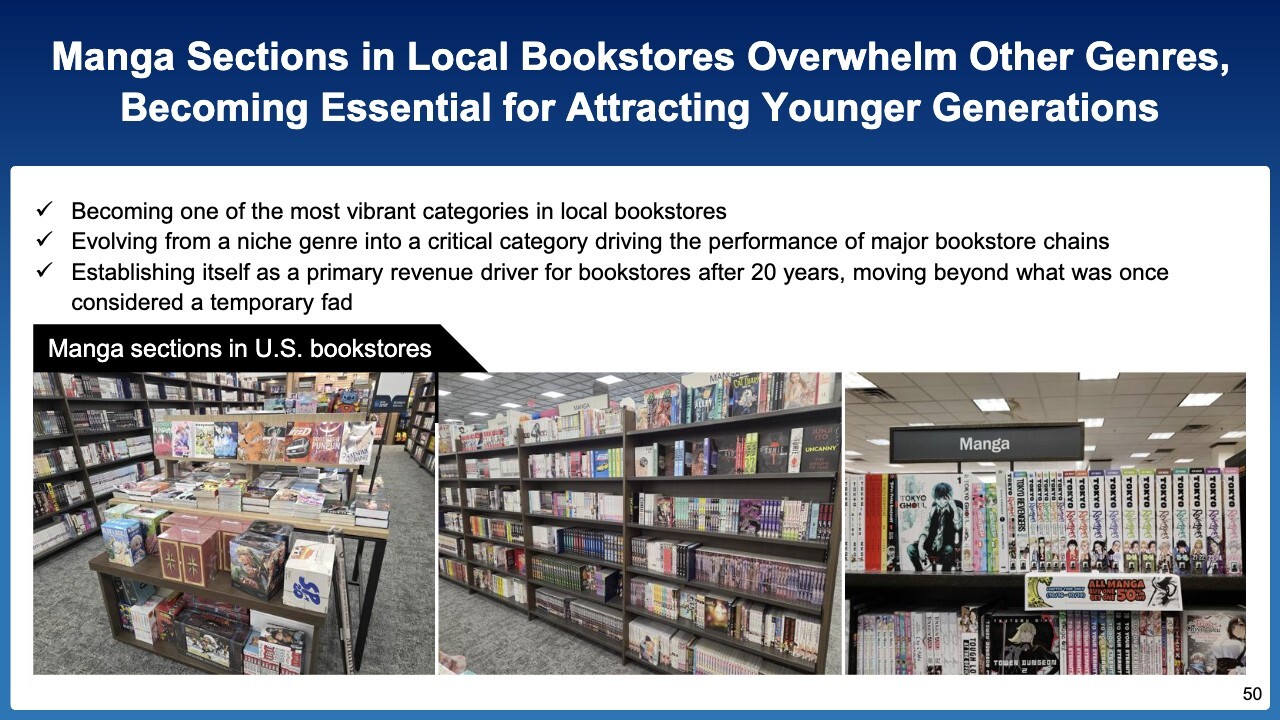

Manga Sections in Local Bookstores Overwhelm Other Genres, Becoming Essential for Attracting Younger Generations

Expanding content offerings is difficult without a market, but since the pandemic, there has been a growing demand for Japanese content, and in some U.S. bookstores, manga now occupies the largest sales floor space.

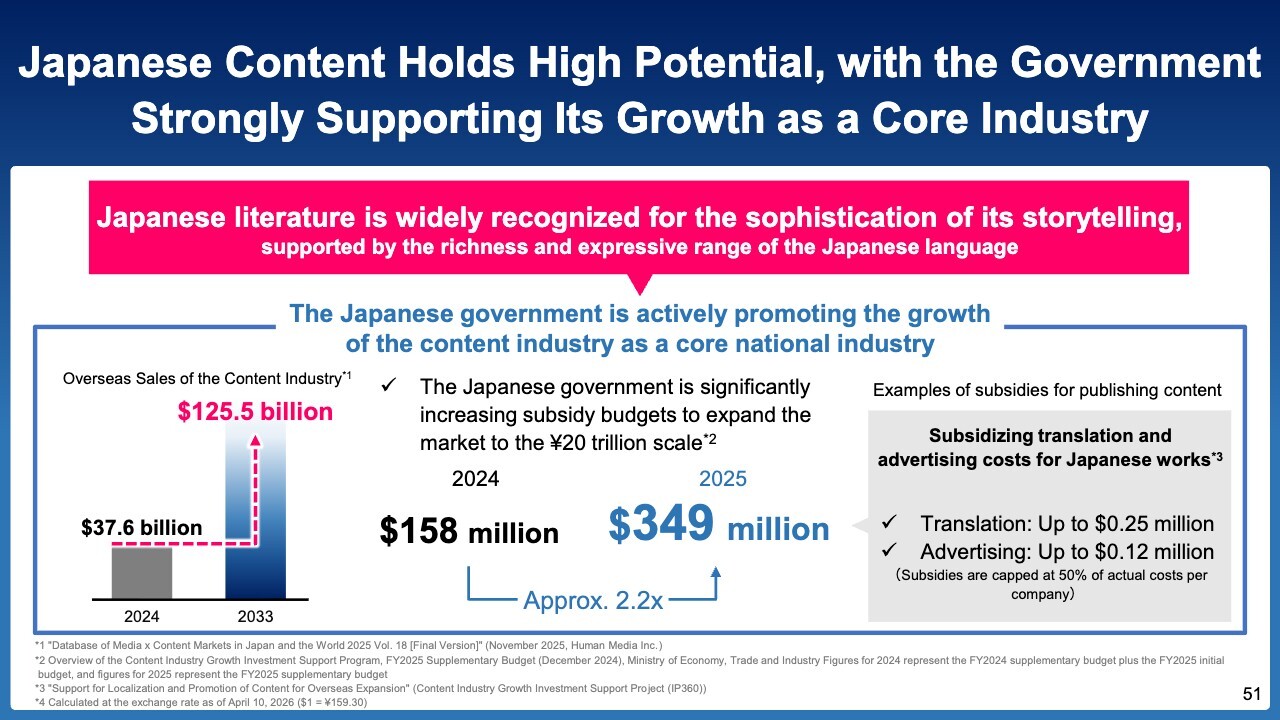

Japanese Content Holds High Potential, with the Government Strongly Supporting Its Growth as a Core Industry

The Japanese government is also actively investing in Japanese content across 17 strategic investment fields. It has set a goal of increasing the content industry’s overseas sales from ¥6 trillion in 2024 to ¥20 trillion by 2033.

We are particularly focused on “books” within the realm of Japanese content. We believe that the majority of the source material for film version such as anime, TV dramas, and movies comes from books. We anticipate that Japanese books will attract even more global attention in the future. In this context, we aim to be at the very center of the movement to spread Japanese books worldwide and contribute to the expansion of Japanese content exports.

As a specific first example is that, until now, Seven Seas has borne 100% of the translation costs for Japanese books. However, since by becoming a subsidiary of MEDIA DO, a Japanese company, it can now take advantage of a government subsidy program that covers a portion of those translation costs. This will help reduce its translation expenses. We also plan to utilize government subsidy programs for advertising.

At the same time, we believe it is important to make various adjustments as we work to establish our position in bringing Japanese content to the world.

Seven Seas’s Content Catalog Growing Annually, Aiming for Further Acceleration

This is the slide I showed you earlier. Since the pandemic, at a time when “Japanese content had a competitive edge and great potential,” MEDIA DO, which does business directly with all Japanese publishers, acquired Seven Seas, a translation publisher that handles more Japanese works than any other in the world and is not affiliated with any major publishers.

As demand for books continues to grow and the catalog expands year by year, we believe that increasing the current collection from 1,000 titles to 2,000 is not a distant prospect.

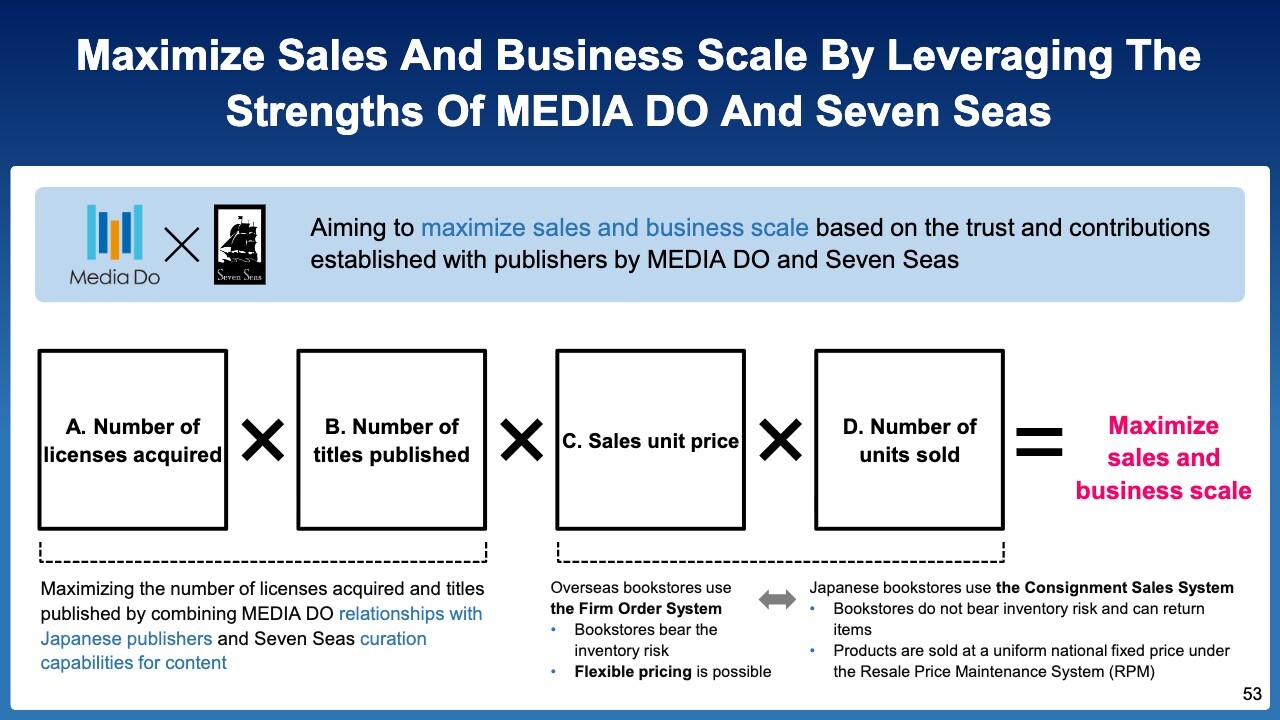

Maximize Sales and Business Scale by leveraging The Strengths Of MEDIA DO And Seven Seas

To achieve steady, strategic growth by leveraging the combined strengths of MEDIA DO and Seven Seas, four KPIs are critical.

First and foremost, the combination of these four KPIs, the number of licenses acquired, the number of titles actually printed and published, the sales unit price, and the number of units sold, is key to maximizing the sales and business scale that our company and Seven Seas aim for. In other words, it determines how effectively we can take responsibility for the distribution and sales of Japanese books.

First, when it comes to “best-selling books,” the number of titles published, denoted as B, is important. However, since B serves as the numerator and the number of licensing acquired, denoted as A, serves as the denominator, the key factor is how many licensing our company can secure.

Through the partnership with MEDIA DO and Seven Seas, we aim to secure licensing that would normally be difficult to obtain, thereby increasing the number of units sold and sales unit price.

We believe we have secured the best possible asset for bringing Japanese content to the world, and we will work to maximize these KPIs in the shortest possible time. In this context, we believe that collaboration with bookstores overseas, particularly in the U.S., will be of critical importance.

Creating New Value Through Regional Assets, Deepening and Expanding Initiatives by Engaging Diverse Stakeholders

This concerns our Sustainability Creation (SC) business. In the eBook industry, we primarily engage with the publishing industry, such as eBook retailer and publishers; however, with regard to regional revitalization initiatives, MEDIA DO aims to become the leading platform for such efforts in Japan.

For this reason, we are working to strengthen our collaboration with all stakeholders and partners.

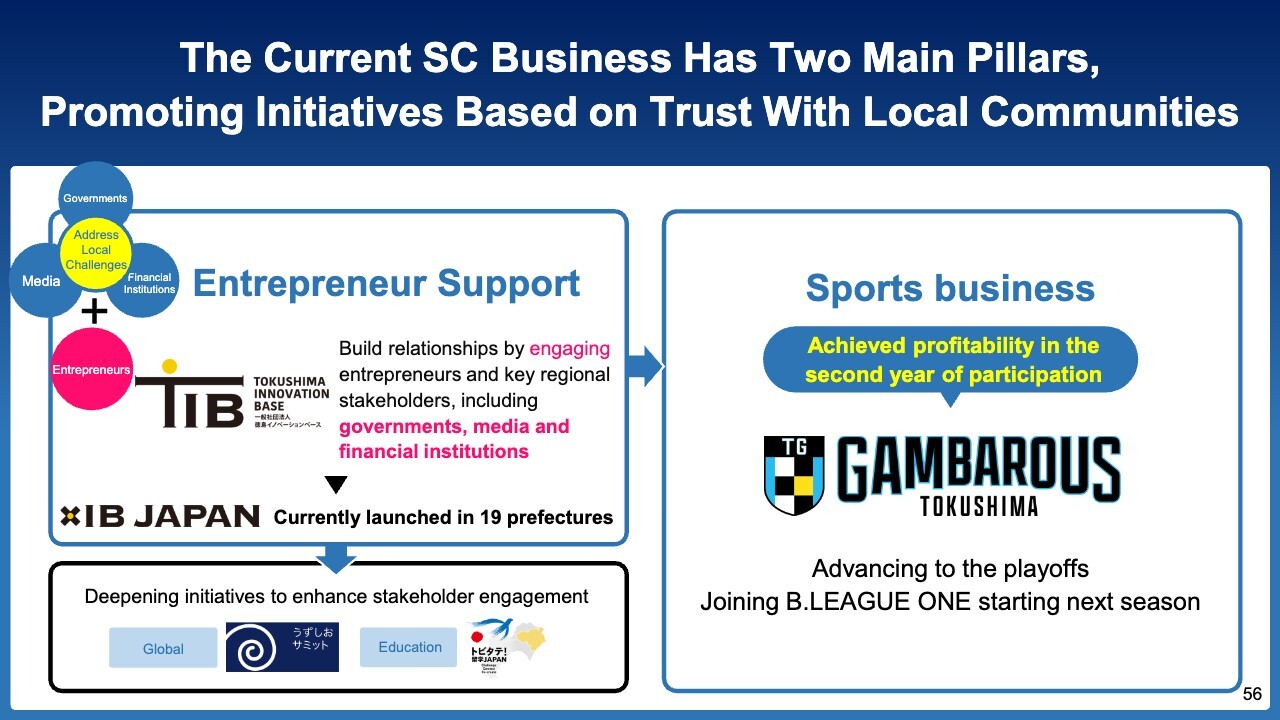

The Current SC Business Has Two Main Pillars, Promoting Initiatives Based on Trust With Local Communities

Our current SC business can be broadly divided into two categories. The first is an entrepreneur support, based on the belief that entrepreneurs will be needed throughout Japan in the future. The second is a sport business to energize people of all ages and genders.

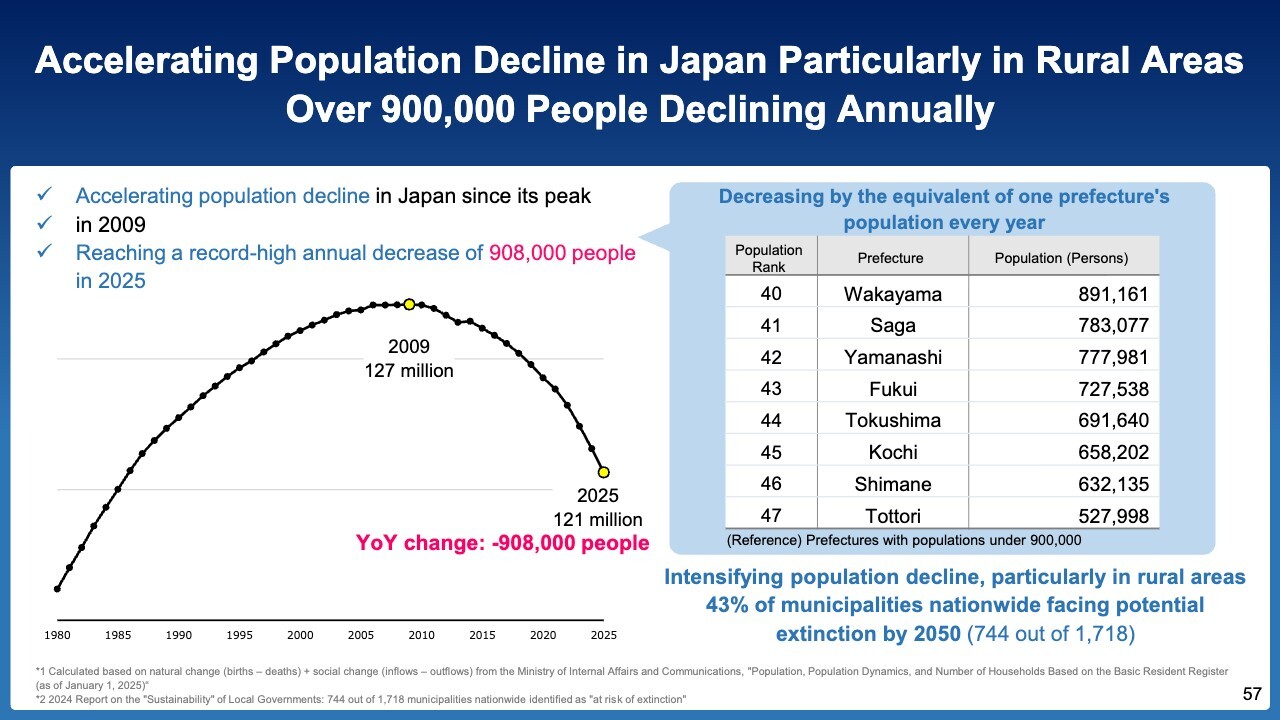

Accelerating Population Decline in Japan Particularly in Rural Areas Over 900,000 People Declining Annually

This situation stems from the fact that Japan is entering a period of major transformation, with its population falling below 120 million by 2026. With the population having declined by 900,000 last year, a figure equivalent to the population of Wakayama Prefecture, and the reality that one prefecture of that size is disappearing every year, immediate action is essential.

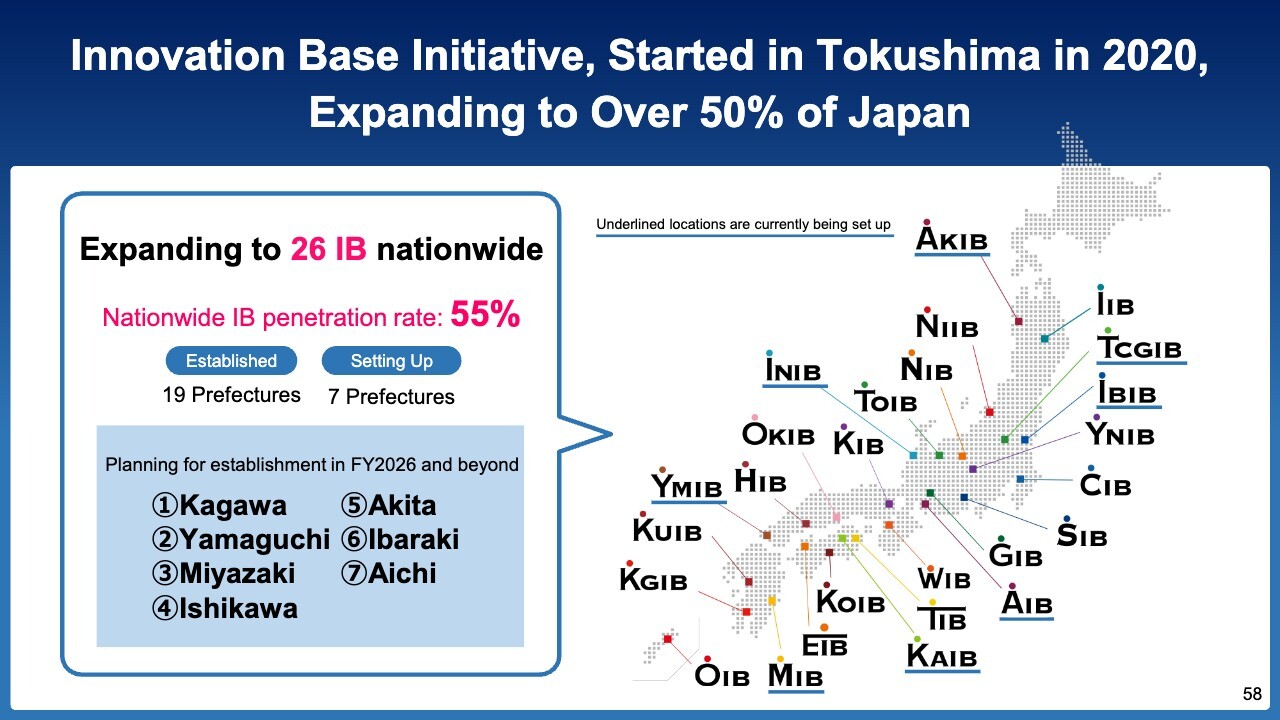

Innovation Base Initiatives, Started in Tokushima in 2020, Expanding to Over 50% of Japan

To revitalize our communities, we need the power of entrepreneurs. In 2020, we launched a platform in Tokushima where entrepreneurs can learn and grow; it has since expanded to 19 prefectures, and next month, Kagawa Prefecture will join, bringing the total to 20. Including those currently in preparation, the total reaches 26 prefectures.

With 26 prefectures, we have now exceeded 50 percent of the 46 prefectures excluding Tokyo. We plan to actively launch the initiative in the remaining prefectures as well.

Uzushio Summit as Tokushima’s Version of the Davos Meetings Rediscovering Regional Value Through Global Engagement

With such platforms already in place, we held the Uzushio Summit in Tokushima as a first step, aiming to engage more people and redefine regional assets.

In collaboration with the Awa Bank, Ltd., the Tokushima Taisho Bank, Ltd., and Tokushima University in Tokushima Prefecture, the summit welcomed a total of 282 participants. Through discussions about Tokushima’s future, various projects and events have emerged.

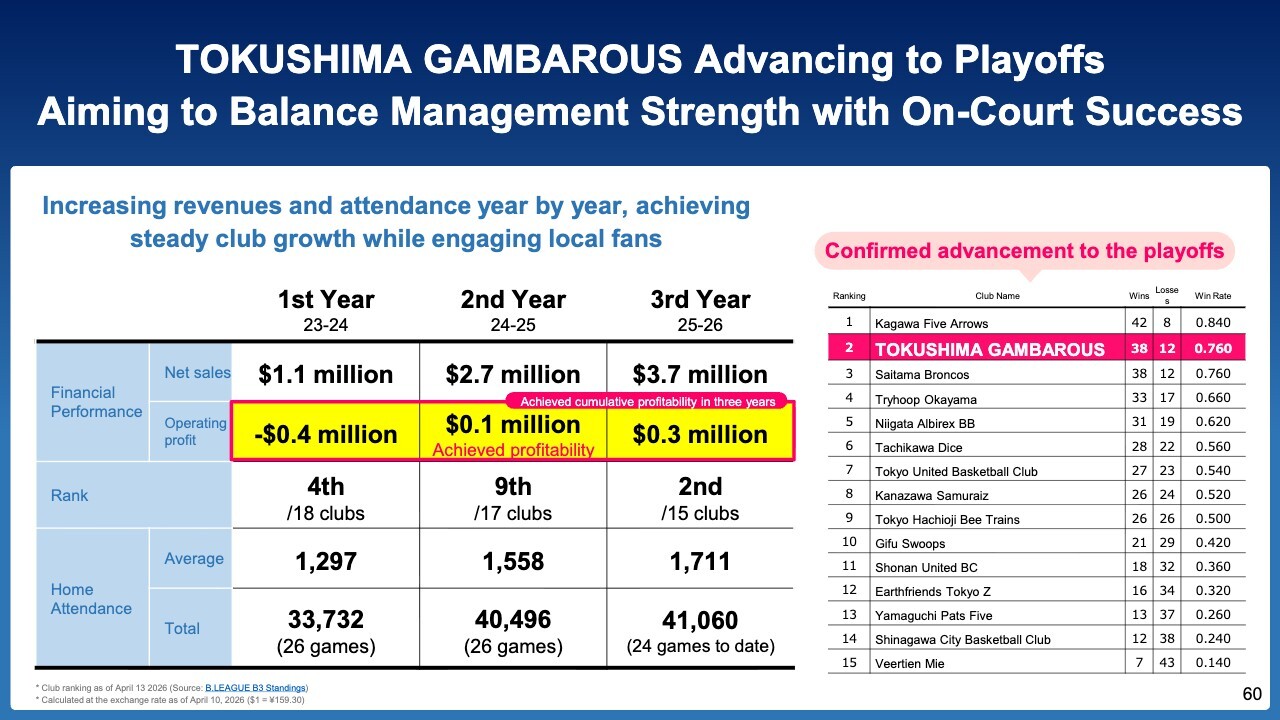

TOKUSHIMA GAMBAROUS Advancing to Playoffs Aiming to Balance Management Strength with On-Court Success

Regarding TOKUSHIMA GAMBAROUS, our basketball club competing in the B.LEAGUE, we received voices of concern when we announced our entry into the sports business.

However, thanks to the platform I just discussed, as well as our collaboration with media partners and local communities, although we posted a deficit of approximately $0.4 million in the first year of the launch phase, we achieved full-year profitability in the second year with profit of $0.1 million, followed by profit of $0.3 million in the third year. As a result, we have reached the point where we can offset the initial $0.4 million deficit within three years.

Not only have we eliminated accumulated losses, but we have also built a strong team. Though in the B3 division, the club currently ranks second and has advanced to the playoffs. In recognition of such club management capabilities, I have been appointed as director of the B.LEAGUE.

Accelerating Regional Revitalization as a Shared Vision Through Partnership Between xIB JAPAN and B.LEAGUE

Seeking various collaborative opportunities to support entrepreneurs nationwide who drive regional revitalization, we announced a partnership agreement yesterday between B.LEAGUE and xIB JAPAN, which provides operational support for innovation bases across the country.

This initiative helps local companies to propose various business projects to the B.LEAGUE. Viewed from the B.LEAGUE’s perspective, it enables collaboration with local companies to host a variety of events and other activities.

For example, if a local company specializes in producing promotional giveaways, it can pitch its ideas to all 55 clubs in the B.LEAGUE at once. We have signed this partnership agreement to proactively create such opportunities and revitalize local communities.

Innovation Base Entering Phase 2 Strengthening Partnerships and Enhancing Development of Regional Business Leaders

The number of Innovation Base (IB) I explained earlier has grown to 26. In the upcoming Phase 2, we aim to scale this initiative to cover 46 prefectures and reach a membership of 5,000 people.

This project will not immediately generate significant profits for our company. However, once the Innovation Bases we have launched and operate spread across the nation and membership reaches 5,000, we will be able to start various new businesses by combining these resources.

Furthermore, if we expand to a scale of 10,000 members in Phase 3, we will be able to make various proposals to government agencies as well.

I have now covered our three growth strategies. Next, I will explain our full-year earnings forecast.

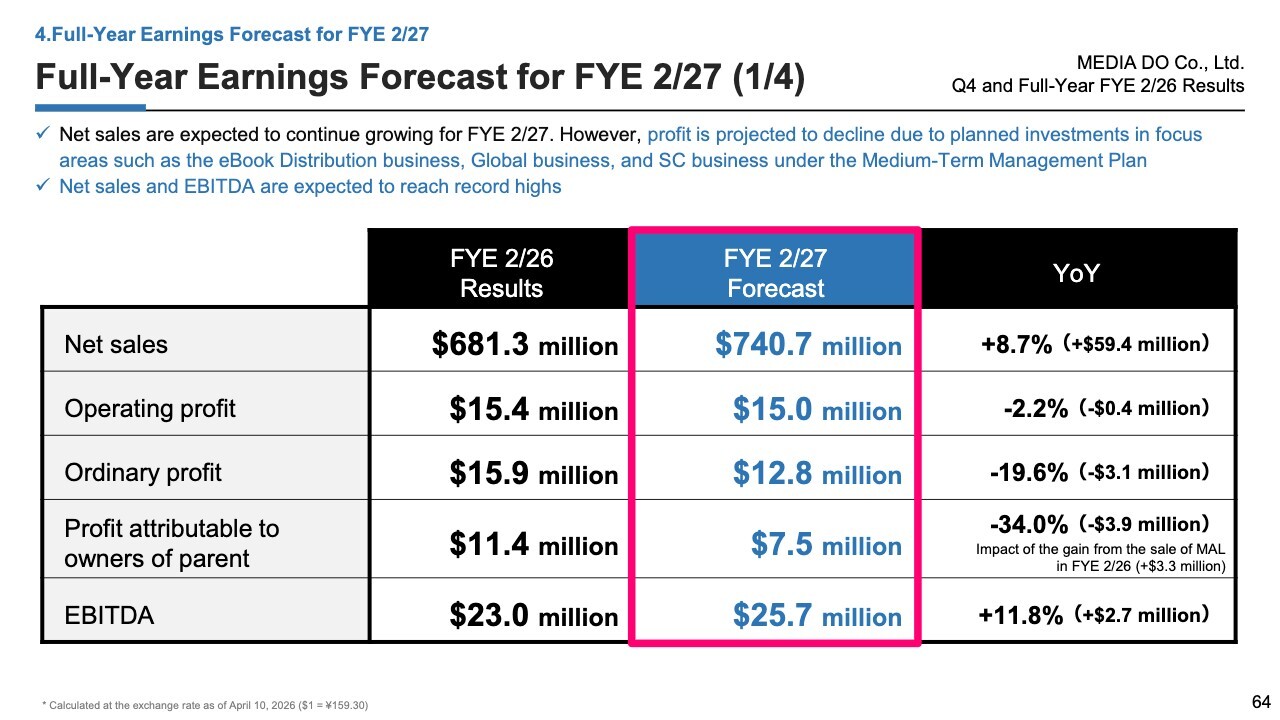

Full-Year Earnings Forecast for FYE 2/27 (1/4)

For FYE 2/27, we forecast net sales of $740.7 million, an increase of $59.4 million, or 8.7% YoY.

On the other hand, operating profit is projected to be $15.0 million, down $0.4 million, or 2.2% YoY. This is due to the investments in the eBook Distribution business discussed earlier, the loss of high-margin services, and various investments including in the SC business.

EBITDA, which represents actual earning power, is projected to increase by $2.7 million, or 11.8% from $23.0 million in the previous fiscal year to $25.7 million this fiscal year.

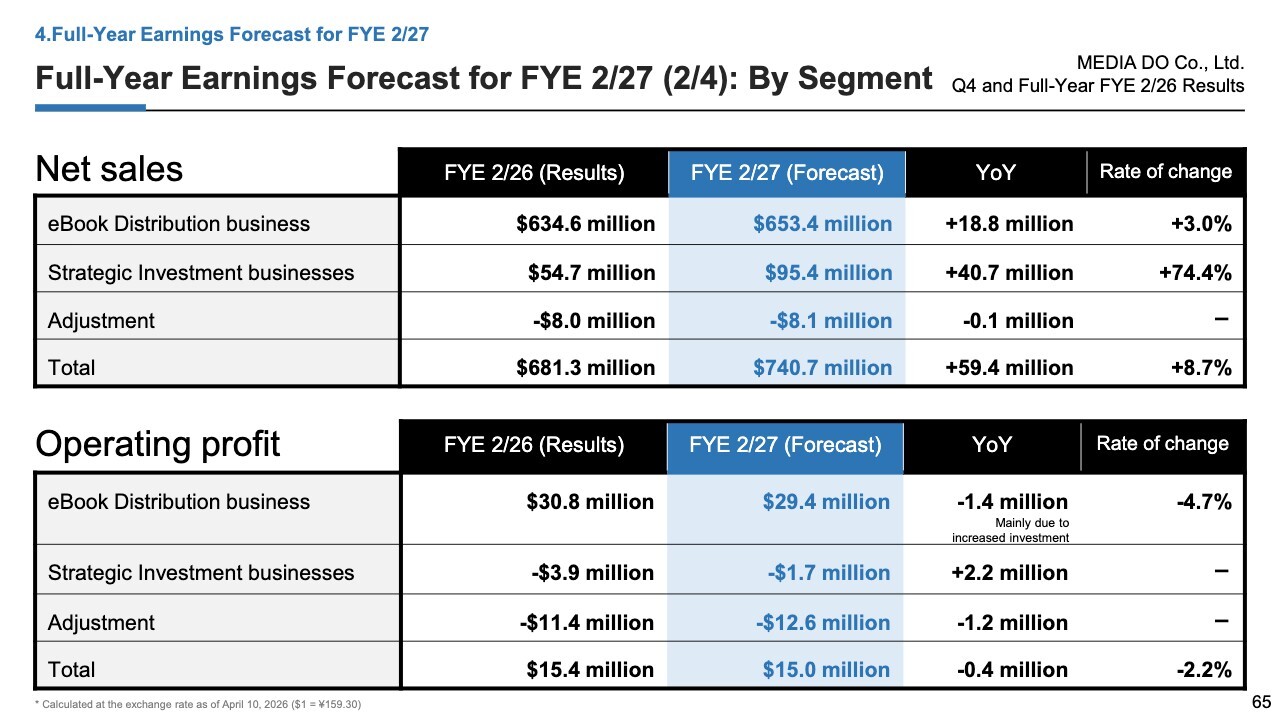

Full-Year Earnings Forecast for FYE 2/27 (2/4): By Segment

Here are the net sales and operating profit by segment. Please take a look at the slide for details.

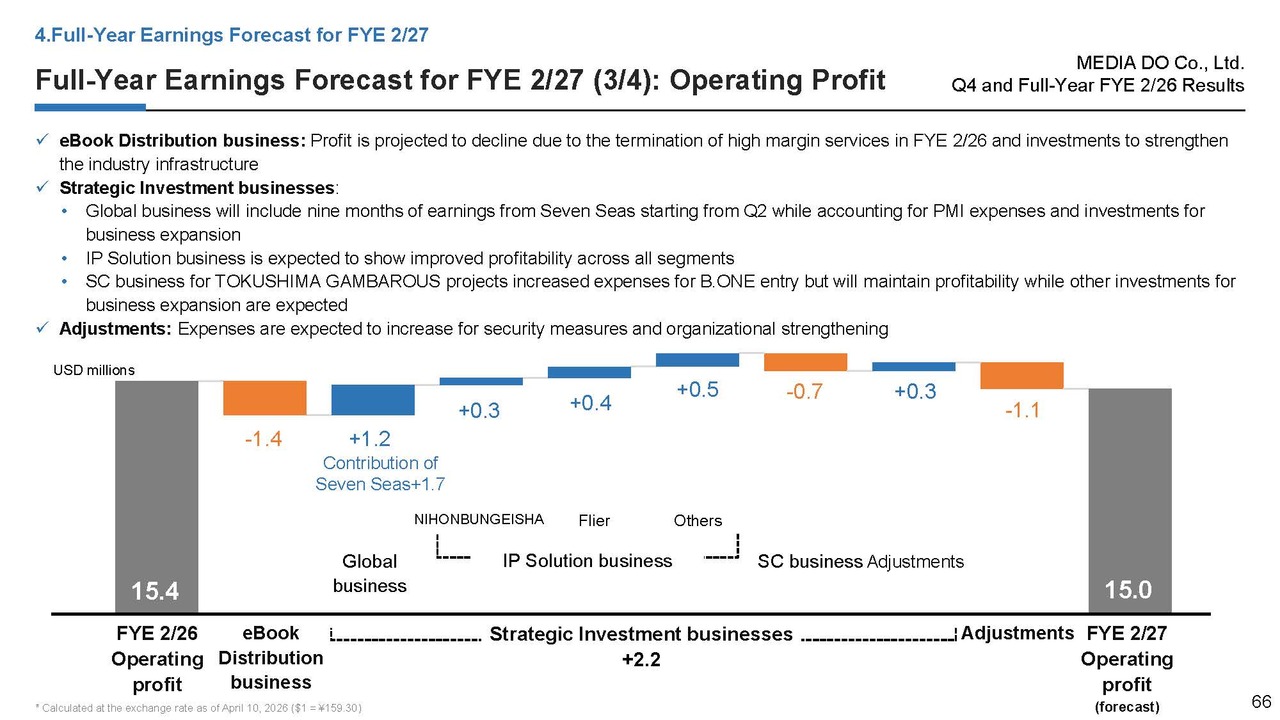

Full-Year Earnings Forecast for FYE 2/27 (3/4): Operating Profit

This slide shows a waterfall chart providing a YoY comparison of operating profit. The reason for the $1.4 million decrease in the eBook Distribution business is as I explained earlier.

During the previous fiscal year, the Strategic Investment businesses, including the Global business, posted acquisition-related expenses at group companies and experienced delays in profit improvement during H2; however, we expect a gradual recovery.

With all these factors added together, our earnings will decrease slightly from the previous year. However, I believe we have put in place the foundations to move closer to a distinctive position in the industry beyond the market leadership.

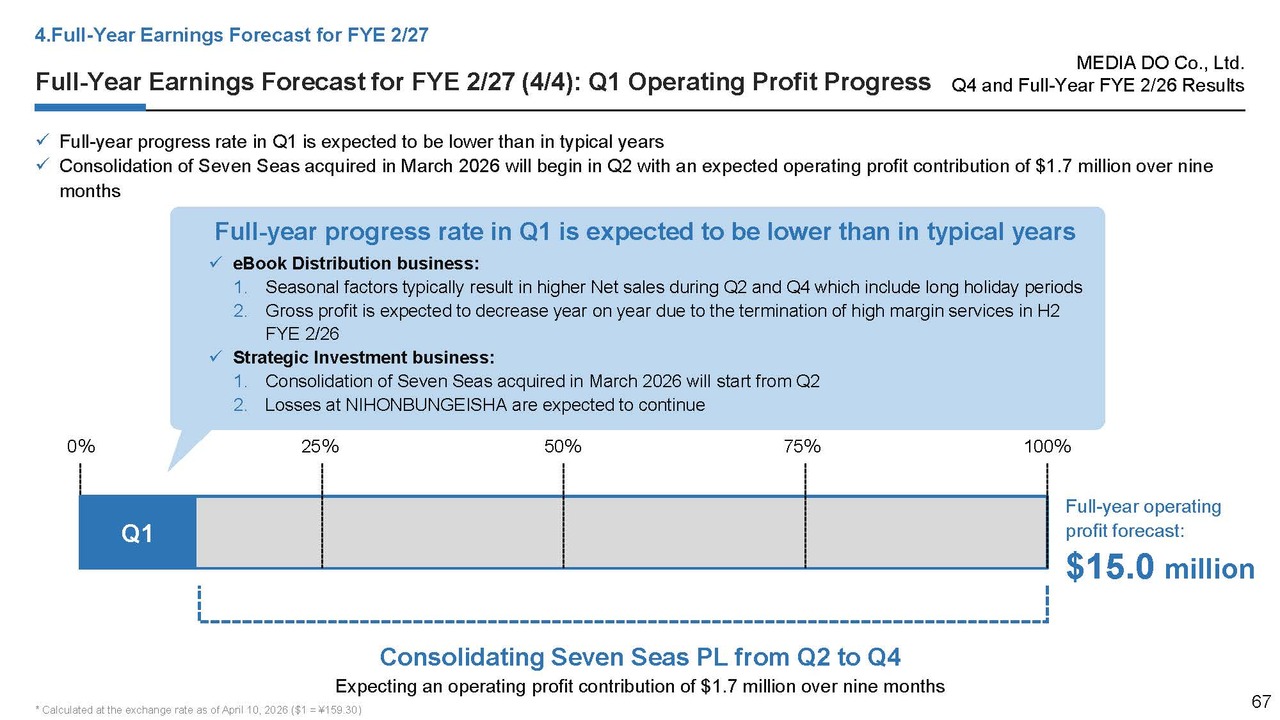

Full-Year Earnings Forecast for FYE 2/27 (4/4): Q1 Operating Profit Progress

For the progress rate in Q1 this fiscal year, we expect it to fall even lower than in typical year, which is slightly below 25% due to seasonal factors. This is because the consolidation of acquired Seven Seas will start in Q2, and we make upfront investments from the beginning of the period.

That said, our business model is tail-heavy in principle. We are determined to achieve our full-year operating profit forecast of $15.0 million.

Review of Business Portfolio

As I have been discussing, we recognize that MEDIA DO has been in a transitional phase, with our “selection and concentration” approach,including consolidating group companies and acquiring Seven Seas with an eye toward future developments.

Now, with the consolidation under the selection and concentration approach largely complete, we are finally entering a phase of “challenge and expansion,” leveraging our position and market share.

Shareholder Return Policy

For our shareholder return policy, as Kuramoto explained earlier, we plan to pay a dividend of ¥40 for FYE 2/26, and expect to maintain the same amount for FYE 2/27, with a dividend payout ratio of around 50%. This is somewhat higher than our policy of a “total return ratio of 30% or more.”

As part of our commitment to our shareholders that we are poised for future growth, our policy is to maintain the dividend at this level at a minimum, without reducing it.

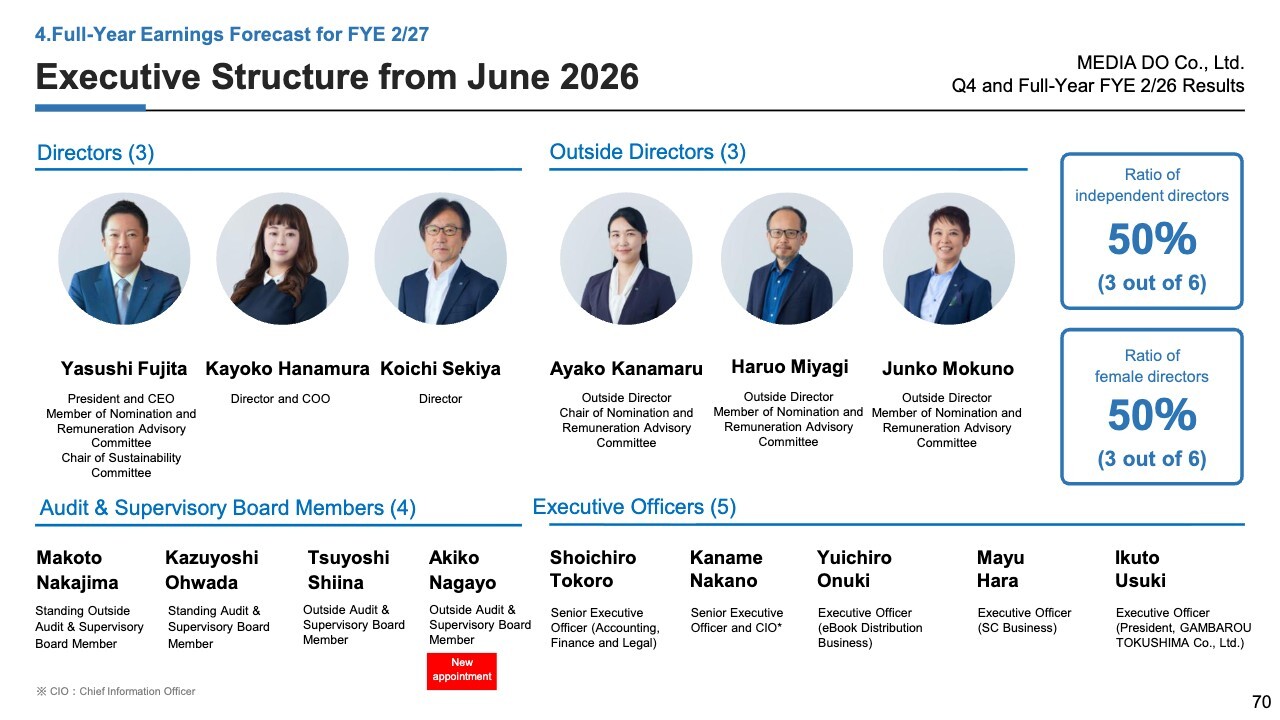

Executive Structure from June 2026

Here is our executive structure for this fiscal year. The ratio of independent directors is 50%, and the ratio of female directors is also 50%.

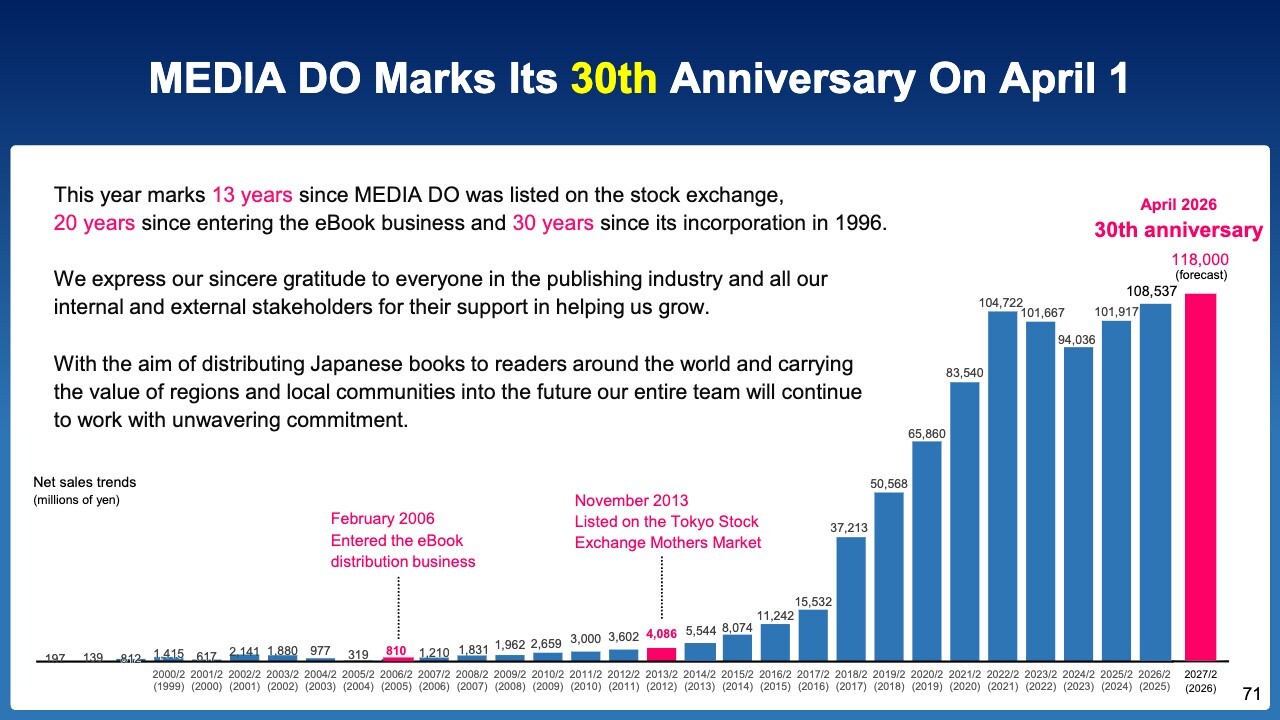

MEDIA DO Marks Its 30th Anniversary On April 1

On April 1, MEDIA DO marked its 30th anniversary since its incorporation. With this year marking 13 years since our listing and 20 years since our entry into the eBook distribution business, we have earned this rare opportunity to take on the challenge of bringing Japanese content to the world.

In the coming 30 years, we aim to turn offensive and work hard with all employees united as one. Please look forward to our future success.

That concludes my presentation. Thank you very much.

Q&A: Seven Seas’ contribution to this fiscal year’s consolidated results

Questioner: It was mentioned that Seven Seas’ contribution to this fiscal year’s consolidated results is expected to be ¥0.28 billion over nine months. However, in the initial explanation, operating profit for FYE 12/24 was stated at ¥1.6 billion. Based on this, I would expect a contribution of around ¥1.0 billion for nine months, what is the reason for this discrepancy?

Kuramoto: The consolidated results for FYE 2/27 will incorporate Seven Seas’ performance for nine months. From Seven Seas’ operating profit, we expect to deduct amortization of goodwill and PMI expenses resulting from the consolidation, which results in ¥0.28 billion.

Let me explain this in a little more detail. Regarding the assumptions used for this consolidation, the adjusted operating profit for FYE 12/23 and FYE 12/24 is approximately ¥1.6 billion, as stated in the materials disclosed on March 2.

For 2026, the assumption is slightly lower than that level, at approximately ¥1.35 billion. From the nine-month portion of that amount, we record ¥0.15 billion in PMI-related expenses and ¥0.58 billion in goodwill amortization, resulting in an expected contribution of ¥0.28 billion to operating profit.

Please note that the figures I just mentioned for goodwill and so forth are provisional estimates used for this fiscal year’s earnings announcements and are not yet finalized.

Fujita: The operating profit for last year was $10 million, and we project $9 million for this year; however, this is our conservative estimate. While the acquisition was made in March, in the preceding months of January and February, the company posted record-high sales.

Given that, I don’t think we need to be overly conservative, but because this is the first year after the acquisition, we are cautiously projecting operating profit at $9 million instead of $10 million.

Q&A: Seven Seas’ profit contribution from next year onward

Questioner: Regarding the contribution of Seven Seas, in addition to the ¥1.6 billion in operating profit, I anticipate standalone growth for Seven Seas from next year onward driven by synergies. Can we expect its full-fledged contribution?

Fujita: The PMI-related expenses primarily involve accounting conversion from the U.S. to Japanese standards.

Furthermore, as MEDIA DO will undertake the acquisition of rights going forward, operations will be far smoother and more efficient than the previous approach of marketing from the U.S. to Japan. With this in mind, we aim to double the number of titles published annually from the current 1,000 as soon as possible.

Given these factors, and also considering recent inflation, we are confident that we can grow its performance.

Q&A: The realistic potential of Japanese content

Questioner: The Japanese content market size is projected to grow from ¥6 trillion to ¥20 trillion in less than 10 years. In your opinion, President Fujita, what level of growth would you consider realistic?

Among the good scenarios and bad scenarios, how much do you expect the market to grow in the areas where MEDIA DO can gain share? What specific benefits do you expect to see? Please elaborate on this little further.

Fujita: The scale is so vast that it’s difficult to clearly visualize how much the ¥6 trillion will grow. On the other hand, I expect video content to show particularly strong growth going forward. I think a major factor in the success of Japanese manga is the past broadcast of anime on conventional terrestrial TV.

Then, video media platforms like Netflix and YouTube, which can reach general consumers, are becoming increasingly prominent. Given this trend, we can certainly expect a supply shortage of content.

In such a situation, companies with larger content inventory will naturally find it easier to secure market share. Therefore, I personally do not view the Japanese government’s goal as unachievable, which aims at growing the market size from ¥6 trillion to ¥20 trillion over the next few years

While this ¥20 trillion encompasses everything from games to movies and TV dramas, the source works for many of these are manga or books. In fact, Seven Seas has received many inquiries from a certain video distribution company. From this perspective, we aim to become one of the mainstream players dealing with books.

Regarding our operations in the U.S., our business model No.1 involves translating Japanese books and selling them at U.S. bookstores through Seven Seas. We must also consider our business model No.2 and No.3.

In the business model No.2, we treat the books we handle as IP, not just publications. Depending on the content of the work, we can pursue downstream monetization of IP through merchandising, anime adaptations, and film adaptations, among others.

In the business model No. 3, we need to consider ways to partner with local bookstores as we continue to expand Japanese content and IP, given that Japanese bookstores typically receive around 25% of sales, while U.S. bookstores receive 50%.

Alternatively, we could collaborate with Japanese publishers or companies and launch new retail initiatives, with MEDIA DO supplying content. While such ventures would be feasible only if content is available, we are in a position to provide it. Therefore, in terms of retail expansion and other initiatives, we believe we can partner with diverse companies, setting aside whether we pursue these projects independently.

Given these factors, the landscape would be totally different for us depending on whether or not we acquire Seven Seas, a company that has already established a strong position in the distribution of print books, the essential foundation for all these initiatives.

Q&A: Actions to address the gap in book prices between Japan and the U.S.

Questioner: I would like to ask about the gap in book price between Japan and the U.S. I’ve heard from presidents of Japanese distributors and some eBook retailers that they have been asking or even demanding that publishers raise book prices, arguing that they are just too low at present.

Mr. Fujita, do you have any plans to make a similar request to publishers to raise book prices?

Fujita: I personally don’t get the impression that Japan is experiencing inflation compared to the rest of the world, in terms of the amount of salary and other factors. Therefore, the balance between income and the purchase price is important.

In other countries, especially those where salary increases and inflation are accelerating, market prices for Japanese content will inevitably rise on the back of this trend. Consequently, it is likely easier to raise prices overseas than it is in Japan.

We have also received requests from publishers to raise prices as much as possible when selling overseas. We hope to work with publishers to achieve appropriate pricing.

Q&A: Seven Seas’ strength in curation

Questioner: I remember you mentioned during the briefing session after the Seven Seas acquisition that one of Seven Seas’ strengths was its strong curation capabilities in selecting Japan’s IPs for publication. As the number of content grows going forward, do you think their curation capabilities will improve further, or will they remain at the current level?

Fujita: Let’s say, we identify titles that we consider promising and approach publishers. The chances of actually acquiring the rights are only a small percentage of those cases.

After bringing Seven Seas into our group, we visited publishers together with them, and the publishers asked us to select titles from the lists of potential works they provide.

Previously, we had to compile our own lists for selection. Now that publishers are providing them, the overall pool of candidates has expanded significantly. Furthermore, there were works Seven Seas previously wanted to publish but couldn’t acquire rights for; however, now they have become a group company of a Japanese firm, and the 20-year track record of MEDIA DO’s business in the industry gives business partners a sense of security.

When it comes to concerns about whether payments will be made on time, I think our clients feel even greater confidence that payments will be made reliably because we are a Japanese publicly listed company.

Therefore, by combining our curation capabilities, the expanded list of titles, and increased share of licenses acquired, I believe the number of titles published will grow.

Q&A: The Japanese manga boom in the U.S.

Questioner: Is Japanese manga experiencing a boom in the U.S.? Will the boom continue to grow? It seems that even relatively niche Ips, known only to specific fans in Japan, are being published as books in the U.S. and selling quite well.

Fujita: I expect the boom to continue to grow further. Like YouTube videos, you can understand much more in a far shorter time by reading manga than by reading a regular book. In terms of the satisfaction from reading experience and the amount of information you gain, it is easier to follow the plot with manga, because it features illustrations and a storyline for each scene.

It’s no exaggeration to say that manga now actually occupies the largest shelf space in U.S. bookstores. Considering that more and more people are becoming familiar with manga, we believe this is not just a temporary fad but a phenomenon that will continue to expand in the future.

Q&A: How to count the number of titles published annually

Questioner: On the slide, you mention Seven Seas publishes 1,000 titles annually. How are the titles counted? For example, do you count the release of volumes 1, 2, and 3 of Demon Slayer: Kimetsu no Yaiba as three separate titles, or do you count the three volumes as a single title under Demon Slayer: Kimetsu no Yaiba?

Fujita: We count it the former way. When we say “title,” we are referring to the volume count. We use the term “series” when referring to Demon Slayer: Kimetsu no Yaiba, for example. The figure of 1,000 titles per year refers to the number of volumes.

Questioner: So does that mean you’re counting the number of ISBNs?

Fujita: Yes, exactly.

Q&A: Contributions to bookstores in Japan

Questioner: Although they probably are not your direct business partners, I suppose we are all aware that the domestic bookstore market is facing quite a tough situation. Your company previously had a business alliance with Tohan Corporation, and you mentioned earlier the differences in bookstore’s margins between Japan and the U.S.

Given that bookstores in the U.S. typically receive about 50% of the sales, do you see any prospects or plans to somehow contribute back to or support the domestic bookstore market in Japan, for example, as you will accumulate expertise in direct transactions in the U.S.?

Fujita: As we work to increase our market share in the U.S. bookstore sector, the number of stores we can open on our own is limited. Therefore, we will need to partner with various companies. The idea is that instead of opening just three stores in a year as a single company, three companies working together can open nine stores.

Japanese bookstores possess the most expertise in the retail operations of bookstores. I think they have expertise in shelf display techniques and various other aspects. While not every Japanese bookstore can become like Kinokuniya Company Ltd., I believe it is possible for us to build up our own expertise and expand our operations jointly with bookstores through joint ventures, for example.