Table of Contents

Hidenori Kobuchi (hereinafter “Kobuchi”): My name is Hidenori Kobuchi, COO and Representative Director of Toagosei Co., Ltd. Thank you very much for taking time out of your busy schedule to attend our financial results briefing today.

Unprecedented volatility continues in the business environment. I would like to explain how our group has built up a record of achievements within this environment and how we intend to adapt from here on out.

I know that time is limited today, but I hope to make this an opportunity to gain your further understanding of and trust in our group. With that, I would like to start. My presentation will follow the outline shown in the slide. I will discuss our new medium-term management plan later in the presentation.

Summary of Financial Results for FY2025

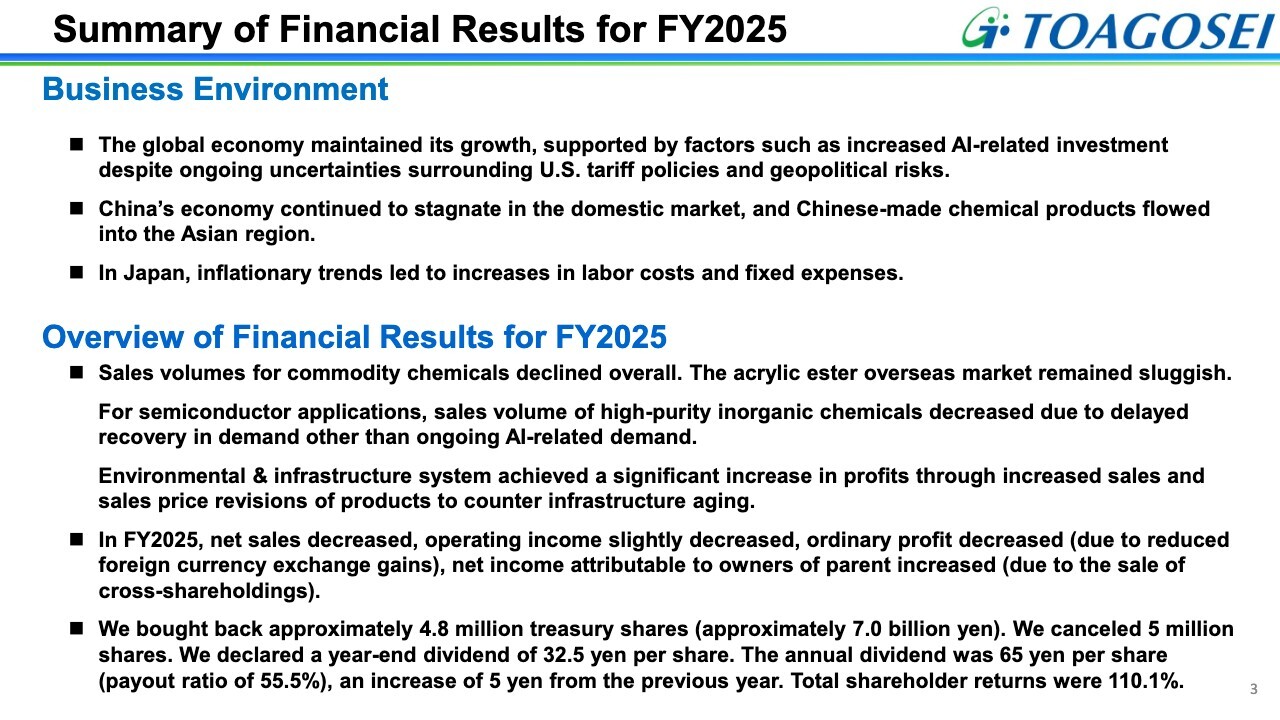

Financial results for the fiscal year ended December 31, 2025 are shown here. In terms of the business environment, despite ongoing uncertainty over U.S. tariff policies and geopolitical risks, growth opportunities were apparent in areas including increased AI-related investment.

However, the business environment remained challenging due to the influx of low-priced Chinese products into the Asian region and a significant increase in labor costs and fixed expenses in Japan.

Taking an overview of our financial results for FY2025, sales volumes of commodity chemicals declined overall. Overseas market conditions for acrylic esters, in particular, remained sluggish due to the influx of inexpensive Chinese products into Asia. Although demand for semiconductors for AI applications expanded, sales of high-purity inorganic chemicals declined due to delayed recovery in demand for other applications.

Aronkasei's environmental & infrastructure system recorded a significant increase in profit due to higher sales and price revisions for products to counter the aging of infrastructure.

As a result, consolidated net sales decreased from the previous year, while operating income declined only slightly. However, ordinary profit decreased due to a decrease in foreign exchange gains (losses).

As a measure to strengthen shareholder returns, we bought back treasury shares worth approximately ¥7.0 billion this fiscal year and increased our annual dividend by ¥5 from the previous year to ¥65 per share. This resulted in a total shareholder return of 110.1%.

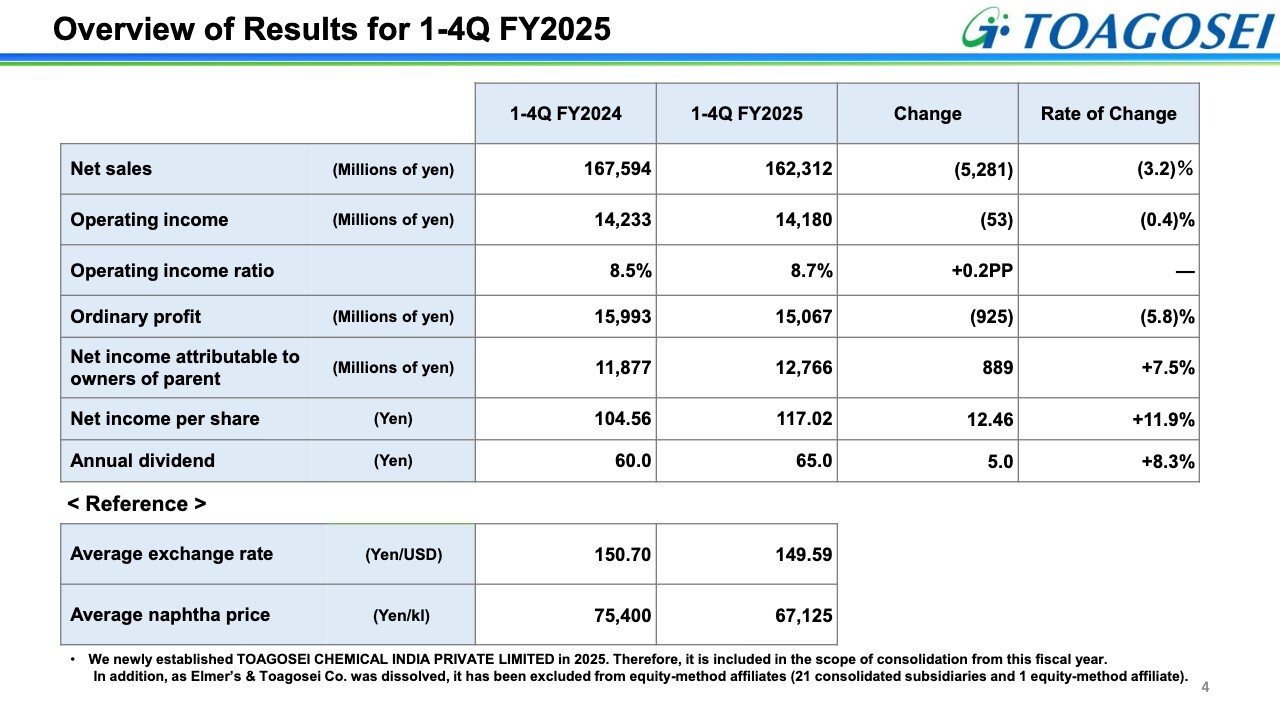

Overview of Results for 1-4Q FY2025

This is a numerical overview of our financial results. Sales and operating income decreased slightly to ¥162,312 million and ¥14,180 million, respectively.

In the Plastics segment, sales of products for activities to counter the ageing of infrastructure were solid, as were sales of Polymer & Oligomer products. However, this was not enough to make up for the overall decline in sales due to the end of contract manufacturing for some products in the Commodity Chemicals segment.

Operating income remained at nearly the same level as the previous year through efforts to revise sales prices in response to rising raw material prices and logistics costs, despite an increase in expenses related to changes in our sales structure in the U.S.

Ordinary profit decreased due to a decrease in foreign exchange gains, while net income attributable to owners of the parent increased to ¥12,766 million, primarily due to proceeds from the sale of cross-held shares. Net income per share was a record-high ¥117.02, due in part to share buybacks.

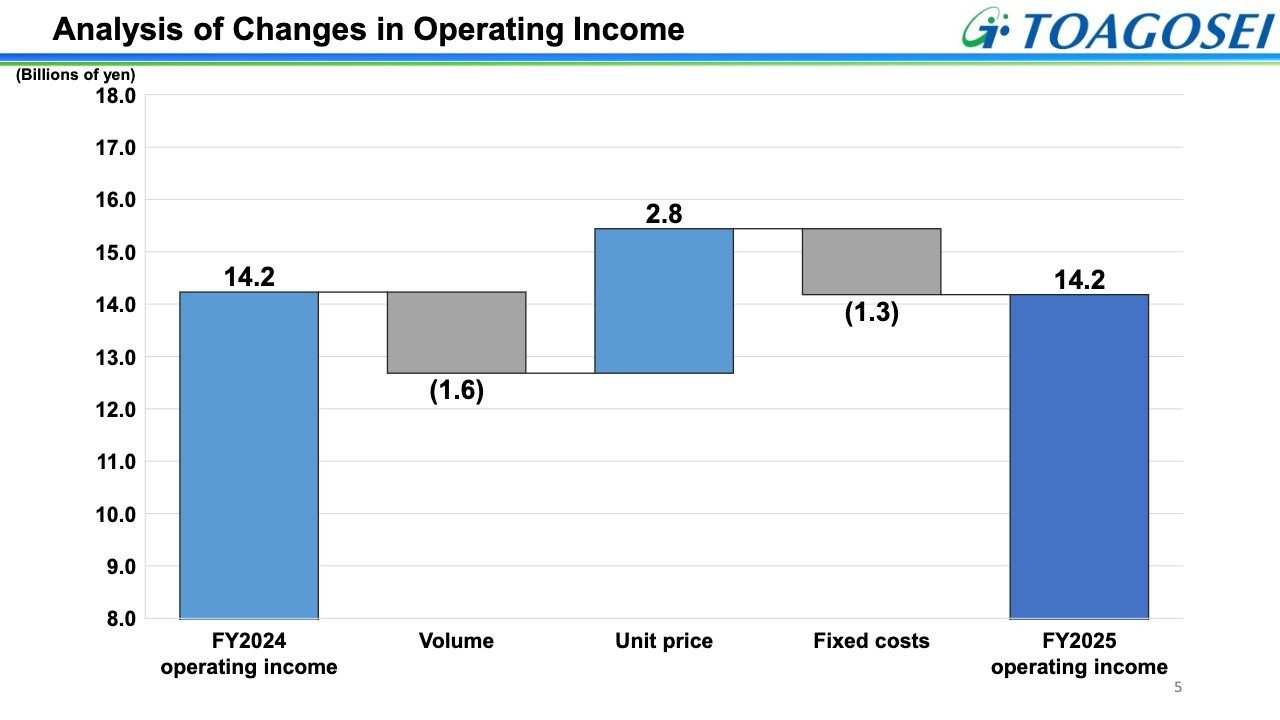

Analysis of Changes in Operating Income

This slide analyzes changes in our operating income. Despite a decrease in sales volume due to the end of contract manufacturing and an increase in fixed costs such as labor costs and depreciation expenses, operating income was approximately ¥14.2 billion, the same level as in the previous year, as a result of appropriate price revisions and profitability improvement.

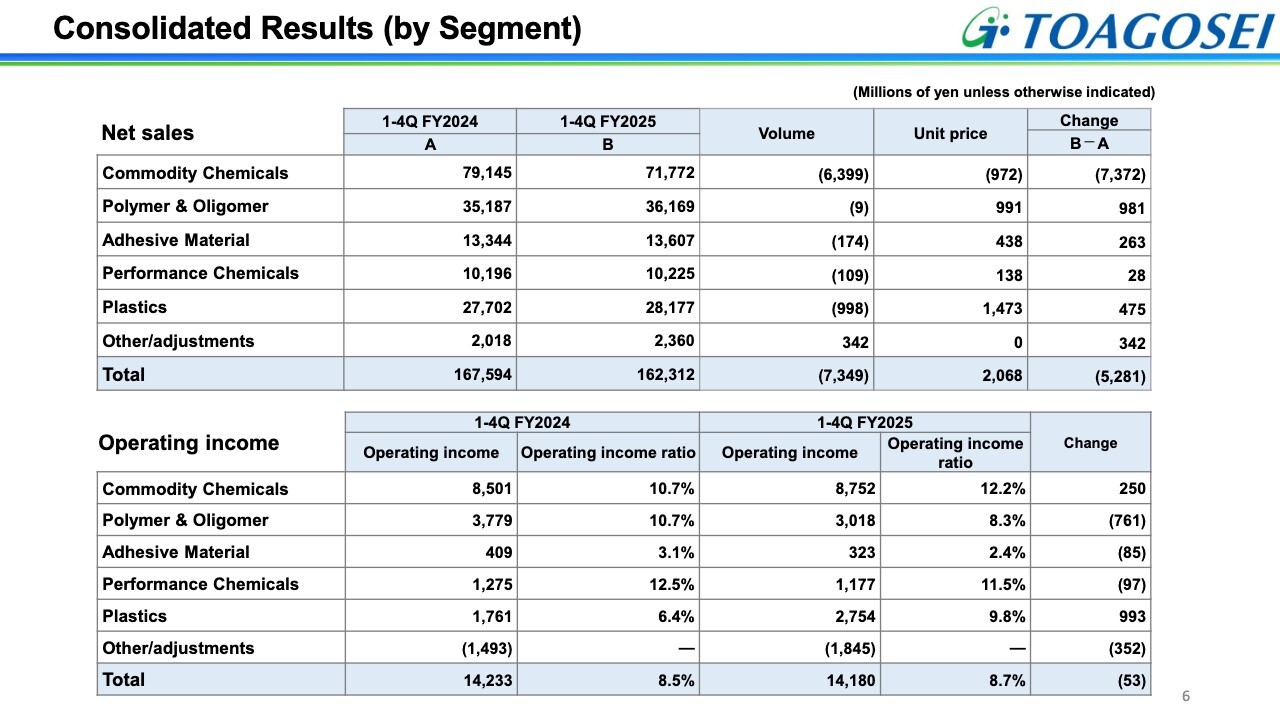

Consolidated Results (by Segment)

This slide presents our consolidated results by segment. Net sales were significantly lower in the Commodity Chemicals segment due to significant impact from the termination of contract manufacturing of some acrylic monomer products. In the Polymer & Oligomer segment, sales increased due to solid sales of products for cosmetics and semiconductors and price revisions for oligomers, but this was not enough to compensate for the overall decline in sales.

Operating income decreased in the Polymer & Oligomer segment due to a decline in lithium ion battery (LIB) binder production operations. A sharp rise in oligomer raw material prices also had an effect. At the same time, the Plastics segment posted a significant increase in profit due to improved profitability as well as strong sales of products to address aging sewage systems.

As a result, overall operating income remained at the level of the previous year.

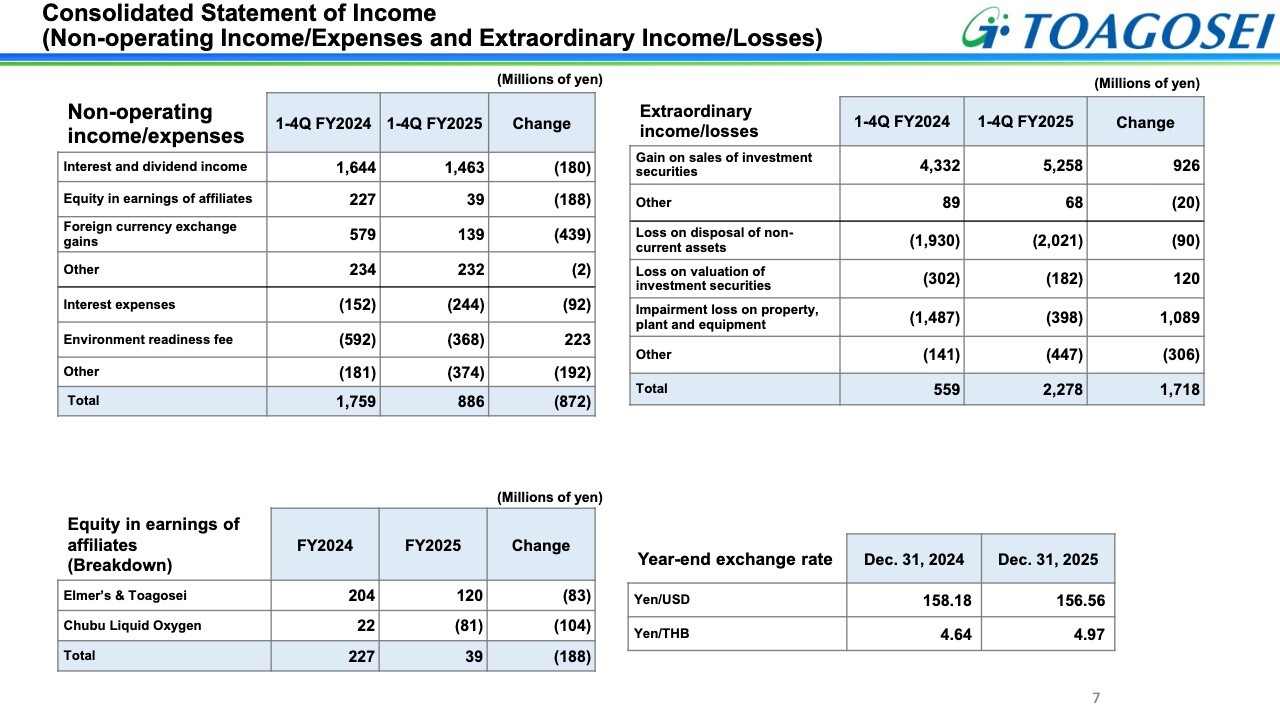

Consolidated Statement of Income (Non-operating Income/Expenses and Extraordinary Income/Losses)

This slide presents our non-operating income and extraordinary income. Non-operating income was significantly affected by a decrease in foreign exchange gains due to the strong yen. In extraordinary items, income increased significantly from the previous year, mainly due to the planned sale of cross-held shares and the absence of the impairment loss on Toagosei Singapore that occurred in the previous year.

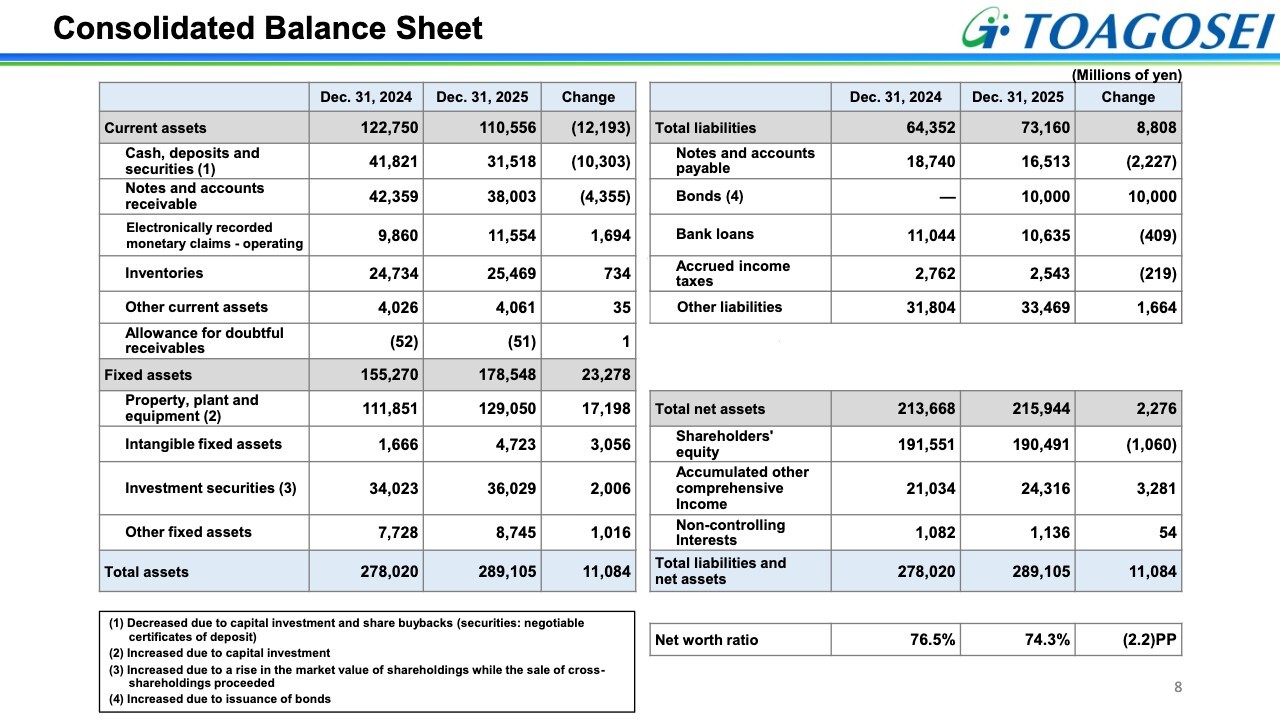

Consolidated Balance Sheet

This is our consolidated balance sheet. Looking at assets, our cash and deposits decreased due to proactive capital investment and share buybacks, while property, plant and equipment increased. Total assets increased from the previous year due to rising stock prices, despite the sale of cross-held shares.

Liabilities increased by approximately ¥8.8 billion, mainly due to the issuance of ¥10.0 billion in bonds. Net assets increased by approximately ¥2.2 billion due to higher share prices of investment securities. The equity ratio was 74.3%, down 2.2 points from the previous year.

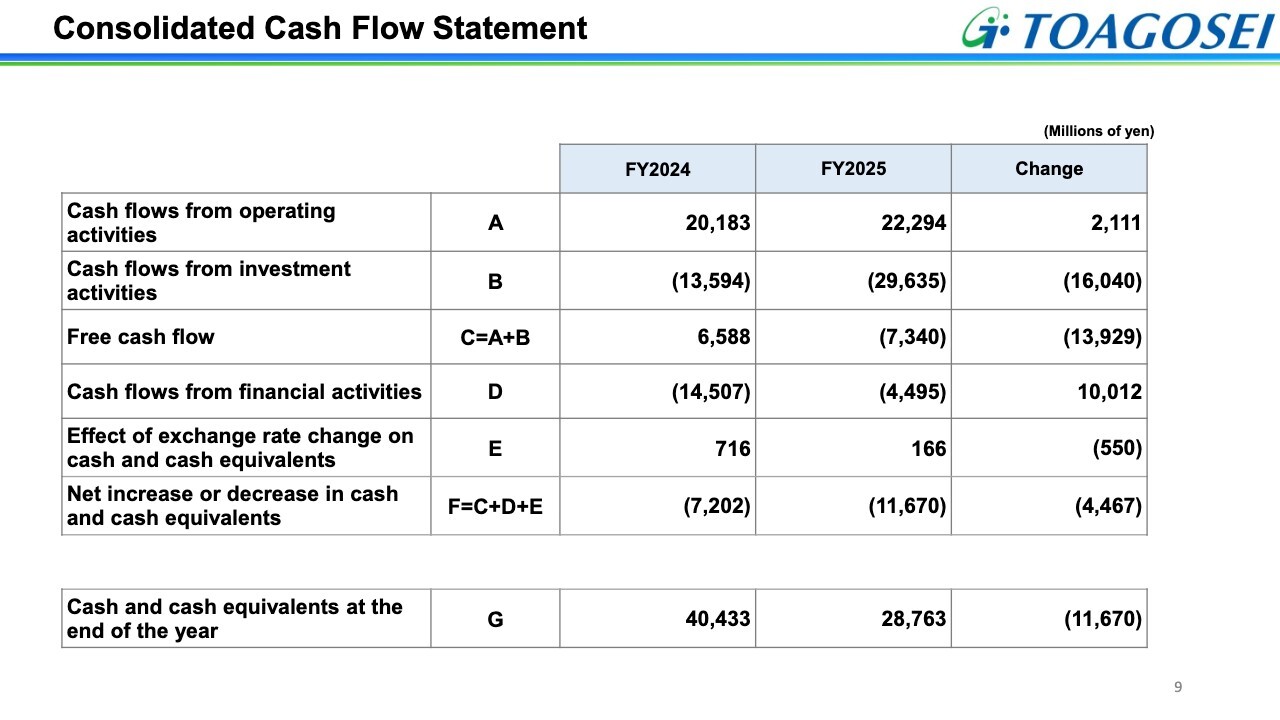

Consolidated Cash Flow Statement

This slide shows our consolidated cash flow statement. Operating cash inflow increased from the previous year due to the end of contract manufacturing and improvements to the cash conversion cycle.

Cash used in investment activities increased from the previous year due to proactive capital investment and an increase in outflows related to the dissolution of a U.S. joint venture. Cash used in financial activities declined, mainly due to the issuance of bonds.

As a result, cash and cash equivalents at the end of the period decreased by ¥11,670 million from the previous year.

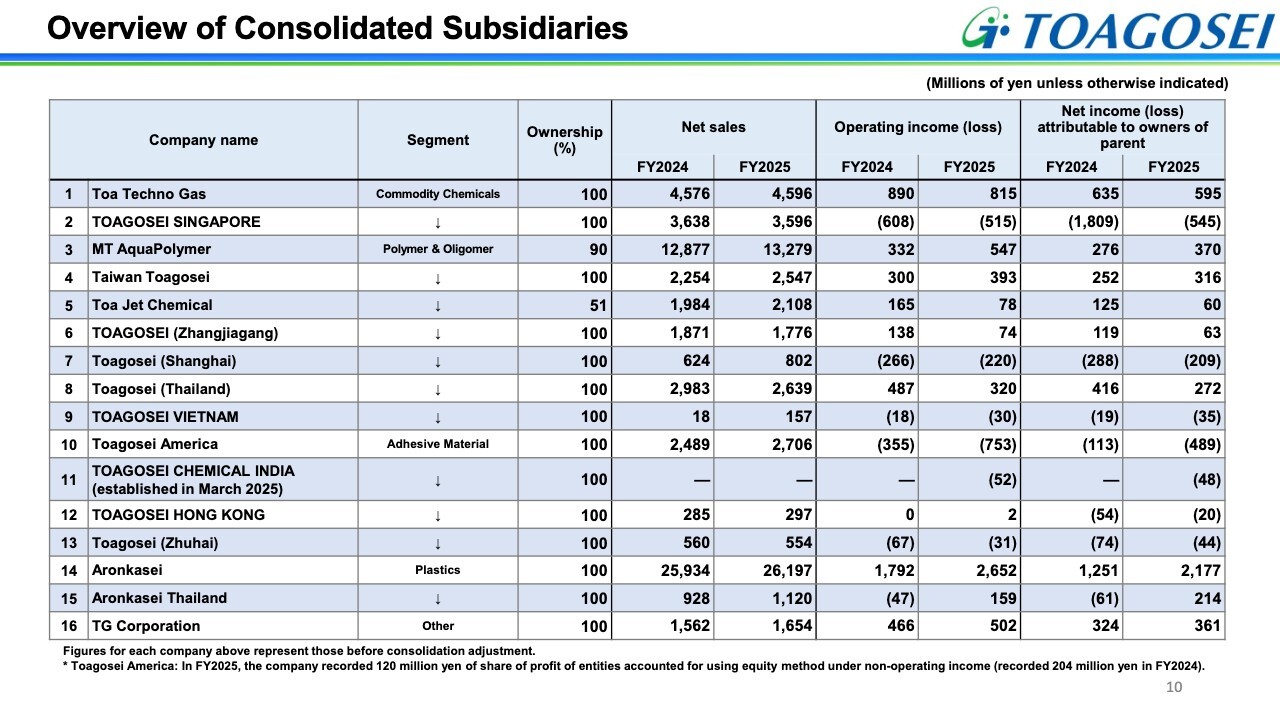

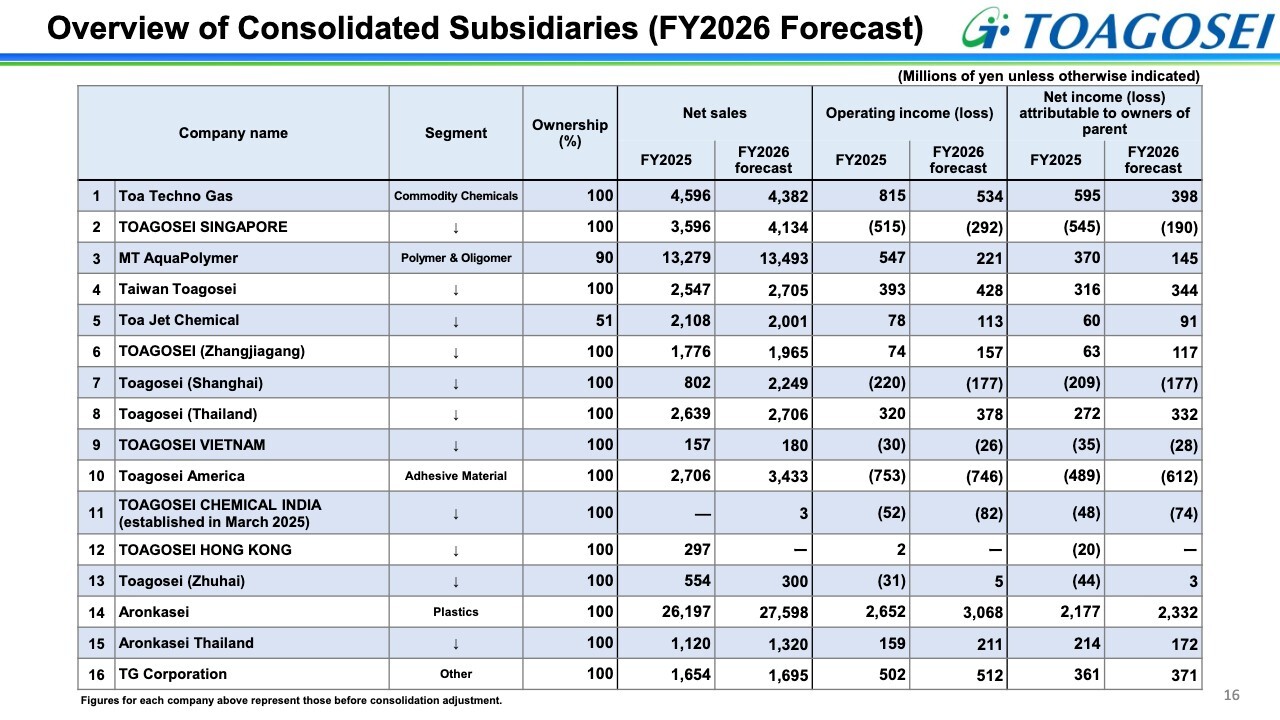

Overview of Consolidated Subsidiaries

The slide presents the results of our affiliates. I will discuss positive impacts in a year-on-year comparison of operating income for FY2025.

The third item on the list, MT AquaPolymer, reported an increase of approximately ¥200 million due to an increase in shipment volume to China and domestic improvement of profitability.

Tenth on the list is Toagosei America, in the Adhesive Material segment. It reported lower operating income due to higher costs related to change of structure following the joint venture dissolution.

For the second item on the list, Toagosei Singapore, operating income was in the red. However, the loss in FY2025 was less than that in the previous fiscal year due to the loss on valuation of the acrylic ester facility in FY2024.

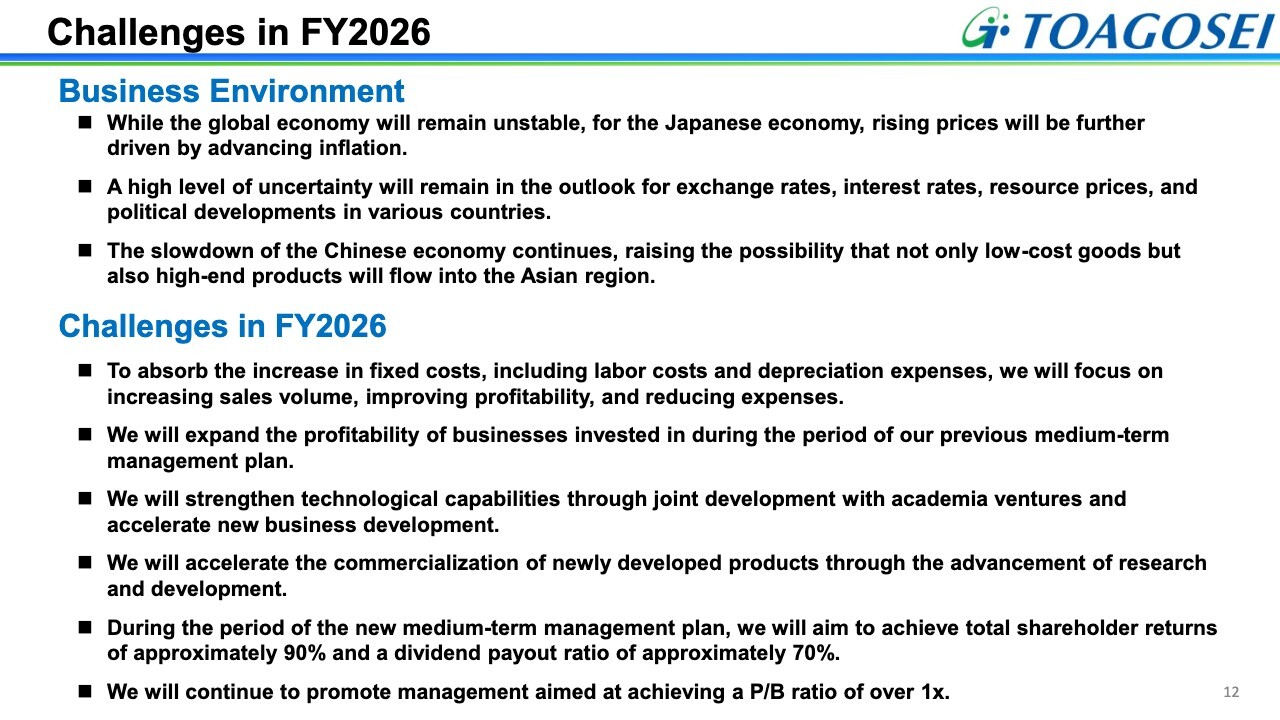

Challenges in FY2026

I would now like to talk about our forecast for the fiscal year ending December 31, 2026. Looking toward the business environment in 2026, we expect that instability will continue in the global economy and that price increases will become even more apparent in Japan.

The outlook for political trends in many countries remains unclear, and there are concerns over the possibility that not only inexpensive Chinese products but also high-end products will flow into the Asian region.

Against this backdrop, we believe that our key issues for FY2026 are increasing sales volume, improving profitability, and reducing expenses in order to absorb increases in fixed costs, as well as increasing the profitability of businesses in which we invested under the previous medium-term management plan.

Strengthening technological capabilities through joint development with academia and venture companies, and the early commercialization of newly developed products through R&D, are also key.

During the period of the new medium-term management plan, we intend to increase total shareholder returns to about 90% and the dividend payout ratio to about 70%. Through these measures, we aim to achieve a PBR of over 1x.

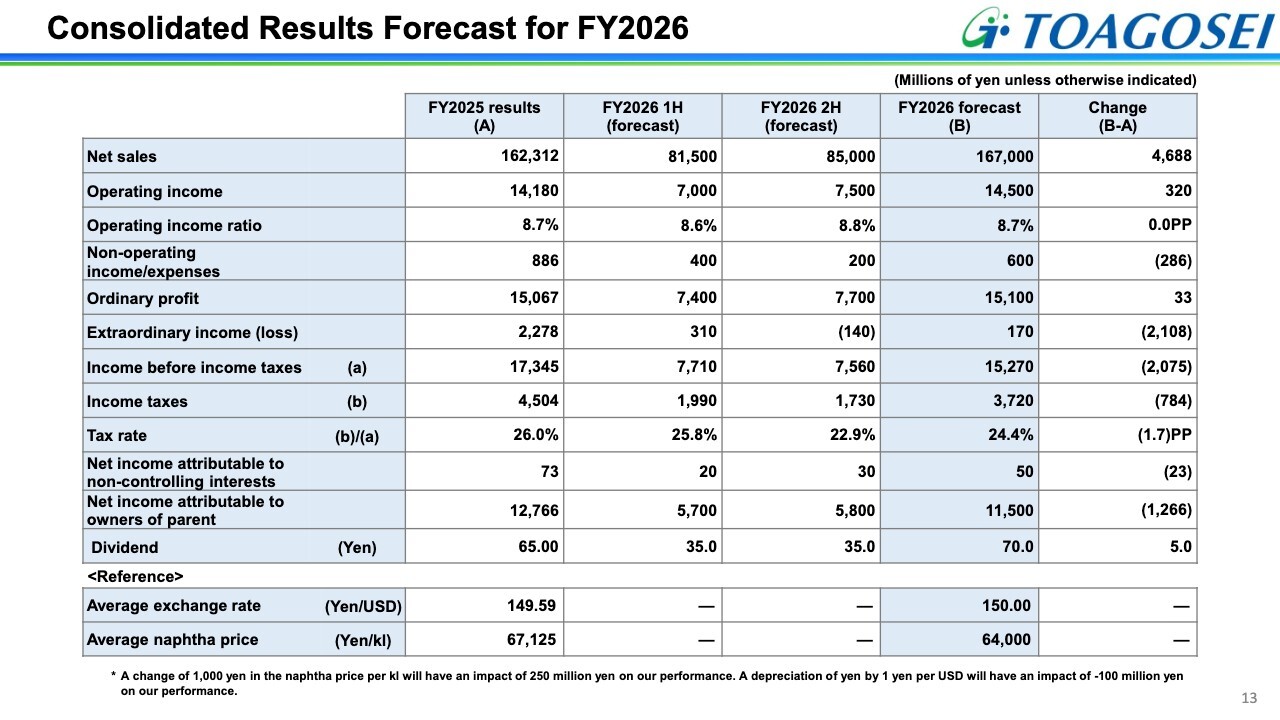

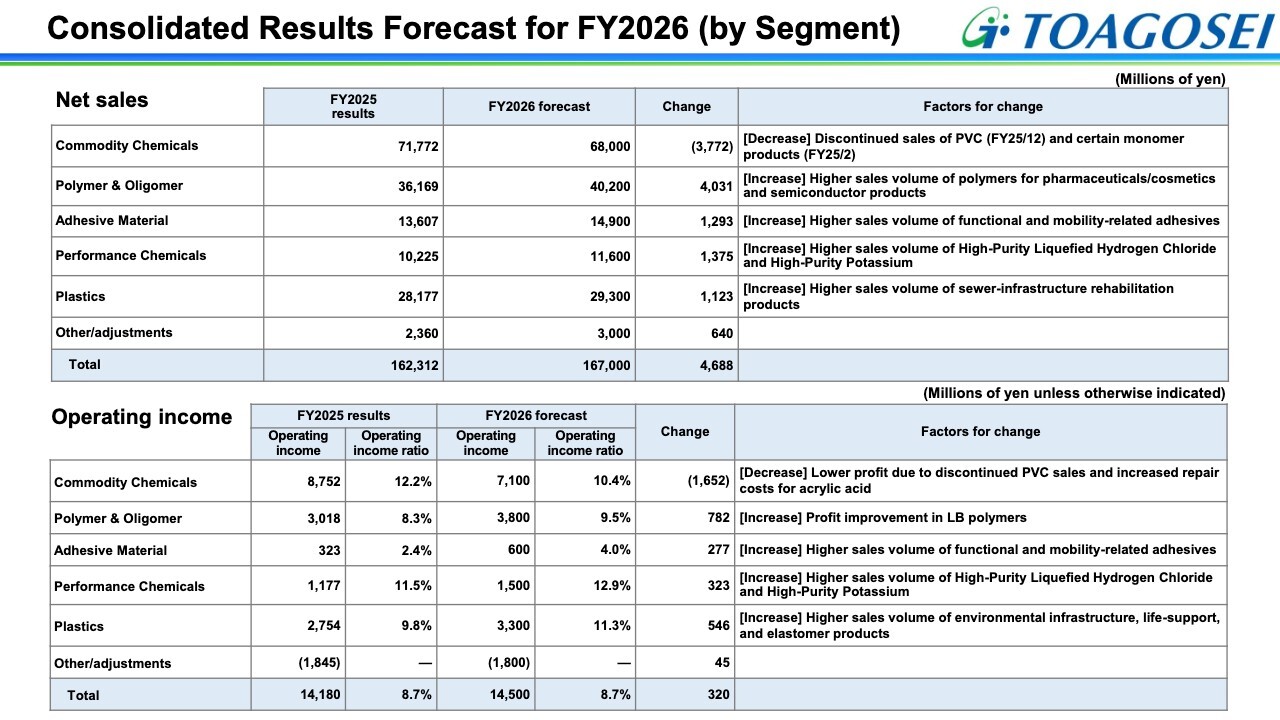

Consolidated Results Forecast for FY2026

This slide presents our consolidated results forecast for the fiscal year ending December 31, 2026. We expect to post higher sales and profit, with net sales of ¥167,000 million and operating income of ¥14,500 million.

Due to the fact that non-operating line does not factor in foreign exchange gains and that, within extraordinary items, gains on the sale of investment securities will decrease from the previous year, we project net income attributable to owners of the parent to be ¥11,500 million. We are increasing the annual dividend by ¥5 to ¥70 per share.

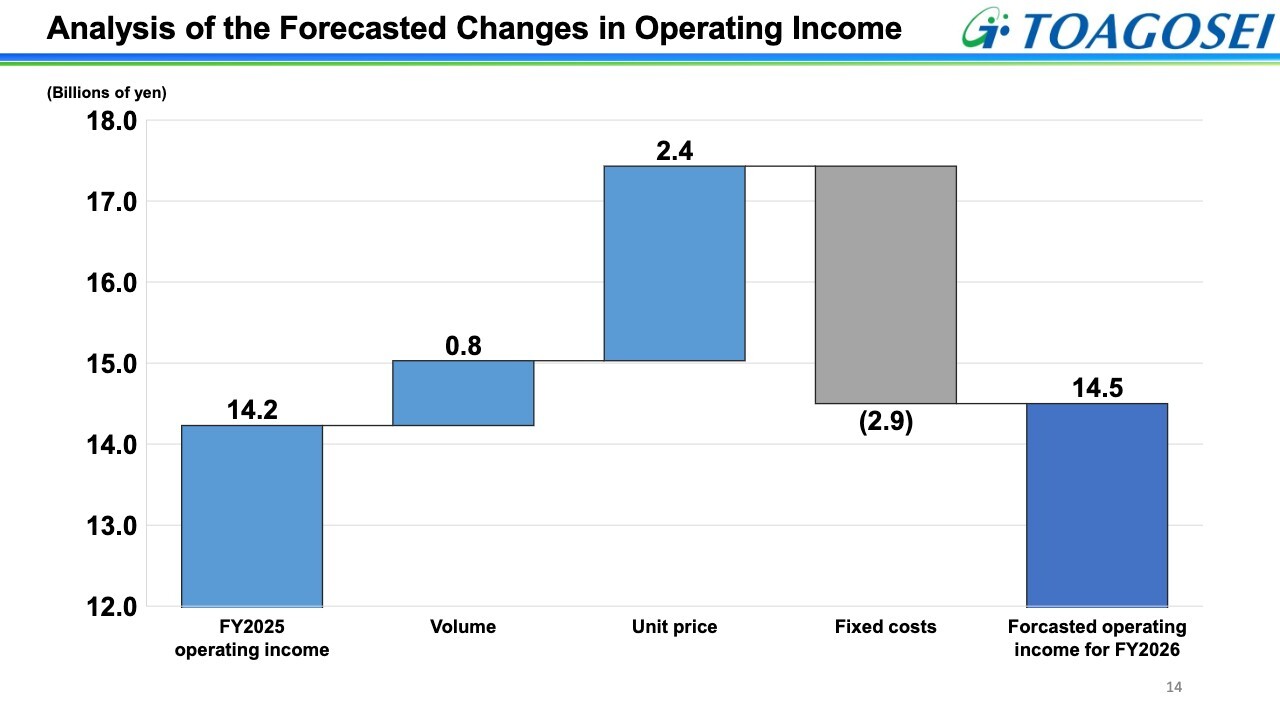

Analysis of the Forecasted Changes in Operating Income

This slide looks at changes in projected operating income. Appropriate price revisions resulted in a unit price gain of ¥2.4 billion, but a volume gain of only ¥0.8 billion. This is due to sales focused on profitability, despite the expectation of volume growth through sales expansion.

Looking at the ¥2.9 billion negative impact from fixed cost difference, we project an increase in labor costs resulting from proactive wage increases and an increase in depreciation expenses resulting from capital investment. As a result, we project operating income for the year ending December 31, 2026 to be ¥14.5 billion, up ¥0.3 billion from the previous year.

Consolidated Results Forecast for FY2026 (by Segment)

Here I would like to talk about our consolidated results forecast by segment. For the Commodity Chemicals segment, we forecast lower sales and profit due to the termination of contract manufacturing of polyvinyl chloride and the termination of contract sales of some monomer products, as well as the impact of large-scale periodic repairs in acrylic acid equipment.

In the Polymer & Oligomer segment, we expect an increase in sales due to higher sales volumes of polymers for medical, cosmetics, and semiconductor applications, as well as improved profitability of polymers for lithium-ion batteries.

In the Adhesive Material segment, we expect an increase in sales volume of functional and mobility-related adhesives as well as a change in structure in the U.S. We expect operating income to increase accordingly.

In the Performance Chemicals segment, we expect sales of high-purity liquefied hydrogen chloride to recover due to AI-related data centers and the recovery trend in semiconductors overall. We expect higher sales volume of high-purity potash for semiconductors to boost sales and profit.

In the Plastics segment, we expect sales and profit to increase due to expanded sales of products to address aging sewage systems and the improvement of profitability in environmental infrastructure and eco-material products. As a result, we expect sales and profit to increase overall.

Overview of Consolidated Subsidiaries (FY2026 Forecast)

This slide presents an overview of our consolidated subsidiaries.

The second subsidiary on the list, Toagosei Singapore, is expected to post year-on-year increases in sales and profit due to volume growth from sales to new customers and fixed cost reductions. At the same time, we expect continuation of the severe situation caused by the inflow of inexpensive Chinese goods into the Asian region. We will examine how to address this situation from various angles.

For the tenth subsidiary on the list, Toagosei America, we expect an increase in sales due to a change in the company’s structure as a result of the dissolution of its joint venture. However, we also expect operating income to remain at the level of the previous year due to increased advertising and marketing expenses aimed at increasing market share.

The seventh subsidiary on the list, Toagosei (Shanghai), is expected to increase sales and profit due to the transfer of trading areas of Toagosei (Zhuhai) and Toagosei Hong Kong and expanded sales of polymers for batteries, semiconductors, and pharmaceuticals.

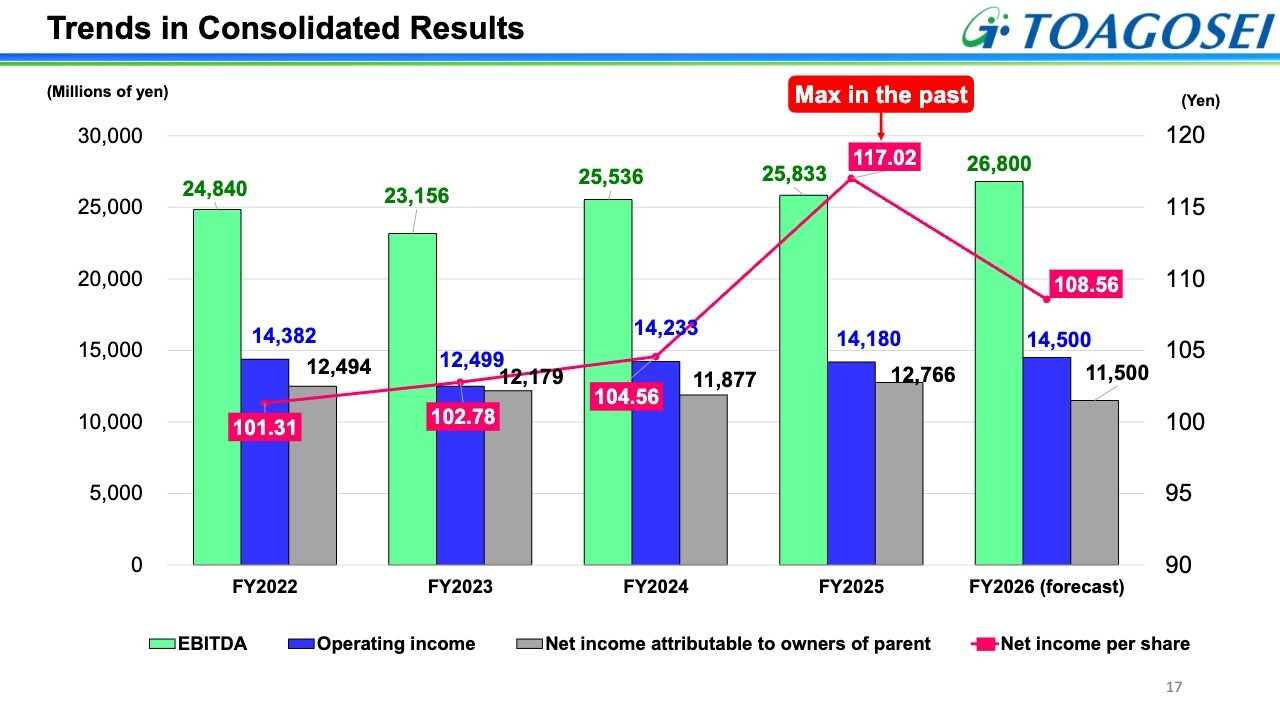

Trends in Consolidated Results

The graph on this slide shows EBITDA, operating income, net income attributable to owners of the parent, and net income per share.

Operating income, shown in blue, has remained stable despite an increase in labor costs due to wage increases and an increase in depreciation expenses associated with proactive capital investment. EBITDA, shown in green, is on a generally upward trend. Net income per share for FY2025 was ¥117.02, a record high.

This concludes my explanation of our financial results. Next is a discussion of our medium-term management plan.

Contents

I would like to explain our new medium-term management plan, covering the three-year period from FY2026 to FY2028. As outlined on the slide, I will review our previous medium-term management plan and explain the new medium-term management plan, focusing on growth and financial strategies.

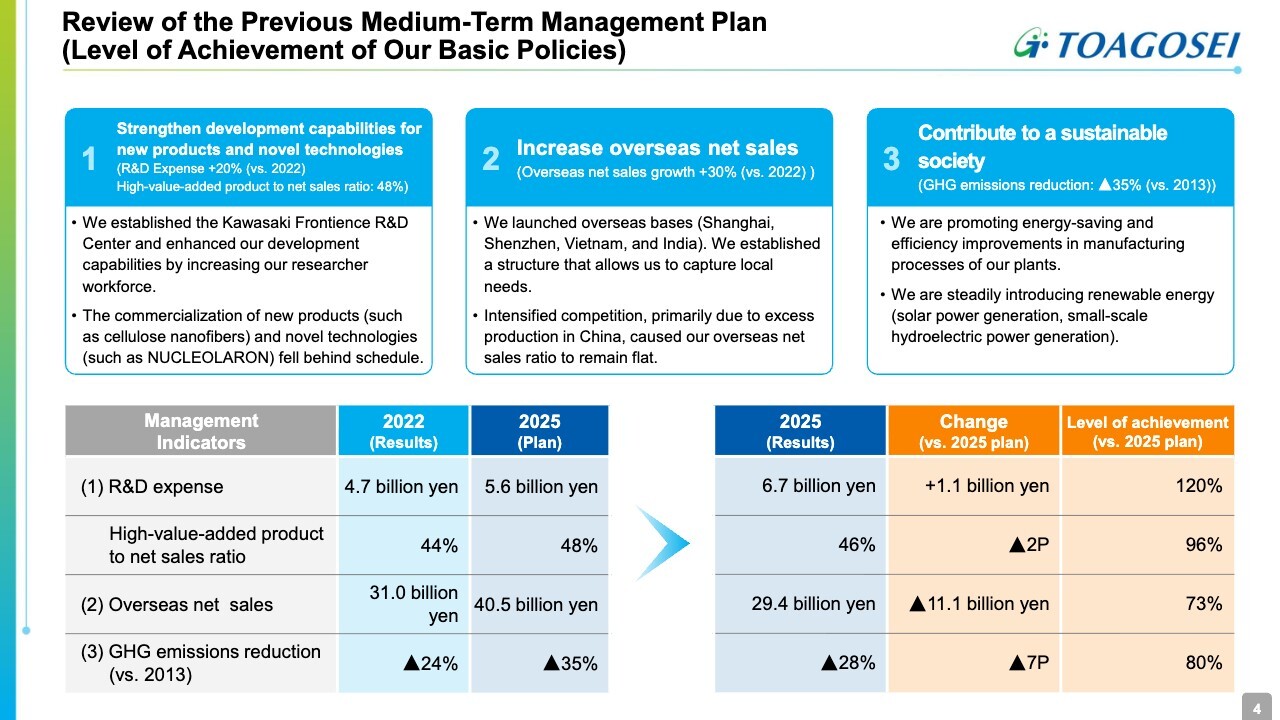

Review of the Previous Medium-Term Management Plan (Level of Achievement of Our Basic Policies)

Here I will review our previous medium-term management plan. The slide describes the level of achievement of the three basic policies of the previous medium-term management plan.

Under the first basic policy, "strengthening development capabilities for new products and novel technologies," we strengthened our development capabilities by opening a new research facility in Kawasaki and increasing the researcher workforce.

As shown in the table at the bottom of the slide, R&D expenses totaled ¥6.7 billion in FY2025, achieving the target of the medium-term management plan. However, the planned commercialization of new products and technologies was delayed, and the net sales ratio of high value-added products fell slightly short of the target.

Regarding the second point, "Increase overseas net sales," during the three years of the previous medium-term management plan we established bases in Shanghai, Shenzhen, Vietnam, and India and established structures to capture local needs. However, under intensified competition mainly due to excess production in China, our achievement rate was 73% and our overseas net sales ratio did not improve.

As for the GHG emissions reduction set forth under the third item, "Contribute to a sustainable society," we have promoted energy conservation and efficiency improvements at our plants along with the introduction of renewable energy. However, as full-scale adoption will occur in 2026, we have only achieved 80% of the target.

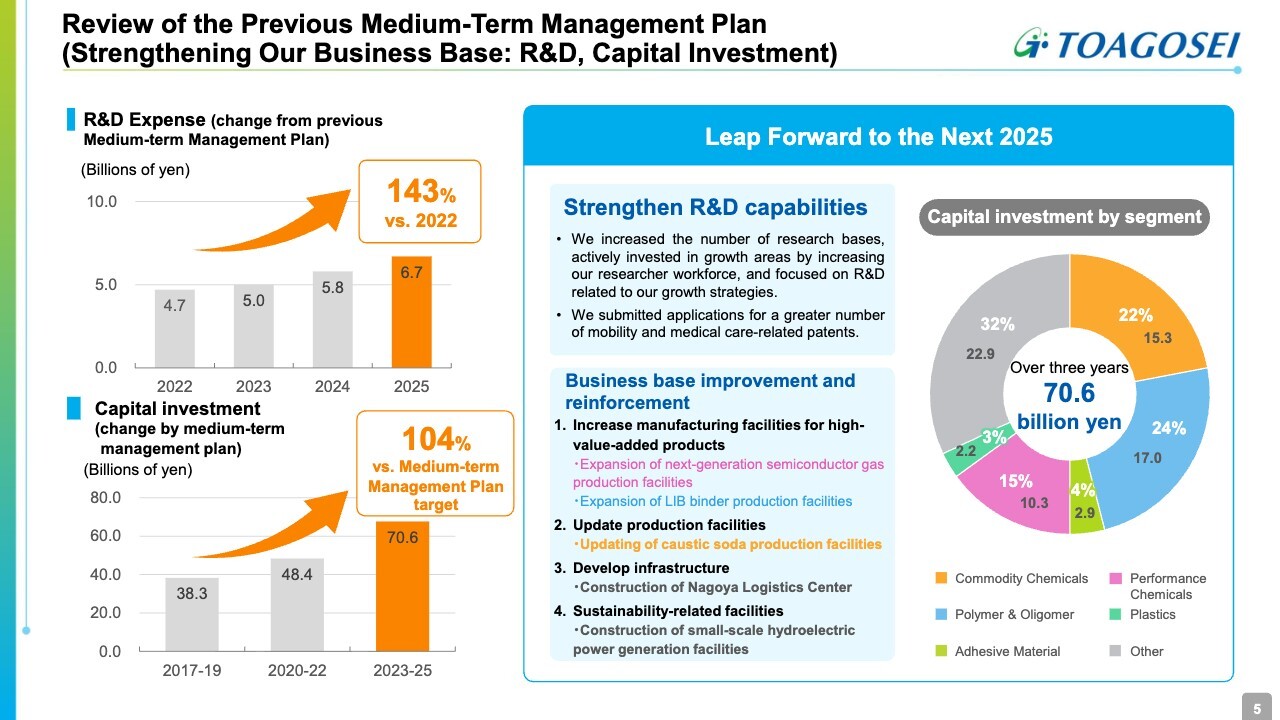

Review of the Previous Medium-Term Management Plan (Strengthening Our Business Base: R&D, Capital Investment)

In the strengthening of our business base, we have focused on R&D and capital investment. R&D expenses have been increasing every year, growing to 143% of FY2022 expenses in FY2025. Our net sales-R&D ratio reached 4%.

Focusing on development in growth areas, we are increasing our number of mobility- and medical care-related patent applications. We aim to achieve early output in all of our research themes.

Capital investment totaled ¥70.6 billion over the three-year period of the medium-term management plan, exceeding the plan’s target of ¥68.0 billion.

Investments were focused on the enhancement of manufacturing facilities for high value-added products, updates to existing facilities, and enhancement of competitiveness through infrastructure development, with growth investment generally accounting for about half of the investment in each segment. Through such balanced investment, we worked to strengthen our business base.

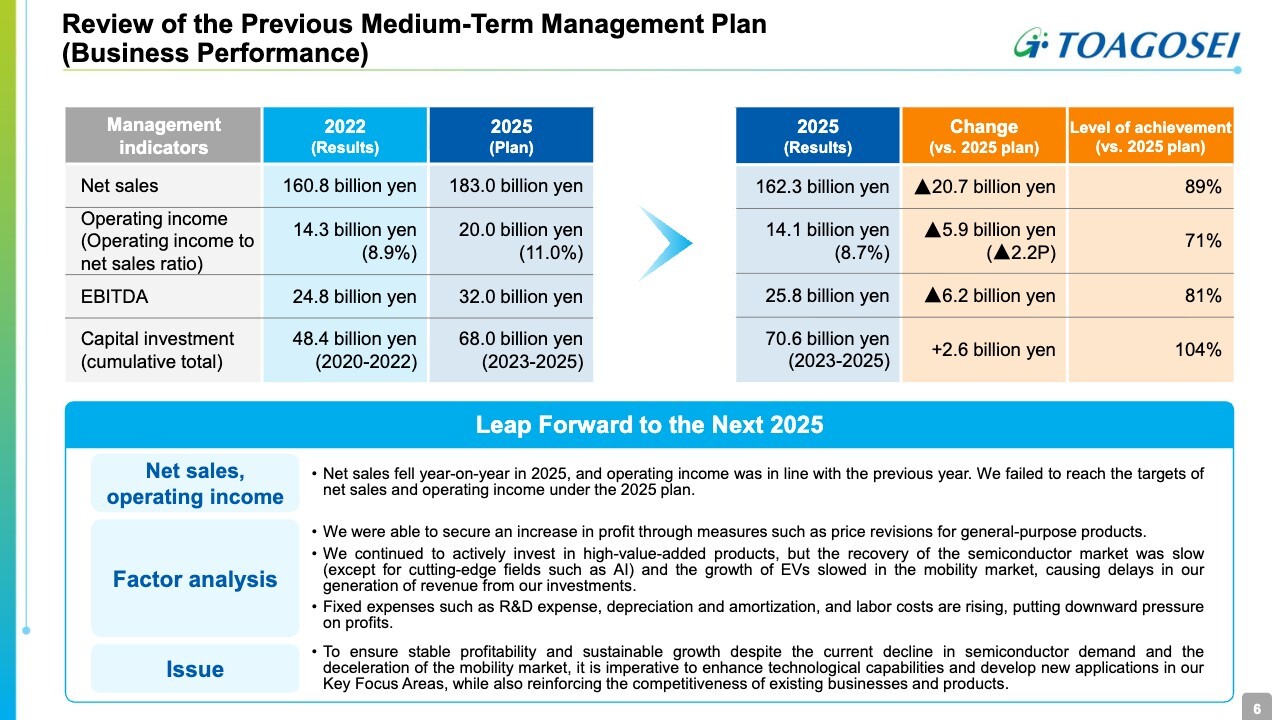

Review of the Previous Medium-Term Management Plan (Business Performance)

This slide looks at the level of achievement of our business results. Net sales and operating income fell short of medium-term management plan targets.

For general-purpose products, we achieved our medium-term management plan targets through means including revisions to product prices. However, high-value-added products were impacted by the slow recovery of the semiconductor market and the slowdown of EV growth. Growth in operating income slowed due to increased fixed costs including R&D expenses, depreciation expenses, and labor costs.

To secure stable profitability and sustainable growth, we plan to enhance our technological capabilities in key focus areas, develop new applications, and reinforce the competitiveness of existing businesses and products.

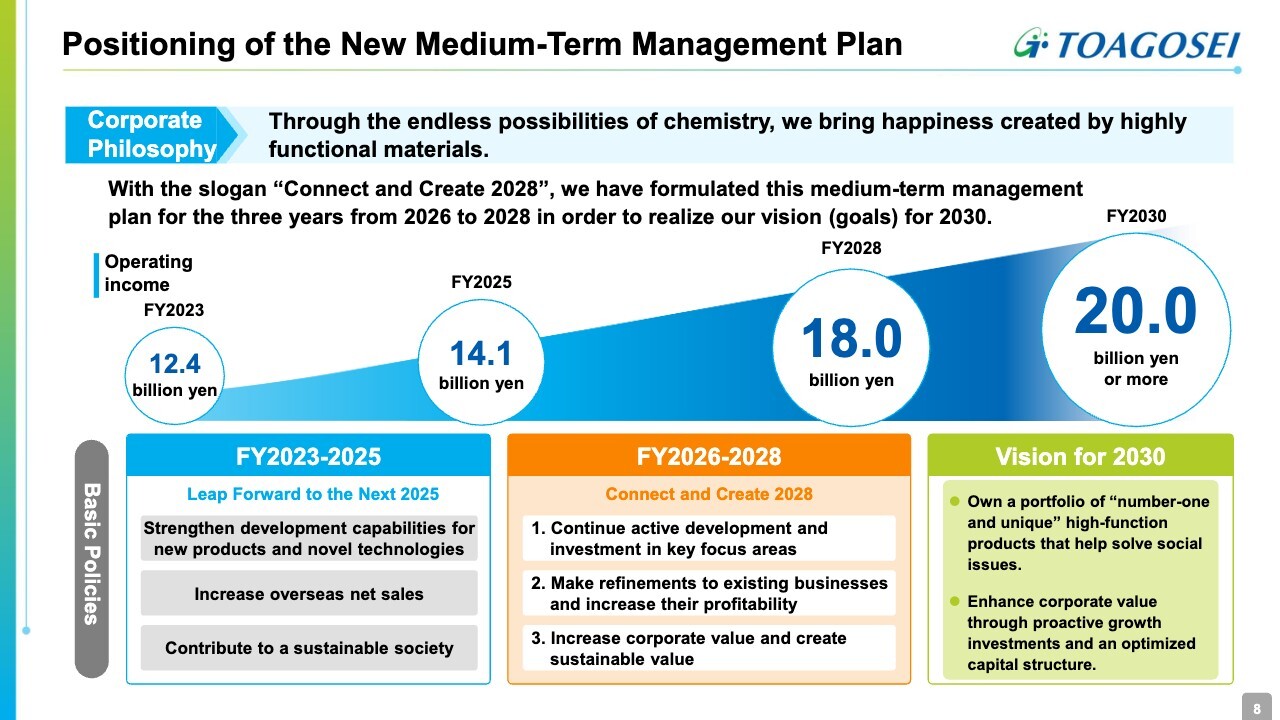

Positioning of the New Medium-Term Management Plan

I would now like to discuss our new medium-term management plan.

The new medium-term management plan is a three-year plan under the slogan “Connect and Create 2028.” It is aimed at achieving the vision we hold for FY2030, expressed as “Own a portfolio of ‘number-one and unique’ high-function products that help solve social issues” and “Enhance corporate value through proactive growth investment and an optimized capital structure.”

The plan incorporates our intention to advance development in cooperation with customers, academia, venture companies, and varied internal divisions to quickly and solidly pioneer the future.

We will take action grounded in the three basic policies shown at bottom on the slide, aiming for operating income of ¥18.0 billion in FY2028 and ¥20.0 billion or more in FY2030.

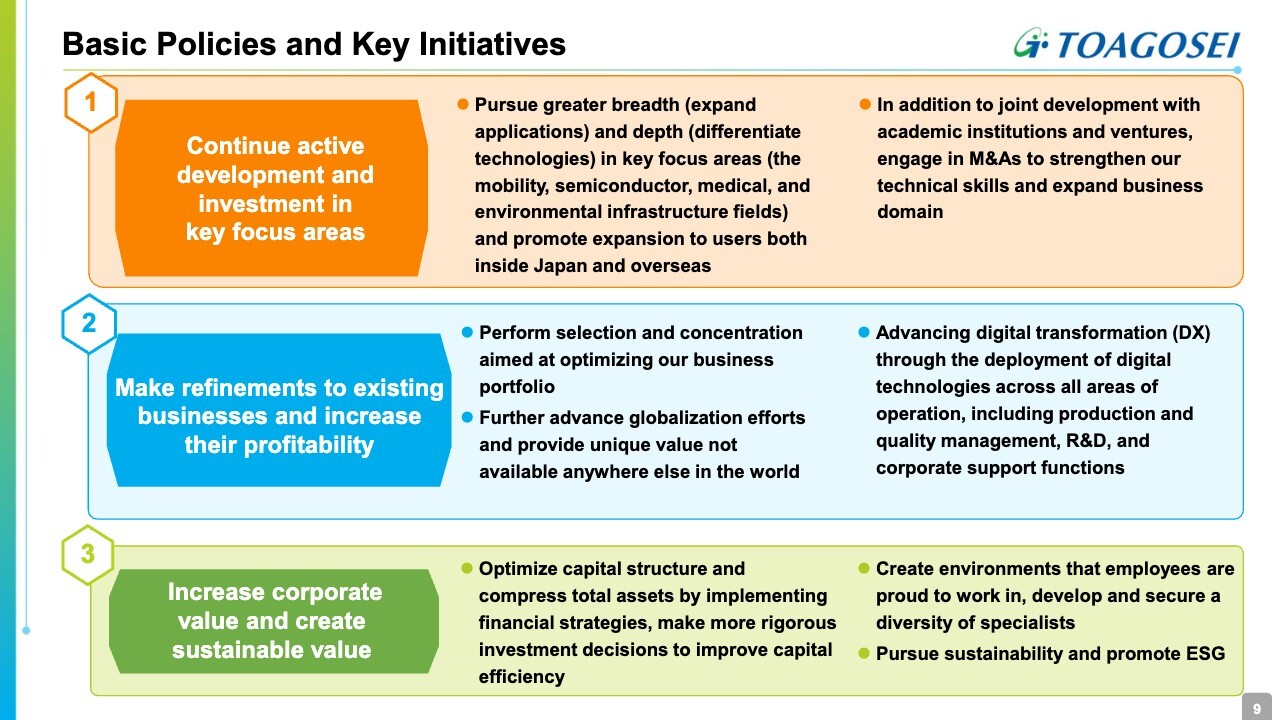

Basic Policies and Key Initiatives

Under the three basic policies that I mentioned, we will implement the key initiatives shown on the slide.

The first is “Continued active development and investment in key focus areas.”

The key focus areas of mobility, semiconductors, medical, and environmental infrastructure are domains encompassing many themes. We will pursue expansion through development of applications and pursue depth through technological differentiation, and will deploy these to users at home and abroad.

In addition to joint development with academia and venture companies, we will also engage in M&A and other means to strengthen our technological capabilities and expand our business domain.

With respect to the second initiative, “Make refinements to existing businesses and increase their profitability,” we will engage in business portfolio optimization, global expansion, and business transformation through DX.

For the third initiative, “Increase corporate value and create sustainable value,” financial and human capital strategies will be key. This will be discussed in more detail later.

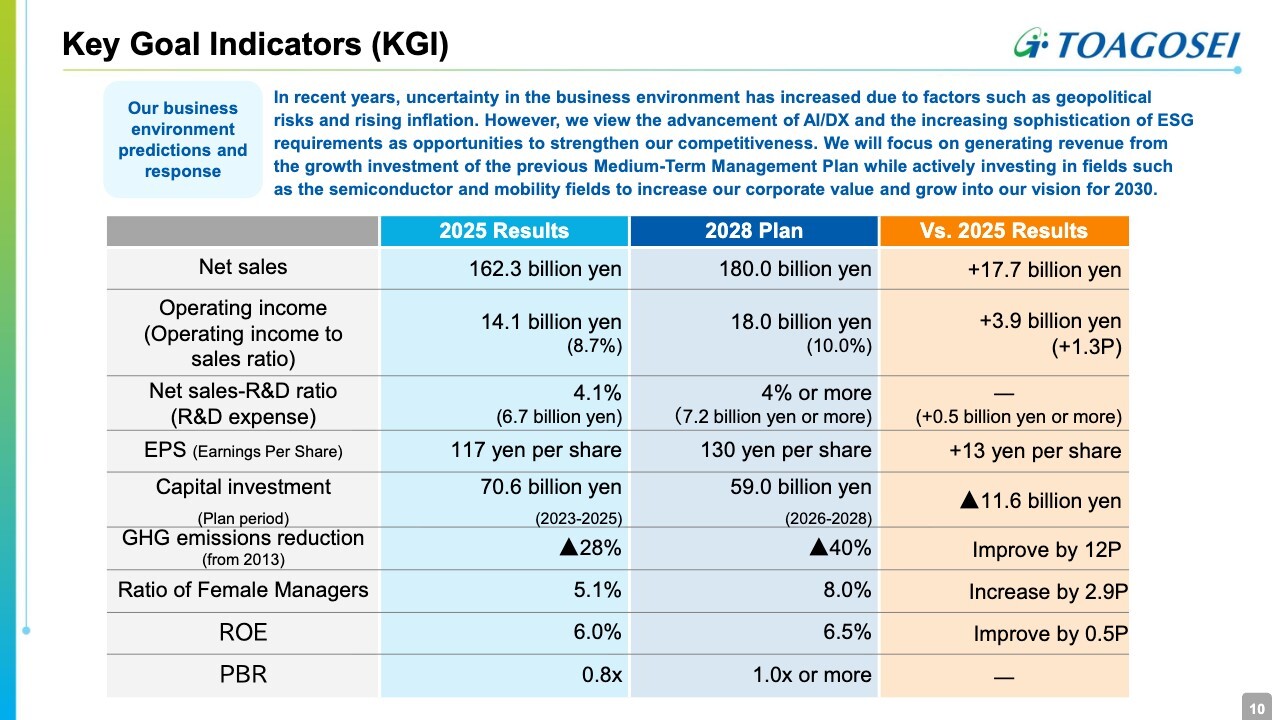

Key Goal Indicators (KGI)

This slide presents key goal indicators in the new medium-term management plan. Under expectations for a highly uncertain business environment, we aim to enhance our corporate value by making proactive investments in the semiconductor and mobility fields, while focusing on generating profit from growth investments made under the previous medium-term management plan.

Under the new medium-term management plan, we aim to achieve net sales of ¥180.0 billion, operating income of ¥18.0 billion, a net sales-R&D ratio of 4% or higher, EPS of ¥130, capital investment of ¥59.0 billion over three years, a GHG emission reduction rate of −40% compared to FY2013, a ratio of female managers of 8%, ROE of 6.5%, and PBR of 1.0x or more.

We expect operating income to increase by ¥3.9 billion over FY2025, absorbing the rise in fixed costs. The capital investment amount was set through careful selection and was reduced from the amount in the previous medium-term management plan.

In the medium-term management plan, we intend to focus on building our ability to efficiently generate profit and, in particular, to achieve a PBR of 1.0x or more through measures aimed at increasing our share price.

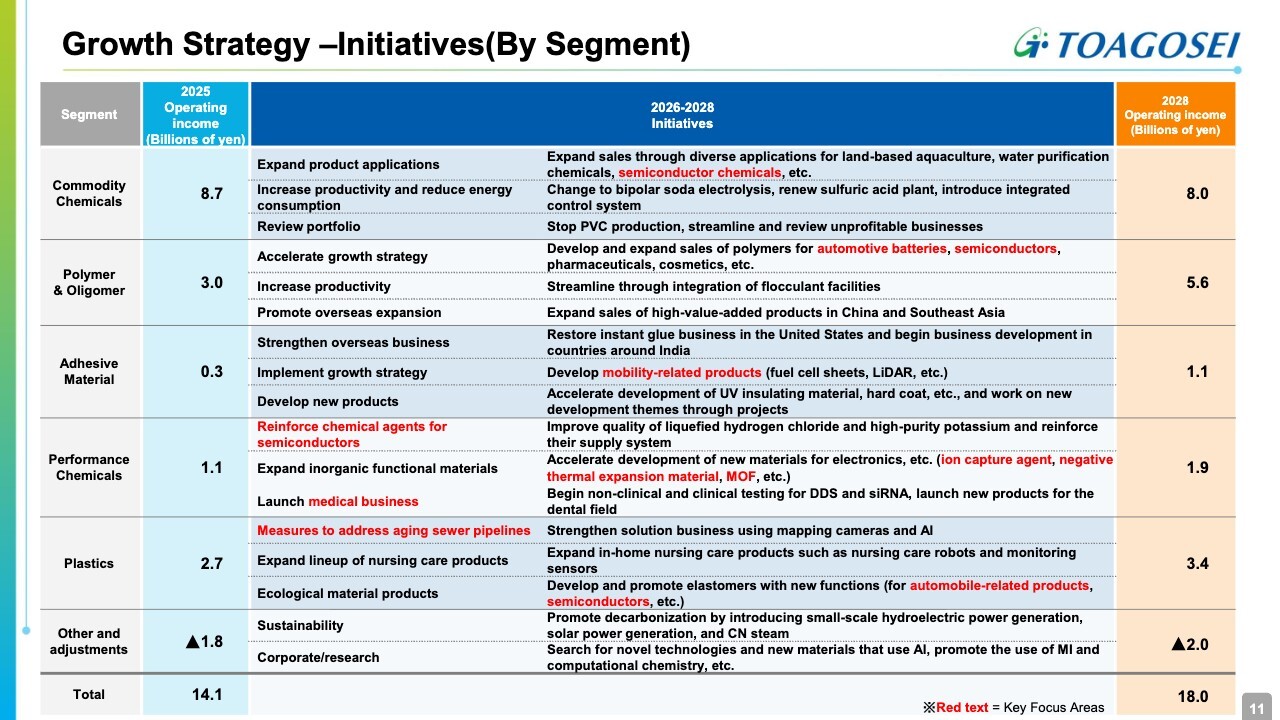

Growth Strategy – Initiatives (By Segment)

The slide looks at our growth strategy by segment. Red text represents our four areas of focus: semiconductors, mobility, medical, and environmental infrastructure.

In the Commodity Chemicals segment, which has been a driver of performance, we expect operating income to decline from FY2025 as a result of portfolio review under the new medium-term management plan, which will focus on selection and concentration toward high value-added products.

At the same time, we aim to achieve total operating income of ¥18.0 billion by solidly advancing the reinstatement of high value-added product groups. Within our high-performance product groups, the Polymer & Oligomer segment posted the largest increase in profit. The key to accelerating our growth strategy is to expand applications and customers in the automotive battery and semiconductor fields, conduct development and expand sales of polymers for pharmaceuticals and cosmetics, and further advance overseas expansion.

For the Adhesive Material segment, we are focusing on rebuilding our U.S. business and developing mobility-related products. In the Performance Chemicals segment business, we will focus on strengthening the quality of and our supply structure for chemical agents for semiconductors, as well as developing new materials and launching a medical business.

In the Plastics segment, in addition to expanding sales of products for aging sewage systems, we aim to establish a firm position by developing the solutions business, through means such as using mapping cameras and AI to identify repair locations.

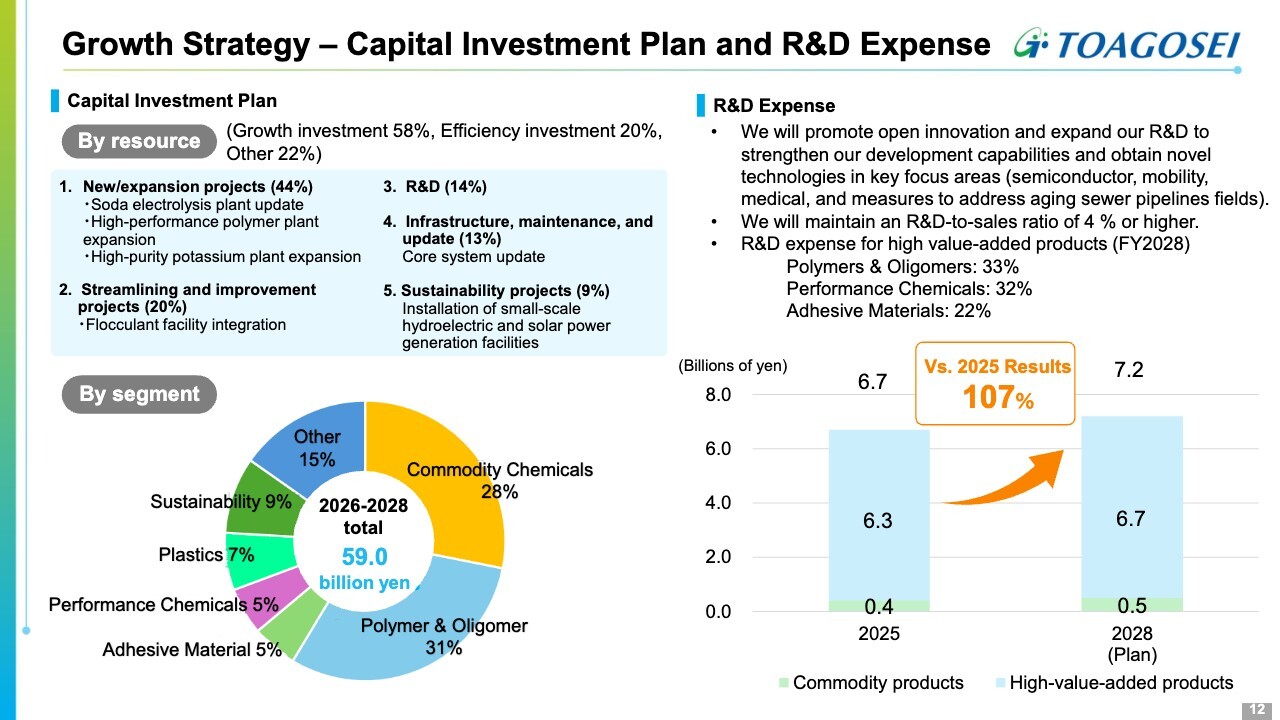

Growth Strategy – Capital Investment Plan and R&D Expenses

The slide shows the capital investment plan and R&D expenditures that are keys to our growth strategy.

We set the content of capital investment through careful selection and limited the amount to ¥59.0 billion over the three-year period, 80% of the level in the previous medium-term management plan. The content of the investment is aggressive, breaking down to 58% growth investments and 20% efficiency investments. The investment also features a roughly 1:1 balance between high value-added product groups and general-purpose products.

New investment includes expansion of our high-performance polymer plant primarily for pharmaceuticals and cosmetics, expansion of our high-purity potash plant for semiconductors, integration of the flocculants facility through the takeover of the flocculants business, and the updating of our core systems through the introduction of SAP S/4 HANA.

Regarding R&D expenses, we will proactively utilize outside resources to strengthen our development capabilities and acquire new technologies in key focus areas including mobility, semiconductors, medical, and environmental infrastructure. We plan to increase our net sales-R&D ratio to at least 4% and to expand R&D expenses in FY2028 to ¥7.2 billion, or 107% of the FY2025 level.

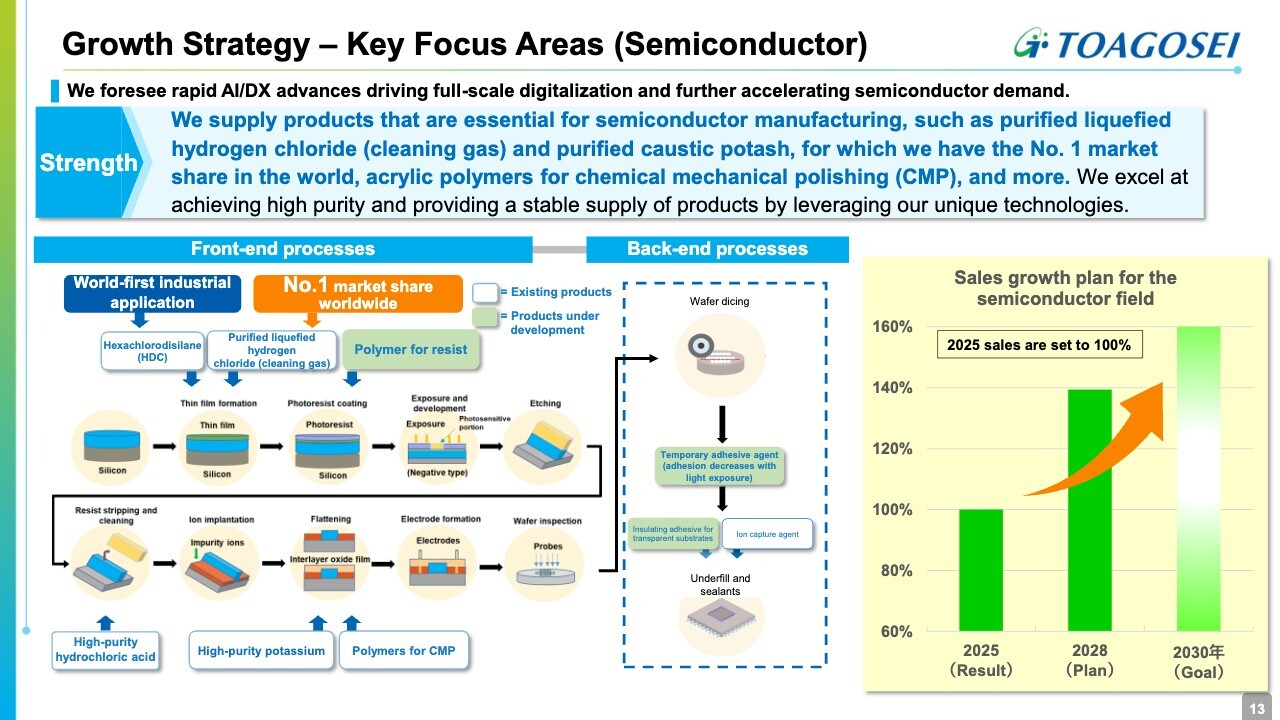

Growth Strategy – Key Focus Areas (Semiconductor)

I will now discuss the four key focus areas that support our growth strategy: semiconductors, mobility, medical, and environmental infrastructure. First is the semiconductor area, which we have positioned as a growth driver.

In terms of the business environment, we expect demand for semiconductors to accelerate as the use of AI and DX advances. We offer products essential for semiconductor manufacturing, such as high-purity liquefied hydrogen chloride and high-purity caustic potash – both products for which we boast the No. 1 share in the global market – as well as acrylic polymers for CMP.

Our strength lies in our ability to provide high purity, stable supply, and products that meet customer needs. As shown on the slide, our products are used in a number of processes. There is also potential to develop many new applications. Our sales expansion plan for 2028 aims for a 1.4-fold increase compared to 2025.

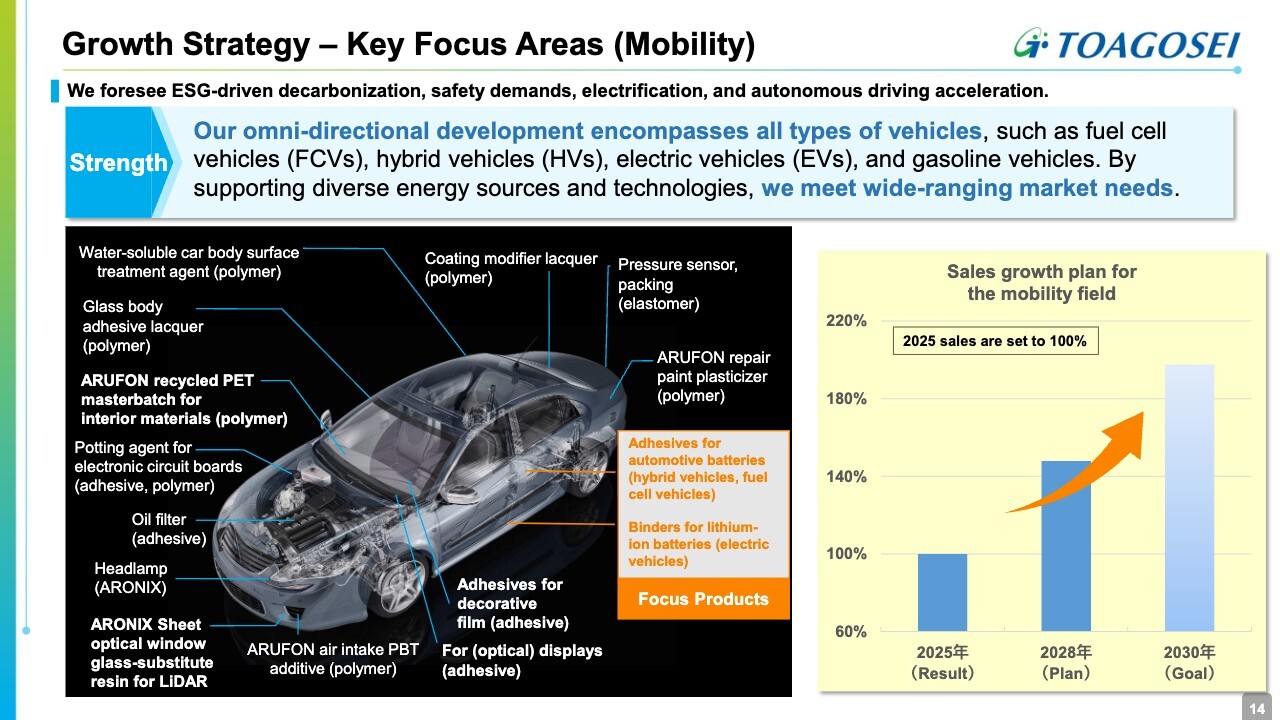

Growth Strategy – Key Focus Areas (Mobility)

Our second growth driver is the mobility area. In terms of the business environment, we expect that electrification, automated driving, and the adoption of environmentally friendly products will continue to progress in line with increasing demands for decarbonization and safety.

Our strength is our all-round development that targets types of vehicles, including fuel cell vehicles (FCVs), hybrid vehicles (HVs), electric vehicles (EVs), and gasoline vehicles. Based on our proprietary technologies and through their adoption in core products, we constantly meet requests for technological improvement and thereby hold competitive advantage.

In the medium-term management plan, we will advance new development with a focus on improving the performance of products for hybrid vehicles, for which the market is expanding, and for EVs, for which use is expected to expand in the future. We will move forward with our plans to expand sales approximately 1.5-fold from 2025 by 2028.

Growth Strategy – Key Focus Areas (Medical)

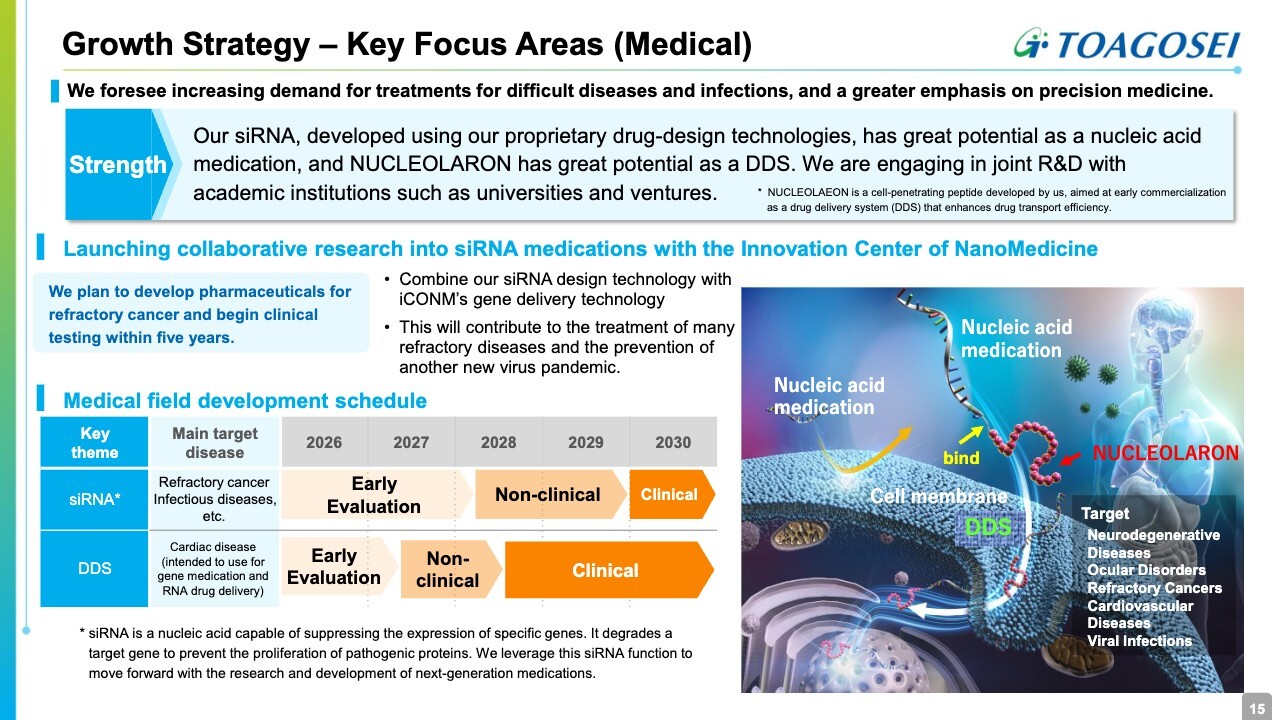

This slide looks at the medical area, which we expect to become a new growth driver.

Our siRNA, driven by drug-design technologies born from our research, holds great potential as a nucleic acid medicine, while our NUCLEOLARONE holds great potential as a drug delivery system (DDS). We are promoting joint development in collaboration with several academic bodies and venture companies in Japan and abroad.

Our products are expected to work as more effective nucleic acid drugs imbued with DDS functionality to precisely deliver drugs within target cells.

Details of our joint development with the Innovation Center of NanoMedicine (iCONM) are publicly available. We are currently collaborating on the development of drugs for the treatment of intractable cancers.

Co-development targeting several other diseases is also progressing. During the period of the medium-term management plan, we plan to advance many non-clinical studies, with some advancing to clinical trials. We expect these initiatives to mark our first full-scale forays into the medical area.

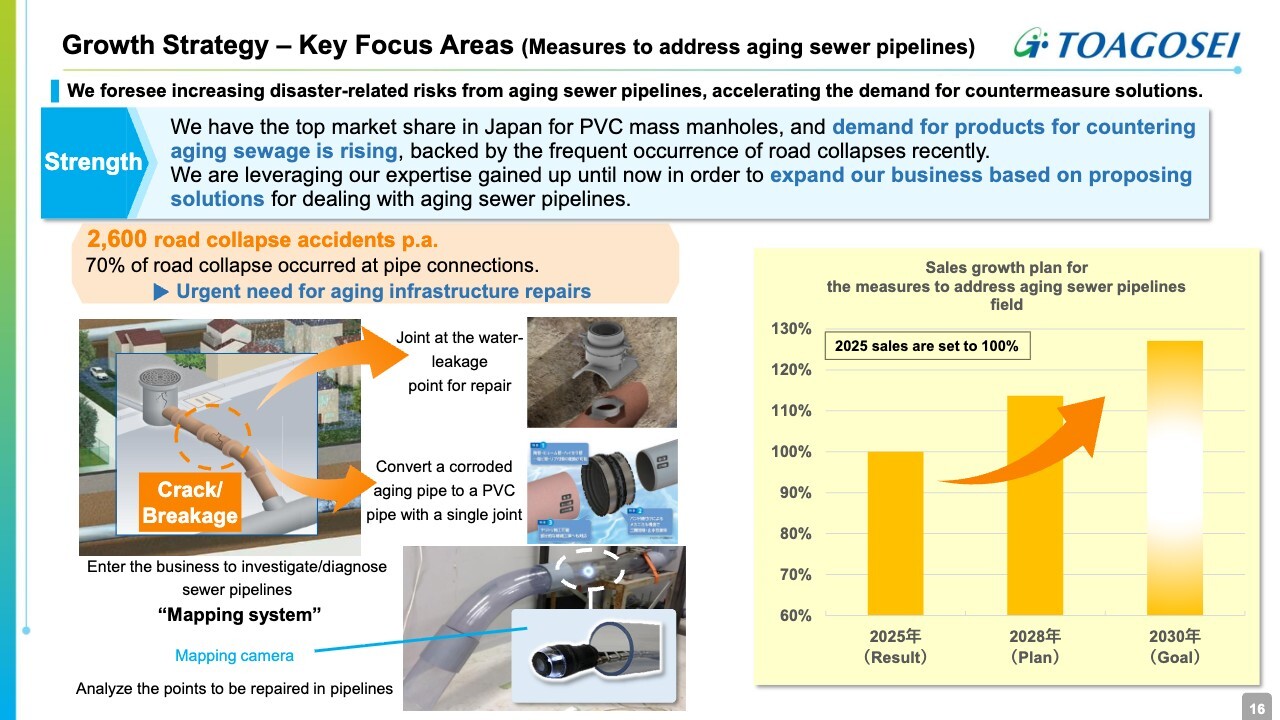

Growth Strategy – Key Focus Areas (Measures to address aging sewer pipelines)

The fourth key focus area is environmental infrastructure systems, particularly products to address aging sewage systems.

A year ago, a tragic road collapse accident occurred in Saitama Prefecture due to a broken sewer pipe. Japan experiences 2,600 road collapse accidents per year, with 70% occurring at lateral pipes connecting to main pipes.

It is expected that sewer pipes will continue to age rapidly, which makes measures to repair aging infrastructure urgently needed. Aronkasei offers a wide range of products to address aging sewage systems, enabling efficient repair in line with the nature of damage.

We are also evaluating a mapping system utilizing cameras and AI. This is expected to further improve repair efficiency by identifying damaged areas and necessary products without drilling. We plan to expand sales by approximately 115% compared with 2025 in 2028.

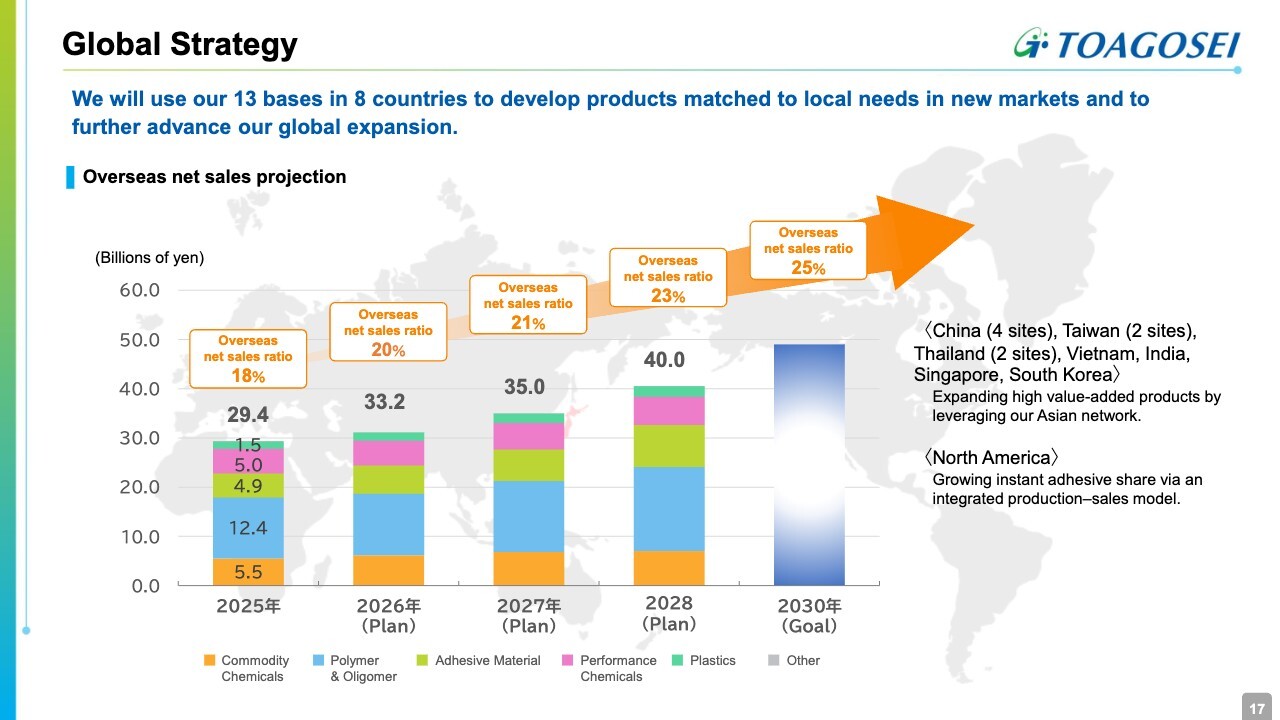

Global Strategy

This slide concerns our global strategy. Under our previous medium-term management plan, our overseas net sales ratio in 2025 was stagnant at 18%. Despite the influx of inexpensive Chinese-made products into the Asian market, over the past three years we have expanded to 13 bases in eight countries overseas.

Our bases will advance the development of high value-added products that meet local needs and will connect these to sales expansion. Our Krazy Glue instant adhesive material business in the U.S. has shifted to an integrated manufacturing and sales structure under sole ownership. We aim to return to profitability by expanding our market share.

Through these measures, we aim to raise the overseas net sales ratio to 23% and net sales to ¥40.0 billion by 2028.

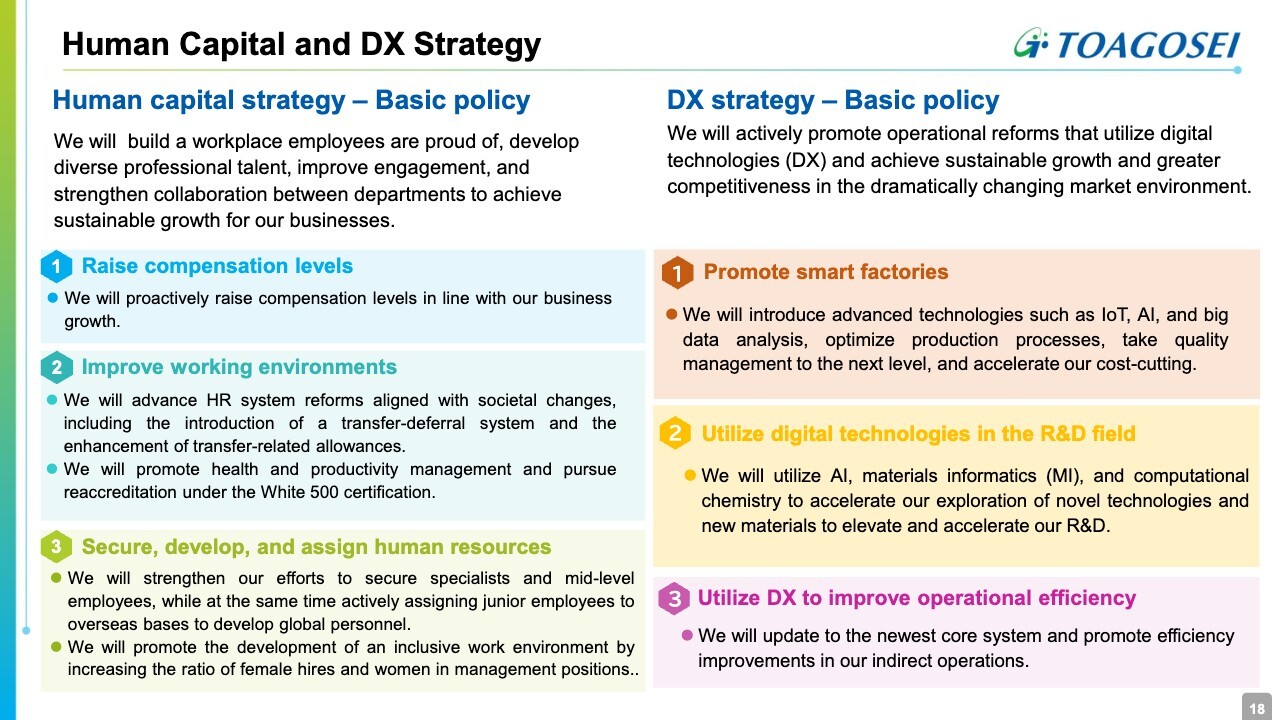

Human Capital and DX Strategy

This slide looks at our human capital and DX strategies. The basic policy of our human capital strategy is to achieve sustainable development through increased engagement and co-creation.

We will improve our working environment through means including raising compensation standards and engaging in a transfer-deferral system and health and productivity management. We will also strengthen the acquisition of human capital, train young employees, and create an environment in which diverse employees can play active roles.

Under our DX strategy, we will achieve sustainable growth and strengthen competitiveness through DX-based business transformation. Specifically, we will promote a shift to smart factories, advance R&D through AI and materials informatics (MI), and enhance efficiency in indirect operations through DX.

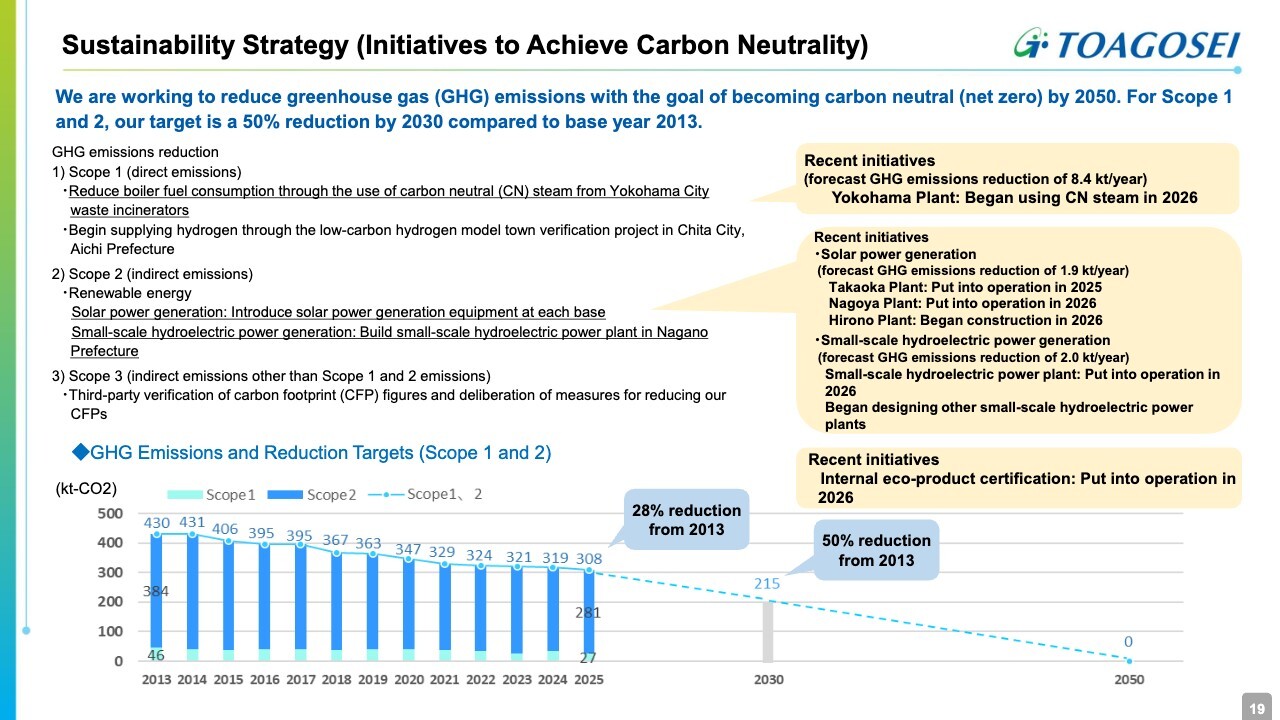

Sustainability Strategy (Initiatives to Achieve Carbon Neutrality)

I will now talk about our sustainability strategy. We aim to achieve carbon neutrality by 2050 and a 50% reduction in greenhouse gas (GHG) emissions by 2030 compared to 2013 levels.

To address Scope 1 direct emissions, we will begin reducing boiler fuel by using carbon neutral (CN) steam from Yokohama City waste incinerators in 2026.

To address Scope 2 indirect emissions, we are progressively introducing renewable energy. We progressively began solar power generation in 2025, and plan to embark on our first operation of small-scale hydroelectric power generation in 2026.

Our GHG emissions in 2025 were 28% below our 2013 level. Through the measures noted, we aim to achieve a 40% reduction from the 2013 level in 2028.

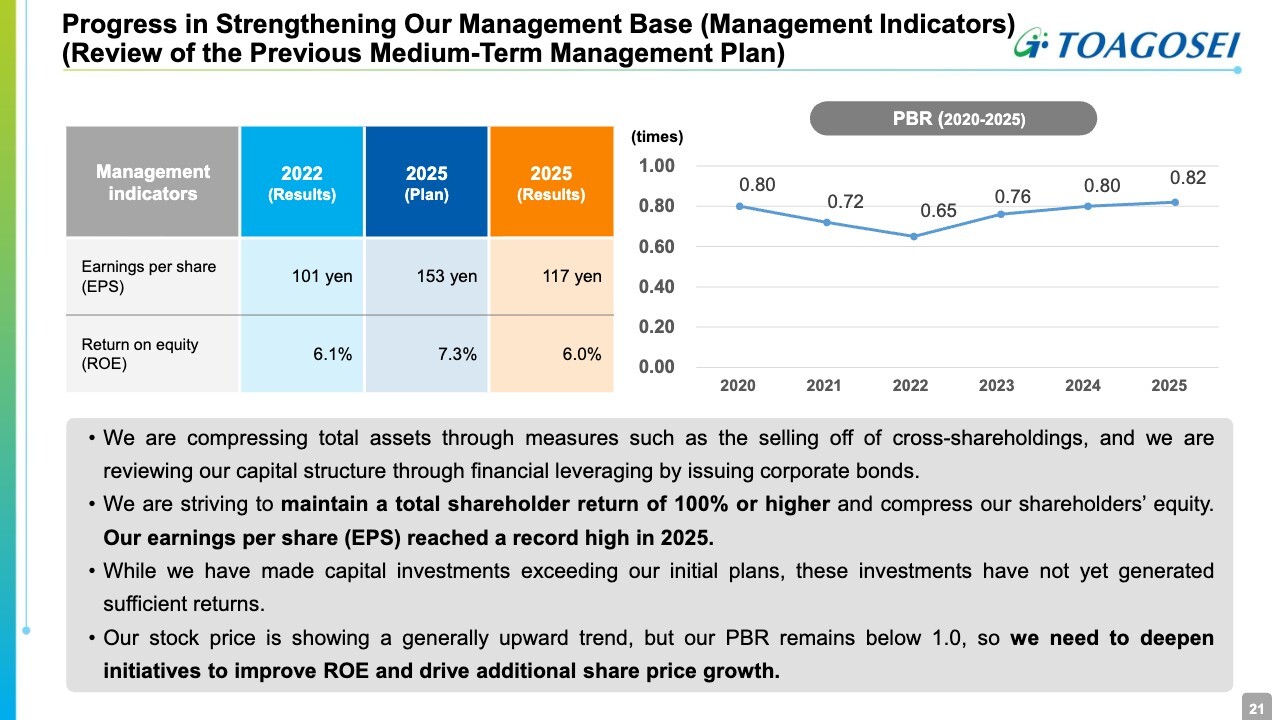

Progress in Strengthening Our Management Base (Management Indicators) (Review of the Previous Medium-Term Management Plan)

I will now discuss our financial strategy. First, let us look back at the previous medium-term management plan. Under that plan, we compressed total assets through measures including the sale of cross-held shares, used financial leverage through the issuance of corporate bonds, and reviewed our capital structure.

By maintaining a total shareholder return of 100% or higher and compressing equity, we achieved our highest-ever earnings per share (EPS) in 2025. At the same time, although we are making capital investments that exceed plans, these continue to fail to generate sufficient returns.

While our stock price is trending upward, our PBR remains below 1.0x. We believe that we need to deepen measures aimed at improvement of ROE and at increase in share price.

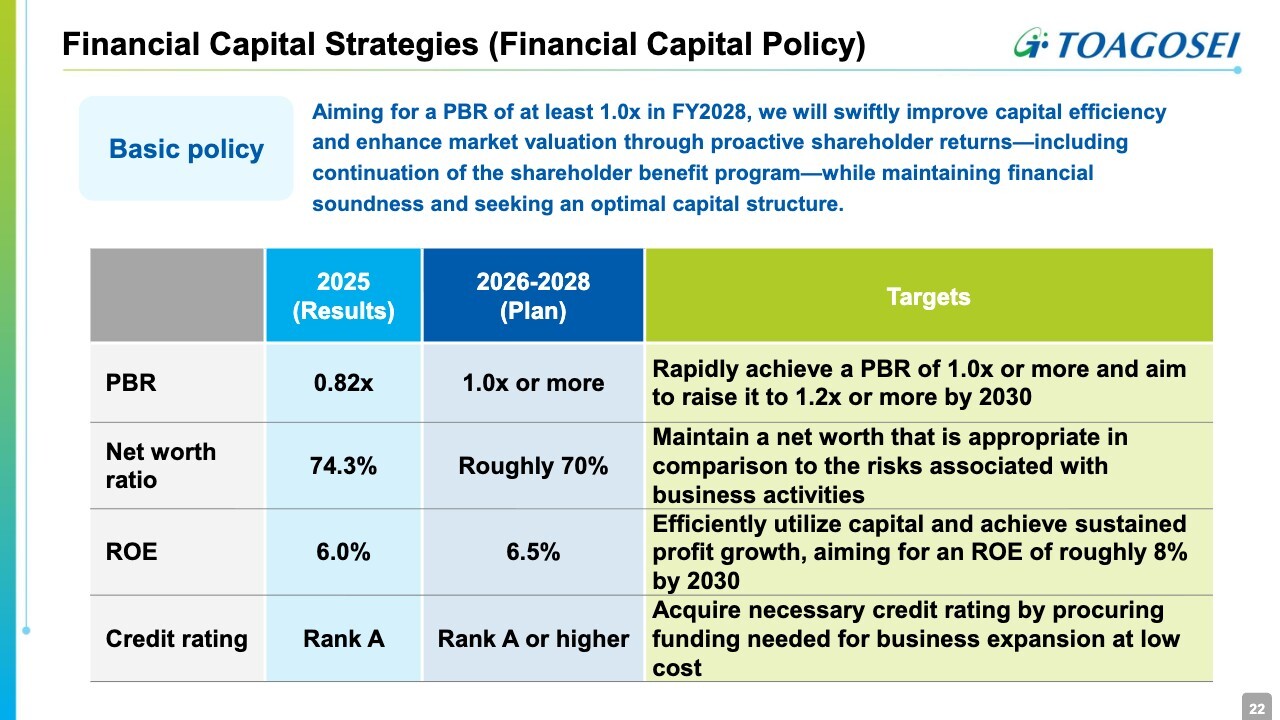

Financial Capital Strategies (Financial Capital Policy)

Under the new medium-term management plan, we aim to achieve a PBR of 1.0x or more by 2028, quickly improve capital efficiency, and raise our valuation in the stock market through active shareholder returns and the continuation of our shareholder benefit program. We will also pursue an optimal capital structure while maintaining financial soundness.

Specifically, we aim to achieve an equity ratio of approximately 70% and, through efficient capital utilization and profit growth, achieve ROE of 6.5% under the new plan and 8% by 2030. We plan to maintain a credit rating of Rank A or higher in order to procure the funding needed for business expansion at low cost.

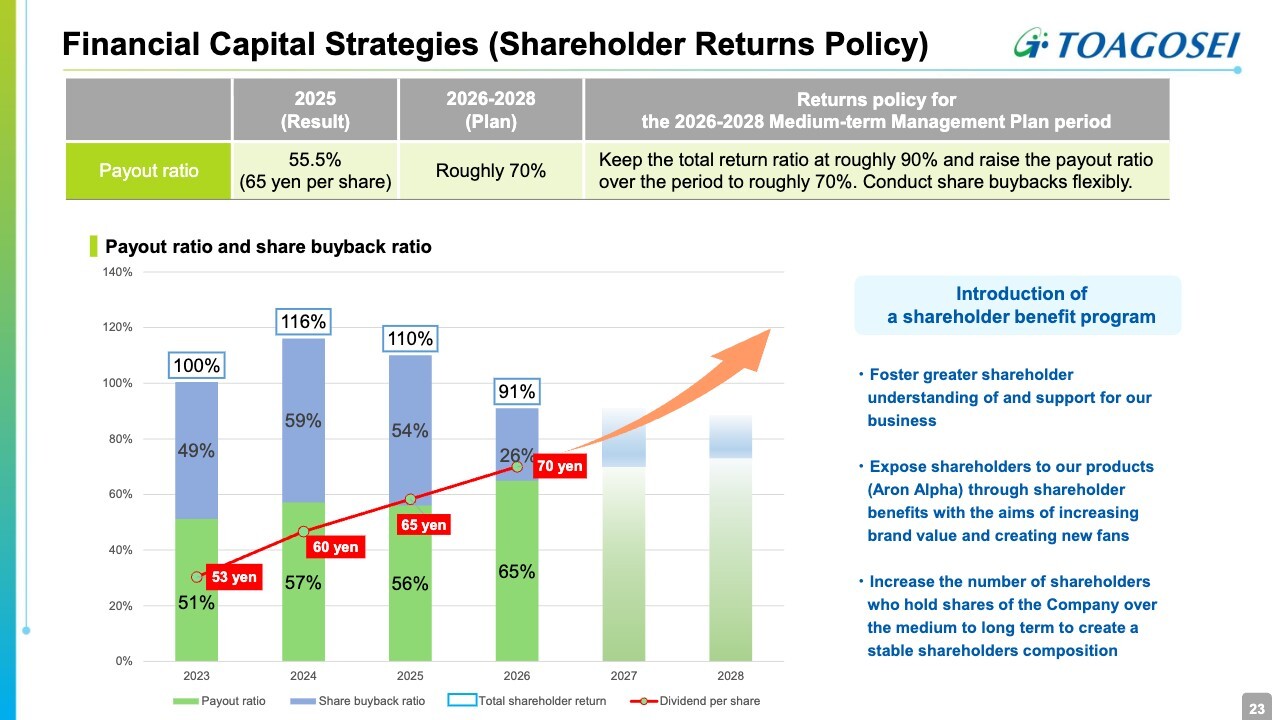

Financial Capital Strategies (Shareholder Returns Policy)

The slide presents our shareholder returns policy. Green indicates our payout ratio, blue our share buyback ratio, and red dividend per share. The top row shows total shareholder return.

Under the previous medium-term management plan, we maintained a dividend payout ratio of slightly over 50% and a total shareholder return of 100% or higher. However, taking into account the appropriate contraction of cash and deposits, as well as the securing of investments in growth and human capital, our policy is to set total shareholder return to approximately 90% under the new medium-term management plan.

We reviewed our ratio of share buybacks to dividends, and decided to increase the percentage of dividends and to set the average dividend payout ratio during the period to about 70%. Based on this policy, we plan to pay a dividend of ¥70 in 2026.

Our shareholder benefit program is one of the most attractive in the chemical sector. We hope to create a stable shareholder structure through shareholders deepening their understanding of our company, becoming fans, and holding shares over the medium to long term.

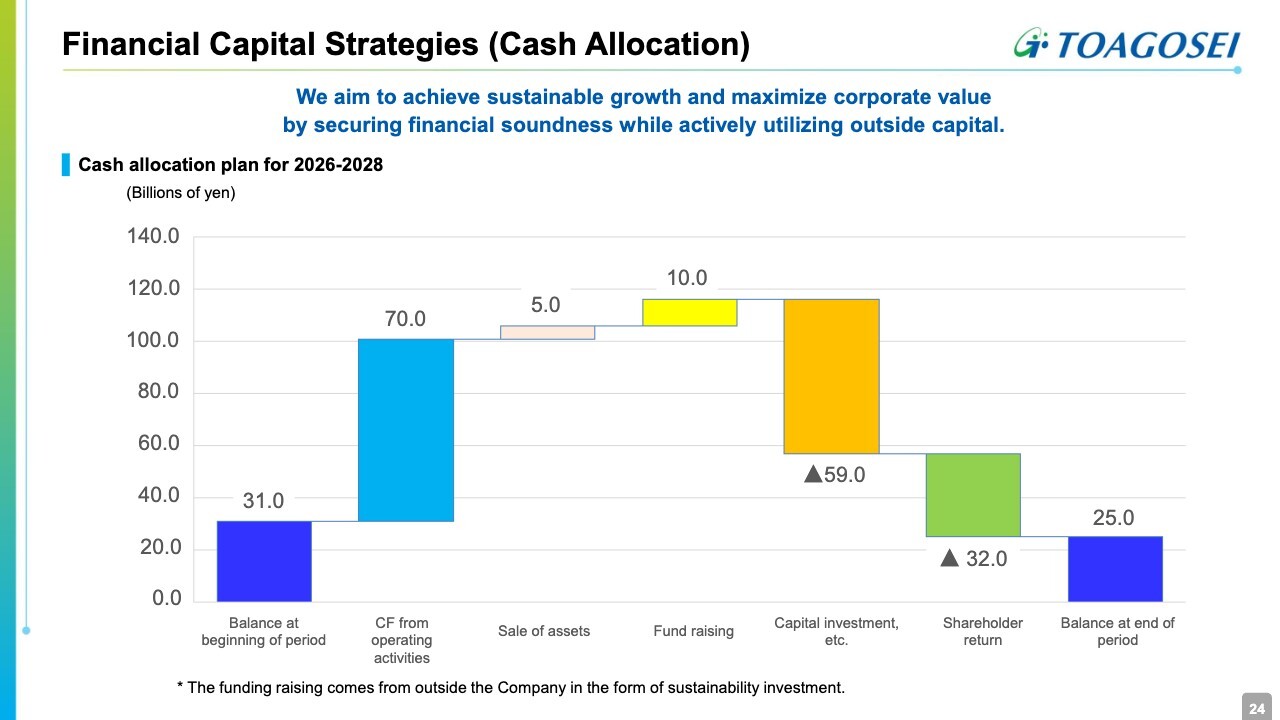

Financial Capital Strategies (Cash Allocation)

Here I will discuss cash allocation. For three-year cumulative net income and depreciation expenses, we expect operating cash flow to be ¥70.0 billion.

Addressing incremental R&D expenses and labor costs, we expect to make proactive capital investments of ¥59.0 billion and pay ¥32.0 billion in shareholder returns, with a total shareholder return of 90%. We expect to raise ¥10.0 billion in funds for sustainability investments.

As a result, we expect a cash and cash equivalents balance of ¥25.0 billion in the final year of the medium-term management plan, the equivalent of two months of net sales. In this way, while maintaining financial soundness, we aim to maximize sustainable growth and corporate value by actively utilizing external funds.

Under the slogan "Connect and Create 2028," we will steadily implement the growth, financial, global, human capital, DX, and sustainability strategies we have outlined, to achieve the goals of the new medium-term management plan. That concludes the presentation.

Question: Fixed cost difference in the 2026 results forecast

Moderator: The question is as follows: "Regarding the background to the ¥2.9 billion negative impact from fixed cost difference in the FY2026 results forecast, do you see higher repair costs in the acrylic acid area, higher depreciation expenses, higher wages, and so on as fully accounting for this? Also, with regard to improvement of profitability, for which products will you be tackling such improvement, other than environmental infrastructure and eco-material products?"

Kobuchi: The ¥2.9 billion negative impact from fixed costs is mostly due to increases in labor expenses, including wage increases, as well as depreciation expenses. As for improvement of profitability, we will essentially address all products. While price revisions have mainly addressed variable costs, we will move forward with price revisions to cover fixed costs. Our policy is to take action to restore the base to its original level and steadily advance growth investments.

Question: Sales expansion of products for semiconductors in the medium-term management plan

Moderator: The question is as follows: “In the semiconductor area, you plan to expand sales by 40% from the 2025 level in 2028. How do you envision the degree of contribution toward this in terms of specific products? “Compared to the increase of 40% in net sales, as shown on Slide 11, operating income in the Performance Chemicals segment does not increase much under the plan. Do you expect to see significant growth in semiconductor-related products in the Polymer & Oligomer segment?”

Kobuchi: On Slide 13, white indicates our products on the market and green, our products currently under development. Of these, high-purity liquefied hydrogen chloride (cleaning gas) has the greatest impact on sales and profit, followed by high-purity hydrochloric acid, high-purity potash, and polymers for CMP.

Operating income in the Performance Chemicals segment has not grown much because Performance Chemicals includes the medical area along with semiconductor-related products.

Because of our active development investment in the medical field, overall profit growth in the Performance Chemicals segment is low. Another factor contributing to lower operating income growth is amortization expenses incurred from capital investment in high-purity liquefied hydrogen chloride and high-purity potash.

Question: Fund raising and sale of assets in the medium-term management plan

Moderator: The question is as follows: “Under financial capital strategy in the medium-term management plan, does the ¥10.0 billion to be raised for sustainability investments mean the use of debt? In addition, ¥5.0 billion in sales of assets seems a small amount when considered as a reduction of cross-held shares. What sort of assets are planned for sale?”

Kobuchi: For the ¥10.0 billion in financing, we plan to use debt. We position a number of investments that are particularly related to sustainability, including small-scale hydroelectric power generation, as sustainability investments.

The ¥5.0 billion in sales of assets is mainly related to cross-held shares. Last year, we sold shares worth ¥7.0 billion. Our original plan was to reduce the ratio of cross-held shares to equity to the 10% level, but we did not reach that target due to a significant rise in stock prices.

Against this backdrop, we intend to carefully scrutinize and agilely address the large remaining number of shares of partners with whom we have formed alliances or are planning to form alliances.

We would like you to understand that our policy is to continue selling stocks for which the significance of holding has diminished.

Question: Measures to improve ROE and PBR in the medium-term management plan

Moderator: The question is as follows: "You have set an ROE target of 6.5% for FY2028, but I think there are some difficulties in aiming for a PBR of 1.0x or more at this ROE level. Although there is also the question of the level of cost of capital, what is behind your belief that you can achieve a PBR of 1.0x or more at an ROE of 6.5%?”

Kobuchi: As you note, some people think that this is difficult at an ROE of 6.5%. However, we have adopted a shareholder benefit program which alone has boosted the share price considerably.

Therefore, while ROE is not high under the plan at present, I will aim for PBR of 1.0x or more while introducing measures that include enhancing PER, while appealing to Toagosei’s presence as a technology company.

The stock price has risen considerably again today, and the number is above 0.9x. We are now at a critical point, and intend to introduce a number of measures to move forward.

Question: Initiatives for loss-generating businesses under the medium-term management plan

Moderator: The question is as follows: "There are several loss-making businesses, such as Toagosei Singapore and the household adhesives business in the U.S. At the same time, there was mention of concentration and selection in the medium-term management plan. How should we interpret these initiatives?"

Kobuchi: Regarding the revision of our portfolio, so far we have withdrawn from the polyvinyl chloride business and discontinued production last year.

As for the instant glue business in the U.S., this had been a loss-generating business. Although our original market share was about 40%, with the formation of a joint venture, end-user information no longer came in, and market share dropped to 13%.

However, after deep discussions among the parties involved, we have gained confidence and conviction that we can regain market share and return to our former scale through the introduction of various measures. Accordingly, we have decided to strengthen this business.

As for Singapore, it is currently under consideration. We are considering how to reduce fixed costs and how to secure sales outlets, especially in the current situation. The potential for expanding sales of two monomers has grown. We have already begun test sales.

As the results of the tests will determine our future policy, we will closely monitor developments as we consider the future potential of Singapore.

There are also several loss-generating businesses, and businesses that will require strengthening. We plan to identify these and consider how to address each.

Question: Enhancement of ROE under the medium-term management plan

Moderator: The question is as follows: “With average ROE for Japanese companies approaching 10%, aren’t the 2028 target of 6.5% and the 2030 target of 8% too slow in terms of time frame?”

Kobuchi: The denominator, equity, and the numerator, profit, are affecting this. As we have made considerable investments so far, how we can proceed with the recovery of profit from those investments will be important.

We plan to make a considerable investment under the new medium-term management plan. We have set the figure at a low 6.5% partly because the timing for individual investments to generate significant profit can slip somewhat.

Regarding reduction of the denominator, we have set the equity ratio to around 70%. As a financial strategy, we intend to increase the use of debt, and are considering the enhancement of our financial leverage. We will continue our efforts to raise ROE above 6.5% as much as possible, taking into account the relationship between the denominator and the numerator, and aim to achieve 8% or higher by 2030.

Question: Measures to improve PBR

Moderator: The question is as follows: “You mentioned taking measures to achieve ROE of 6.0% and PBR of 1.0x or more. Should we understand that the path toward a PBR of 1.0x or more has been drawn to some extent? “Could you elaborate a bit more on the logic behind your initiatives to achieve PBR in excess of 1.0x or more even at ROE 6.5%?”

Kobuchi: PBR is a multiple of ROE and PER. I think it is a matter of how to raise PER even with low ROE. In short, we are considering how far we can raise the level of expectations toward Toagosei's future.

As noted earlier, the introduction of our benefits program alone has considerably boosted the share price and PER. However, we want to do not only that, but to also take action that raises expectations for our future potential in a real way.

In these presentation materials, many of the measures related to the new medium-term management plan are spelled out. We are proud of the quality and quantity of the themes, and we believe that the steady launch of these alone will significantly raise expectations. We also believe that if we can achieve these themes even a bit more quickly, that will lead to higher profits and ROE.

Toagosei has many face-to-face customers, and in many cases, we cannot be open about technical details. We have seen a number of cases involving our company given extensive coverage in newspapers recently.

However, we will enhance our PER by showcasing Toagosei as a technology company as much as possible, and by showing that we contribute to society.

Furthermore, we believe that by our actually generating profit, ROE will rise and PBR will move to a higher level.

Message from Mr. Kobuchi

Kobuchi: I would like to thank all of you for your participation today.

Whatever the changes in the environment, we will continue demonstrating strong will and achievements aimed at realizing sustainable growth through company-wide efforts under responsible management. We appreciate your continued support and guidance.

Thank you very much for your time today.