FY12/25 Financial Results Briefing

Shinichiro Fujisaki (“Fujisaki”): Hello, everyone. I am Fujisaki, President and CEO of AUCNET INC. Thank you very much for joining us today for the presentation of the financial results for FY2025.

Last year marked the 40th anniversary of our company's founding, and we positioned it as a year of preparation, or investment, with costs for future growth taking precedence. However, the resulting operating and other figures were favorable, allowing us to achieve a sixth consecutive year of sales and profit growth, as well as a fifth consecutive year of record profits. We would like to take this opportunity to thank everyone for their support. Thank you very much.

On the other hand, we revised and updated our medium-term management plan, as the results have far exceeded its target figures. At today's briefing, I would also like to share some of its details.

Table of Contents

This is the table of contents. I will give an overview of the financial results for FY2025, followed by a performance summary and details by segment, a forecast for FY2026, and some topics that I would like to share with you at the time of closing, and then I will discuss the details of our medium-term management plan.

Full Year 2025 Consolidated Financial Results

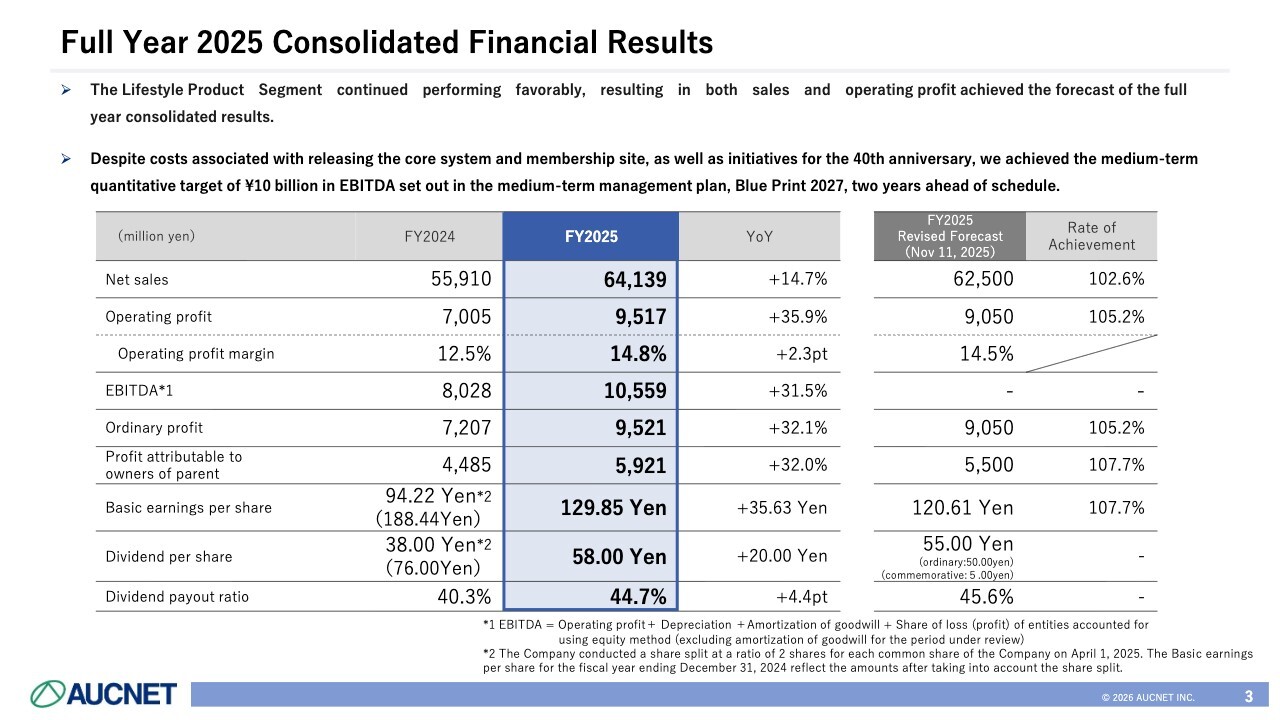

First, here is a summary of the financial results for FY2025. The Lifestyle Products Segment continued to perform well from the previous fiscal year, achieving the consolidated forecasts for both net sales and operating profit.

In the Automobile Business, a core system and a membership site were released. In addition, although we recorded various costs, including those related to the 40th anniversary initiatives I mentioned earlier, we were able to achieve our medium-term quantitative EBITDA target of 10 billion yen two years ahead of schedule, which was set in the three-year plan in our medium-term management plan, Blue Print 2027.

As specific figures, net sales increased 14.7% year on year to 64,139 million yen, and operating profit increased 35.9% year on year to 9,517 million yen. Compared to the upward revision made in November last year, the net sales achievement rate was 102.6%, and the operating profit achievement rate was 105.2%.

Operating profit margin was 14.8%, up 2.3 percentage points year on year; EBITDA was 10,559 million yen, up 31.5% year on year; ordinary profit was 9,521 million yen, up 32.1% year on year; and profit attributable to owners of parent was 5,921 million yen, up 32.0% year on year. Basic earnings per share were 129.85 yen, and dividend per share was 58 yen, raising the dividend payout ratio to 44.7%.

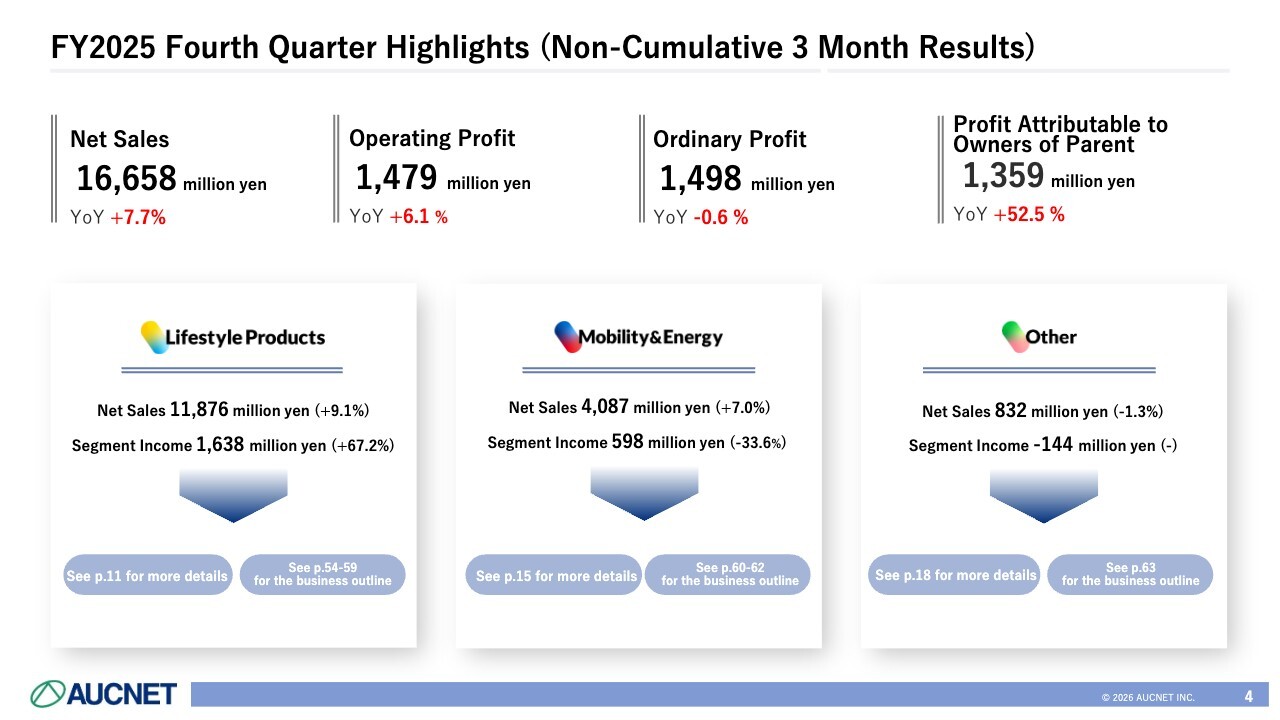

FY2025 Fourth Quarter Highlights (Non-Cumulative 3 Month Results)

These are the highlights for the most recent three-month period, the fourth quarter of FY2025. Net sales increased 7.7% year on year to 16,658 million yen, and operating profit rose 6.1% to 1,479 million yen. Profit attributable to owners of parent was 1,359 million yen, up 52.5% year on year, a significant improvement.

In terms of operating profit by segment, the Lifestyle Products Segment increased 67.2% year on year to 1,638 million yen; the Mobility & Energy Segment decreased 33.6% year on year to 598 million yen; and the Other Segment posted a loss of 144 million yen.

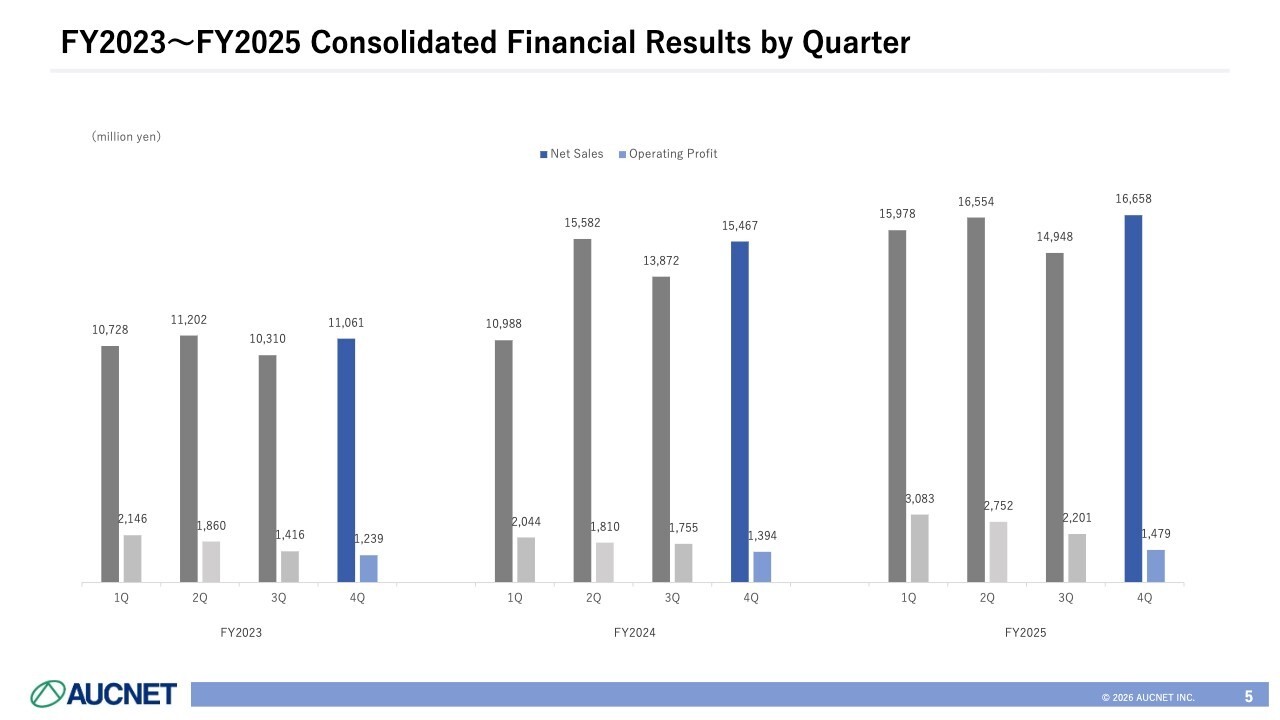

FY2023-FY2025 Consolidated Financial Results by Quarter

This is the quarterly performance trend. Operating profit for the fourth quarter is down slightly, but we will explain this later.

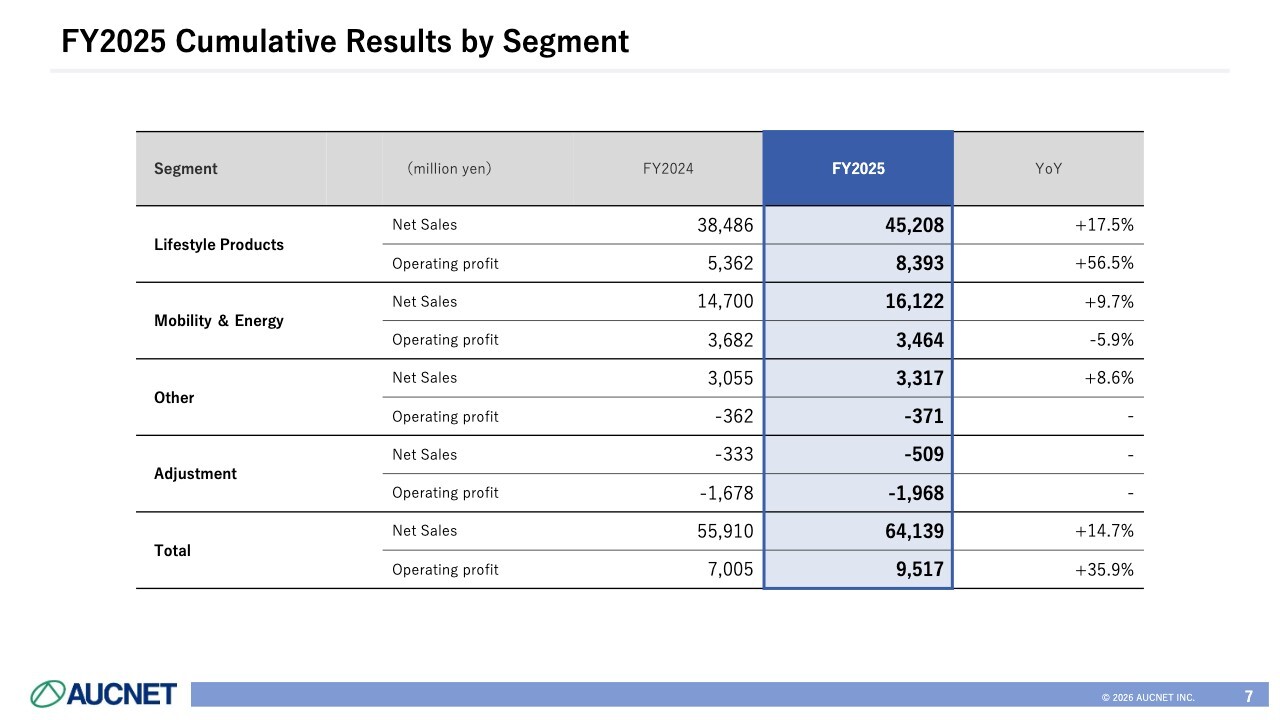

FY2025 Cumulative Results by Segment

This is a summary of results by segment. For operating profit by segment, the Lifestyle Products Segment posted 8,393 million yen, up 56.5% year on year; the Mobility & Energy Segment recorded 3,464 million yen, down 5.9%; the Other Segment posted a loss of 371 million yen; and adjustments, expenses, etc., were a loss of 1,968 million yen. As a result, the total operating profit was 9,517 million yen.

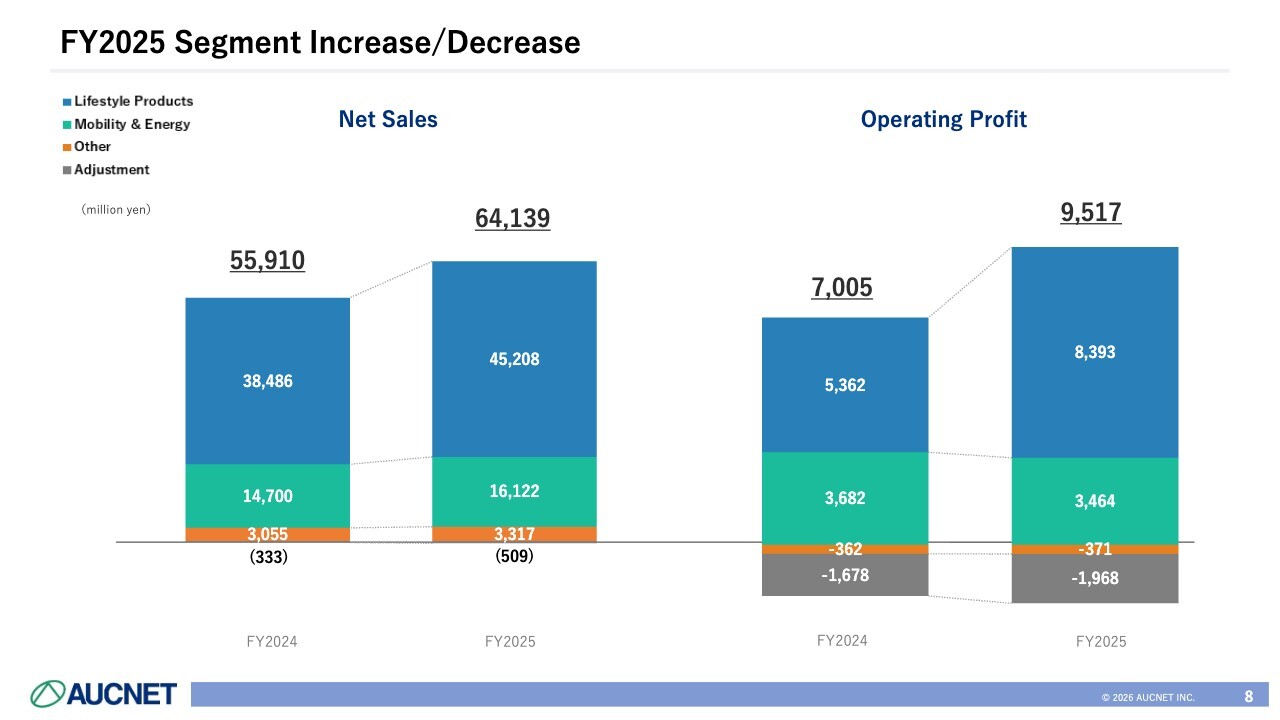

FY2025 Segment Increase/Decrease

The slide shows a bar chart of net sales and operating profit by segment. As I mentioned at the beginning, the Lifestyle Products Segment has contributed significantly to our revenues with a large increase in earnings.

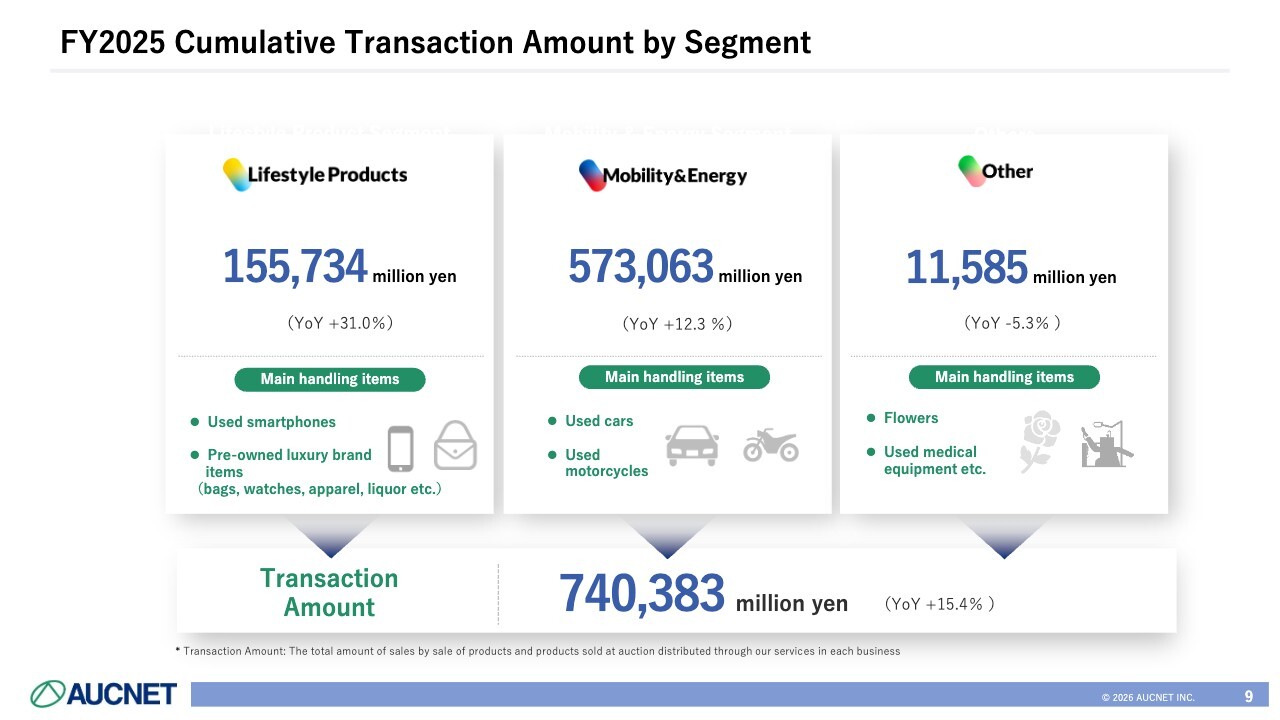

FY2025 Cumulative Transaction Amount by Segment

This describes the transaction amount for each segment. The Lifestyle Products Segment totaled 155,734 million yen, up 31.0% year on year. Please understand that this increase is the result not only of the market price, but also of a significant increase in sales units themselves. The Mobility & Energy Segment increased 12.3% year on year to 573,063 million yen, while the Other Segment decreased 5.3% to 11,585 million yen.

The total transaction amount exceeded 700 billion yen at 740,383 million yen, an increase of 15.4% year on year.

FY2025 Cumulative Results

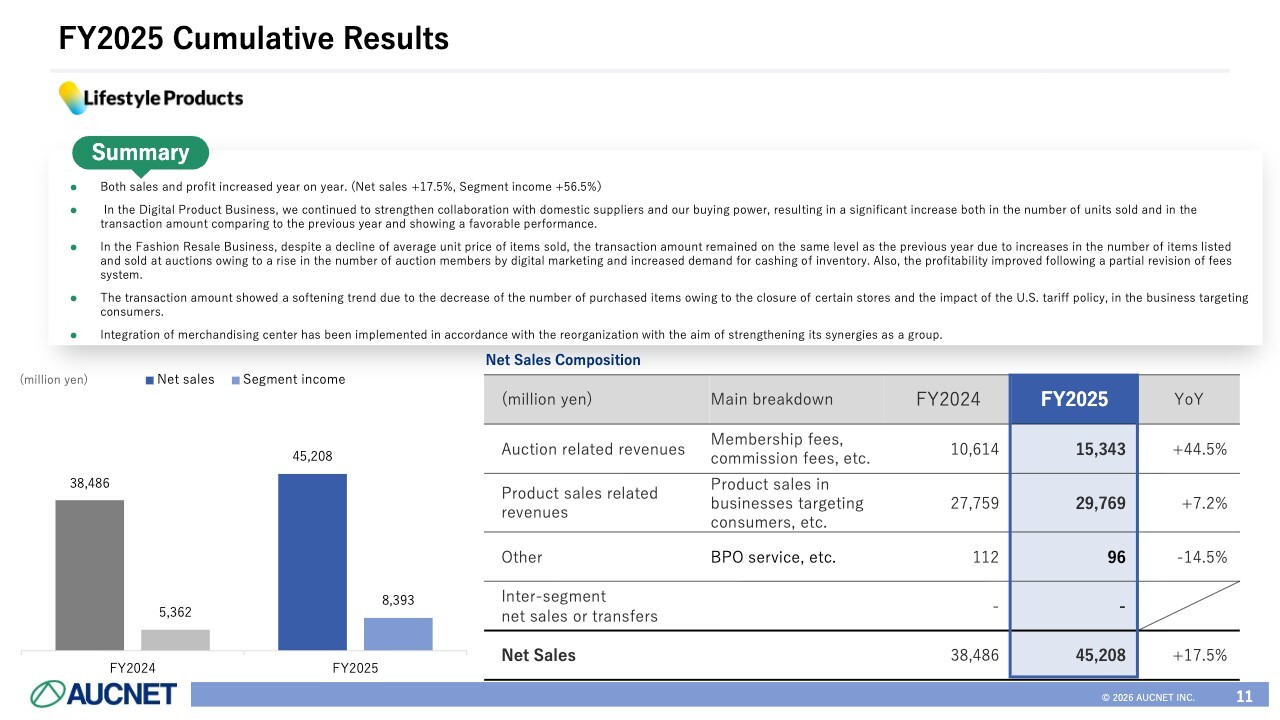

The following is a detailed description of each segment. First, let me discuss the Lifestyle Products Segment. Both sales and profits increased year on year, with net sales up 17.5% and segment income up 56.5%.

In particular, for the Digital Product Business, especially smartphones, prices increased due to strengthened collaboration with domestic suppliers, an increase in the number of items listed, and stronger buying power. As a result, the sales units have increased significantly. In addition, the transaction amount was also significantly higher than in the previous fiscal year.

On the other hand, in the Fashion Resale Business, which handles branded goods and other items, the average unit price of items sold declined slightly, although market prices remained relatively stable. However, the number of items listed and sold increased significantly, particularly in digital marketing, due to an increase in the number of international members and demand for cashing of inventory. As a result, the transaction amount remained on the same level as the previous fiscal year, but profitability improved due to a revision to some commission fees and other factors.

In the business targeting consumers, which focuses on purchases, the transaction amount remained sluggish due to a decline in the number of purchases resulting from the closure of some stores, the U.S. tariff policy, and a decline in the number of visitors from Greater China. At the same time, we are integrating and reorganizing centers to strengthen group synergies in BtoB, CtoB, and BtoC.

As a result, net sales and segment income, shown on the lower left of the slide, increased, with segment income of 8,393 million yen.

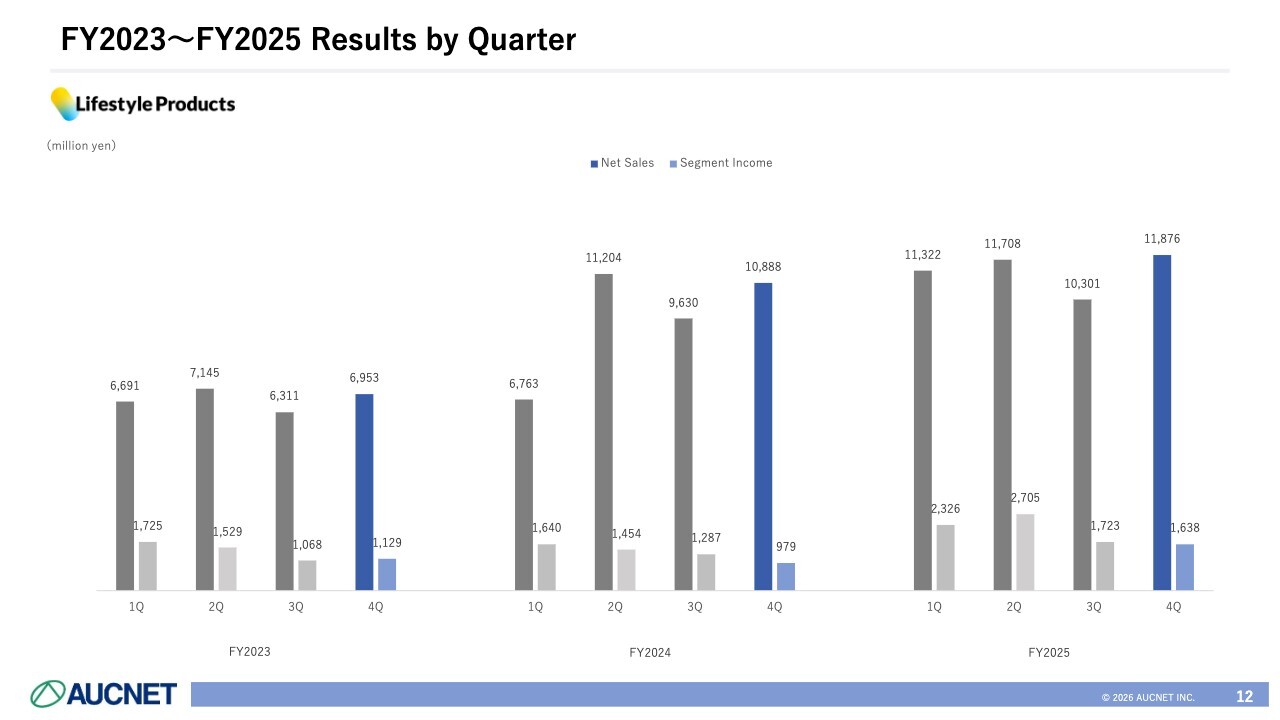

FY2023-FY2025 Results by Quarter

This shows the quarterly trend for the Lifestyle Products Segment. Due to M&A and other factors, net sales have grown significantly compared to FY2023.

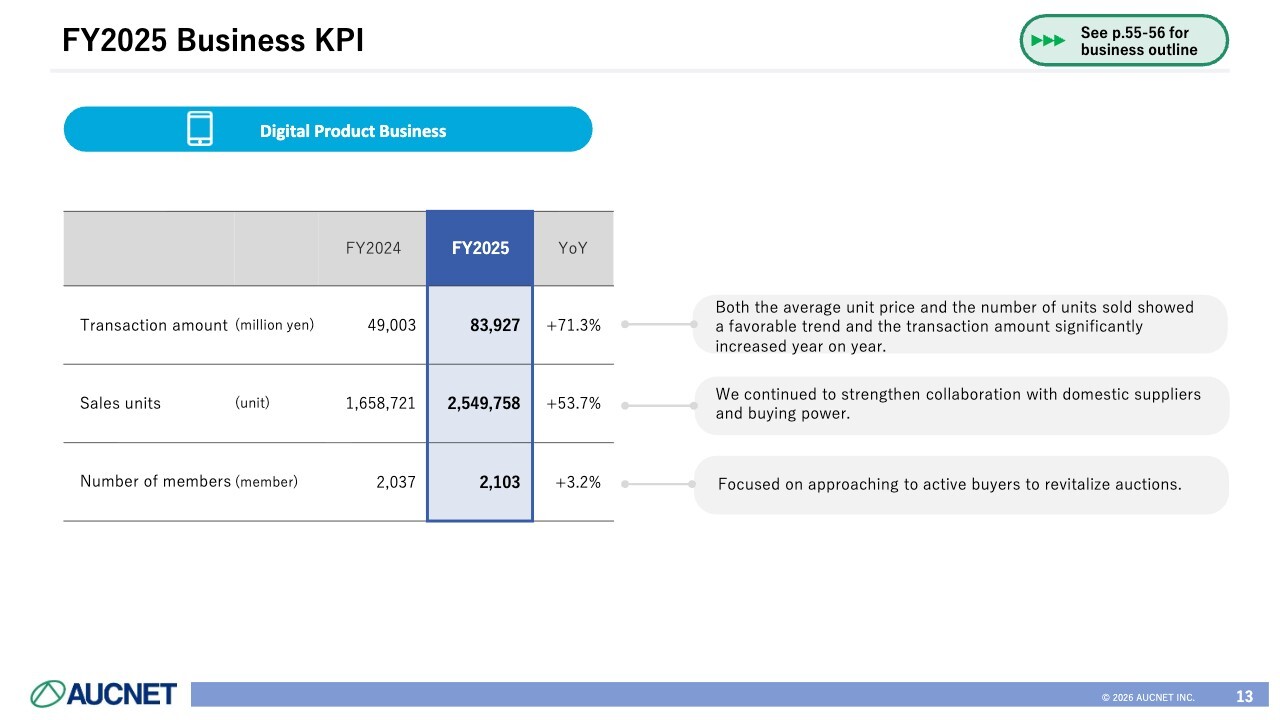

FY2025 Business KPI

I will now explain the business KPIs. The transaction amount in the Digital Product Business was 83.9 billion yen, and sales units increased 53.7% year on year to 2.54 million units. In particular, we have been able to greatly strengthen our collaboration with suppliers, our domestic listing sources. The number of members grew slightly by 3.2% year on year to 2,103 members, but rather than increasing the number of members, we focused on approaching active buyers who are willing to participate in auctions during the year.

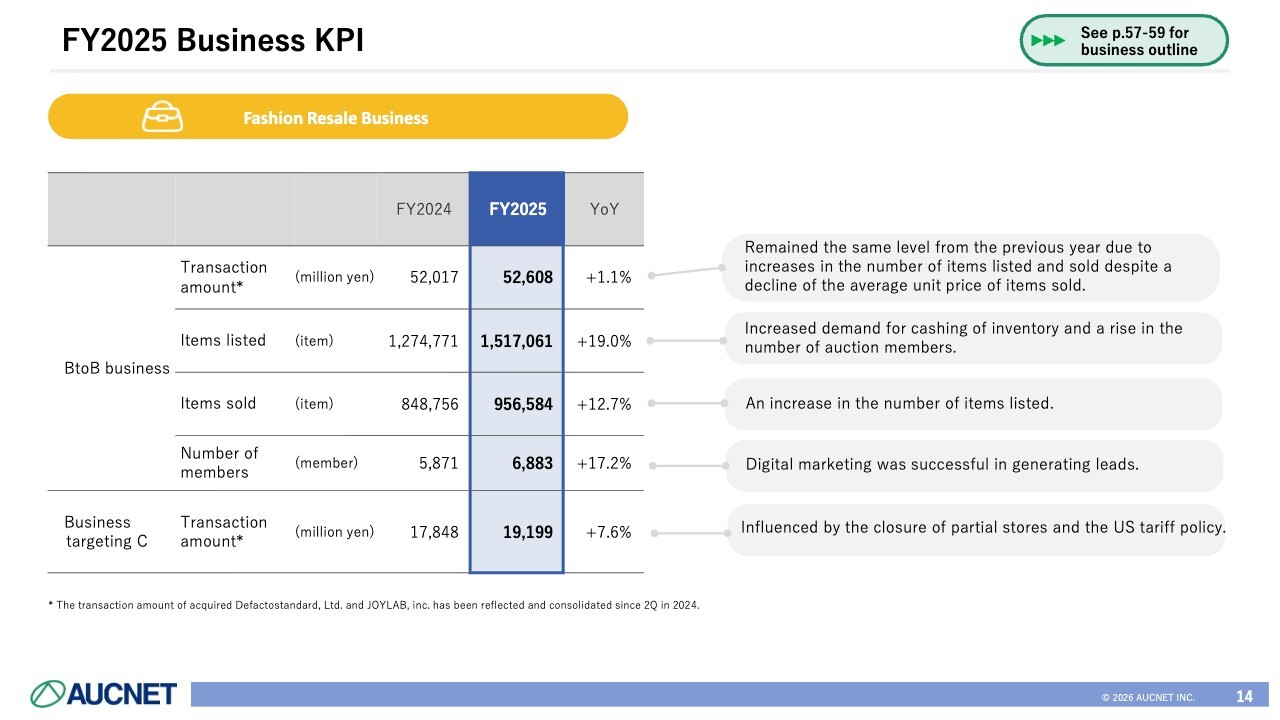

FY2025 Business KPI

This is about the Fashion Resale Business. The transaction amount in the BtoB business was 52.6 billion yen, up 1.1% year on year. The number of items listed was 1,510,000, and the number of items sold, or items ultimately distributed, was 956,000. The significant increase in the number of items listed was accompanied by an increase in the number of items sold, up 12.7% year on year. The number of members also increased steadily to 6,883, up 17.2% year on year.

On the other hand, the transaction amount for the business targeting consumers was 19,199 million yen, up only 7.6% year on year.

FY2025 Cumulative Results

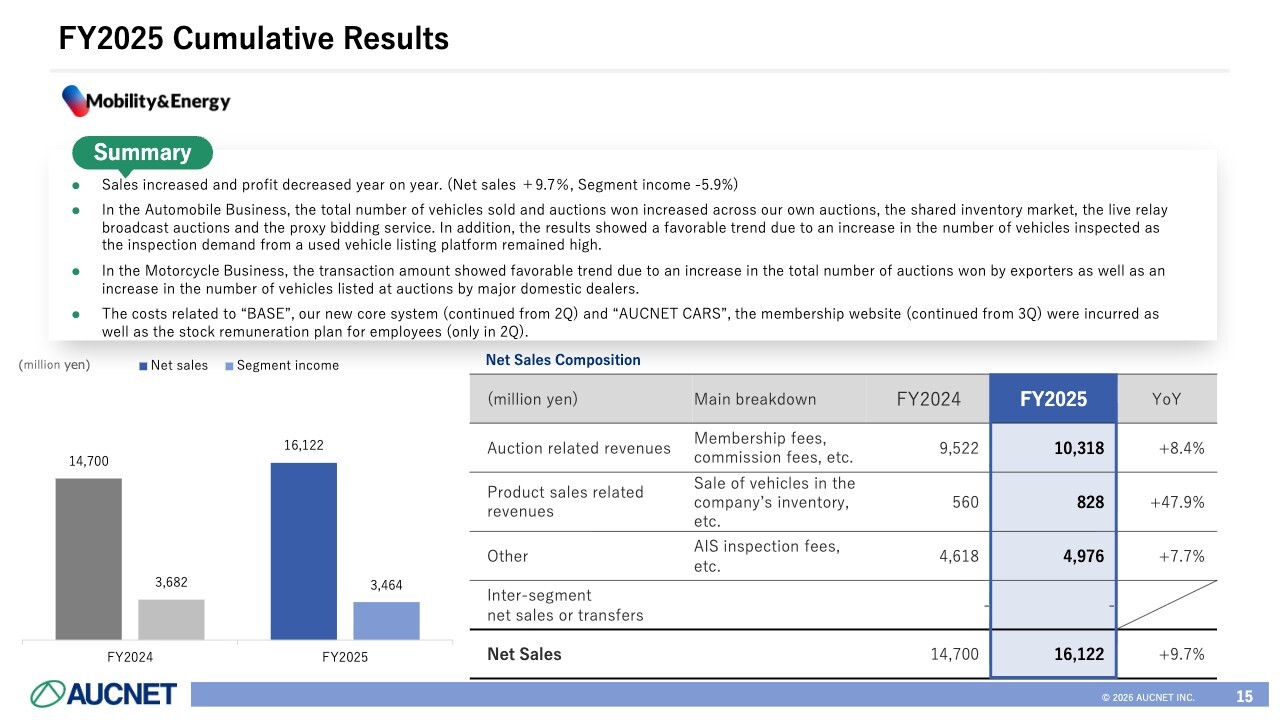

The Mobility & Energy Segment reported higher sales and lower profits compared to the previous year. Net sales increased 9.7% year on year, but segment income decreased 5.9% year on year. In the Automobile Business for used vehicles, which accounts for a large portion of the business, both AUCNET-hosted auctions and the shared inventory market are increasing. In addition, the number of vehicles distributed and sold both increased, including those from live relay broadcast auctions in partnership with other auction venues and a proxy bidding service. Furthermore, the inspection demand from a used vehicle listing platform remained high, and the number of vehicles inspected is increasing.

As for the Motorcycle Business, the number of vehicles listed and sold increased due to the participation of major domestic dealers in auctions. As for buyers, exporters continue to participate actively, with a steady increase in transaction amount.

Meanwhile, last year was also a year of increased costs. We have renewed the system that had been in use for more than a decade, resulting in amortization expenses for the core “BASE” system and the “AUCNET CARS” membership website. In addition, segment income turned negative due to the combined factors of one-time costs associated with the system release, stock remuneration for employees, and the cost impact from the large workforce in the automotive business. However, net sales and profits related to auctions and inspection fees are growing steadily.

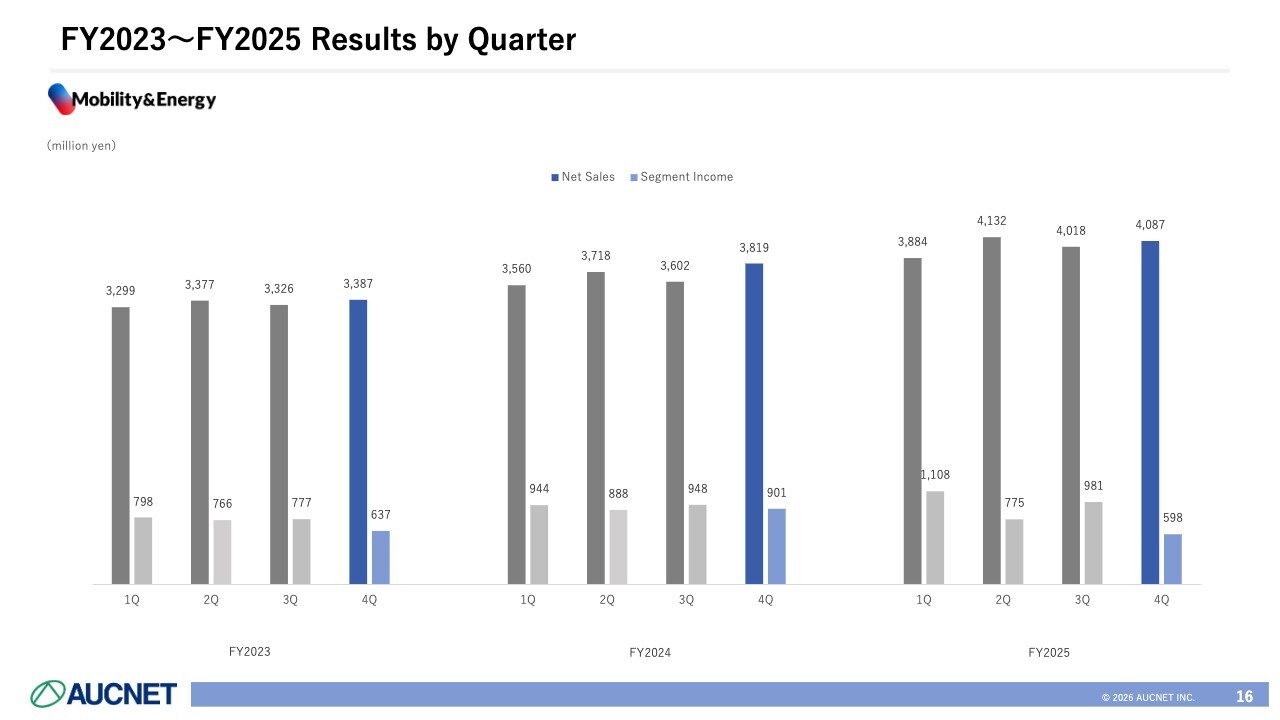

FY2023-FY2025 Results by Quarter

The bar chart on the slide shows the quarterly trends for the Mobility & Energy Segment. They are relatively stable.

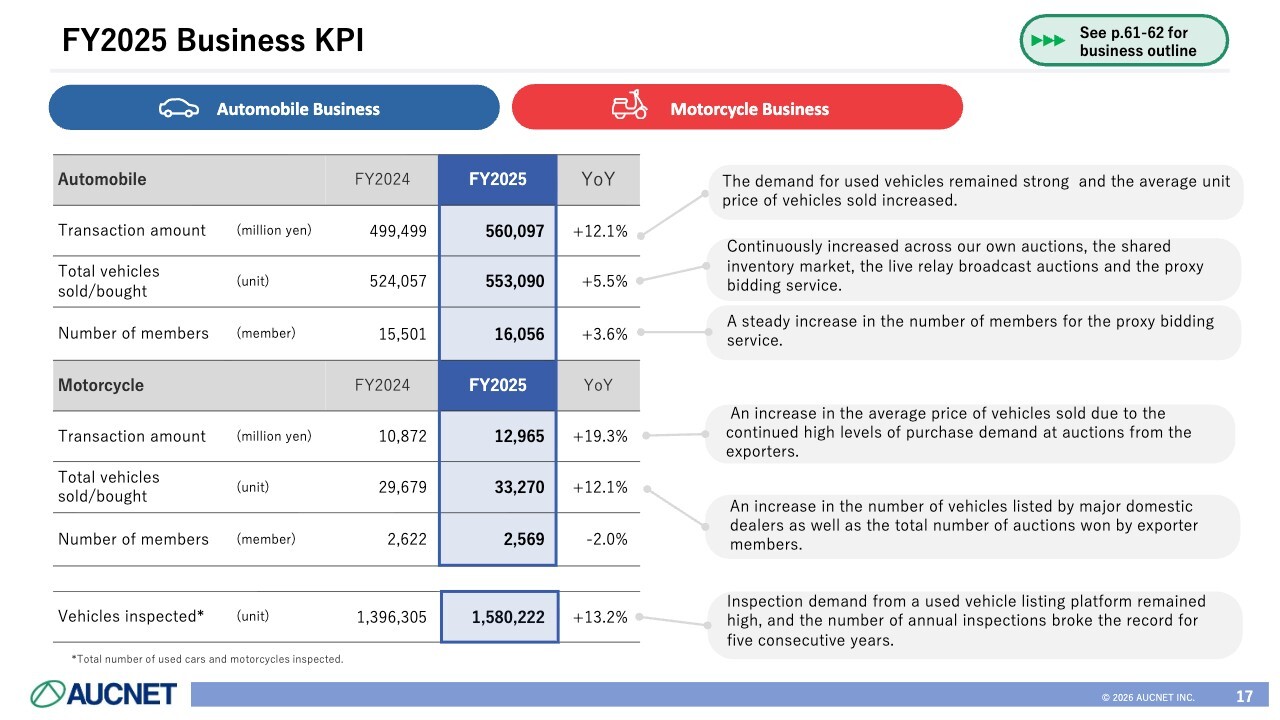

FY2025 Business KPI

Let me explain the business KPIs. The transaction amount for the Automobile Business was 560,000 million yen. The demand for used vehicles continues to grow, and prices for used vehicles are still rising. The number of vehicles sold totaled 553,000 units, with continued growth in both AUCNET-hosted auctions and auctions conducted in partnership with other companies. The number of members has exceeded 16,000. In particular, the number of members for the proxy bidding service provided by subsidiary i-Auc has been steadily increasing.

The transaction amount for the Motorcycle Business was 12,900 million yen, and the average unit price is rising due to continued strong exports. The number of vehicles sold was 33,000 units. On the other hand, the number of members has declined slightly, likely due to the fact that smaller companies are struggling. The total number of vehicles inspected reached 1.58 million, a record high for the fifth consecutive year.

FY2025 Cumulative Results

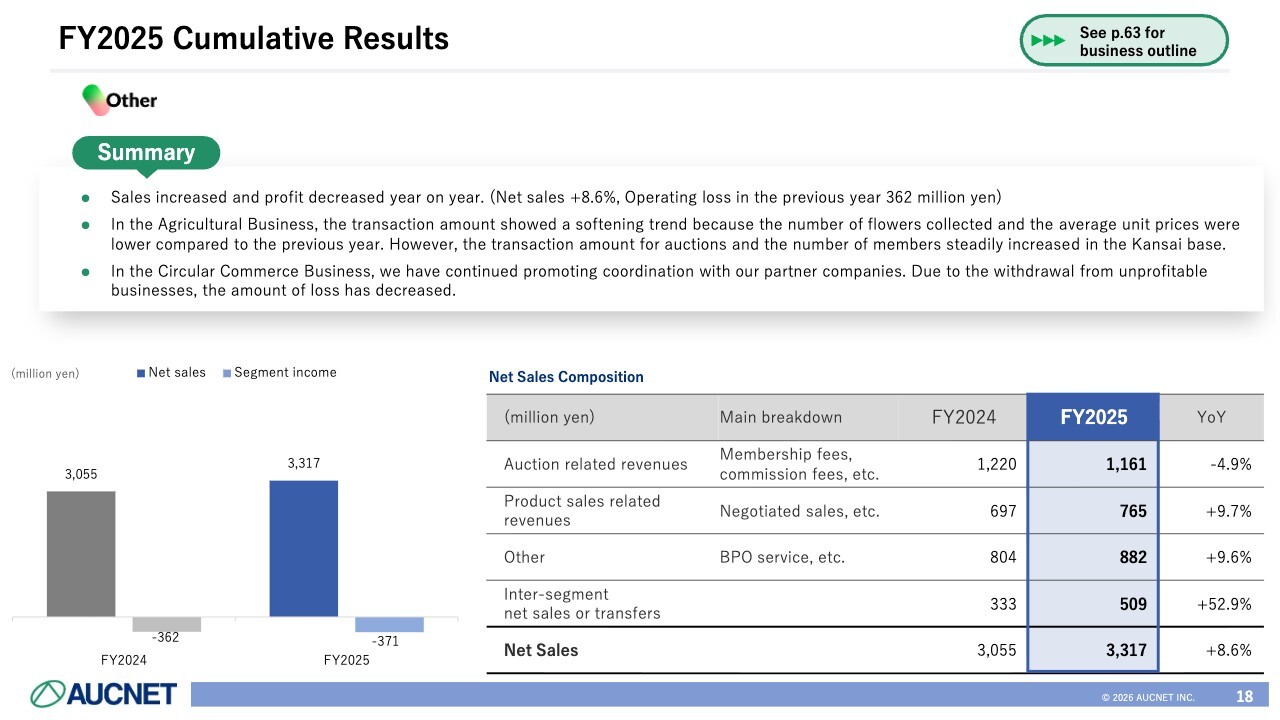

As for the Other business, sales increased and profit decreased year on year. Net sales increased 8.6% year on year, with an operating loss of 371 million yen. In the Agricultural Business, the number of flowers collected and the average unit prices were slightly lower than in the previous year, but the transaction amount for auctions and the number of members at the Kansai base, which has been in operation since the previous year, increased steadily. For our new Circular Commerce Business, we are promoting coordination with partner companies. On the other hand, the loss decreased due to withdrawal from some unprofitable businesses.

Forecast of FY2026 Consolidated Results

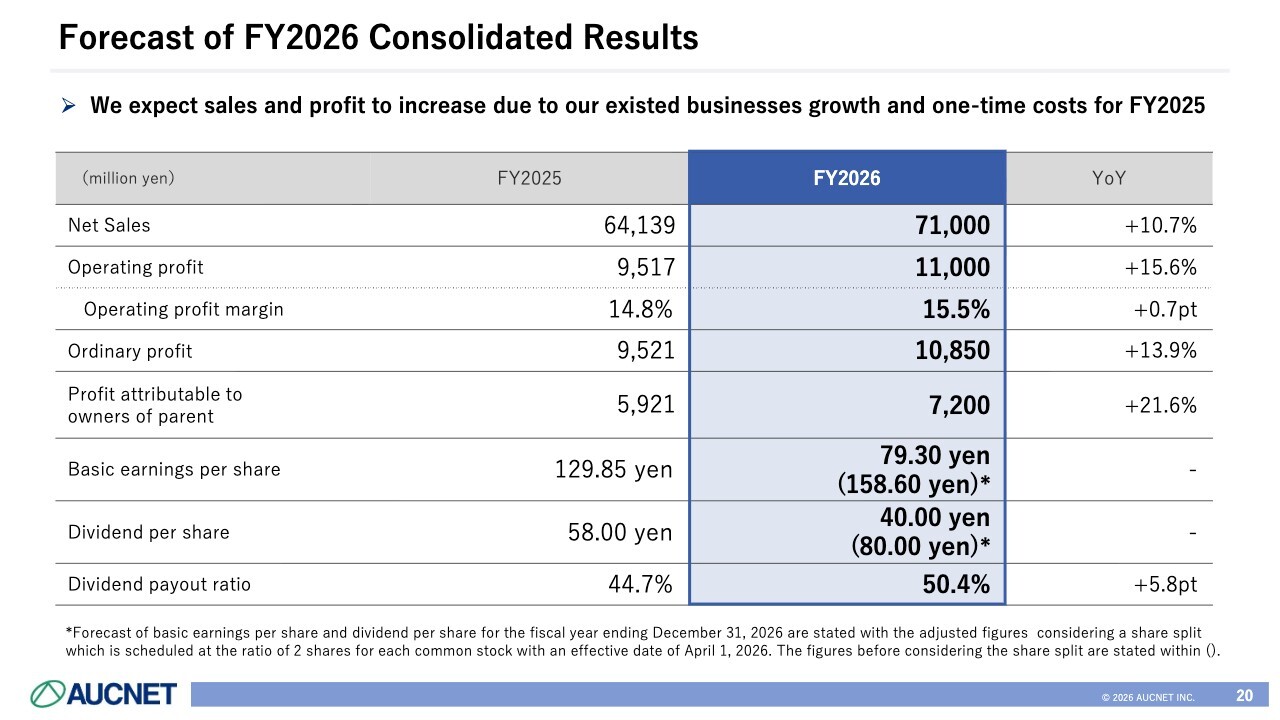

Next, I will explain the forecast for FY2026. For the current fiscal year, we expect an increase in both sales and profit, as growth in existing businesses will be added to the absence of one-time costs incurred in the previous fiscal year. Net sales are targeted at 71.0 billion yen, an increase of 10.7% year on year. Operating profit is targeted at 11 billion yen, an increase of 15.6% year on year. Operating profit margin is expected to be 15.5%, ordinary profit 10,850 million yen, and profit attributable to owners of parent 7,200 million yen.

Basic earnings per share will be 79.30 yen, which would be 158.60 yen if the share split to be explained later is not taken into account. Dividends per share for FY2026 are expected to be 40 yen after the share split and 80 yen before the share split, while a commemorative dividend was added for FY2025. The dividend payout ratio has been set at 40% or more, but for FY2026, we aim to achieve a payout ratio of 50.4%.

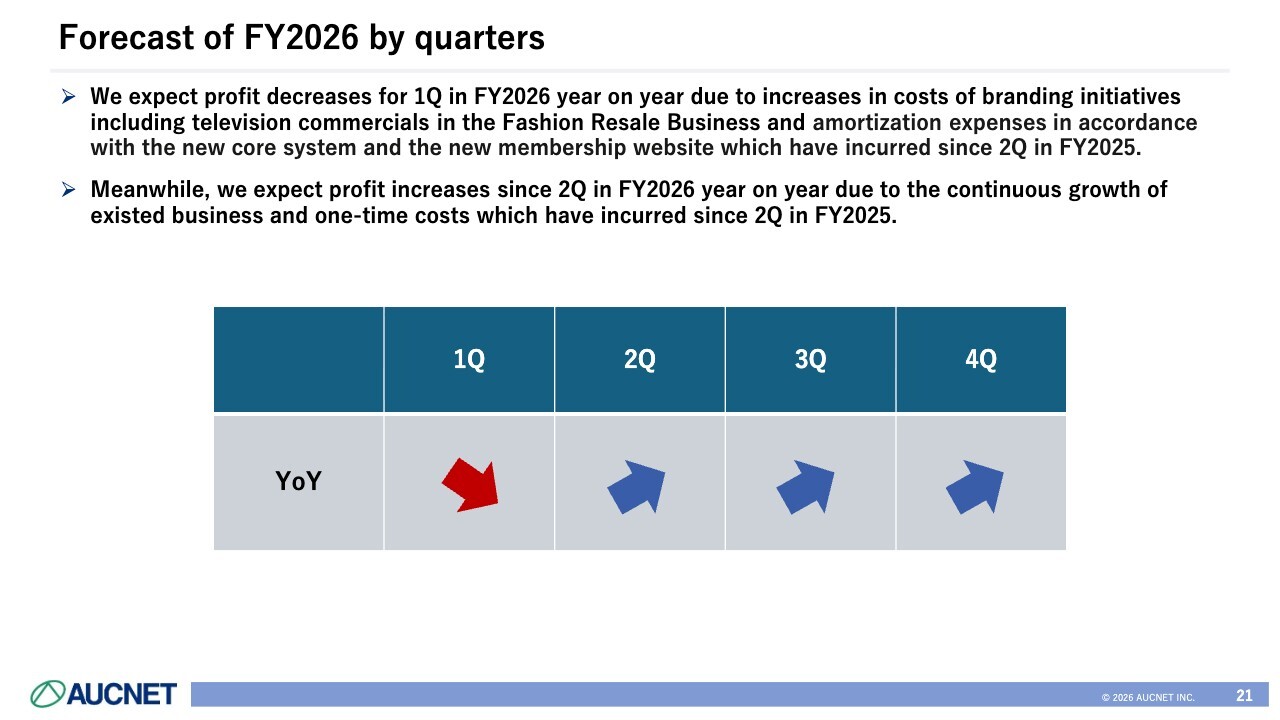

Forecast of FY2026 by Quarter

This is about the quarterly forecast. As represented by the up and down arrows on the slide, the first quarter figures are expected to be slightly lower than the same period last year. We are aiming for an upturn from the second quarter onward, and ultimately for an increase in both sales and profit.

In the Fashion Resale Business, we expect an increase in expenses associated with branding initiatives. Specifically, this is because of the TV commercials featuring Riisa Naka for the Brandear business. Meanwhile, taking into account amortization and other expenses that have been incurred since the second quarter of FY2025, we expect the profit trend to turn upward from the second quarter of FY2026 onward.

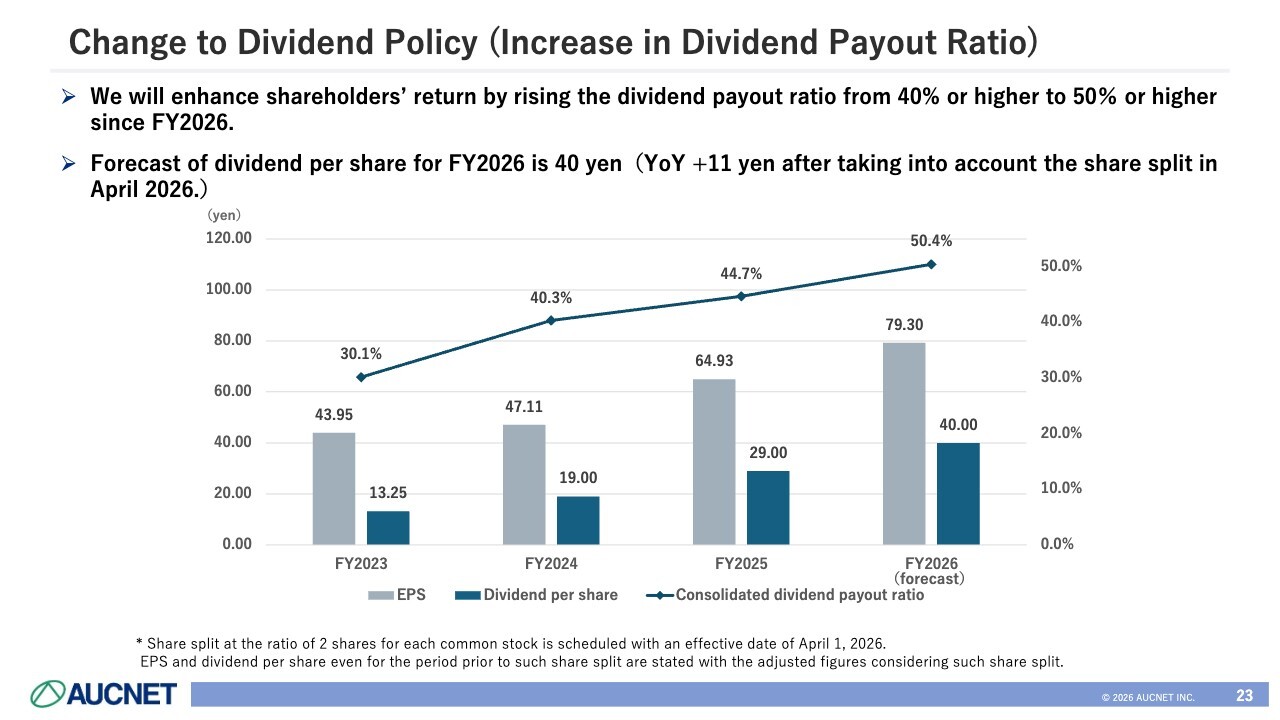

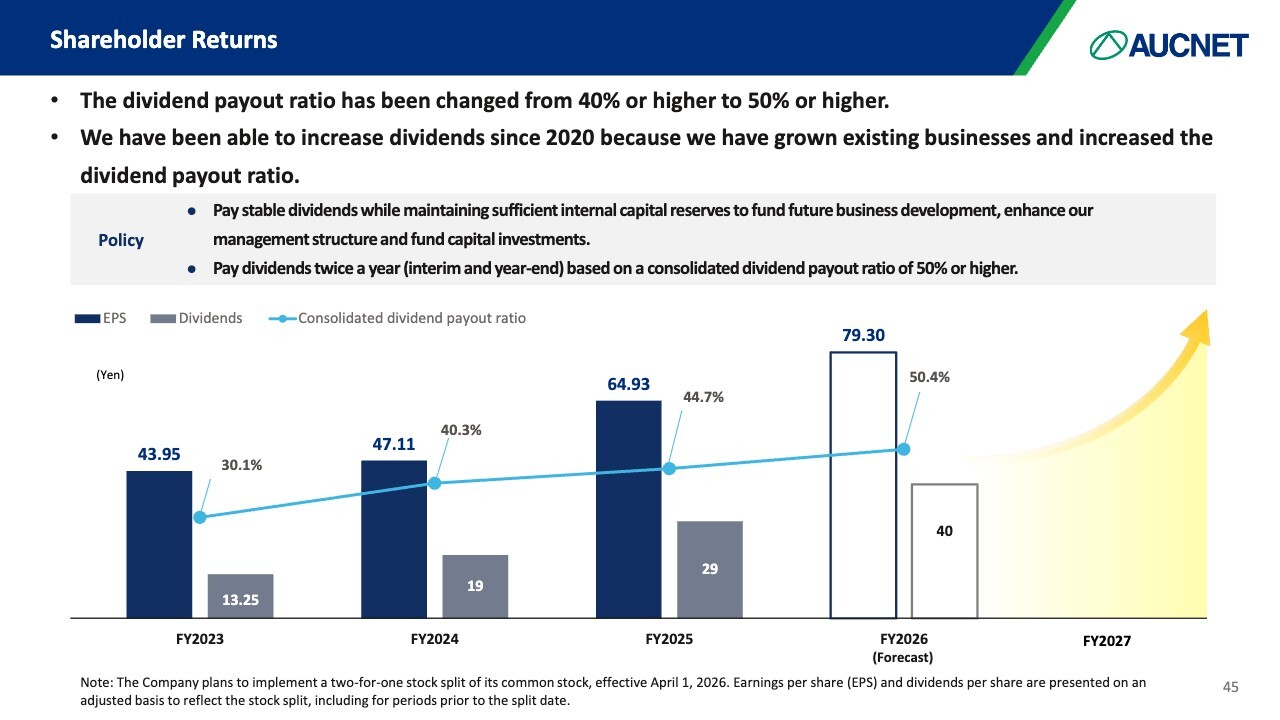

Change to Dividend Policy (Increase in Dividend Payout Ratio)

Next, I will explain the details of the announcement we made during the earnings report. The first is a policy of increasing the dividend payout ratio. The dividend payout ratio, previously set at 40% or more, will be raised to 50% or more from FY2026. This will further strengthen shareholder returns. As a result, we expect the dividend for FY2026 to be 40 yen.

As shown in the graph at the bottom of the slide, the dividend payout ratio was 30.1% for FY2023, 40.3% for FY2024, and 44.7% for FY2025, and we are aiming for 50% or higher for FY2026.

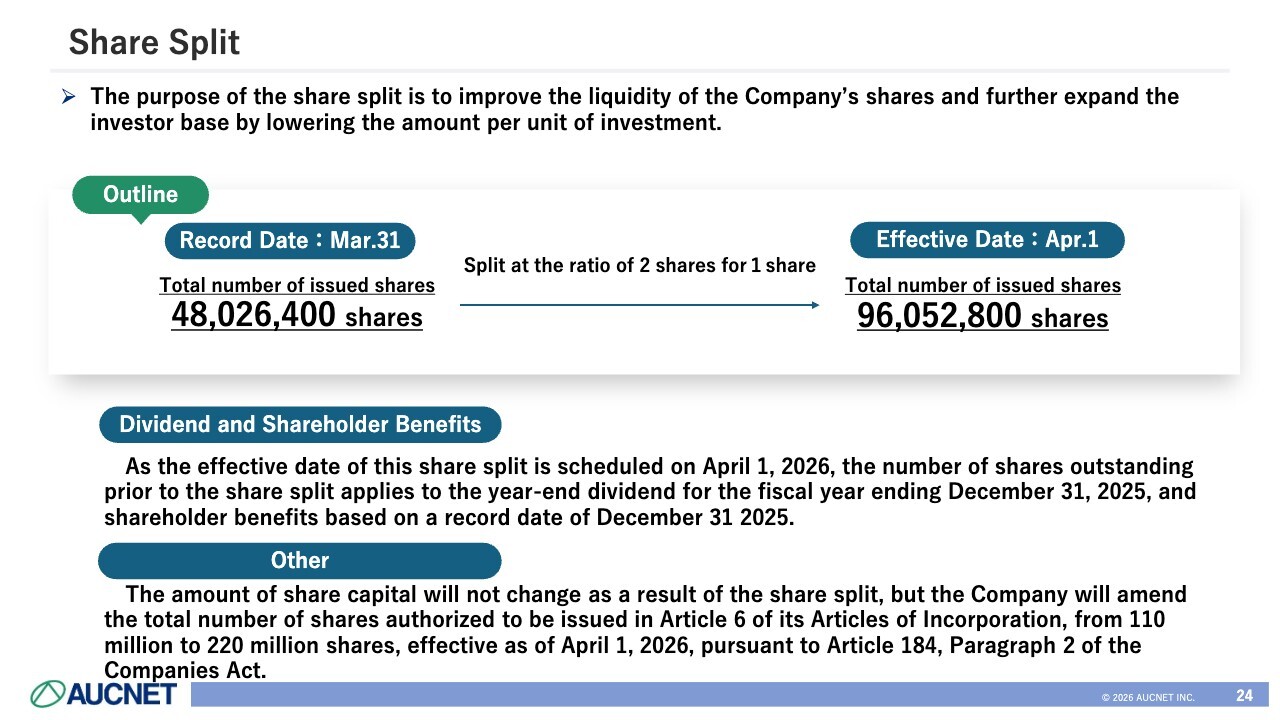

Share Split

We also plan to conduct a share split. Regarding the investment unit price per share, the share price has fortunately been rising and the investment amount per unit has also increased slightly. Therefore, we plan to split our shares effective April 1, 2026, to provide a standard that will make it easier for ordinary investors to invest in the Company. The plan is to split 48 million shares in two.

Summary

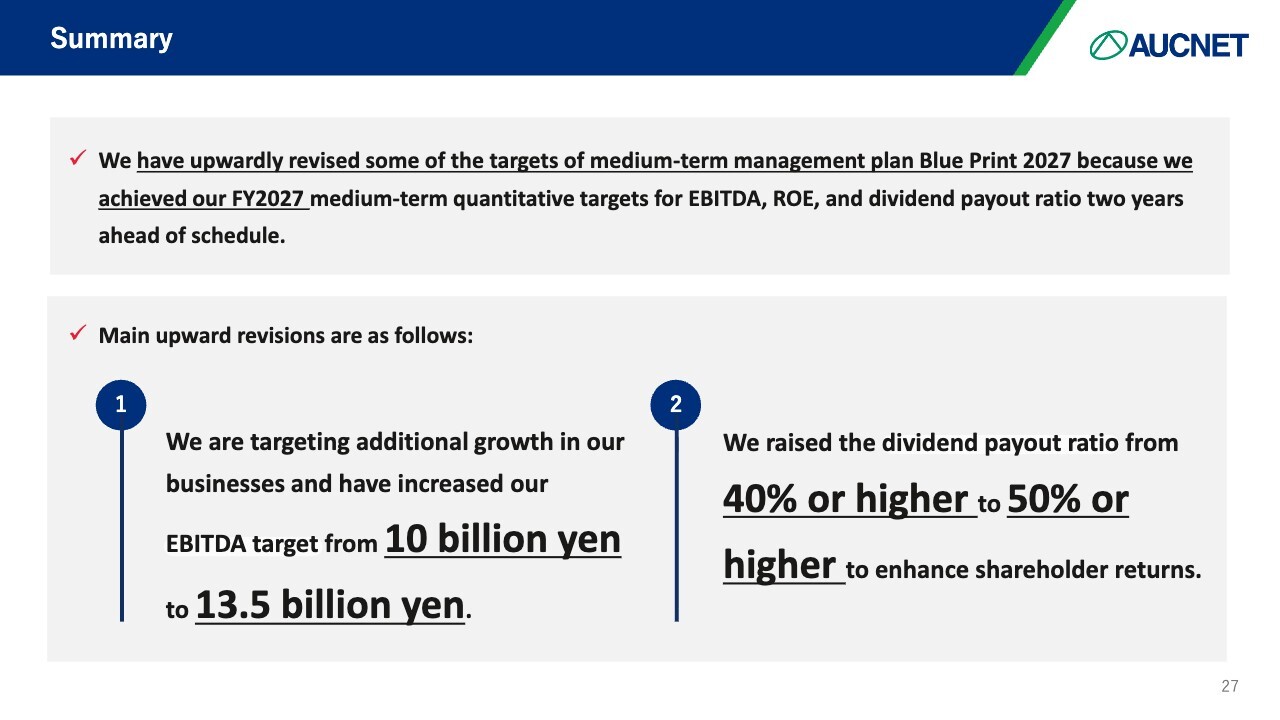

I will now report on our medium-term management plan, Blue Print 2027, though we plan to make some changes.

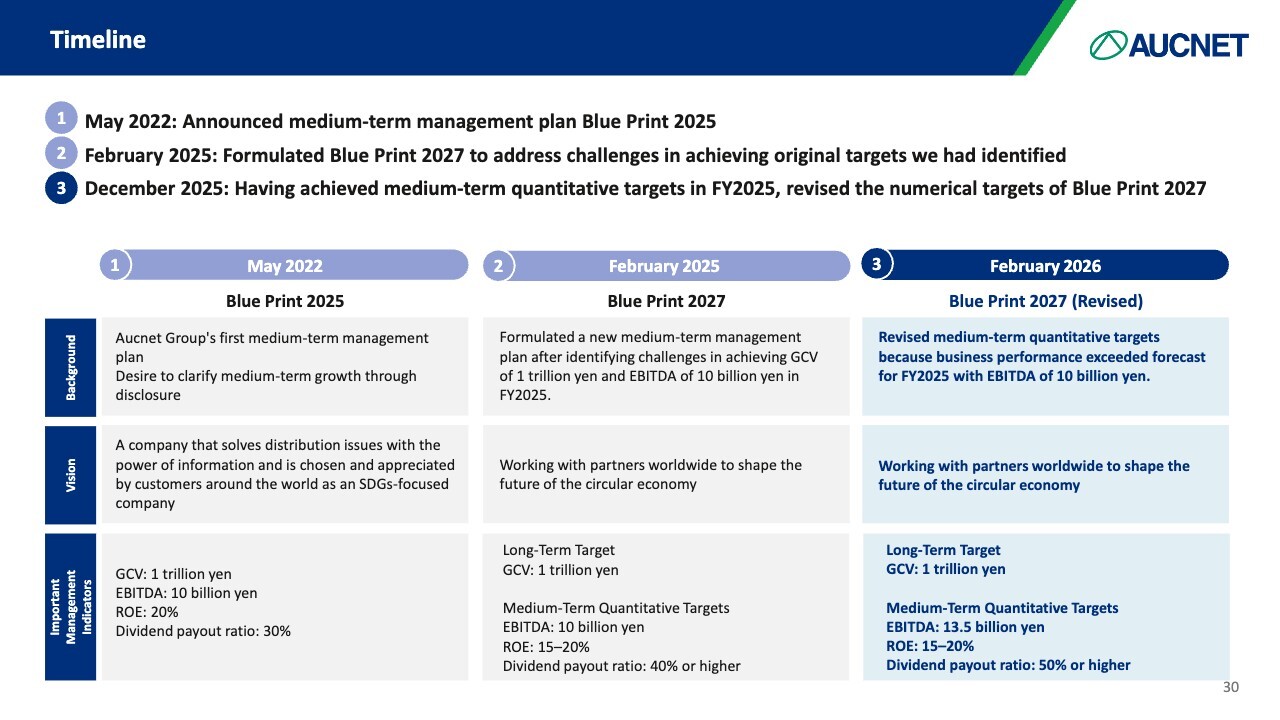

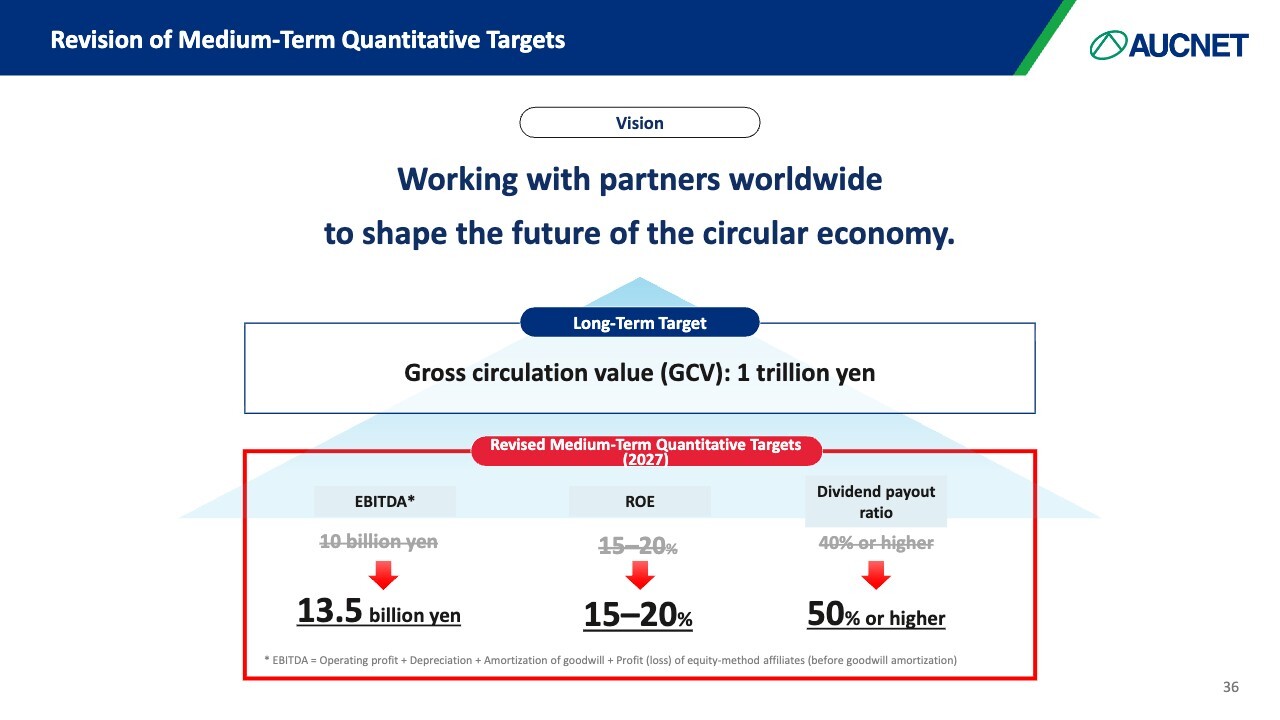

Blue Print 2027 sets goals with an eye toward the end of this and the next fiscal year, with FY2027 as its final fiscal year. We have established EBITDA, ROE, and dividend payout ratio as our three quantitative targets. However, since we achieved our EBITDA target two years ahead of schedule as of last year, we intend to revise some of our quantitative targets upward. The key points of the change are as shown in the slide. In order to achieve further business growth, we would like to raise our EBITDA target from 10 billion yen to 13.5 billion yen.

The dividend payout ratio, previously set at 40% or higher, has been changed to 50% or higher in order to firmly strengthen shareholder returns in light of the Company's balance sheet.

Timeline

Here is a description of the contents of Blue Print 2027. In May 2022, we formulated a medium-term management plan with FY2025 as its final year. However, as of February 2025, we determined that it would be difficult to achieve the target EBITDA of 10 billion yen for FY2025. To this end, we have formulated a new three-year plan, Blue Print 2027, with FY2025 as its first year. As a result, we were able to meet our EBITDA target as of the end of FY2025, which is why we revised some of our numerical targets before the year 2027.

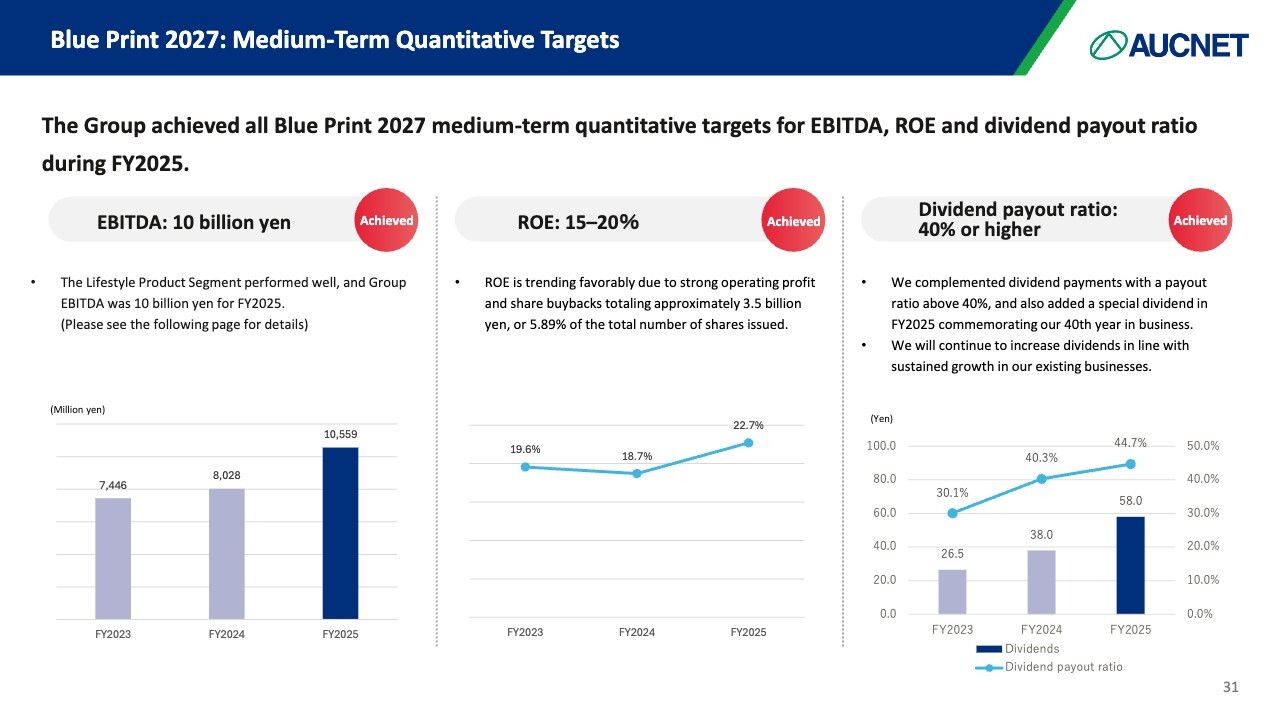

Blue Print 2027: Medium-Term Quantitative Targets

Three quantitative targets are discussed. EBITDA on the left side of the slide had progressed to 7.4 billion yen in FY2023 and 8.0 billion yen in FY2024, so we thought the target of 10.0 billion yen for FY2025 might be a bit challenging. However, we are revising this figure upward because the Lifestyle Products Segment ultimately performed very well, enabling us to reach 10.5 billion yen in FY2025.

As for ROE, we were able to exceed 20% and land at 22.7% for FY2025 as a result of strong operating profit and share buybacks, among other measures.

The dividend payout ratio was originally 40%, but after adding an extra 5 yen as a commemorative dividend for the 40th anniversary of the Company's founding in FY2025, the final dividend payout ratio was 44.7%. The amount of dividends has maintained a steady upward trend due to sustained growth in existing businesses.

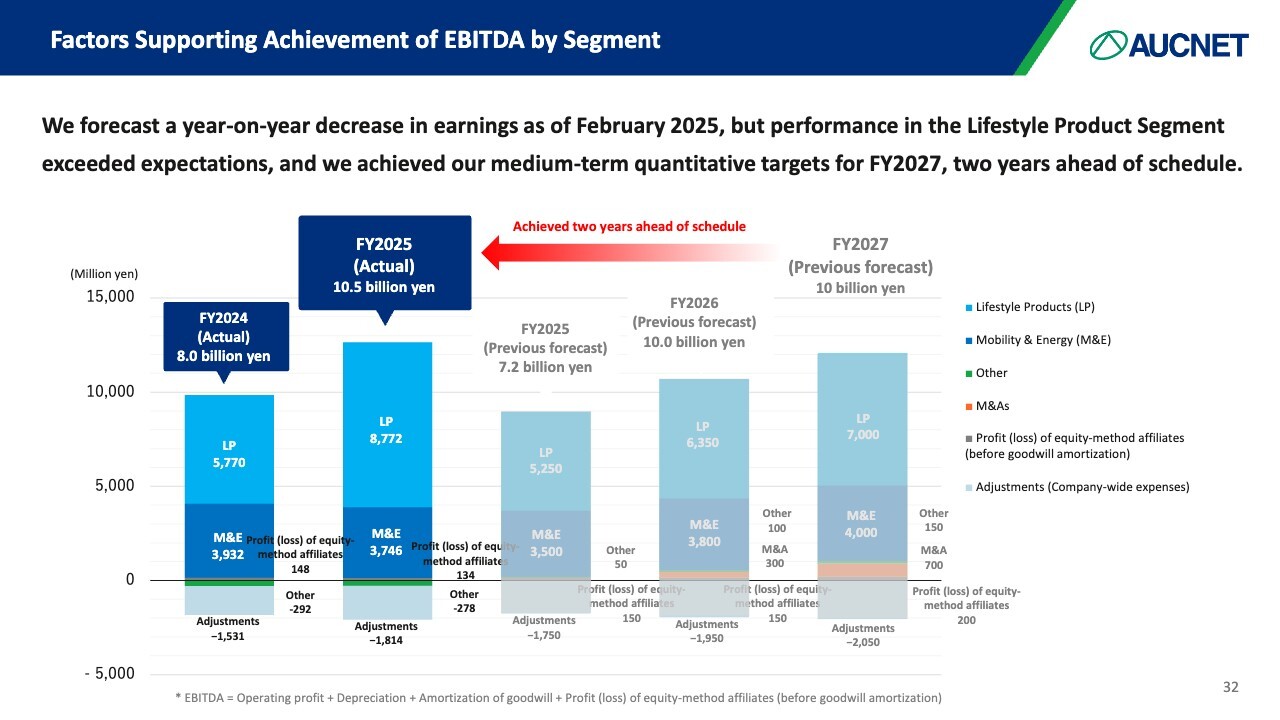

Factors Supporting Achievement of EBITDA by Segment

As of February 2025, we were forecasting an increase in sales and a decrease in profits from FY2024 to FY2025. However, the Lifestyle Products Segment significantly outperformed our forecast, enabling us to achieve our quantitative target for FY2027, two years ahead of schedule.

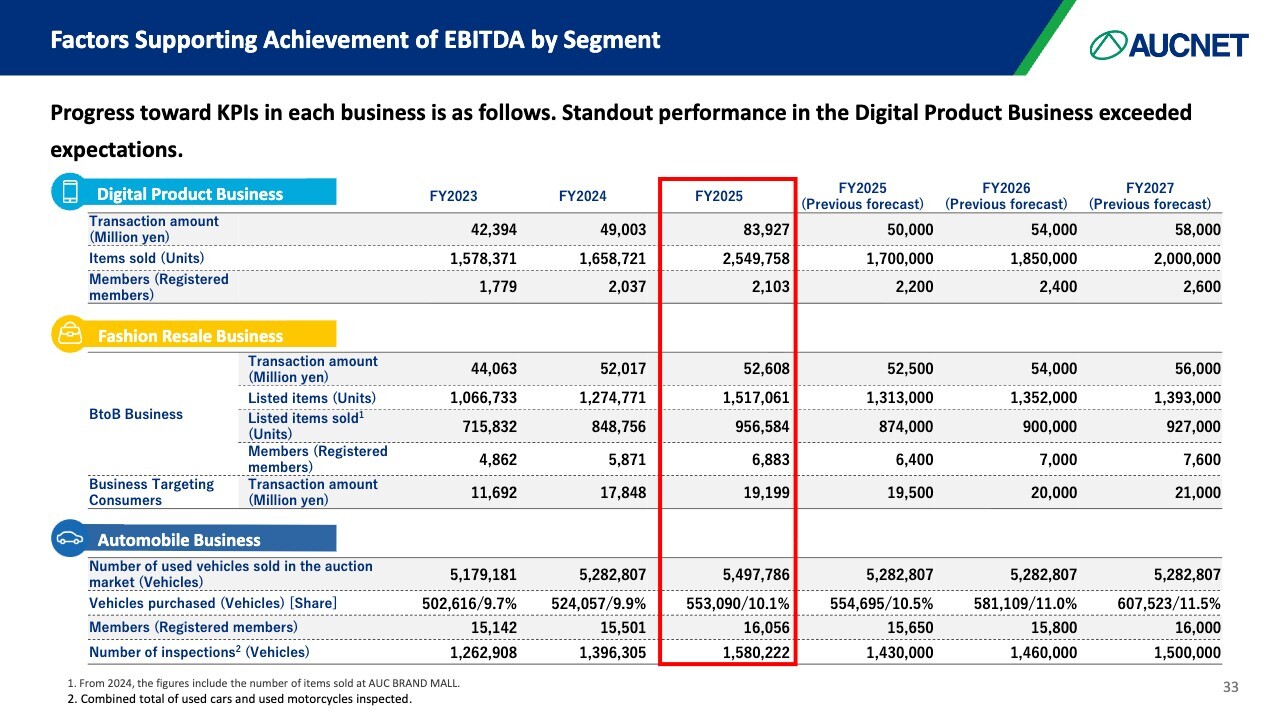

Factors Supporting Achievement of EBITDA by Segment

The Digital Product Business has sold over 2.5 million items, and we are tracking progress based on KPIs. The fact that we have exceeded our forecast for FY2027 at this time, compared to our initial forecast shown on the right side of the slide, was a major driver in this area.

Other businesses are also doing very well. For the BtoB Fashion Resale Business, the number of items sold, which is a particularly important factor, reached 950,000, exceeding the target for FY2027. As for the business targeting consumers, it is in the process of growing, but we will make further investments to achieve returns in the future.

The Automobile Business also continues to perform well, with 550,000 vehicles purchased and a market share of over 10%. Demand is particularly strong in the inspection sector, where the number of vehicles has grown to 1.58 million.

Stock-Related Indicators in Review

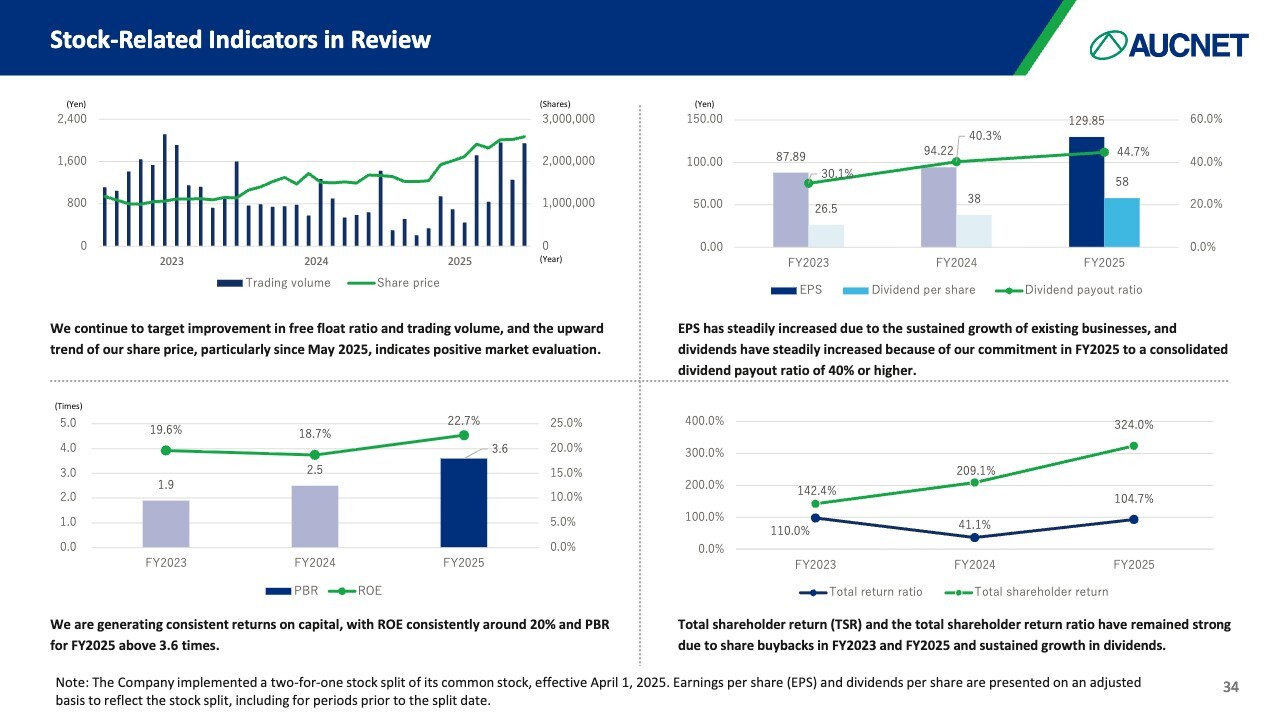

I will review the indicators of the stock. We continue to aim for improvements in the free float ratio and trading volume, shown in the upper left corner of the slide. The share price has been on an upward trend, especially since May 2025, and we believe it reflects the market's positive evaluation. The trading volume declined slightly around 2024, but has remained strong since then due to robust IR activities and, of course, solid performance that followed suit.

Earnings per share have steadily increased due to consistent growth in existing businesses. EPS has also increased. We believe that we were able to steadily increase the dividend amount from 26.5 yen in FY2023 to 58.0 yen in FY2025, backed by the change in the consolidated dividend payout ratio to 40% or higher in FY2025.

ROE has remained at around 20%, and we were particularly able to significantly increase PBR. As of the end of FY2025, the ratio had more than tripled, reaching 3.6 times. We recognize that a certain return on capital has been secured.

With respect to shareholder returns, the total return ratio has exceeded 100% due to share buybacks in 2023 and 2025. Sustained dividend growth has kept the total return ratio and the total shareholder return ratio at high levels.

We aim to provide reliable returns that satisfy our shareholders, and we believe that our ability to do so has led to these results.

Revision of Medium-Term Quantitative Targets

This is a partial revision to the medium-term management plan, Blue Print 2027. There is no change to the vision and long-term target at the top of the slide, but the medium-term quantitative targets have been revised. Specifically, EBITDA is set at 13.5 billion yen, ROE remains at 15% to 20%, and the dividend payout ratio is set at 50% or higher.

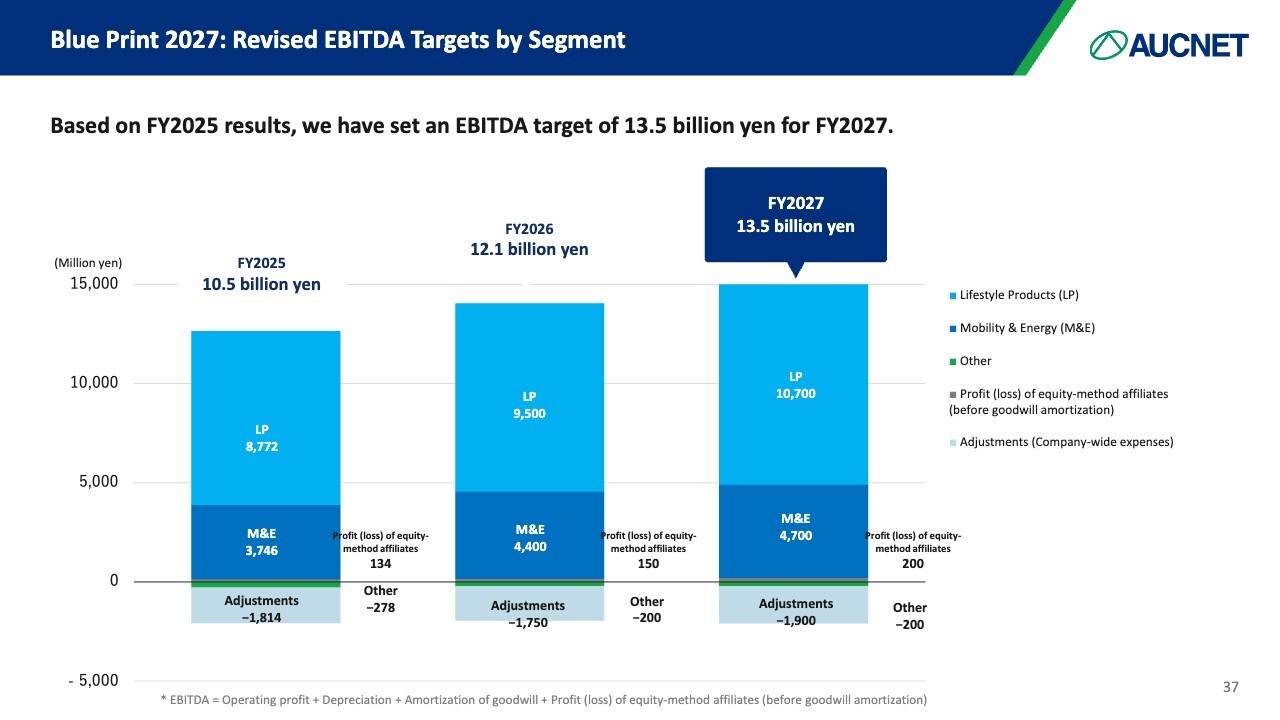

Blue Print 2027: Revised EBITDA Targets by Segment

EBITDA, which was 10.5 billion yen in FY2025, is expected to be 12.1 billion yen in FY2026, and 13.5 billion yen in FY2027. By segment, both the Lifestyle Products (LP) and Mobility & Energy (M&E) segments are targeting growth, with the Lifestyle Products Segment expected to continue to have a higher growth rate.

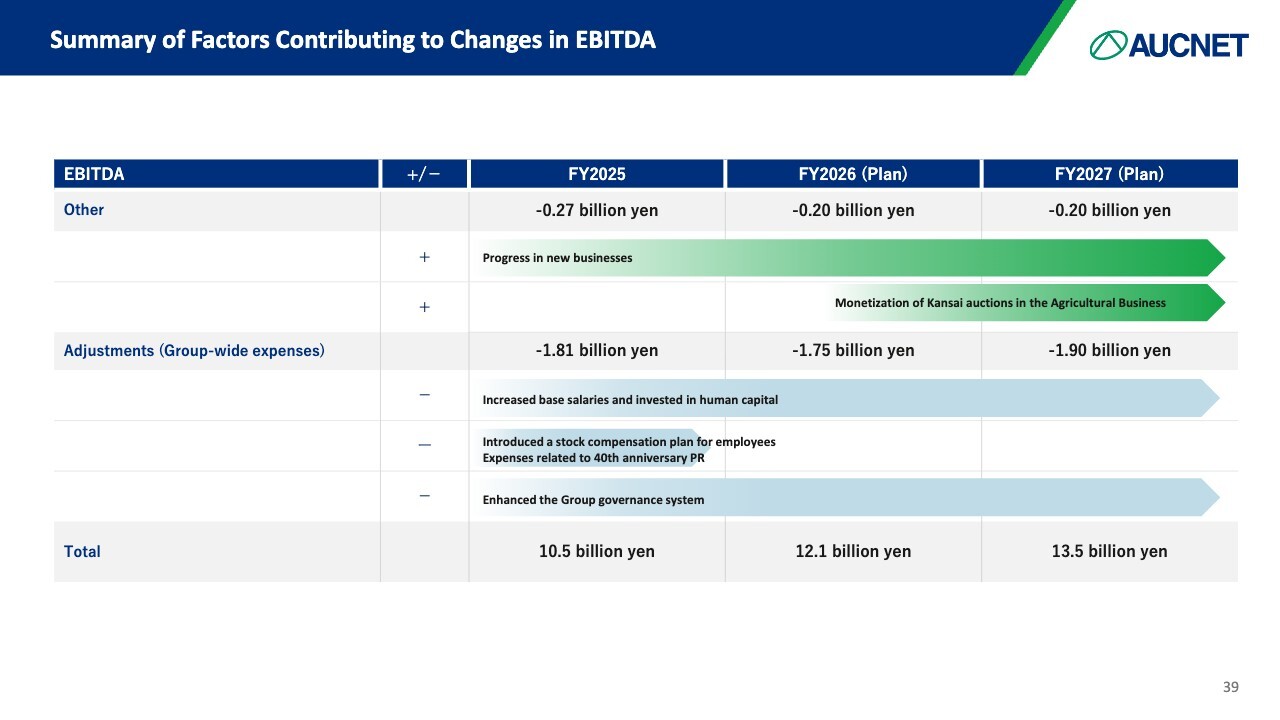

Summary of Factors Contributing to Changes in EBITDA

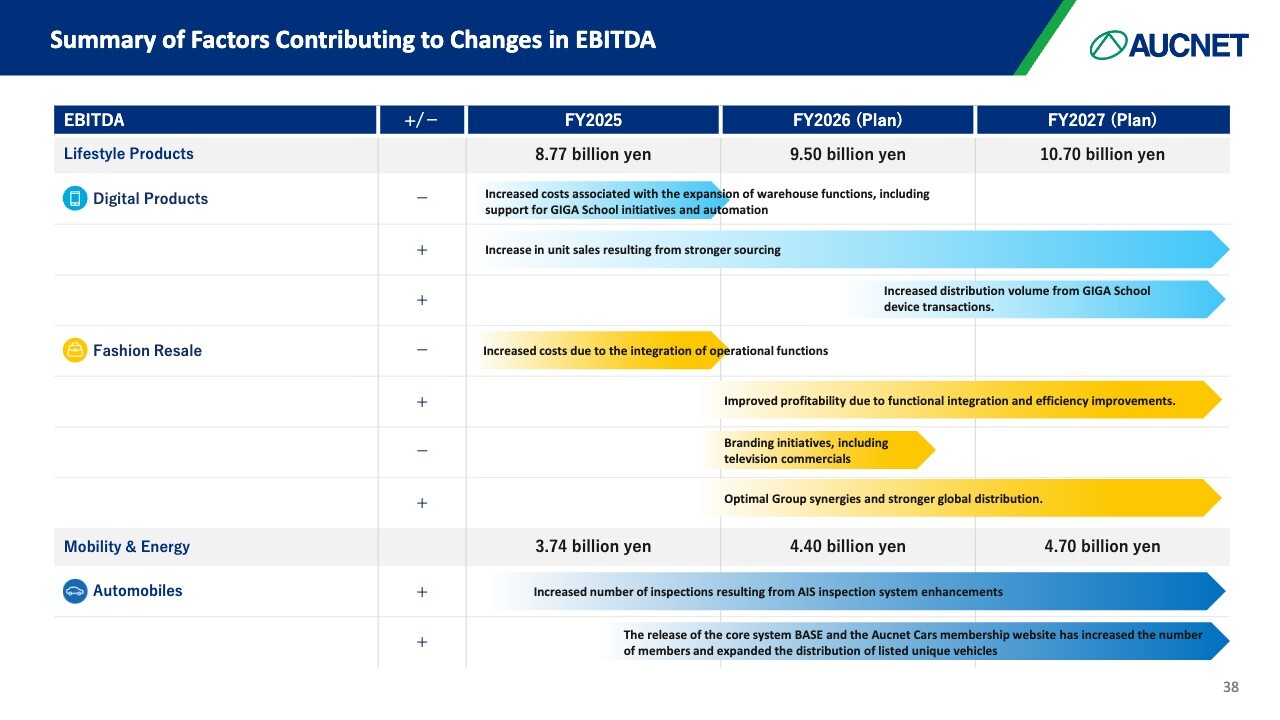

The slide details the factors for increases and decreases in each segment. For the Digital Product Business, there were some costs incurred in FY2025. In particular, some costs increased in the warehouse functions in part due to GIGA School initiatives and automation of the centers. On the other hand, unit sales increased due to stronger sourcing. The number of devices, such as those for GIGA School, is currently expected to increase, and we anticipate this trend to continue through FY2027.

For the Fashion Resale Business, costs increased due to the integration of operational functions from the middle of last year. On the other hand, this functional integration has led to increased efficiency, the results of which are certainly reflected in the current earnings. Therefore, we expect to see this earnings improvement for FY2026 for sure.

In the business targeting consumers, on which we are focusing our efforts, promotional costs are being incurred. However, we are considering synergies between the BtoB and consumer-targeting businesses as our next measure and aim to maximize them. In addition, we would like to establish global distribution, although currently it is mainly from Japan.

Thus, the Digital Product and Fashion Resale businesses will continue to be the drivers of growth, and we are targeting earnings of 10.70 billion yen in FY2027, the final year of the plan.

With respect to the Mobility & Energy Segment, the AIS inspection system in the Automobile Business is a challenge. Although demand is very high, there are still many gaps in coverage because the inspection system has not kept pace. To address this issue, we will secure and train inspectors and aim to increase the number of vehicles inspected.

For the renewed website, we have adopted an agile style of sequentially adding services, rather than releasing full services, in last year's service enhancement. Through this initiative, we aim to improve ease of use and increase membership and sales volume. By implementing these measures, the Mobility & Energy Segment targets revenues of 4.70 billion yen for FY2027.

Summary of Factors Contributing to Changes in EBITDA

As for the Other and new businesses, we plan to steadily materialize the initiatives currently in development. Regarding the Agricultural Business, we are expanding in the Kansai region and promoting it to make it profitable from FY2026 and return it to the black as soon as possible. We aim to create an environment that will enable us to make a solid contribution to earnings in FY2027.

Adjustments (Group-wide expenses) mainly refer to cost control, and we continue to pursue initiatives such as base salary increases and human capital expansion. Specifically, we introduced a stock remuneration plan for employees in FY2025. In addition, we have incurred very significant costs related to PR activities for the 40th anniversary.

Meanwhile, the number of employees has also increased. We are expanding our capital from a human capital management perspective, and in addition to major expenses incurred in FY2025, certain costs are expected to continue to be incurred in FY2026 and beyond.

The Company has grown significantly in scale, including through M&A. With more than 1,100 employees on a consolidated basis, we aim to further strengthen the Group governance system in FY2026 and beyond.

By promoting these initiatives, we seek to increase EBITDA from 10.5 billion yen in FY2025 to 12.1 billion yen in FY2026 and to 13.5 billion yen in FY2027.

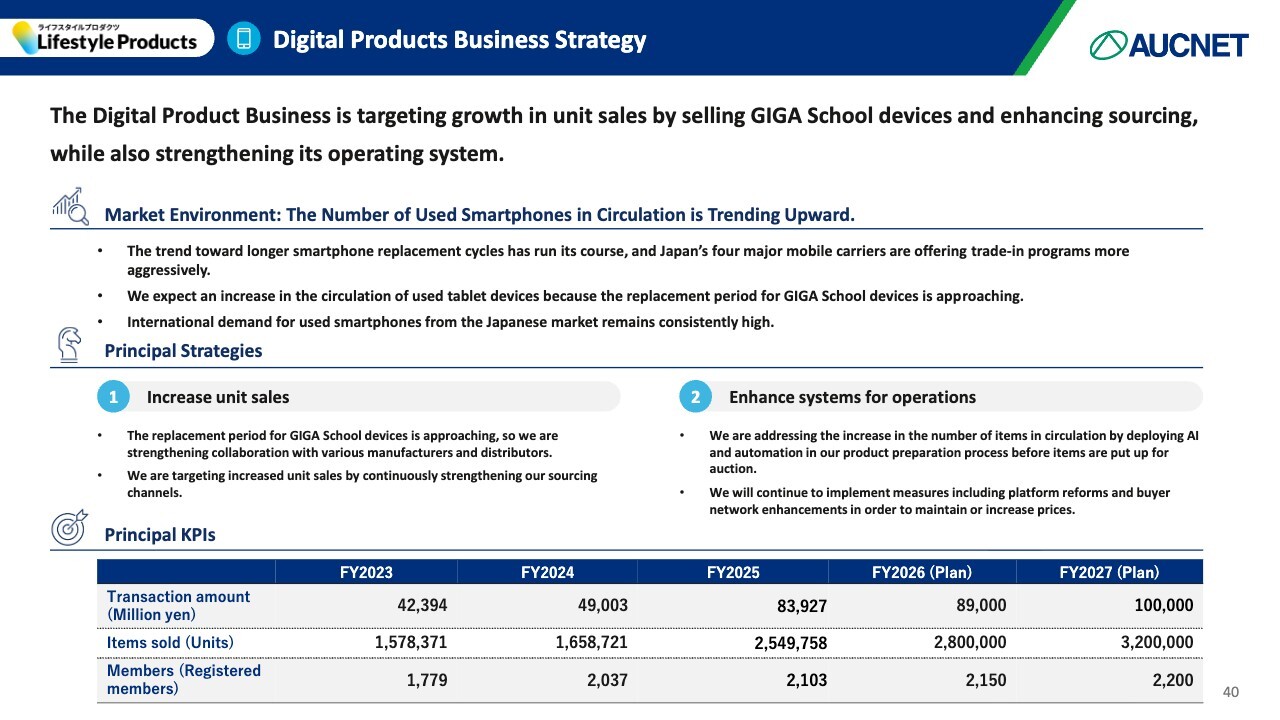

Digital Products Business Strategy

The strategies for each segment are explained below. First, in the Digital Product Business of the Lifestyle Products Segment, we aim to increase unit sales by selling GIGA School devices and enhancing sourcing, while steadily pursuing our existing approach of strengthening our operational system.

In terms of the market environment, the smartphone replacement cycle has run its course after a prolonged period and has become relatively stable. In addition, major mobile carriers are aggressively pursuing trade-in programs, resulting in an increase in the number of trade-in handsets.

Furthermore, the period for the full-scale replacement of GIGA School devices is approaching, and the number of sales units, especially used tablet devices, is expected to increase. Overseas, demand for used smartphones remains high. Based on this situation, we aim to further increase the number of sales units.

There are two principal strategies. The first is an increase in unit sales. As the replacement period for GIGA School devices is approaching, we are strengthening collaboration with various manufacturers and distributors to address this issue. We will continue to develop sourcing and sales channels to increase the number of sales units.

The second is to enhance systems for operations. In the past few years, we have been working to automate our merchandising system up to the point of sale at auction in order to be able to handle an increase in the number of sales units. We intend to continue to implement AI and automation technologies.

Price is also a very important factor. Our services are being selected because of the growing perception that using our distribution channels enables distribution at a higher price. To this end, we will continue to implement platform reforms and enhance our buyer network.

Among the principal KPIs, the number of items sold totaled 2.55 million in FY2025 and is targeted to exceed 3 million in FY2027.

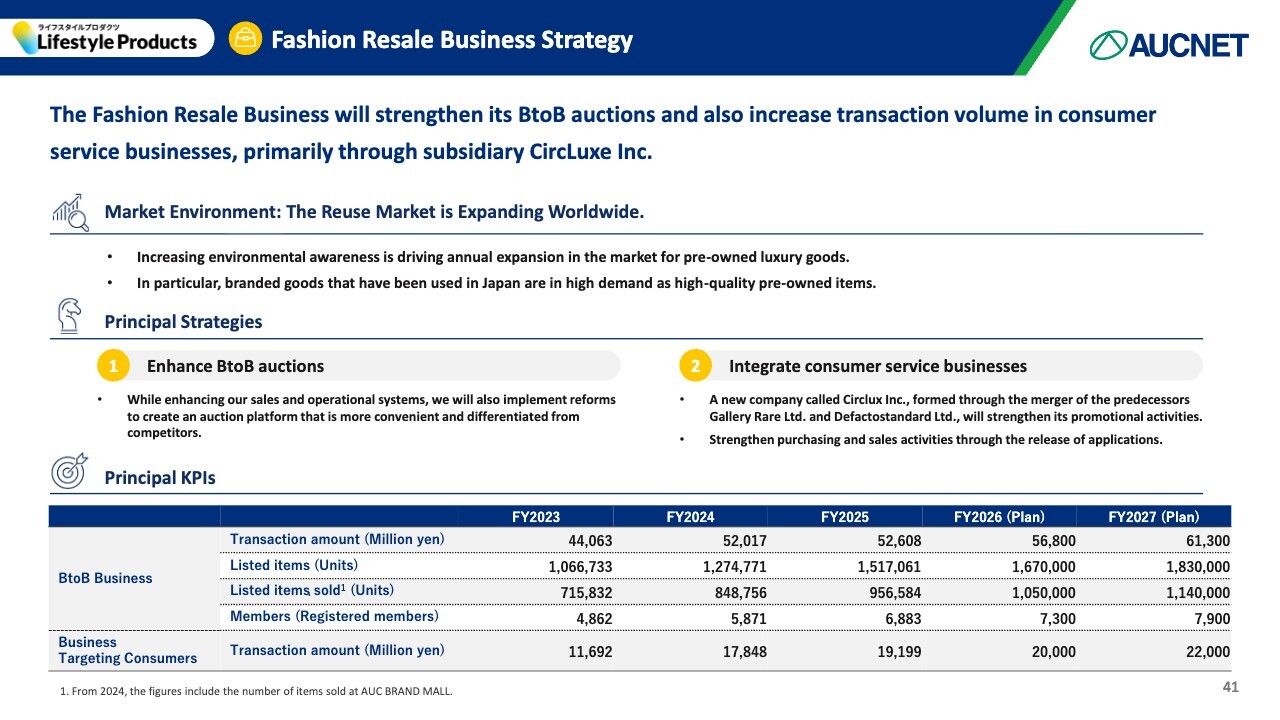

Fashion Resale Business Strategy

This is about the Fashion Resale Business. We will continue to strengthen BtoB auctions, our main business. In addition, the two subsidiaries operating the consumer service businesses were merged as CircLuxe. We also intend to increase the transaction amount in the consumer service businesses.

In terms of the market environment, the reuse market for pre-owned luxury goods continues to increase and expand, backed by growing environmental awareness. In particular, since Japanese people use branded goods with great care, brand-name products used in Japan, known as “Used in Japan,” have become very popular around the world and are expected to remain in high demand.

In this context, there are two principal strategies. The first is to enhance BtoB auctions. Beyond basic enhancements to our sales system and operations, we will also implement reforms to create an auction platform that is highly convenient and differentiates us from competitors. While I believe we have already differentiated ourselves from our competitors in certain areas, we aim to further strengthen these differentiators.

The second is to integrate the consumer service businesses. Last year, we merged Gallery Rare and Defactostandard to form a new company called CircLuxe. Going forward, we intend to firmly strengthen the branding and promotion of CircLuxe. In particular, we would like to release an application for Brandear to enhance purchase and sales, not only through the web but also through the app.

Among the principal KPIs, the number of items sold in the BtoB business totaled 0.95 million in FY 2025, and we aim to increase this to 1.14 million in FY2027. In addition, while the transaction amount for the business targeting consumers was 19 billion yen in FY2025, we seek to increase this to 22 billion yen in FY2027.

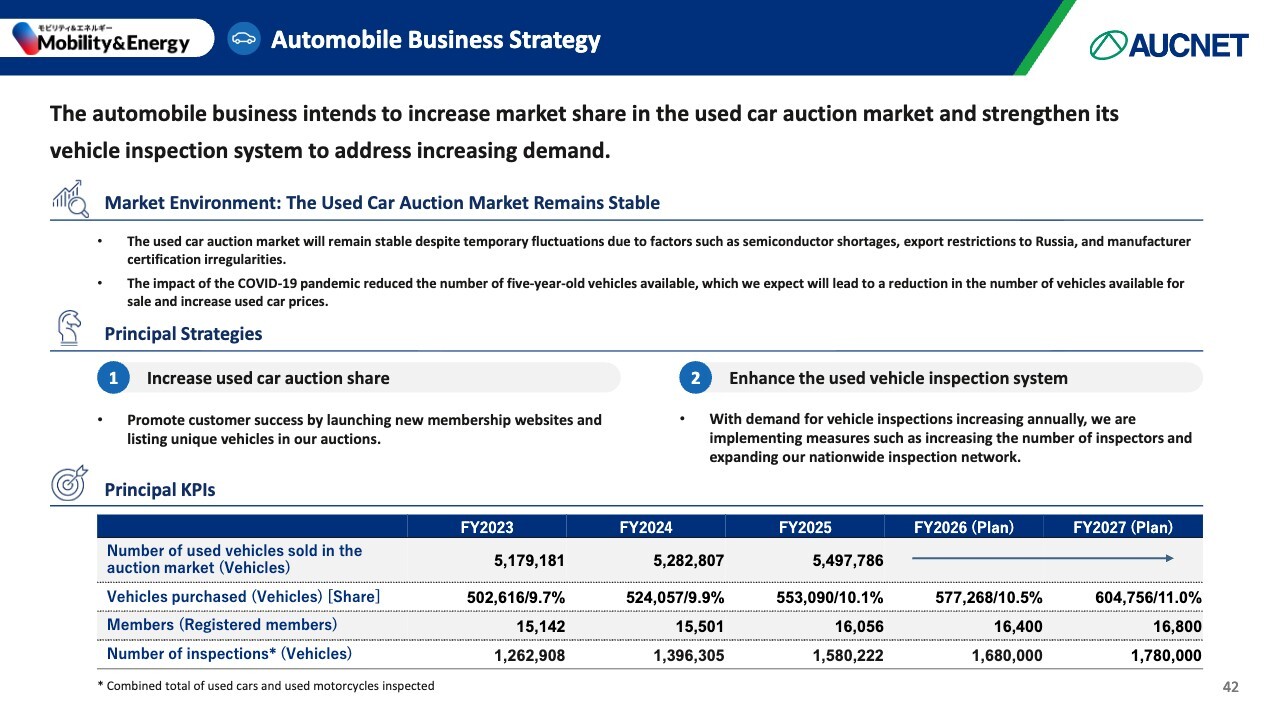

Automobile Business Strategy

This is about the Automobile Business. Our strategy through FY2027 is to continue to increase our share of the used car auction market. In particular, we intend to firmly strengthen our system for vehicle inspection services to address increasing demand.

Although there are many headwinds in the market environment, such as the impact of the semiconductor shortage, export restrictions to Russia, and the issue of manufacturer certification irregularities, we believe that the business environment is relatively stable over the long term.

On the other hand, the semiconductor shortage and other factors have had a significant influence on the new car sales market for about five years due to the impact of the COVID-19 pandemic. As a result, the number of vehicles listed is still declining, and the resulting decrease in supply is expected to continue to drive used car prices higher.

There are two principal strategies. The first is to increase the share of used car auctions. Through the launch of new membership websites and the listing of unique vehicles in our auctions, we will focus on customer success and work to make our company the choice of buyers in the industry.

The second is to enhance the used vehicle inspection services. We intend to increase the number of inspectors and expand our nationwide inspection network to firmly capture inspection demand.

Among the principal KPIs, while the number of vehicles purchased and share was 550,000 units and 10.1% respectively in FY2025, we aim to increase them to 600,000 units and 11.0% in FY2027. We also seek to increase the number of vehicles inspected from 1.58 million in FY2025 to 1.78 million in FY2027.

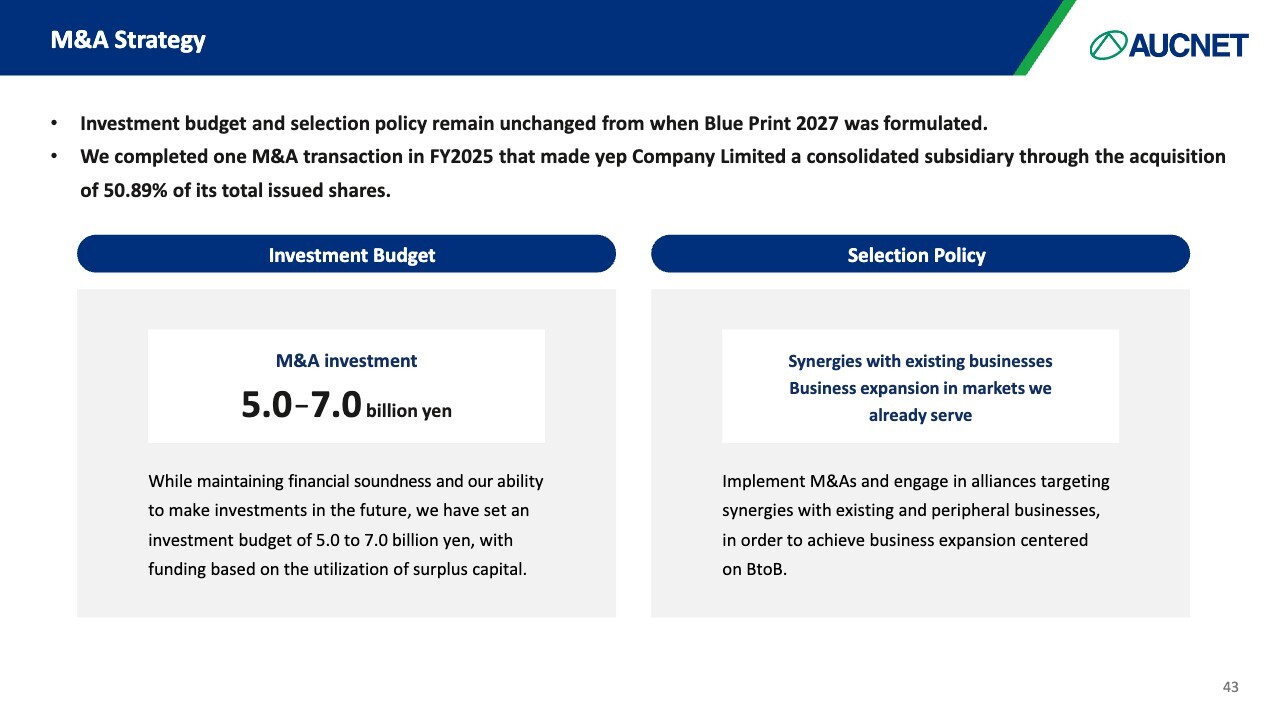

M&A Strategy

With regard to the M&A strategy, the investment budget and policy remain unchanged from when Blue Print 2027 was formulated. The budget for M&A-related investments is set at 5 billion yen to 7 billion yen. This budget is established to ensure the effective use of surplus capital while maintaining financial soundness. As for the current situation, we completed one M&A transaction in 2025 that made yep, a system development-related company, a consolidated subsidiary.

The selection policy is described on the right side of the slide. We intend to continue to implement M&As and engage in alliances, limiting them to areas in the markets we already serve to achieve synergies with existing businesses and business expansion.

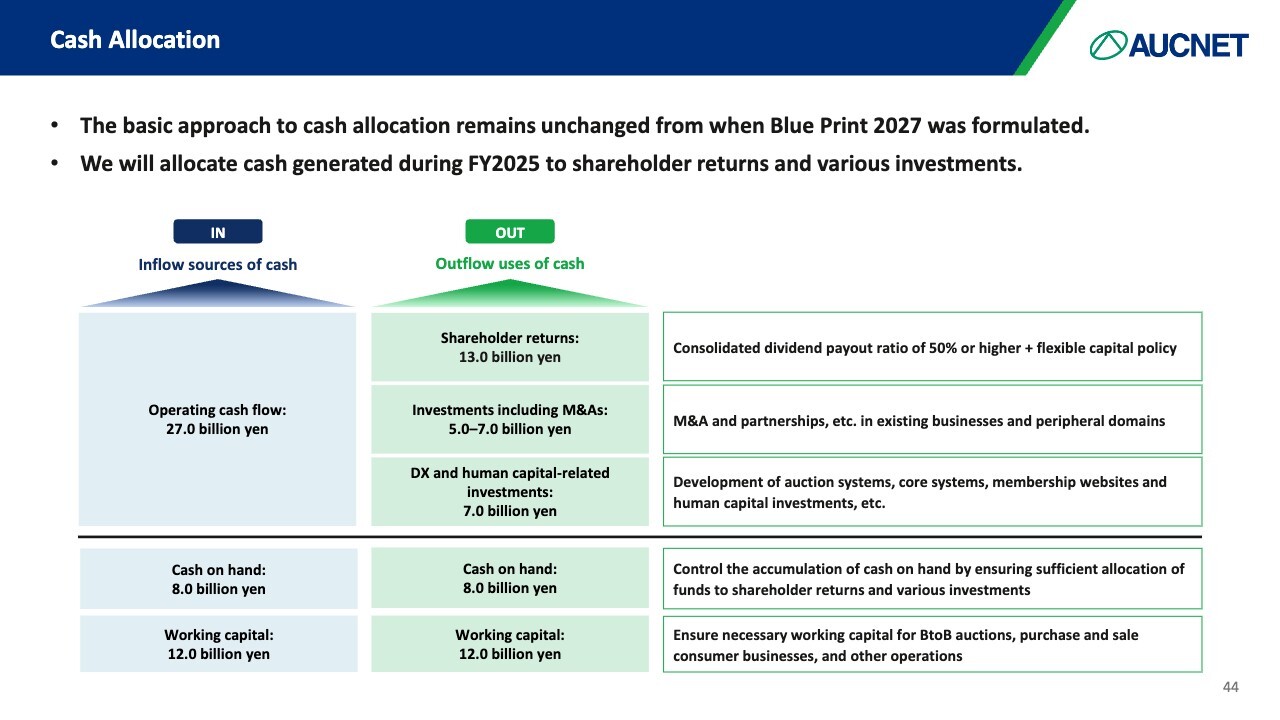

Cash Allocation

This is about cash allocation. There is no change to the basic approach regarding the use of cash that will accumulate if things go according to plan through FY2027. Operating cash flow is expected to build up to 27.0 billion yen, of which about half, 13.0 billion yen, will be used for shareholder returns. We will maintain a dividend payout ratio of at least 50% while implementing a flexible capital policy.

In addition, M&A and other investments are expected to range from 5.0 billion yen to 7.0 billion yen. As a web-based company, we plan to steadily promote DX and allocate 7.0 billion yen for human resource enhancement and human capital-related investments. Through such investments, we aim to achieve both further growth and shareholder returns.

We conduct auctions, which move funds commensurate with the very large transaction amount on a weekly and, in some cases, daily basis. Therefore, we would like to keep 20 billion yen on hand for those demands as working capital.

Shareholder Returns

With respect to shareholder returns, we have increased our dividend payout ratio from 40% or higher to 50% or higher. Dividends have steadily risen since FY2020 due to growth in existing businesses and an increase in the dividend payout ratio. We intend to continue to balance business growth with shareholder returns.

I took the time to share our vision for the future based on our mid-term future. As I said at the beginning that we have recorded our highest profits for five consecutive years, I can truly feel the company is growing in size alongside the increase in the number of employees. We look forward to your continued support as we move forward to become a company worthy of its size.

Q&A: Growth Potential of Digital Product Business

Moderator: We have a question: “Will the growth potential of the Digital Product Business continue this fiscal year?”

Fujisaki: In the Digital Product Business, we believe that the extent to which we can grow our performance, especially in smartphones, will have a very important impact on the achievement of our medium-term management plan through FY2027.

Frankly, we believe that we have achieved more in FY2025 than we had anticipated. We see this as a better-than-expected result, with transaction amount growing about 70% year on year and the number of sales units also increasing over 50% year on year. Although we continue to anticipate progress in acquiring new customers, stronger cooperation with sourcing partners, and an increase in sales units, we do not expect the growth rate to be as high in FY2026 as it was in FY2025.

In FY2026, the handling of GIGA School devices is expected to increase in particular. Therefore, we intend to continue stable growth this year and next by capturing these areas on a firm footing.

Q&A: Future Development of Business Targeting Consumers

Moderator: We have a question: “The results for FY2025 appear strong, except for the business targeting consumers in the Fashion Resale Business. How specifically do you plan to revitalize the business targeting consumers?”

Fujisaki: We operate an auction business for BtoB. While it is relatively affected by world market prices, we have found that the degree of this impact is very large since we started the business targeting consumers. We believe it is extremely important to minimize this negative impact while achieving growth.

Most recently, due to U.S. tariff policies and a decline in the number of visitors to Japan from Greater China, we were unable to successfully attract overseas customers, which led to a decline in market prices and the overall market for the business targeting consumers.

To overcome this situation, we opened an operation center for consumers right next to the operation center for BtoB. We aim to streamline operations by tightly integrating operations for BtoB and for consumers.

In addition, in the business targeting consumers, it is very important how much promotion can be done. We will firmly integrate mid-priced Brandear and high-priced Gallery Rare and advance promotional activities to gain recognition from customers in the business targeting consumers.

Furthermore, in order to facilitate the buying process, we will thoroughly develop not only our website and LINE account but also our smartphone app. We will promote buying through an easy-to-use app with an excellent user experience. As we move forward with this initiative, costs will initially rise slightly at the beginning of FY2026. However, we will strive to capture growth starting from the following fiscal year.

Q&A: Reason for Updating the Medium-Term Management Plan

Moderator: We have a question: “Having achieved the medium-term quantitative targets, I think it would be reasonable to disclose a new medium-term management plan along with an update to the company's overall growth strategy. What was the reason for the decision to update instead?”

Fujisaki: We have made some revisions as an update to our medium-term management plan. We have restructured our three-year plan, and at the end of the first year, the results of our performance are very positive. However, we believe that there are still areas where the results have not yet been fully realized, such as the direction that each business should aim for and the strategies, tactics, and measures that should be implemented over the three years. Therefore, we do not consider these figures to be the result of complete success in these areas, and we believe there is still room for growth in the strategies themselves.

For this reason, while we will update the quantitative targets for profit and revenue, we currently see no need to change the strategies for each business. We will maintain these strategies while steadily improving the numbers. This update focuses solely on revising how we allocate the accumulated cash resulting from this approach and adjusting the quantitative targets.

Q&A: Factors Behind Strong Performance and Cost Usage

Moderator: We have a question: “Have the one-time costs disclosed at the beginning of the period been fully utilized?”

Fujisaki: I think you are asking for confirmation that the strong performance in FY2025 was merely due to these costs not being fully utilized. In conclusion, we have indeed fully utilized these costs. They are appropriately used for subsequent growth.

As I explained earlier, we spent about 700 million yen to transform the business targeting consumers, including integrating warehouse functions for our branded goods business, reforming the business targeting consumers, and closing some stores. In addition to this, we recorded approximately 500 million yen in one-time costs, including for 40th anniversary events and stock remuneration for employees, resulting in total costs of approximately 1.2 billion yen.

Q&A: Factors Contributing to Decline in Profit in Mobility & Energy Segment

Moderator: We have a question: “In the Mobility & Energy Segment, why did segment profit decrease year on year despite strong performance in each KPI and revenue growth?”

Fujisaki: In the Mobility & Energy Segment, about 90% is the Automobile Business, including used vehicles, and less than 10% is the Motorcycle Business. Basically, the market trends and environment are very similar in both businesses.

The number of vehicles listed and sold in the market has seen a slight increase. Meanwhile, exporters are doing well, and with the weak yen, a key factor is the exceptionally strong purchasing power of overseas buyers. Our auctions are characterized by a large number of purchases by exporters, and I believe we were able to take full advantage of this tailwind this year.

As a result, net sales in the Mobility & Energy Segment increased approximately 10% year on year. As you noted, we are growing as a business with a solid increase in commission income. On the other hand, one of the factors contributing to lower profits is the investment in systems, which we have been telling you about for some time. This investment was subject to amortization after release, which was particularly burdensome in the second half of the fiscal year.

In addition, development-related costs included both capitalized assets and one-time expenses, and we believe the impact of these expenses was significant. Furthermore, stock remuneration for employees was recorded as an expense, and the very large number of employees in the Automobile Business also contributed to this impact. For example, the business employs approximately half of our total workforce, including subsidiaries like AIS, an inspection-related company, and i-Auc, resulting in a substantial cost burden.

Since revenue itself has been growing steadily, you can look forward to continued performance in the next fiscal year and beyond.