Contents

Mr. Shinji Oe (“Oe”): Thank you very much for attending our financial results meeting for the fiscal year ended 28 February 2026.

Here is the agenda for today’s financial results presentation: first, FY2026 earnings report; second, FY2026 review; and third, FY2027 projection.

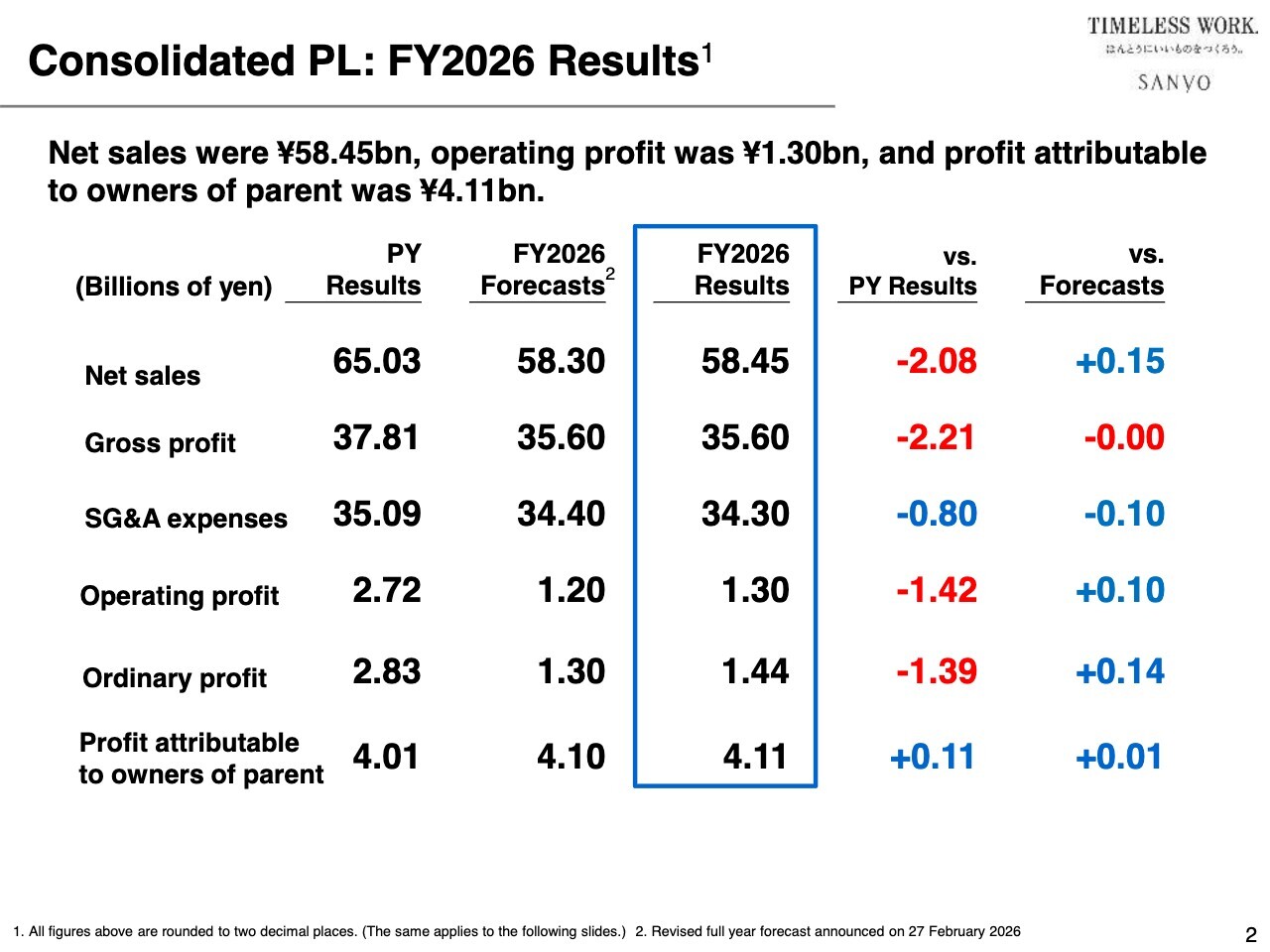

Consolidated PL: FY2026 Results

I will present our results for FY2026. The slide shows the quantitative results, along with YoY comparisons and variances from the forecast. Here, the forecast refers to the revised forecast announced on 27 February 2026.

Net sales totaled JPY58.45 billion, down JPY2.08 billion YoY and JPY0.15 billion above the forecast. Gross profit was JPY35.60 billion, down JPY2.21 billion YoY and in line with the forecast. SG&A expenses came to JPY34.30 billion, down JPY0.80 billion YoY and JPY0.10 billion below the forecast.

Operating profit was JPY1.30 billion, down JPY1.42 billion YoY and JPY0.10 billion above the forecast. Ordinary profit was JPY1.44 billion, down JPY1.39 billion YoY and JPY0.14 billion above the forecast. Profit attributable to owners of parent was JPY4.11 billion, up JPY0.11 billion YoY and JPY0.01 billion above the forecast.

As explained, net sales and all profit lines through ordinary profit decreased year on year. Compared with the initial forecast, results fell significantly short, but compared with the revised forecast, they came in slightly above plan.

Meanwhile, profit attributable to owners of parent increased by JPY0.11 billion YoY, reflecting a gain on sale of investment securities recorded as extraordinary income. It also exceeded the initial forecast by JPY0.01 billion.

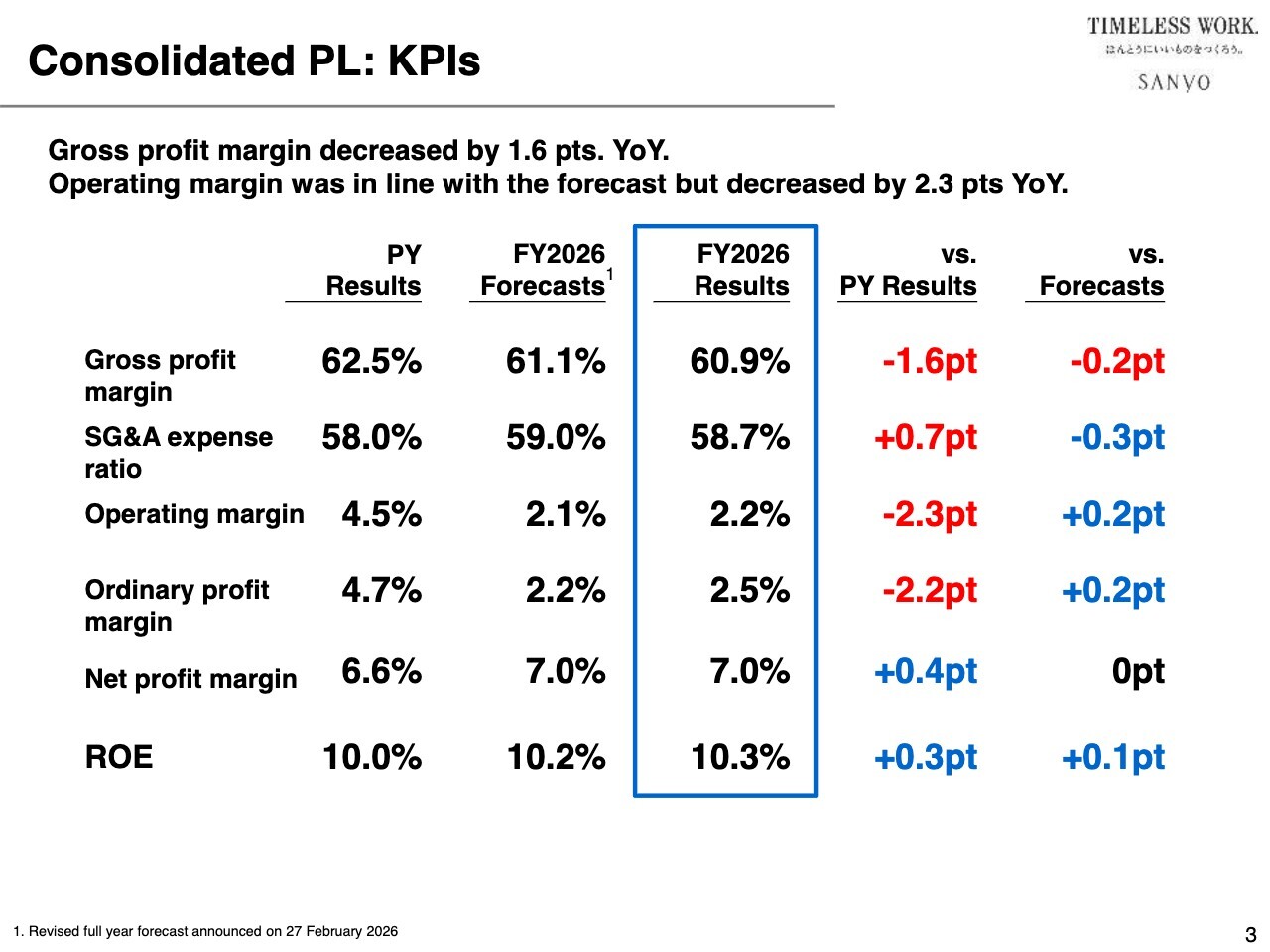

Consolidated PL: KPIs

Let me explain the KPIs. Gross profit margin was 60.9%, down 1.6 percentage points YoY and 0.2 percentage points below the forecast. SG&A expense ratio was 58.7%, up 0.7 percentage points YoY and 0.3 percentage points below the forecast.

Operating margin was 2.2%, down 2.3 percentage points YoY and 0.2 percentage points above the forecast. Ordinary profit margin was 2.5%, down 2.2 percentage points YoY and 0.2 points above the forecast. Net profit margin was 7.0%, up 0.4 percentage points YoY and in line with forecasts.

ROE was 10.3%, up 0.3 percentage points YoY and 0.1 percentage points above the forecast.

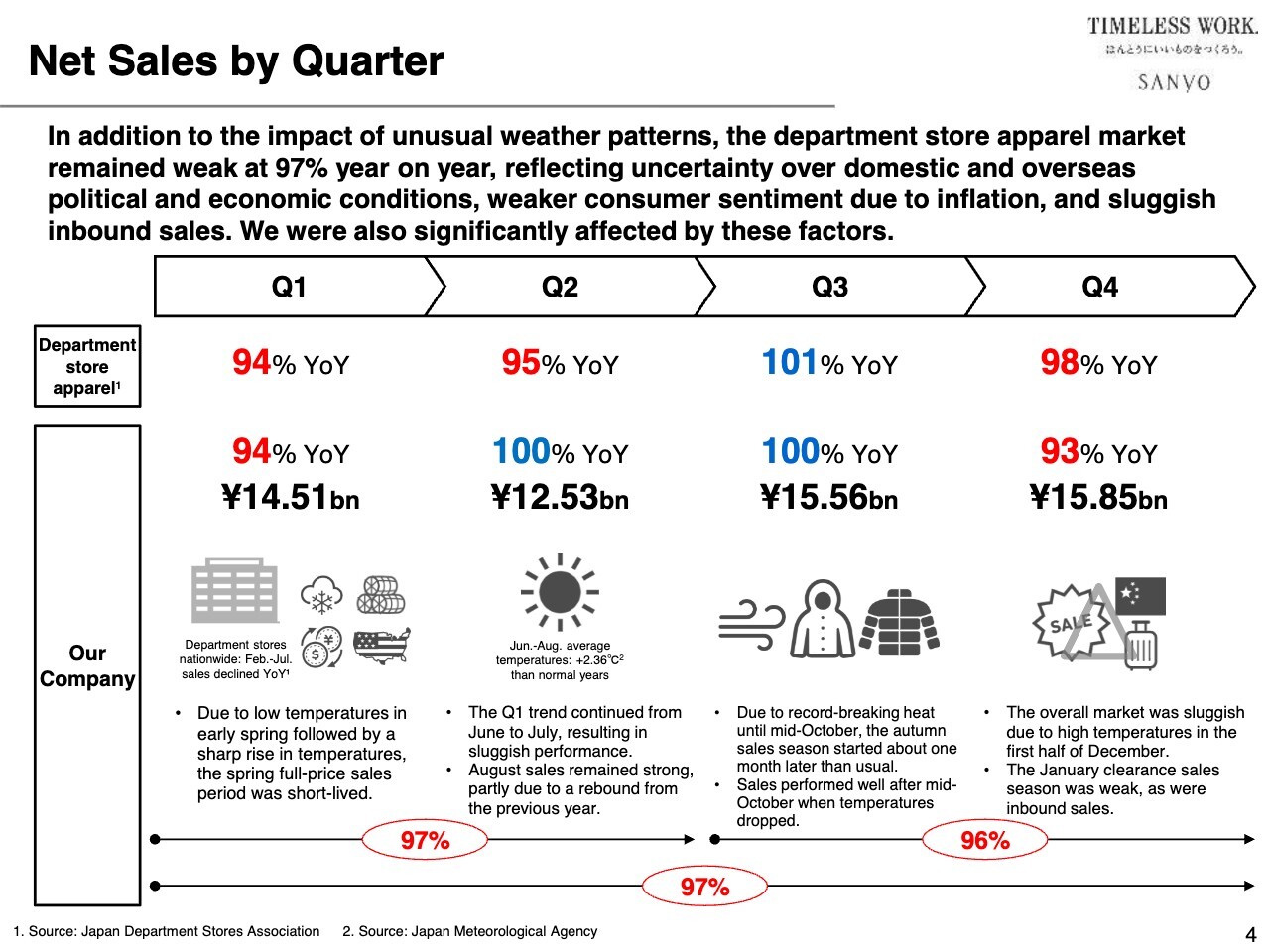

Net Sales by Quarter

This slide summarizes quarterly sales trends. Net sales fluctuated somewhat from quarter to quarter, but remained sluggish throughout the fiscal year, resulting in a full-year outcome of 97% YoY.

Two factors drove this: low temperatures in early spring followed by a sharp rise in temperatures, which shortened the spring full-price selling period, and record-breaking heat from August through early October, which significantly delayed the start of the autumn/winter selling period. As a result, the full-price sales period for autumn/winter was also compressed, reflecting the impact of unusual weather patterns.

Furthermore, uncertainty over domestic and overseas political and economic conditions, together with persistent inflation, heightened consumers’ defensive mindset and weakened consumer sentiment. As price consciousness increased, the low-price mass market remained strong, while the mid- to high-end market was broadly sluggish.

In addition, inbound sales, which had previously driven the market, were weak. This was due in part to factors such as lower demand from Chinese visitors amid heightened concerns over travel to Japan, and inbound sales remained weak throughout the fiscal year. As a result, department stores faced particularly challenging conditions, with apparel sales for the 12 months of FY2025 reaching only 97% YoY.

Because more than 60% of our sales come from department stores, we were directly affected by this weakness.

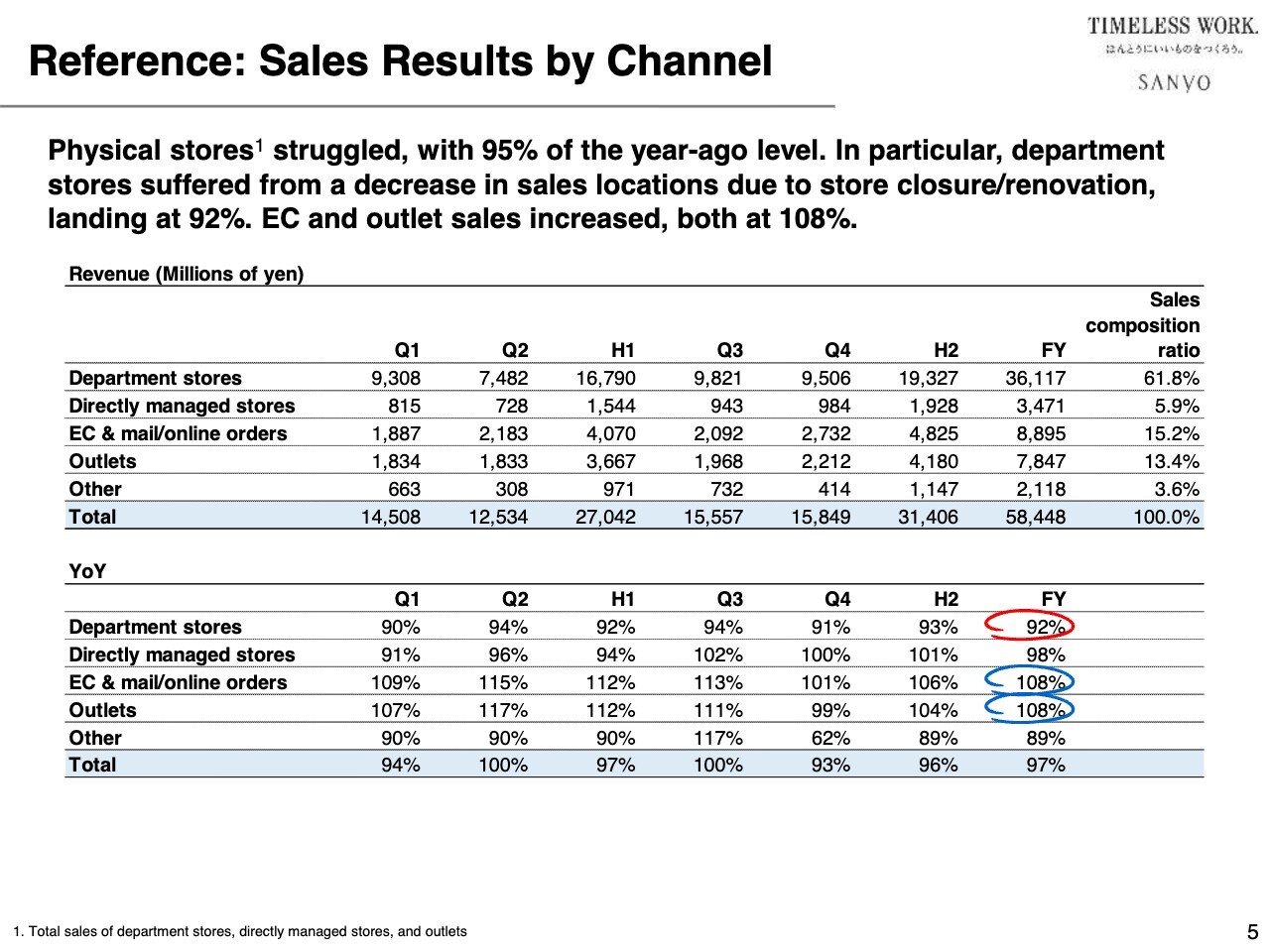

Reference: Sales Results by Channel

This slide shows sales results by channel. First, please look at the bottom section. Department stores were 92% YoY, directly managed stores 98%, e-commerce (EC) & mail/online orders 108%, and outlet stores 108%.

Full-price channels—department stores and directly managed stores—declined YoY, while markdown-driven channels—EC and outlet stores—grew to 108% YoY. This clearly shows that stronger markdown sales offset weak full-price performance.

The top section of the slide shows the channel mix, or sales composition by channel. Department stores accounted for 61.8%, down 2.8 percentage points YoY. Directly managed stores were 5.9%, unchanged YoY. EC & mail/online orders rose to 15.2%, up 1.6 percentage points YoY, and outlet stores increased to 13.4%, up 1.4 percentage points YoY.

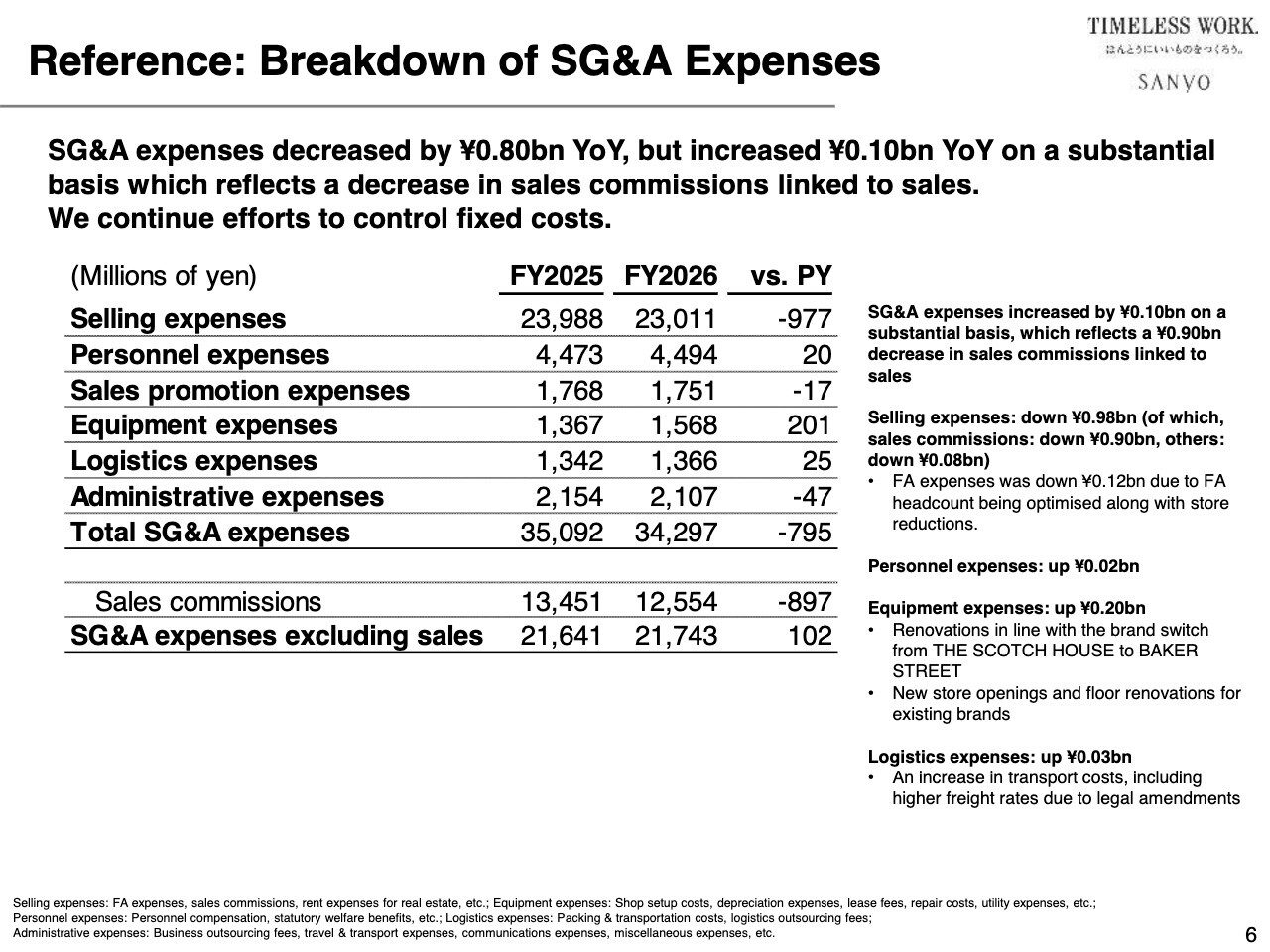

Reference: Breakdown of SG&A Expenses

This slide shows SG&A expenses. As shown, SG&A expenses decreased by JPY795 million YoY. However, this was mainly due to a JPY897 million decrease in sales commissions linked to sales, reflecting the shortfall in net sales.

Excluding this factor, underlying SG&A expenses increased by JPY102 million YoY and came in JPY60 million below the forecast.

YoY changes by item are shown on the right side of the slide.

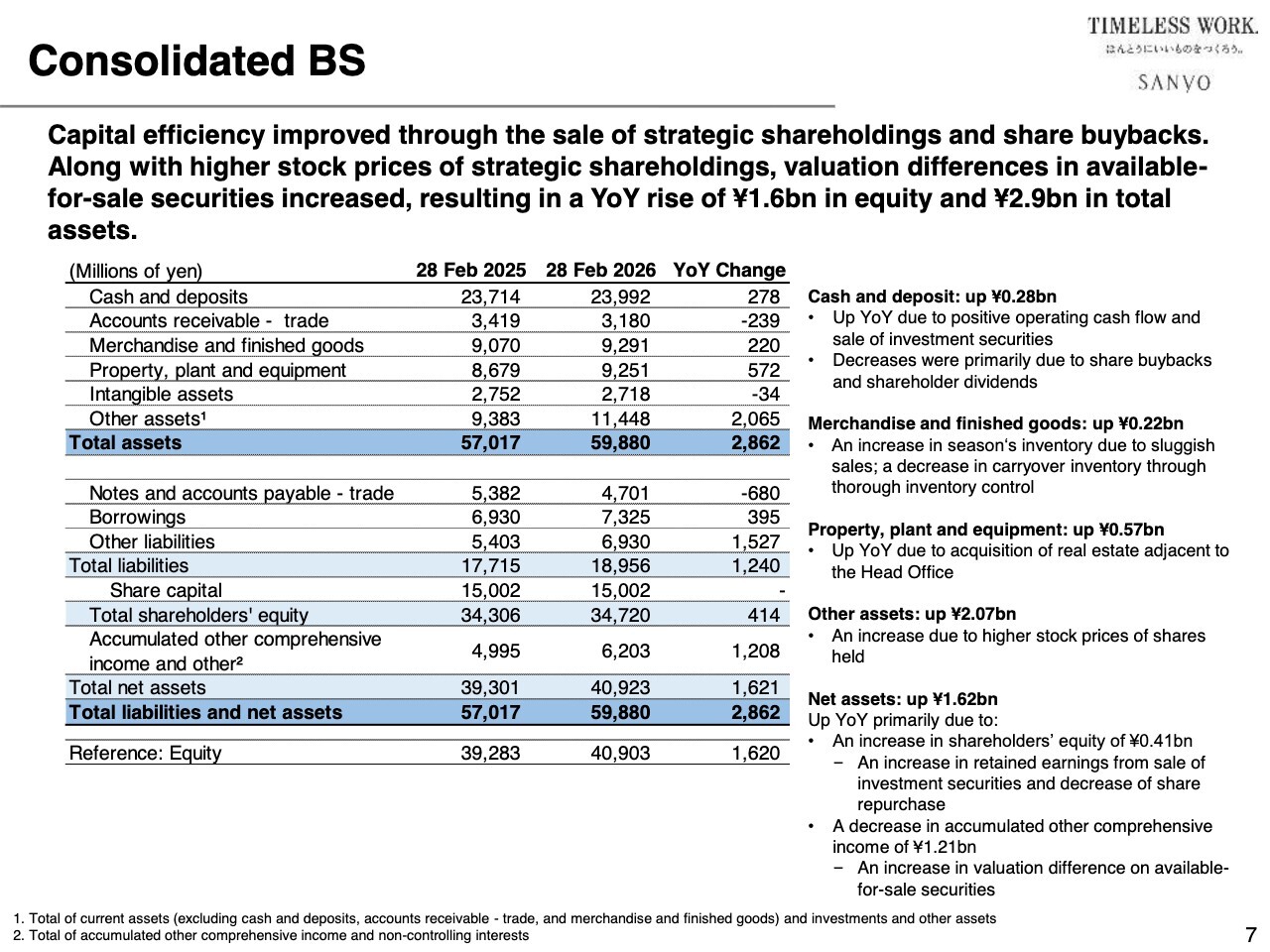

Consolidated BS

This slide presents the consolidated balance sheet. It shows YoY comparisons for the key items. Detailed changes by item are listed on the right side of the slide.

Total assets were approximately JPY59.9 billion at year-end, up JPY2,862 million YoY. Net assets were approximately JPY40.9 billion, up about JPY1,620 million YoY. As a result, the equity ratio was 68.3%, down 0.6 percentage points YoY.

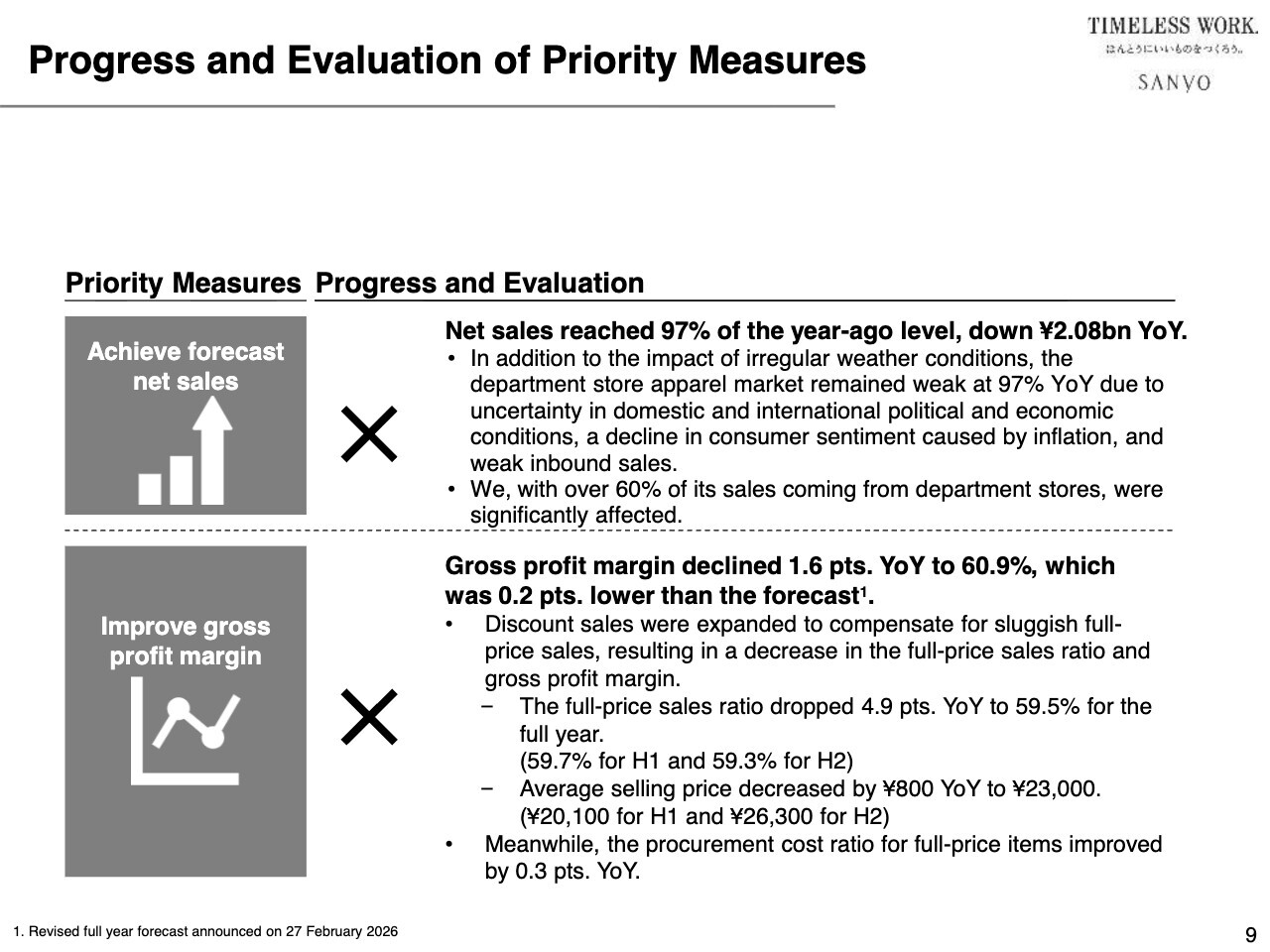

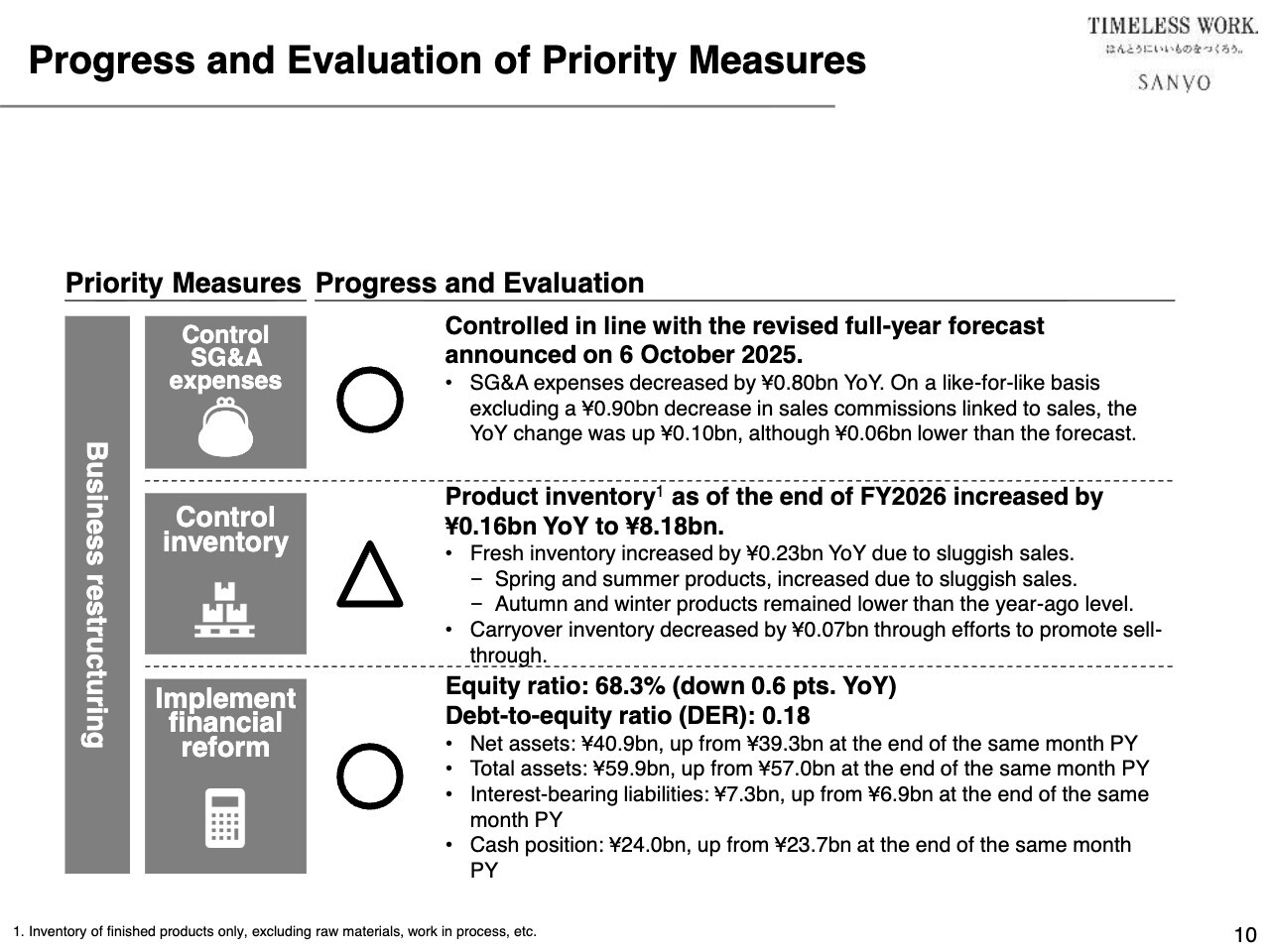

Progress and Evaluation of Priority Measures

I will review our performance for FY2026 and provide our self-assessment. First, on “Achieve forecast net sales,” net sales reached 97% YoY, a decrease of JPY2.08 billion, and we rate this negatively. The reasons are as previously explained.

On “Improve gross profit margin,” gross profit margin was 60.9%, down 1.6 percentage points YoY. It also fell short of the revised forecast by 0.2 percentage points, and we also rate this negatively. Throughout the previous fiscal year, weak full-price sales were consistently offset by markdown sales.

As a result, the full-price sales ratio came to 59.5% for the full year, down 4.9 percentage points YoY. The average selling price also declined by JPY800 YoY to JPY23,000.

Meanwhile, the procurement cost ratio for full-price items improved by 0.3 percentage points YoY. Ultimately, the benefit from cost reductions was offset by the decline in the full-price sales ratio.

Progress and Evaluation of Priority Measures

On “Control SG&A expenses,” SG&A expenses decreased JPY0.80 billion YoY. However, as sales commissions linked to sales declined by JPY0.90 billion, underlying SG&A expenses increased by JPY0.10 billion. That said, SG&A expenses came in JPY0.06 billion below the forecast, and we maintained cost reduction; we therefore rate this as positively.

Next, on “Control inventory,” year-end inventory was JPY8.18 billion, up JPY0.16 billion YoY. However, a closer look shows that fresh inventory for the current and following fiscal year increased by JPY0.23 billion, while carryover inventory declined by JPY0.07 billion. While total inventory increased, the ratio of old inventory declined; we therefore rate this as mixed.

On “Implement financial reform,” the equity ratio was 68.3%, down 0.6 percentage points YoY, but we maintained a high level. The debt-to-equity ratio (DER) remained low at 0.18x, and overall financial soundness stayed solid; we therefore rate this positively.

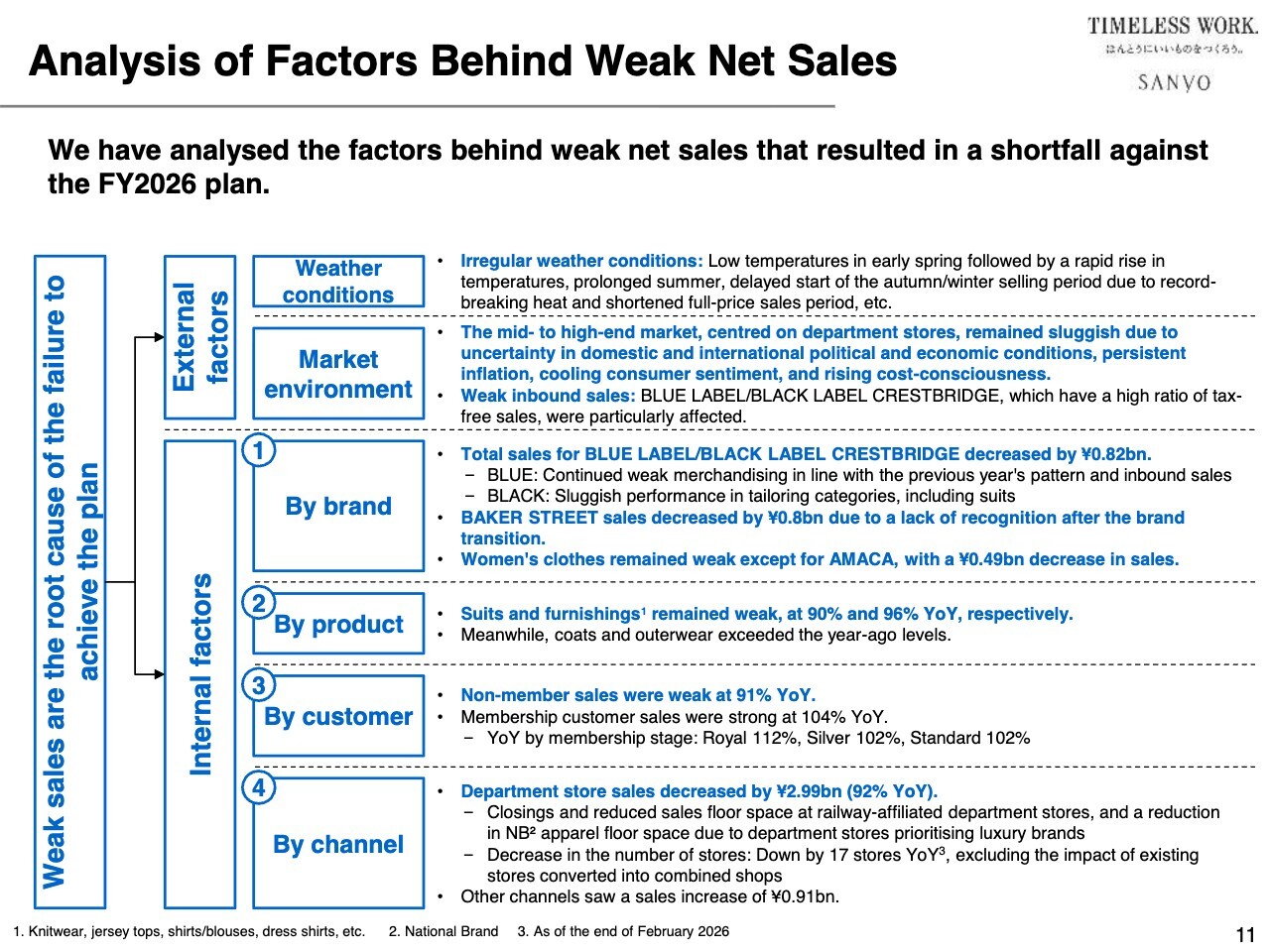

Analysis of Factors Behind Weak Net Sales

This slide summarizes our analysis of factors behind weak sales. As noted earlier, the top line remained weak at 97% YoY, which also led to a deterioration in key KPIs.

In addition to the external factors such as weather conditions and market environment discussed earlier, several internal factors also contributed to the weak sales. These are presented across four dimensions: brand, product, customer, and channel.

First, on the brand dimension. BLUE LABEL/BLACK LABEL CRESTBRIDGE recorded a combined sales decline of JPY0.82 billion YoY. These brands have a relatively high exposure to inbound sales, and inbound sales fell by approximately JPY0.43 billion YoY. In other words, about JPY0.43 billion of the JPY0.82 billion decline was driven by the drop in inbound sales.

In addition, for BLUE LABEL CRESTBRIDGE, merchandising (MD) was somewhat base on the previous year’s approach, and the refresh of the product lineup did not progress as expected. For BLACK LABEL CRESTBRIDGE, another factor was sluggish sales of tailoring items, including suits, which are a core category for the brand.

BAKER STREET recorded a sales decline of JPY0.80 billion on its own. We transitioned this business from the licensed brand THE SCOTCH HOUSE to our private brand, BAKER STREET, following the termination of the license agreement. After the switch, limited brand awareness—particularly the inability to capture sales from non-member customers—led to weaker sales.

Women’s clothes comprises four brands. While AMACA performed strongly, the other three brands were weak, resulting in an overall sales decline of JPY0.49 billion for the segment.

Combined, these four brands recorded a sales decline of approximately JPY2.10 billion, with decreases across three business areas. This decline drove the overall sales shortfall, while the other brands were broadly in line with the previous year.

Next, on the product dimension. Heavy-weight clothing, such as coats and outwear—one of our strengths—exceeded the previous fiscal year. However, suits reached only 90% YoY. In addition, furnishings—specifically light/medium-weight clothing underperformed, reaching only 96% YoY.

On the customer dimension, the various measures implemented for membership customers delivered solid results, with membership customer sales reaching 104% YoY. In particular, sales to top-tier Royal customers rose to 112% YoY, demonstrating the effectiveness of these measures. ON the other hand, sales to non-member customers remained at 91% YoY.

On the channel dimension, sales at department stores declined to 92% YoY, resulting in a decrease of approximately JPY3.00 billion in this channel alone. In contrast, channels other than department stores generated an increase in sales of JPY0.91 billion.

As for the weakness in department store sales, in addition to the overall department store market declining YoY, some railway-affiliated department stores were closed or downsized, and floor space was also reallocated under policies prioritizing luxury brands. As a result, the number of our department store sales locations effectively decreased by 17 YoY.

In summary, department store sales were impacted by both a weak overall market and a reduction in our sales floor space, resulting in performance of 92% YoY.

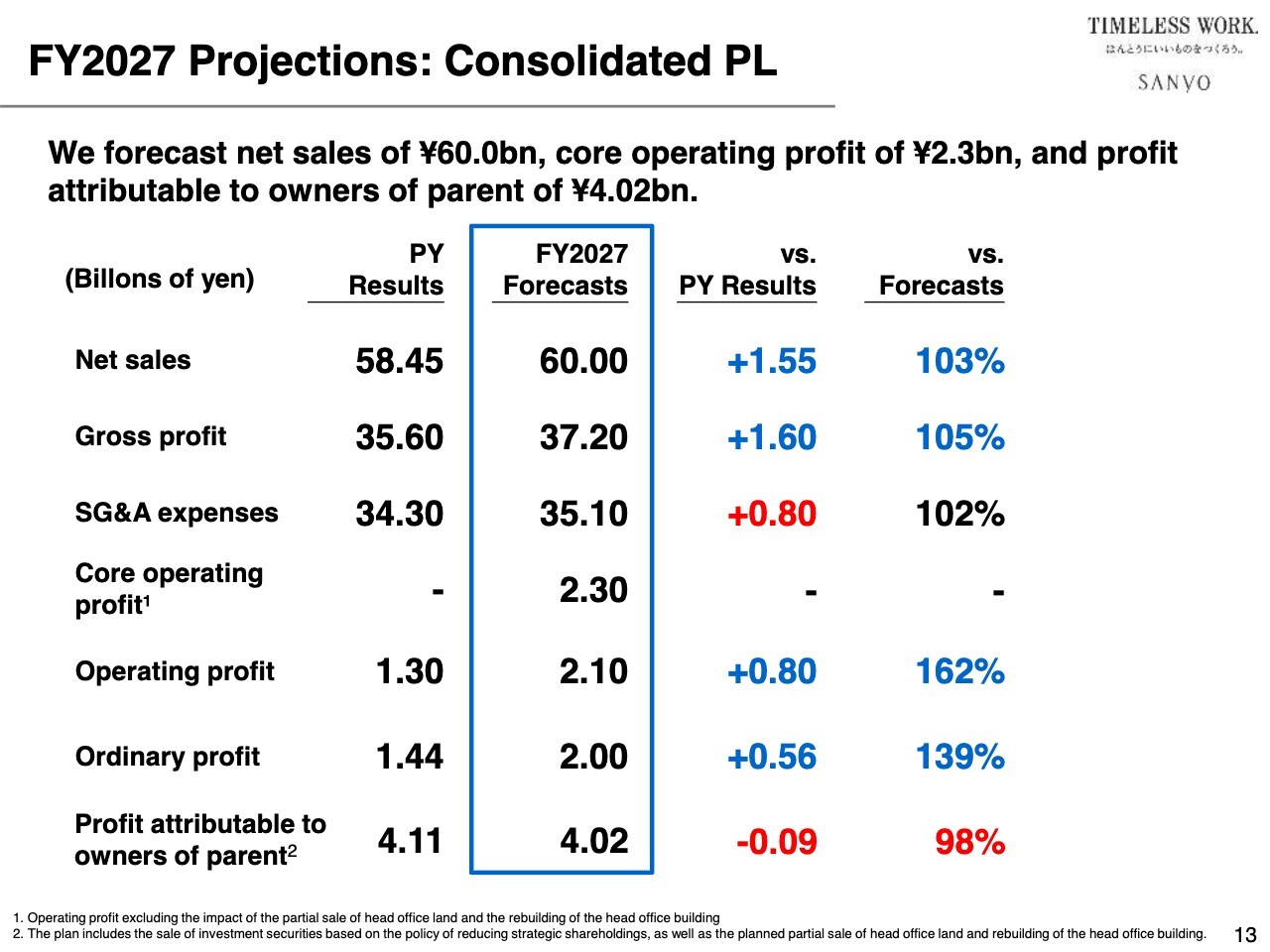

FY2027 Projections: Consolidated PL

Next, I will explain our projections for FY2027. This fiscal year corresponds to the second year of our current Medium-Term Business Plan (MTBP). As I will explain later, the quantitative plan has been revised, and the FY2027 plan, as the second year of the plan, has likewise been updated from the initial forecast.

As shown on the slide, net sales are expected to be JPY60.00 billion, up JPY1.55 billion YoY. Gross profit is expected to be JPY37.20 billion, up JPY1.60 billion YoY. SG&A expenses are expected to be JPY35.10 billion, up JPY0.80 billion YoY.

Core operating profit is expected to be JPY2.30 billion, up JPY1.00 billion compared with the previous fiscal year’s operating profit. Operating profit is expected to be JPY2.10 billion, up JPY0.80 billion YoY. Ordinary profit is expected to be JPY2.00 billion, up JPY0.56 billion YoY. Profit attributable to owners of parent is expected to be JPY4.02 billion, down JPY0.09 billion YoY. This completes our projections for FY2027.

As we will explain later, on 3 April 2026 we announced the transfer of a portion of the land of the head office building and rebuilding the head office. We expect to incur related costs starting from FY2027. The core operating profit shown on the slide excludes the impact of rebuilding the head office. In contrast, operating profit includes these effects. We present both figures separately in a two-line format.

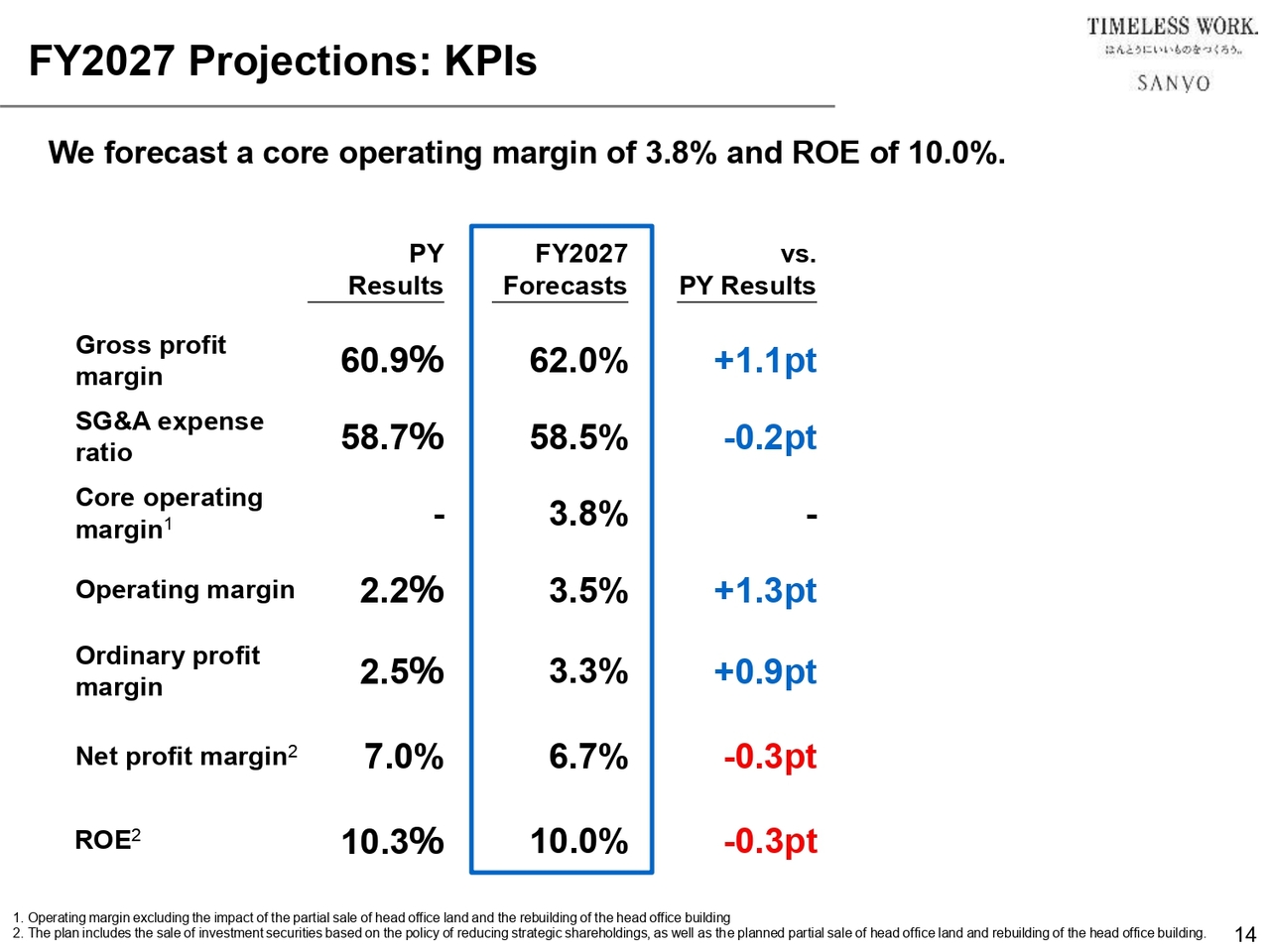

Consolidated PL: KPIs

I will explain our KPIs. Gross profit margin is expected to be 62.0%, an improvement of 1.1 percentage points YoY. SG&A expense ratio is expected to be 58.5%, down 0.2 percentage points YoY. Core operating margin is expected to be 3.8%, up an improvement of 1.6 percentage points compared with the previous fiscal year’s operating margin.

Operating margin is expected to be 3.5%, an improvement of 1.3 percentage points YoY. Ordinary profit margin is expected to be 3.3%, an improvement of 0.9 percentage points YoY. Net profit margin is expected to be 6.7%, down 0.3 percentage points YoY. ROE is expected to be 10.0%, down 0.3 percentage points YoY. This concludes our projections for FY2027.

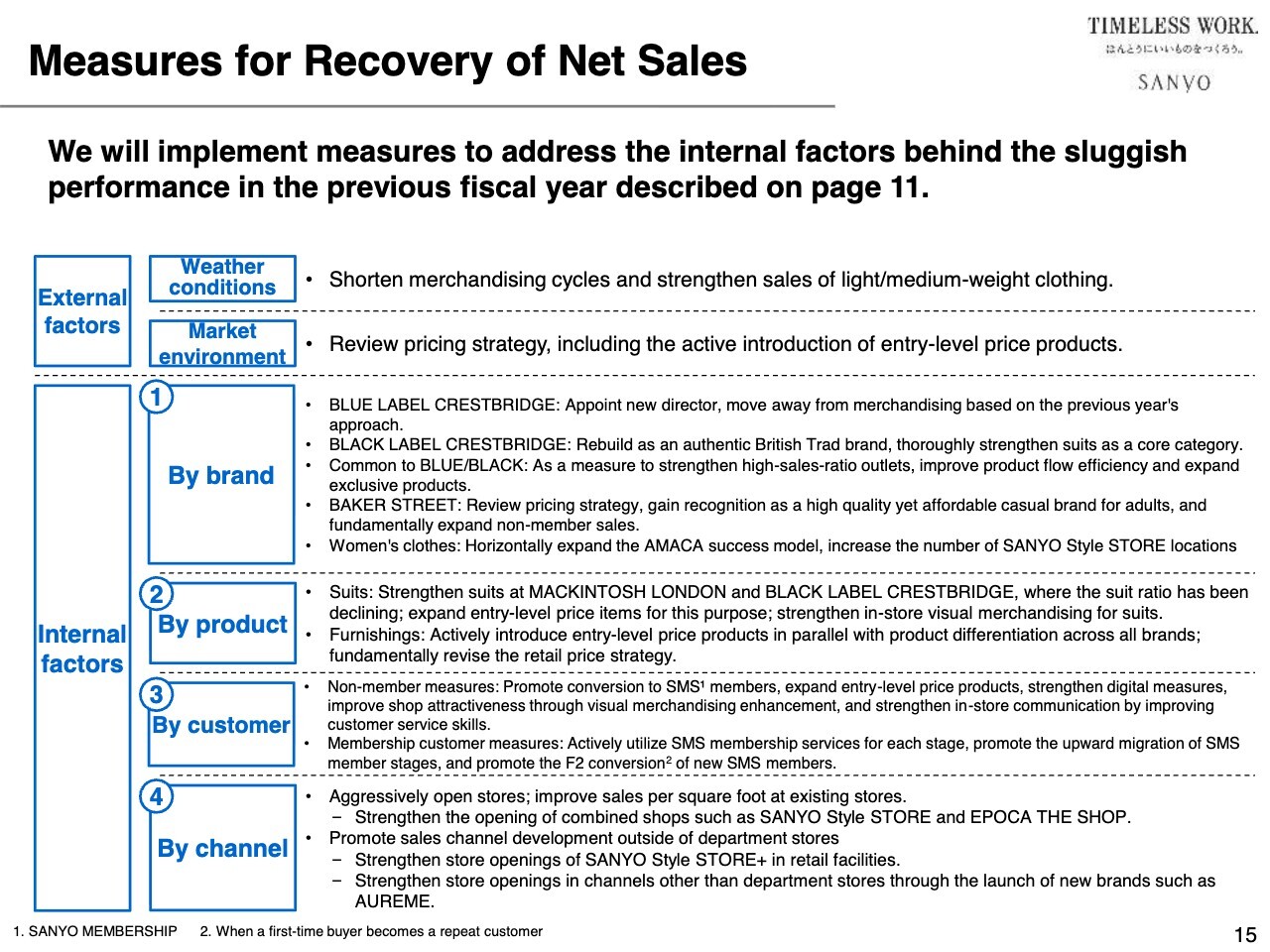

Measures for Recovery of Net Sales

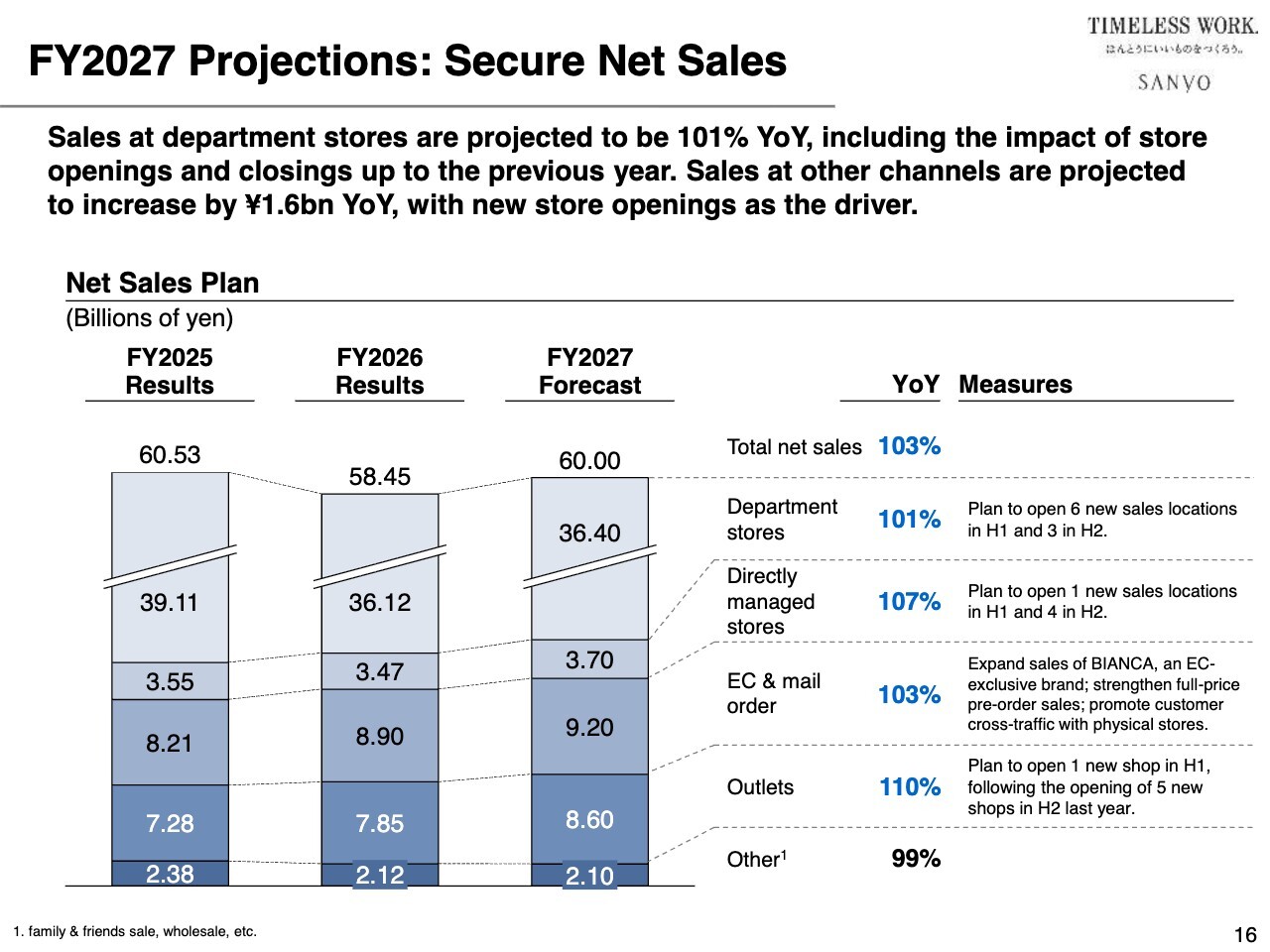

I will explain the measures for recovery of net sales. For FY2027, we plan sales at 103% YoY, an increase of JPY1.55 billion, and the slide summarizes the key measures to achieve this target.

We believe overcoming the previously explained factors behind the sluggish performance in the previous fiscal year is key to driving sales growth, and the slide outlines our specific initiatives to achieve this.

To address external factors such as weather conditions and the market environment, we will shorten our MD cycle, strengthen light and light/medium-weight clothing, and review our pricing strategy, including the proactive introduction of entry-level price products.

We also provide detailed initiatives to address internal factors that are more directly within our control.

First, on the brand dimension. To address the previously explained factors behind the sluggish performance across the three business areas, we have already appointed a new director for BLUE LABEL CRESTBRIDGE and are executing a fundamental overhaul of MD, moving away from MD based on the previous year's approach.

BLACK LABEL CRESTBRIDGE has shifted somewhat too far toward casual styles, and as a result has taken on some of the characteristics of a casual brand. By thoroughly strengthening its core categories, particularly suits and tailoring items, we aim to rebuild its image as an authentic British Trad brand.

Another shared characteristic of BLUE/BLACK LABEL CRESTBRIDGE is their relatively high outlet sales mix. Accordingly, as a measure to strengthen outlet sales, we will improve inventory product flow efficiency and expand exclusive products.

For BAKER STREET, we will fundamentally review our pricing strategy and gain recognition as a high quality yet affordable casual brand for adults. We are particularly focused on significantly expanding non-member sales.

In women's clothes, we will horizontally expand AMACA’s successful model across the other three brands. In addition, we currently operate more than a dozen SANYO Style STORE, multi-brand shops featuring four brands, and we plan to further expand the store network.

On the product dimension, we will address last year’s weakness in suits. While Paul Stuart has maintained a relatively high suit mix, we will significantly strengthen suits at MACKINTOSH LONDON and BLACK LABEL CRESTBRIDGE, where the mix has declined. To support this, we will expand entry-level price products and enhance in-store visual merchandising (VM).

For apparel, particularly light/medium-weight clothing, we will differentiate products across all brands while fundamentally revising our pricing strategy. By broadening our offering, we aim to strengthen appeal, particularly to non-member customers.

On the customer dimension, strengthening appeal to non-member customers is critical. In particular, our SANYO MEMBERSHIP (SMS) member acquisition campaigns have demonstrated that increasing new member sign-ups directly drives growth in sales from non-member customers. We will therefore further intensify these campaigns. We will also expand entry-level price products, strengthen digital initiatives, and advance other supporting measures.

Membership customer sales were strong at 104% YoY; we will further strengthen our membership customer measures to drive additional sales growth.

On the channel dimension, with closures and downsizing at railway-affiliated department stores largely complete, we plan to aggressively expand our store network. However, securing space in department stores remains challenging, so expanding non-department store channels and growing their sales will be a key priority.

As a concrete measure, we will strengthen in-store expansion of combined shop shops such as SANYO Style STORE and EPOCA THE SHOP. We will also launch a new store format, SANYO Style STORE+, in commercial facilities outside department stores.

In addition, we will actively expand store openings in non-department store channels, including the newly announced brand AUREME.

FY2027 Projections: Secure Net Sales

This shows net sales by channel.

FY2027 Projections: Improve Gross Profit Margin

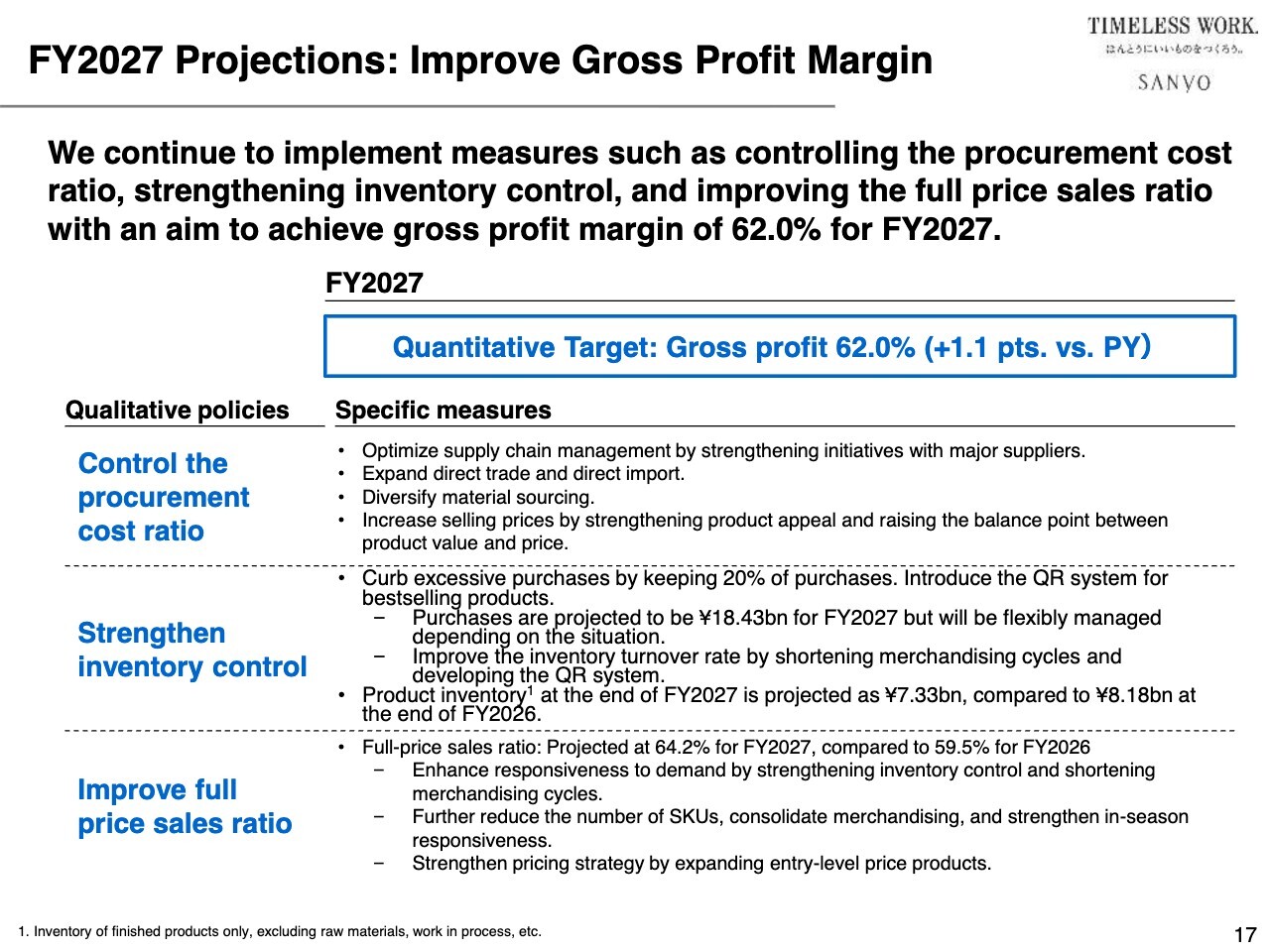

I will outline our initiatives to improve gross profit margin. We plan a gross profit margin of 62.0%, an improvement of 1.1 percentage points YoY. To achieve this, we will continue to execute our existing initiatives.

In revising our pricing strategy, controlling procurement costs will be a particularly important challenge. One of the key initiatives in this regard is to diversify material sourcing as materials represent a very significant cost factor.

In other words, we aim to broaden our options for material sourcing by seeking a wider range of proposals not only from existing suppliers but also from new ones. In addition, as one measure already partly underway, we will actively promote the development of cross-brand materials, or so-called common materials, for use across multiple brands.

Strengthening inventory control and improving the full-price sales ratio are closely linked priorities. To enhance inventory control, we will continue to utilize the 20% procurement pool, further advance quick response (QR) capabilities for best-selling products, and shorten the MD cycle to improve precision. These actions will reinforce a practical demand-driven ordering model.

In addition, we have established a dedicated task force since the previous fiscal year to focus on clearing carryover inventory, and this team will drive a thorough reduction. As a result, we aim to reduce year-end inventory from JPY8.18 billion at the end of the previous fiscal year to JPY7.33 billion by the end of FY2027.

By strengthening inventory control, we aim to lift the full-price sales ratio by 4.7 percentage points YoY to 64.2%. This level is in line with the ratio achieved two fiscal years ago. Accordingly, we aim to restore the full-price sales ratio to the level achieved two fiscal years ago, recovering from the decline in the previous fiscal year.

FY2027 Projections: Control SG&A Expenses

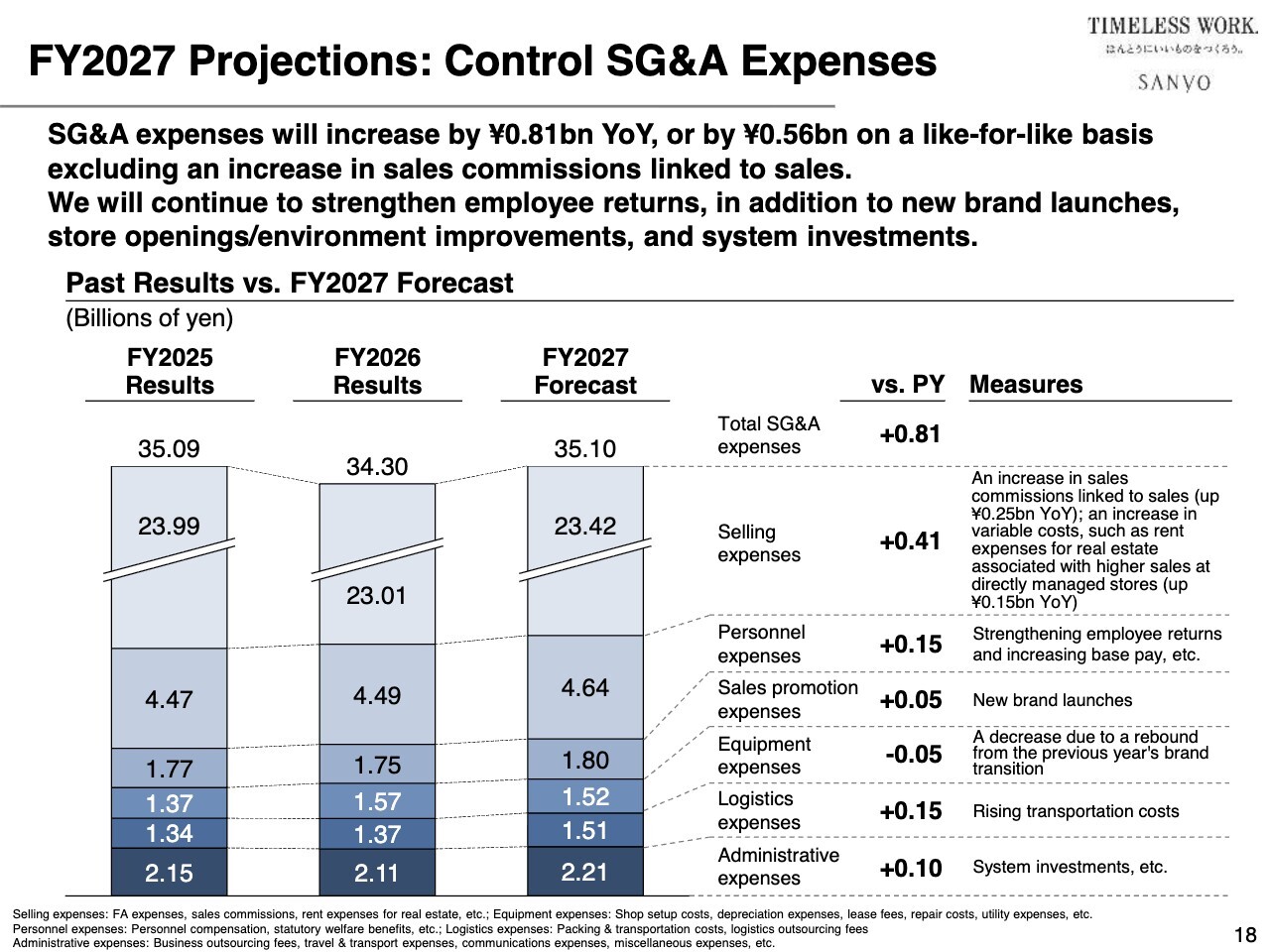

Let me explain how we will control SG&A expenses. We plan SG&A expenses of JPY35.1 billion for FY2027, up JPY0.81 billion YoY. Of this increase, JPY0.25 billion reflects higher sales commissions linked to sales, resulting in a net increase of JPY 0.56 billion in underlying SG&A expenses. The breakdown of this underlying increase is shown on the slide.

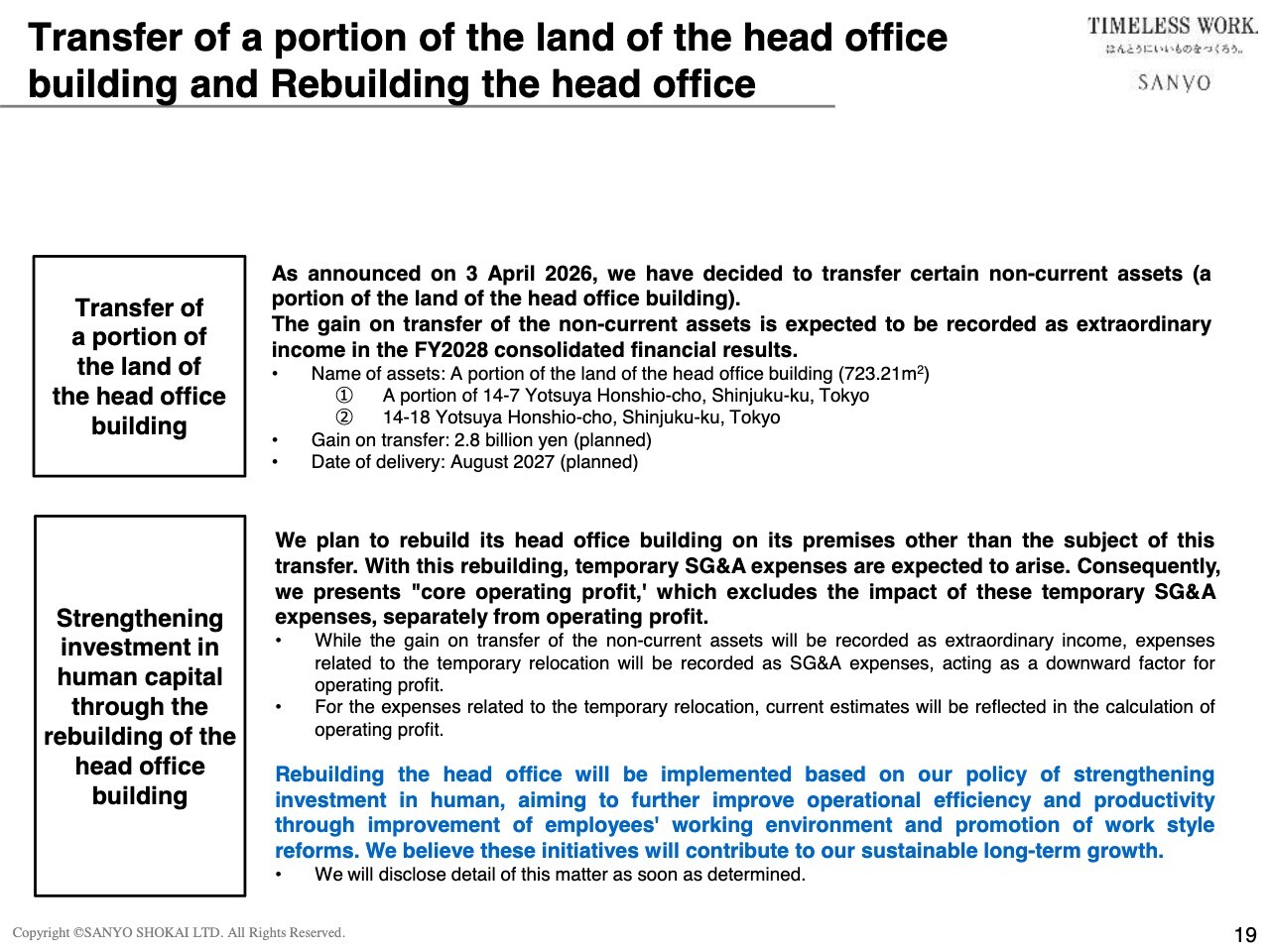

Transfer of a portion of the land of the head office building and Rebuilding the head office

Let me address the transfer of a portion of the land of the head office building and the rebuilding of the head office building. This matter was already announced this on 3 April 2026.

We decided to partially transfer a portion of the land of the head office building and rebuild the head office building because the current head office building is now 56 years old and has reached the end of its useful life. Due to the aging of the building and the year-by-year deterioration of the office environment, rebuilding has become essential.

Against this backdrop, we received an offer from a prospective buyer interested in acquiring part of the head office site. Following discussions, we decided on a plan to sell approximately 219 tsubo (723.21 sq. m.) of the head office land and construct a new head office building on the remaining approximately 480 tsubo (1,586.78 sq. m.).

We expect a gain on transfer of JPY2.8 billion, which we will use to partially offset rebuilding costs. Specifically, this will cover demolition costs, relocation to a temporary office, and rent for the temporary office.

Although part of the gain on transfer can be offset against the rebuilding costs, the accounting treatment differs between the two. The gain on transfer will be recorded in full as extraordinary income when the transfer is executed, whereas the rebuilding costs will be recorded as SG&A expenses, which will have a negative impact on operating profit. For this reason, we have explained profit at two levels: “core operating profit,” which excludes this factor, and operating profit, which includes it.

In any case, we believe that rebuilding the head office building will lead to an improved working environment, further operational efficiency, higher productivity, and greater employee motivation. We therefore concluded that this initiative is also fully aligned with our human capital strategy.

Progress of MTBP

Next, I will update you on the progress of our MTBP.

Mission, Vision, Values

We announced this MTBP last April, and there have been no material changes to its core policies or content. Our Mission, Vision, and Values also remain unchanged.

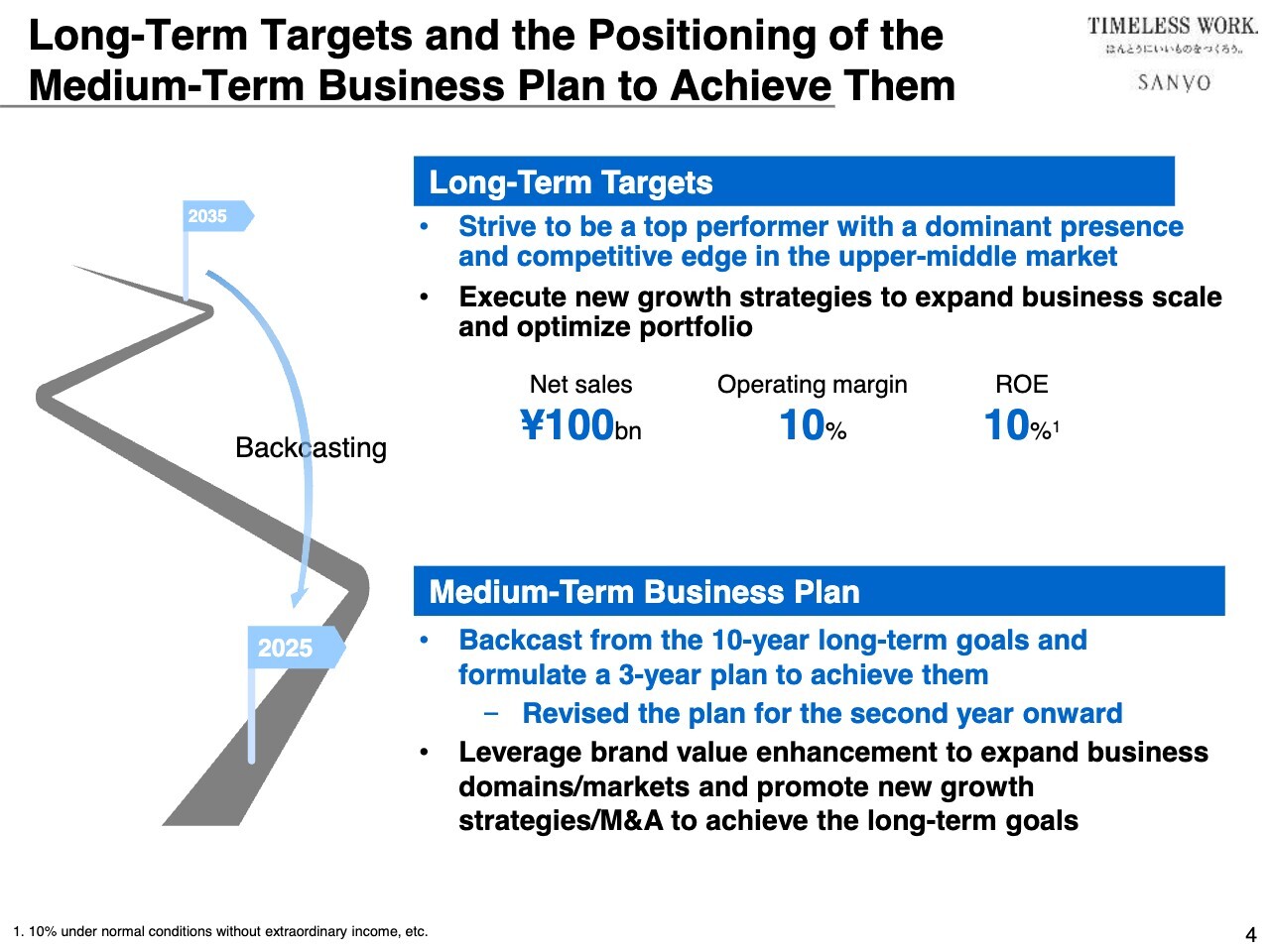

Long Term Targets and the Positioning of the MTBP to Achieve Them

Let me explain long-term targets and the positioning of the MTBP to achieve them. As shown on the slide, we continue to take a backcasting approach from our 10-year goals and formulate a three-year plan to drive their achievement, with no change to this overall framework.

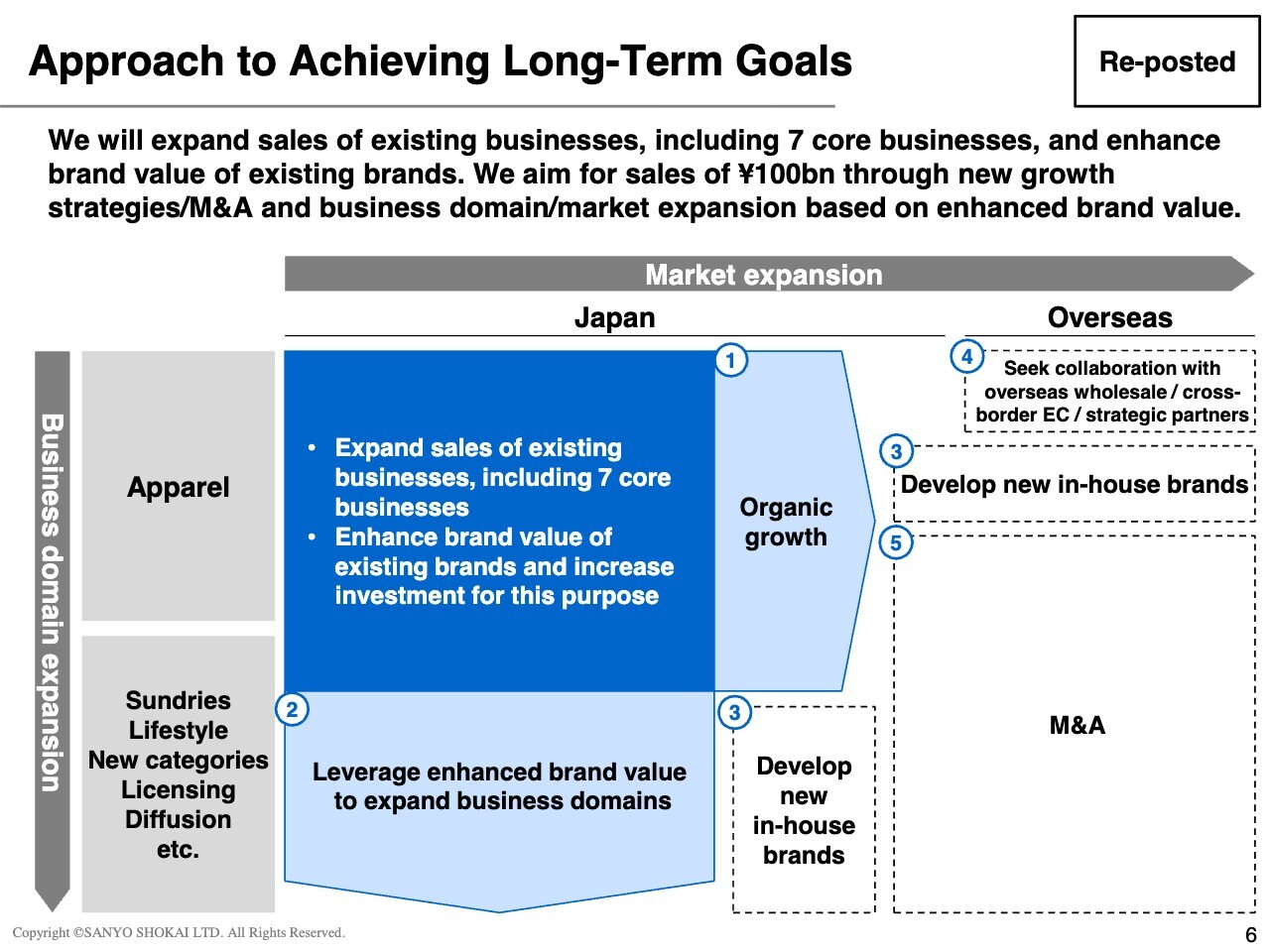

Approach to Achieving Long Term Goals

To achieve our long-term targets, we position organic growth as the core strategy to expand our existing businesses.

In addition, we will expand the scope of our existing businesses, develop new in-house brands, expand overseas, and execute M&A, all in line with the initial forecast.

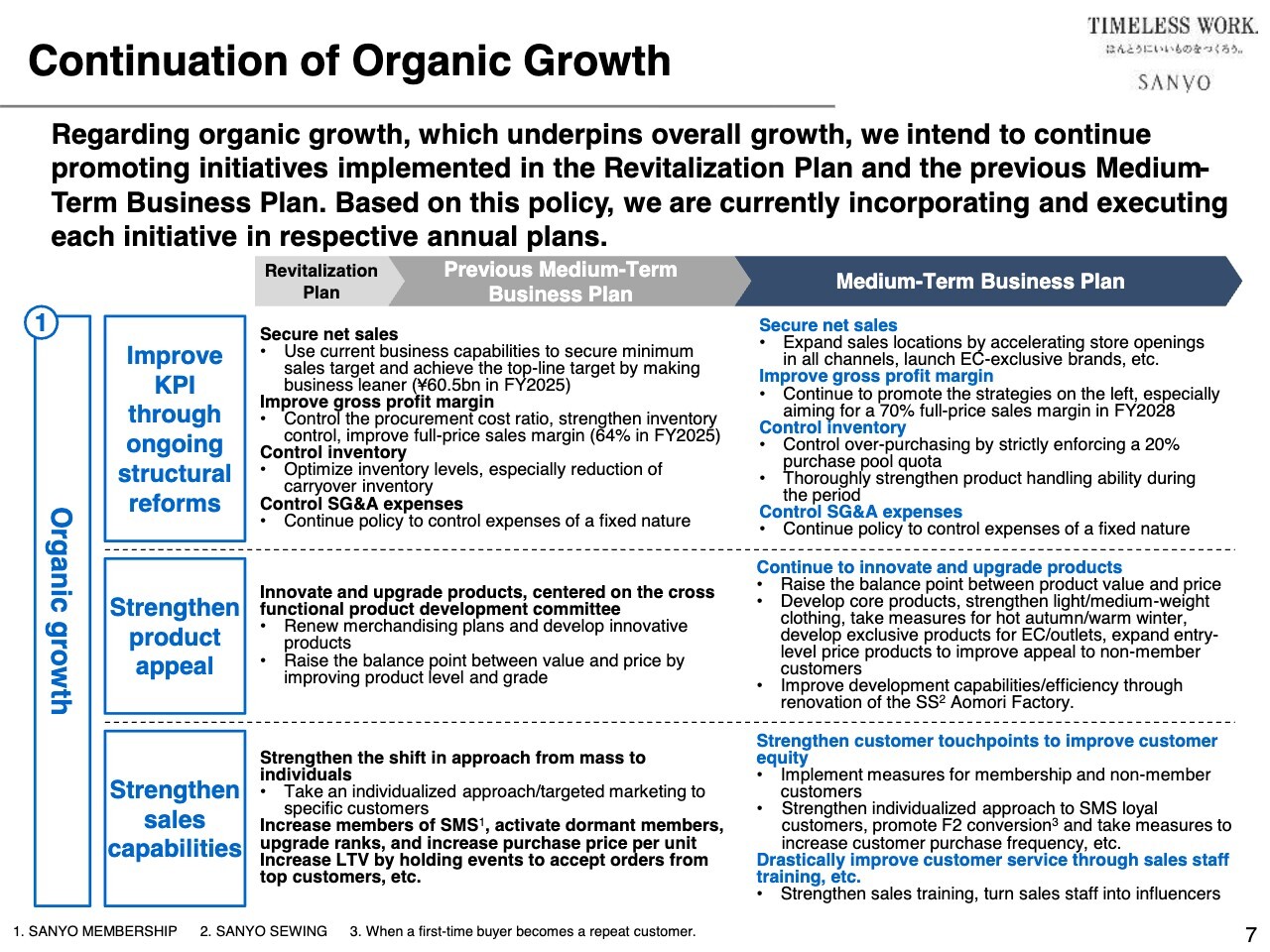

Continuation of Organic Growth

These are the initiatives to drive our core strategy of organic growth. As shown on the slide, we will improve KPIs through ongoing structural reforms, strengthen product appeal, and enhance sales capabilities, with no changes from the initial forecast.

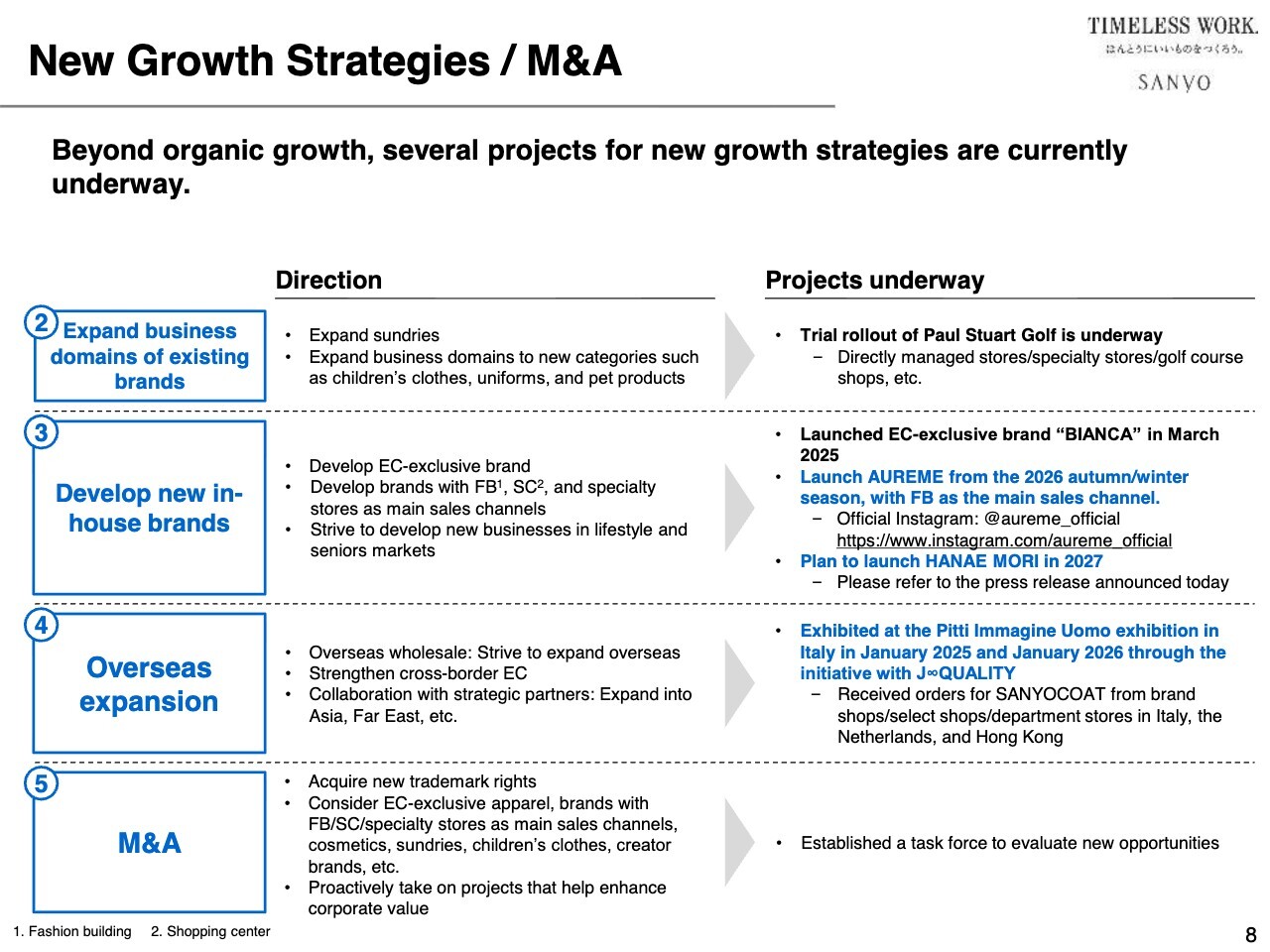

New Growth Strategies/M&A

As for growth strategies beyond organic growth, there were several developments in the previous fiscal year. The projects currently underway are shown on the right-hand side of the slide.

As part of expanding business domains of existing brands, we have already begun rolling out Paul Stuart Golf.

For new in-house brand development, we launched the EC exclusive brand BIANCA in the previous fiscal year. We will also begin rolling out the already announced AUREME from this autumn/winter season, with fashion buildings (FB) as the primary sales channel. In addition, we plan to launch HANAE MORI and issued a press release today.

In overseas expansion, as part of the J∞QUALITY FACTORY BRAND PROJECT led by the Japan Apparel and Fashion Industry Council, we exhibited at Pitti Immagine Uomo in Italy last year, showcasing SANYOCOAT and secured orders worth several million yen. At our second exhibition this year, orders increased significantly. We have already secured orders worth tens of millions of yen from multiple companies, and we are seeing very strong momentum.

Going forward, we will actively showcase our made-in-Japan Sanyo Summit Series products—such as Aomori Down and Fukushima Jacket—to drive further order growth.

For M&A, we have already established a dedicated task force and are actively advancing our review process. We have progressed from a long list to a middle list, and are now narrowing down to a short list.

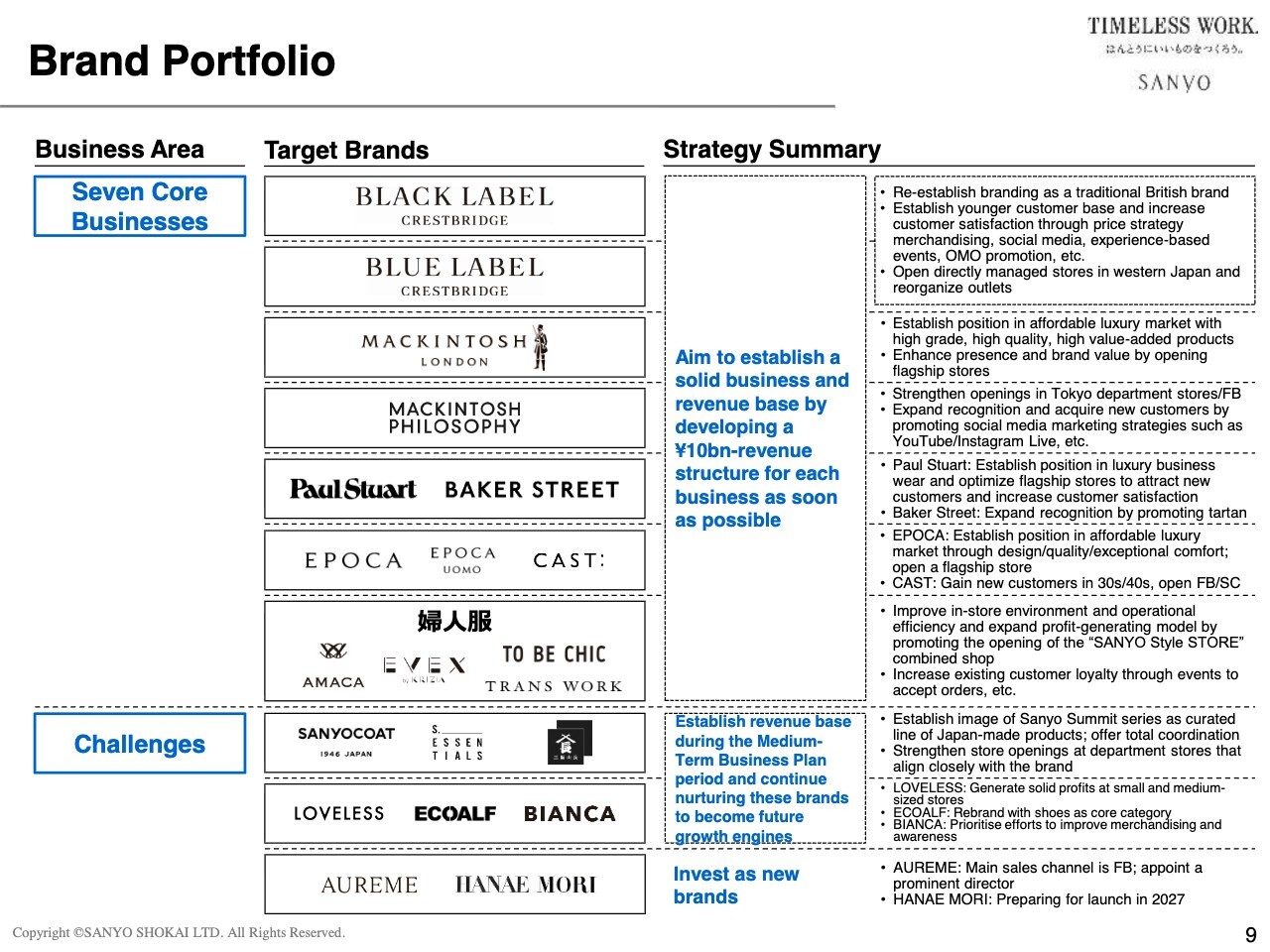

Brand Portfolio

There are no changes to our brand portfolio from the initial forecast.

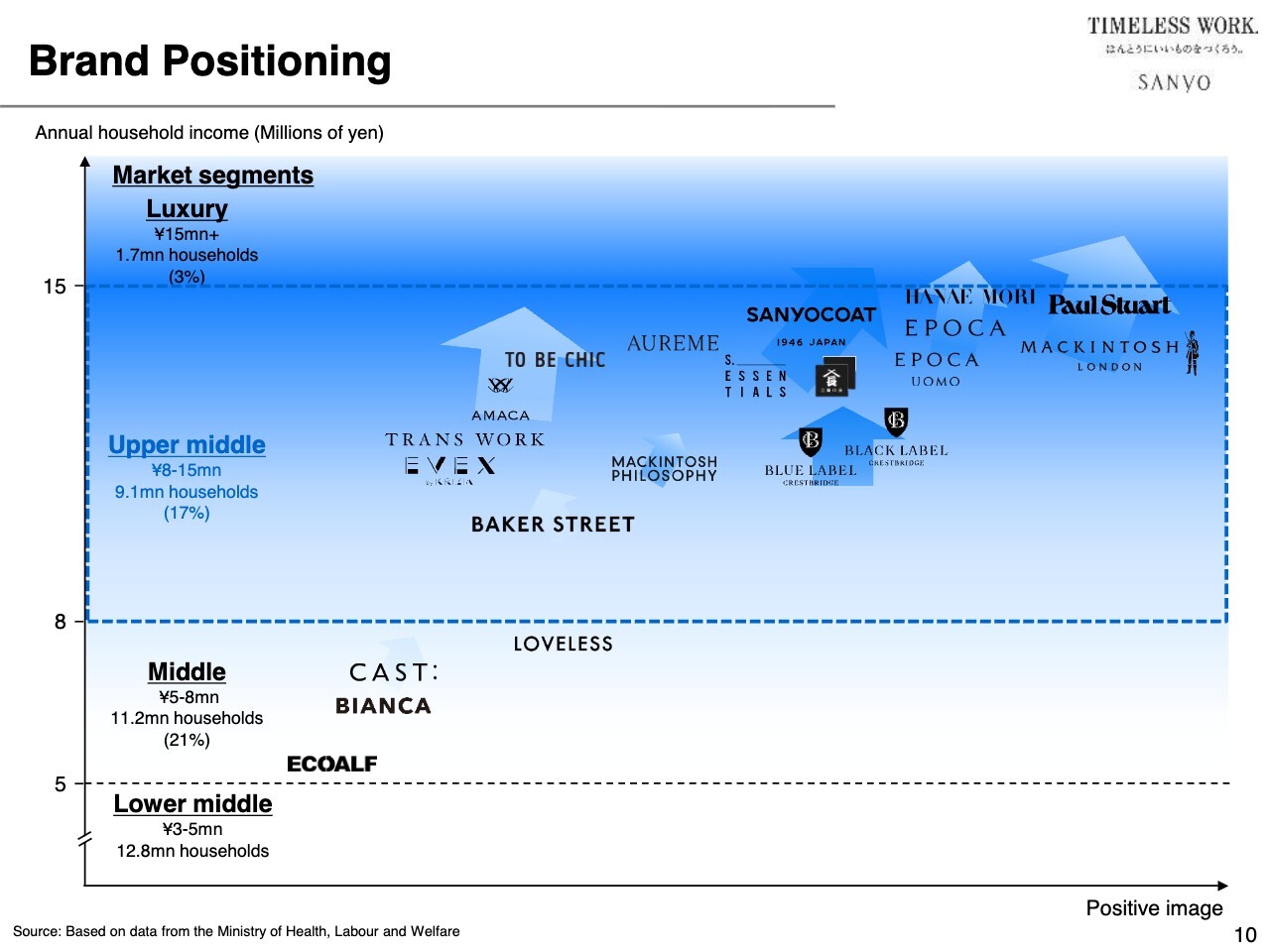

Brand Positioning

There are no changes to our brand positioning from the initial forecast.

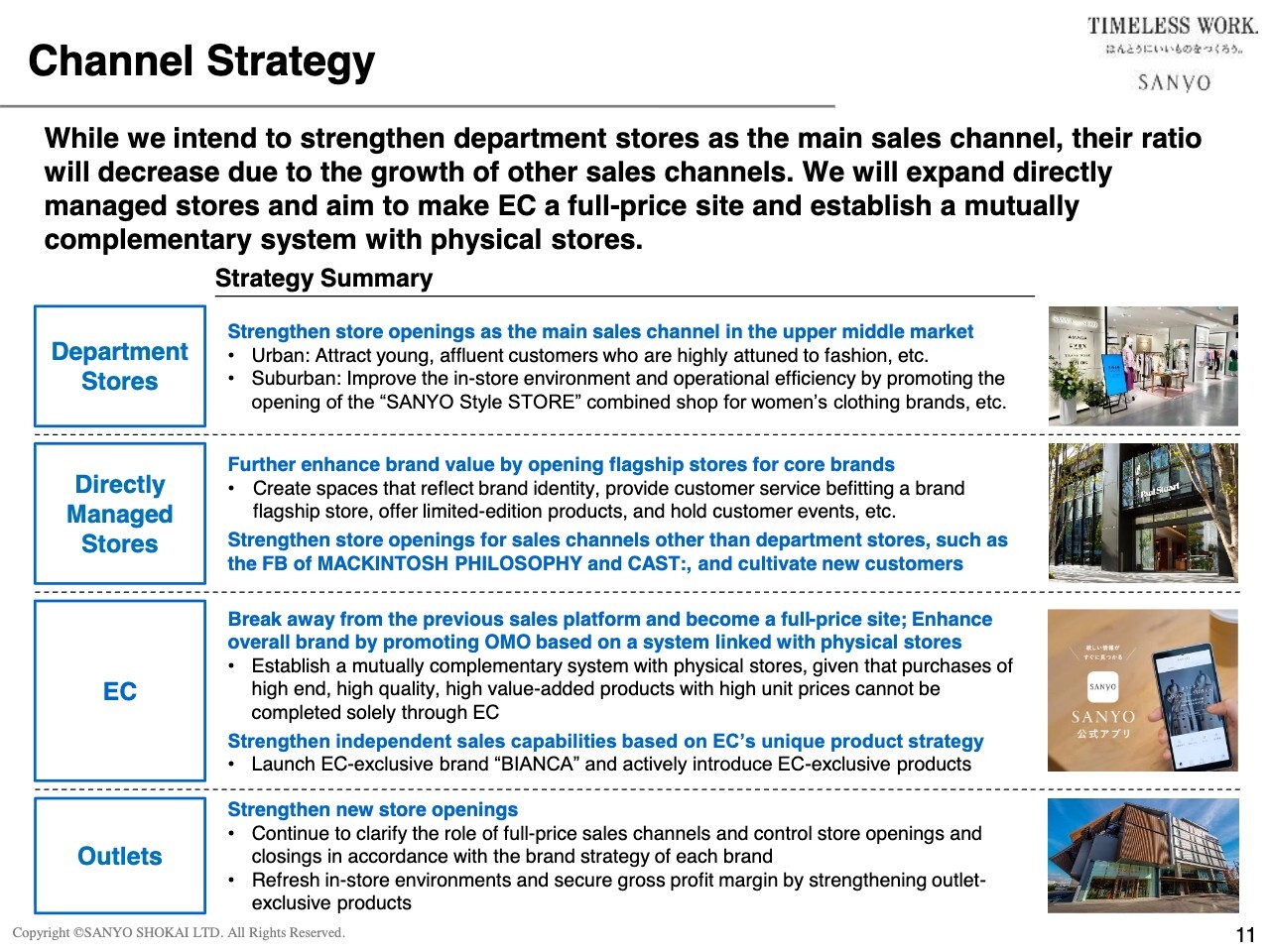

Channel Strategy

There are no changes to our channel strategy from the original plan.

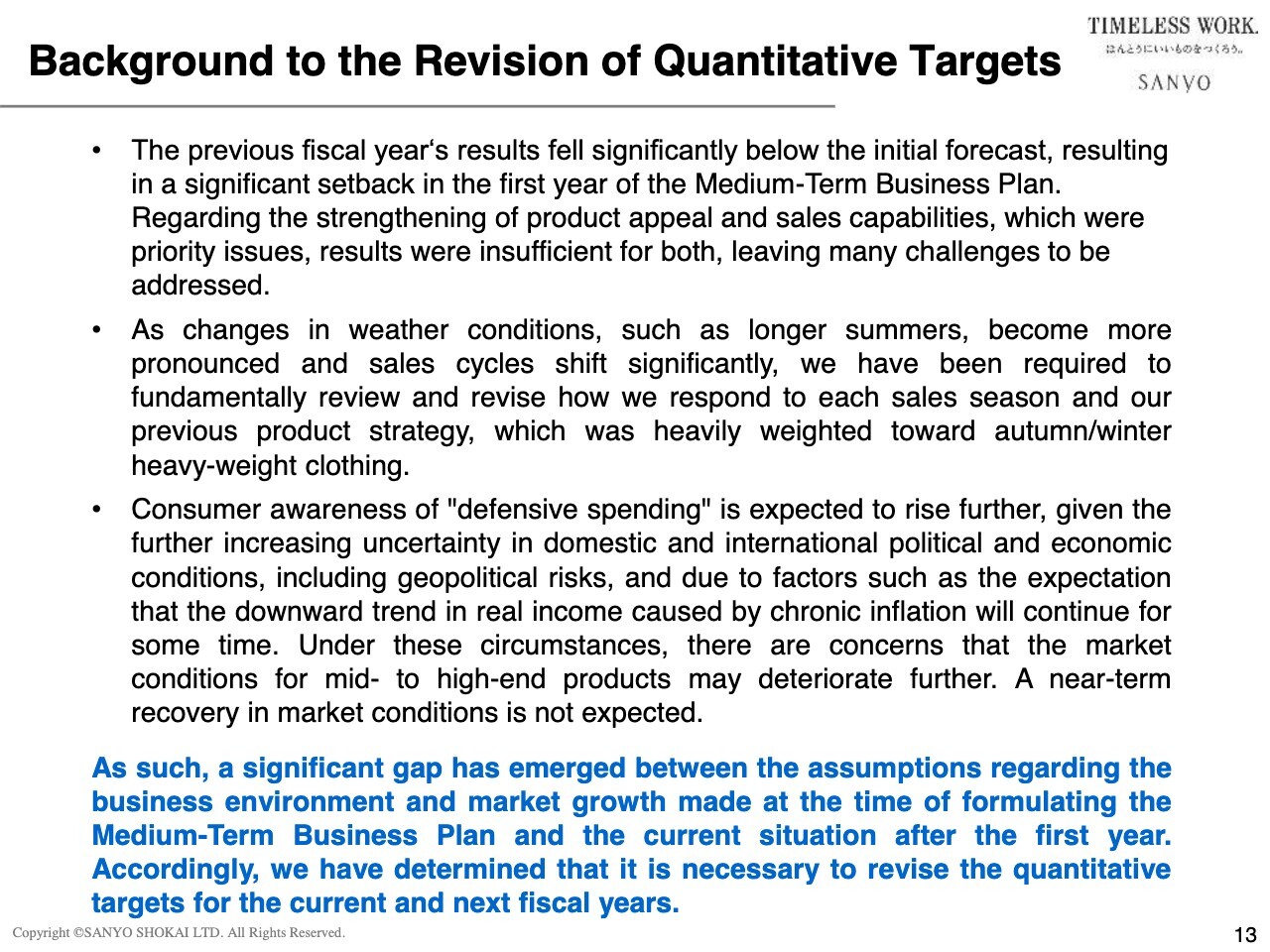

Background to the Revision of Quantitative Targets

We have revised our quantitative targets to reflect the results of the previous fiscal year and current conditions. This slide outlines the background to these revisions.

First, our results in the previous fiscal year fell significantly short of the initial forecast, resulting in a significant setback in the first year of the MTBP. In addition, we did not deliver sufficient progress in strengthening product appeal and sales capabilities—both priority issues—leaving many challenges unresolved and highlighting that our core competitiveness remains insufficient.

Furthermore, changes in weather conditions, such as longer summers, become more pronounced. As selling cycles shift significantly, we have been required to fundamentally review and revise how we respond to each selling period and our previous product strategy, which was heavily weighted toward autumn/winter heavy weight clothing.

In addition, consumers’ defensive mindset is expected to rise further, given the further increasing uncertainty in domestic and international political and economic conditions, including geopolitical risks, and due to factors such as the expectation that the downward trend in real income caused by chronic inflation will continue for some time.

Under these circumstances, there are concerns that the conditions for mid to high-end market may deteriorate further. A near term recovery in market conditions is not expected.

As such, a significant gap has emerged between the assumptions regarding the business environment and market growth made at the time of formulating the MTBP and the current situation after the first year. Accordingly, we have determined that it is necessary to revise the quantitative targets for the current and next fiscal years.

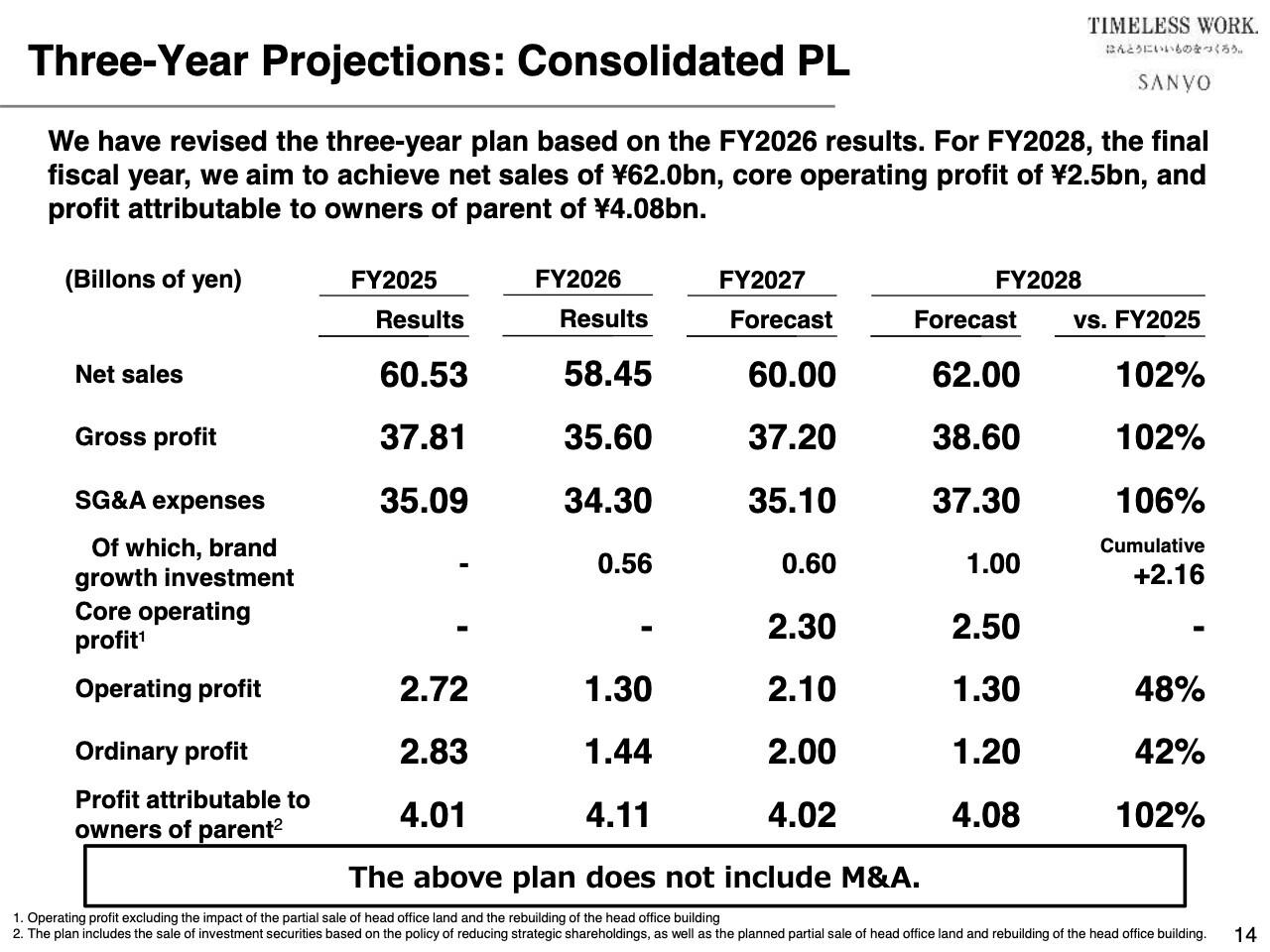

Three-Year Projections: Consolidated PL

Here’s three-year consolidated PL. FY2027 projections are as I explained earlier.

Let me walk you through the revised forecast of FY2028, the final fiscal year. We aim to achieve net sales of JPY62.00 billion, gross profit of JPY38.60 billion, SG&A expenses of JPY37.30 billion, core operating profit of JPY2.50 billion, operating profit of JPY1.30 billion, ordinary profit of JPY1.20 billion, and profit attributable to owners of parent of JPY4.08 billion. This is the quantitative plan for the final year.

There is a difference of JPY1.20 billion between core operating profit and operating profit; this is because rebuilding costs, including demolition costs associated with the rebuilding of the head office building as well as relocation costs and rent for the temporary office will be incurred primarily during this period.

In addition, the approximately JPY2.8 billion difference between ordinary profit and profit attributable to owners of parent is due to a gain on sale of the land of the head office building. This is because we plan to sell the property during this fiscal year, which will result in a gain on sale. We also expect to record a gain on sale of investment securities as extraordinary income.

As noted at the bottom of the slide, the sales plan of JPY62.00 billion does not include any contribution from M&A or similar initiatives. In other words, if an M&A transaction is realized, there is potential for the plan to be exceeded.

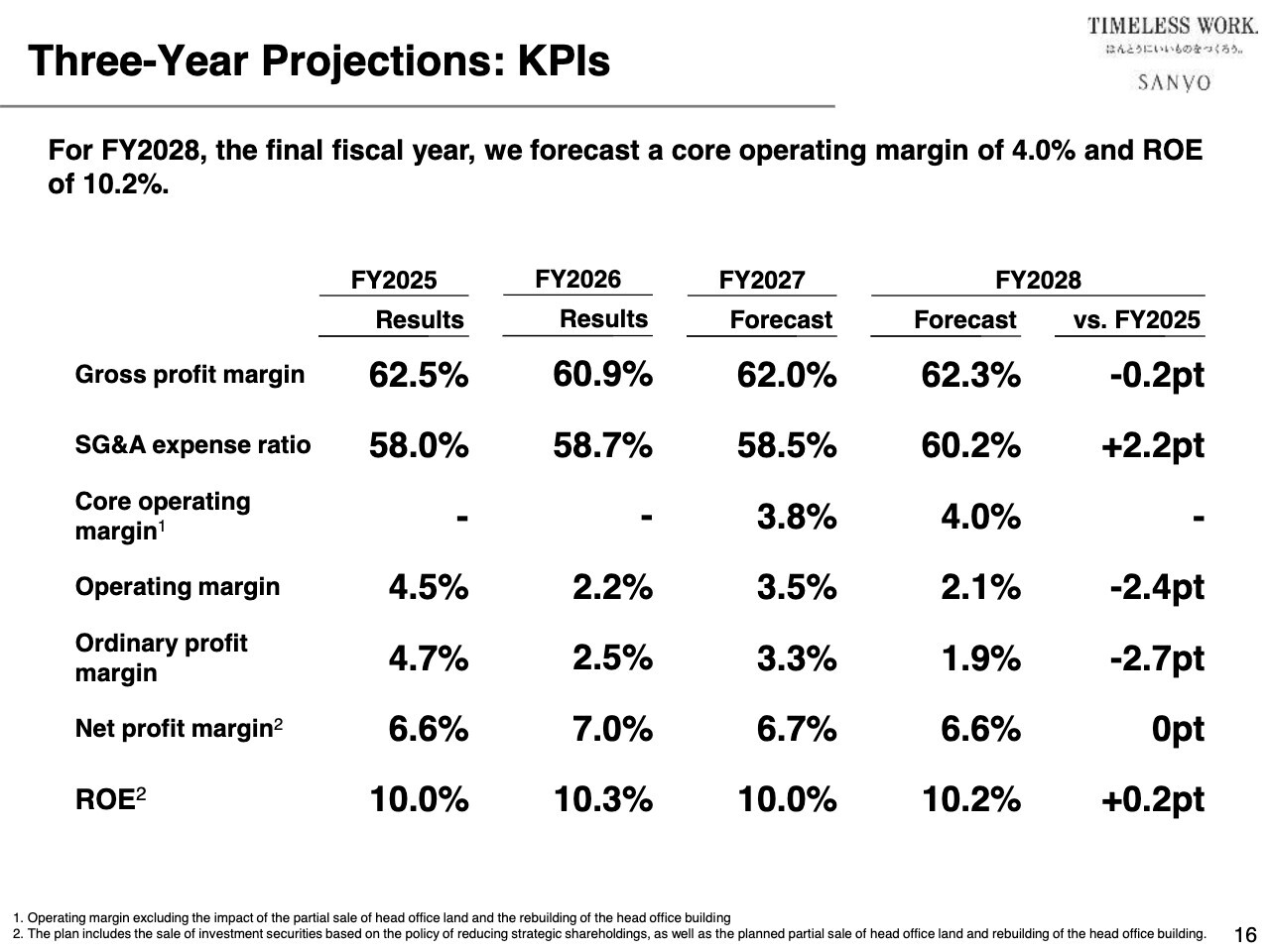

Three-Year Projections: KPIs

These are the KPIs for the three-year projections. FY2027 forecast is as I explained earlier. I will now explain the forecast of FY2028, the final fiscal year.

We forecast a gross profit margin of 62.3%, an SG&A expense ratio of 60.2%, a core operating margin of 4.0%, an operating margin of 2.1%, an ordinary profit margin of 1.9%, a net profit margin of 6.6%, and ROE of 10.2%.

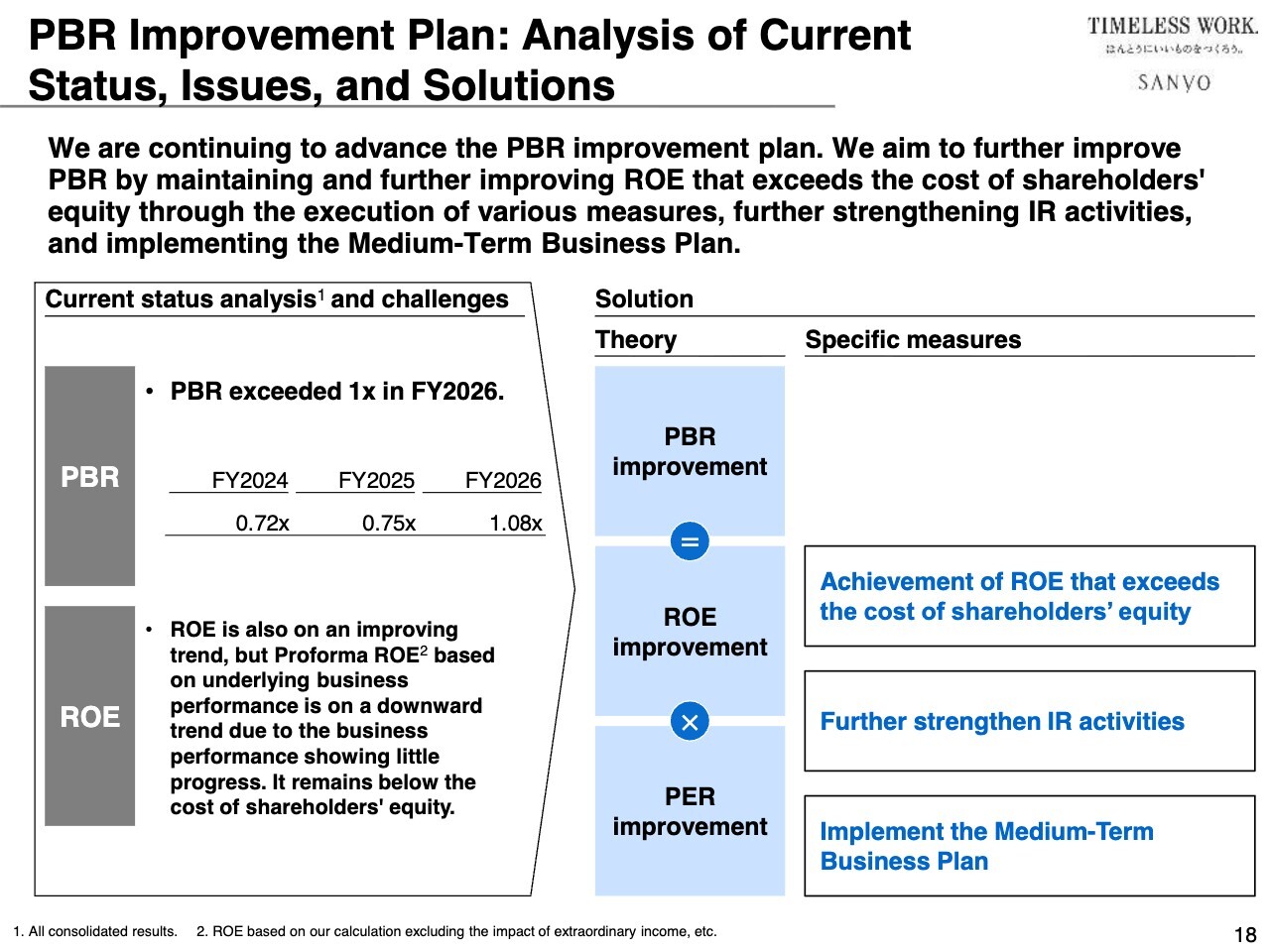

PBR Improvement Plan: Analysis of Current Status, Issues, and Solutions

There are no significant changes to the capital strategy from the initial plan. As the core strategy, we will improve ROE. ROE improvement will enhance PER and PBR.

PBR was 0.72x two years ago, but has most recently risen above 1.0x. We believe this reflects the effects of our various capital policies.

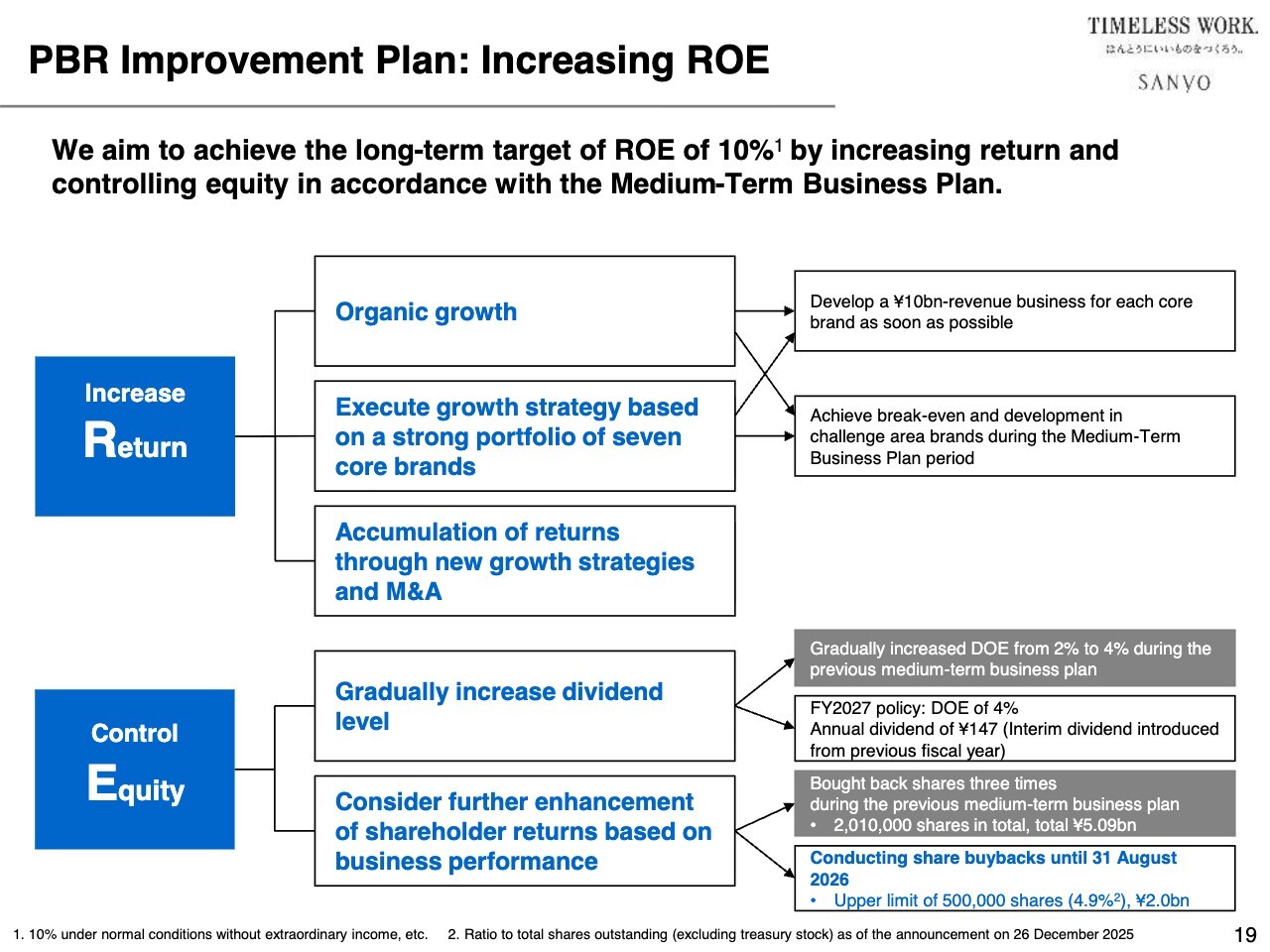

PBR Improvement Plan: Increasing ROE

There are no changes to the measures to improve ROE from the initial plan. To increase the numerator, Return, and control the denominator, Equity, we will proactively implement investment for growth, employee returns, and shareholder returns.

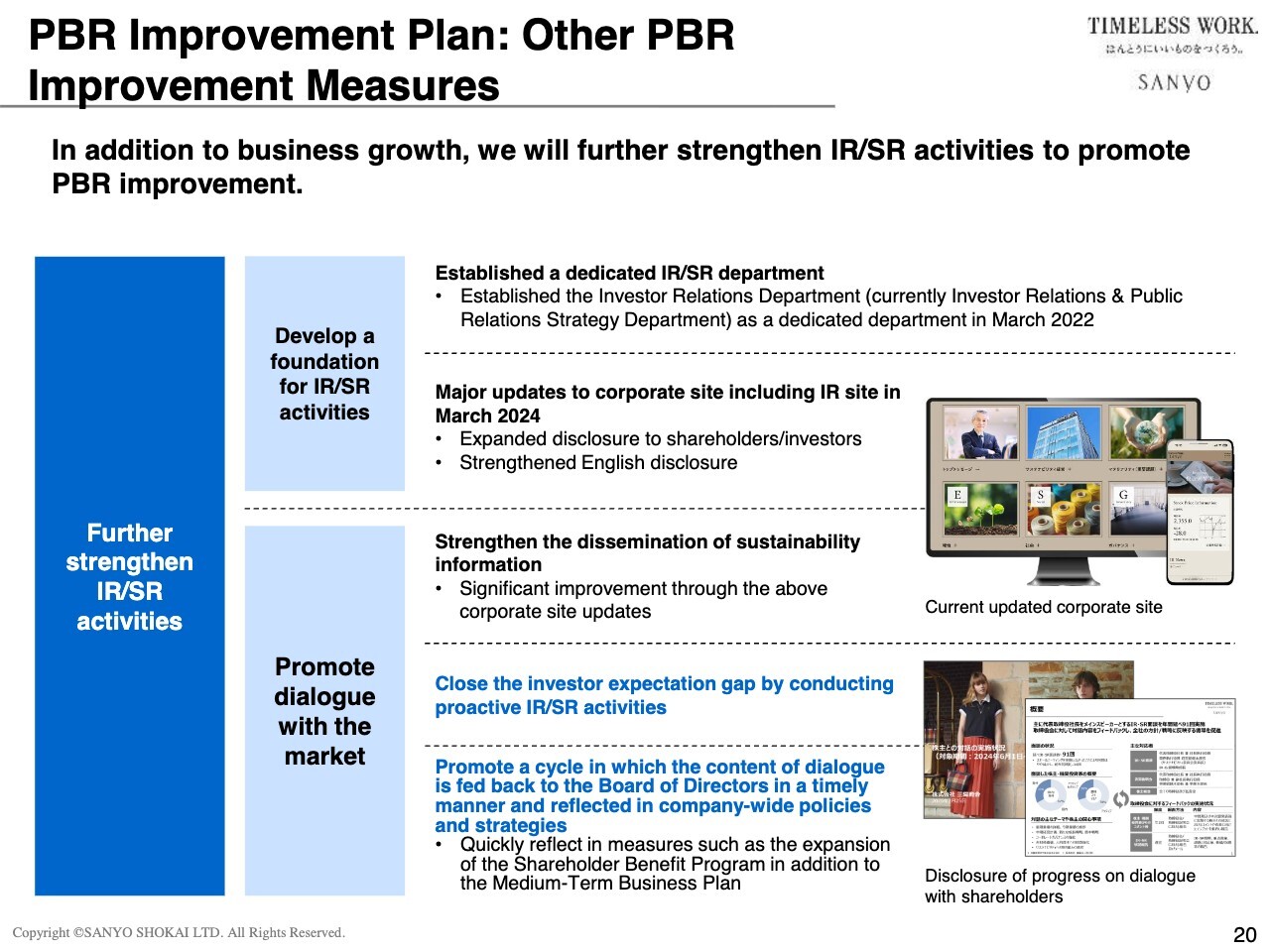

PBR Improvement Plan: Other PBR Improvement Measures

In addition to business growth, we will further strengthen IR/SR activities to promote PBR improvement. We are also proceeding with these initiatives in line with the initial plan.

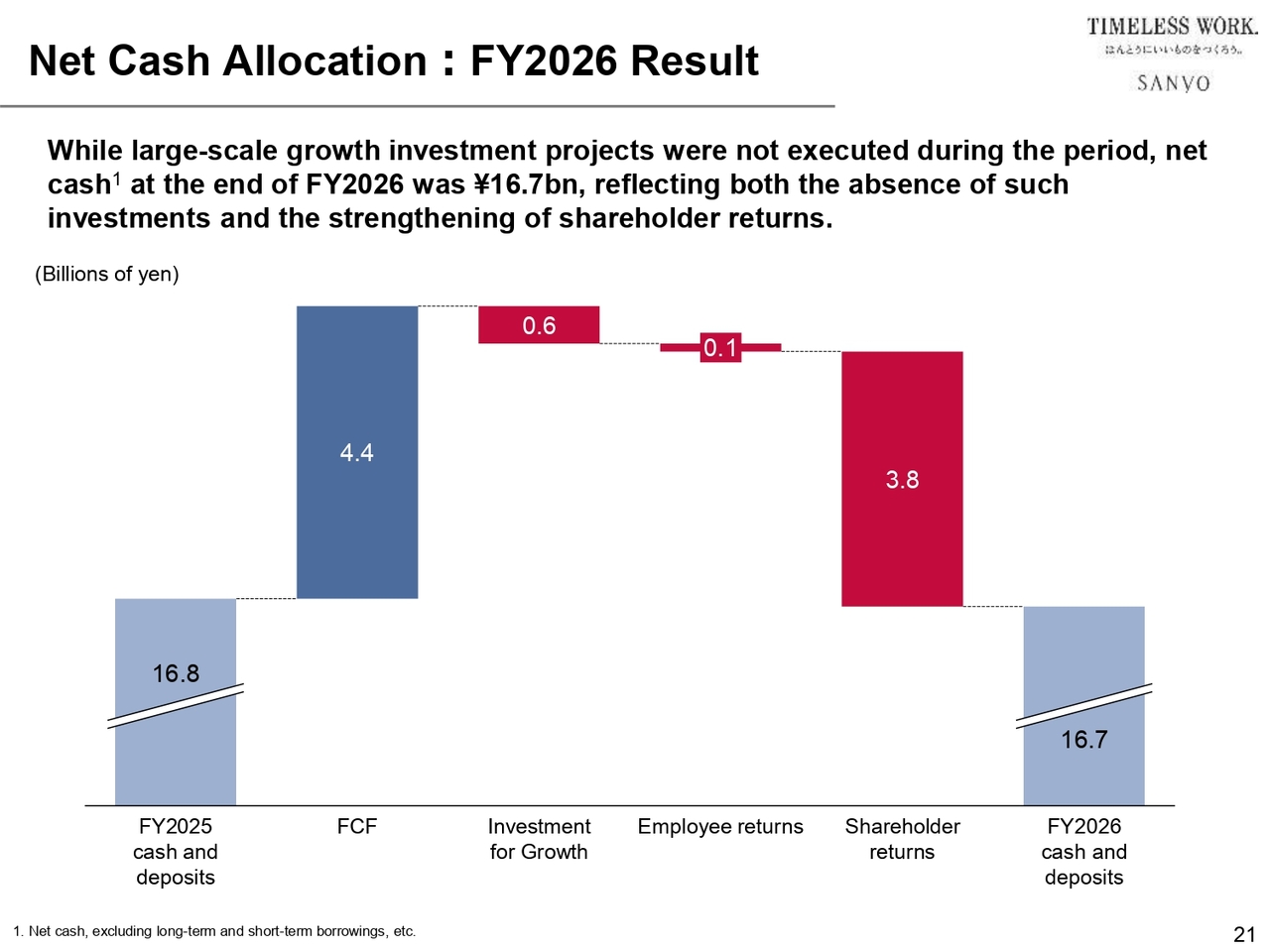

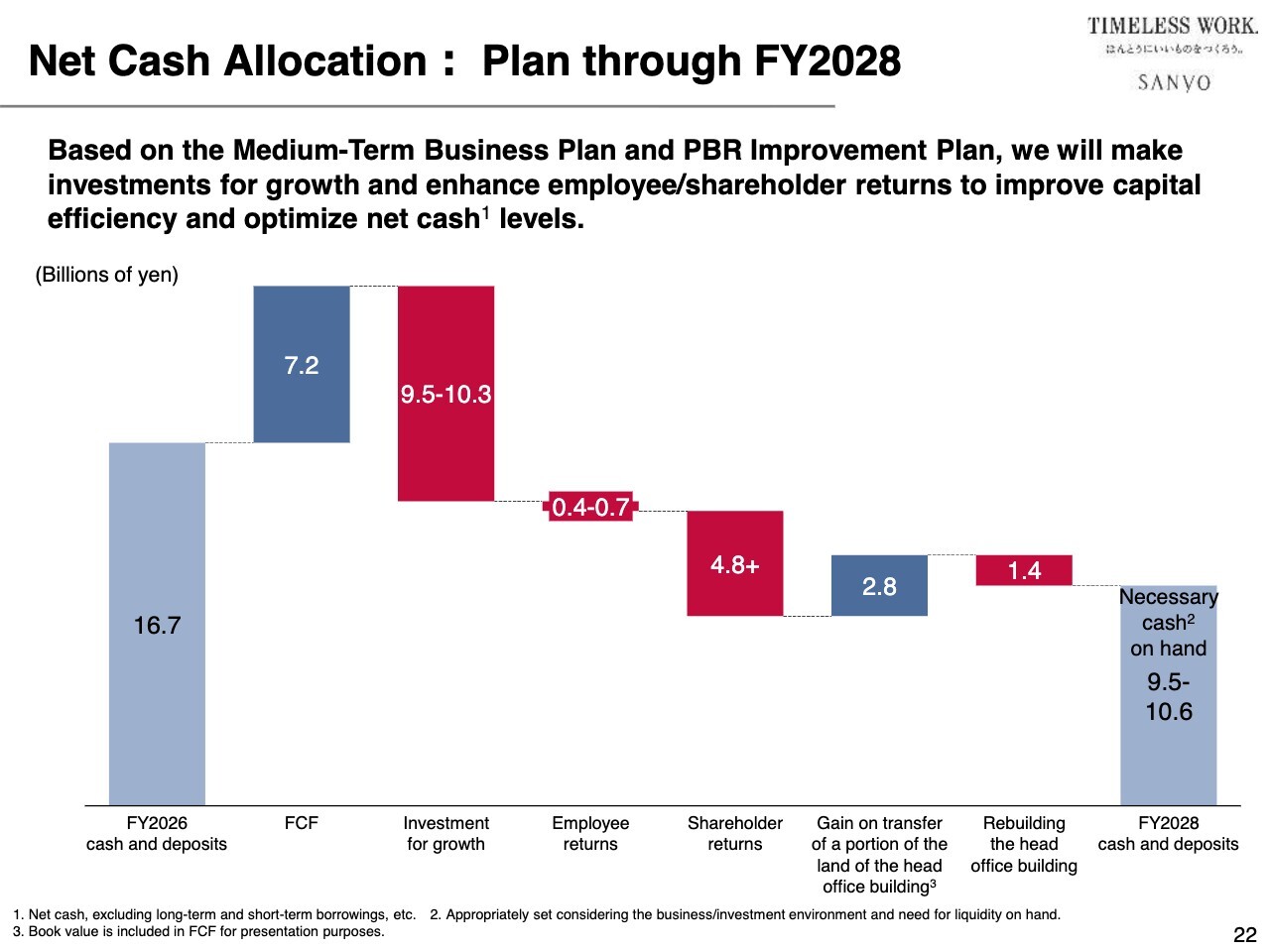

Net Cash Allocation: FY2026 Result

Slides 21 and 22 outline our net cash allocation. First, let me explain the results for FY2026. Net cash at the beginning of FY2026 was JPY16.8 billion, and cash inflows during the period totaled JPY4.4 billion.

Against this, we used JPY0.6 billion for investment for growth, JPY0.1 billion for employee returns, and JPY3.8 billion for shareholder returns. As a result, net cash at the end of FY2026 stood at JPY16.7 billion, a decrease of JPY0.1 billion. Shareholder returns include not only dividends but also the two share buybacks executed during FY2026.

Net Cash Allocation: Plan through FY2028

Slide 22 shows the net cash allocation for FY2027 and FY2028.

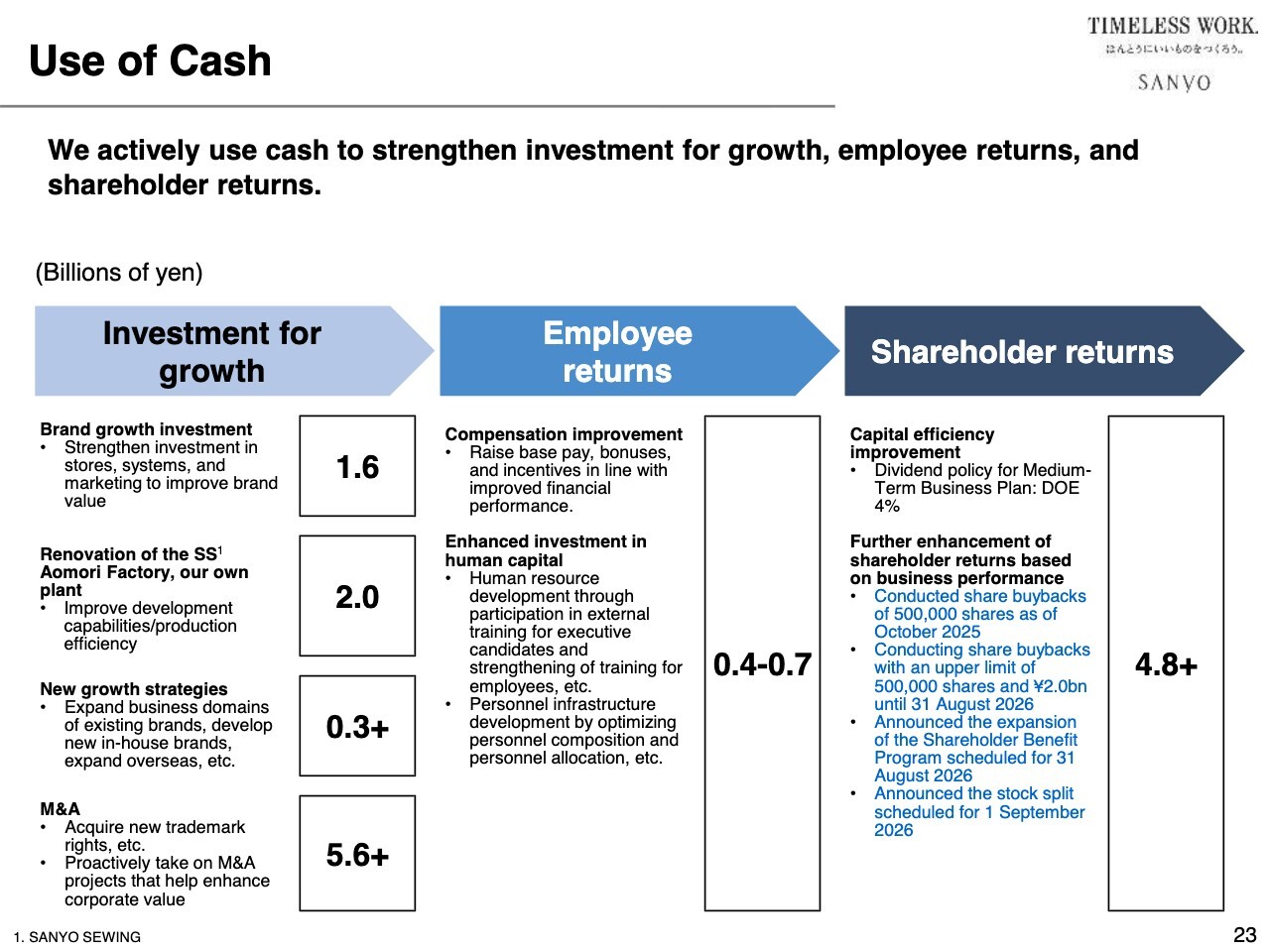

Use of Cash

Although this is only a rough estimate, the slide provides a breakdown of use of cash by investment for growth, employee returns, and shareholder returns.

In particular, regarding investment for growth, we have decided to rebuild SANYO SEWING Aomori Factory, and it has already decided that approximately JPY2.0 billion will be invested for this purpose. In addition, initiatives such as the launch of new brands and overseas expansion are already underway.

In addition, with regard to M&A, we have already moved to the shortlist stage and are envisaging an investment of slightly over JPY5.0 billion.

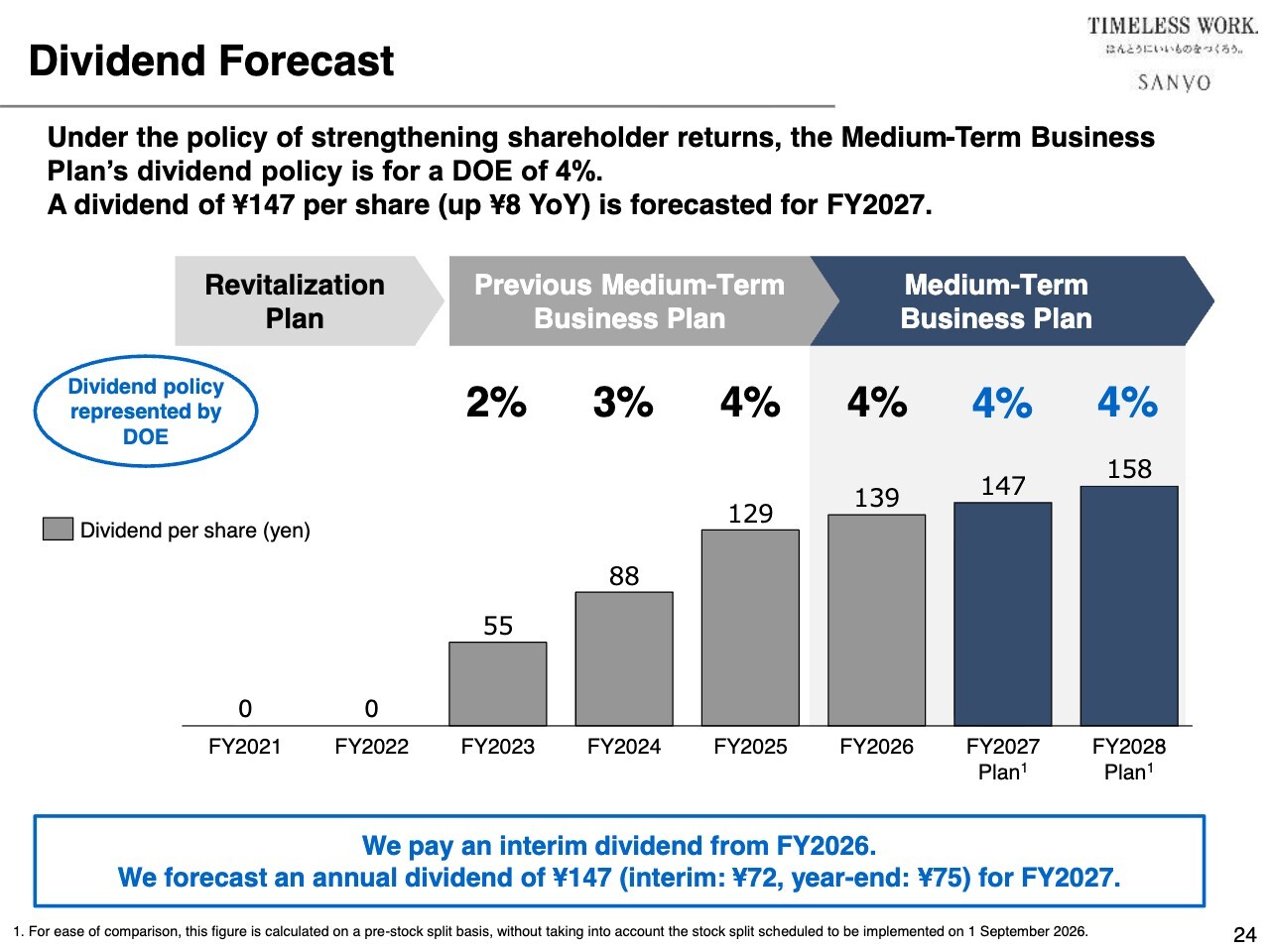

Dividend Forecast

This is about the dividend policy. We plan to maintain a DOE of 4% during the MTBP period. In FY2026, we paid an interim dividend of JPY69, a year-end dividend of JPY70, and an annual dividend of JPY139.

For FY2027, as mentioned earlier, we plan to maintain a DOE of 4% and forecast an interim dividend of JPY72, a year-end dividend of JPY75, and an annual dividend of JPY147.

However, as we plan to implement a three-for-one stock split on 1 September 2026, the year-end dividend per share is expected to be JPY25 after the split.

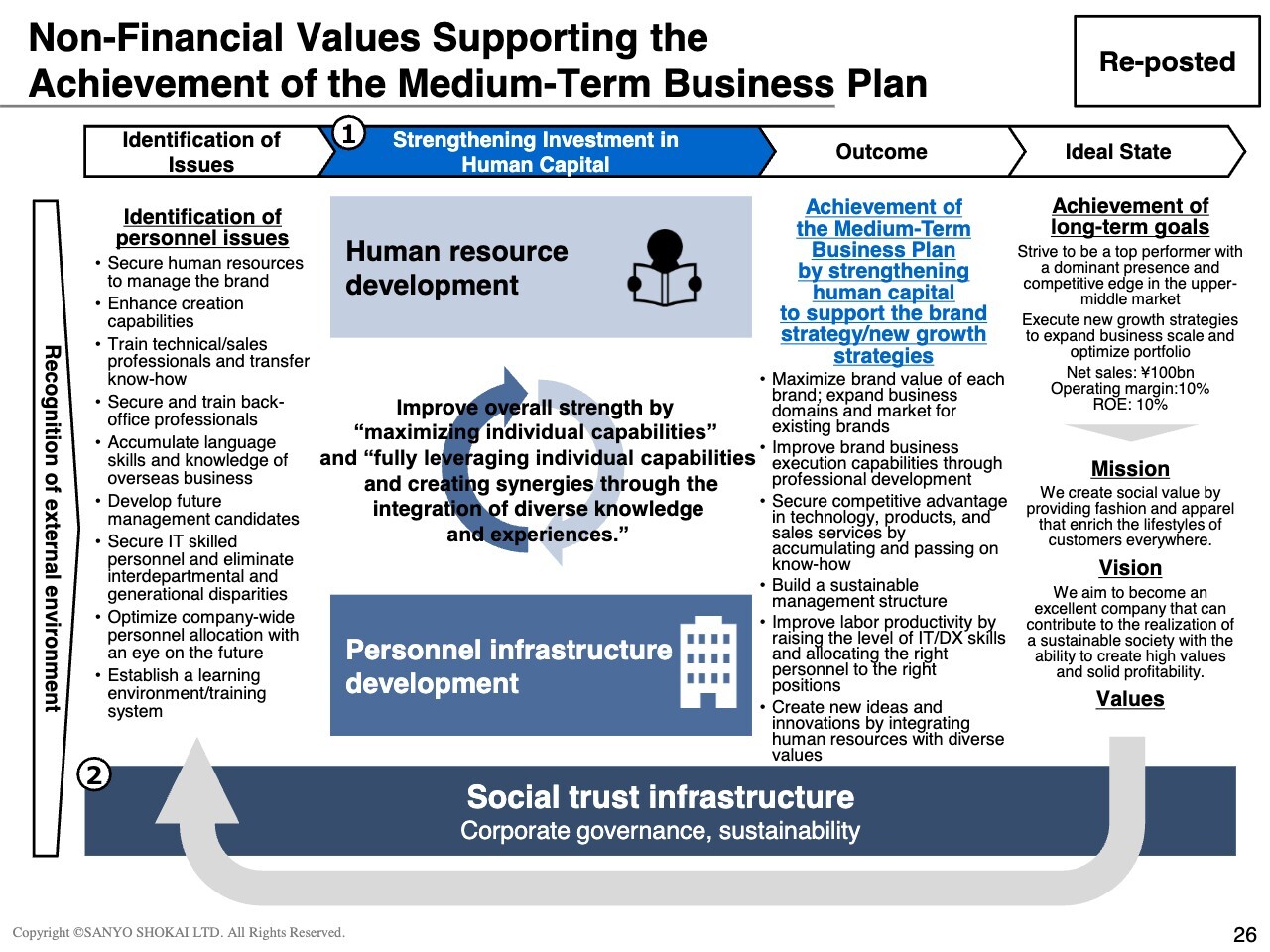

Non-Financial Values Supporting the Achievement of the MTBP

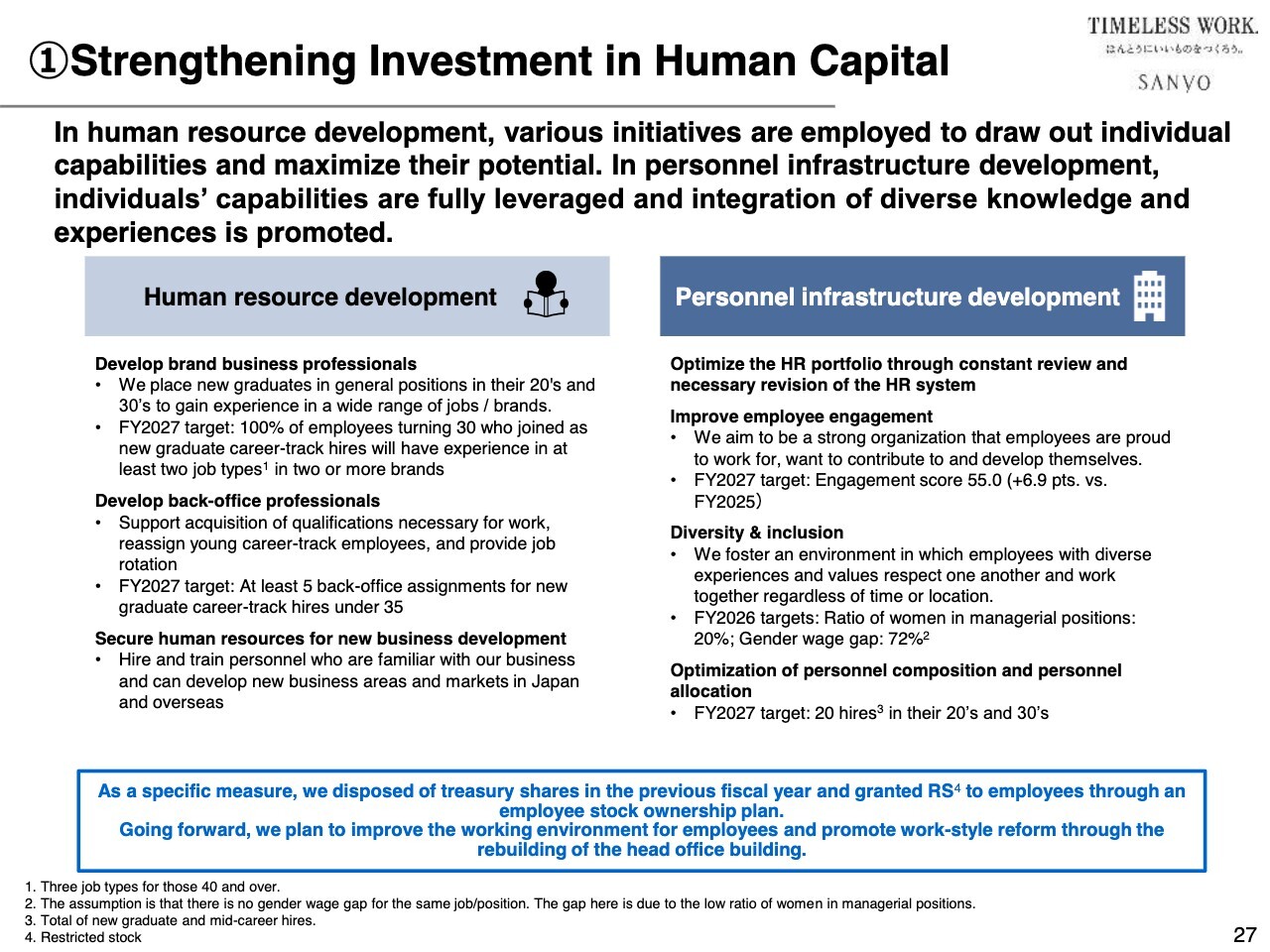

I will explain non-financial values. First, there are no changes to human capital-related initiatives from the initial plan. As a basic initiative, we are promoting human resource development and personnel infrastructure development as our priority issues.

① Strengthening Investment in Human Capital

Each detail is also in line with the initial plan. As for progress made in FY2026, the ratio of women in managerial positions has most recently risen to the 19% range, bringing the target of 20% within reach.

In addition, we are granting a portion of the treasury shares acquired through the share buybacks to employees as restricted stock (RS) through an employee stock ownership plan. Furthermore, the working environment for employees will be improved through the rebuilding of the head office building.

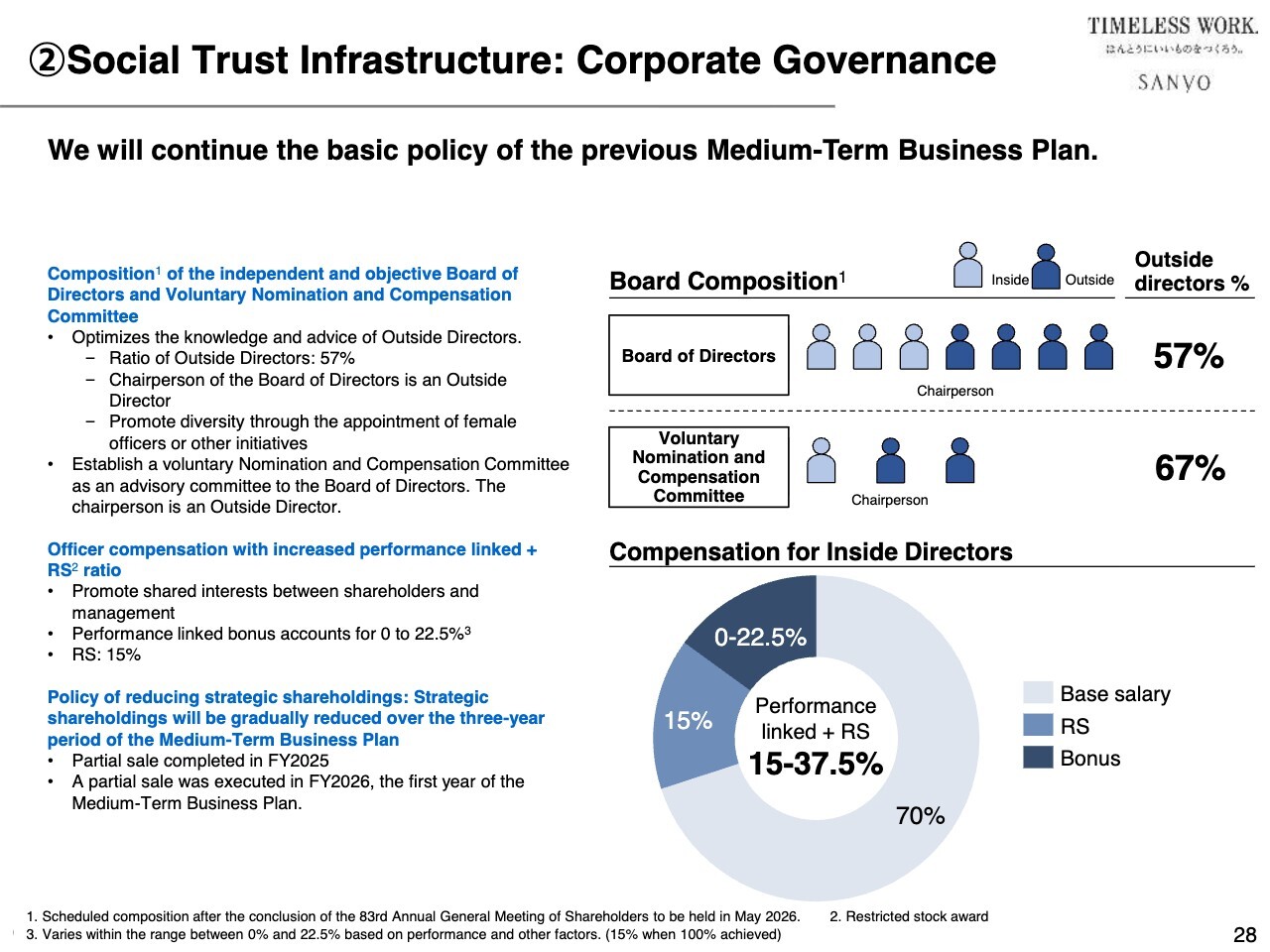

② Social Trust Infrastructure: Corporate Governance

Corporate governance is also in line with the plan.

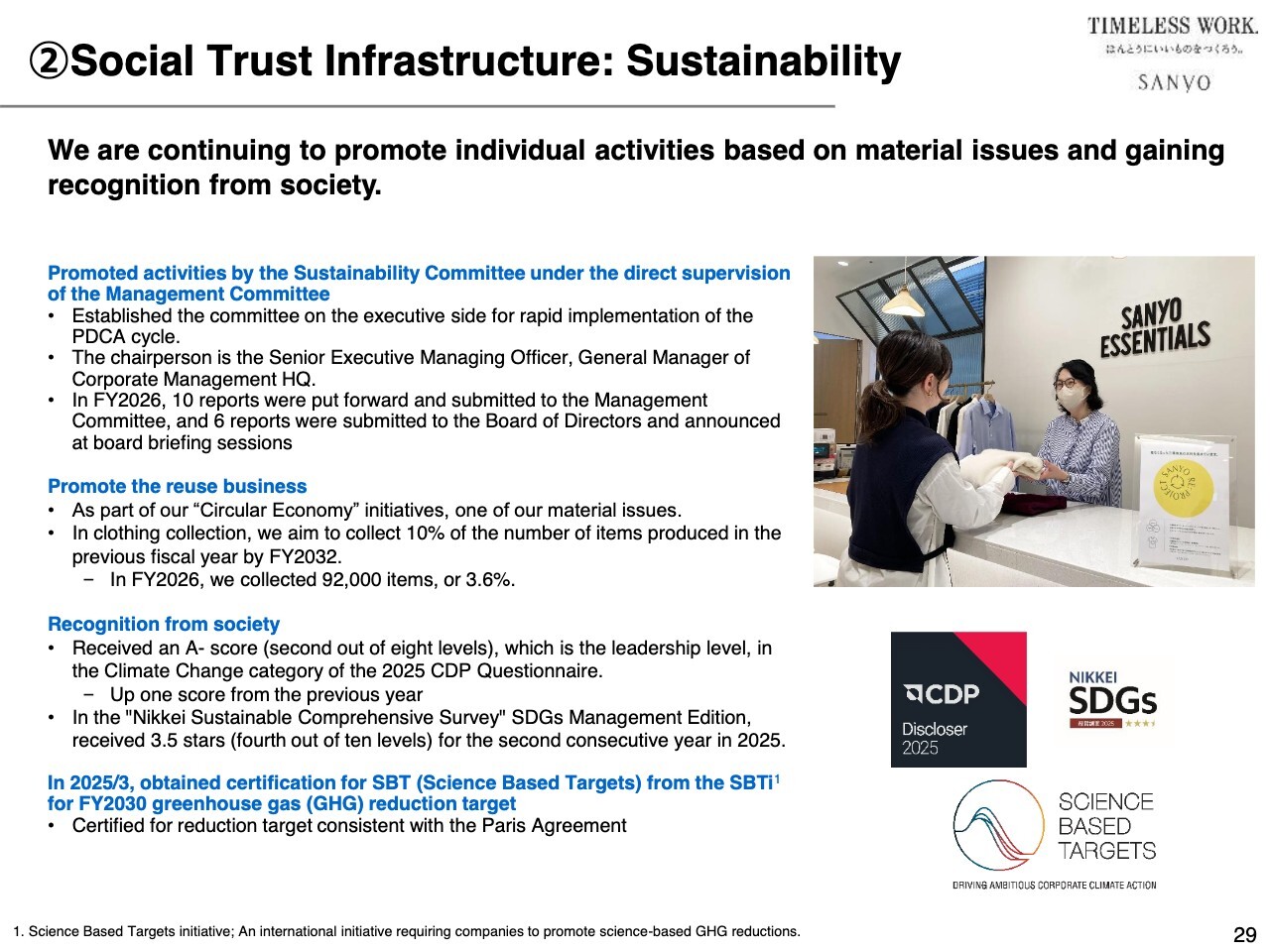

② Social Trust Infrastructure: Sustainability

I will explain our sustainability-related initiatives. Through the Sustainability Committee, we formulate and implement various measures.

Regarding the reuse business, we collected 92,000 items of clothing in FY2026. This is nearly doubled from just under 50,000 items collected the year before, and represents 3.6% of the total number of items produced in FY2026. We continue to aim to collect 10% of the number of items produced in the preceding fiscal year.

External evaluations of the Company’s sustainability initiatives have also improved. First, we received an A- score in the Climate Change category of the CDP Questionnaire. In addition, we received 3.5 stars for the second consecutive year in the SDGs Management Edition of the Nikkei Sustainable Comprehensive Survey.

This is the end of the explanation regarding the financial results for the fiscal year ended 28 February 2026 and the progress of the MTBP.

Q&A: Change in President and Division of Roles under the New Management Structure

Participant: I’d like to ask about the change in the president. What do you expect from the new management structure under Mr. Hirabayashi, the incoming president? As the current president, Mr. Oe, becomes Chair, how will roles be divided between Mr. Oe and Mr. Hirabayashi?

Oe: Six years have passed since I assumed the position of President, and given my age, I cannot continue in this role indefinitely. The Company has a voluntary advisory committee called the Nomination and Compensation Committee (NCC). At this committee, we have identified succession planning as a priority issue and have continued discussions on the topic. As a result, we have concluded that Mr. Hirabayashi is the most suitable successor.

Although I will be stepping down as President, I will continue to manage the Company alongside the president in my new role as Representative Director and Chair. By establishing a dual-leadership structure, we will strengthen both governance and business execution. Through this, we aim to break out of the performance stagnation of the past two years or so, improve performance, and put the Company back on a growth trajectory.

As Mr. Hirabayashi has gained extensive experience in a wide range of roles at MITSUI & CO., LTD. over many years, I personally believe he possesses a wealth of knowledge and insight. Since he is younger than I am, I hope that his fresh ideas and unique perspective on management and business execution will help bring about renovation.

Q&A: Response to Rising Raw Material Costs Due to the Situation in the Middle East and the Impact on the Store Opening Strategy

Participant: Given the situation in the Middle East, rising raw material costs are currently a hot topic. To what extent has your company factored in the increase in raw material costs? Alternatively, if you have already implemented measures to ensure a stable supply of products, please let us know.

Oe: The situation in the Middle East has no direct impact on the Company, because we mainly procure raw materials from Asia and do not import from the Middle East. However, we are concerned that various indirect effects may emerge in the future.

One reason for this is that, while some of the products we handle are made from natural fibers, a very high proportion of them are made from synthetic fibers. Since most synthetic fibers are petroleum-based products, there is concern that rising raw material prices will lead to higher procurement costs for the Company.

Furthermore, as I have mentioned before, uncertainty surrounding domestic and international political and economic conditions—including geopolitical risks—is having a significant impact on consumer sentiment. Combined with rising prices, this has led to a sharp increase in customers’ price consciousness and defensive mindset.

This situation is having various effects on the mid to high-end market, in which the Company operates. This is why department stores performed so poorly in the previous fiscal year. While there is no direct impact, we believe the indirect impact is significant.

We don’t have any breakthrough solutions, but since we have thoroughly analyzed the factors behind our poor performance in the previous fiscal year, I believe the only course of actions is to implement steady, careful measures for each issue one by one.

Participant: Regarding indirect impacts, for example, some homebuilders have announced that they would suspend orders for certain materials. Could this affect your store expansion strategy?

Oe: I think it could. Since we open dozens of new stores every year, this could potentially affect costs such as store setup costs.

Q&A: Impact of Naphtha Shortage Caused by the Situation in the Middle East and the Timing of Price Revisions

Participant: I apologize for another question regarding the situation in the Middle East, but there are also concerns about naphtha shortage. If price revisions or increases are going to be discussed at your company, when would that likely be? While they could take place in the current autumn/winter season, but could it be later than that? Please let us know the likely timing, to the extent possible.

Oe: In fact, we have received such requests from some of our suppliers. Vice President Kato will answer this question.

Ikuro Kato (“Kato”): It is true that some raw material suppliers have requested price increases for outer fabrics, linings, and accessories.

In response to price increases, we will take measures such as consolidating materials. Additionally, for this autumn/winter season, we plan to mitigate the impact of price increases by procuring winter materials early and consolidating orders across brands.

Q&A: Reflections on Mr. Oe’s Six Years and Challenges Ahead

Participant: I’d like to ask President Oe a question. Since you will serve as Representative Director and Chair under the new management structure, I’d like to take a moment to look back—even if it’s a bit early. Exactly six years ago, around this time, when you took office as President, the Company had posted operating losses for four consecutive years. Furthermore, on top of that situation, the COVID-19 pandemic struck, so I imagine you became President during an extremely challenging period. Looking back on these past six years, what would you say has been your greatest achievement?

Also, while this may overlap with your earlier remarks, what do you consider to be the remaining challenges that you and the incoming president, Mr. Hirabayashi, must address together?

Oe: Looking back over the past six years, I believe they can be broadly divided into two distinct phases: the first three years and the latter three years. During the first three years, we carried out a thorough business restructuring amid the impact of the COVID-19 pandemic. Specifically, we focused on cost reduction, risk management, and, in particular, inventory management, and have been thoroughly dedicated to securing the bottom line of the earnings structure. I believe we achieved clear results in this regard.

Following the Revitalization Plan, we achieved profitability in the third year. In particular, during the first and second years of the previous MTBP, we secured net sales and profits that significantly exceeded the plan, and we conclude that we delivered results in line with the scenario.

However, starting in the third year of the previous MTBP, we hit a bit of a plateau, and as soon as we entered the new MTBP, as I explained earlier, we ended up falling significantly short of the plan. We had entered the next phase—focusing on how to implement growth strategies and put the company back on a growth trajectory while securing the bottom line of our earnings structure—but far from delivering results, we actually stagnated and even regressed slightly. I feel a deep sense of regret regarding this. I will continue to support the company, but I hope that under the new president, we can break through the current impasse by incorporating new ideas and employing approaches different from my own.

On the other hand, considering the nature of Sanyo Shokai as a company and the various assets it holds, I still believe that our basic strategies and policies are appropriate. Going forward, I believe it will be necessary to reexamine how we apply these strategies and policies—that is, our methodology—and to adopt more effective approaches.

In any case, I myself intend to continue working alongside the president for the time being and to enhance our executive capabilities through a dual-leadership structure.

Participant: What are the main changes compared to six years ago?

Oe: All employees share the experience of success: starting from a situation where we were stuck in a prolonged operating loss and were unsure of what to do, we defined a certain direction, acted based on the hypothesis that this will lead to that result, and ultimately achieved positive outcomes.

Therefore, I believe that it was not so much the management itself, but rather the fact that all employees implemented the PDCA cycle and achieved this success that brought about a significant shift in their mindset.

Although sales declined and profits decreased in the previous fiscal year, we were still able to remain profitable. In this regard, while the results of the previous fiscal year were indeed disappointing and unsatisfactory, I believe they also demonstrated the resilience of the Company’s earnings structure.

I am confident that if we can strengthen our top line a bit more steadily, we will be able to consistently generate and expand profits as long as we maintain our current structure.

While there are still some shortcomings in our methodology, we believe that we have developed a sufficient shared understanding among the employees responsible for execution regarding how to generate profits.

Q&A: Launch of a New Brand and Strategy for the Upper-Middle Market

Participant: I understand that AUREME will launch in this year’s autumn/winter season, and HANAE MORI will launch in next year’s autumn/winter season. I had the strong impression that the new brand announced last year was positioned more in the mid-range segment, whereas this time it seems to be brands targeting the upper-middle market, or even a higher segment. Could you please share your current policy regarding the future rollout and development direction of the new brands?

Kato: First, regarding AUREME. As announced, it is positioned as one of our key strategies under a new growth strategy of the MTBP, to develop new in-house brands primarily targeting channels other than department stores, such as FB, commercial facilities, and e-commerce (EC). Based on this policy, we will begin rolling out the brand starting with the 2026 autumn/winter season.

We plan to begin sales through stores and EC in September 2026, and aim to expand to approximately 10 stores—primarily in FB—and achieve sales of JPY2.0 billion within five years.

We have appointed Ms. Misako Kushibe as the brand director. Under the brand concept of “Daily wear for the future that wraps you in air and caresses your skin,” we propose high-value daily wear that combines functionality and fashion, designed to address the climate and environmental changes faced by city dwellers. AUREME is developed based on this concept.

Next, I would like to talk about HANAE MORI, which we announced today. As part of the new growth strategy presented in the MTBP, it aims to drive new brand development, market expansion, and business expansion.

In partnership with MN Inter-Fashion Ltd., we have decided to launch a project to begin planning, manufacturing, and sales of the women’s total collection brand HANAE MORI starting with the 2027 autumn/winter season.

Our long-term goal is to become a top player with an overwhelming presence and competitive advantage in the upper-middle market. We position HANAE MORI as one of the brands that will drive this strategy.

Furthermore, this project—launched to mark the 100th anniversary of Hanae Mori’s birth—reinterprets the HANAE MORI brand, a pioneer among Japanese designers who expanded into international markets, from a contemporary perspective, presenting it anew as a brand with timeless value.

Centered on “timeless elegance,” this is a total collection that expresses the world of HANAE MORI—defined by minimalist yet striking design and high quality at an attainable price—through a contemporary sensibility.

We have appointed Mr. Satoshi Otsuki as the brand’s creative designer. He has over 10 years of experience at leading maisons in Paris and a proven track record as a director for domestic brands. We will begin development with the aim of targeting the upper-middle segment and, ultimately, the very top tier of the market.

Oe: To elaborate, high-end luxury brands continue to drive the apparel market. However, prices have risen so sharply that they are now out of reach for the average consumer.

In response, department stores realize they cannot rely solely on luxury brands forever, so they are seeking brands in the so-called “affordable luxury” or “accessible luxury” segments. For example, Isetan Shinjuku Store carries a wide range of such brands.

While we are also exploring the mid-market segment with some of our brands, our basic strategy is to target the higher-price segment and aim to enter the affordable luxury market.

For example, among our existing brands, we are aiming to position MACKINTOSH LONDON, Paul Stuart, and EPOCA in that segment. In addition, we believe it will be necessary to launch new brands designed specifically for that market from the outset. Based on this approach, while the form that the current HANAE MORI will take is still undecided, we are considering it as one potential option.

Q&A: Current M&A Strategy and Initiatives to Acquire Brands

Participant: I have a question regarding M&A. This topic was briefly mentioned in the MTBP presented during last year’s annual financial results, and I believe discussions have progressed since then. At the same time, I get the impression that M&A activity within the apparel industry has been accelerating recently, particularly over the past year. In light of this, could you explain how you plan to acquire strong brands as part of your current M&A strategy?

Oe: Regarding M&A, we have formed a task force and have now progressed to the stage of narrowing down the candidates to a shortlist. However, based on past experience, M&A transactions tend to have a relatively low success rate.

Therefore, we should carefully consider whether a project will enhance our corporate value, as well as whether we can truly take a hands-on approach to it from the perspectives of governance and operational management.

Over the past year, we have seen sales growth stagnate somewhat, and we have come to realize that achieving significant growth through organic growth alone is difficult. For this reason, we believe that methods such as launching new brands and securing business rights through acquisitions are indispensable in the growth strategy.

Q&A: Background to the Change in Management Structure

Participant: Your largest shareholder changed recently—did that aspect influence this change in management structure?

Oe: We are engaging in various discussions and maintaining close communication with our largest shareholder, but I will refrain from disclosing the specific details of the discussions.

This personnel change is unrelated to our largest shareholder. The change in management structure was decided by the NCC and the Board of Directors following careful internal deliberation, and there was absolutely no outside pressure and suggestions.

Participant: I understand that Mr. Hirabayashi, the candidate for the next president, is a former employee of MITSUI & CO., LTD., like President Oe. Did they know each other beforehand, or were Mr. Hirabayashi’s capabilities recognized by Mr. Oe?

Oe: Although I had no direct working relationship with Mr. Hirabayashi, I had heard from various people at MITSUI & CO., LTD. that he was highly regarded as an exceptionally capable individual. I consider him to be a person of exceptionally high caliber in every respect, including character and insight.

It should be noted that the fact that he is a former employee of MITSUI & CO., LTD. is purely coincidental; Mr. Hirabayashi was selected by the NCC after it determined that he was the most suitable candidate from among many.

Q&A: Measures to Address Climate Change

Participant: While you mentioned that weather conditions are contributing to the decline in net sales, I believe your company was among the first in the industry to implement season-based MD. Could you please explain why you are struggling, identify the most critical factors, and describe the measures you are taking to address them?

Kato: From 2023 through 2024, we have been actively promoting product development and the segmentation of MD to respond to the prolonged summer season from an early stage. However, that alone is not sufficient to address all challenges, as different factors come into play at different times, including pricing issues.

For example, stocking up on products in anticipation of the intense heat in August and September proved to be somewhat effective. However, we discovered that the purchasing behavior of fashion-conscious customers—such as buying items in advance—is more highly segmented than initially anticipated. As a result, through various trials over the past two years, we have learned that we need to improve pricing and seasonal product deployment based on more detailed analysis.

In addition, during the autumn/winter season—particularly from December through February—we need to respond to irregular weather conditions, such as warmer-than-usual winters or sudden cold snaps. For example, cold waves may hit in January or February, causing a sharp increase in demand for cold-weather products. We intend to leverage the lessons learned over the past two years to respond thoroughly in FY2027.

Q&A: Department Store Sales Channels

Participant: Department store sales channels currently account for approximately 60% of your net sales composition ratio. What composition ratio do you expect in the future?

Kato: Department stores are an important sales channel for us to maintain strong competitiveness in the mid to high-end market. At the same time, we must also actively develop brands tailored to other sales channels, such as FB, shopping malls, and EC. While formulating strategies based on the assumption that the share of department stores will gradually decline in the future, we intend to continue making every effort.

Oe: We have not changed our positioning of department store channels. Naturally, department stores remain our core sales market. Sales through department store channels declined year-on-year in the previous fiscal year, mainly due to a decrease in inbound sales, but have recovered this fiscal year and are now trending above the previous fiscal year.

I’ve heard that, more recently, inbound sales across department stores exceeded the previous-year level in March, partly due to the weaker yen. Although performance was weak in the previous fiscal year, I do not believe this trend will continue.

As I mentioned earlier, in connection with the closure of some railway-affiliated department stores, Meitetsu Department Store closed in February this year. We believe that with this closure, the phase of large-scale sales floor reductions has now largely come to an end. We expect the situation to remain mostly stable going forward.

Furthermore, regarding the department store market, the differentiation of sales floors has continued to progress over the past few years. We believe that the department store market has become more clearly positioned as a high-end market, and that its status and presence as a special sales channel distinct from other markets have increased compared with before.

However, the issue is that department stores are increasingly focusing on luxury products and prioritizing their watch and jewelry sections. Due to this policy, we are facing a challenge in securing sales floor space. However, that is precisely why we need to step up our efforts toward department stores—not only to maintain our current sales floor space but also to secure new space.

For this reason, we will not only focus on our existing brands but also strengthen our combined shops, such as EPOCA THE SHOP and SANYO Style STORE. At the Matsuzakaya Nagoya Store, EPOCA THE SHOP has achieved excellent results by shifting from a free standing format to an in-store format. We believe it is essential to develop new store models like this and propose store formats that are attractive to department stores as well.

We believe that, as for our customers, those who can truly recognize and appreciate the product and brand value of upper-middle brands like ours are, indeed, department store customers. Since our target demographic does not always align well with the customer base at commercial facilities, our core customer base remains department store customers.

For example, most of our top customers—our so-called loyal customers—are department store customers. Therefore, we certainly don’t view department stores negatively. However, given that securing sales space in department stores has become increasingly difficult, we face the dilemma that growth will be hard to achieve if we remain overly dependent on department stores. Therefore, we believe that our future strategy will likely be to develop channels beyond department stores and increase non-department-store channels, thereby reducing the relative dependence on department stores while still growing department store sales.

Q&A: Opening of SANYO Style STORE+ in Suburban Shopping Centers

Participant: Could SANYO Style STORE+—which you mentioned is a new version— also be expanded into suburban shopping centers?

Oe: You’re absolutely right. However, the existing product line of SANYO Style STORE is not entirely aligned in terms of price range, and we also need to differentiate it from department stores. Therefore, we are considering creating a new line under the existing brand, adjusting the price range somewhat, and expanding into some GMS-type commercial facilities as well. We plan to roll out this initiative as a separate version from the existing SANYO Style STORE, with a revised product lineup.

Q&A: Thoughts on Going Private

Participant: From our perspective as investors seeking short-term returns, the biggest issue is how to provide exit opportunities for activists. Is privatization currently being considered?

Oe: We have no plans to go private at this time. We believe that maintaining our listing and achieve sustainable growth under stringent conditions such as maintaining listing standards will lead to an increase in corporate value over the medium to long term.