SECTION

Kosuke Kiyokawa: Hello investors and shareholders. I am Kosuke Kiyokawa, CEO of COPRO-HOLDINGS. Co., Ltd. Today, I will walk you through the briefing materials of the financial results for 3Q FYE3/2026.

Today’s briefing consists of Sections 1 through 5. Sections 6 and 7 are provided as reference materials.

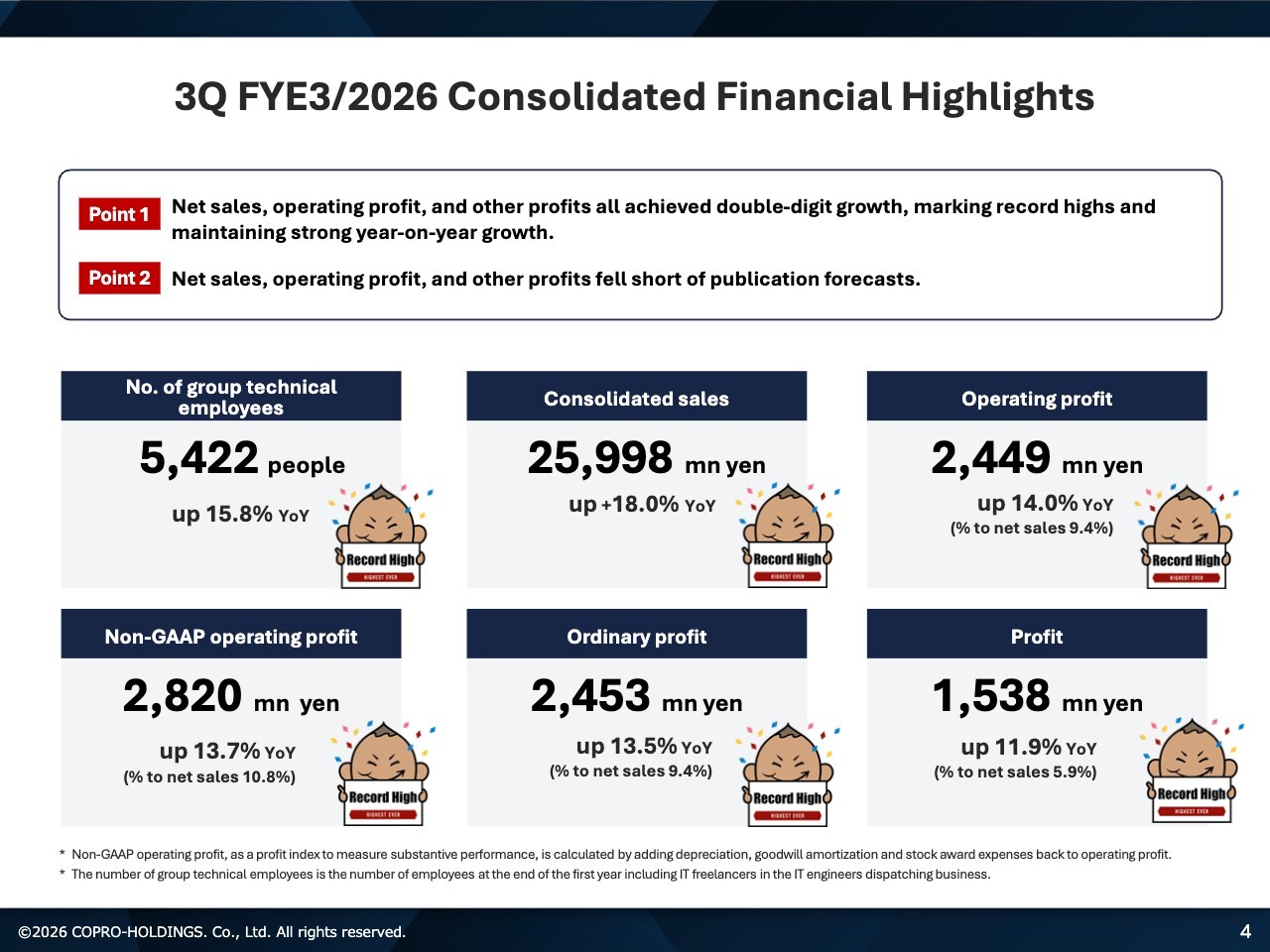

3Q FYE3/2026 Consolidated Financial Highlights

In Section 1, I will summarize the financial results for 3Q FYE3/2026. This slide presents the consolidated financial highlights. We list six key metrics below, and I would like to focus on two main points.

First, we marked record highs across all key metrics, including net sales and operating profit margin.

Second, we achieved double-digit year-on-year growth in both net sales and profits, maintaining strong growth. Let me now walk you through the key figures in detail.

The number of group technical employees was up 15.8% YoY to 5,422. Consolidated sales were up 18% YoY to ¥25,998 million, and operating profit was up 14% YoY to ¥2,449 million, with operating profit margin of 9.4%.

Non-GAAP operating profit was up 13.7% YoY to ¥2,820 million, representing 10.8% of net sales. Ordinary profit was up 13.5% YoY to ¥2,453 million, representing 9.4% of net sales.

Profit was up 11.9% YoY to ¥1,538 million, representing 5.9% of net sales. As you can see, we achieved record highs across all areas.

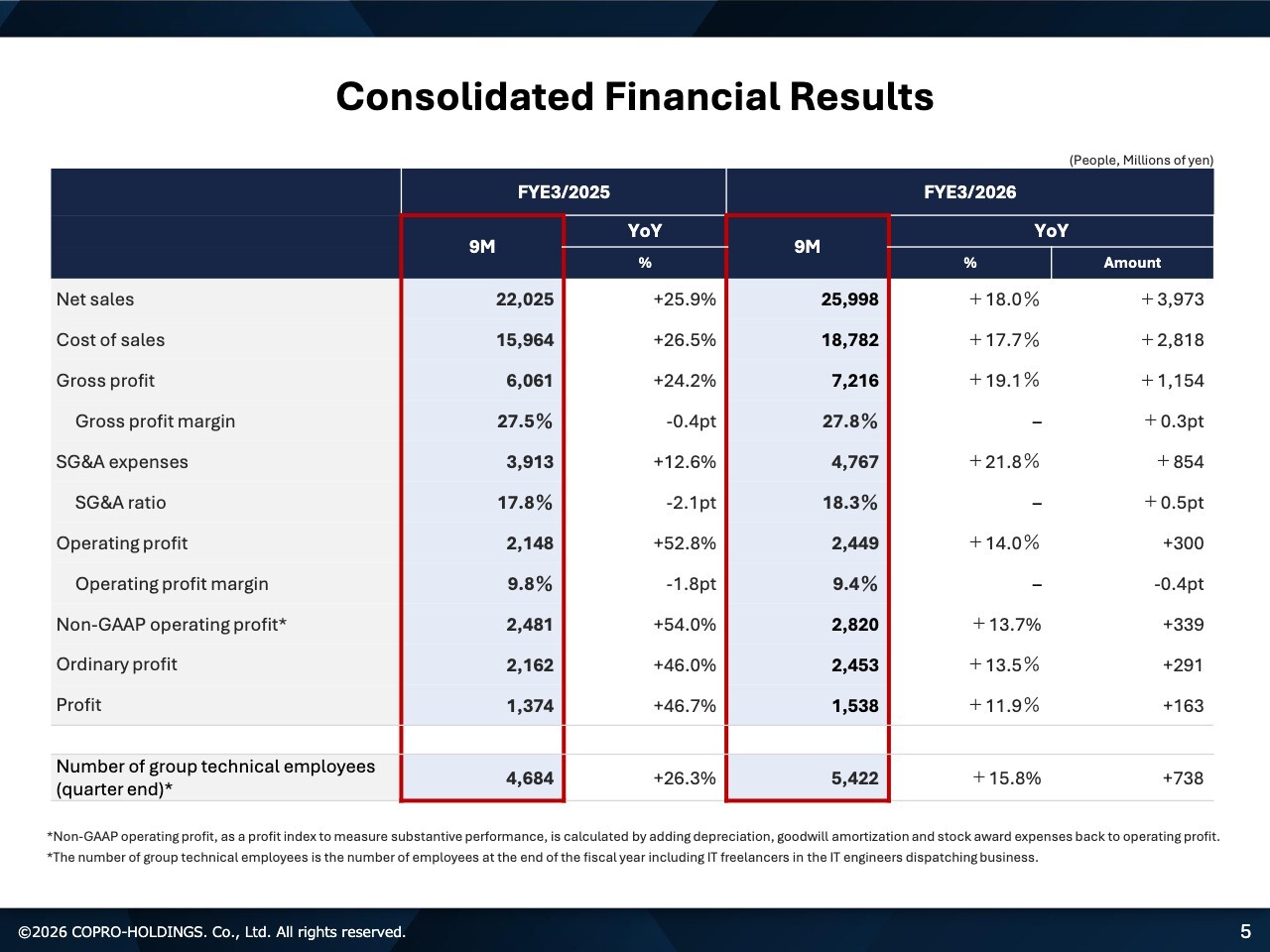

Consolidated Financial Results

Let me turn to the consolidated financial results. This slide shows the P/L. In addition to the points I just covered, gross profit reached 27.8% of net sales, an improvement of 0.3 % YoY. Please refer to the slide for the detailed figures.

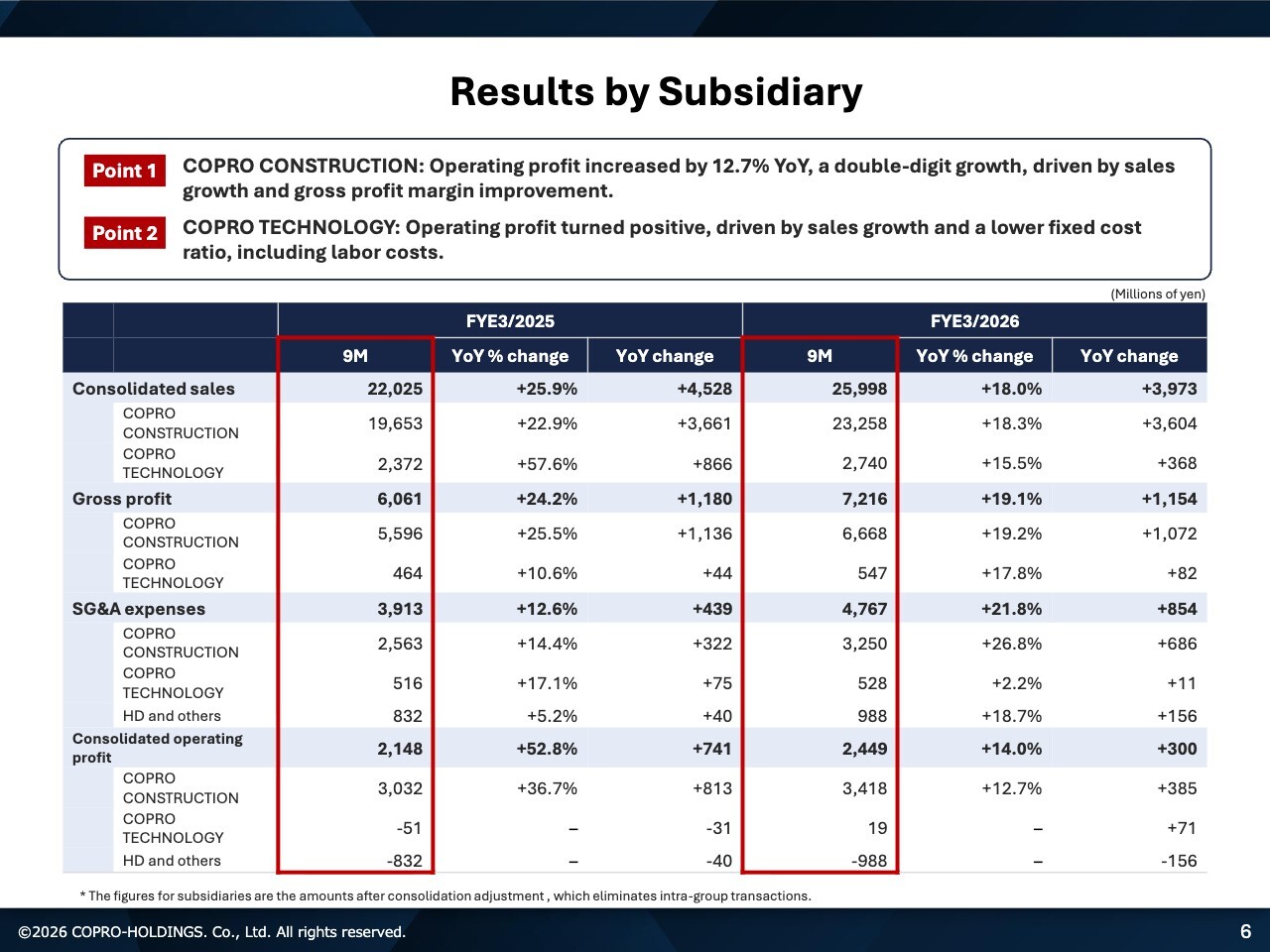

Results by Subsidiary

Let me walk you through the results by subsidiary. There are two key points to highlight.

The first key point relates to COPRO CONSTRUCTION. In the construction sector, higher net sales drove gross profit growth, more than offsetting the increase in SG&A expenses. As a result, operating profit rose 12.7% YoY, delivering double-digit growth.

The second key point is COPRO TECHNOLOGY. In the mechanical & electrical, semiconductor, and IT sectors, operating profit turned positive, driven by higher net sales and lower fixed costs, including labor costs.

We have prepared detailed figures for net sales, gross profit, SG&A expenses, consolidated operating profit, and P/L. Please review them at your convenience.

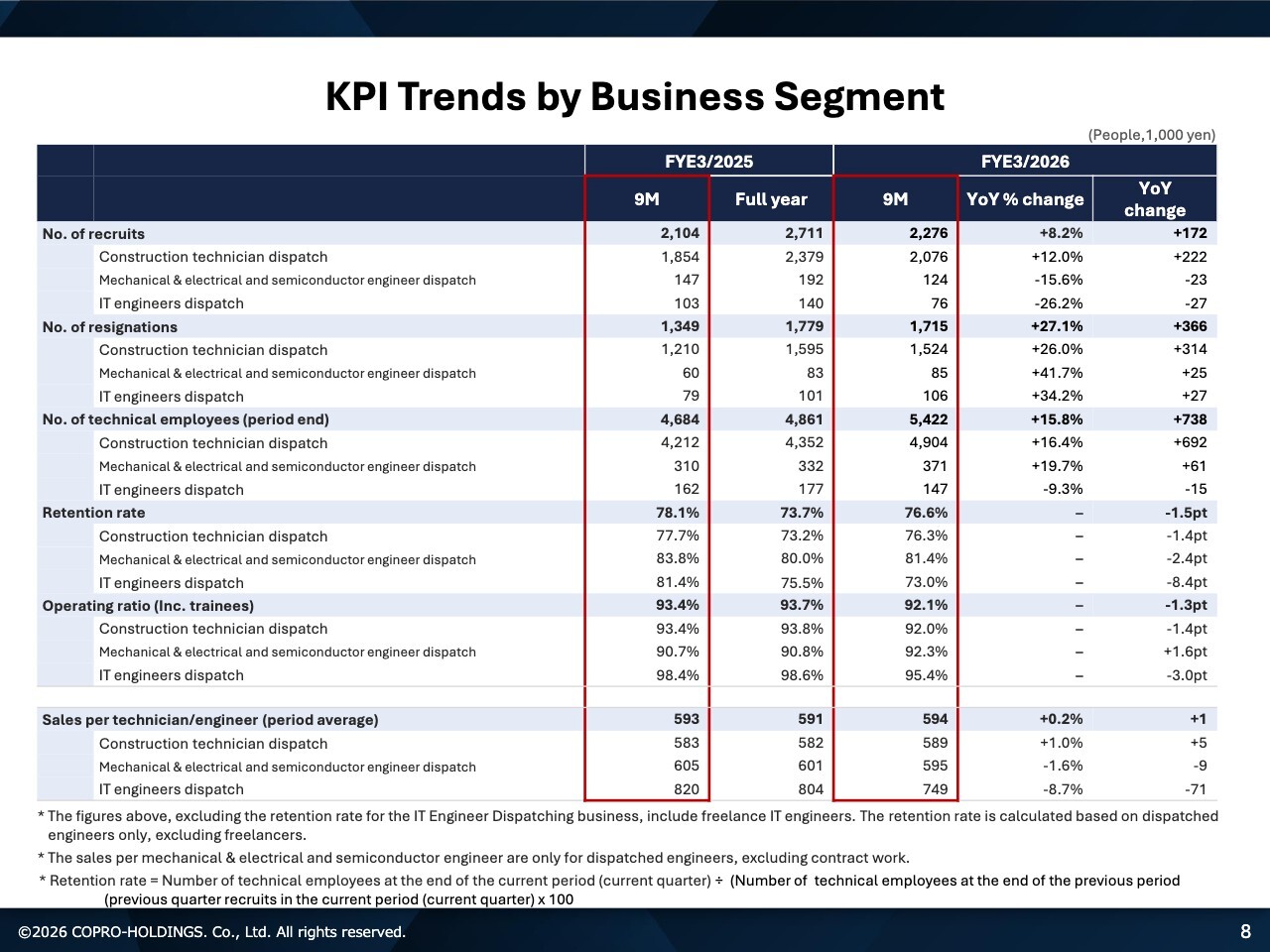

KPI Trends by Business Segment

In Section 2, I will review our KPI performance by business segment. First, let me walk you through the KPI trends by business segment. This slide shows the number of recruits, the number of resignations, the number of technical employees (period end), retention rate, operating ratio (including trainees), and sales per technician/engineer (period average).

As you can see, we faced some challenges in recruiting. Retention rate declined by 2.5 % YoY. Operating ratio also decreased, from 93.4% to 92.1%.

One factor, as summarized in 3Q, was that the accuracy of matching new recruits with incoming projects was somewhat low. As a result, retention rate declined and operating ratio edged down slightly.

In response, we plan to focus on strengthening our core priorities—enhancing sales activities, increasing recruitment, expanding our applicant pool, and improving our matching capabilities—and will work diligently on these improvements going forward.

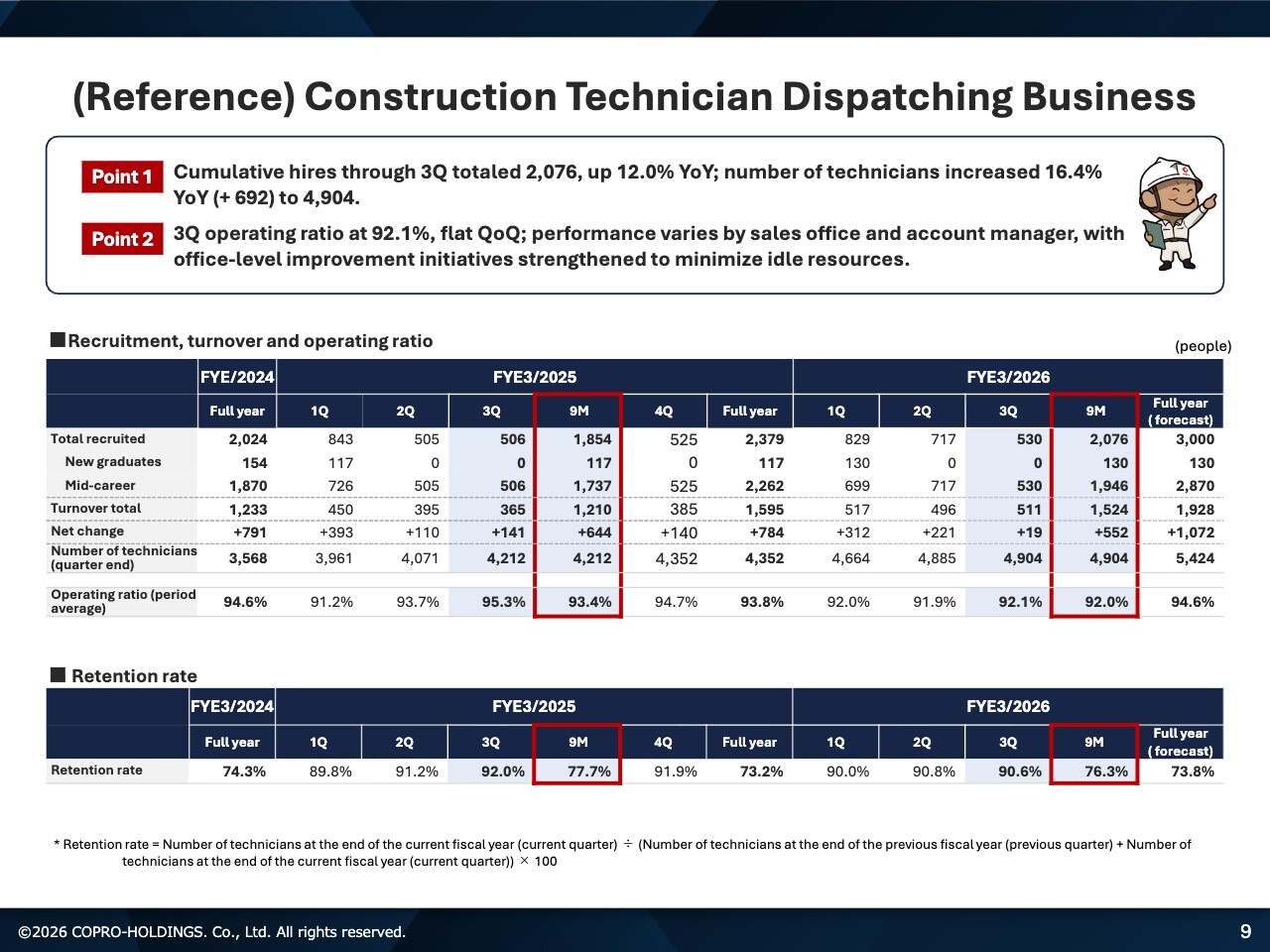

Construction Technician Dispatching Business

Let me address each segment in turn. In the field of construction technician dispatch, there are two key points to highlight.

First, cumulative hires through 3Q increased 12% YoY to 2,076. The number of technical employees rose 16.4%, or 692, to 4,904.

Second, operating ratio in 3Q was 92.1%, in line with 2Q.

As I mentioned earlier, performance varies by sales office and account manager. In 4Q, we are standardizing these processes to raise productivity across all offices and account managers and to minimize the number of standby engineers.

Mechanical & Electrical and Semiconductor Engineer Dispatching and Contracting Business

Let me turn to the field of mechanical & electrical and semiconductor engineer dispatching business. There are two key points to highlight.

First, the number of technical employees rose 19.7%, or 61, to 371. Within this total, the number of semiconductor engineers increased by 35 YoY to 156. Mechanical design engineers rose by 26 to 215.

Second, hiring is lagging behind our full-year forecast. While we have secured a solid applicant pool, offer acceptance rate remains weak. Accordingly, we will analyze and monitor hiring yield at each stage of the hiring process to identify where issues are arising, and take swift action to resolve problems.

In addition, we will streamline and improve our hiring processes and operations. We will execute decisively in 4Q to deliver on our full-year targets.

The retention rate shown at the bottom of the slide is significantly higher than in our core construction sector.

Although the nature and intensity of the work, as well as the in-house working environment, differ significantly, we believe we can further increase retention rate among mechanical & electrical and semiconductor engineers. Accordingly, we will focus on improving retention among younger employees. Through these initiatives, we aim to further raise our overall retention rate.

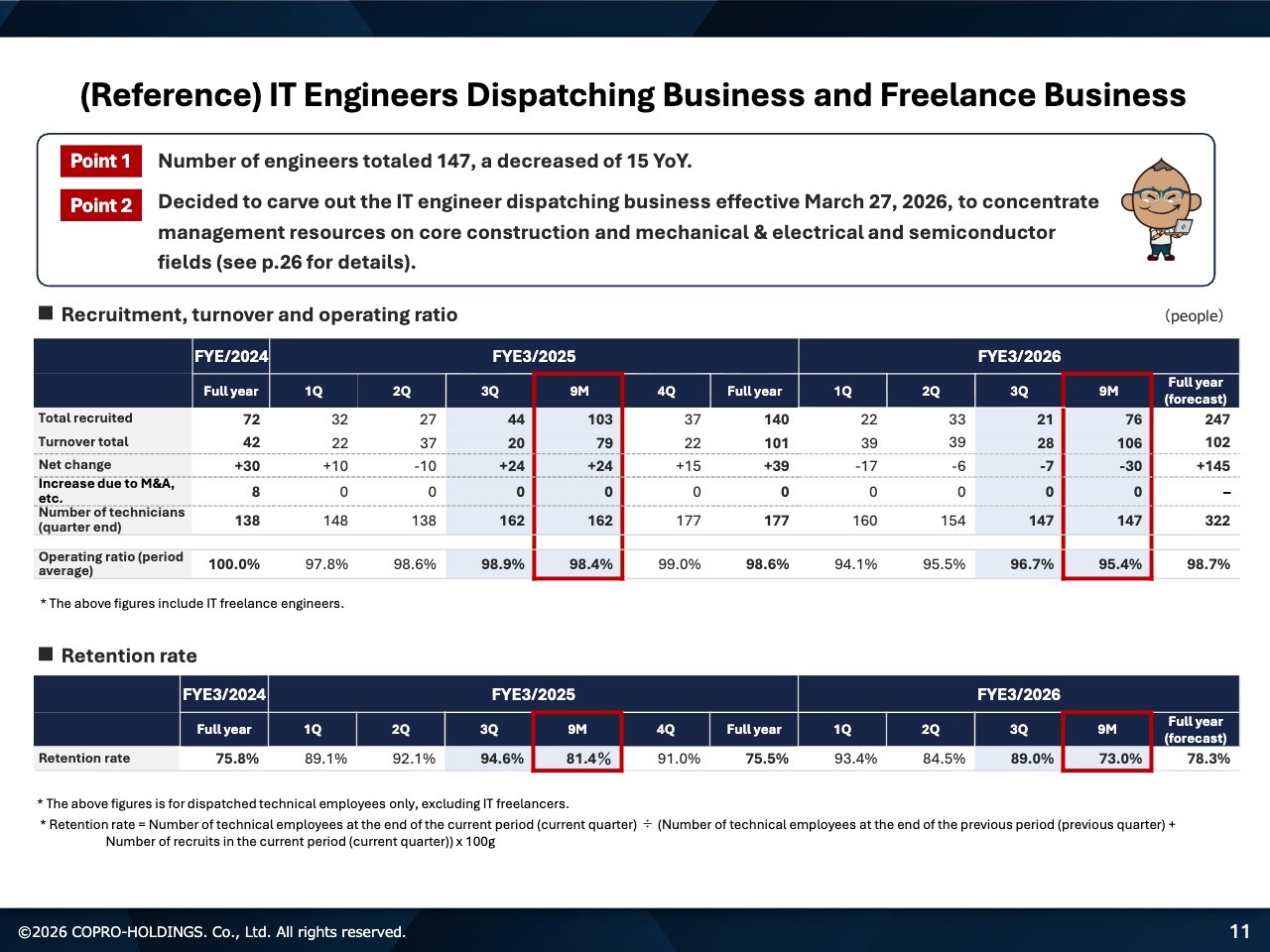

IT Engineers Dispatching Business and Freelance Business

Let me turn to the IT sector. There are two key points to highlight.

First, the number of technical employees declined by 15 YoY to 147.

Second, to concentrate management resources on core construction sector and mechanical & electrical and semiconductor fields, we have decided to carve out the IT engineer dispatching business as of March 27, 2026. I will provide more details on this shortly.

I will skip the review of the key KPIs for now.

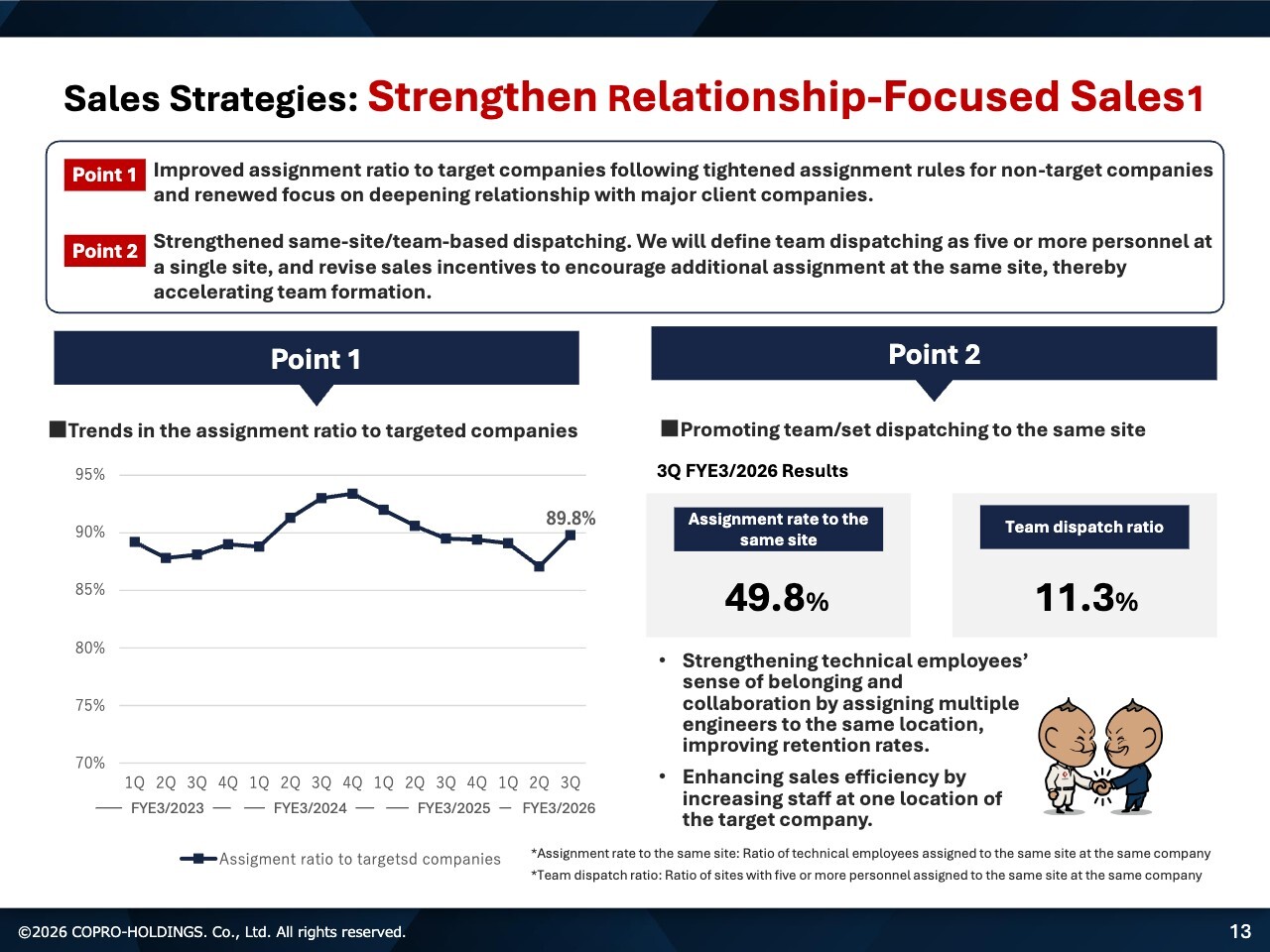

Sales Strategies: Strengthen Relationship-Focused Sales1

In Section 3, I will outline the field of construction technician dispatch. This slide summarizes the sales strategies we are executing. These are ongoing initiatives, but I will briefly revisit them here. There are two key points to highlight.

First, under our sales strategy, we have tightened assignment rules for non-target companies. By refocusing on deepening relationship with major client companies, we have improved the ratio of assignments to target companies.

Second, let me address our strategy. We have made retention of younger employees our top priority. Specifically, rather than dispatching younger employees on their own, we prioritize assigning them to sites where our experienced and mid-career engineers are already deployed and performing well. We call this our “assignment at the same site” strategy.

In addition, we define “team dispatching” internally as assigning five or more employees to the same site.

We believe that increasing the assignment rate to the same site and improving the team dispatching rate will directly improve retention rate among younger employees. We will continue to refine and strengthen this approach.

On the other hand, the assignment rate to the same site currently stands at 49.8%, close to 50%. However, given that it exceeded 50% in 1Q and 2Q, the overall ratio has declined. Similarly, the team dispatching rate has edged down slightly to 11.3% in 3Q.

To execute our current sales policy and fully implement initiatives that increase retention rate based on established rules and evidence, we must further raise the assignment rate to the same site. Increasing the team dispatching rate is also a key strategic priority for us. We will continue to focus on lifting both metrics.

Sales Strategies: Strengthen Relationship-Focused Sales2

Let me now explain another key sales strategy.

First, in April 2025, the sales headquarters—headed by President Koshikawa of our operating subsidiary COPRO CONSTRUCTION—relocated from our founding city of Nagoya to Tokyo. Capturing market share in the Kanto area, particularly Tokyo, which accounts for the largest share of construction investment, is critical. Consequently, we have relocated the president and key staff to focus on this market. The president will take direct command in the Kanto area to drive a focused and effective market strategy.

Second, while regional sales growth is sluggish, the Kanto area remained resilient, covering struggles in other areas and driving overall performance.

While growth in our regional branches has slowed, the regional markets still hold significant potential. Pursuing opportunities in the Kanto region while strategically expanding in other areas is a key challenge for our nationwide operations.

We need a balanced strategy that goes beyond simply concentrating resources in one area. It is critical that we deliver our services effectively across Japan and actively capture market share nationwide.

Let me explain the diagram on the slide. The Point 1 chart compares the number of engineers we have in the Kanto area against our competitors. We recognize that we currently rank third in the industry in this region. Our focus is on improving this ranking by executing targeted strategies, initiatives, and actions to capture market share decisively.

The Point 2 chart shows quarterly growth rate of sales. The red line represents YoY net sales in the Kanto area, while the black line shows net sales in all other areas.

We aim to grow the Kanto area steadily, maintaining consistent upward momentum rather than pursuing rapid expansion. At the same time, we are addressing the slight decline in sales at our regional branches and actively working to restore consistent growth. We will continue executing this approach with discipline and focus.

Recruiting Strategies: Enhance Our Strength of “Low Unit Price for Recruitment”

Let me explain our recruiting strategy. We are committed to our “low unit price for recruitment” approach designed to operate independently without relying on external parties. We view this as a critical area for ongoing focus and continuous improvement. Looking back at 3Q, two key points stand out.

First, the number of recruits in 3Q increased by 4.7% YoY to 530. However, the unit price for recruitment was ¥521,000, up QoQ due to lower yield.

Second, the number of recruits in 3Q cumulative increased by 12.0% YoY to 2,076.

Please refer to the bar and line charts under Point 1 on the left side of the slide. In 3Q, the total number of recruits reached 530, with the unit price for recruitment settling at ¥521,000.

On the right side of the slide, Point 2 shows cumulative hires and the ratio of inexperienced hires. As of 3Q, cumulative hires totaled 2,076, with 77.5% of them being inexperienced hires.

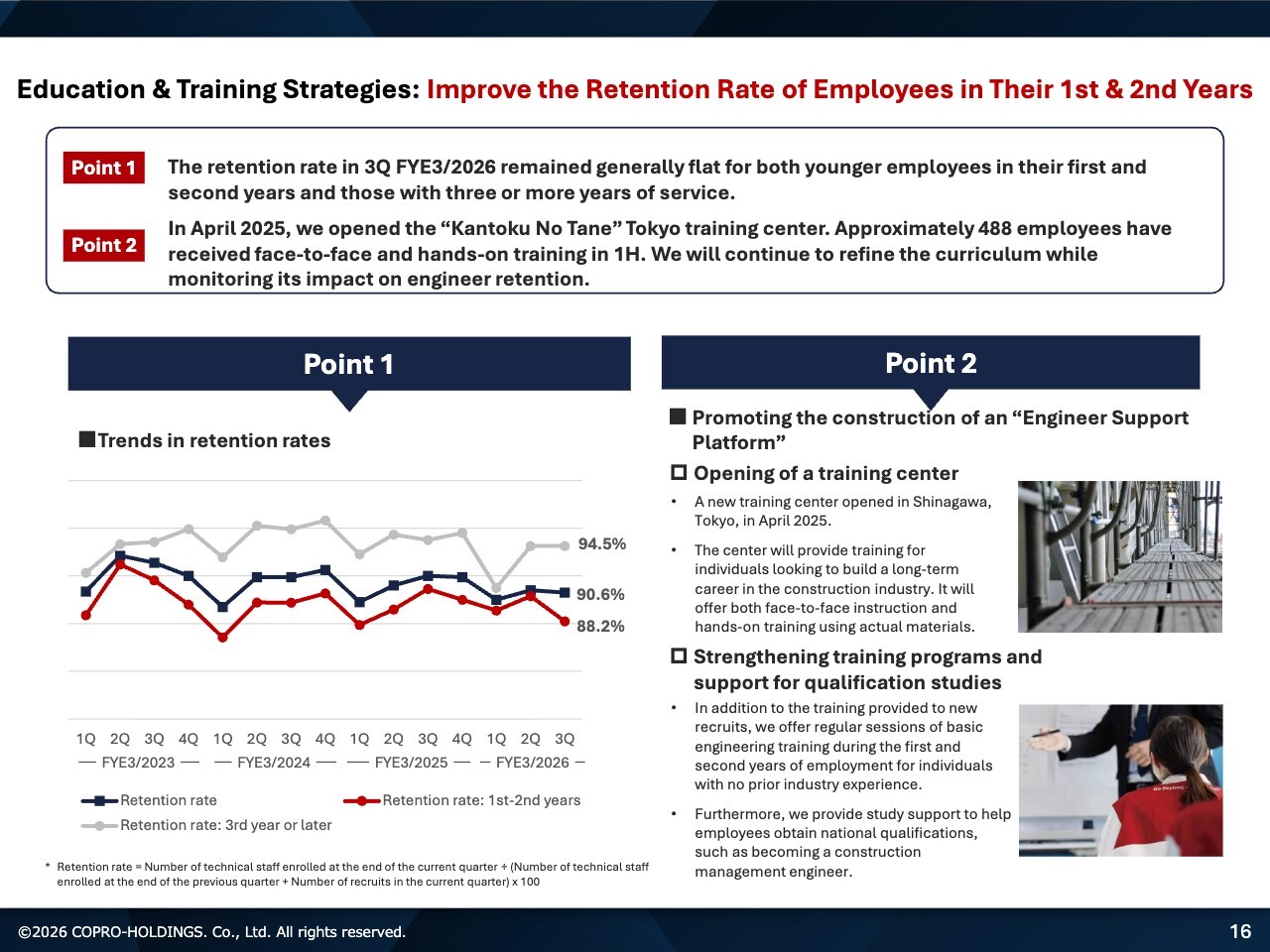

Education & Training Strategies: Improve the Retention Rate of Employees in Their 1st & 2nd Years

Let me explain our education and training strategy. This approach focuses on improving retention rate among younger employees in their first and second years.

First, in 3Q, retention rates remained generally flat for both younger employees in their first and second years and those with three or longer years of service.

Second, in April 2025, we opened the “Kantoku No Tane” Tokyo training center. Engineers who have received face-to-face and hands-on training at this center are beginning to show early signs of reduced short-term turnover.

Moving forward, we will continue refining the curriculum to meet on-site needs, while closely evaluating its impact on medium- to long-term retention.

In April 2025, we opened a training center in the Shinagawa area of Tokyo. The center provides training for young employees to improve retention rate in their first and second years. Supporting employees as they advance into their third year and beyond—where higher billing rates are expected—is a critical focus, and we are actively driving initiatives to achieve this.

Aiming for an Overwhelming No.1 Position in the Industry for Construction Technician Dispatch

Section 4 focuses on our strategy to aim for an “Overwhelming No.1 Position in the Industry.”

We aim to become an “Overwhelming No.1 Position in the Industry” in the field of construction technician dispatch. Rather than launching a new strategy, we are focused on updating and refining the strategies we have consistently pursued.

There are two key points to highlight. First, building on a strong sales foundation—anchored in deeply cultivated sales activities targeting companies that prioritize engineers—we have established and continuously strengthened our own low-cost hiring system that does not rely on external recruitment agencies, achieving the industry’s highest growth rate.

Second, in addition to expanding industry share, we are improving retention rates—a key measure of satisfaction for both engineers and customer companies—to aim for an “Overwhelming No.1 Position in the Industry.” We also pursue a world where the value of dispatched engineers is fully recognized, embodying our commitment to “copro, the responsive pros.”

As shown in the slide, we are aiming for an “Overwhelming No.1 Position in the Industry” for both scale and quality.

Overview of the Share Acquisition

Now, let’s shift to a different topic. This year marks our 20th anniversary and seven years since our listing, during which we have made significant management decisions. I will now explain our acquisition of shares in TRYT Inc. and TRYT Engineering Inc.

We will acquire 100% of the shares of TRYT Inc. and TRYT Engineering Inc. from a special purpose company (SPC) formed by Carlyle, a U.S.-based investment fund. The acquisition cost is ¥29,243 million.

By leveraging our sound financial strength, we plan to fund the acquisition using excess cash on hand together with borrowings from its bank. The closing is scheduled for March 1, 2026.

Structure of the Share Acquisition

The slide illustrates the structure of the share acquisition. The diagram shows the process and structure of how we will acquire the shares from Carlyle.

In brief, we will separate the TRYT Group into construction and non-construction businesses, bringing TRYT and TRYT Engineering—responsible for the construction worker dispatching business—into the COPRO Group.

The diagram on the right side of the slide shows the post-transaction structure, illustrating how the company will be transformed into the COPRO Group.

Strategic Significance

Let me explain the strategic significance of this move. Our company is committed to aiming for the “Overwhelming No.1 Position in the Industry” for both scale and quality. Externally, our industry is now entering a wave of industry consolidation.

As mergers and capital and business alliances unfold across the industry, we aim for the “Overwhelming No.1 Position in the Industry” and recognize that we must take the lead in driving this consolidation.

This major management decision is made against that backdrop. It can be broken down into three key elements.

The first element is securing technicians/engineers as the foundation for business growth. To drive organic growth, we must continue recruiting talent and promote low-cost hiring. At the same time, by bringing a competitor into our group, as we have done in this case, we can secure a truly overwhelming number of engineers.

To meet customer demand for a stable and sufficient supply of technicians/engineers and high retention, we aim to further enhance our human resource services by combining TRYT Engineering’s high-quality talent, our nationwide office and customer network, and digital marketing–driven recruitment of experienced technicians/engineers.

The second element is creating scale advantages. We and TRYT Engineering have competed directly and have driven mutual improvement through years of head-to-head competition. We serve many of the same client companies and place similar types of talent. By building greater scale, we will strengthen our negotiating leverage with customers and aim to increase contract unit prices.

In Japan, inflation is prompting both large corporations and SMEs to raise employee benefits and compensation by 5% to 6%. By increasing our contract unit prices, we will improve benefits for our valued engineers.

The third element is laying the groundwork for further industry consolidation. This share acquisition marks a critical step toward realizing our vision of becoming the “Overwhelming No.1 Position in the Industry.” We aim to create value for all stakeholders, including society, customers, employees, and shareholders by establishing us as a leading company and exercising clear competitive advantages.

We will also lay the groundwork to take a leading role in the consolidation of the construction technician dispatching industry by building a strong foundation and proven track record within the industry.

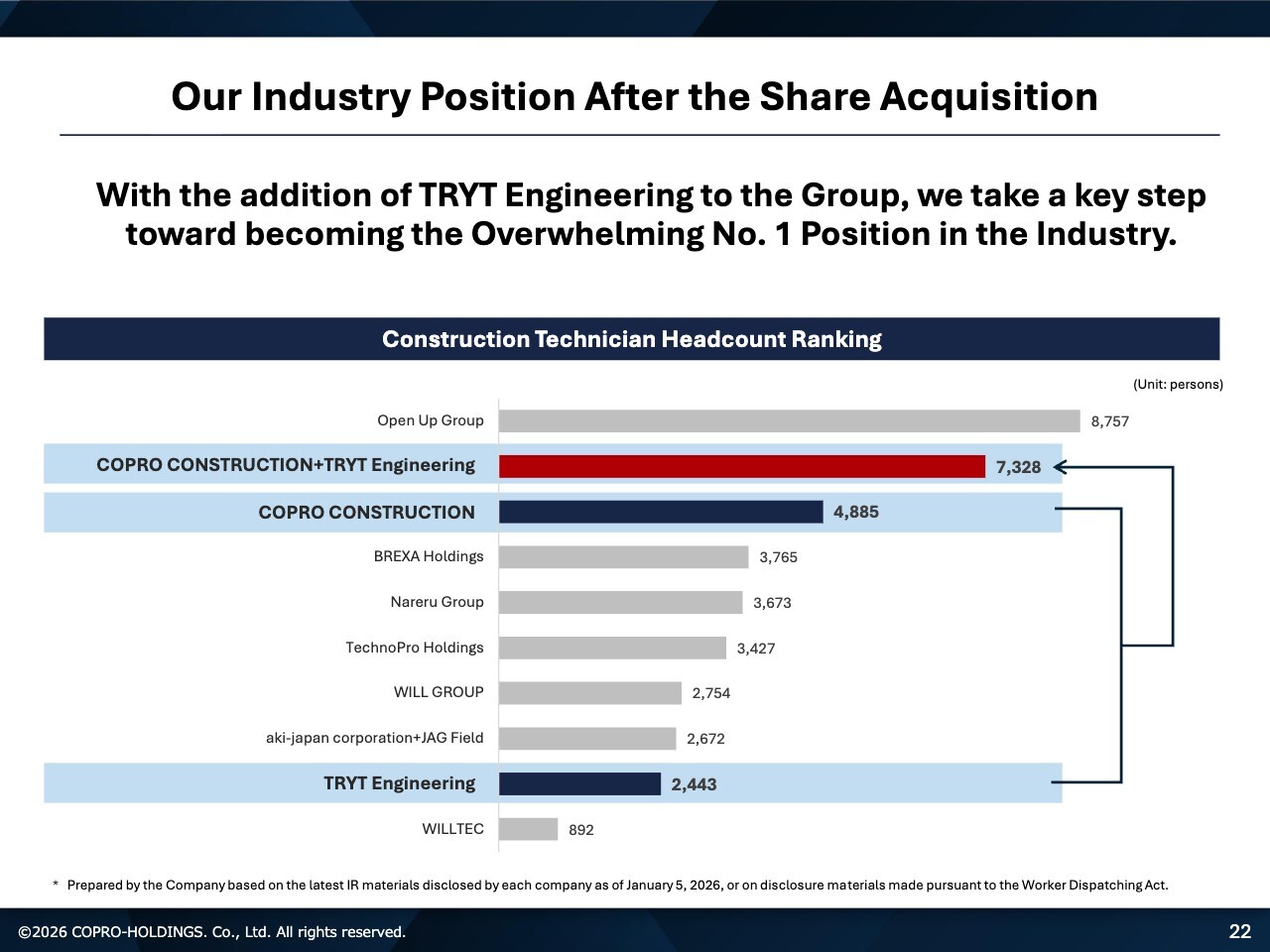

Our Industry Position After the Share Acquisition

Let me explain our post-share acquisition position in the industry using this chart. By bringing TRYT Engineering into the COPRO Group, we take a key step toward becoming the “Overwhelming No. 1 Position in the Industry.”

The chart at the bottom of the slide shows the ranking by number of construction technicians. Currently, the construction sector under Open Up Group ranks No. 1 in the industry, with the largest workforce of construction technicians.

Before bringing TRYT Engineering into our group, we ranked No. 2 in the industry, with 4,885 technicians. TRYT Engineering, which will join our group, ranked No. 8 and employed 2,443 technicians.

As shown by the red bar, combining COPRO CONSTRUCTION and TRYT Engineering brings our total technician headcount to more than 7,300. This puts us within striking distance of the industry leader, the construction sector under Open Up Group.

Going forward, we will fully capture synergies between COPRO CONSTRUCTION and TRYT Engineering. In addition to driving organic growth, we intend to take further steps to lead industry consolidation.

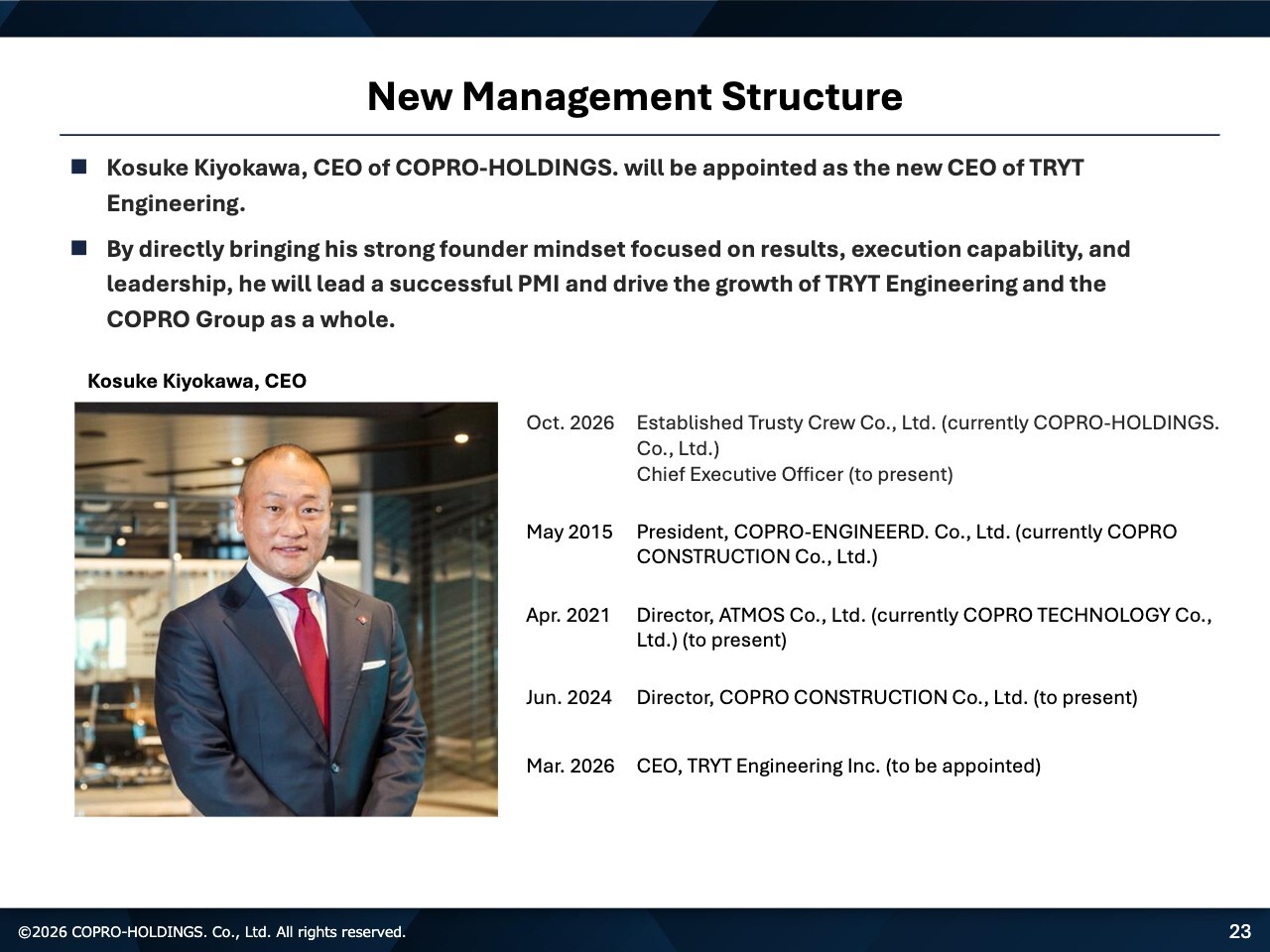

New Management Structure

This slide outlines our new management structure. You can see my photo on the slide. We view this investment—close to ¥30,000 million—as a major strategic commitment.

I will personally serve as CEO of TRYT Engineering, exercise strong leadership, and ensure a successful PMI. At the same time, I will lead growth across the entire COPRO Group, starting with TRYT Engineering. I will take the lead in delivering growth that justifies this significant investment.

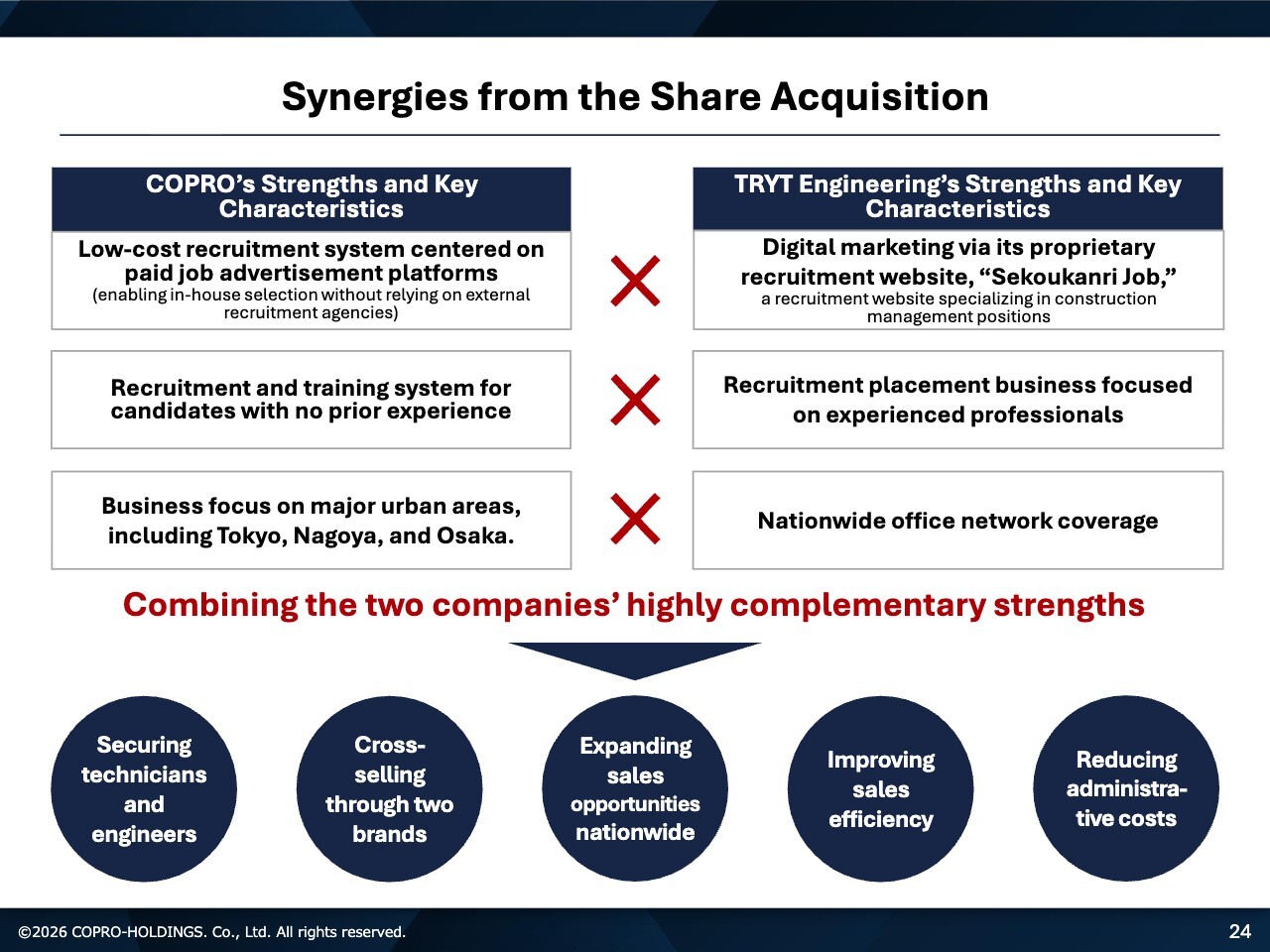

Synergies from the Share Acquisition

Let me explain the synergies we expect from our acquisition of TRYT Engineering. There are several areas of synergy, but today I will focus on the table shown on this slide. On the left, we outline COPRO’s strengths and key characteristics. On the right, we highlight TRYT Engineering’s strengths and key characteristics.

First, let me outline COPRO’s strengths and key characteristics. We believe our greatest strength is our ability to recruit at exceptionally low cost by leveraging paid job advertisement platforms centered on our proprietary recruitment website. We also differentiate ourselves by aggressively recruiting candidates with no prior experience and supporting them with a rigorous, fully developed training system.

We operate primarily in major urban areas, especially Tokyo, Nagoya, and Osaka. While we also maintain branches in regional cities, our strong market presence in Tokyo, Nagoya, and Osaka is a key competitive advantage.

Next, let me highlight TRYT Engineering’s strengths and key characteristics. TRYT Engineering’s key advantage is its powerful digital marketing via its proprietary recruitment website, “Sekoukanri Job.”

TRYT Engineering has a clear strength that we do not: recruiting experienced professionals. While we excel at recruiting inexperienced candidates, TRYT Engineering leverages its strong digital marketing capabilities to specialize in recruiting experienced professionals. Another major strength is its well-established recruitment placement business. In addition, TRYT Engineering operates a nationwide office network.

By combining the highly complementary strengths of both companies, we will drive the five initiatives outlined at the bottom of this slide. I will take the lead and drive execution to deliver the five initiatives outlined at the bottom of the slide.

Financial Statements Based on Simple Aggregation

Let me explain the financial statements based on simple aggregation. While we present these figures on a simple aggregated basis, we are currently conducting a detailed review of the numbers in preparation for full consolidation. There are two key points to highlight.

First, in FYE3/2027, business scale will expand significantly with the consolidation of TRYT Engineering, while operating profit will be temporarily constrained primarily by goodwill amortization and integration costs.

Second, from FYE3/2028 the transition to IFRS (International Financial Reporting Standards) is expected to significantly change the earnings structure from the previous year due to the non-amortization of goodwill and the absence of integration costs.

At the bottom of the slide, we present the financial statements of our group—COPRO—and TRYT Engineering, which is scheduled to join the group, based on figures for FYE9/2025. We used September as the reference point because due diligence began at that time, and the December year-end figures were not yet available. Accordingly, the figures shown on the right side of the slide represent a simple aggregation based on the September results.

On a simple aggregated basis, net sales totals ¥52,014 million and operating profit reaches ¥5,163 million, resulting in 9.9% of net sales. Non-GAAP operating profit stands at ¥5,820 million, resulting in 11.2% of net sales. Profit totals ¥3,370 million, and earnings per share (EPS) come to ¥88.11.

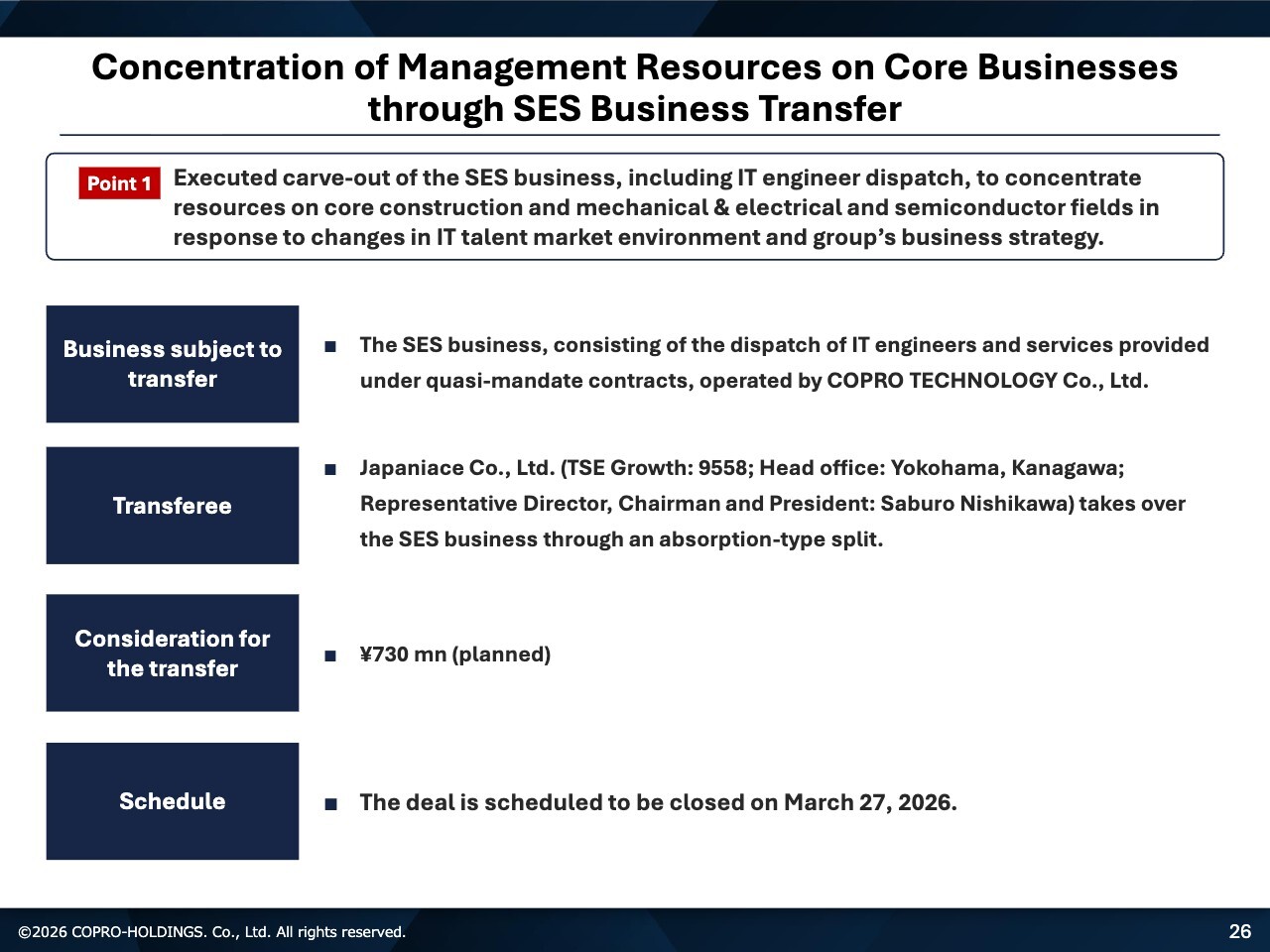

Concentration of Management Resources on Core Businesses through SES Business Transfer

Let me explain our concentration of management resources on core businesses through SES business transfer. We made a significant strategic decision in this regard and have formally disclosed it.

In response to changes in IT talent market environment and group’s business strategy, we decided to carve out the SES business, which primarily provides IT engineer dispatch. This decision allows us to concentrate resources on core construction field, and on the mechanical & electrical and semiconductor fields, which we are developing as our second earnings pillar.

The business subject to transfer is the SES business, consisting of the dispatch of IT engineers and services provided under quasi-mandate contracts, operated by our operating subsidiary, COPRO TECHNOLOGY Co., Ltd.

The transferee is Japaniace Co., Ltd., a company listed on the Tokyo Stock Exchange Growth Market. They will take over the SES business through an absorption-type split. The planned consideration for the transfer is ¥730 million. The deal is scheduled to be closed on March 27, 2026, and the process is currently underway.

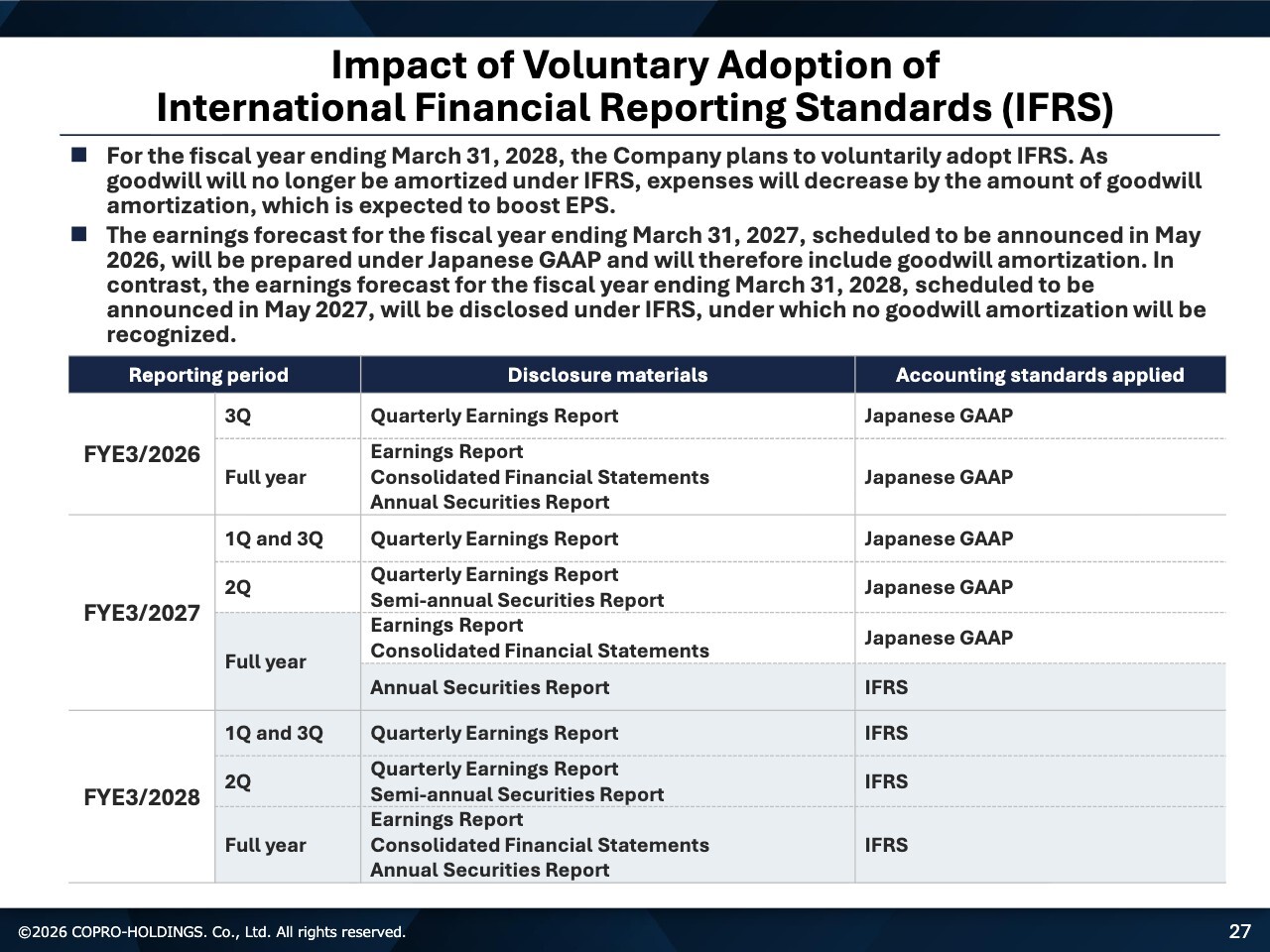

Impact of Voluntary Adoption of International Financial Reporting Standards (IFRS)

Let me address the impact of our voluntary adoption of IFRS. The slide outlines two key points and includes a timeline detailing how we plan to disclose financial results under our fiscal year. Please refer to it for further details.

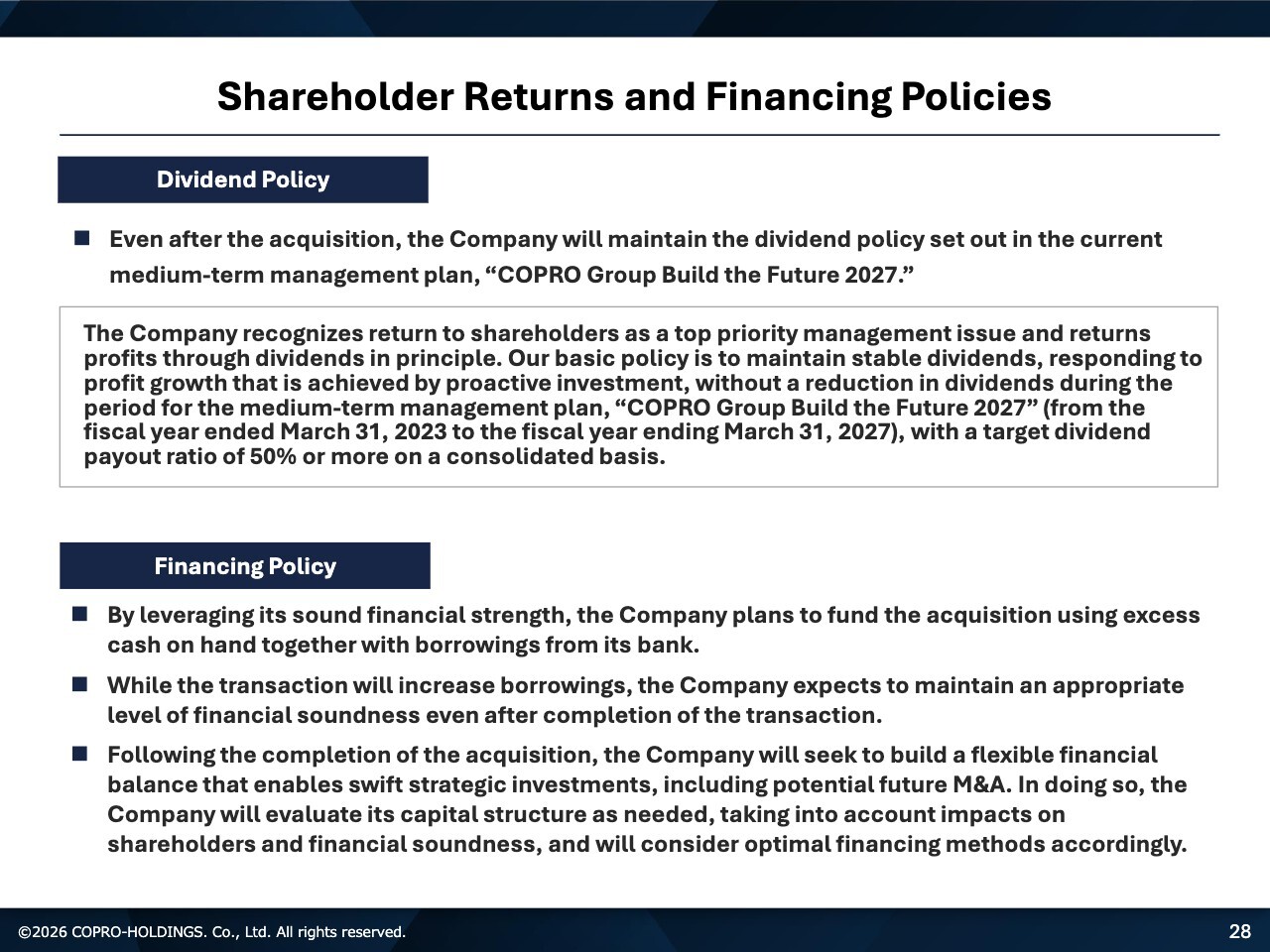

Shareholder Returns and Financing Policies

Let me explain our approach to shareholder returns and our financing policy following the acquisition of TRYT Engineering. First, on our dividend policy, even after the acquisition, we will maintain the dividend policy set out in the current medium-term management plan, “COPRO Group Build the Future 2027.”

Our dividend policy is as follows. We recognize return to shareholders as a top priority management issue and return profits through dividends in principle. We will not reduce dividends during the period for the medium-term management plan, “COPRO Group Build the Future 2027.”

Our basic policy is to maintain stable dividends, responding to profit growth that is achieved by proactive investment with a target dividend payout ratio of 50% or more on a consolidated basis. We intend to maintain this dividend policy even after this significant investment.

Let me explain our financing policy. By leveraging our sound financial strength, we plan to fund the acquisition using excess cash on hand together with borrowings from our partner bank. While the transaction will increase borrowings, we expect to maintain an appropriate level of financial soundness even after completion of the transaction.

Following the completion of the acquisition, we will seek to build a flexible financial balance that enables swift strategic investments, including potential future M&A. In doing so, we will evaluate our capital structure as needed, taking into account impacts on shareholders and financial soundness, and will consider optimal financing methods accordingly.

Summary of the Full Year Earnings Forecast for FYE3/2026

In Section 5, I will outline our earnings and dividend forecasts for FYE3/2026. The slide presents the summary of the full year earnings forecast. Let me begin by highlighting the key points.

Acquisition-related expenses (e.g., advisory fees) will be incurred in connection with the share acquisition of TRYT Engineering scheduled to be closed on March 1, 2026. The timing of consolidation and the impact on current-year results are currently under review. If any matters requiring disclosure arise, we will promptly make an announcement.

Next, here is the summary of the full year earnings forecast for FYE3/2026. We expect the number of group technical employees to increase by 29% YoY to 6,271, consolidated sales to increase by 26.6% YoY to ¥38,000 million, and operating profit to increase by 37.5% YoY to ¥3,800 million, representing 10.0% of net sales.

Non-GAAP operating profit is projected to increase by 32.9% YoY to ¥4,425 million, representing 11.6% of net sales, ordinary profit by 36.5% YoY to ¥3,800 million, representing 10.0% of net sales, and profit by 35.7% YoY to ¥2,470 million, representing 6.5% of net sales.

We expect to achieve record highs across all areas.

FYE3/2026 Consolidated Earnings Forecast

This slide presents the statement of profit or loss (P/L) for the FYE3/2026 consolidated earnings forecast. Please feel free to review it at your convenience.

FYE3/2026 KPIs by Business (Forecast)

Here are the KPI forecasts by business for FYE3/2026. We encourage you to review the number of recruits, the number of resignations, the number of technical employees (period end), retention rate, operating ratio (including trainees).

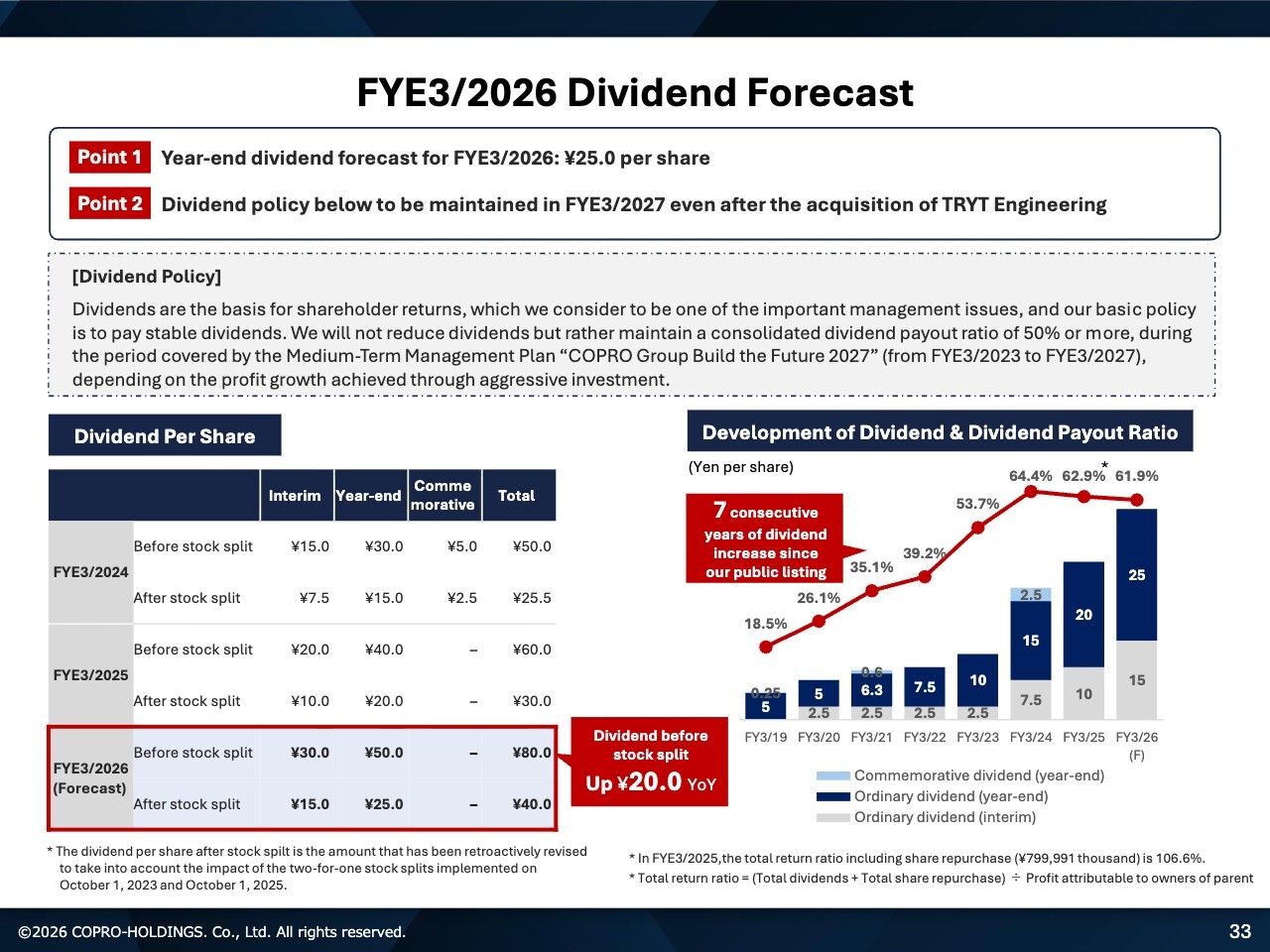

FYE3/2026 Dividend Forecast

Finally, let me outline our dividend forecast for FYE3/2026. As mentioned earlier, I will focus on the key points. First, we forecast a year-end dividend of ¥25 per share for FYE3/2026.

Second, even after the acquisition of TRYT Engineering, we will maintain the same dividend policy in FYE3/2027 as outlined earlier. Our dividend policy is as previously stated.

On the left side of the slide, we show the dividend per share for FYE3/2026. On the right, a graph illustrates the development of dividends and payout ratio since our listing. Please review the details at your convenience.

Message from CEO

The January 15 announcement regarding the acquisition of TRYT and TRYT Engineering, along with the carve-out of our IT business, represents a major strategic decision and a significant investment.

As mentioned earlier, our group has many capable leaders who can serve as president. However, given the scale of this ¥30,000 million investment, I have determined that it is necessary for me to concurrently serve as CEO of the operating subsidiary and exercise strong leadership to ensure a successful PMI, thereby maximizing synergies across the COPRO Group and enhancing the value of this company. For this reason, I concluded that I must personally serve concurrently as the CEO.

I approach this major strategic decision with full determination and a strong commitment to growing the COPRO Group into an even more valuable company. I sincerely ask for your continued support and encouragement as we move forward.

This concludes our financial highlights for 3Q FYE3/2026. Thank you for your attention.