FY2025 Highlights (1)

Takayuki Ueda (hereinafter: “Ueda”): I am Takayuki Ueda, Representative Director, President & CEO of INPEX CORPORATION. Thank you for taking time out of your busy schedule to join us today. Also, thank you to all of you who are participating online. Today, I will explain our financial results and outlook for this year.

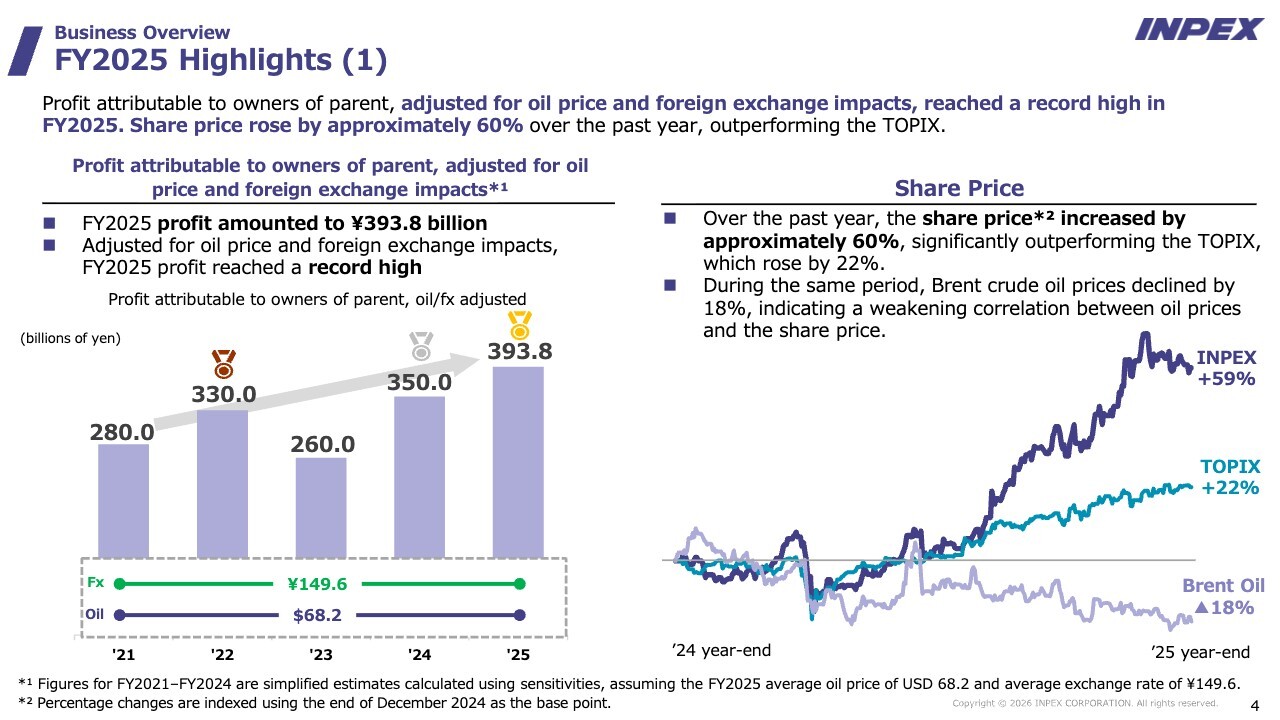

First, I would like to discuss the financial results for FY2025. Profit was ¥393.8 billion.

In absolute terms, the current ¥393.8 billion is the third highest level ever recorded. However, a simplified calculation assuming oil prices of about $68, and an exchange rate of about ¥149, the averages for FY2025, shows that the result for FY2025 is the best figure ever.

There are a variety of external circumstances, and while I do not have a particular opinion regarding these numbers themselves, I believe that our earning power is steadily improving.

Thanks to this, the share price has recently risen significantly. We are often asked what we think of our share price, and we believe that the rise in share price is due to investors deepening their understanding of our company, for which we are sincerely grateful.

The P/B ratio has also recently been close to 1. However, when compared with various Japanese companies, for example, there are 86 companies with a market capitalization of over ¥3 trillion on the TSE Prime Market, and the average P/B ratio of these companies is about 3.8.

In the global peer group, the average P/B ratio of American and European IOCs, including Exxon and Shell, is about 2.1. On the other hand, the average P/B ratios of Japanese oil and natural gas companies are generally in the range 1.3 to 1.4.

In light of this situation, we are grateful for the significant increase in the share price, and we are also considering the potential for further growth.

When you look at our financial position, growth strategy, and shareholder returns, we are confident that we are not inferior to other companies. In this sense, although the current share price level has risen, it is certainly not high, and in fact we think that it is still undervalued compared with other companies.

FY2025 Highlights (2)

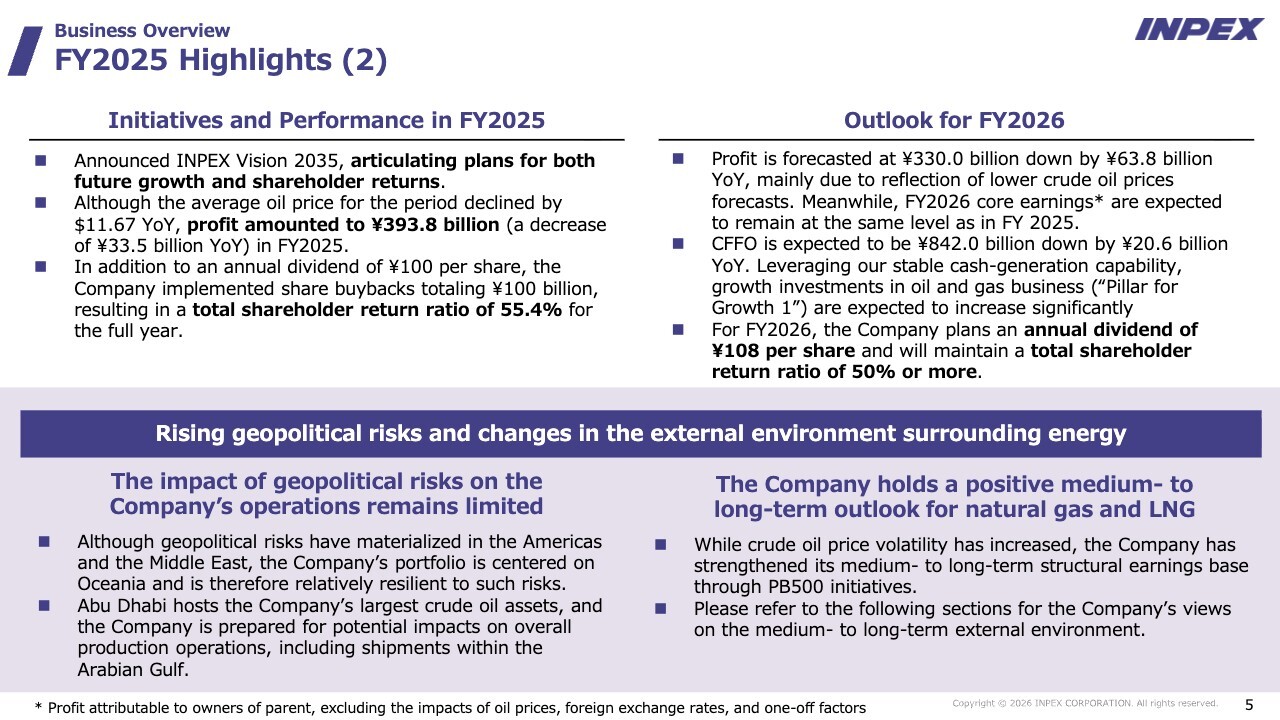

These are the highlights for FY2025. The annual dividend is ¥100 per share, with a total payout ratio of 55.4%.

In the forecast for FY2026, we have assumed slightly conservative oil prices and exchange rates, and expect a profit of about ¥330 billion. I know some of you may be thinking, “This is not enough,” but I will explain this later.

The annual dividend will be increased by ¥8 to ¥108 per share. We maintain our commitment to a total payout ratio of at least 50%.

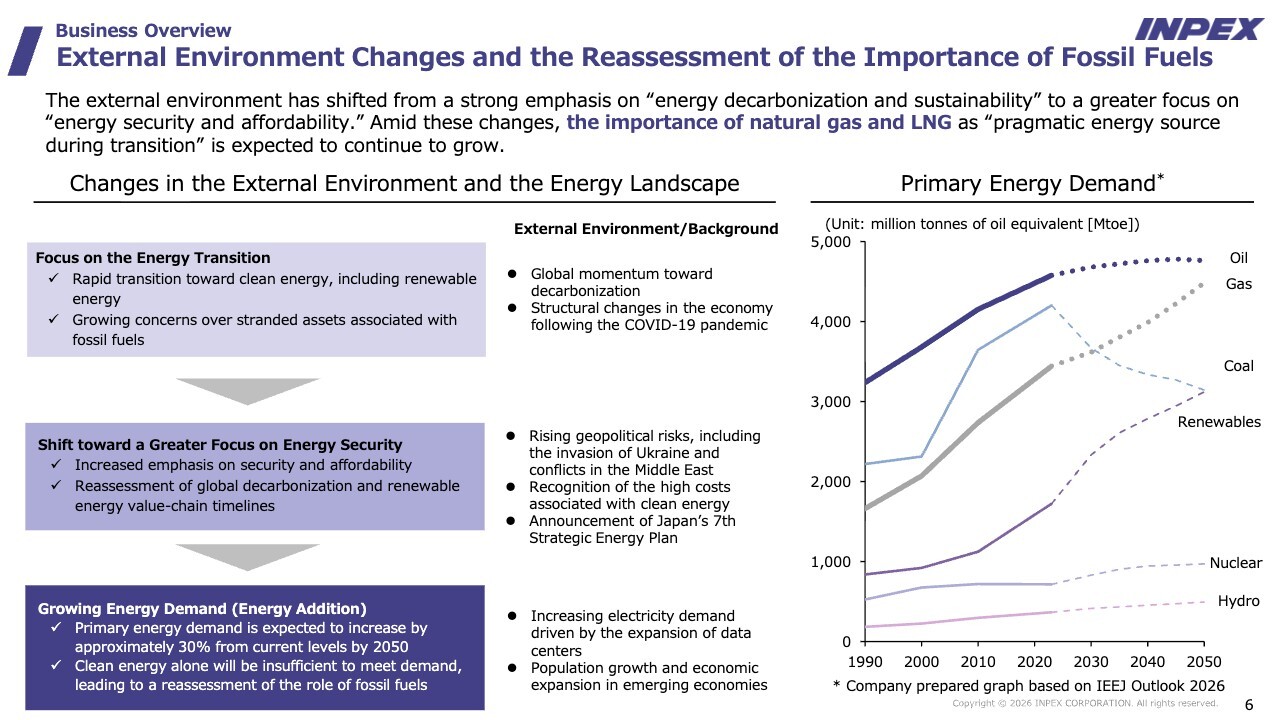

External Environment Changes and the Reassessment of the Importance of Fossil Fuels

Before I get into specific business results, I would like to explain the recent external environment. Here is a single sheet showing changes in the external environment.

The external environment of our company, especially oil and gas, has changed dramatically since before the war in Ukraine. Recently, we have explained these changes divided into three phases.

Prior to the Ukrainian war, many companies placed great emphasis on energy transitions. Behind this was the idea that “we should rapidly shift to clean energy, including renewable energy,” and the accompanying concern that fossil fuels would become stranded assets. At that time, when I met with investors, they would say, “How long is INPEX going to be in the oil and gas business?” We have heard the comment, “What if it becomes a stranded asset?”

In this context, we said, “even so, demand for oil and gas will not disappear anytime soon.” We conveyed the idea that, “we will take on the challenge of renewable energy and other clean energies, but the foundation of our management is the solid work we have done in the oil and gas business.” This was characteristic of the external environment at that time.

Later, since the beginning of the war in Ukraine, many companies have moved in the direction that energy security and stable supply are very important.

Security, affordability, and the right amount at the right price were voiced, but “it’s not all about decarbonization, we need to balance that with energy security,” has been a major global turning point since the start of the war in Ukraine.

At present “energy addition” is a term that is receiving a lot of attention. This term indicates that demand for primary energy is expected to increase by about 30% from the present level by 2050.

In particular, demand for electricity is on the rise, and power demand is expected to increase globally due to AI and data centers, etc. This is an ongoing phenomenon on an international scale.

Therefore, the use of clean energy, especially renewable energy, is important, but it is not sufficient to cover the demand by itself. This trend towards “how do we respond to this energy addition on the supply side?” represents a major shift in the global energy sector over the past year or two.

The need to further advance energy addition while balancing energy transitions and energy security is emphasized. The world’s perception of energy has changed greatly over the past few years against the backdrop of the war in Ukraine.

Regarding the recent outlook, the graph on the right side of the slide shows the primary energy demand. We use data from the Institute of Energy Economics, Japan (IEEJ), which is very close to our view.

Regarding how primary energy demand will change toward 2050, we assume that oil may peak at some point, but will remain flat after that.

Demand for natural gas is expected to grow at a roughly constant pace from 2040 to 2050. On the other hand, demand for coal is expected to decrease significantly. The share of renewable energy is expected to increase.

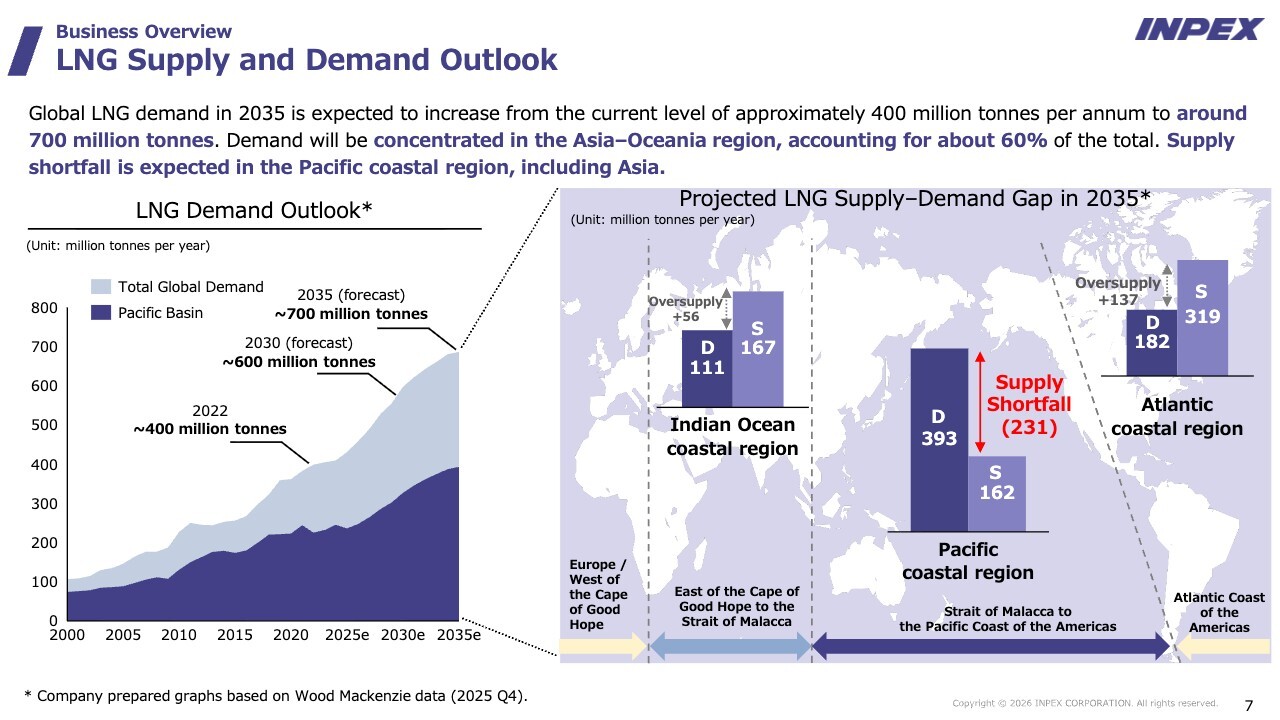

LNG Supply and Demand Outlook

Here I will discuss our main product, natural gas. Focusing on liquefied natural gas (LNG) in particular, global annual demand in 2022 is estimated to be approximately 400 million tons.

Looking ahead, we expect to see a significant increase from the current 400 million tons to approximately 600 million tons by 2030 and 700 million tons by 2035.

From a supply and demand perspective, it is easy to see in the figure on the right side of the slide in which areas demand is concentrated. In Asia, supply is inadequate to meet overwhelming demand. The slide contents show an image of the 2035 cross-section, but the trend is clear.

There is some demand on the Atlantic coasts of the United States and Europe, as well as on the Indian Ocean coasts, including the Middle East, but supply is expected to exceed this demand. In other words, when looking at the global LNG balance, the region with the greatest supply shortfall will be Asia.

It is considered that LNG demand will continue to grow in the long term through 2040 and even into 2050. A particular challenge in this context is how to meet Asian energy demand. I would like to emphasize that the supply of natural gas to Asia is a major issue in the energy industry, and that a strategy based on this is the main focus of our company.

Business Activities - Oil & Gas Business -

So far, I have discussed general matters, but now I will explain what happened in 2025.

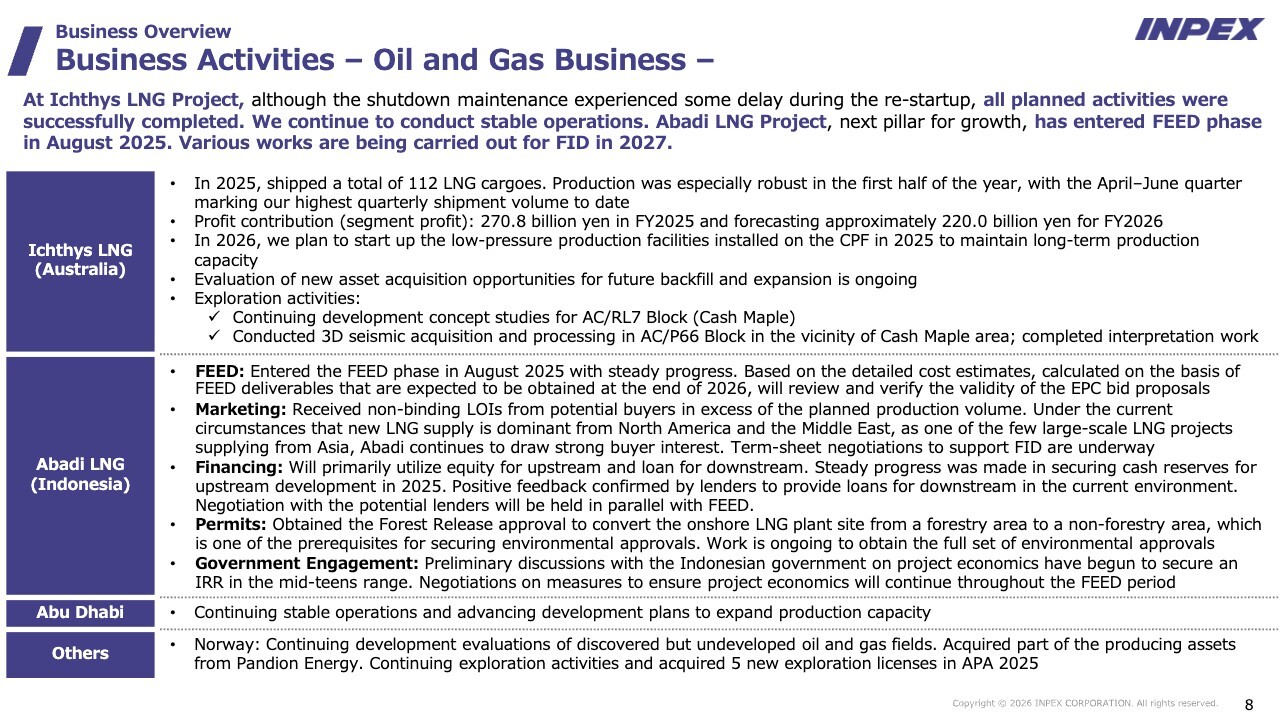

For the Ichthys LNG Expansion Project (hereinafter referred to as “Ichthys”), 112 LNG cargoes were shipped. There was planned shutdown maintenance in FY2025. Although there was a problem with its start-up being somewhat later than planned, overall, 112 cargoes were very close to the original plan, and the profit contribution was ¥270.8 billion.

For FY2026, the low-pressure production facility is scheduled to begin operation. As production increases, the more resources are extracted from the underground, thus reducing subsurface pressure. Therefore, in order to maintain stable production in the long term, even when underground pressure drops, work to install a low-pressure booster compressor module of approximately 5,000 tons at the CPF, Ichthys’ offshore production facility, was undertaken in 2025, and this has progressed very well.

Although there is no planned shutdown maintenance in FY2026, there is some work to be done, including the commissioning of this booster compressor module. Production will not fully recover in 2026 due to the need to shut down some equipment during this process. Although a significant recovery is not expected, the number of cargoes shipped is expected to increase from 2025, and the number of LNG cargoes shipped is expected to be about 10 cargoes per month.

In addition, various efforts are still underway regarding the acquisition of new assets for future backfill and third train expansion. At this point, we have not yet reached the stage where we can share this information with you, but we hope to do so at some point in the future.

The “Abadi LNG Project” (hereinafter referred to as “Abadi”) made significant progress last year. As we have informed you, the project moved to the FEED (front end engineering design) phase in August 2025, and that work is currently progressing smoothly.

We expect to have some cost estimates by about the end of 2026. We have already begun marketing activities and financing work. We have had discussions with many potential customers regarding marketing.

Returning to our earlier discussion, LNG produced in Asia is currently very valuable. The United States and Qatar supply a lot of LNG, but the volume of LNG produced in Asia at present is not that large.

Asian-produced LNG is very popular due to the absence of geopolitical risks such as the Strait of Hormuz risk and the short transport distances by ship to Asia, the largest demand area.

At this time, we have not reached a final binding agreement, but we are developing marketing activities that are very well received. The company plans to negotiate specific terms and conditions for a long-term contract in order to achieve a Final Investment Decision (FID).

Financing for natural gas is now viewed very positively, reflecting the recent global situation, unlike in the past. We believe that this is also proceeding smoothly at this time. Regarding the permitting procedures, we are confident that we will soon be able to obtain an Environmental Impact Assessment (AMDAL) permit.

Although there are various issues regarding Abadi, as described above, the work is currently progressing smoothly.

With regard to the Abu Dhabi Offshore and Onshore Oil Field (hereinafter referred to as “Abu Dhabi”), unfortunately, the UAE President’s visit to Japan as a state guest did not materialize, and we missed the opportunity to directly communicate what we had prepared. However, we are taking various steps to expand our production capacity in Abu Dhabi.

Abu Dhabi as a country has plans to expand its production capacity from 4 million to 5 million barrels per day. The Company intends to invest aggressively in line with this policy.

In particular, we plan to make a major investment in FY2026. The biggest factor is the investment in Abu Dhabi to increase production capacity. Through these efforts, we will increase production and expand profits.

Various other activities are also underway in Norway, Indonesia, Malaysia, and other countries.

Business Activities - Lower-carbon solutions, Energy and Resources fields -

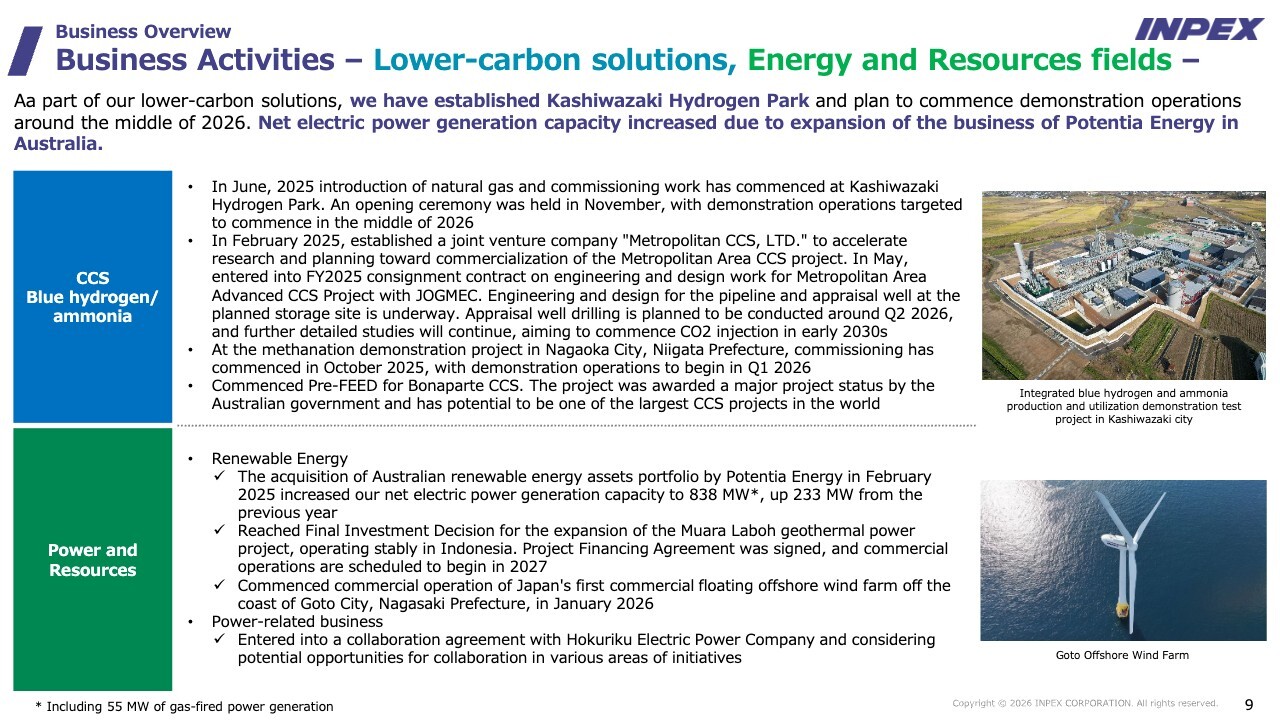

I will now discuss the clean energy area. In November 2025, we held an opening ceremony for the Blue Hydrogen demonstration project in Kashiwazaki, Niigata Prefecture.

In this project, we will produce blue hydrogen from domestic natural gas produced in Niigata Prefecture. CO2 emitted in the production process is stored underground using CCS technology at the aging Higashi-Kashiwazaki gas field. Full-scale operation is expected to begin soon.

With regard to methanation, we are constructing an e-methane facility in Nagaoka City, Niigata Prefecture, in cooperation with Osaka Gas. Commissioning has begun at this plant.

While the renewable energy sector in Japan as a whole continues to face difficult conditions, we have been pursuing renewable energy investments in Australia through Potentia Energy, a 50/50 joint venture with Enel from Europe.

Currently, our net electric power generation capacity has reached 838 megawatts worldwide. We will continue to promote this initiative.

In addition, a Final Investment Decision (FID) was made for the expansion of the Muara Laboh geothermal power plant in Indonesia.

Also, in January 2026, Japan’s first floating offshore farm began commercial operation off the coast of Goto, Nagasaki Prefecture. Toda Corporation is playing a central role in this project, in which we are also participating.

In addition, we concluded a “Collaboration Agreement” with Hokuriku Electric Power Company last year, and discussions are underway to materialize this agreement.

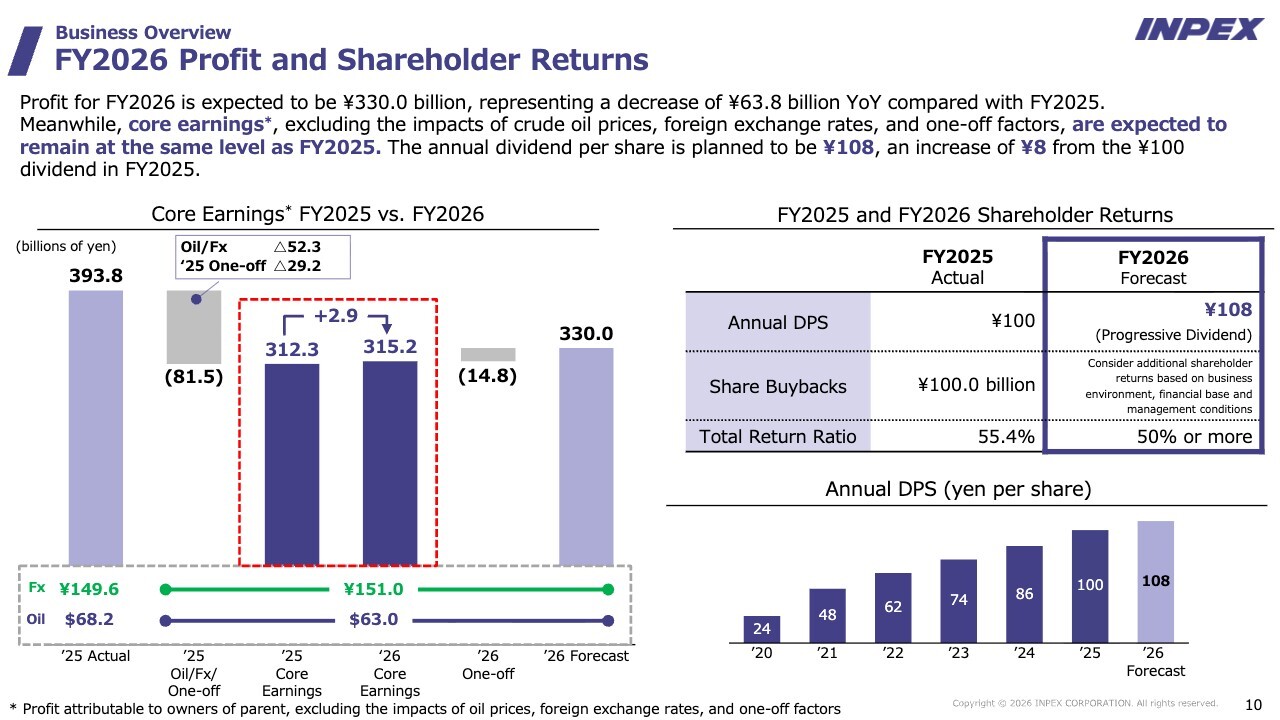

FY2026 Profit and Shareholder Returns

Here I will discuss the forecasts for FY2026. Profit is projected to be ¥330.0 billion, assuming a Brent oil price of $63 and an exchange rate of ¥151.

The current Brent oil price is slightly below $70. We have set a conservative figure of $63, taking into account that many consultants are of the view that there will be a slight oversupply in 2026. I also consider myself to be somewhat conservative. The exchange rate is very difficult to predict, but we have assumed ¥151.

Based on these assumptions, annual profit for FY2026 would be ¥330.0 billion. However, if one-off revenues are excluded, core earnings would be ¥315.2 billion. Also, the FY2025 figure of ¥393.8 billion, after adjusting for an exchange rate of ¥151 and an oil price of $63 and excluding one-off revenues (one-offs), is also almost the same, at ¥312.3 billion.

Some may say that our forecast of ¥330.0 billion is a small amount and is insufficient, but we believe that even under these low oil price conditions it is possible to generate solid earnings.

The dividend forecast was set at ¥108 per share, an increase of ¥8 per share. There has been some debate within the company as to whether it is necessary to raise the dividend when revenues fall to ¥330.0 billion, but I believe the following.

Our growth potential is still very strong, our financial position is solid, and we have good cash flow. In the long term, we have the Abadi LNG project in the pipeline, but we are investing very heavily this year.

The overall investment for FY2025 was approximately ¥400 billion, and for FY2026, we plan to double that amount to approximately ¥850 billion.

Part of this investment, which was planned for 2025, will be made in 2026. These investments are intended not only for the purpose of preparing for the long-term Abadi LNG project, but also for immediate growth through asset acquisitions and other initiatives in the short and medium term.

These investments are very solid, and we are confident that they will enable us to grow. Our approach to giving back is based on the traditional statement, “We grow, and we will give back the fruits of our growth.”

Our forecast for 2026 is for a profit of ¥330.0 billion, partly due to the effect of low oil prices, but our medium- to long-term growth policy and direction have not changed at all. We are confident that cash flow and profits will increase sufficiently over the medium to long term, although it depends on the external environment.

Because of this confidence, we have set a dividend of ¥108 per share based on the policy that “we will grow properly and fully repay the fruits of our growth,” even though we have given the market a forecast of ¥330.0 billion for the year 2026.

That completes my explanation. Best regards.

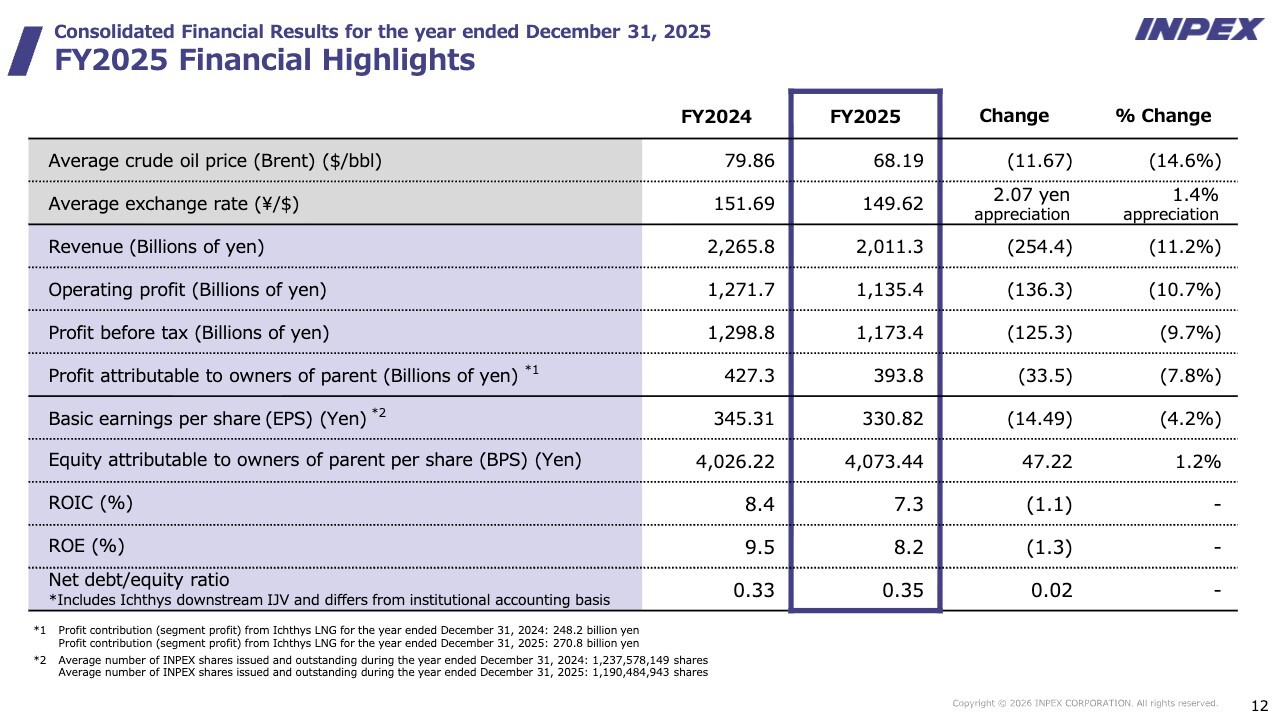

FY2025 Financial Highlights

Daisuke Yamada (hereinafter: “Yamada”): My name is Daisuke Yamada, Director, Senior Managing Executive Officer, Senior Vice President, Finance & Accounting. Today I will explain our financial results for the fiscal year ending December 31, 2025.

As explained earlier by the Representative Director, President & CEO, profit attributable to owners of parent company for the year 2025 is ¥393.8 billion, a decrease in revenue and profit compared with 2024. The main factors were lower oil prices and the planned shutdown maintenance of the Ichthys LNG expansion project, which had a significant impact. However, as you can see, balance sheet control through “Profit Booster 500” and a significant return of income tax expenses helped us achieve the result of ¥393.8 billion.

We believe that the fact that we generated profits of around ¥400 billion when oil prices were in the $60 range is evidence of our increasing intrinsic profitability. Adjusted for oil prices and exchange rates, this result is the highest in our history, and we also view this positively.

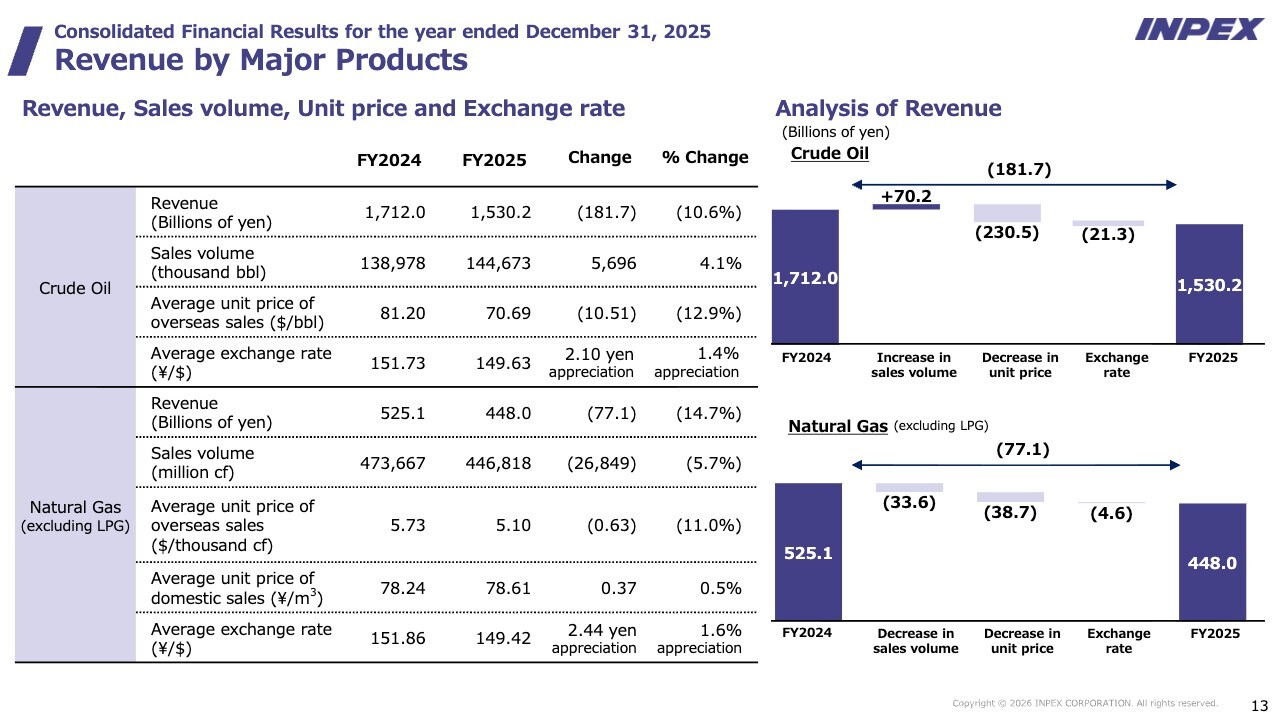

Revenue by Major Products

The following is an analysis of our revenue. The top row of the slide shows crude oil and the bottom row shows natural gas.

Crude oil sales volume increased, but unit selling prices fell due to a significant drop in Brent oil prices, resulting in a decrease in revenue to ¥1,530.2 billion.

Natural gas sales volume declined. This is due to the planned shutdown maintenance of Ichthys as explained earlier. Unit prices also fell in line with the price of Brent crude oil, resulting in a decrease in revenue to ¥448.0 billion.

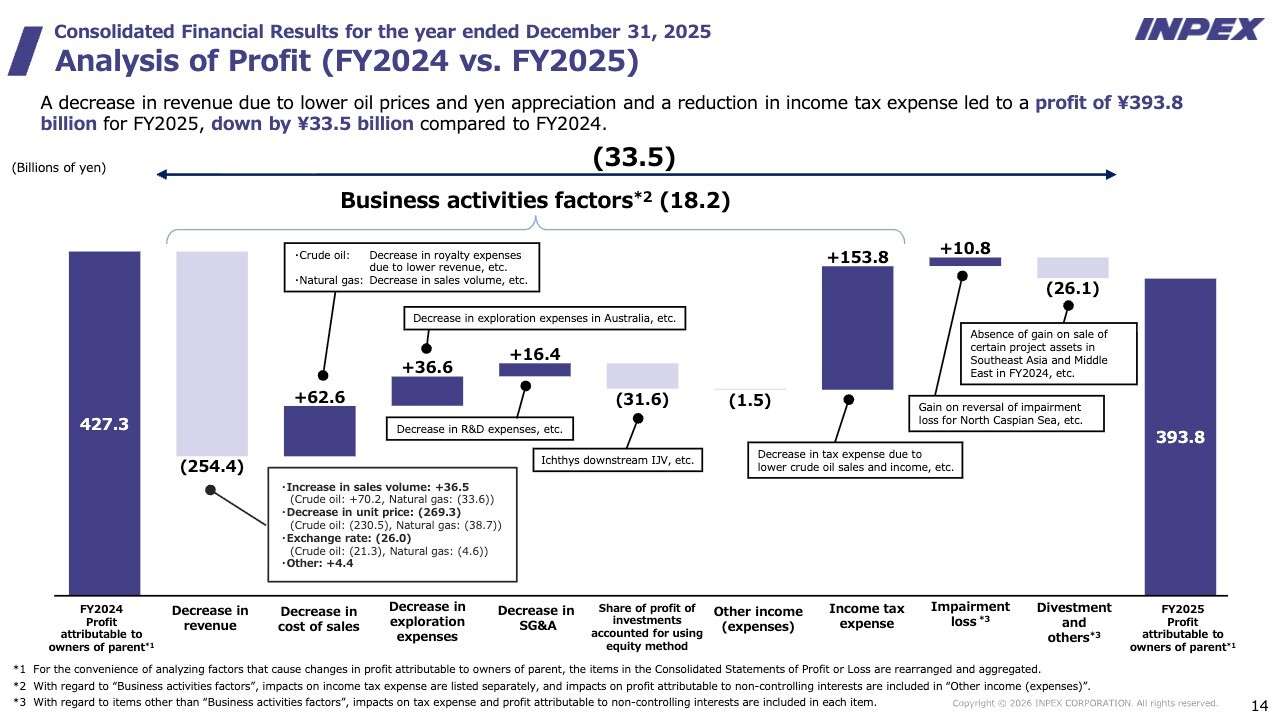

Analysis of Profit (FY2024 vs. FY2025)

Profit for FY2025 was ¥393.8 billion, down ¥33.5 billion from ¥427.3 billion in FY2024.

The main reason for the decline was lower revenues, which were affected by the lower oil prices. On the other hand, exploration expenses, which dropped sharply last year due to exploration failures in Australia, recovered this year.

Also, for divestments on the right side of the slide, divestment earnings in Southeast Asia fell off in 2024. The positive ¥36.6 billion decrease in exploration expenses and the negative ¥26.1 billion decrease in divestment and others are all impacts in 2024.

Otherwise, the impact is in 2025. In addition to the decline in revenues, Ichthys downstream revenues, which are included in equity in earnings, also fell in tandem with oil prices. On the other hand, income tax expenses decreased by ¥153.8 billion as a positive factor. This was largely the result of a decrease in taxation in high-tax countries.

Income tax expenses and other profit and loss items include “Profit Booster 500.” This is the effect of TA recycling and investment incentives in Europe and the Middle East, which amounted to about ¥80 billion in 2025, and the difference between before and after the disclosure of the “Profit Booster 500” was ¥65 billion.

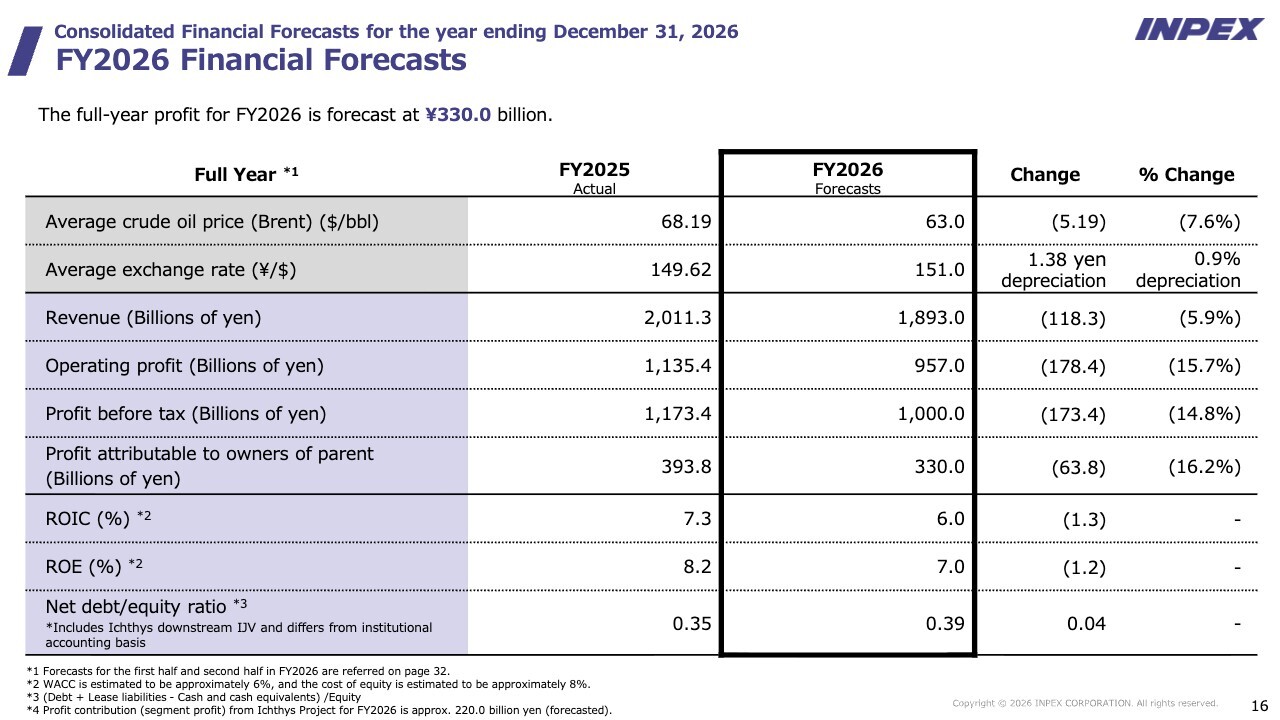

FY2026 Financial Forecasts

The forecast for FY2026 is ¥330.0 billion. This assumes a crude oil price of $63.0 and an exchange rate of ¥151, a level that “may be somewhat inadequate.”

In fact, the profit forecast for 2025 was set at ¥330.0 billion at the beginning of the period. The assumption at the time was a crude oil price of $75. As a result, the crude oil price was $68, $7 lower than expected, but the actual result was ¥393.8 billion.

In 2025, although the impact of oil prices and foreign exchange rates reduced our initial forecast by about ¥40 billion, we have added ¥100 billion to that amount to achieve ¥393.8 billion.

It is unclear whether the same progress will be made in 2026, but the intrinsic profitability of the company is steadily improving. In addition, the large fixed assets on our balance sheet contain unrealized gains and losses for financial and tax purposes.

Events such as “now we can do this, now we can do that” and “Profit Booster 500” cannot be factored in at the initial forecast stage, but will be monetized as the fiscal year progresses. Please understand that this ¥330.0 billion is an approximate starting point figure.

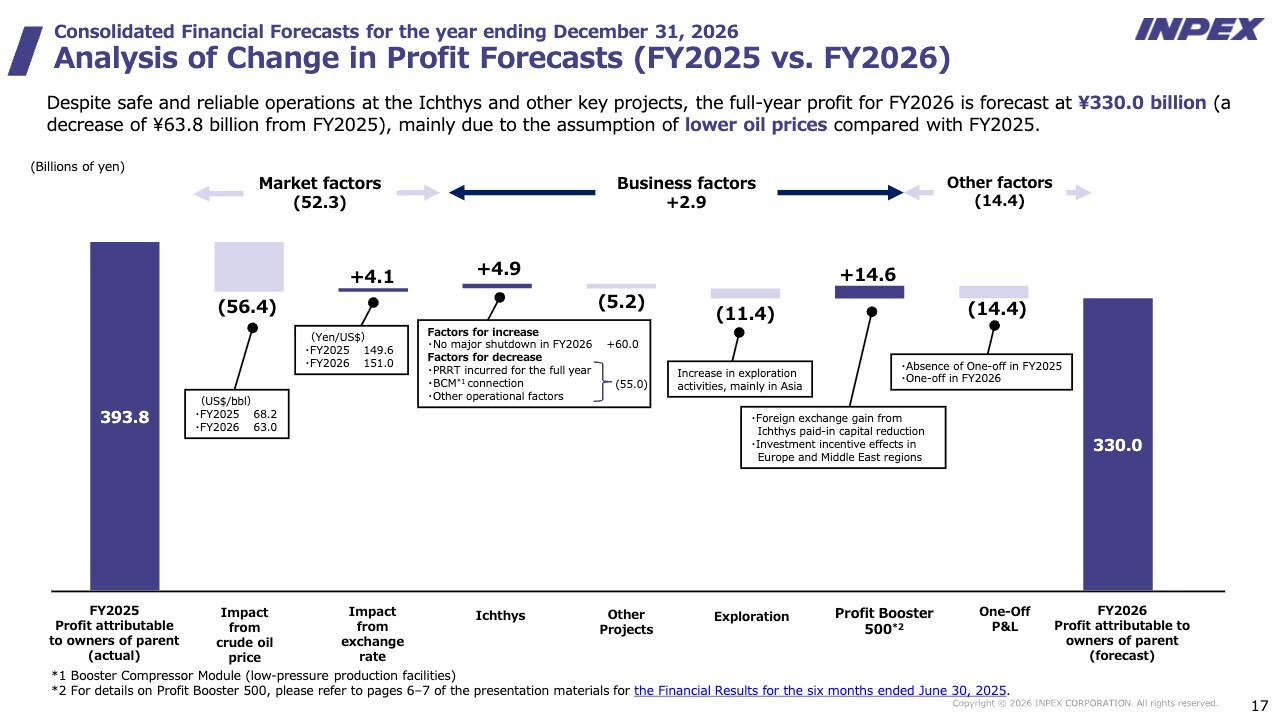

Analysis of Change in Profit Forecasts (FY2025 vs. FY2026)

This is an analysis of the factors contributing to the increase or decrease in profit attributable to owners of the parent company. The main factor, and the most significant influence, is the crude oil price, but note the Ichthys section in the center.

The increase was ¥4.9 billion, but there are significant fluctuations in the breakdown. In 2025, the planned shutdown maintenance caused a decrease in profit of about ¥60 billion, but in 2026, its recovery will lead to a positive figure of about ¥60 billion.

On the other hand, in 2026, the utilization rate will be slightly lower due to the work on commissioning the low-pressure production facility called the “Booster Compressor Module.”

In addition, the Petroleum Resource Rent Tax (PRRT) was only imposed for a half year in 2025, but will be imposed for the full year in 2026, which is the factor for decrease of approximately ¥16 billion. After subtracting these factors, the result was a positive ¥4.9 billion increase in profit.

Regarding “Profit Booster 500,” we expect the actual amount of TA recycling and investment incentive effects to total about ¥95 billion in 2026. Total profit is projected to be ¥330.0 billion. This may sound repetitive, but please understand that this is an approximate starting point figure. We hope you can rely on us.

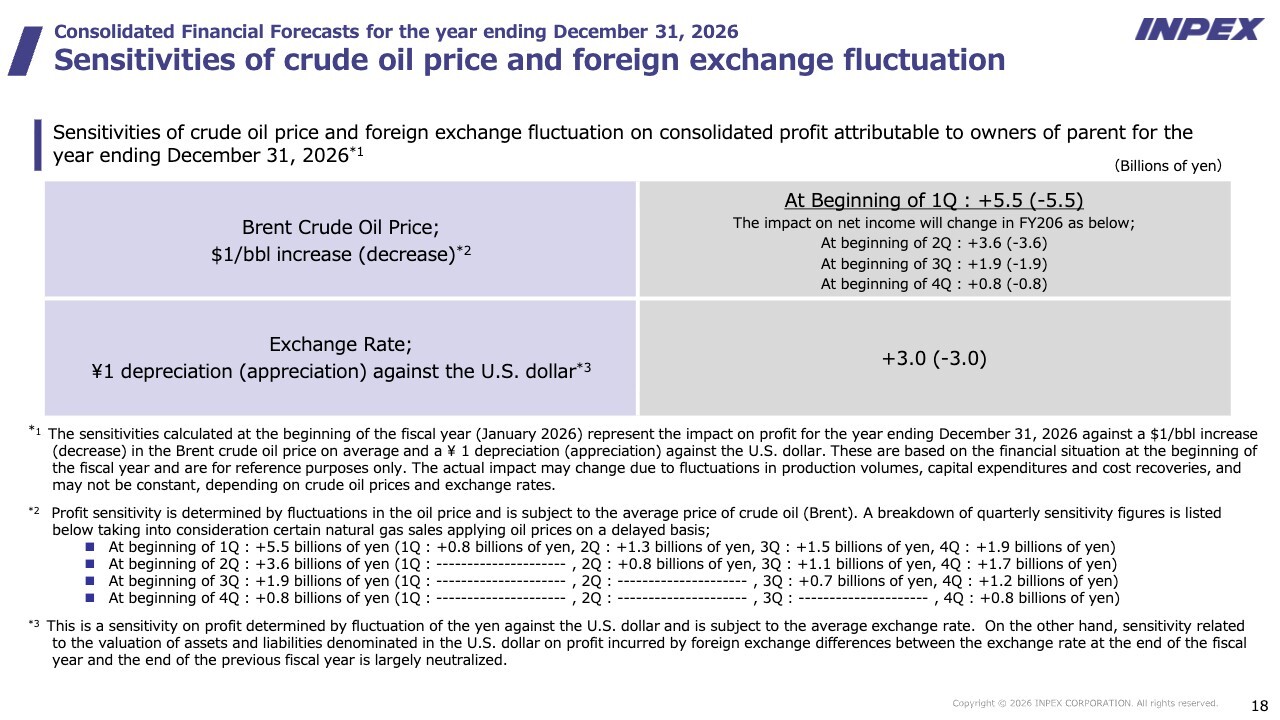

Sensitivities of crude oil price and foreign exchange fluctuation

These are the exchange rate sensitivities that we have traditionally shown. A one-dollar change in the oil price would have an impact of ¥5.5 billion, and a one yen change in the exchange rate would have an impact of about ¥3.0 billion. Please refer to this page for your reference.

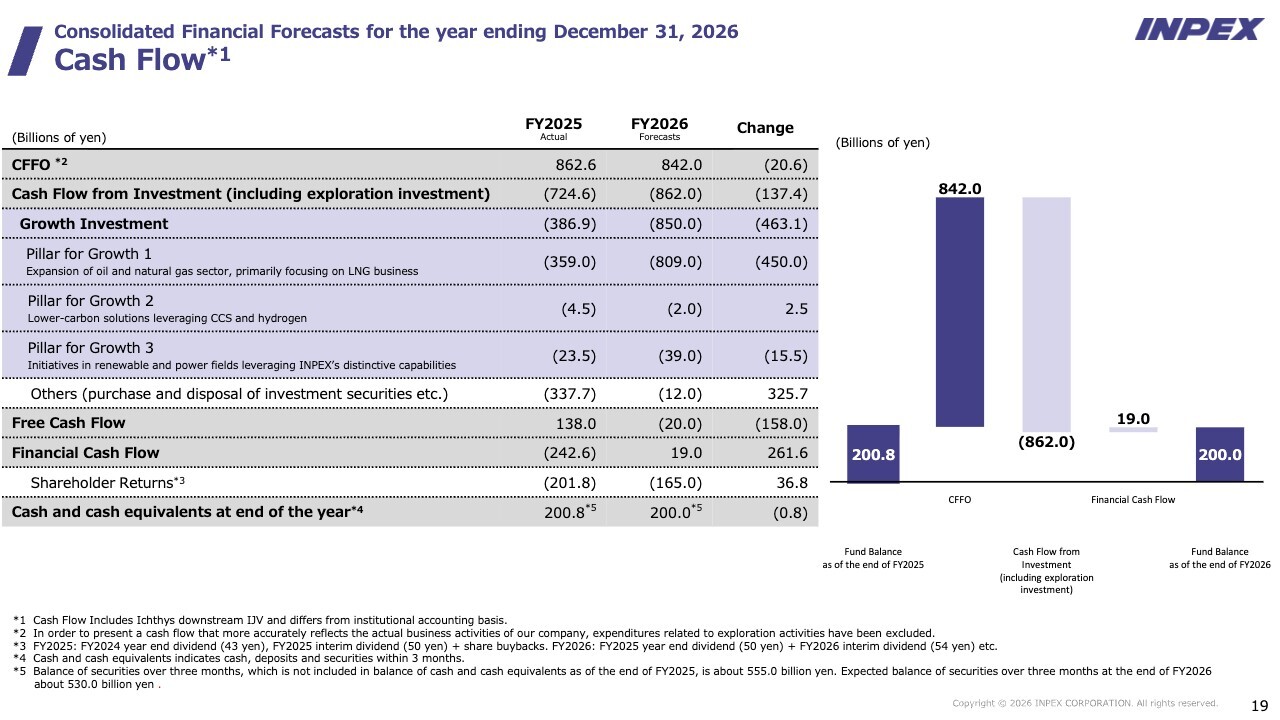

Cash Flow

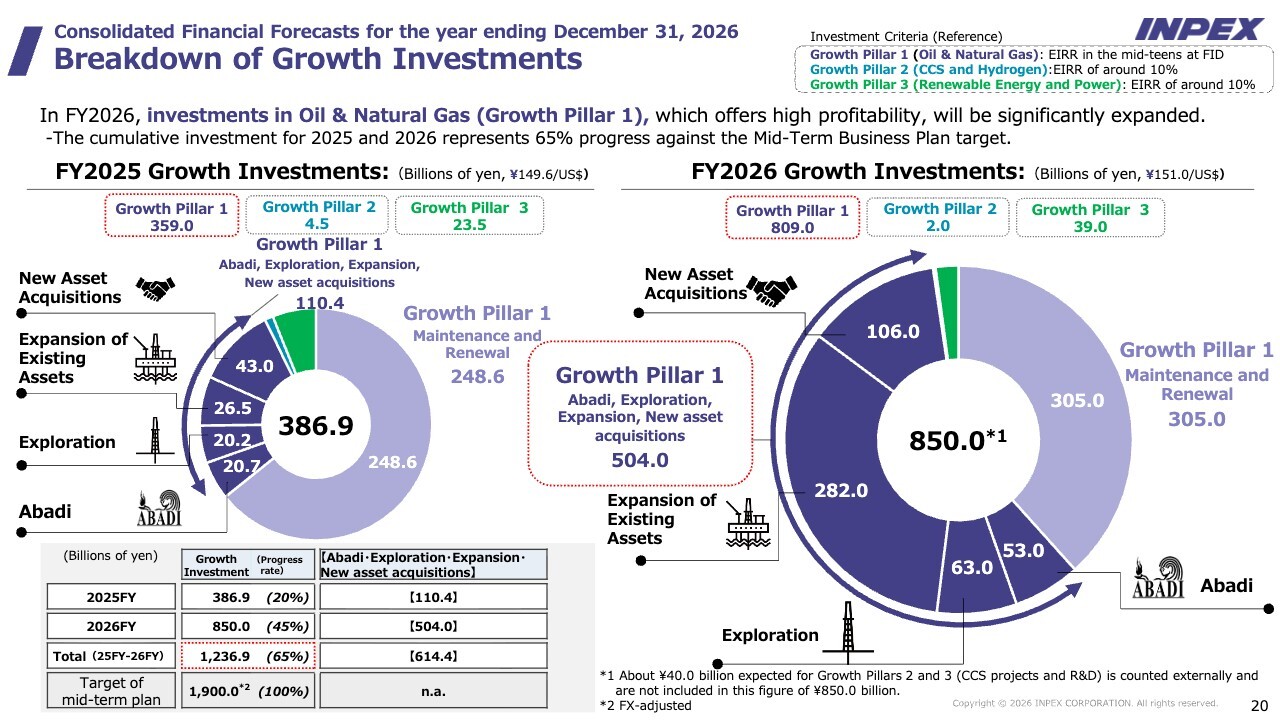

Here I will discuss investments. The cash flow from operations is ¥842.0 billion, but a large investment of ¥850.0 billion is planned for 2026 as growth investment. The increase will be about ¥460 billion in 2026, relative to ¥386.9 billion in 2025.

This major investment will be focused on the growth pillar 1, the oil & gas business. You have all asked us how we will earn revenue until the Abadi LNG project, and we believe that this year’s investments will pay off in the late 2020s and early 2030s. This year we plan to make a stake everything investment.

Breakdown of Growth Investments

See the table at the bottom left of the slide. The ¥850.0 billion investment for 2026 may seem very large, but this scale is due to the ¥1.9 trillion investment planned in the Mid-term Business Plan. We believe that we are making good progress, with a total investment of ¥386.9 billion in 2025 and when combined with 2026, a two-year cumulative progress rate of 65%.

See the graph on the right side of the slide for a breakdown of investments. The ¥850.0 billion is shown in blue with white text. It includes investment in the Abadi LNG project, and other exploration and expansion of existing projects. Investment in Abu Dhabi production capacity increase is also factored in here. We cannot give specific examples of new acquisitions yet, but we intend to broadly pursue the acquisition of interests, particularly in core regions such as Australia, Indonesia, Asia, Norway, and Japan.

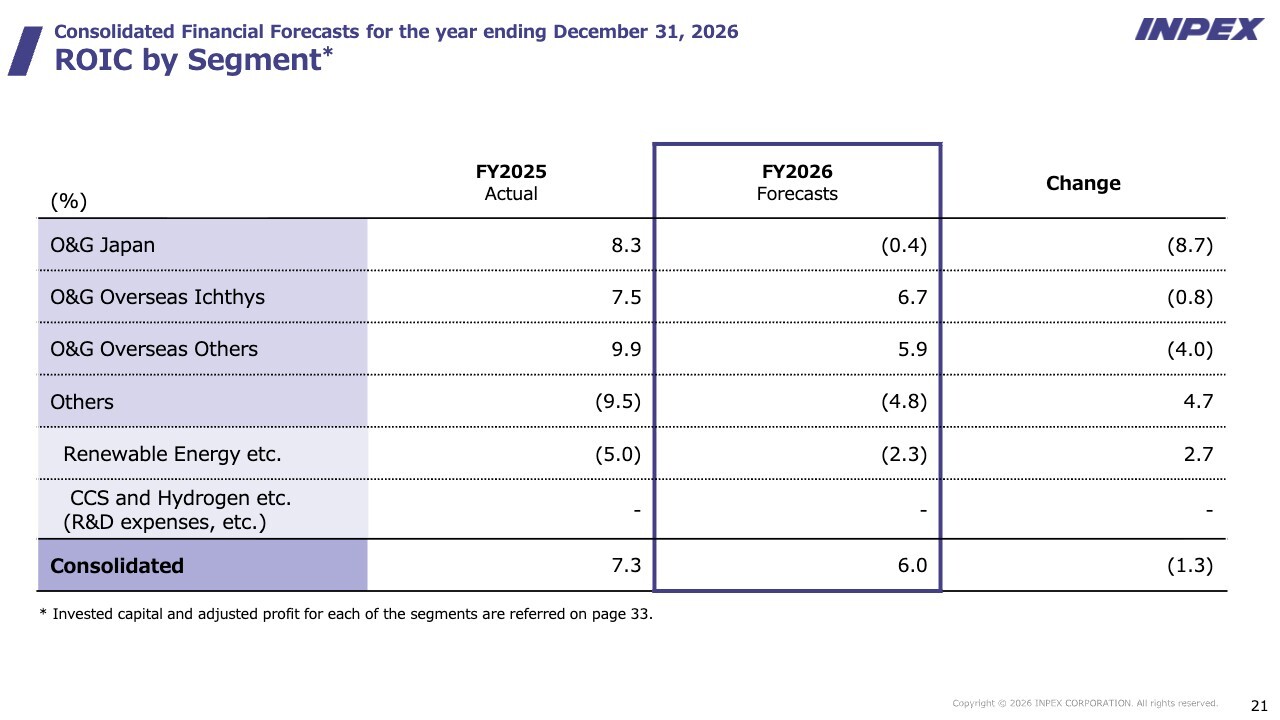

ROIC by Segment

Unfortunately, ROIC is expected to drop slightly this year. In 2025, the rate was 7.3%, but is forecast to be around 6% in 2026. Although not shown here, ROE is also expected to be around 7% in 2026.

The reason for the lower ROE is due to the very large amount of equity rather than the amount of earnings. Reducing equity will increase ROE, but we are currently cautious about reducing equity through large-scale share buybacks. There is one reason for this.

The Abadi LNG project will now begin. Downstream financing for the Abadi LNG project is done through a scheme called “Trustee Borrowing.” This is part of corporate finance. Therefore, we must raise funds based on our creditworthiness.

In light of this, we would like to maintain some equity. Although the investor’s perspective differs from the creditor’s perspective, we believe that a certain amount of equity is necessary from the creditor’s perspective. Therefore, rather than thinking of reducing equity as much as we can just because we have excess cash, we intend to maintain a certain level of equity while preparing to raise funds for the next investment.

That is all I have to say. Thank you very much.

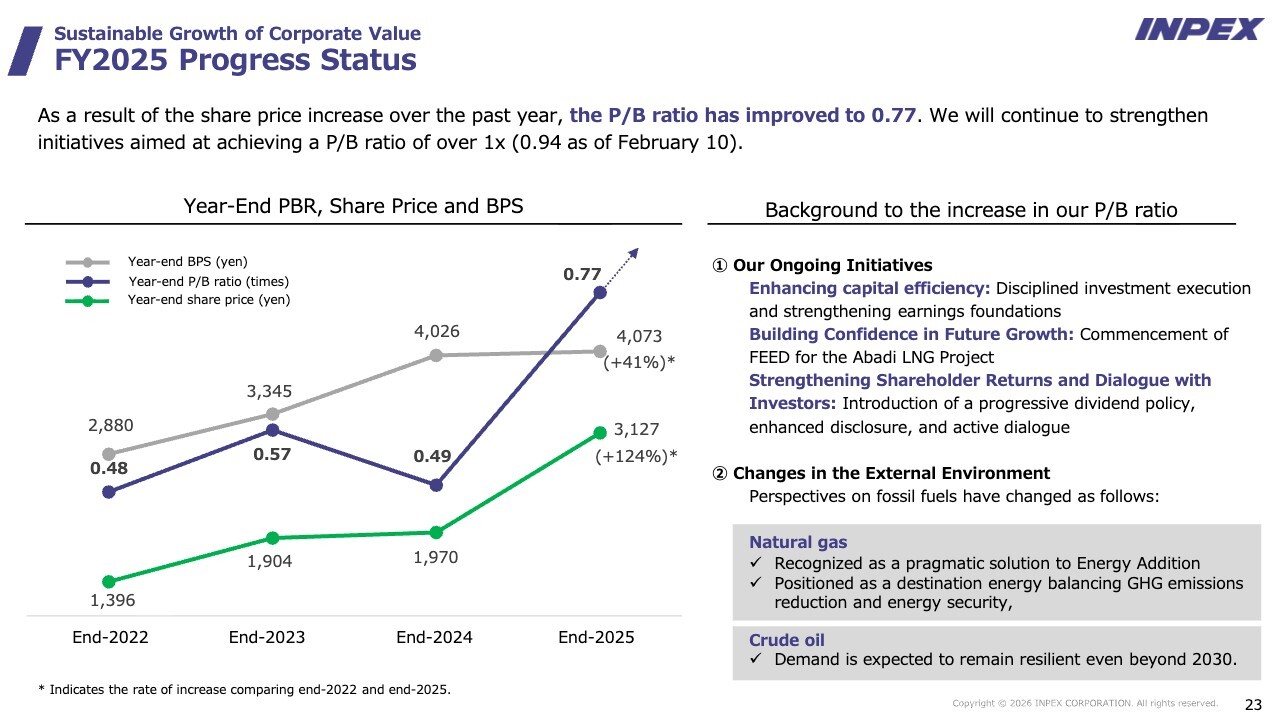

FY2025 Progress Status

Toshiaki Takimoto (hereinafter: “Takimoto”): I am Toshiaki Takimoto, Director, Senior Executive Vice President, Corporate Strategy & Planning. Next, I will explain “Sustainable Growth of Corporate Value.”

This was prepared in accordance with a request from the Tokyo Stock Exchange in March 2023. We report on our progress in each fiscal year as our response to achieving share price and cost-of-equity conscious management. I will explain our efforts this year and the results of last year’s activities.

The graph on the slide shows the share price and PBR. The dark blue color shows the P/B ratio at the end of the year and the green color shows the share price at the end of the year.

At the end of FY2022, the share price was ¥1,396 and the P/B ratio was 0.48. By the end of FY2025, the share price had risen to ¥3,127 and P/B ratio to 0.77. At today’s close, the share price is ¥3,998 and the P/B ratio has improved to 0.98.

As noted on the right side of the slide, we believe that the increase in P/B ratio is due to our ongoing efforts and changes in the external environment.

Specifically, we are working to enhance shareholder returns, strengthen dialogue with investors, and improve capital efficiency.

Another major factor is changes in the external environment. The reassessment of the importance of natural gas and LNG has increased attention to our core businesses, which is natural gas and LNG, leading to an increase in our share price. As a result, we believe this has contributed to the improvement in P/B ratio.

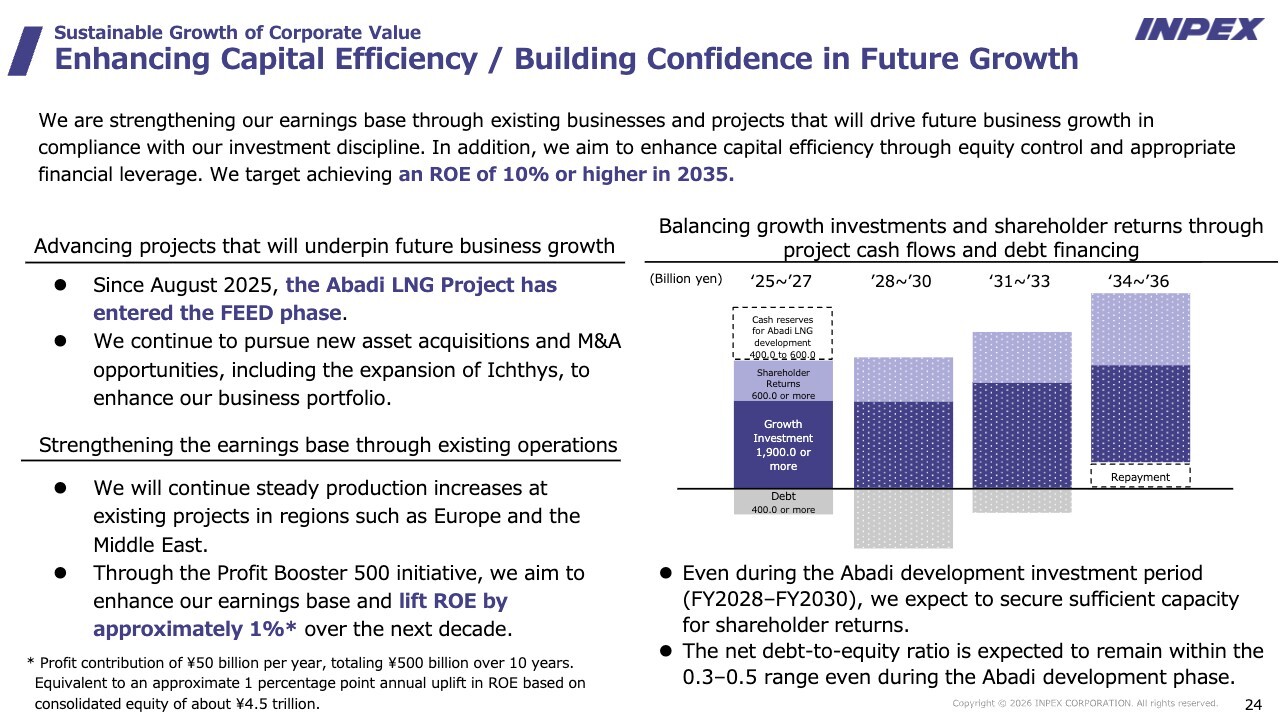

Enhancing Capital Efficiency / Building Confidence in Future Growth

I will now discuss enhancing capital efficiency and building confidence in future growth. As I mentioned earlier, the start of production at Abadi, scheduled for the early 2030s, is the next major point of expected growth.

As shown in the slide, Abadi moved into the FEED phase starting August 2025, and we recognize that the development work has approached a more realistic stage.

We also recognize that what kind of growth story we can draw up by the time Abadi goes into production in the early 2030s is a pressing issue for our company. In the course of interviews with investors, we sometimes receive evaluations from investors that the company’s performance is satisfactory, that shareholder returns are relatively satisfactory, and that they are fully satisfied with IR activities and IR disclosures.

On the other hand, we recognize that the question is “How do we describe the growth story up to the start of Abadi production?” We believe that materializing the acquisition of new assets will help us gain credibility in the market, which will lead to growth.

In addition, we believe that we have the ability to raise ROE by approximately 1% over the next 10 years by strengthening our profit base through the “Profit Booster 500,” in addition to continuing to steadily increase production in our projects in Europe and the Middle East as we strengthen our profit base through our existing businesses.

See the graph on the right side of the slide. This graph shows that the company has sufficient capacity to invest in growth and return to shareholders even during the period from 2028 to the early 2030s, when investment in Abadi will be in full swing.

Although borrowings will increase slightly, the company will keep the Net D/E ratio between 0.3 and 0.5, indicating that we will proceed with the goal of both shareholder returns and growth investment.

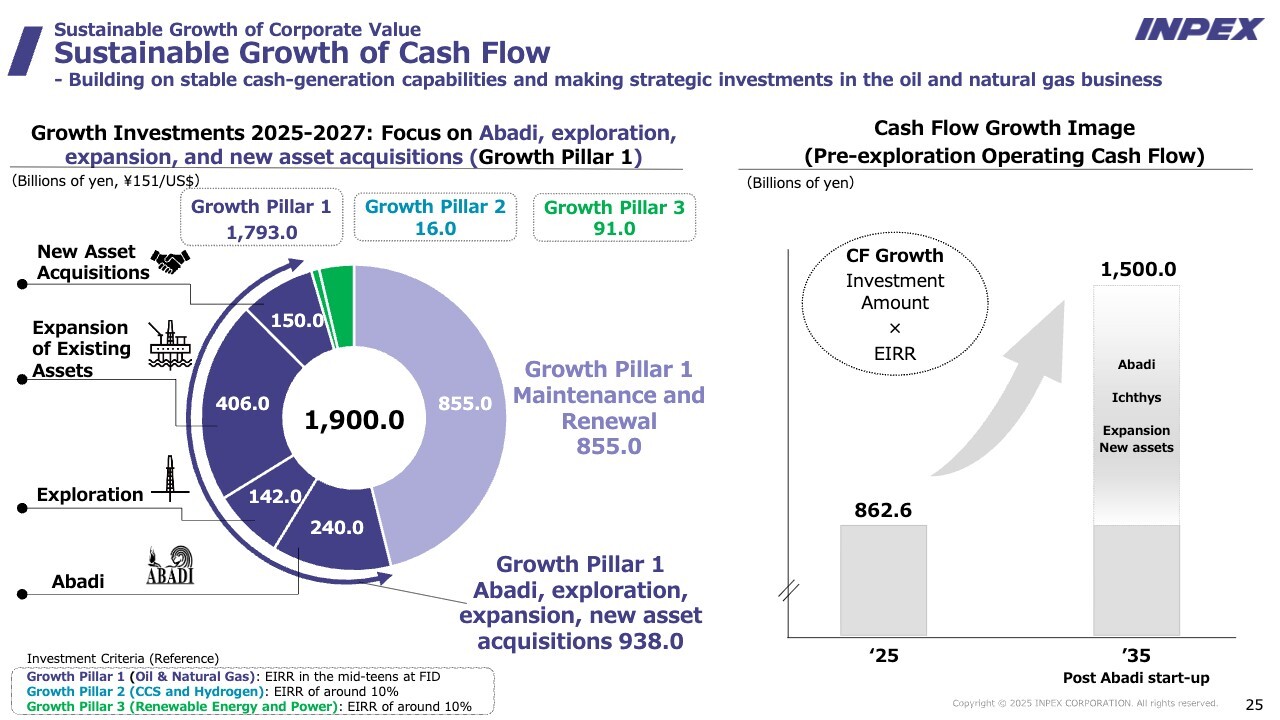

Sustainable Growth of Cash Flow - Building on stable cash-generation capabilities and making strategic investments in the oil and natural gas business

Here I will discuss growth investments. Yamada explained earlier about growth investment in a single year. On the other hand, the three-year investment plan based on the Mid-term Business Plan “INPEX Vision 2035” announced last year is ¥1,900.0 billion.

The first pillar for growth is the expansion of oil and natural gas, especially expansion of natural gas and LNG. Maintenance and renewal costs in this area are expected to total ¥855.0 billion over a three-year period. In addition, ¥938.0 billion is planned to be invested in the Abadi LNG project, exploration, expansion of existing assets, and new asset acquisitions, bringing the overall amount in the first pillar for growth to ¥1,793.0 billion.

Investments in the second and third pillars for growth will also proceed as shown on the slide. Through these efforts, we aim to achieve the goal of 60% expansion of cash flow from operations set forth in “INPEX Vision 2035,” and expand the scale of our business.

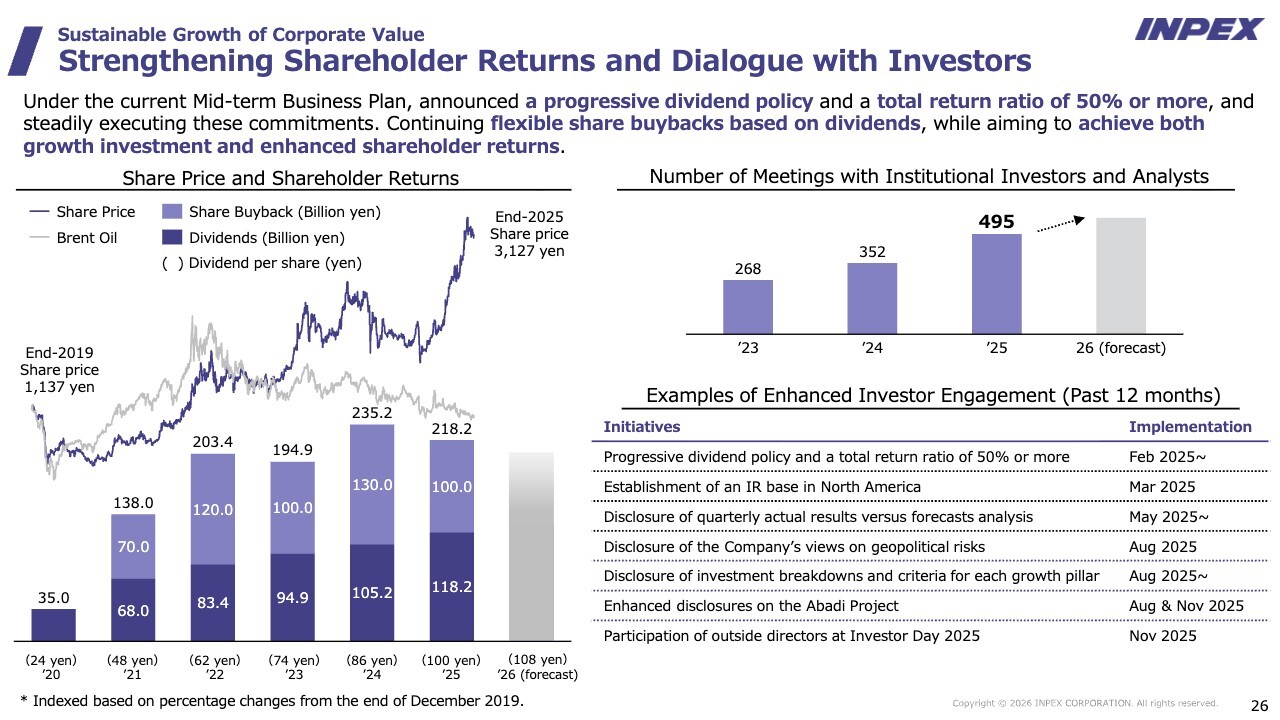

Strengthening Shareholder Returns and Dialogue with Investors

Here I will discuss strengthening shareholder returns and dialogue with investors. See the graph on the left side of the slide. The blue line shows the share price trend after 2020, and the gray line shows the six-year trend of the Brent oil price.

As you can see, since the beginning of 2025, share prices have been rising despite falling oil prices, as if the mouth of the crocodile had opened. One of the factors contributing to this is the company’s shareholder return of around ¥200 billion starting in 2022.

In addition, changes in the business environment, which were discussed earlier, have also had an impact. We believe that natural gas and LNG are realistic solutions to ensure energy security and energy affordability, in other words energy at low cost, while reducing GHGs. Its importance is growing, and we believe it is very much appreciated that we have made it our core business.

Of course, that is not the only factor. The number of individual shareholders has increased approximately 17-fold compared with 2019. In addition to the impact of the new NISA, this can be attributed to the fact that we frequently explain our business to investors, and their understanding of the energy business environment has deepened.

The president mentioned earlier that we should not be satisfied with a P/B ratio of 1, and we aim to go beyond that, promoting management with an awareness of capital efficiency and cost of equity.

The right side of the slide describes the enhancement of investor dialogue. In the last fiscal year, 495 investor dialogues and investor interviews were conducted. As indicated in the lower right corner of the slide, “Examples of Enhanced Investor Engagement,” measures to strengthen business and IR have been developed through these investor dialogues.

I have listed seven such examples on the slide, and I believe that these business activities were also appreciated by investors and led to the realization of today’s closing share price of ¥3,998.

We also feel that understanding of and support for our business has improved as investors have gained a better understanding of our business.

We will continue these efforts to improve our share price and achieve cost-conscious management of equity. This completes my presentation.

Q&A: Outlook for Achievement of Core Earnings Targets

Questioner: This question is about core earnings. This is the first time I have become aware of the ¥330.0 billion analysis. Page 16 of today’s document shows ROE of 7.0% and ROIC of 6.0% on the basis of ¥330.0 billion.

However, your company’s Mid-term Business Plan targets do not include a quantitative ROE goal, but rather use phrases such as “exceeding the cost of equity.” On the other hand, the bottom of page 16 of the document states that “weighted average cost of capital (WACC) and cost of equity are expected to be around 6% and 8%, respectively.” I think it is wonderful that your company has such a specific description.

However, on a core earnings basis, the forecast ROE of 7.0% is below the cost of equity of 8%. Also, the ROIC of 6.0% is consistent with the WACC of 6%, which leads to the conclusion that the company is not producing corporate value.

We are in the middle of our Mid-term Business Plan, but can you tell us if you expect to raise ROE to 8% or more on a core earnings basis, and if that is achievable before the monetization of the Abadi LNG project?

Yamada: First, I would like to reiterate the logic regarding the core earnings that the president explained earlier.

We have newly defined core earnings for the purpose of presenting them to you for the first time. We wanted to convey in our document that “the figure of ¥330.0 billion for FY2026 is not that bad.”

Profit for 2025 was ¥393.8 billion, but the oil price and exchange rate in the 2026 budget is set at $63 and ¥151 respectively, which, when corrected and excluding the one-off profit in 2025 (one-off), would be ¥312.3 billion.

Note that the figures for oil prices and exchange rates have not changed, but the projected profit for 2026 is ¥330 billion, and after deducting one-off profit is ¥315.2 billion. In other words, it appears that profits have decreased by the difference between ¥393.8 billion and ¥330.0 billion, but the fundamentals remain the same.

Our earnings management by ROE and ROIC is not based on core earnings, but on profit. Therefore, we calculate ROE and ROIC based on the assumption that one-off profit come in positive or negative from period to period.

The ¥330.0 billion figure for 2026 would result in an ROE of 7%, which is less than the currently estimated cost of equity of about 8%. ROIC will be 6% with the budget of ¥330.0 billion for 2026, which is a net zero at the WACC level. These numbers alone are not an indicator that will meet your expectations.

As I said earlier, the ¥330.0 billion figure is based on the profit forecast at the beginning of the fiscal year.

There are actually several other revenue opportunities that we are not able to present to you at this time. We aim to raise this figure as we review our full-year forecasts in May, August, and November.

We expect ROE and ROIC to improve in the process. However, please understand that this is such a figure because there are some aspects that cannot be determined without actually working on them.

Q&A: Free Cash Flow Forecast

Questioner: I have a question regarding free cash flow. As you explained earlier regarding the amount of investment in FY2025, looking at the cash flow from investment, it appears that the free cash flow in FY2025 was almost balanced.

Given the increase in investment in FY2026, free cash flow could continue to be balanced or even negative. Please explain the changes between FY2025 and FY2026 in terms of free cash flow and cash flow from investment.

Yamada: I will answer regarding free cash flow. Free cash flow for the year ending December 31, 2025 was ¥138.0 billion, a positive difference between cash flow from operations before exploration investment and cash flow from investment.

Free cash flow of ¥138.0 billion was a solid figure, and the company was generating sufficient earnings. Free cash flow is expected to be negative in FY2026 due to the budgeted growth investment of ¥850.0 billion. In other words, the investment exceeds the cash flow from operations before exploration investment.

Therefore, we believe we must raise funds this year. Note that this is the first time since the fiscal year ended March 31, 2019 that free cash flow has been negative.

To date, we have not raised funds and have invested and returned to shareholders using our own funds. However, this year we plan to make a major investment, and if we proceed with a total payout ratio of 50%, we will require ¥165.0 billion, so we will have to raise funds.

We do not believe that negative free cash flow is a major problem for our management. It is part of normal management activities to implement appropriate procurement for solid investments and growth.

The key question is how financial discipline will be maintained as a result. Based on this year’s investments and procurement, we expect a net D/E ratio of 0.39. This figure falls within our financial discipline range of 0.3 to 0.5. Therefore, we do not see any financial problem in using financing to offset negative free cash flow and make investments.

I hope you are reassured regarding the above points.

Questioner: I understand. We expect to earn core earnings plus an additional amount.

Q&A: Breakdown of Growth Investments and their Contribution to Earnings

Questioner: This investment plan is a significant increase over last year. Page 20, for example, mentions investments to augment existing projects, particularly in Abu Dhabi and the Middle East. This was explained in the president’s opening presentation, but please tell us about the specifics of this investment, and how it will contribute to earnings.

In particular, I would like to know the time frame and scale of the revenue contribution for investments to augment existing projects. Am I correct in understanding that the equity IRR will be in the mid 10% range? Please be as specific as possible with a breakdown of the investment, and the time frame in which it is expected to contribute to profits.

Yamada: The overall investment plan is ¥850.0 billion, which is a rare large-scale investment in recent years.

Investments are broken down into the categories of “Abadi LNG project,” “Exploration,” “Expansion of Existing Projects,” and “New Asset Acquisitions.” The “Abadi LNG project” and “exploration” are as previously indicated.

The “expansion of Existing Projects” refers to investment in the expansion of production at existing facilities. For example, it includes investments to increase production capacity in Abu Dhabi, and a substantial investment is accounted for here.

The term “new asset acquisition” refers to a project in which a new asset is acquired, and in some cases, M&A is also included in this category. The Company expects to invest approximately ¥282.0 billion in expansion of existing projects and approximately ¥106.0 billion in new asset acquisitions. The regions include investments for the connection related to the Ichthys LNG expansion project in Australia, in accordance with our portfolio strategy.

We are also making relatively diversified investments in the growth regions of Asia, Abu Dhabi, and Japan, with a focus on oil and gas.

“Exploration” takes time, but the overall investment includes several projects that are highly immediate, although we cannot give you specific project names. We assume that these can contribute to earnings this year and next.

As the president mentioned, the bridge to the Abadi LNG project is an urgent issue for our company. This effort has accelerated over the last year and into this year.

With oil prices hovering in the $60 range, the environment is not bad. We believe this is a good time to make a new investment, such as asset acquisition, because it can be handled at an appropriate price.

Please understand that even if free cash flow becomes negative, it is a sign of our determination to raise funds and reap the next big fruit.

Q&A: Progress and Milestones of the Abadi LNG Project

Questioner: This is about the Abadi LNG project. I think FEED started in earnest last summer, but do you envision any milestones by the end of this year? At this time, can you tell us if there are any significant developments or milestones planned for 2026 related to Abadi, for example, discussions with the Indonesian government or agreements with vendors?

Can you comment on the possibility of concrete progress in 2026 toward the target by the end of 2027, within the limits of what is currently envisioned?

Ueda: I would like to discuss the milestones for Abadi. This year we plan to basically move forward with FEED.

The biggest point is to obtain an environmental permit called “AMDAL” from the Indonesian government, which is very important. Once we receive the permit, we can proceed to the actual various tasks, so we believe that this will be one important milestone.

After acquiring AMDAL, we also need to start full-scale engagement with the local community in the local area of Indonesia, the region where the project will be carried out. We believe that this will be another milestone.

In addition, we have already received a number of LOIs (letter of interest) regarding marketing. In order to put this into a concrete contract, we need to proceed with interim processes. We call this our “Key Term Sheet,” and we believe that finalizing some of the key terms will be a milestone for this year.

Preliminary discussions have already begun regarding negotiations with the Indonesian government on terms and conditions, although it is difficult to proceed in earnest until some results of the FEED are obtained. Brainstorming discussions on project costs are also underway, and such discussions are expected to get more intense this year.

Then, investment is as Yamada has discussed. While securing profit in the short to medium term is very important, there are some matters that we cannot yet discuss with you.

For example, regarding exploration, we have already acquired six exploration blocks in Malaysia, and we plan to start exploratory drilling of about nine wells this year. In addition, Malaysia already has many pipelines in place, so success in exploration could lead to production in the medium term.

The same applies to Norway. For example, in Norway, the company announced that it has acquired assets from Pandion.

These efforts will lead to short- and medium-term production and even revenue. In addition, we are taking various budgetary considerations into account with respect to existing production assets, which are immediately linked to revenues.

Therefore, we believe that as these measures take shape, it will be possible to secure medium-term revenues before connecting to Abadi.

Abu Dhabi is of course our largest project, but I hope you will consider this year’s major investment as being aimed for such an initiative.

Q&A: New Investment Environment

Questioner: You spoke earlier about investing in the acquisition of assets. At that time, I believe you explained that the current environment is favorable. On the other hand, my recollection is that the seller side, or sellers, are always very bullish, and I am concerned that this may result in pushing less profitable projects.

With that in mind, can you tell us again about the environmental aspects surrounding investment in new acquisitions?

Ueda: Regarding the investment, you ask whether the environment is good, and whether the seller is bullish.

Frankly, it is a difficult situation to determine whether the environment for purchasing is favorable. However, as I mentioned at the beginning, in the market, natural gas must be the core for the time being, and there is a mixture of the desire to acquire many natural gas assets and the desire to sell them.

In that sense, I think now would be an appropriate time to consider this.

We have set a hurdle rate. In the case of oil and gas in particular, we consider this in detail as country risk varies from country to country, but we generally set the hurdle rate in the mid-teens range. Therefore, our basic policy is to invest in what satisfies that rate.

We believe that this is a matter of investment discipline, and we will be taking such aspects into consideration as we proceed.

Q&A: Financial Planning

Questioner: This question is about the “Profit Booster.” First, for the fiscal year ending December 31, 2025, is it correct to understand that it will be about ¥80 billion?

Next, regarding the fiscal year ending December 31, 2026, please tell us if we should assume that the “Profit Booster 500” will be used as the base, and that various other factors will be built on top of it?

Yamada: The “Profit Booster 500” was first discussed with you last year. As you have been informed, the first is TA recycling, i.e., transferring what is in the foreign currency translation adjustment to retained earnings through the P/L. The other is investment incentives.

In FY2025, we mentioned the numbers “80” and “65” billion, but in terms of financial results, it contributed approximately ¥80 billion of profits. However, when we discussed this with you, we had a specific definition. Although the “Profit Booster 500” program began in 2025, similar investment incentive effects were actually partially in place prior to 2024. Therefore, when considering the “Profit Booster 500,” the actual amount for FY2025 is approximately ¥80 billion, but when considered as a change, it is necessary to subtract the figure that had been expressed before the “Profit Booster 500” was announced.

Subtracting the amount that had been disclosed before the announcement as “Profit Booster 500” from the approximately ¥80 billion, the result is a figure of approximately ¥65 billion. In the financial statements, the actual amount in effect is ¥80 billion, but the figure we shared with you is approximately ¥65 billion because we were considering the change.

In other words, in FY2025, we have achieved ¥65 billion compared with the “Profit Booster 500,” and that is precisely what we have done.

In FY2026, that figure will be ¥80 billion, an increase of ¥15 billion from FY2025.

Also, regarding what you said about “building up earnings over the next year,” earnings are not generated simply by controlling the balance sheet. For example, OPEX reductions and other factors also contribute to earnings.

On the other hand, it is the tax expense that is considered important to us. As you know, we pay taxes in the range of ¥800 to ¥900 billion. Therefore, it is important to make good use of tax benefits here.

Of course, while taxes are paid correctly, it is also important to properly account for tax effects.

Currently, we have a huge balance sheet of over ¥7 trillion. In foreign exchange conversion and valuation of fixed assets, factors such as financial and tax gains and losses and unrealized gains for tax purposes arise as oil prices and exchange rates fluctuate on a daily basis.

How these are combined is important. We will naturally work to ensure profitability while maintaining proper control of our balance sheet.

The balance sheets for period N and “N+1” are correct because the company has IFRS financial statements. This builds the balance that should be in place.

Under the IFRS approach, the difference between “N+1” and N corresponds to the P/L. Therefore, as long as the correct balance sheet exists, we believe that the correct P/L should be prepared from the difference.

Therefore, part of our financial management is to generate profits while effectively combining unrealized gains and losses, and financial and taxable gains and losses on the balance sheet.

We also hope to increase revenues in FY2026 based on this, including talk of “approximate starting point figure” and “stay tuned.”

Q&A: Ichthys low-pressure production facility and its impact on production volume

Questioner: I am referring to what was said about the “Due to the connection work at Ichthys low-pressure production facility, production will not reach full capacity in FY2026 .” I am sorry if I just did not know this, but I do not recall hearing such information before.

With regard to the operation of this low-pressure production facility, I would like to ask about the fact that it will not produce much in FY2026. Is it that what was originally included in the previous plan has now materialized as an FY2026 story? Or is this something that has been considered relatively recently?

Also, please tell us about the production profile of the Ichthys LNG expansion project, whether it will be in full production from FY2027 on, or whether shutdown maintenance is planned at some point? I would like to take this one step further and ask for an update.

Ueda: Regarding the update to the production profile of Ichthys, specifically the low-pressure production facility, this was naturally expected.

Let me explain again what a low-pressure production facility is. This is a mechanism that enables production to continue even at low pressure so that a plateau can be maintained over the long term, even if well pressure drops in the future. To this end, a booster compressor module was installed early last year at CPF, an offshore production facility.

Over the course of last year and this year, work began with placing the equipment and connecting the wiring. The piping consists of an enormous amount of wiring and pipelines, which is a daunting task, so it was assumed that commissioning would be performed.

Specifically, the estimate of how much time and reduced production would be required for commissioning work on low-pressure production facilities was obtained comparatively recently.

Therefore, while we have not talked much about this aspect of the project, the fact that there would be such work was in itself expected.

However, these are one-off tasks. We hope you understand that this is a temporary operation, as we will move to full-scale operation once the low-pressure production facility is commissioned.

We are still in the process of formulating a concrete plan for operation in 2027, but since some kind of maintenance will be required, we believe that the details of this plan need to be organized as a future issue.

Q&A: Oil Price Impact for the Current Year

Questioner: I would like to ask about the impact of oil prices on your full-year forecast for FY2026. The oil price impact listed on page 17 is a negative factor of ¥56.4 billion, which appears large when compared with the oil price assumptions, past sensitivities, etc. Is this simply “this is what is calculated,” including timing discrepancies, etc.?

Also, regarding your earlier mention that the ¥330.0 billion is an approximate figure, please explain whether this ¥56.4 billion includes a similar conservative element.

Yamada: In the actual results for FY2025 and the budget at the beginning of the fiscal year, the impact of external factors such as oil prices and exchange rates was ¥52.3 billion.

This includes the lagging effect of natural gas and LNG. This breakdown shows that the impact of oil prices is about ¥30 billion. In addition, the impact of the lagging effect and spread adjustments between oil grades, which are reflected in LNG sales with a delay of several months based on the lowered oil price, is approximately ¥20 billion. These are the breakdown of the approximately ¥50 billion.

The sensitivities I mentioned earlier are viewed from the beginning of this year, not simply “sensitivities times something,” which is a $5 drop from $68 to $63, and multiplying out to get ¥25 billion.

When preparing the budget at the beginning of the period, the oil price impact and the lagging effect were taken into account, which together are defined as the oil price impact. Therefore, the ¥52.3 billion figure represents the oil price and exchange rate impact when viewed plainly.

Q&A: Operation Schedule for Low-pressure Production Facility

Questioner: This is a follow-up question regarding the low-pressure production facility. Am I correct in understanding that this impact will mainly occur in the first half of the year? What is your sense of schedule?

Ueda: Regarding the low-pressure production facility, this is not a process like shutdown where all the machines are stopped and connected, but the work is performed while the machines are operating.

For example, when connecting pipelines, some related facilities are temporarily shut down before the pipeline is connected and then they are restarted. Therefore, it is different in nature from so-called shutdown maintenance, which is performed during a shutdown for a certain period of time.

Such work will not be limited to the first or second half of the year, but will be carried out sequentially throughout the year. So, we are assuming that the number of cargoes of LNG we will ship this year will be about 10 cargoes per month.

Q&A: Production Cost Projections

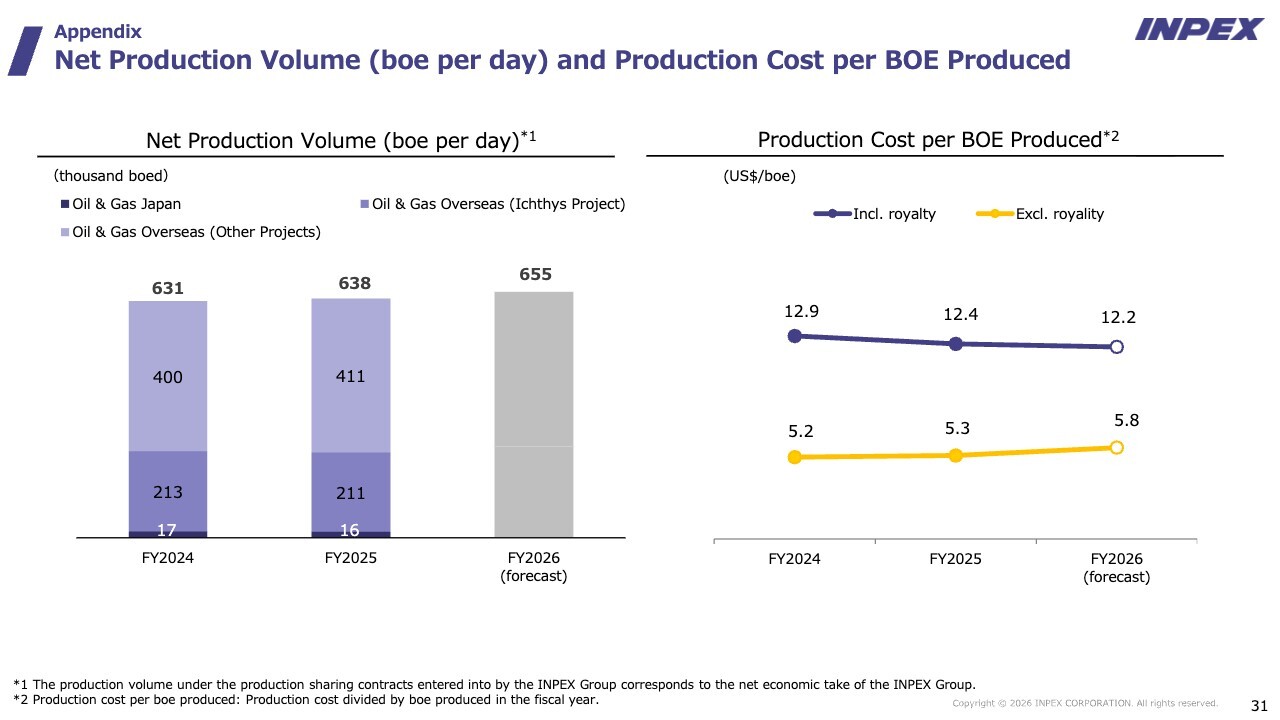

Questioner: This question is about the forecast for production costs. The forecast is for an increase on a non-royalty basis, but a decrease when royalties are included. Please give us as much background on this as possible.

Takimoto: We expect the production cost per barrel to be $5.8 in 2026.

Production costs will vary depending on the balance between European and Middle Eastern production and Ichthys’ production, as well as the associated OPEX. Therefore, production costs will vary depending on whether the ratio of royalty-inclusive and royalty-exclusive operations, especially the ratio in Europe and the Middle East where royalties have a significant impact, increases or decreases.

Therefore, depending on the balance of production in Europe and the Middle East and the trend of OPEX, it is considered that a slight decreasing trend in royalty inclusive and an increasing trend in royalty-exclusive will occur.

Questioner: Am I correct in understanding that there is no overall increase in costs, but only an increase in the percentage of the larger cost portion, which causes the overall number to fluctuate?

Takimoto: That is correct. The Ichthys LNG project, for which we are the operator, is making further efforts this year for cost reductions in particular.

Therefore, we aim to further reduce the OPEX of Ichthys, but we have already made considerable progress in reducing it and are in the process of approaching the lower limit. We hope you understand that the extent to which we can proceed within this context will be determined taking into consideration the overall balance of production.

Q&A: Basis for setting dividend (increased to ¥108) and discussion

Questioner: I would like to ask about the thinking regarding this dividend increase. We are very encouraged by the confidence you have shown in your performance growth and cash flow.

In this context, what kind of discussion did you go through to set the level of ¥108? Ultimately, I think it is a comprehensive decision, but in the past, the resulting dividend payout ratio has often been around 30%.

This time, the dividend payout ratio has been raised to just under 40% when calculated simply from earnings per share (EPS). The figure of ¥108 seems hardly a rounded number, but can you tell us a little more about your thinking and what the discussion was behind it?

Ueda: There was a lot of discussion about how much to pay out. Naturally, one consideration is EPS and how profits will be returned this year.

As Yamada mentioned, if profits are ¥330 billion and the total payout ratio is 50%, the total shareholder returns would be ¥165 billion. If the dividend is set at ¥108, the amount needed is approximately ¥120 billion, and there is still a gap between the two.

However, this ¥330 billion is only a forecast at this point, and whether it can be achieved or not has not been determined. However, we decided that with some foresight, we could afford a dividend amount of ¥108.

In order to achieve a total payout ratio of 50%, the company will need to either increase dividends or repurchase shares during the term. One reason for this is the idea of setting a level that allows for a margin of safety.

On the other hand, some argued that since profits have not risen that much, it would be fine if they were the same as in 2025.

There was also discussion about price increases. In the past, during times of deflation, a dividend yield of 3%, for example, was directly translated into a real dividend for investors. However, with prices rising at the current rate of 3%, the real dividend yield will diminish by that amount.

Therefore, we comprehensively considered the factor that “exactly the same” would not be good either, and set the price at the level of ¥108 this time.