Financial and Management Results Briefing for the Second Quarter (First Half) of Fiscal Year Ending March 2026

Kazuaki Tokiwa (hereinafter “Tokiwa”): Good morning. My name is Kazuaki Tokiwa, Representative Director, President & CEO of RIKEN TECHNOS CORPORATION. Thank you very much for taking time out of your busy schedules to attend our financial and management results briefing today.

Today’s presentation will first cover the financial results summary for the first half of the fiscal year ending March 2026 (1H FY2025). Following that, I’ll explain the progress of our three-year medium-term business plan, which began in April of this year.

I’d now like to explain our overview of financial results for 1H FY2025.

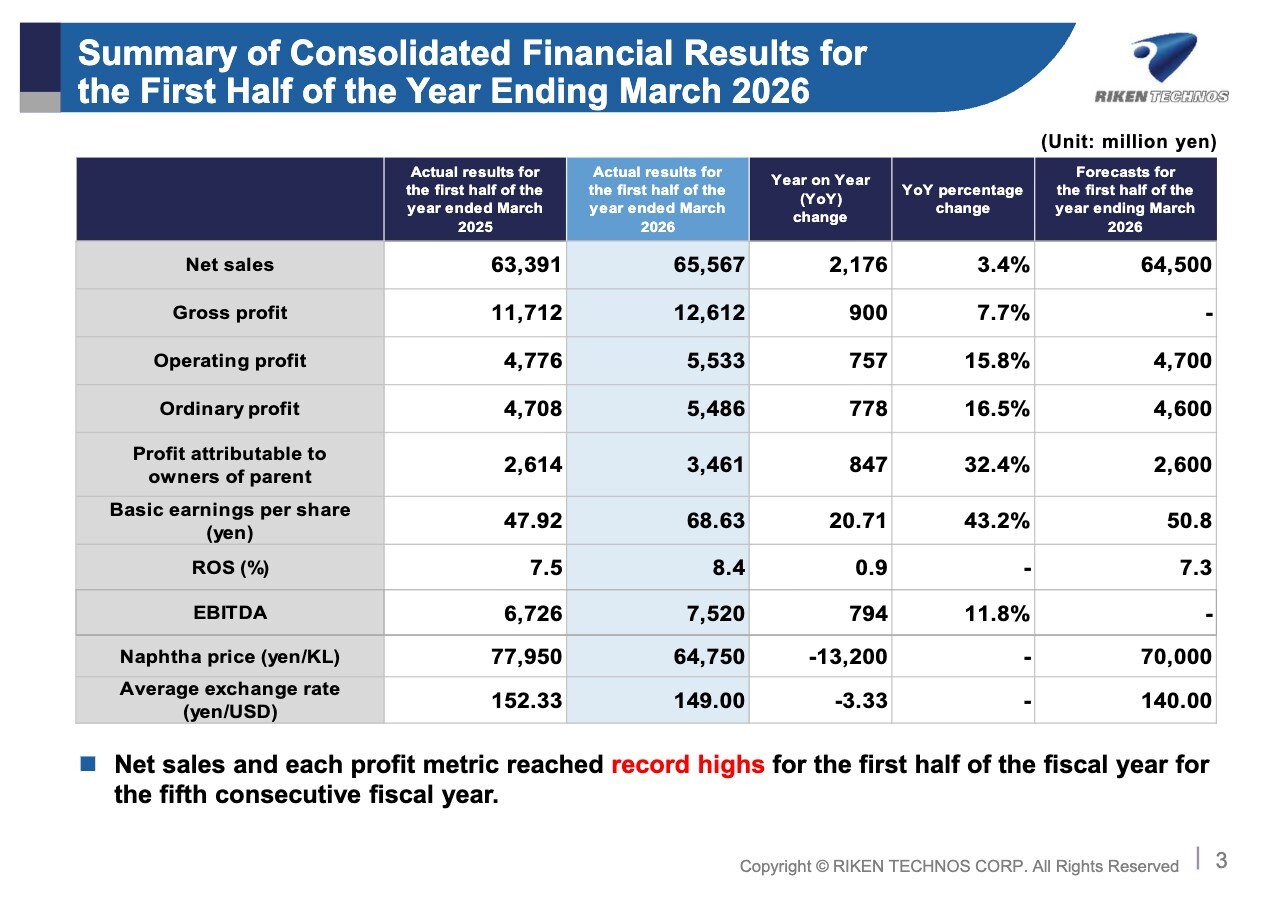

Summary of Consolidated Financial Results for the First Half of the Year Ending March 2026

The first is a summary of our consolidated financial results. For 1H FY2025, consolidated net sales reached 65,567 million yen, a YoY increase of 2,176 million yen, or 3.4%. Operating profit was 5,533 million yen, a YoY increase of 757 million yen, or 15.8%. Ordinary profit was 5,486 million yen, a YoY increase of 778 million yen, or 16.5%. Profit attributable to owners of parent was 3,461 million yen, a YoY increase of 847 million yen, or 32.4%.

Consolidated net sales and profits at each earnings level have reached record highs for the fifth consecutive half-year period. ROS stands at 8.4%, and EBITDA was 7,520 million yen.

ROS also reached a new record high for the first half.

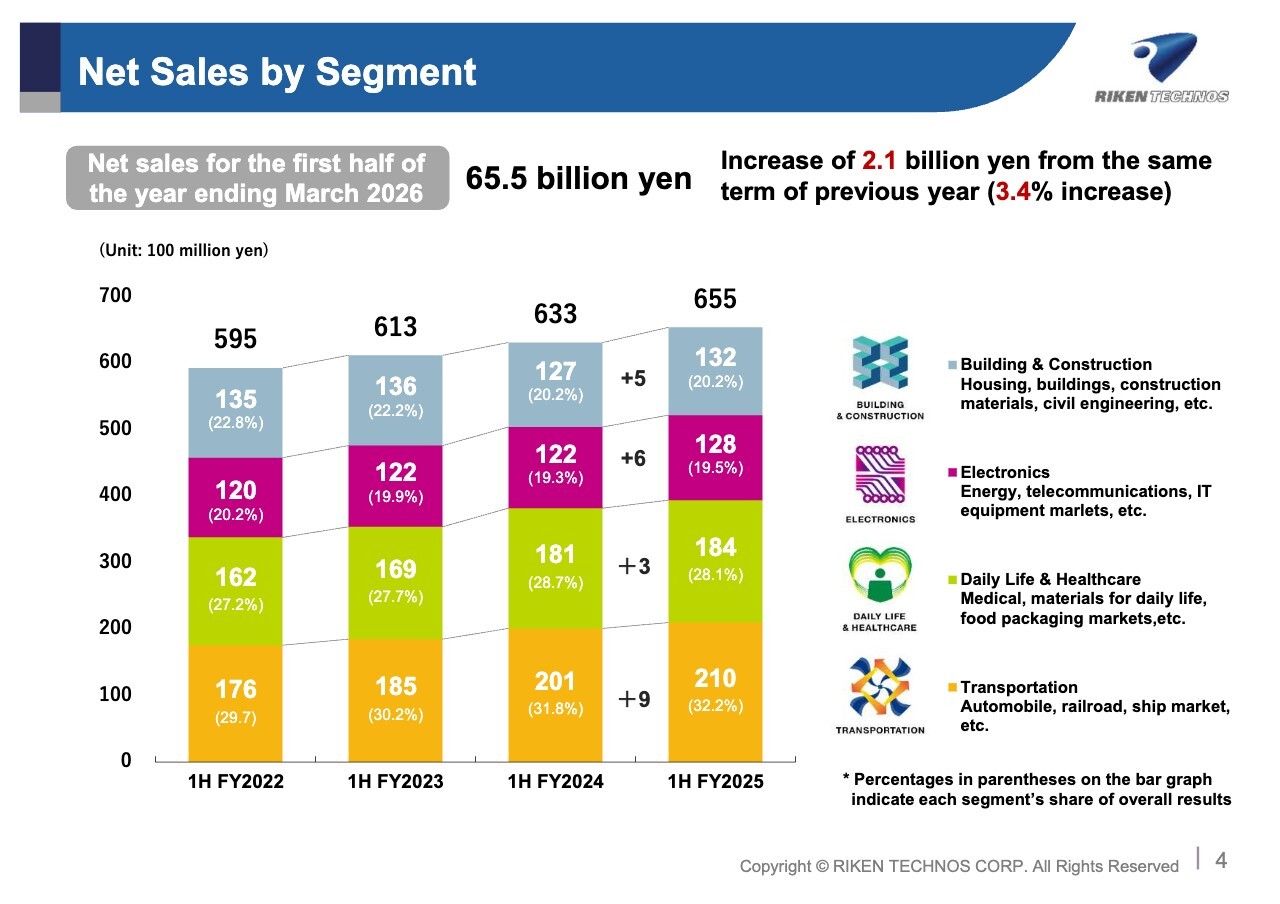

Net Sales by Segment

Next, I’ll explain the trend in net sales by segment. Sales in the Transportation segment, which includes automotive products, reached 21,000 million yen, a YoY increase of 900 million yen.

Sales in the Daily Life & Healthcare segment, which includes medical supplies, materials for daily life, and food packaging, reached 18,400 million yen, a YoY increase of 300 million yen.

Sales in the Electronics segment, which includes telecommunications and IT equipment markets, were 12,800 million yen, a YoY increase of 600 million yen.

Sales in the Building & Construction segment, which includes housing construction materials and the civil engineering market, were 13,200 million yen, a YoY increase of 500 million yen.

Details on each segment will be provided later.

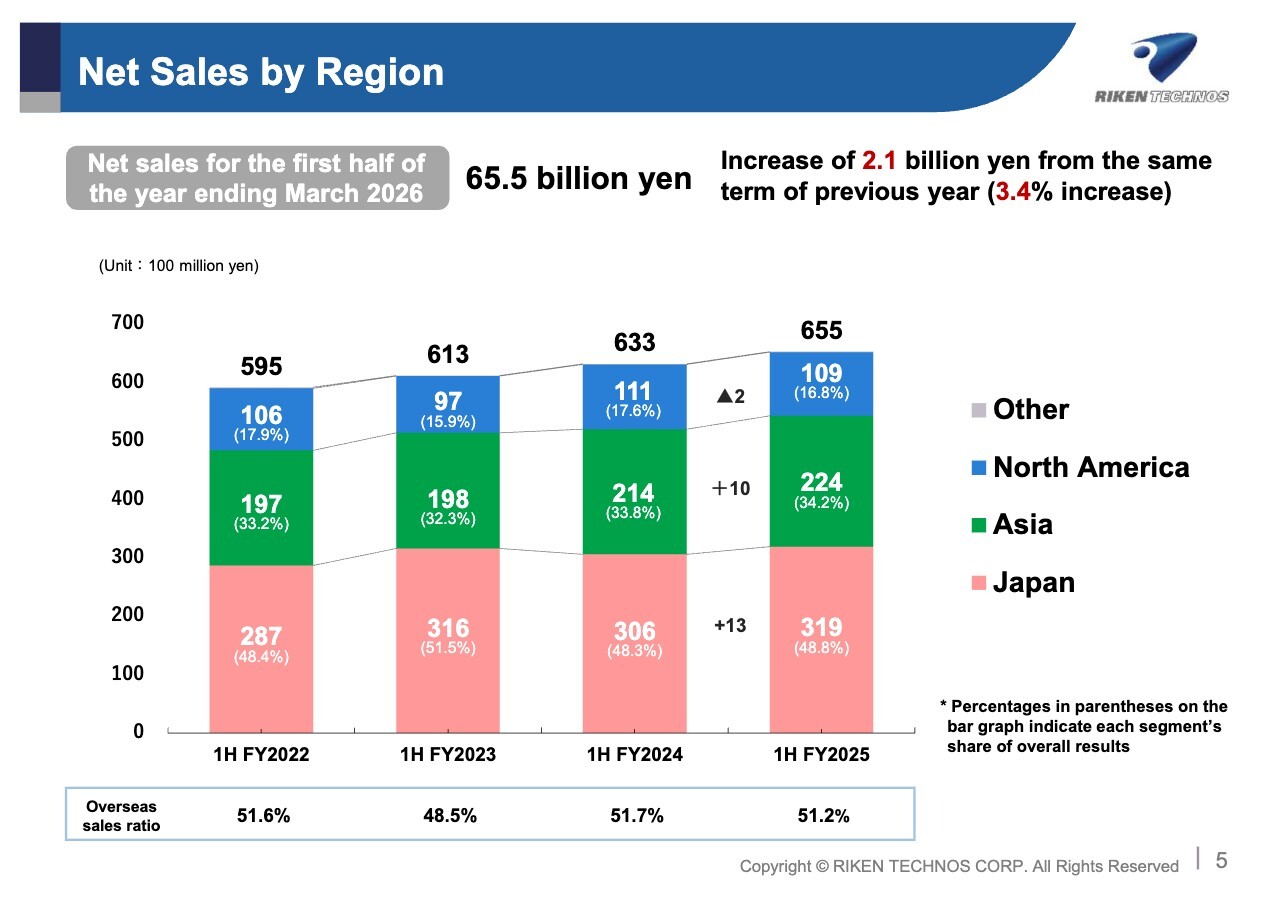

Net Sales by Region

Next is the trend in net sales by region. Japan recorded 31,900 million yen, a YoY increase of 1,300 million yen. Asia recorded 22,400 million yen, a YoY increase of 1,000 million yen. On the other hand, North America recorded 10,900 million yen, a YoY decrease of 200 million yen, partly due to exchange rate effects.

The regional composition ratio is as follows: Japan accounted for 48.8%, Asia for 34.2%, North America for 16.8%, and other countries for 0.2%. The overseas sales ratio stands at 51.2%, a decrease of 0.5 percentage points YoY.

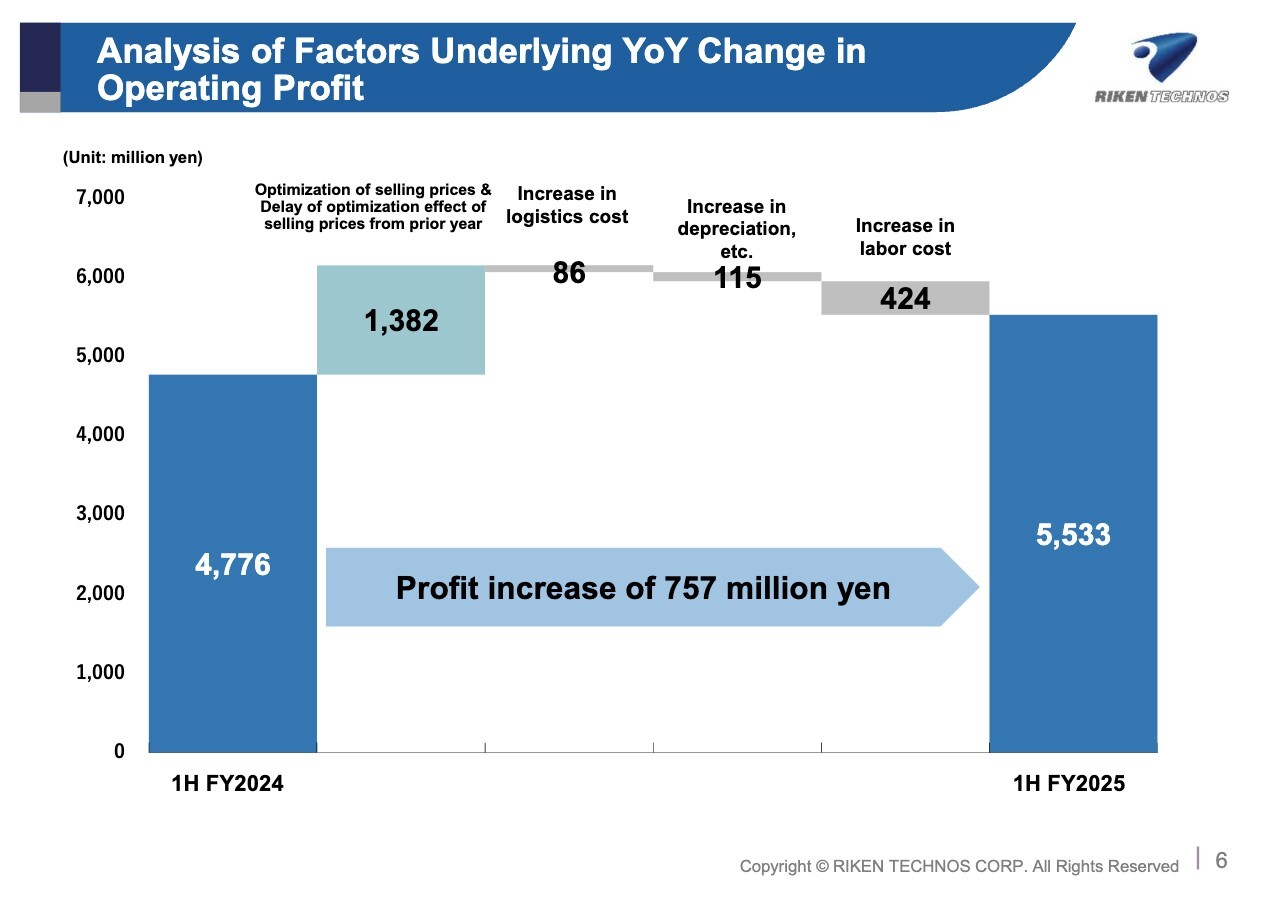

Analysis of Factors Underlying YoY Change in Operating Profit

Next is an analysis of the factors underlying the YoY change in operating profit.

Operating profit for H1 FY2024 was 4,776 million yen. The main factors that drove the increase were the pass-through of rising raw material and auxiliary material costs, as well as increased business expenses, to product prices. Together with the above factors, the timing lag from price revisions also contributed, resulting in an increase in profit of 1.382 billion yen.

On the other hand, factors reducing profit included an 86 million yen increase due to higher logistics costs, a 115 million yen increase due to higher depreciation associated with proactive investments, and a 424 million yen increase due to increased labor costs. In total, these factors resulted in a profit increase of 757 million yen, bringing the operating profit for H1 FY2025 to 5,533 million yen.

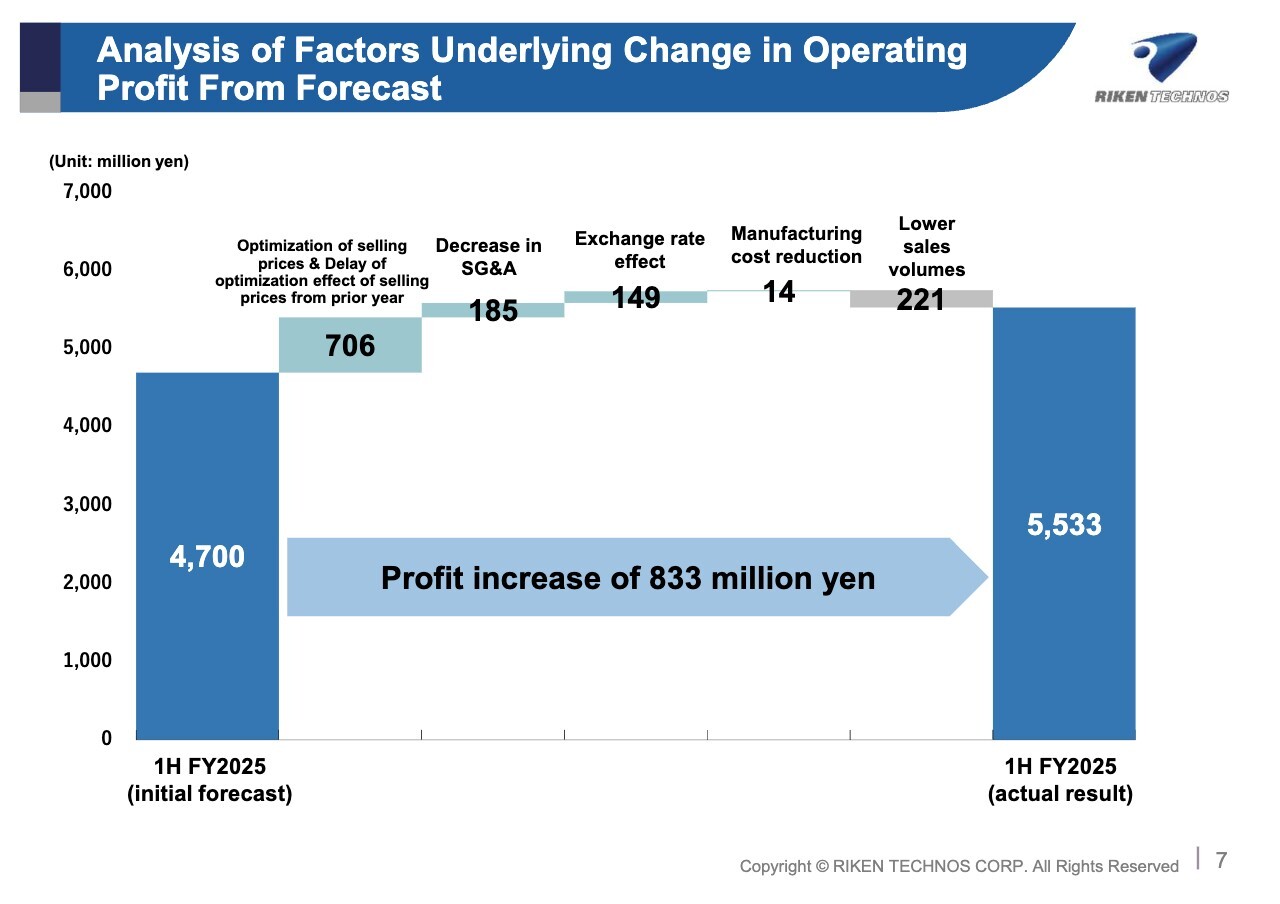

Analysis of Factors Underlying Change in Operating Profit From Forecast

Next, I’ll explain the factors underlying the change in operating profit from the initial forecast for 1H FY2025. The initial forecast projected an operating profit of 4,700 million. Factors contributing to the increase in profit were a 706 million yen gain from selling price optimization and the delay of the optimization effect of selling prices from the previous year; a 185 million yen reduction in SG&A; a 149 million positive impact from the weaker yen; and a 14 million yen reduction in manufacturing costs.

Conversely, factors reducing profit included falling short of the initial sales volume forecast by 3%, resulting in a 221 million yen decrease. Combined, these factors led to a net increase of 833 million yen, resulting in an operating profit of 5,533 million yen for 1H FY2025.

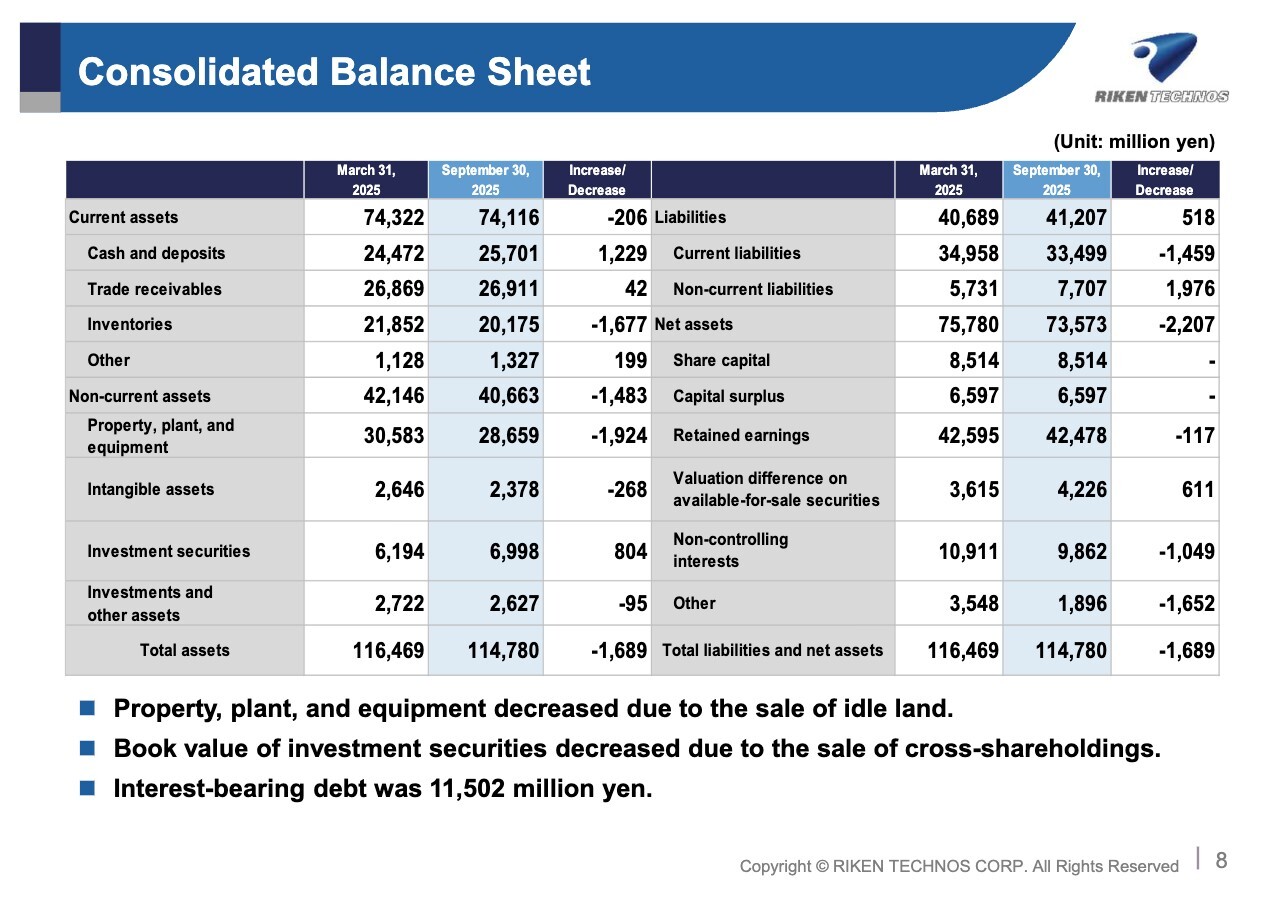

Consolidated Balance Sheet

Next is our financial position as of September 30, 2025. Total assets amounted to 114,780 million yen, a decrease of 1,689 million yen compared to the previous fiscal year-end. Liabilities amounted to 41,207 million yen, an increase of 518 million yen compared to the previous fiscal year-end. Net assets were 73,573 million yen, a decrease of 2,207 million yen compared to the previous fiscal year-end.

The equity-to-asset ratio is 55.5%.

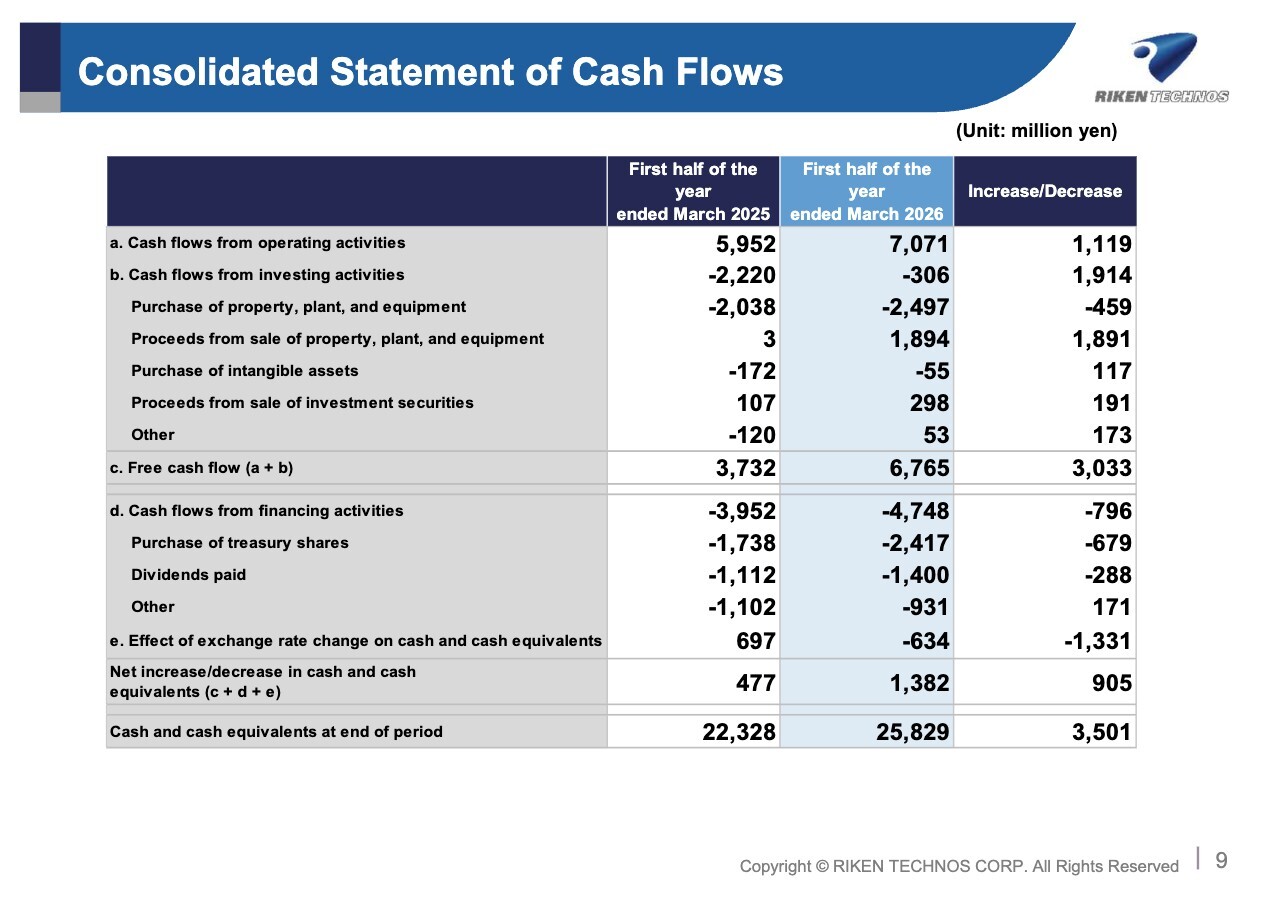

Consolidated Statement of Cash Flows

I’d like to explain the consolidated cash flow statement. Cash flows from operating activities amounted to 7,071 million yen. Cash flows from investing activities included 1,894 million yen proceeds from sale of property, plant, and equipment, resulting in a net outflow of 306 million yen. Cash flows from financing activities amounted to a net outflow of 4,748 million yen. The net increase from these items totaled 1,382 million yen, bringing the balance of cash and cash equivalents at the end of the period under review to 25,829 million yen.

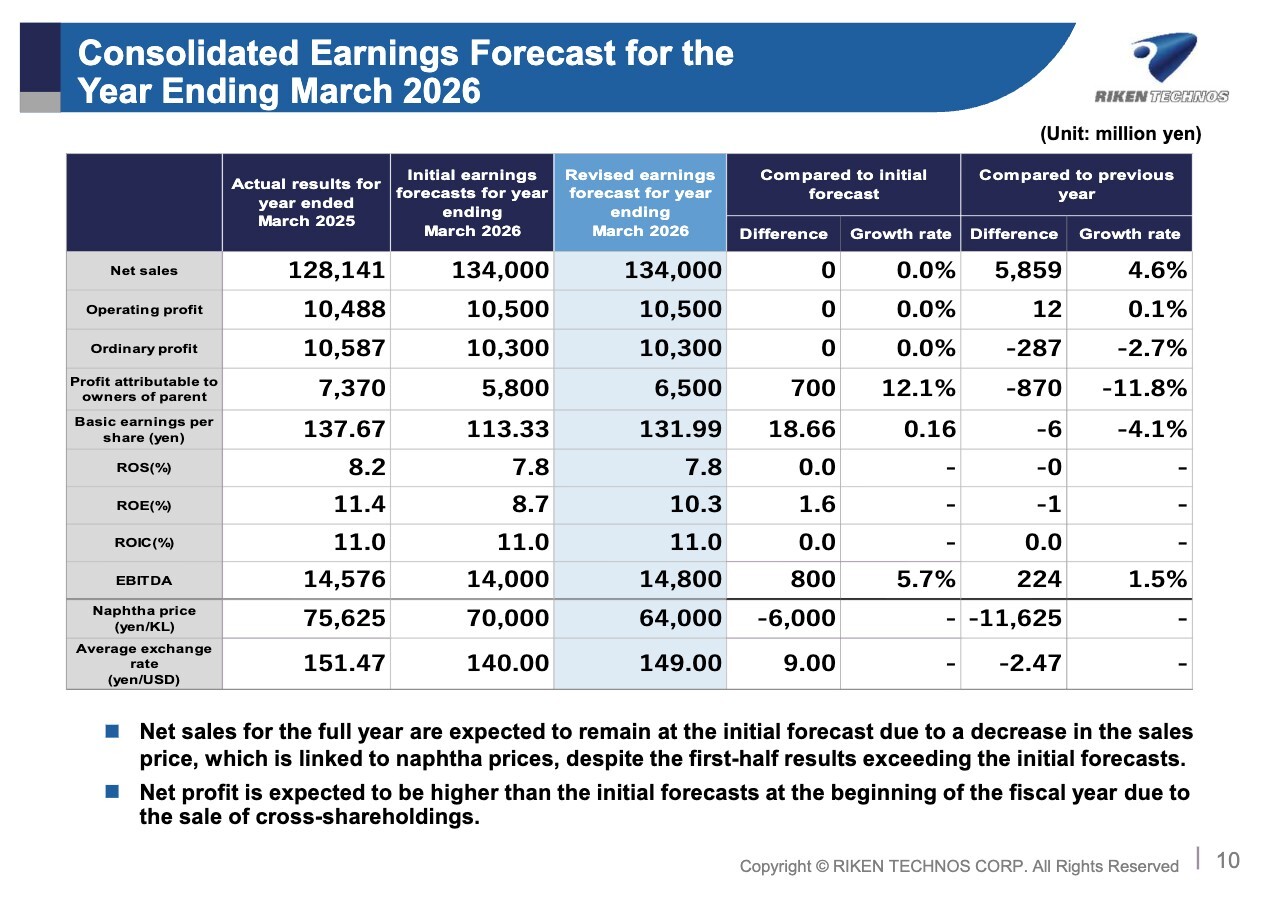

Consolidated Earnings Forecast for the Year Ending March 2026

Next is the consolidated earnings forecast for the year ending March 31, 2026. We project net sales of 134,000 million yen, operating profit of 10,500 million yen, ordinary profit of 10,300 million yen, and profit attributable to owners of parent of 6,500 million yen. Compared to the initial forecast announced on April 30 this year, ordinary profit remains unchanged, reflecting the current uncertain economic outlook. However, profit attributable to owners of parent has been revised upward by 700 million yen to 6,500 million yen, reflecting the anticipated sale of cross-shareholdings.

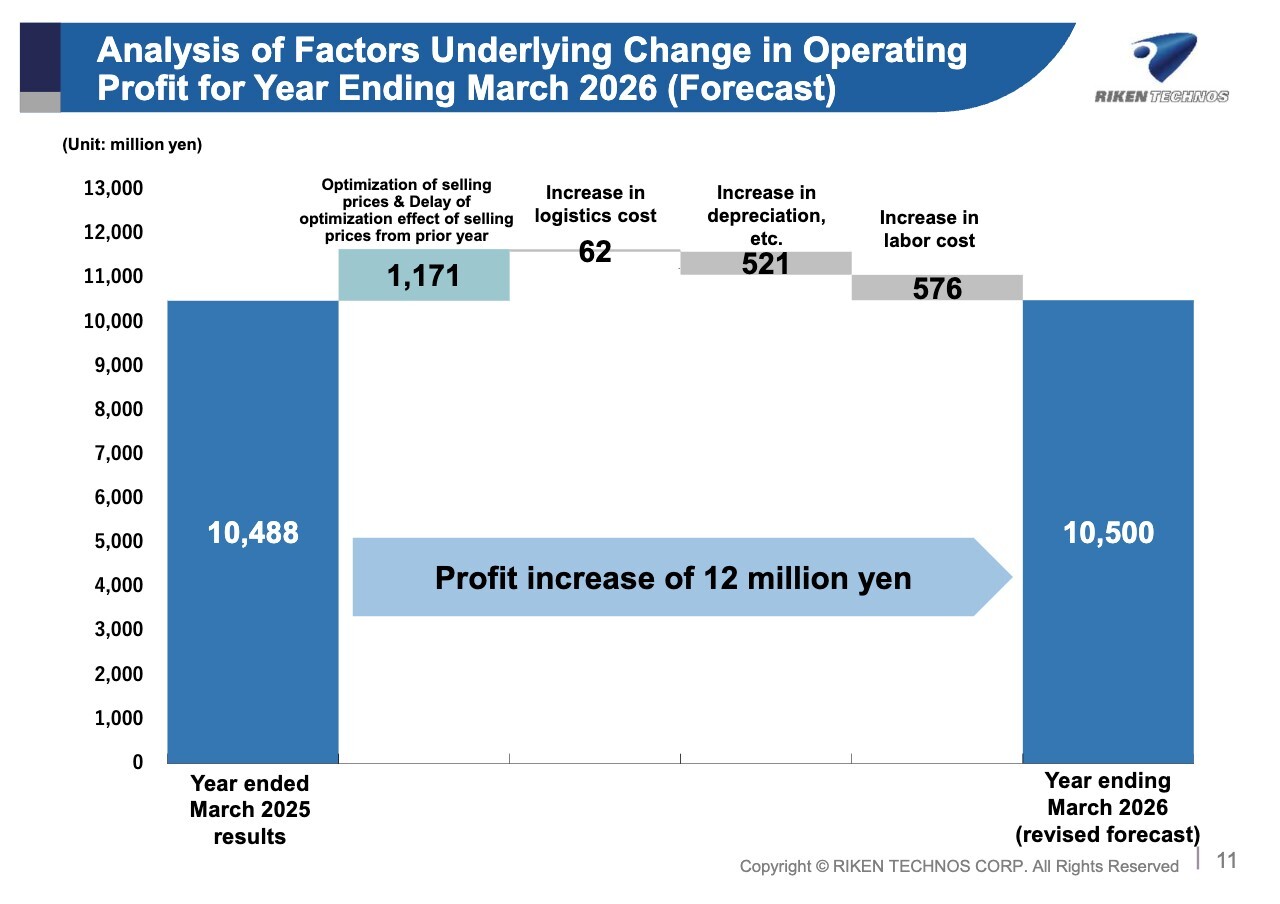

Analysis of Factors Underlying Change in Operating Profit for Year Ending March 2026 (Forecast)

Next, I’d like to present our full-year operating profit forecast, alongside an analysis of the factors contributing to the increase or decrease compared to FY2024. Operating profit for FY2024 was 10,488 million yen. Factors contributing to an increase include an expected 1,171 million yen gain from optimization of selling prices and the delay of the optimization effect of selling prices from the prior year. Factors contributing to a decrease include an increase in logistics costs of 62 million yen, an increase in depreciation, etc., of 521 million yen, and an increase in labor cost of 576 million yen. The net effect of these factors is an increase of 12 million yen, resulting in an operating profit of 10,500 million yen for FY2025.

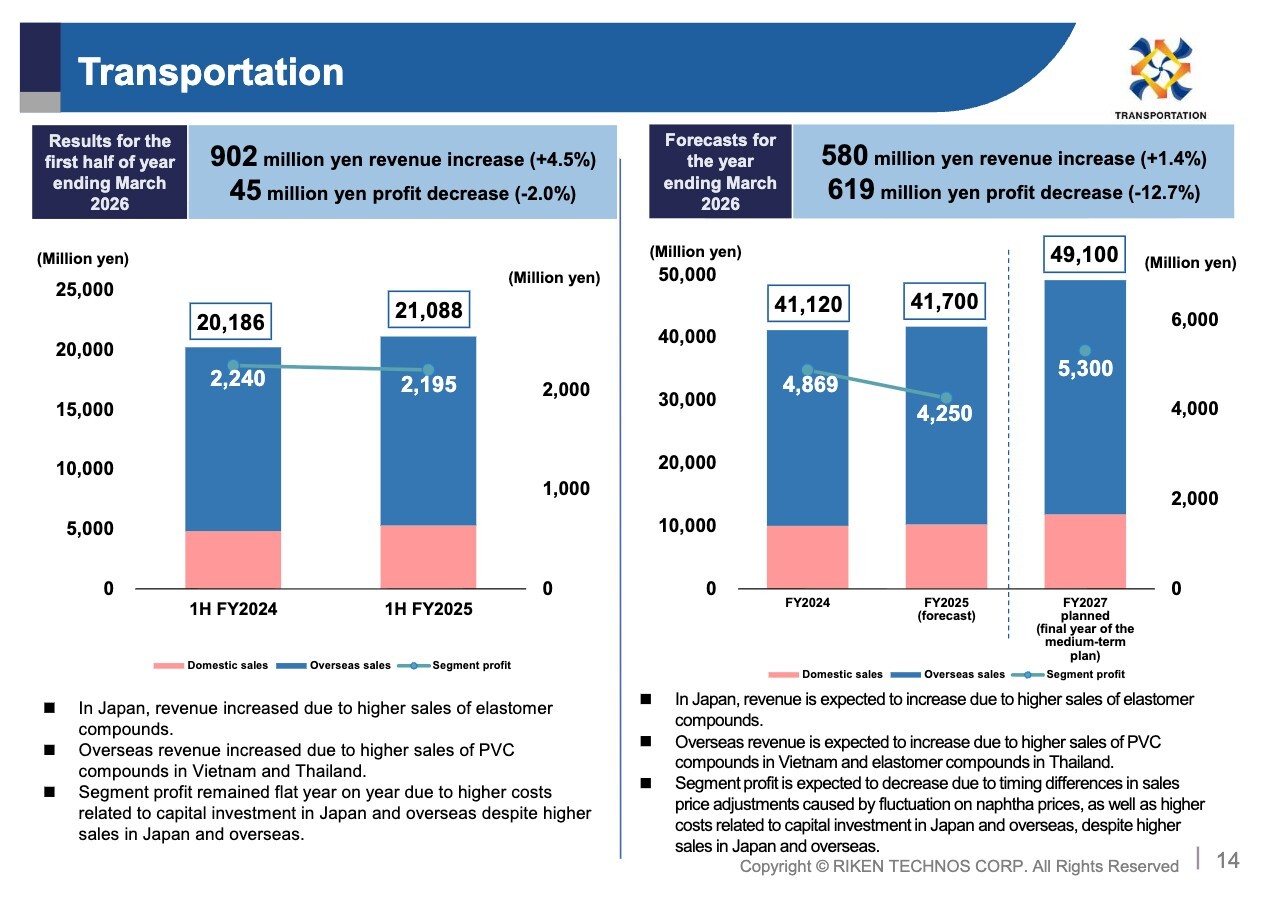

Transportation

Next, I’ll provide an overview of each segment. I’d like to first introduce the situation of the Transportation segment, which includes automobiles. For 1H FY2025, the Transportation segment recorded sales of 21,088 million yen, a YoY increase of 902 million yen, or 4.5%. Domestically, sales of elastomer compounds remained robust, contributing to growth in sales.

Overseas, sales increased due to higher sales of PVC compounds. Segment profit came to 2,195 million yen, a YoY decrease of 45 million yen. Although sales grew significantly, profit declined because depreciation expenses rose as a result of capital investments, leaving profit roughly in line with the previous year.

Regarding the full-year forecast for FY2025, net sales are projected to increase by 580 million yen YoY to 41,700 million yen. Segment profit is expected to decrease by 619 million yen YoY to 4,250 million yen. Although sales are expected to grow both domestically and internationally, profit is expected to decline due to rising depreciation, coupled with the impact of product price revisions and timing differences.

Transportation

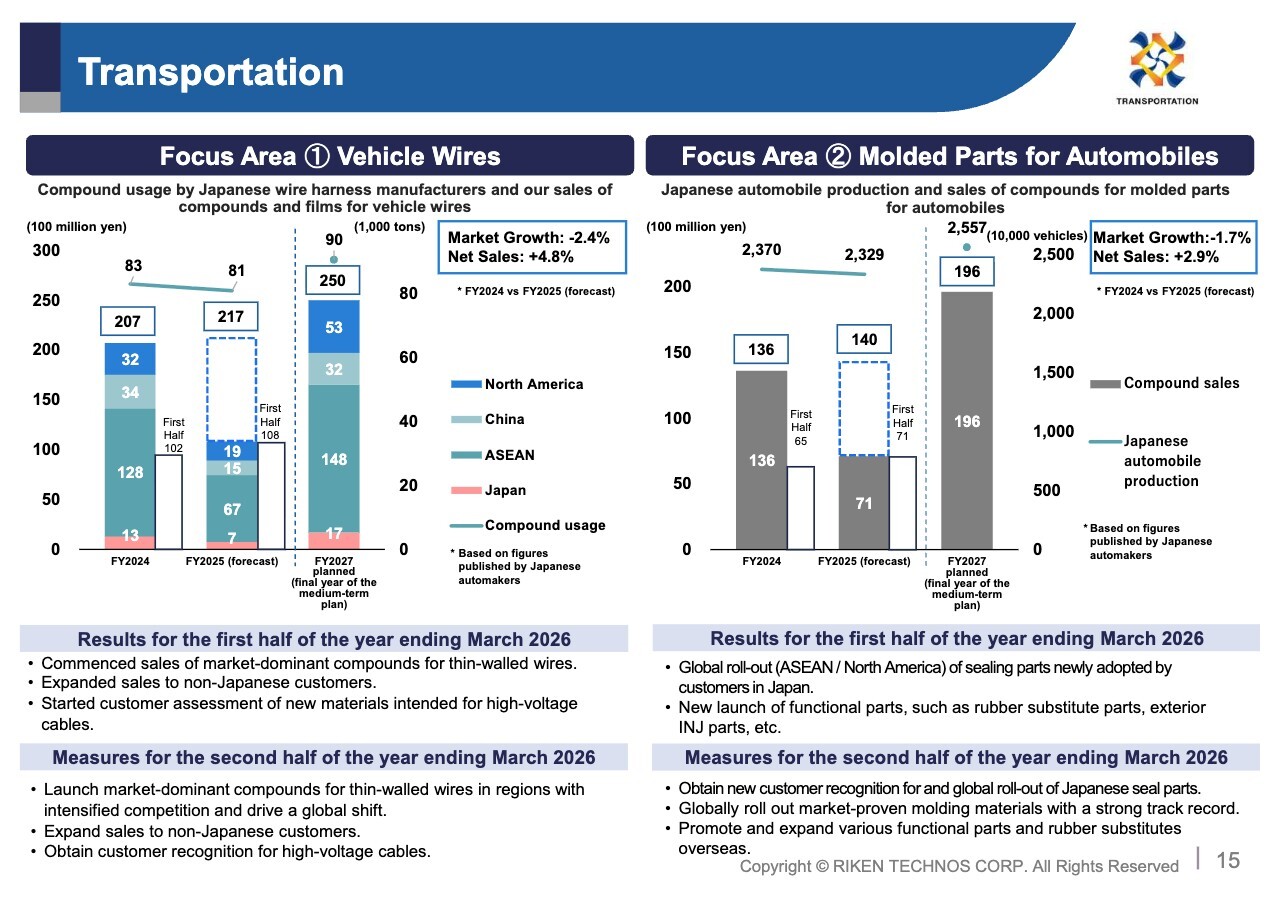

Next is the status of focus areas within the Transportation segment. First, I’ll explain the situation regarding vehicle wires, our first focus area.

Regarding the market situation, the projected compound usage volume by Japanese wire harness manufacturers for FY2025 is expected to decrease by 2.4% YoY, due to reduced automobile production.

Our sales of compounds and films in this segment are projected to reach 21,700 million yen, representing a YoY increase of 1,000 million yen. We’ll also expand global sales of our compounds for thin-walled wires, which offer strong market competitiveness by meeting automotive OEMs’ needs for lighter-weight components.

Additionally, we plan to expand sales to non-Japanese customers. We’ll also pursue new materials, such as high-voltage cables. The second focus area is molded parts for automobiles. Regarding market conditions, global automobile production by Japanese automakers is forecast to reach 23.29 million units in FY2025, representing a 1.7% decrease YoY. Our sales of compounds for molded parts for automobiles are projected to reach 14,000 million yen, a YoY increase of 400 million yen. We plan to globally roll-out our materials that are market-proven in Japan.

We plan to further promote rubber substitutes and expand sales of functional parts.

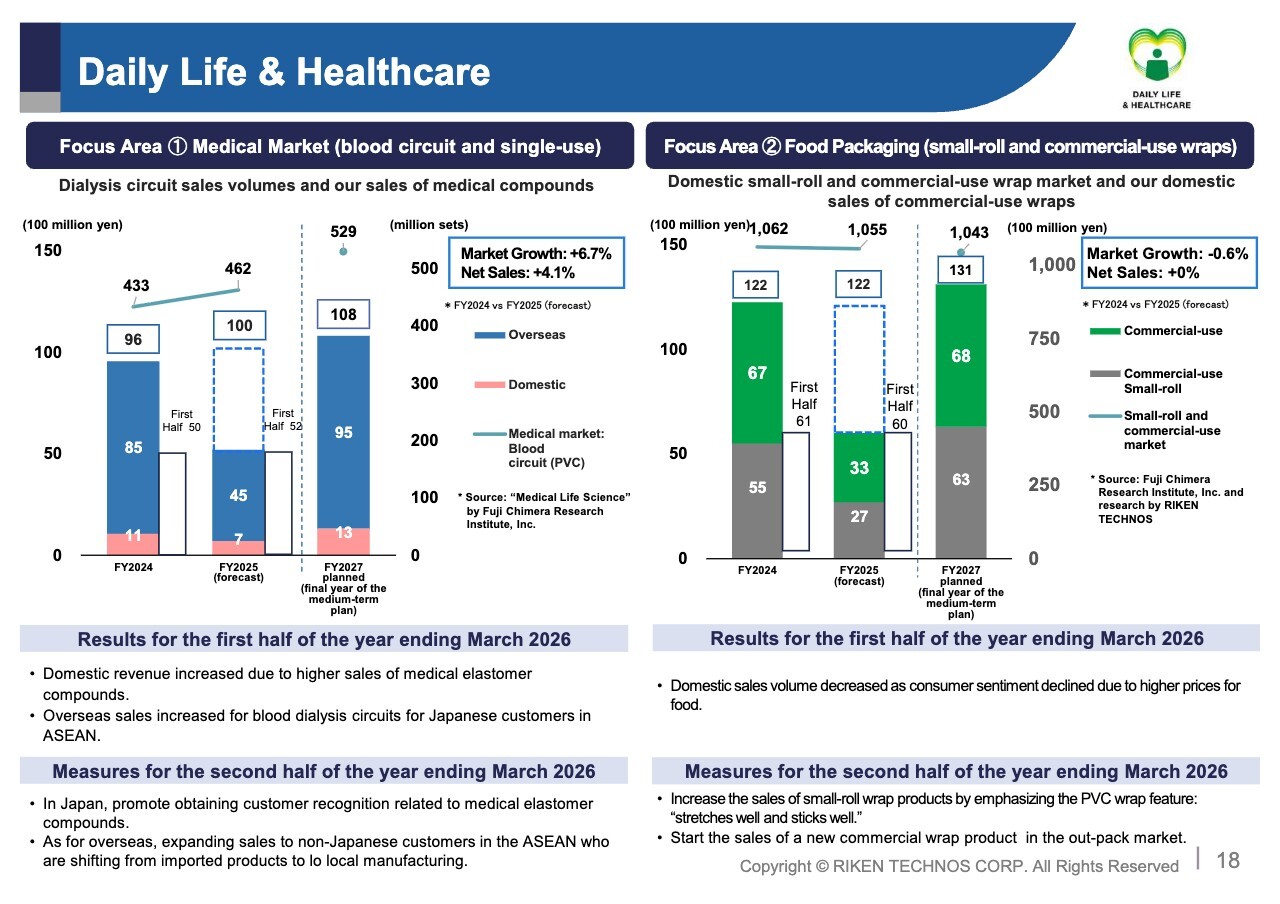

Daily Life & Healthcare

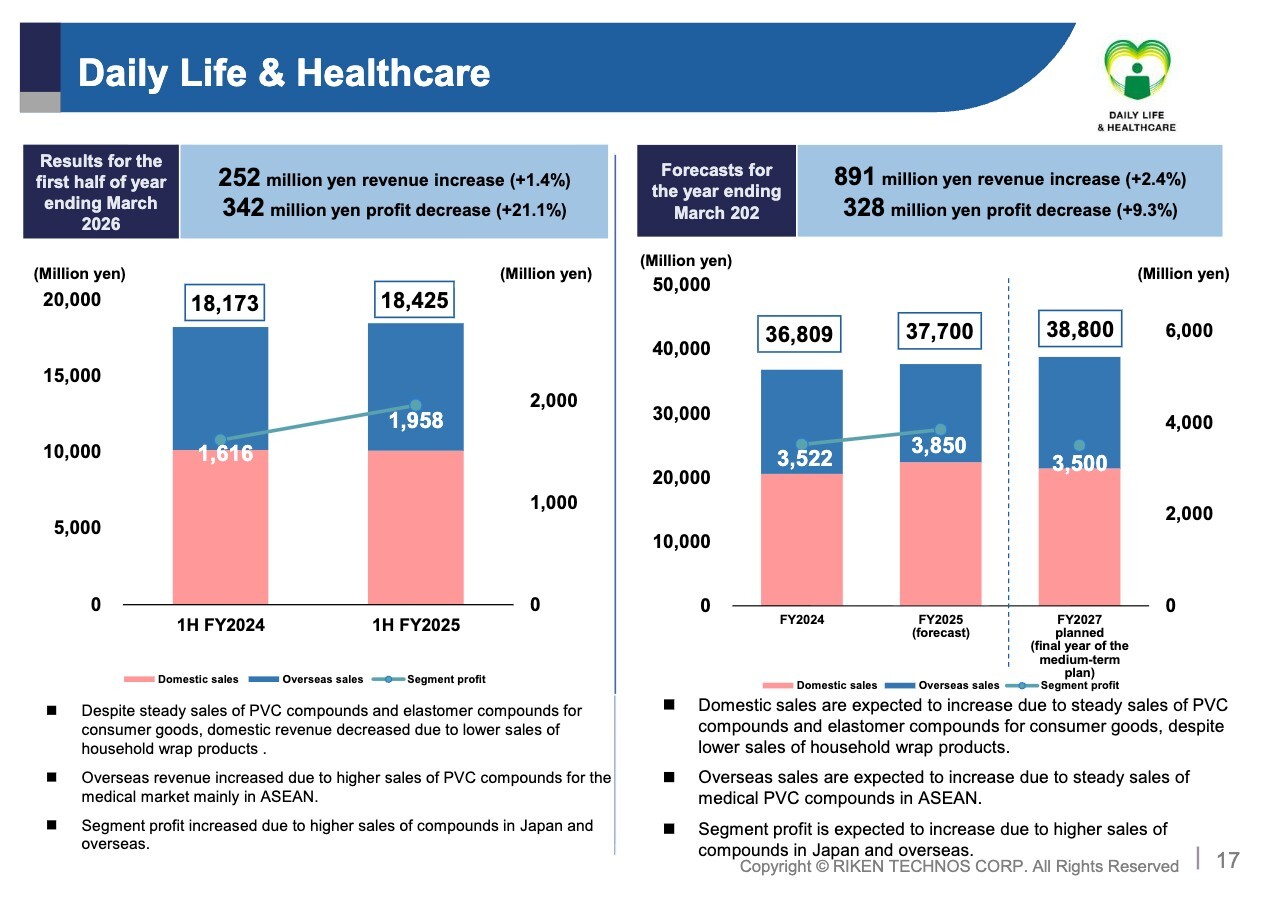

I’d now like to explain the situation for the second segment, the Daily Life & Healthcare segment. Sales for 1H FY2025 in this segment were 18,425 million yen, an increase of 252 million yen, or 1.4%, YoY. Domestically, despite steady sales of compounds for consumer goods, domestic revenue decreased due to lower sales of household wrap products. Overseas, however, revenue increased due to higher sales of PVC compounds for the medical market.

Segment profit was 1,958 million yen, a YoY increase of 342 million yen. Higher sales of compounds in Japan and overseas contributed to this profit growth. For the full year FY2025, sales are projected to increase by 891 million yen YoY to 37,700 million yen, with segment profit expected to rise by 328 million yen to 3,850 million yen. Segment profit is expected to increase due to higher sales of compounds both in Japan and overseas.

Daily Life & Healthcare

Next is focus areas within the Daily Life & Healthcare segment. The first of these is the medical market. Regarding the dialysis circuit market, our primary target in the medical field, we anticipate steady growth of 6.7% for FY2025.

Regarding our medical compounds, we forecast sales of 10,000 million yen for FY2025, which is a 400 million yen increase YoY. Domestically, we aim to increase sales of medical elastomer compounds. Overseas, we plan to expand the supply of compounds for blood dialysis to Japanese customers while also expanding sales to non-Japanese customers in the ASEAN region.

I’ll now explain the situation in the second focus area, small-roll and commercial-use wraps for food packaging materials. Regarding the overall market situation, for FY2025 as well, the domestic market for small-roll and commercial-use wraps is projected to see a slight YoY decrease. We expect our sales of small-roll and commercial-use wrap products to reach 12,200 million yen, nearly on par with the previous year.

Despite the decline in consumer sentiment due to higher food prices, we’ll proactively expand sales in the market for small-roll wrap products market by emphasizing the PVC wrap feature: “stretches well and sticks well.” We’ll also introduce new products for out-pack applications to drive sales growth in the commercial-use wrap market.

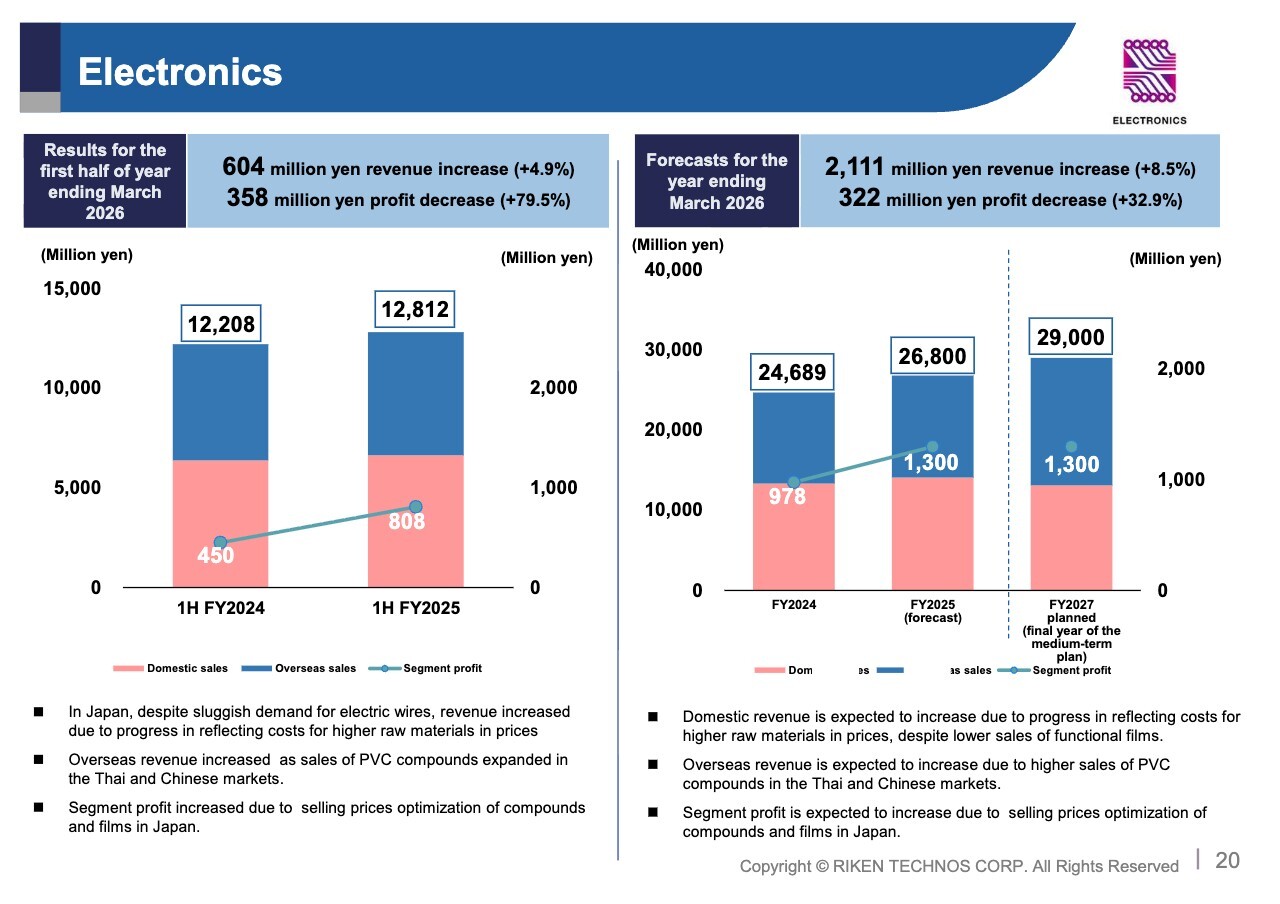

Electronics

Next, I’ll explain the third segment, the Electronics segment. For 1H FY2025, sales revenue in the Electronics segment was 12,812 million yen, a YoY increase of 604 million yen, or 4.9%.

In Japan, despite sluggish demand for electric wires, revenue increased due to progress in price optimization. Overseas revenue increased as sales of PVC compounds grew in the Thai and Chinese markets. Segment profit reached 808 million yen, a YoY increase of 358 million yen. Segment profit increased due to selling prices optimization of compounds and films in Japan. Our full-year forecast for FY2025 projects sales of 26,800 million yen, a YoY increase of 2,111 million yen.

Segment profit is projected to be 1,300 million yen, a YoY increase of 322 million yen.

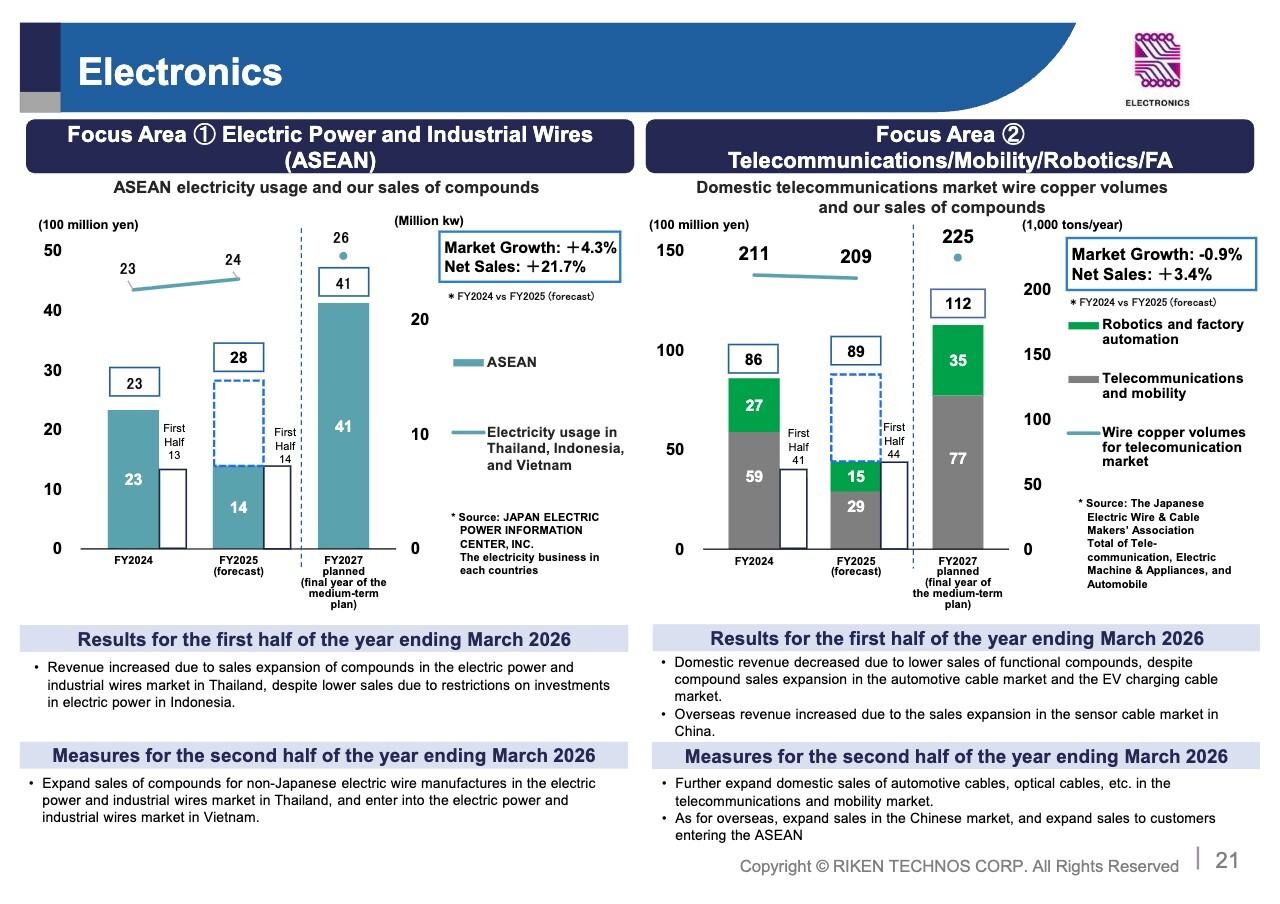

Electronics

Next, I’ll explain the focus areas for this segment. The first of these is electrical power and industrial wires in the ASEAN region. Regarding market conditions, electricity usage in the ASEAN region is expected to continue expanding steadily alongside economic growth. Regarding our sales of compounds in this market, we project 2,800 million yen for FY2025, aiming to achieve a 500 million yen increase YoY. We’ll further expand sales by meeting wire specifications in ASEAN countries and differentiating ourselves through performance and quality.

The second focus area is telecommunications/mobility/robotics/FA. Regarding market conditions, the telecommunications market is expected to continue growing significantly due to the establishment of new AI data centers.

Our sales of compounds in this market are projected to reach 8,900 million yen, a YoY increase of 300 million yen. Domestically, we’ll target the automotive cable and optical cable markets, while overseas we’ll expand sales in the Chinese market and advance sales growth in the ASEAN region.

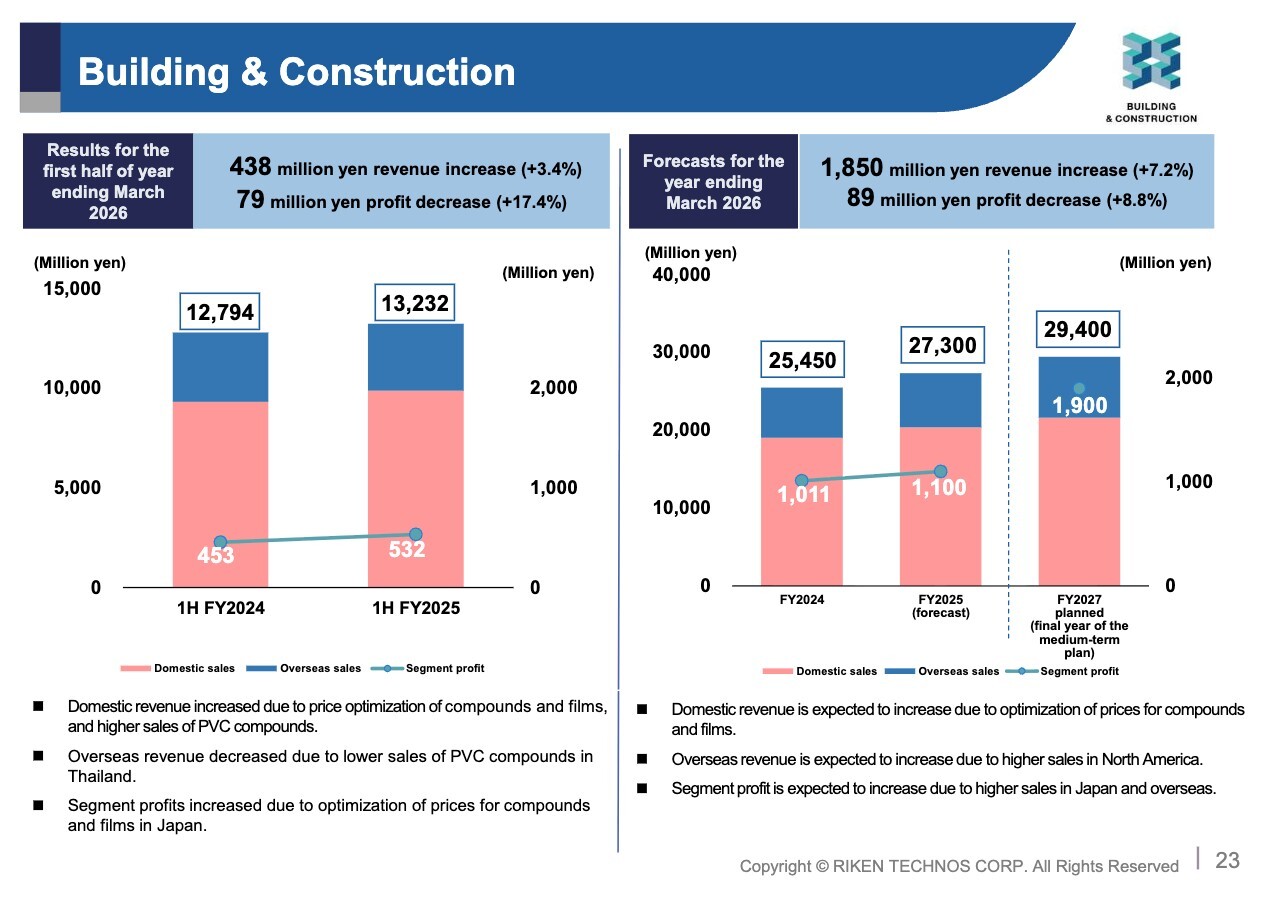

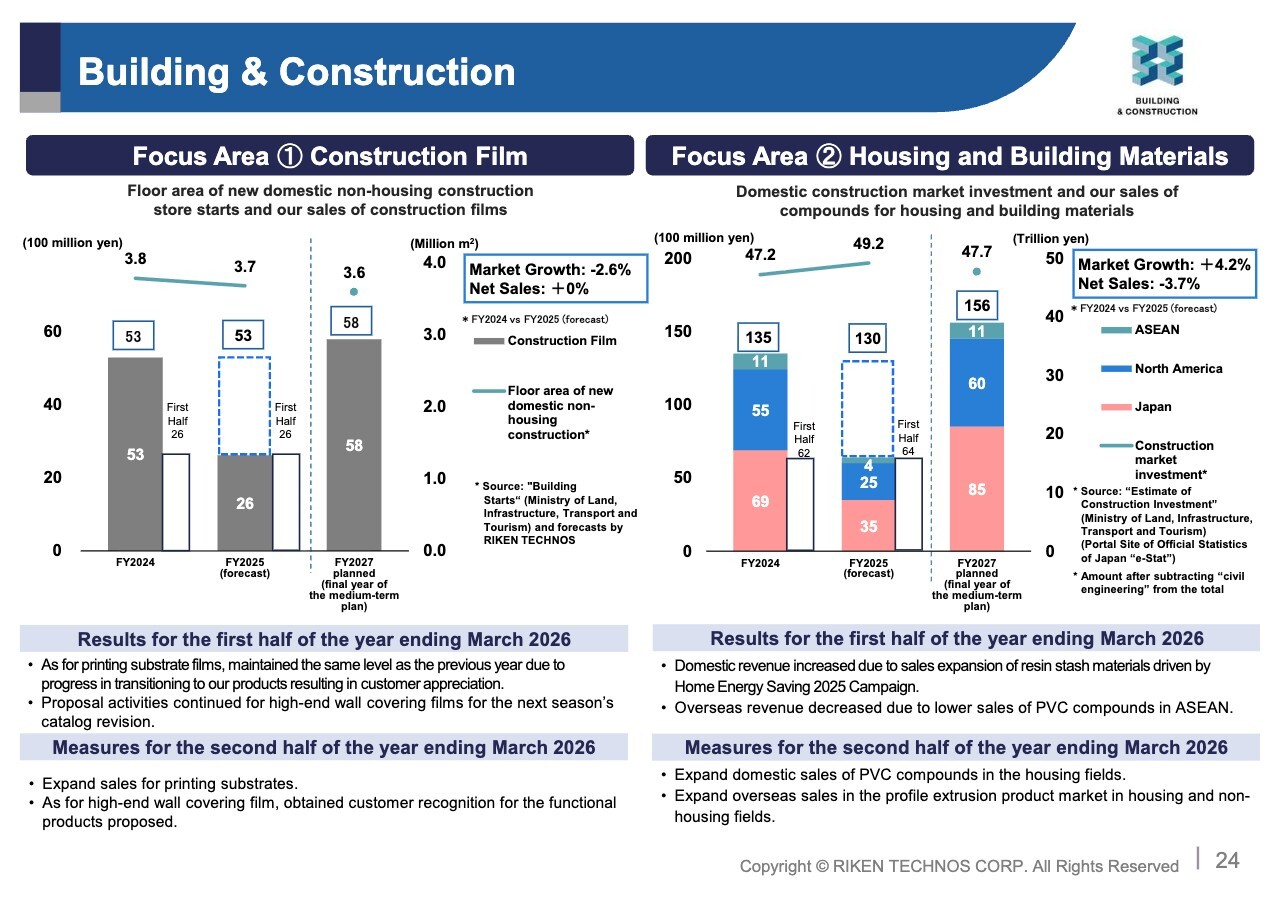

Building & Construction

Next, I’ll explain the situation in the fourth segment, the Building & Construction segment. For FY2025, sales in this segment amounted to 13,232 million yen, a YoY increase of 438 million yen.

Domestically, revenue increased due to price optimization as well as higher sales of PVC compounds. Overseas, however, revenue decreased due to lower sales of PVC compounds in Thailand. Segment profit was 532 million yen, a YoY increase of 79 million yen.

For the full-year FY2025, sales are projected to reach 27,300 million yen, a YoY increase of 1,850 million yen. Segment profit is forecast to be 1,100 million yen, a YoY increase of 89 million yen.

We’ll continue to expand sales both domestically and internationally.

Building & Construction

Next is the status of focus areas within the Building & Construction segment. The first area is construction film. Regarding market conditions, the floor area of new non-housing construction store starts in Japan is projected to decrease by 2.6% YoY.

In this market, we anticipate sales of our construction film to reach 5,300 million yen, remaining largely unchanged from the previous year. We’ll pursue further sales expansion by promoting substrate films with superior print characteristics and developing products that meet market needs.

Next, the second focus area is housing and building materials. Regarding the market situation, we expect to see a 4.2% YoY increase driven by the Home Energy Saving 2025 Campaign. We project that our sales of compounds for housing and building materials will reach 13,000 million yen, a YoY increase of 500 million yen.

Domestically, increased sales of resin sash materials are expected due to the impact of the Home Energy Saving 2025 Campaign. Overseas, we aim to expand sales of profile extrusion products.

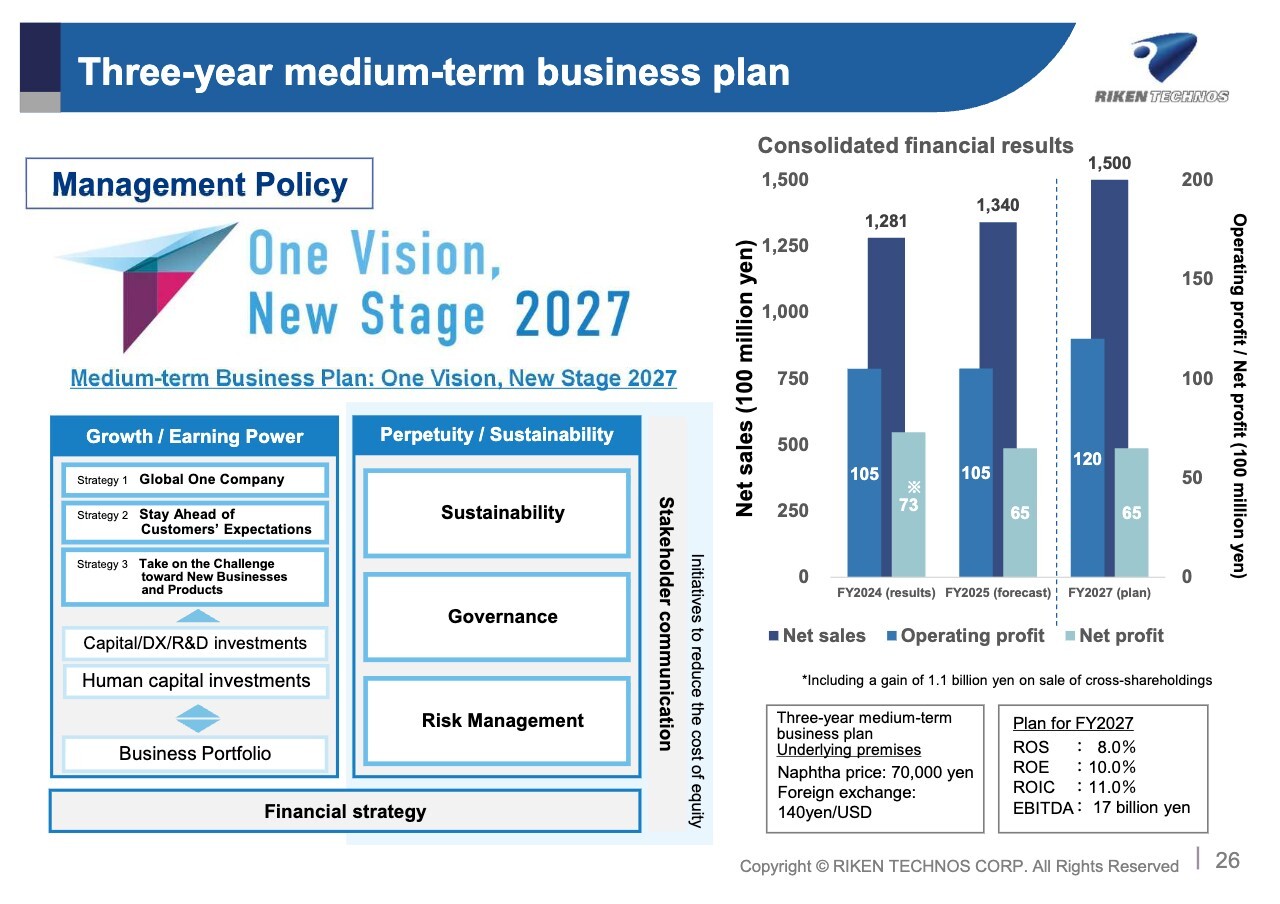

Three-year medium-term business plan

Next, I’ll explain the progress of our three-year medium-term business plan. Under the management policy “One Vision, New Stage 2027,” we launched the current three-year medium-term business plan this April. The plan focuses on two pillars: enhancing our earning power and sustainability.

We have identified three strategies to strengthen our earning power: Strategy 1, “Global One Company,” Strategy 2, “Stay Ahead of Customers’ Expectations,” and Strategy 3, “Take on the Challenge toward New Businesses and Products.” Additionally, to ensure the company’s long-term sustainability, we are committed to strengthening our efforts in sustainability, governance, and risk management. In terms of numerical targets, for FY2027, which is the final year, we’re targeting sales of 150,000 million yen, operating profit of 12,000 million yen, and net profit of 6,500 million yen. Please refer to the slide for the other numerical targets.

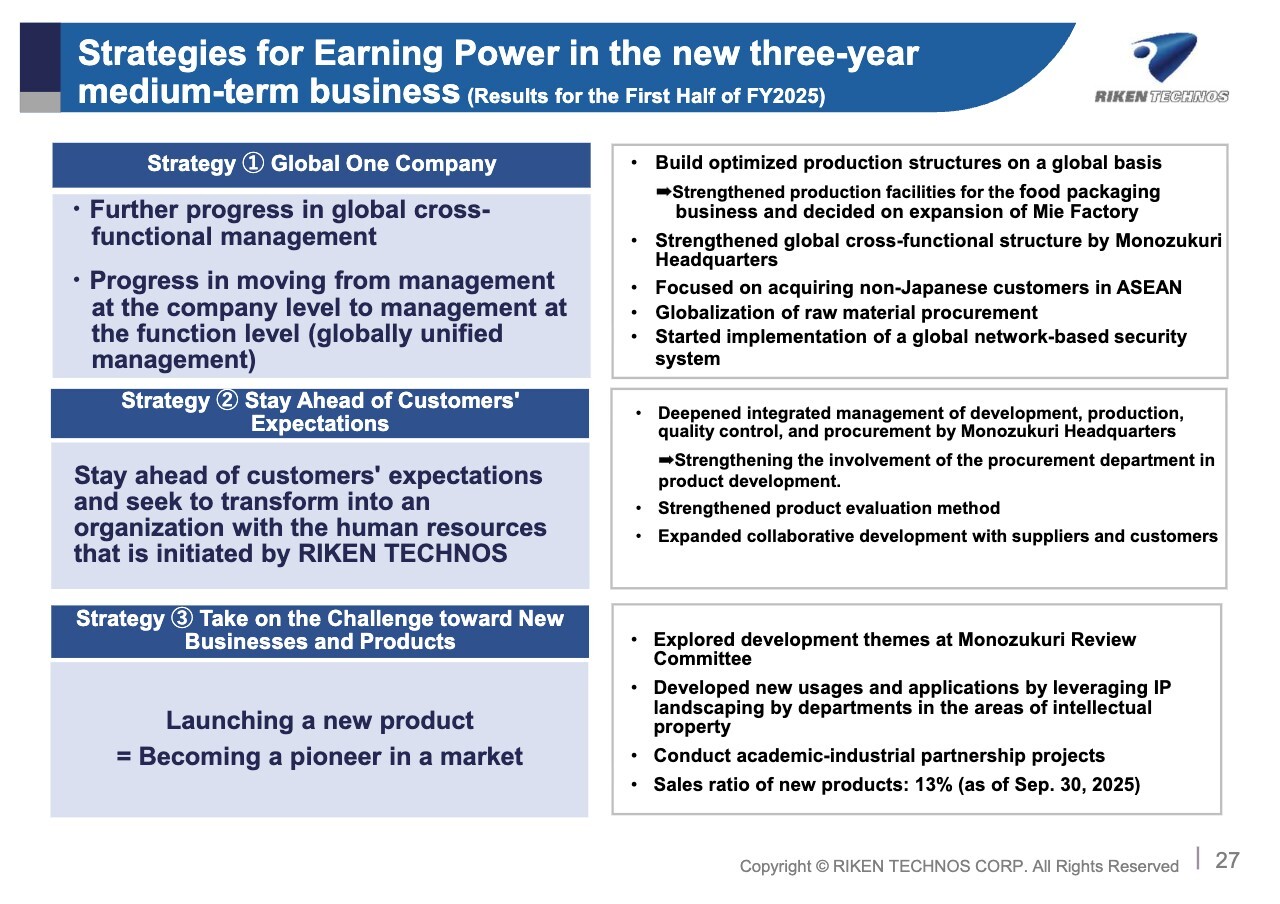

Strategies for Earning Power in the new three-year medium-term business (Results for the First Half of FY2025)

Next, I’ll explain the main developments resulting from our efforts in the first half of 2026 regarding the three strategies for earning power outlined in our medium-term business plan.

First, under Strategy 1, “Global One Company,” we’re building an optimized production structure on a global basis. Specifically, we’ve decided to strengthen the production facilities for our food packaging business and expand the Mie Factory. In the ASEAN region, our focus is on acquiring non-Japanese customers and further strengthening the globalization of raw material procurement.

Next, under part of Strategy 2, “Stay Ahead of Customers’ Expectations,” our Monozukuri Headquarters is working to strengthen our integrated global operations. We have strengthened the Procurement Division’s involvement from the product development stage. And we’re expanding collaborative development with suppliers and customers.

For Strategy 3, “Take on the Challenge toward New Businesses and Products,” we established the Monozukuri Review Committee to explore new development themes. We’re also working with departments in the areas of intellectual property to explore new applications using IP landscaping. Furthermore, we’re promoting industry–academia partnership projects.

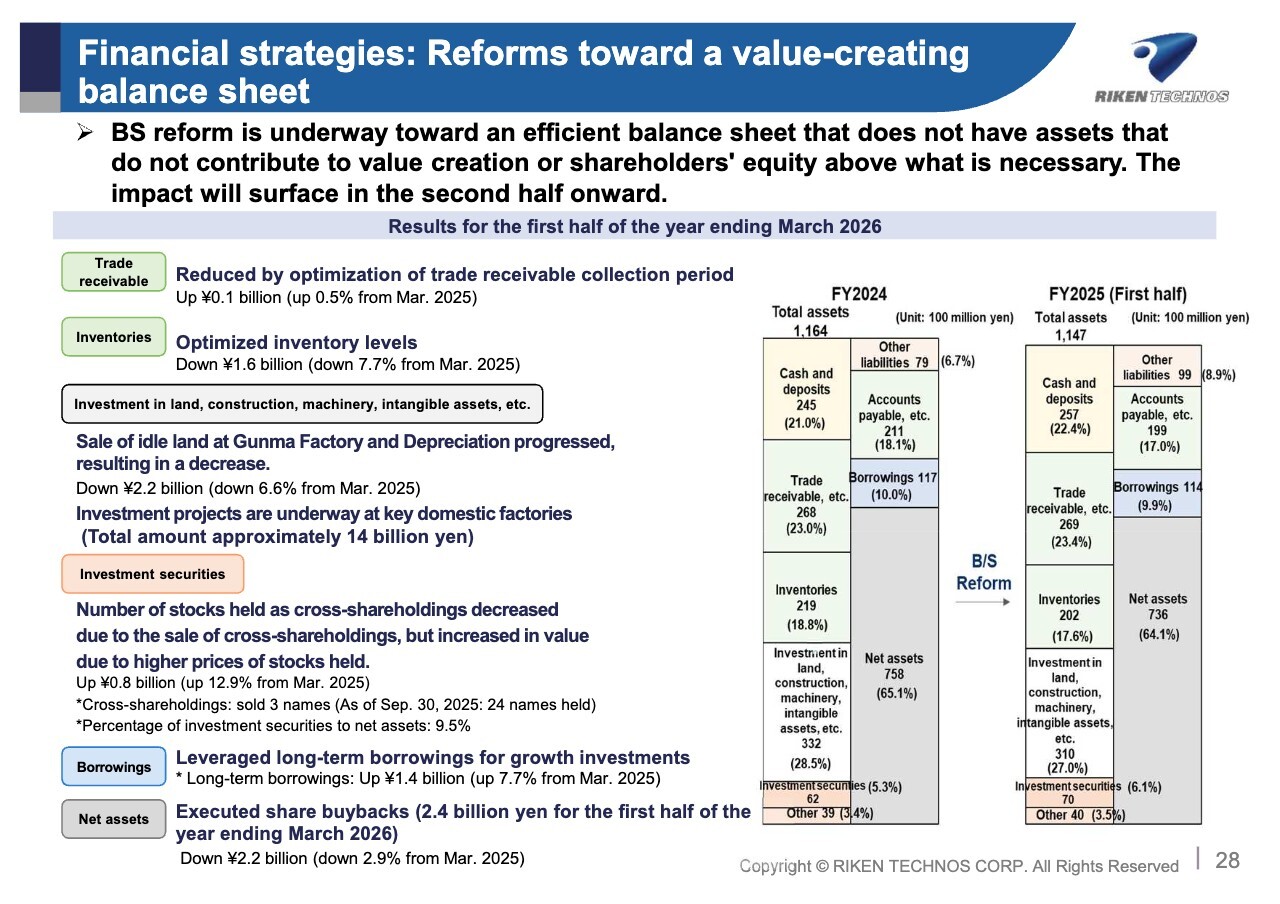

Financial strategies: Reforms toward a value-creating balance sheet

Let me explain our reforms toward a value-creating balance sheet. We are pursuing reforms aimed at building an efficient balance sheet that does not retain excess shareholders’ equity.

Now I’d like to present our results for 1H FY2025. We optimized accounts receivable collection periods and inventory levels, and sold idle land. Additionally, we’re advancing investment projects at our domestic factories. Regarding investment securities, we reduced holdings after verifying the rationale for retaining them. We’ll continue to reduce assets that do not contribute to value creation, generate necessary cash, and implement growth investments and shareholder returns.

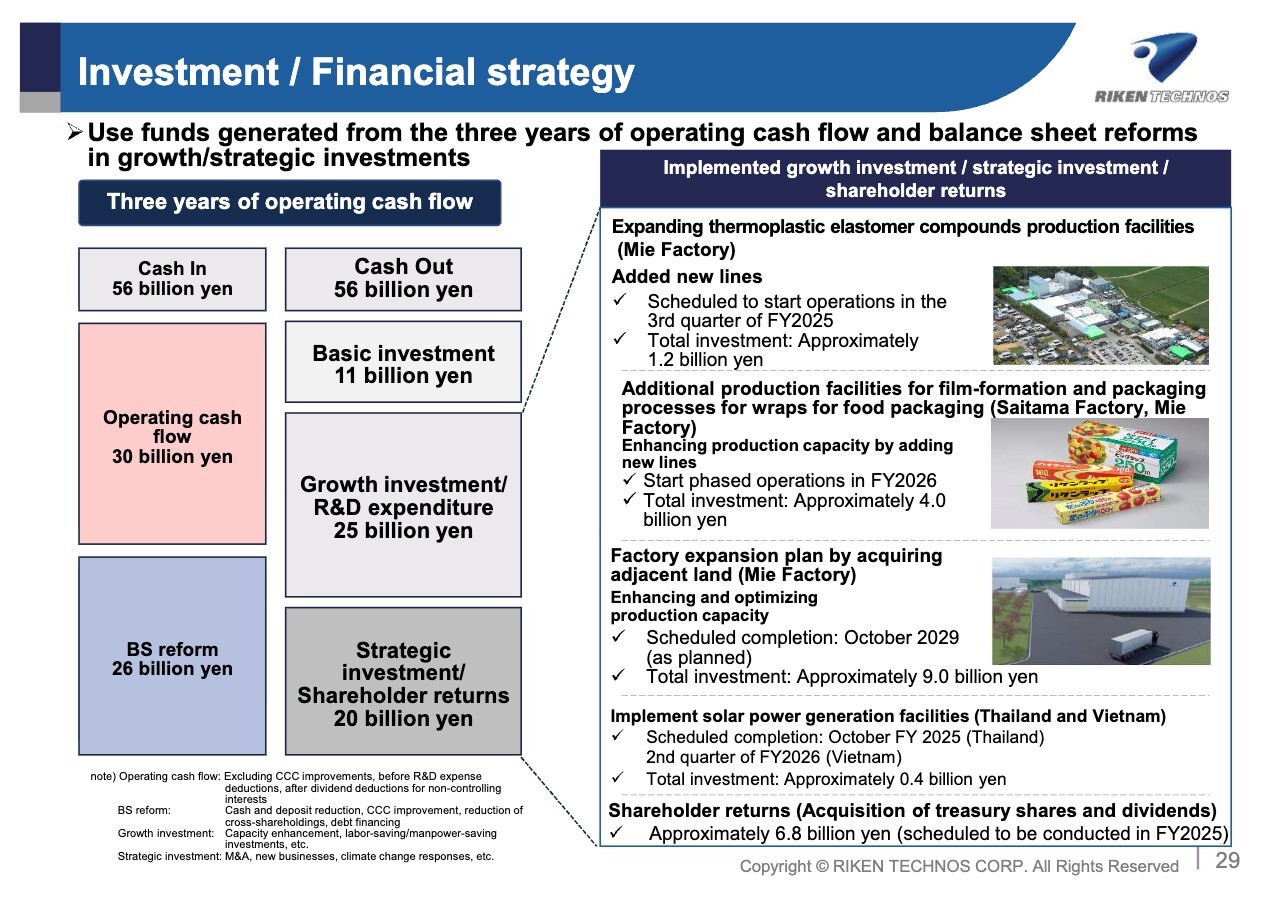

Investment / Financial strategy

Next, I’ll explain our investment and financial strategy. In addition to the operating cash flow generated over the three-year period of the current medium-term business plan, we’ll use funds created through balance sheet reform for capital investments, growth investments, R&D investments, strategic investments, and shareholder returns. Growth investments will include investments totaling approximately 4 billion yen for the addition of production facilities for film-formation in Saitama Factory and Mie Factory, and approximately 9 billion yen for the Mie Factory expansion plan.

In terms of shareholder returns, our plans include acquiring treasury shares and increasing dividends. We’ll also continue to actively pursue a variety of investments that support the enhancement of our earning power and the expansion of key business areas.

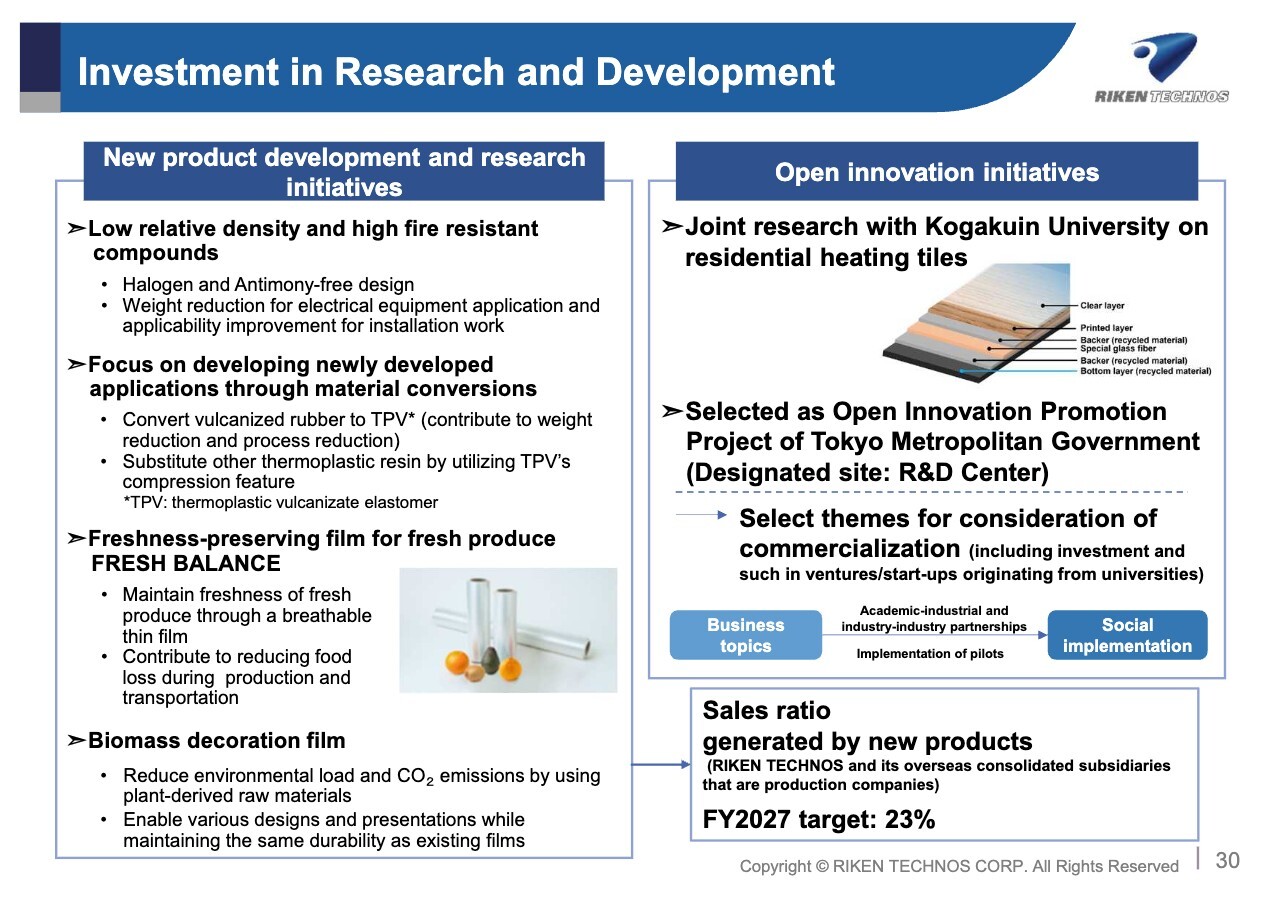

Investment in Research and Development

Next, I’ll explain our investment in research and development. Regarding new product development and research initiatives, in the compound field, we’re advancing the development of low-relative-density, high-fire-resistant compounds. Our focus is on developing new applications that draw upon the characteristics of elastomers, as well as promoting the shift from rubber to elastomer materials. In the film field, we’ve launched a freshness-preserving film called FRESH BALANCE. Development of biomass decoration film is also progressing.

Regarding our open innovation initiatives, the Promotion Department For Startup And New Business Creation is leading the way in advancing joint research with external organizations. Specifically, we’re working on selecting themes for business feasibility studies. By steadily implementing these initiatives, we’ll increase the sales ratio of new products.

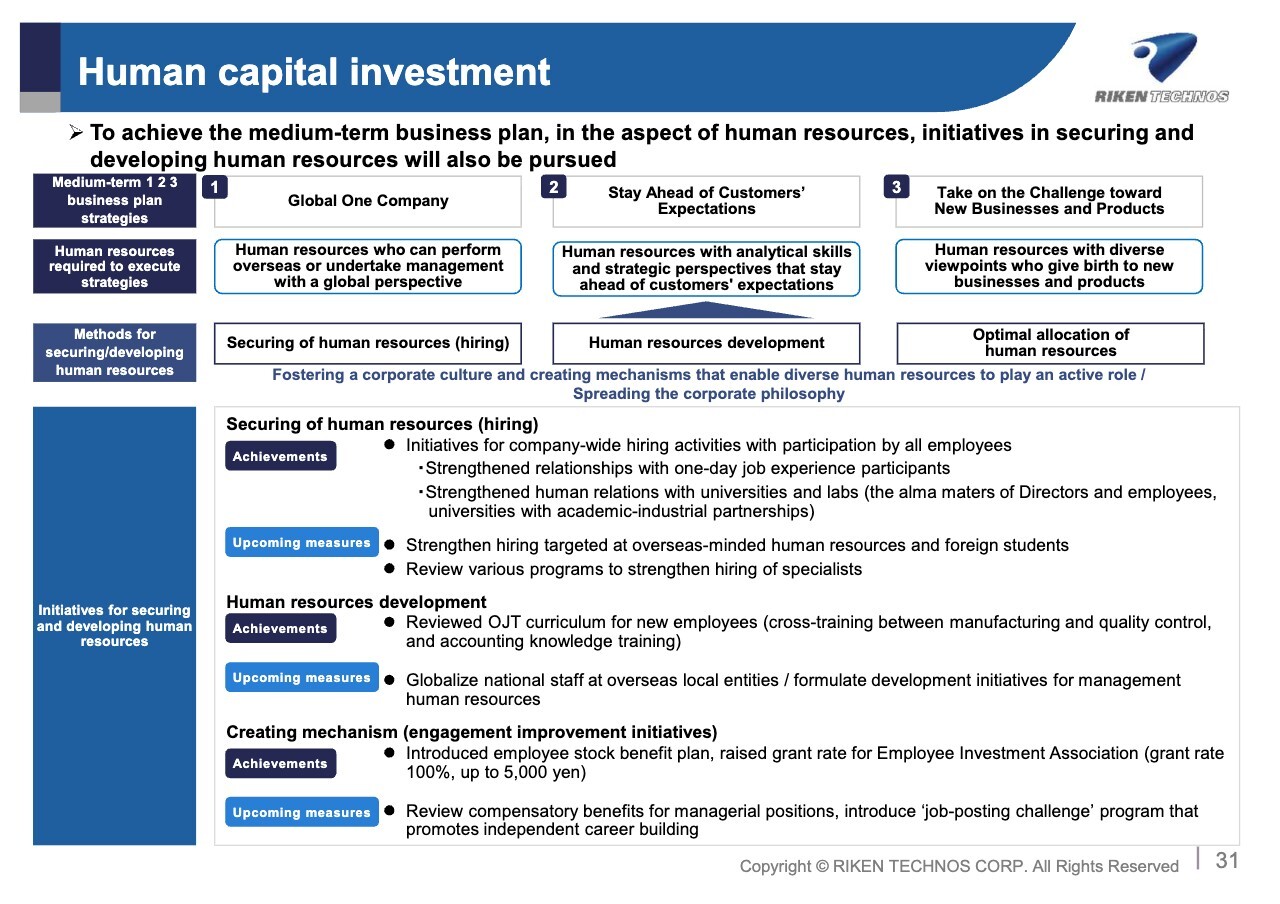

Human capital investment

Next is human capital investment. To ensure successful execution of our medium-term business plan strategies, we’re planning to advance initiatives to secure and develop human resources, making proactive investments. First, in terms of securing human resources, we’re undertaking company-wide hiring activities in which all employees participate.

Going forward, we’ll strengthen hiring of overseas-minded human resources and review various programs. In terms of human resources development, we’ve reviewed, revised, and reimplemented our on-the-job training (OJT) curriculum for new employees. We’ll also implement measures to develop national staff at overseas locations into management personnel.

To enhance engagement in support of these initiatives, we introduced an employee stock benefit program and increased the grant rate for the Employee Investment Association. Going forward, we’ll review compensatory benefits for managerial positions and introduce a program that promotes independent career building.

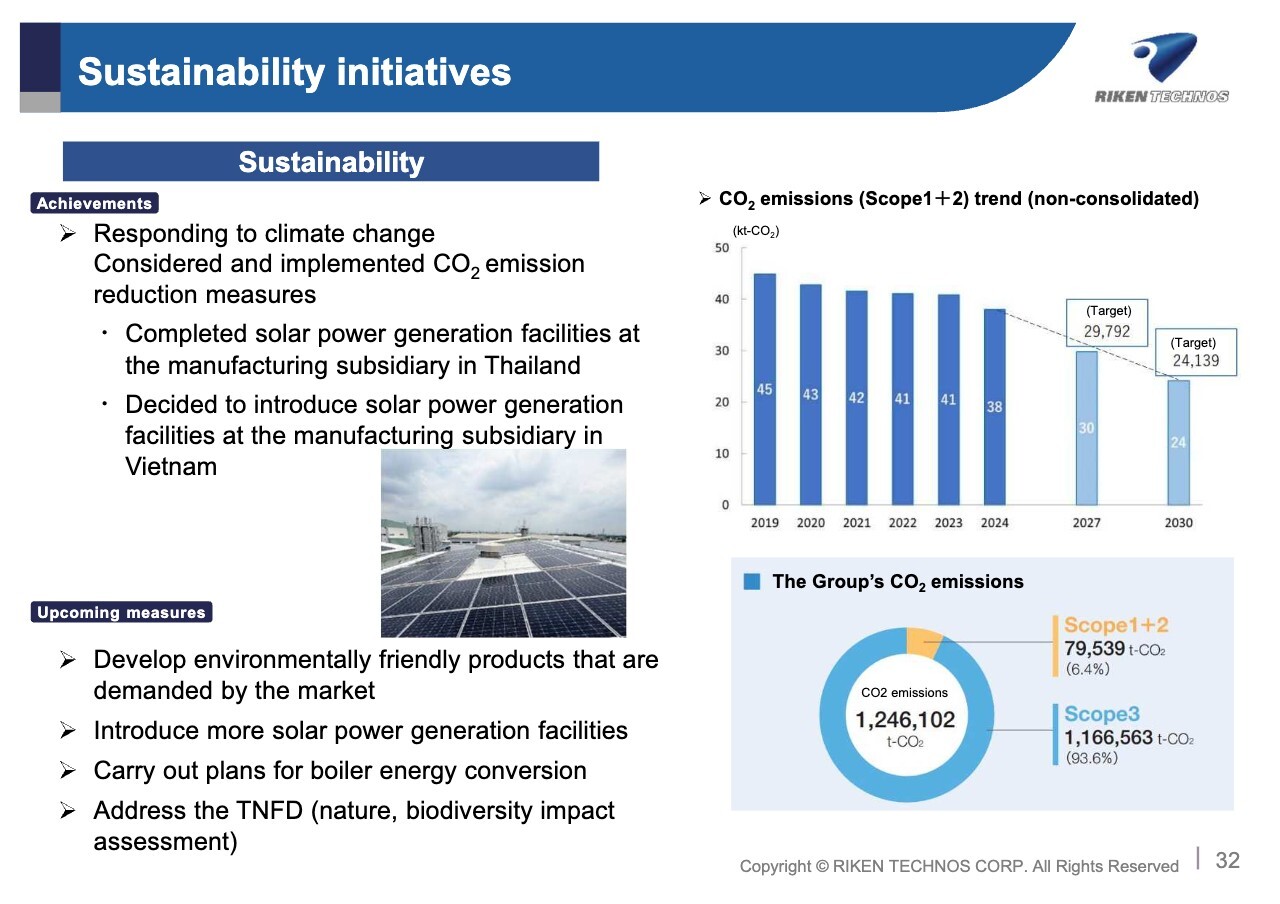

Sustainability initiatives

Next is an explanation of our sustainability initiatives. As part of our response to climate change, we have set targets to reduce CO2 emissions by 46.2% by fiscal 2030 and to achieve group-wide carbon neutrality by fiscal 2050. We’re examining and implementing various measures to meet these goals. This year, we’re introducing solar power generation at our manufacturing subsidiaries in Thailand and Vietnam. We’ll continue our efforts to reduce CO₂ emissions going forward.

Additionally, we’ll advance the development of environmentally friendly products demanded by the market, expand our disclosure of information, and further promote initiatives to raise employee awareness of sustainability.

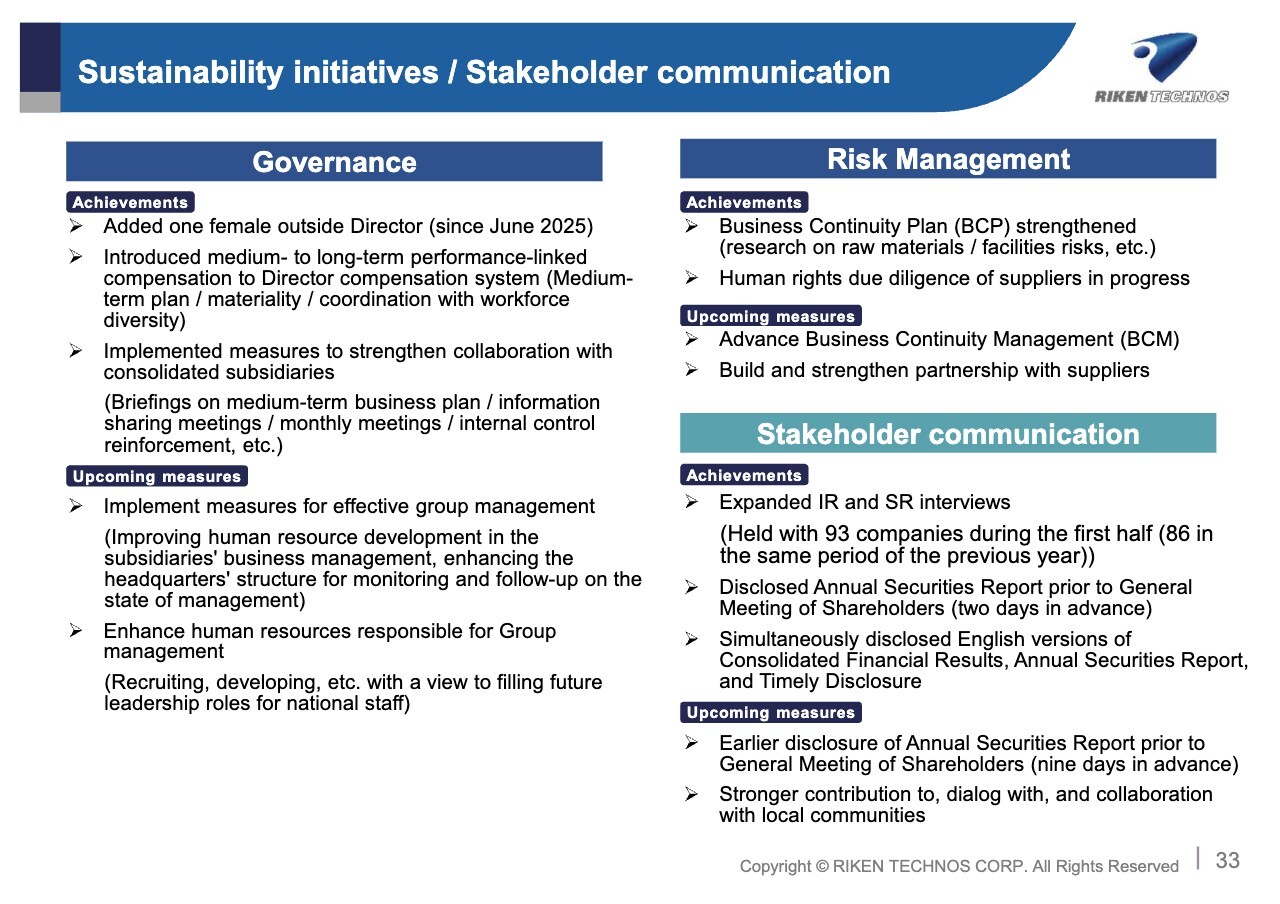

Sustainability initiatives / Stakeholder communication

Next, regarding governance. We increased the number of female directors and introduced medium- to long-term performance-linked compensation into our Director compensation system. We’re also implementing measures to strengthen collaboration with consolidated subsidiaries. We will continue to implement measures to improve the effectiveness of group management. We’ll also focus on developing human resources responsible for group management. In terms of risk management, we’re working to strengthen our business continuity plan (BCP) and human rights due diligence processes.

Going forward, we’ll work to strengthen partnerships with our suppliers. In our communication with stakeholders, we have expanded our IR and SR meetings. We also provide early disclosure of our Annual Securities Report ahead of the Ordinary General Meeting of Shareholders.

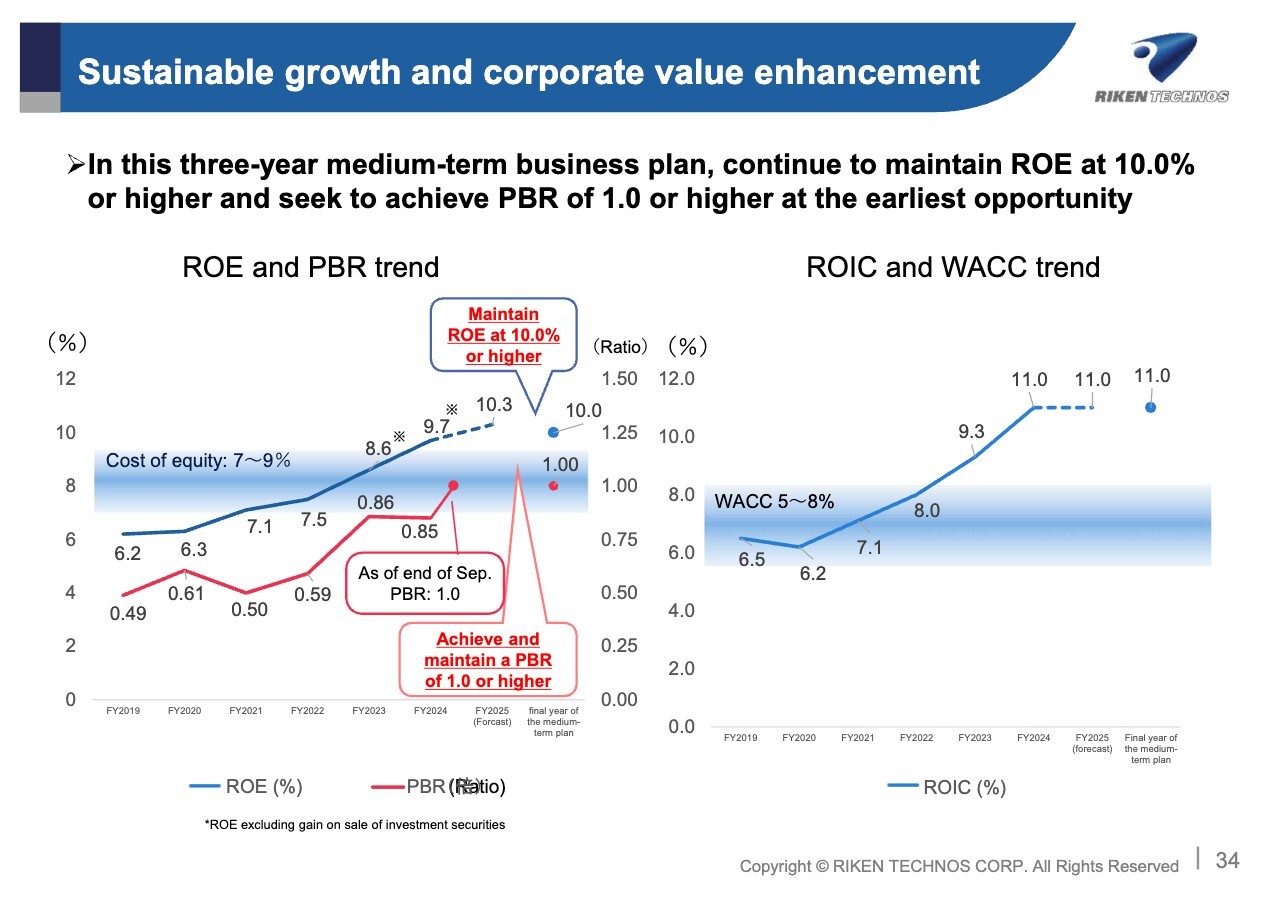

Sustainable growth and corporate value enhancement

By steadily executing these strategies, we will maintain an ROE of over 10% under the current three-year medium-term business plan. As for PBR, we have already achieved a level of 1.0 times or higher as of the end of September this year.

We intend to maintain and improve these levels. The trend for our company-wide ROIC and WACC is shown on the slide.

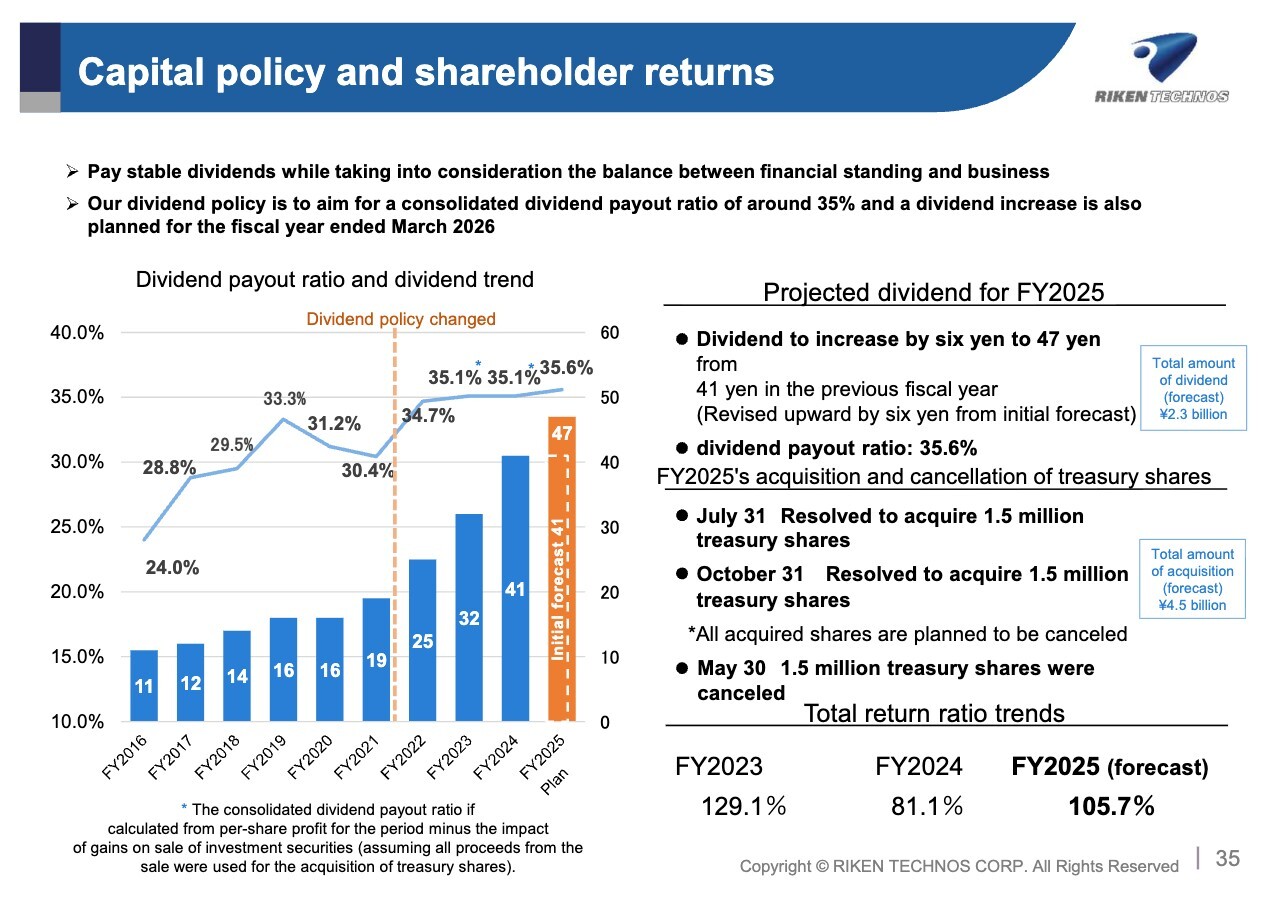

Capital policy and shareholder returns

Finally, I’ll explain our capital policy and shareholder returns. Our dividend policy aims for a consolidated dividend payout ratio of around 35%. The fundamental approach is to provide stable dividends while considering future business investments and the strengthening of our capital base. For FY2025, we plan to increase dividends further, targeting 47 yen per share, which is a YoY increase of 6 yen per share.

Additionally, we have resolved to repurchase a total of 3 million shares in July and October of this year. All repurchased shares are planned to be canceled. Taking into account the share repurchase, we anticipate a total payout ratio of 105.7% for this fiscal year. That concludes my explanation. Thank you very much for listening to the end.

In line with the “One Vision, New Stage 2027” business policy of our medium-term business plan, the RIKEN TECHNOS Group will continue to strive to become a leading company that provides comfort to all living spaces. Thank you for your kind attention.

Q&A Session: Current status of price revisions and future pass-through of raw material costs

Questioner: I believe you mentioned that price optimization has contributed to higher profits. Should we understand that the price revisions in question have already been completed? Also, could you explain whether there have been any recent changes in the supply–demand balance for raw materials that may require additional price pass-through?

Gakuyuki Kajiyama (hereinafter “Kajiyama”): My name is Gakuyuki Kajiyama, Director, Senior Managing Executive Officer, and Senior General Manager of the Sales & Marketing Division. Price pass-through was largely completed in the first half. currently taking place. While not on a daily basis, prices are rising due to ongoing price revisions and a tightening market. We’ll reflect these changes as they occur. Looking ahead to the second half, although the future remains uncertain, we intend to implement appropriate price adjustments as necessary.

Tokiwa: I’d like to add to this. It’s true that most of it is finished. However, if the price of special materials such as antimony oxide increases significantly, we’ll probably have to pass on the additional cost to future prices.

Also, for the Transportation segment, with regard to automobiles, we use naphtha price fluctuations. Therefore, when prices rise, the mechanism is designed to increase prices retroactively.

Currently, raw material prices are peaking and beginning to decline. The reason for the decline in profits is that, while we were able to benefit from rising raw material prices, selling prices are now beginning to fall.

Such a situation may occur again in the future. However, as one of our fundamental policies, when raw material prices rise, we carefully explain the situation to our customers and pass on the cost increase accordingly.

Q&A Session: Factors contributing to revenue decline in the U.S. market and future outlook

Questioner: In net sales by region, I believe the U.S. market saw a decline. Could you please explain the outlook going forward, and whether any measures need to be implemented to improve performance?

Tokiwa: First, as explained earlier, the yen has strengthened compared to the first half of the previous fiscal year. This has led to a decrease in revenue, including the impact of exchange rates.

Sales volume has remained largely unchanged. However, we consider the lack of change in sales volume to be problematic. Our market share of PVC compounds in the U.S. market remains at a mere 3–4%.

Therefore, much work remains to be done, and we’re currently implementing various measures to strengthen our sales capabilities based in the U.S.

Kajiyama: As mentioned earlier, we are expanding our capacity in the U.S. by adding new production lines. In terms of sales, we have four focus areas or segments. Among these, the Building & Construction segment is one of our strengths in the U.S., and we plan to further strengthen it. We’re advancing these initiatives globally.

Tokiwa: As reported in today's Nikkei, car sales in U.S. aren’t that bad, and the outlook doesn't seem pessimistic going forward. We plan to use this situation to steadily capture market share.

Junji Irie (hereinafter “Irie”): My name is Junji Irie, Representative Director, Executive Vice President, and Senior General Manager of the Administrative Division. For your reference, I’ll touch on foreign exchange rates. In 1H FY2024, the U.S. dollar averaged 152.33 yen. In contrast, 1H FY2025 saw the yen strengthen to 149 yen.

However, on a global scale, the Thai baht has moved in the direction of yen depreciation. Focusing solely on the U.S., yen appreciation has resulted in reduced sales and profits.

Regarding this fiscal year's earnings forecasts, calculations are based on an exchange rate of 149 yen. However, recent movements show yen depreciation, ranging from 153 to 155 yen. Therefore, revisions or adjustments may be necessary toward the end of the fiscal year due to the impact of exchange rates.

Q&A: Boiler fuel conversion plan and GHG reduction at Saitama Factory

Questioner: One of the upcoming measures listed in the slide is “Carry out plans for boiler energy conversion.” Could you explain, to the extent possible, where specifically the conversion will occur, what will be converted from what, and by how much GHG emissions will be reduced?

Tomozo Ogawa (hereinafter “Ogawa”): My name is Tomozo Ogawa, Managing Executive Officer and Senior General Manager of the Monozukuri Headquarters and the Procurement Division. While still in the planning stage, we are considering proceeding with fuel conversion for the boilers at Saitama Factory. Specifically, we plan to switch from heavy oil to natural gas.

Regarding the investment scale, we anticipate spending around 500–600 million yen, although some aspects still require detailed review. We believe this plan could enable annual CO2 reductions of around 1,200–1,300 tons. However, we’re still in the process of thoroughly reviewing the plan.

Questioner: Is it correct to understand that this will be completed within the timeframe of the medium-term business plan?

Ogawa: We plan to implement this during the period of this medium-term business plan.

Tokiwa: We’ll make the implementation decision within this fiscal year, but completing all related work, including construction, will take about another two years. We expect the timeline to be just manageable. We’ll make the decision soon, but we envisage starting construction in about a year's time.

Q&A Session: Expansion plan for production facilities for wraps for food packaging

Questioner: Regarding your capital investment plan, I understand that the production capacity for wraps for food packaging is being expanded at both Saitama Factory and Mie Factory. May I assume that this involves adding further film production lines for wraps at both locations?

Tokiwa: That’s correct. This is currently underway, and elastomer production lines will be introduced around December. After that, we’re introducing film production lines and subsequent rewinding facilities at both Saitama Factory and Mie Factory for the plastic wrap.

Questioner: Should I assume that one line will be added at each plant?

Tokiwa: We’re unable to provide specific numbers regarding the number of production lines. However, for the film production lines and small-roll lines, we plan to significantly expand capacity rather than adding just one line. We have plans to substantially enhance our facilities.

Irie: It is not simply a matter of adding new lines. Another challenge is that production facilities at each factory have been in operation for about 50 years, incurring significant overhaul costs.

Therefore, we’re introducing the latest facilities to enhance production efficiency and achieve labor-saving and manpower-reduction.

Although introducing new facilities will increase depreciation expenses under the straight-line method, it’s expected to reduce overhaul costs. For our facilities, which have an eight-year depreciation period, profits are projected to turn positive once this period has ended. This approach aims to deliver dual benefits. First, it should increase production capacity and decrease labor and manpower requirements. On the other hand, it will improve energy efficiency and reduce CO2 emissions.

At Saitama Factory, we’re advancing initiatives to hire women as skilled production workers. Manufacturing sites have traditionally been perceived as male-dominated workplaces, with facilities such as locker rooms and baths often limited to a single unit. We have now addressed this issue, creating a more comfortable working environment for female employees.

Additionally, while setting large rolls of wrap (20 kilograms) onto machinery can sometimes be difficult for women's strength, current facilities allow for the use of assistive devices, enabling handling without the need for significant physical strength.

We’ve already introduced one such facility at Saitama Factory, and we’re advancing efforts to create a more comfortable working environment for women by incorporating such facilities. We’re developing plans based on the principles of diversity and inclusion (D&I).

Questioner: So that means it includes replacements as well as simple additions. I understand. Thank you.

Q&A Session: Competitive landscape and the advantages of data center products

Questioner: Regarding wires for data centers, given characteristics like heat radiation, would it be difficult for local Chinese companies to replicate them? Or, if there are competitors, could you tell us who they are?

Kajiyama: Various wire types are used for data centers. This is particularly true in fields requiring extremely high reliability, such as optical applications as well as heat and pressure resistance. Japanese manufacturing excels in this area, and it's not limited to cables.

Therefore, we believe we’re competitive against overseas players, or overseas companies—although I don’t intend to single out China. Furthermore, our compounds are also made in Japan, which we see as an advantage.

However, there are also domestic rivals. Although we originally specialized in manufacturing PVC compounds, we now handle various materials, ranging from PVC to elastomers. In contrast, rival manufacturers focus on olefin-based compounds rather than PVC.

Therefore, we’re advancing our business by competing with manufacturers handling olefin compounds—that is, by focusing on the moldability and performance of our compounds.

Questioner: Against olefin compounds, where do you see your advantages and disadvantages?

Kajiyama: Flame resistance. Olefins lack flame resistance, whereas PVC possesses it. To address this challenge, flame resistant materials are used. Antimony is one of the excellent flame resistant materials, but its price has skyrocketed recently.

While I’m unable to share the technical details, we’re advancing a strategy to improve flame-resistant technology for differentiation and to establish a competitive advantage in this field.

Questioner: May I understand correctly that price pass-through is possible due to the flame-resistant properties?

Kajiyama: Yes, that’s correct. As a company that specializes exclusively in compounds, we add various functionalities to our products, not limited to flame resistance.

Questioner: Could you elaborate on “various functionalities?”

Kajiyama: For example, voltage resistance capabilities.

Our performance against voltage is excellent. Although the wires are primarily designed for indoor use, they are sometimes used in outdoor cable installations as well as inside the data centers, so they require weather resistance. Furthermore, while our competitors mainly handle olefins produced in large-scale plants, we specialize in compounds and can offer custom solutions.

This difference could be advantageous or disadvantageous, and we carefully evaluate these factors when proceeding with development.

Q&A Session: Expanding resin compound capacity at the Mie Factory and future plans

Questioner: I have a few follow-up questions about slide 29. The first concerns the capacity expansion for resin compounds in Mie. While this investment involves acquiring new land, could you please explain whether there are plans for further expansion after the scheduled 2029 completion, and what the blueprint for that expansion looks like.

Tokiwa: This year, we’ll introduce a TPE compound manufacturing line at the Mie Factory through a scrap-and-build process, with operations set to begin in December. However, this investment will leave us with a significant shortage of space at Mie Factory.

When considering further expansion, we envisage shifting our focus from rubber products to elastomers, and being able to handle various materials. However, we believe that adding more production facilities would be challenging.

Therefore, although we considered reconfiguring the layout of Mie Factory, our plan is to acquire adjacent land, expand the factory, and construct a new building there to house the production lines. This project is scheduled to begin with land preparation and construction of the new building in 2029. Although it’ll take some time, we’ll determine which lines to install as the project progresses.

Furthermore, as Executive Vice President Irie explained earlier, it is challenging to secure sufficient personnel as we pursue efficiency across all operations. Therefore, we plan to advance labor-saving measures and introduce various equipment, while also consolidating warehouses to this location if feasible.

However, although we have some plans in place, we intend to spend the next one to two years specifically examining how to make use of this land in future.

Questioner: The area is 30,000 square meters. Am I correct to understand that not all of this will be filled from the outset?

Irie: The 30,000 square meters are subject to certain legal restrictions. When expanding the current Mie Factory, the upper limit is 0.5 times the existing site area. The current Mie Factory site covers about 62,000 square meters. Multiplying this by 0.5 gives us approximately 30,000 square meters. After extensive discussions with the administrative authorities over the past two years, it was determined that 30,000 square meters is the maximum area that can be secured this time.

Tokiwa: In answer to the question just raised about whether everything will be filled from the outset, that’s not the case. We envisage constructing the building, securing space for several lines within it, and then sequentially introducing new lines.

Questioner: By the way, when it comes to expanding the production of this resin compound, can we understand this to mean specifically an elastomer compound?

Tokiwa: There are various factors involved, but at this point, your understanding is correct in terms of our expansion concept. However, as I mentioned earlier, due to the difficulty of securing enough personnel, we also need to discuss which production system would be optimal.

Therefore, we’re considering using other materials as well. For the current expansion, though, it’s definitely TPE, that is, thermoplastic elastomer compounds.

Q&A Session: Investment plans and production capacity for food packaging wrap

Questioner: Regarding the investment in wraps for food packaging, I understand that operations are scheduled to begin sequentially starting in fiscal 2026. May I assume that all of the additional facilities will be operational within fiscal 2026?

Ogawa: Starting in fiscal 2026, we plan to sequentially introduce several facilities at both Saitama Factory and Mie Factory. We plan to introduce the facilities between 2026 and 2027, bringing them online sequentially.

Questioner: So, ultimately, this investment will be completed by fiscal 2027. Would that be correct?

Ogawa: Yes. We plan to commence operations over a three-year period starting in 2026.

Questioner: You have factories in China and Nagoya. Am I correct to understand that there are currently no plans for these factories?

Tokiwa: At this point, there are no plans. However, regarding China, we sell a significant volume to Japan. Given the current low cost of raw materials in China, production there remains profitable even when transportation costs are factored in. That said, determining the optimal structure following the expansion is still under consideration.

Questioner: Could you tell me specifically how much the investment this time around will increase production capacity?

Tokiwa: Please accept my apologies, as we refrain from disclosing the number of production lines or production volumes outside our company. We hope you understand.

Q&A Session: Tokyo Metropolitan Government's Open Innovation Promotion Project and restructuring of R&D framework

Questioner: Regarding your selection for Open Innovation Promotion Project by the Tokyo Metropolitan Government, I recall that during a previous briefing session, you mentioned considering restructuring your research and development framework. What is the current status of this?

Ogawa: Regarding Tokyo's Open Innovation Promotion Project, we applied because we believe strengthening industry–industry collaboration and industry–academia collaboration is essential to continuously generate new products.

Over these three years, we plan to build a system for creating new products through various activities, with the aim of increasing the ratio of new products. Specifically in the first year, we aim to undertake initiatives focused on laying the groundwork—essentially sowing the seeds.

Tokiwa: Please refer to the slide on our strategies for increasing earning power. Regarding the research structure you asked about, significant changes were made starting in April of this year. Until then, we operated under a vertically divided structure consisting of the R&D Division, the Manufacturing Division, the Quality Assurance Division, and the Procurement Division. The R&D Division covered compounds, films, and food packaging materials.

This year, we established the Monozukuri Headquarters at the top level of the organization, under which we placed the Compound Division. Within this division, we have placed the R&D, manufacturing, and quality assurance divisions. In addition, we created the Films Division, which similarly includes its own R&D, manufacturing, and quality assurance functions.

Additionally, we have established the Procurement Division alongside the Monozukuri Headquarters, creating an organizational structure that fosters a sense of unity across the entire operation. In essence, rather than focusing solely on research and development, we prioritize this sense of unity and have organized our structure around materials accordingly.

To further evolve this integrated operational approach, we have implemented various initiatives over the past six months. While the previous structure had its merits, we feel that the current organization demonstrates a unified strength in manufacturing, encompassing product development, production, quality control, and procurement.

We believe that as the effects of this unity become apparent, more advanced development will follow. That would be my explanation. I hope this answers your question.

Q&A Session: Facility expansion plan for R&D Center in Ota-ku, Tokyo

Questioner: I’ve heard that the R&D Center in Ota-ku, Tokyo is considering future capital investments and facility expansions. Will you be continuing your efforts in this regard?

Tokiwa: Our sales volume has increased, and overseas business development has also grown significantly. As a result, we’re making considerable use of our R&D Center in Kamata, Ota City, Tokyo.

While we’ll need to hold discussions over the next three years, I personally believe that even though the R&D Center expanded its space by 1.5 times four to five years ago, it is still insufficient.

Therefore, while the site currently houses a logistics warehouse for Tokyo, we must consider whether to keep the warehouse as it is or to expand it further by doubling the research and development space.

This is also under consideration at present. While we cannot yet share specific figures with you, we intend to address this matter when we reach our 100th fiscal year, and we’re currently gathering opinions internally.

Q&A Session: Capital allocation as well as progress and measures relating to the medium-term business plan

Questioner: My question relates to the section on capital allocation. As your medium-term business plan has now progressed for six months, are there any areas where you recognize deviations from the plan or points that you are particularly mindful of?

Possibilities may include profits being stronger than expected, potentially leading to upward revisions; whether to accelerate asset sales further given the favorable stock price in relation to balance sheet reform; or capital expenditures becoming more costly due to inflationary pressures.

What potential deviations do you foresee? Or, if a deviation is perceived, how will you manage it? I would appreciate your thoughts on this.

Michio Noishiki: My name is Michio Noishiki, Senior Executive Officer and Senior General Manager of the Corporate Planning Division. Regarding cash allocation, we believe it’s progressing smoothly at this point, covering foundational, growth and strategic investments.

Regarding M&A, as this involves elements of opportunity, I cannot provide specific details at this time. However, we are proceeding with other growth and foundational investments according to the originally planned schedule, disclosing them sequentially at appropriate times. We don’t believe any particular delays have occurred.

Regarding balance sheet reform, as outlined on slide 28, we’re advancing various measures. However, as we’re only halfway through the year, the effects are not yet significantly apparent. Nevertheless, the measures are being steadily implemented, and we’re confident that we’re progressing reliably toward the ideal balance sheet outlined in our medium-term business plan.

On this point, there are no particular causes for concern at this stage. We’re continuing to make progress in line with the vision set out in our medium-term business plan.

Irie: To add to that, we receive various opinions from our investors through our IR and SR activities. Among these opinions, we understand that there is a request for us to actively generate cash and direct it toward growth investments when possible, or to prioritize generous shareholder returns otherwise. Against this backdrop, we have been steadily selling our cross-shareholdings over the past few years.

As the stock price rose, book value has decreased while the market value has increased, creating the appearance of increased value as of the end of September. However, this does not mark the end of the process. We plan to continue this initiative throughout the current fiscal year.

Regarding the unused land at Gunma Factory, given its current non-cash-generating status and the lack of future investment plans, we intend to sell it and use the proceeds to fund growth investments, such as acquiring fixed assets for food packaging materials and expanding Mie Factory.

We’ll actively pursue growth opportunities in areas where there is significant scope for investment, both domestically and internationally. As Michio Noishiki just mentioned, regarding changes to the balance sheet over the six months ended September 30, inventory decreased slightly while other items increased. However, our overall strategy remains focused on selling non-essential assets to generate cash, shortening the collection periods for accounts receivable to create cash flow, and allocating these funds toward growth investments.

There is no discrepancy whatsoever between the initial announcement of the medium-term business plan and its current content, and I believe we’re on a growth trajectory. That concludes my remarks.

Tokiwa: I’d like to add one point. I believe that our ongoing initiatives are progressing smoothly without any delays.

Regarding the sales ratio of new products, this figure indicates the proportion of total sales accounted for by products developed by our research and development over the past three years. In the current three-year medium-term business plan, we have set this target at 23% as our medium-term goal.

In the first half through September 2025, new products accounted for 13% of sales. We haven't shared this widely, but at the end of March 2025, it was 10%. It has increased by 3 percentage points. Therefore, we plan to raise it by 6 percentage points, aiming for “3×6=18.” The biggest challenge for us as a manufacturer is how we increase this portion.

Regarding investment in research and development, this hasn’t yet been reflected in our specific figures. However, I believe it’s something we must actively pursue in the future to improve the figures for the next medium-term business plan and subsequent plans. We’ll continue to examine this point further.