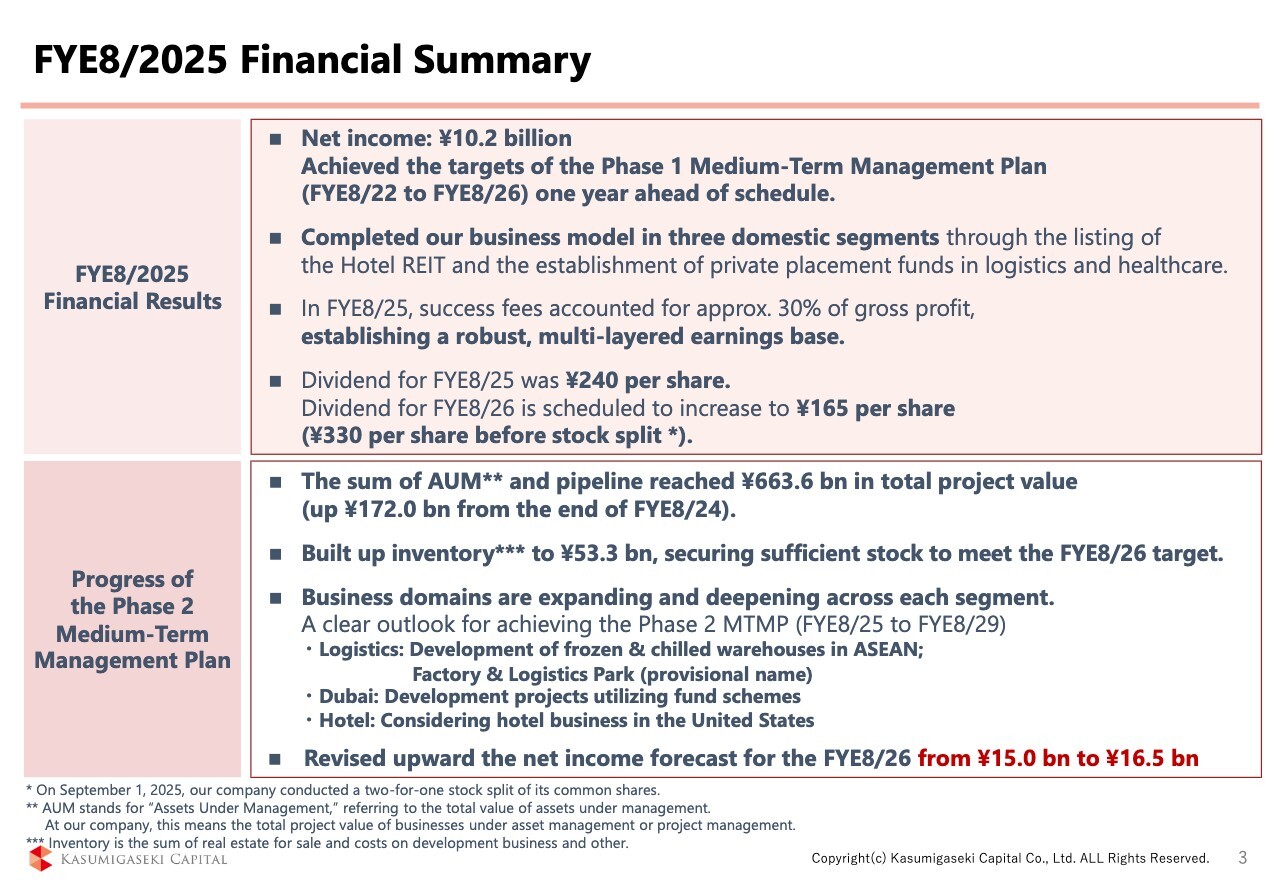

FYE8/2025 Financial Summary

Mr. Koshiro Komoto (hereinafter referred to as "Komoto"): Hello, everyone. I am Komoto, President & CEO. We will begin to explain Kasumigaseki Capital's financial results for the fiscal year ending August 31, 2025 (FYE8/2025). First, let's look at the summary.

This is a review of the FYE8/2025. The first point is that net income was 10.2 billion yen. Many of you may have been skeptical when we told you four years ago at the October 2021 financial results meeting that we would increase net income tenfold to 10 billion yen in five years, but we achieved 10 billion yen in four years instead of five.

Second, we raised a total of 150 billion yen in funds through the listing of a J-REIT specializing in hotels and the establishment of private placement funds in logistics and healthcare facilities. Our business model is to acquire land and formulate plans in the first phase, construct buildings using development funds in the second phase, and transfer the completed properties to a stable fund for medium- to long-term management in the third phase.

REITs and private funds fall under this third phase. Over the past year, we successfully completed our business model across all three of our core asset segments.

Third, in the FYE8/2025, there was a significant change in the revenue structure, with approximately 30% of gross profit coming from success fees. This was largely the result of the establishment of medium- to long-term management funds, including REIT.

The fourth point concerns the dividend for the FYE8/2026. On September 1, we conducted a two-for-one stock split. After the split, we plan a dividend of 165 yen per share, equivalent to 330 yen per share before stock split. The company plans to increase its dividend by just under 40% compared to the 240 yen per share for the FYE8/2025.

Next, I would like to explain our progress of the Phase 2 Medium-Term Management Plan.

I will touch on it again later, so I will talk about it briefly here. First, the project pipeline increased by approximately 170 billion yen from the end of FYE8/2024 to approximately 660 billion yen. In addition, with inventory of 53.3 billion yen, the outlook for the FYE8/2026 is favorable.

Furthermore, business domains are expanding across each segment. From the FYE8/2026, we plan to fully embark on overseas expansion, and in the logistics business, we plan to develop frozen & chilled warehouses in ASEAN, first of all in Malaysia. In addition, we will start a business called Factory & Logistics Park (provisional name) as a developmental system of logistics warehouses.

In Dubai, we announced about two weeks ago that we will start a housing development business in a joint venture with Daito Trust Construction Co., Ltd. In the hotel business, we are also considering initiatives in the United States.

Finally, regarding net income for the FYE8/2026, the medium-term management plan had announced 15 billion yen, but this has been revised upward to 16.5 billion yen.

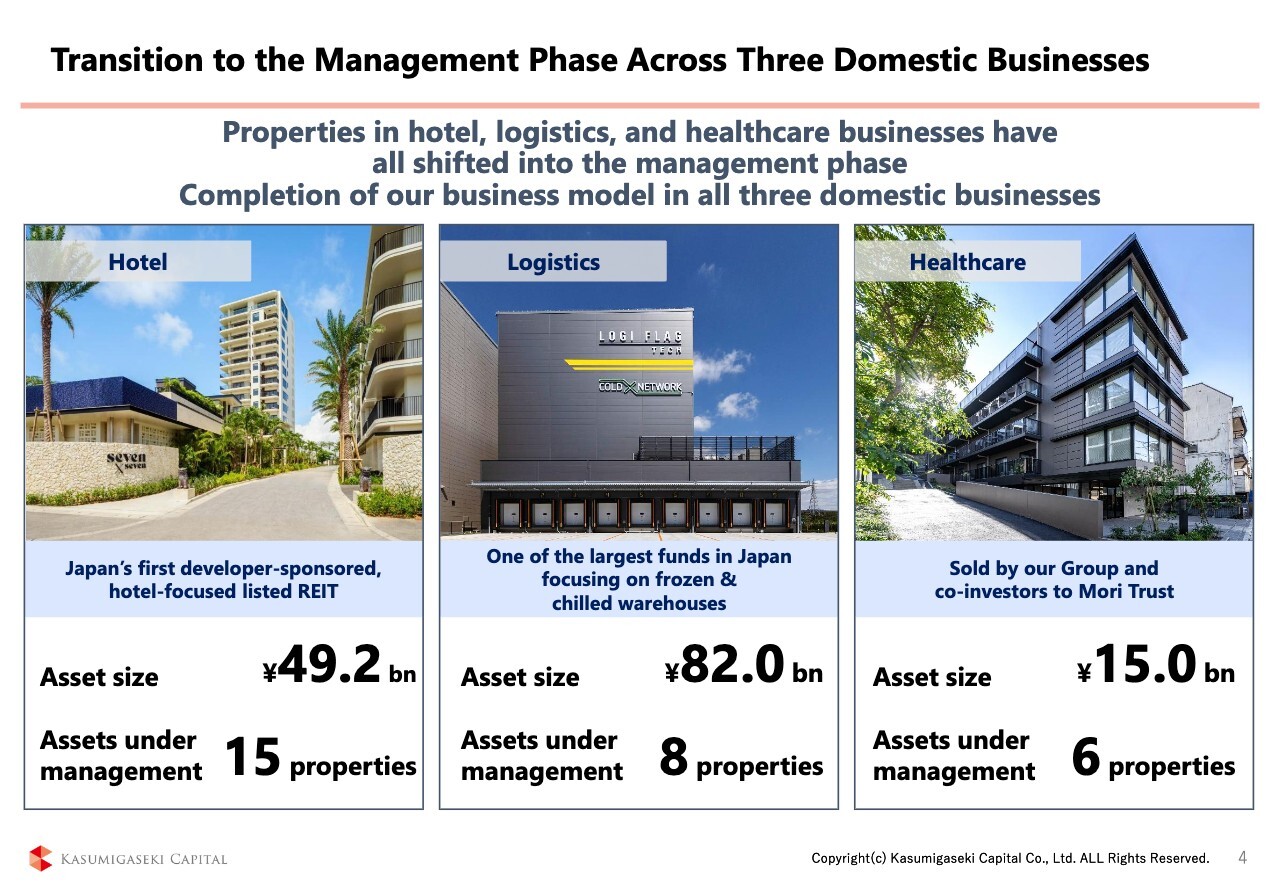

Transition to the Management Phase Across Three Domestic Businesses

One of the topics for the FYE8/2025, as I mentioned earlier, is the establishment of stable medium- to long-term management funds for assets in all three of our core businesses.

We have established a REIT with approximately 50 billion yen in hotel properties, a private fund with approximately 80 billion yen in logistics facilities targeting frozen & chilled warehouses, and a private fund with 15 billion yen in healthcare facilities, totaling approximately 150 billion yen. It should be noted that all of the properties incorporated in these funds were developed by the Company.

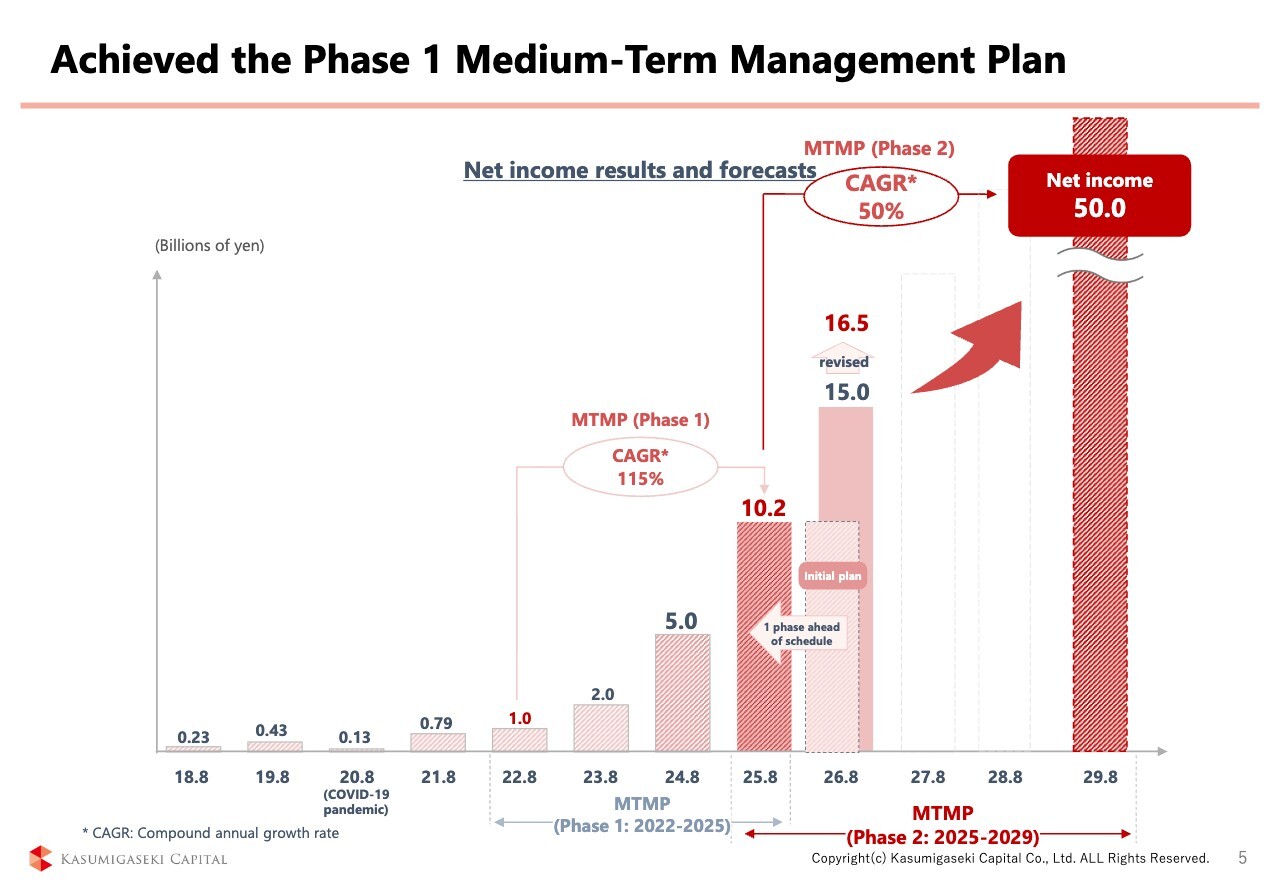

Achieved the Phase 1 Medium-Term Management Plan

This slide shows the progress of the Phase 1 Medium-Term Management Plan, which began in 2022, as well as its future outlook.

The Phase 1 MTMP achieved a CAGR (compound annual growth rate) of 115%, having completed one year ahead of schedule. And in the Phase 2 MTMP, we have set a target of 50.0 billion yen in net income for the FYE8/2029, and the CAGR to achieve this goal is 50%. Toward this goal, we are first looking to ensure that we achieve net income of 16.5 billion yen in the FYE8/2026.

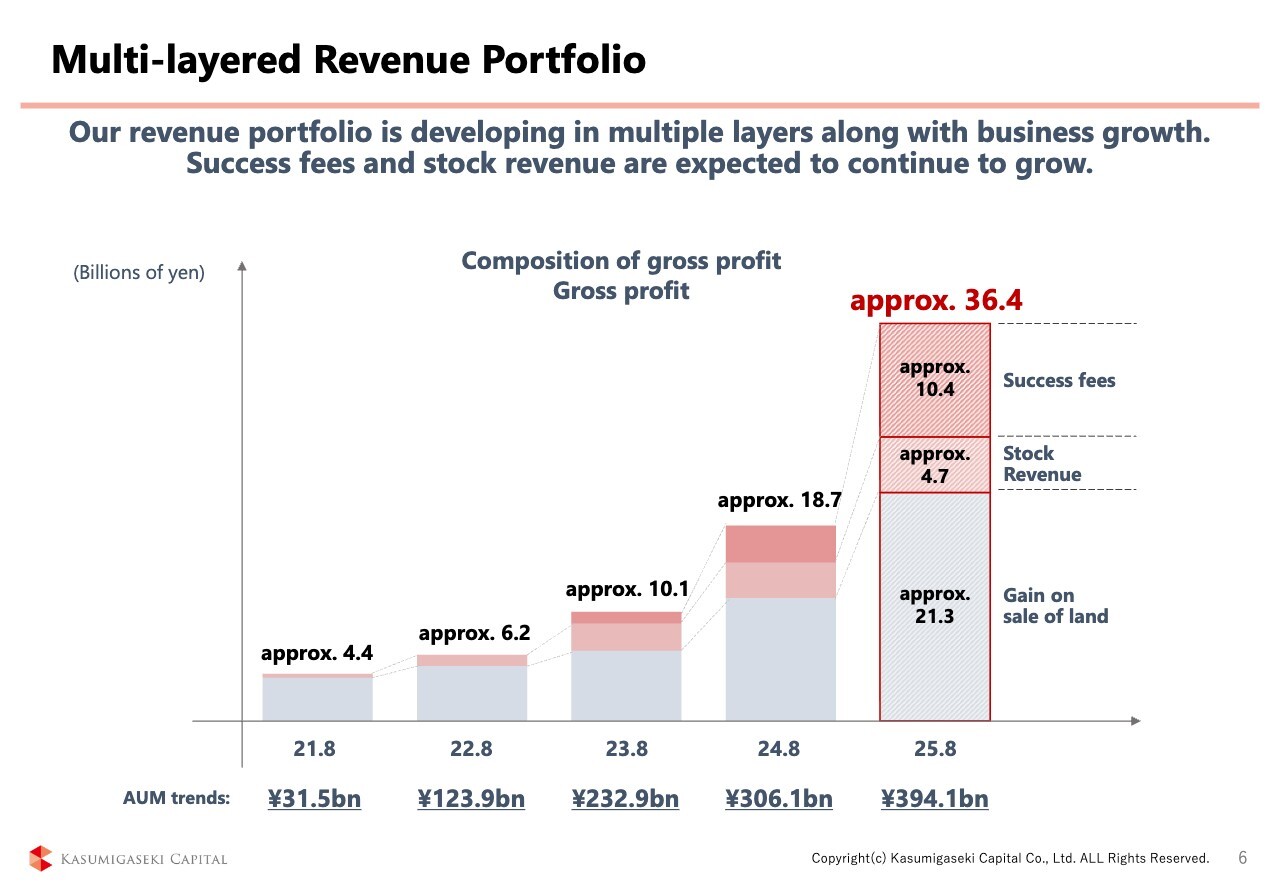

Multi-layered Revenue Portfolio

As I mentioned at the outset, there has been a change in our revenue structure for the FYE8/2025. Let me once again explain the revenue opportunities in our business model. There are three revenue opportunities.

The first is the gain on sale of land when it is transferred from the Phase 1 fund to the development fund in Phase 2; the second is the success fees earned when the building is completed in the development fund and the property is transferred to the stable fund; and the third is the AM fees and project management fees earned from the development fund and stable fund. These three are our main revenue opportunities.

As shown in the slide, success fees increased significantly in the FYE8/2025. This was due in part to the fact that we were able to establish the REIT and stable funds.

These are the topics for the FYE8/2025.

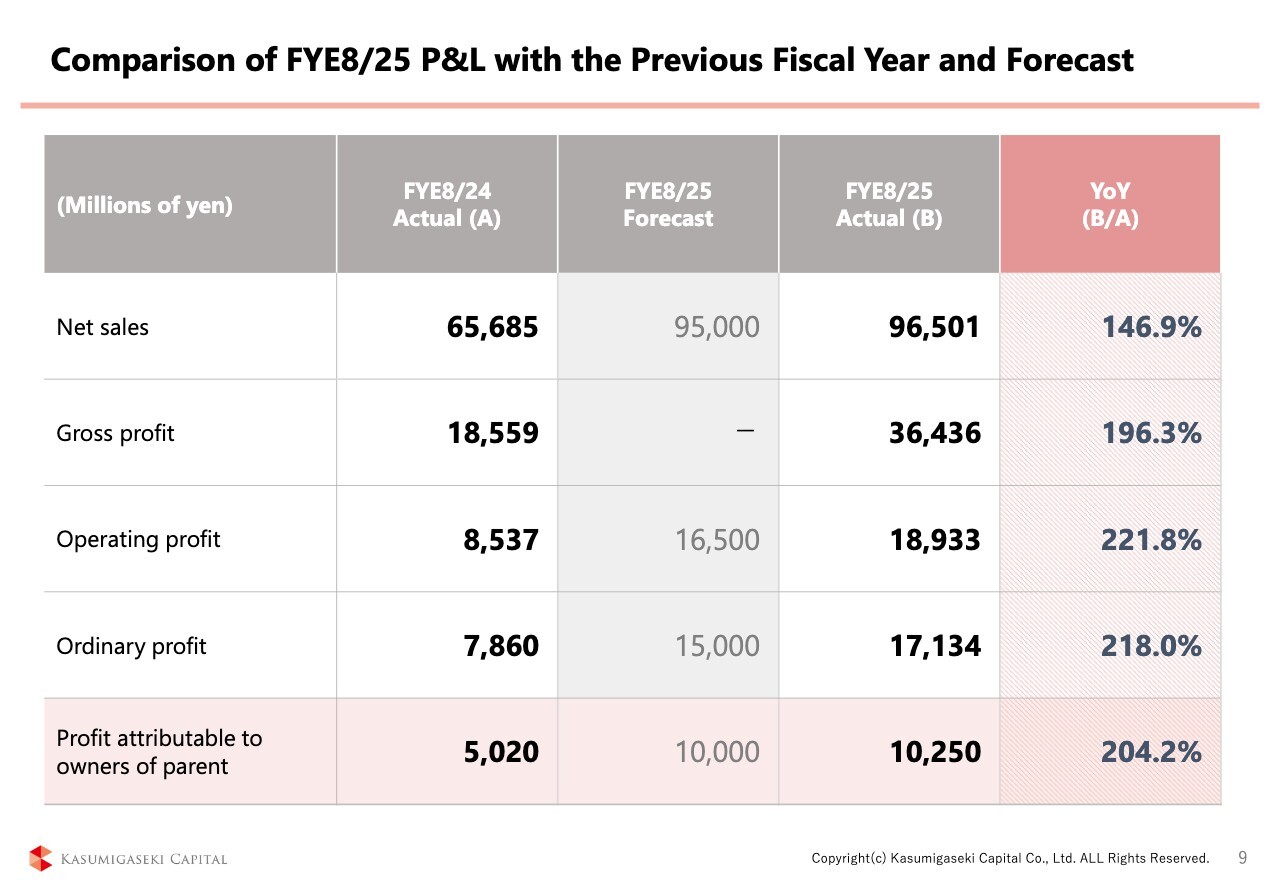

Comparison of FYE8/25 P&L with the Previous Fiscal Year and Forecast

Next, I will provide a summary of the financial results and performance outlook. You can grasp the main points by reviewing the slides, so I will highlight a few key pages and talk about them. This slide shows a comparison of net sales and each profit item with those of the FYE8/2024.

As you can see, net sales are 1.5 times higher, and each of the profits, such as gross profit, ordinary profit, and profit attributable to owners of parent, are about twice as high. In other words, you can see that the profit to sales ratio is increasing.

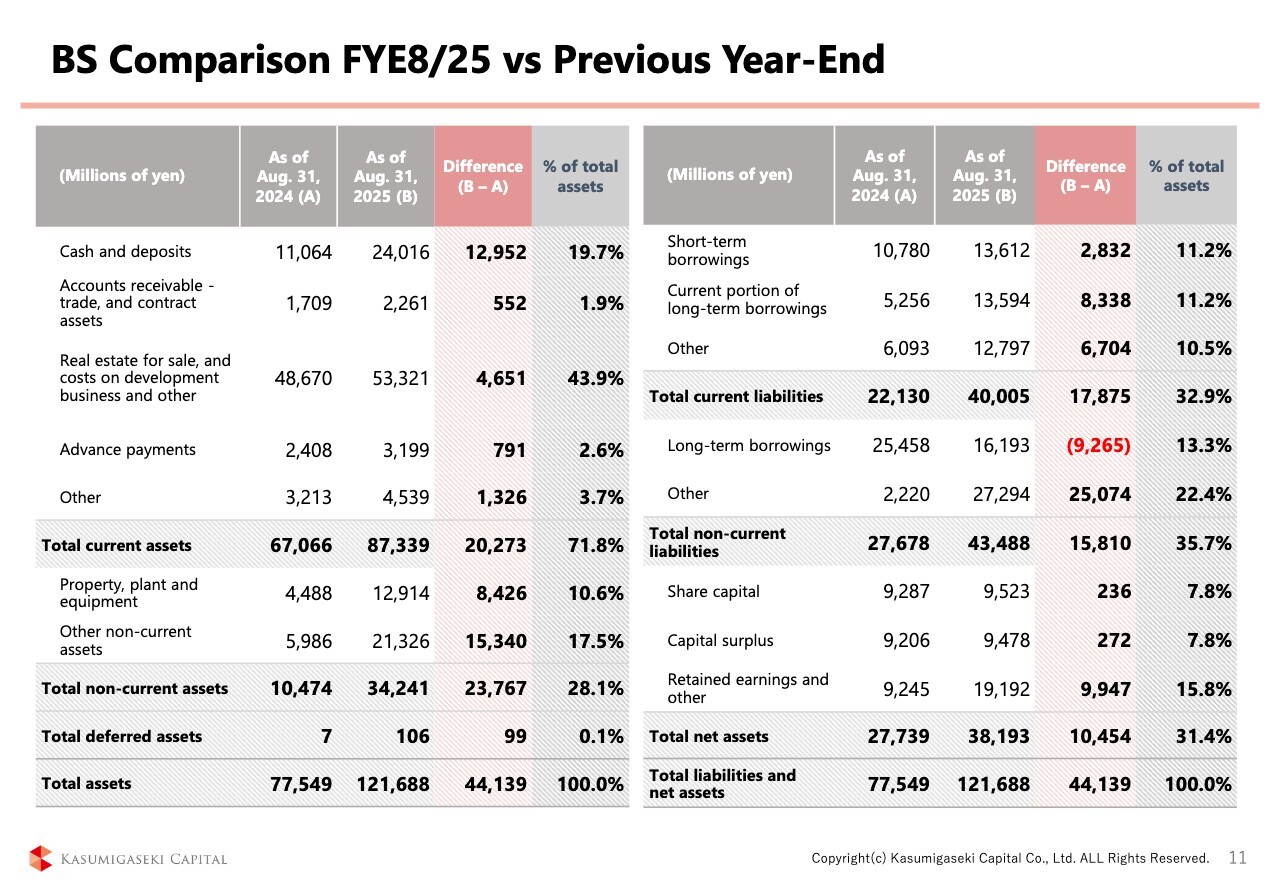

BS Comparison FYE8/25 vs Previous Year-End

Next, I will go over the balance sheet. The overall balance sheet increased by about 44 billion yen to 120 billion yen, partly due to the 22 billion yen raised through Euroyen CBs last November. The main items that increased in assets were a 13.0 billion yen increase in cash, a 5.0 billion yen increase in real estate for sale, an 8.0 billion yen increase in property, plant and equipment, and a 15.0 billion yen increase in other non-current assets.

Let me explain a little more about property, plant and equipment, as well as other non-current assets.

Of the 13 billion yen in property, plant and equipment, approximately 9 billion yen is essentially in the nature of real estate for sale. Specifically, there are several hotel properties undergoing renovation. For those properties, we have adopted a method of breaking down the land and building and having an outside company own the land, while we own and renovate only the building.

The goal is to lighten the balance sheet as much as possible and reduce financial burdens. We envision a scenario in which the property is renovated over a period of two to three years to achieve stable operations, and then sold together with the externally owned land.

Therefore, please consider that approximately 9 billion yen of what is recorded as non-current assets is effectively real estate for sale in the medium term. In addition, over 10 billion yen of other non-current assets are investment securities, of which approximately 6 billion yen are similar in nature to accounts receivable.

Specifically, we established a private fund for logistics facilities in the third quarter of the FYE8/2025, and a J-REIT specializing in hotels in the fourth quarter. Accordingly, the properties were sold from the development funds and the development funds recorded gain on the sales.

Since we holds equity interests in development funds, these are recorded on the balance sheet as investment securities measured at fair value, reflecting the gain on the sales. The development funds use the SPCs, but as of the end of August, that SPCs had not yet finalized their financial periods, so they were recorded as investment securities.

Therefore, during the first quarter when the SPC's financial periods are completed, approximately 6 billion yen of these securities will be converted to cash, which is effectively similar in nature to accounts receivable.

Approximately 9 billion yen of the property, plant and equipment can be organized as substantially real estate for sale. It also means that approximately 6 billion yen of other non-current assets contain the same nature as accounts receivable. This concludes the explanation of the balance sheet.

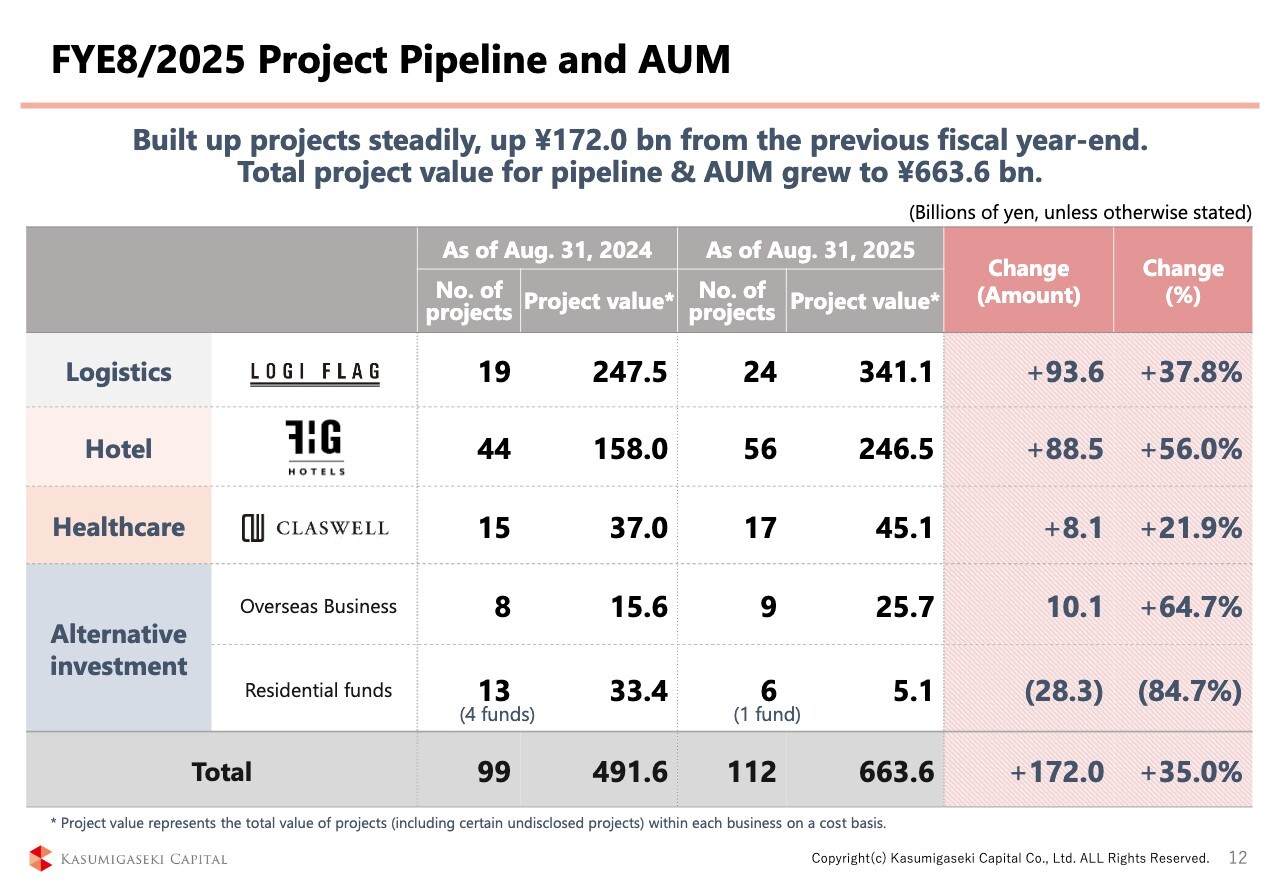

FYE8/2025 Project Pipeline and AUM

I will explain the project pipeline. Over the course of the year, the amount increased by approximately 170 billion yen, reaching around 660 billion yen. As you can see, each sector is growing steadily.

Logistics facilities increased by approximately 93 billion yen, hotels by approximately 88 billion yen, healthcare facilities by approximately 8 billion yen, and overseas business by approximately 10 billion yen. On the other hand, the residential funds decreased by approximately 28 billion yen. These funds were not a collection of properties developed by the Company, but rather a fund of rental housing purchased in the market.

Originally, STOs and other digital securities were utilized to collect properties for smaller lots. However, current demand for STOs appears to be focused more on hotels and offices. Therefore, we decided to close the residential funds sequentially.

As a result, AUM decreased by approximately 28 billion yen. However, in other words, after subtracting a decrease of approximately 28 billion yen, the overall pipeline has increased by approximately 170 billion yen, so please consider that the real pipeline has increased by approximately 200 billion yen.

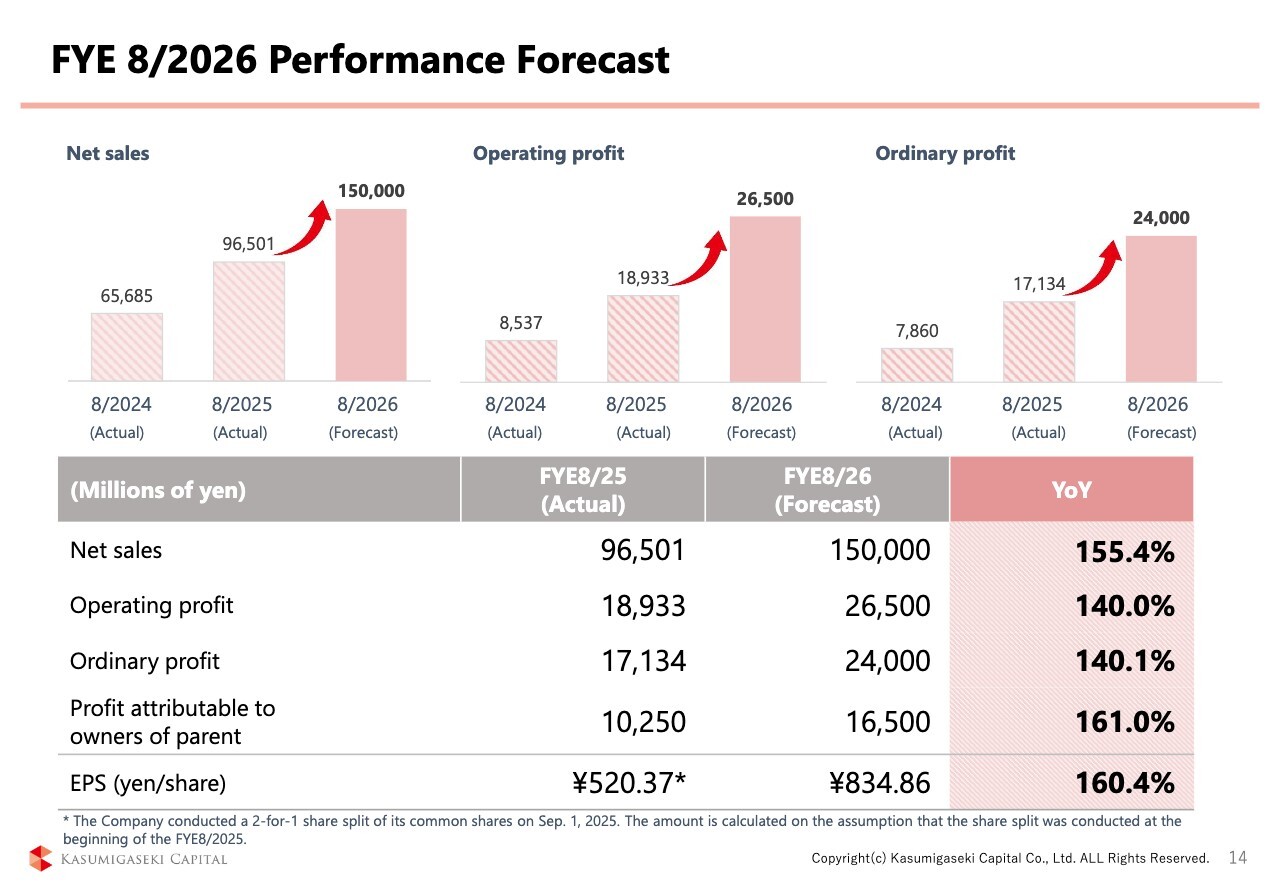

FYE 8/2026 Performance Forecast

I would like to explain our performance forecast for the FYE8/2026. Net sales are projected to be 150 billion yen, operating profit 26.5 billion yen, ordinary profit 24 billion yen, and profit attributable to owners of parent 16.5 billion yen, revised upward from the previously announced 15 billion yen.

Our business continues to grow steadily. The Phase 2 Medium-Term Management Plan is also making steady progress.

From here, we would like to give a business overview of each sector. The hotel and logistics businesses will be explained by their respective managing directors, Ogata and Sugimoto.

1. Hotel Business

Hidekazu Ogata: Hello. I am Ogata, Managing Director of Kasumigaseki Capital. Thank you very much for gathering here today. Let me explain about the hotel business.

The hotel business is centered on three brands: "fav," "seven x seven," and "BASE LAYER HOTEL.

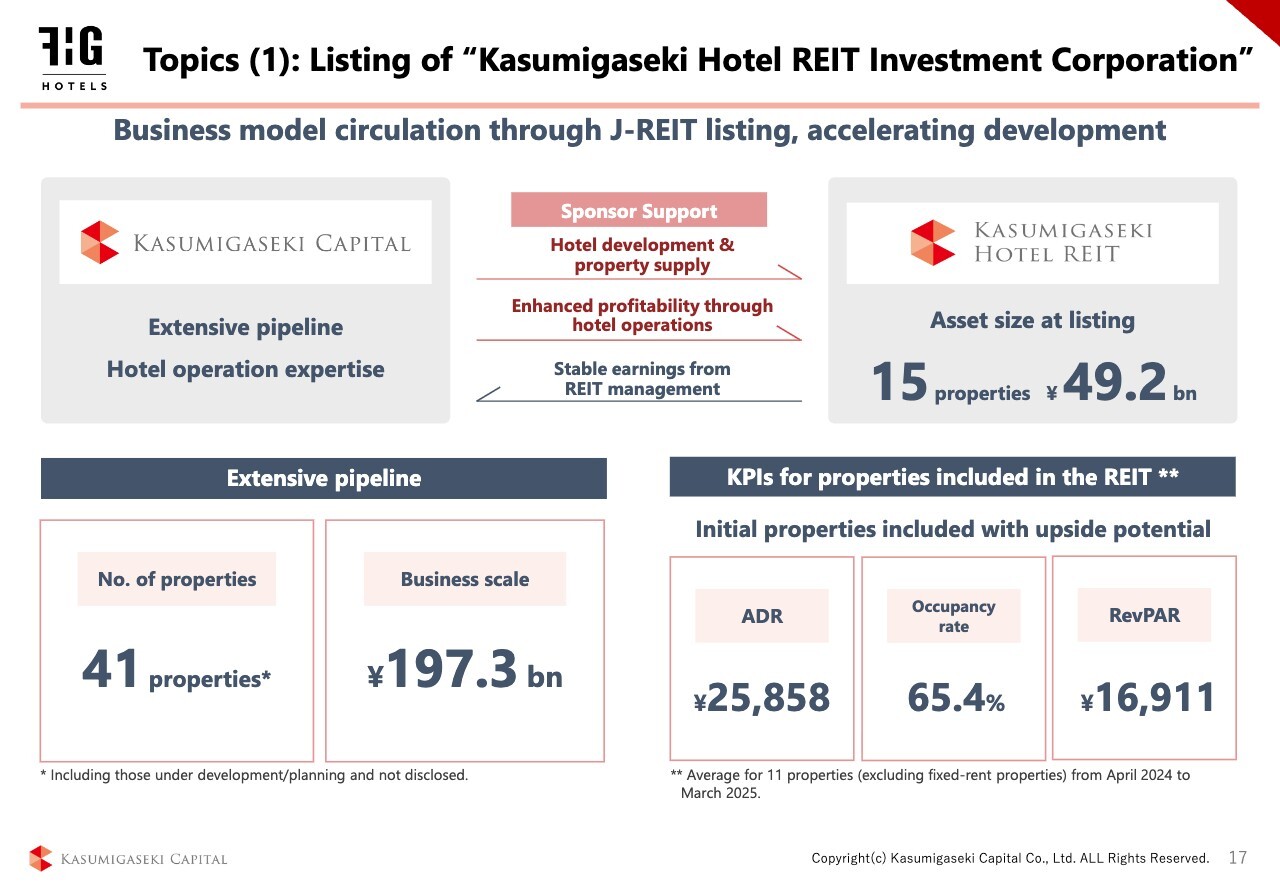

Topics (1): Listing of “Kasumigaseki Hotel REIT Investment Corporation”

Topics for the FYE8/2025. As explained at the beginning of this report, we were listed as a J-REIT in August of this year. I believe we have successfully achieved our goal of listing on the J-REIT, which we have pursued since the start of our hotel business.

When we first started our hotel business, we launched the fav business with the idea of turning vacation rentals into a financial product. However, due to the weak legal basis for vacation rentals, we abandoned that idea. Instead, we decided to take the strengths of the vacation rental business model—for example, group stays and models that keep the per-person rate low—and develop them directly within hotels. This approach is what led to the creation of the fav business.

From there, we decided to develop "seven x seven" as a new fusion of luxury and the self-hospitality concept we had cultivated with "fav," in other words, the DX of hotels through self check-in and other self-service features.

As a result, we created everything from planning, development, and branding from scratch, which enabled us to achieve an IPO in five years with a portfolio that was 100% in-house developed. We would like to thank again everyone who has supported us. Thank you so much.

Needless to say, being listed on the J-REIT provides a significant advantage that will further accelerate investment development in the future, as the company now has a means of raising capital through the REIT. More importantly, however, we see this as a new challenge—an opportunity to introduce the brand we have built up to the capital market.

In addition, incorporating a capital market perspective will require greater transparency and sustainability in our performance than ever before. We believe this will further strengthen both our operations and our brand.

We already have a pipeline of approximately 200 billion yen, enabling us to anticipate substantial external growth for the REIT.

In addition, many of the properties included in the REIT are hotels that have been in operation for an average of two to three years. Even at present, ADR stands at around 25,000 yen and the occupancy rate at about 65%, achieving our original targets.

However, we believe that there is still room for upside and that the REIT is in a position to grow steadily in terms of internal growth.

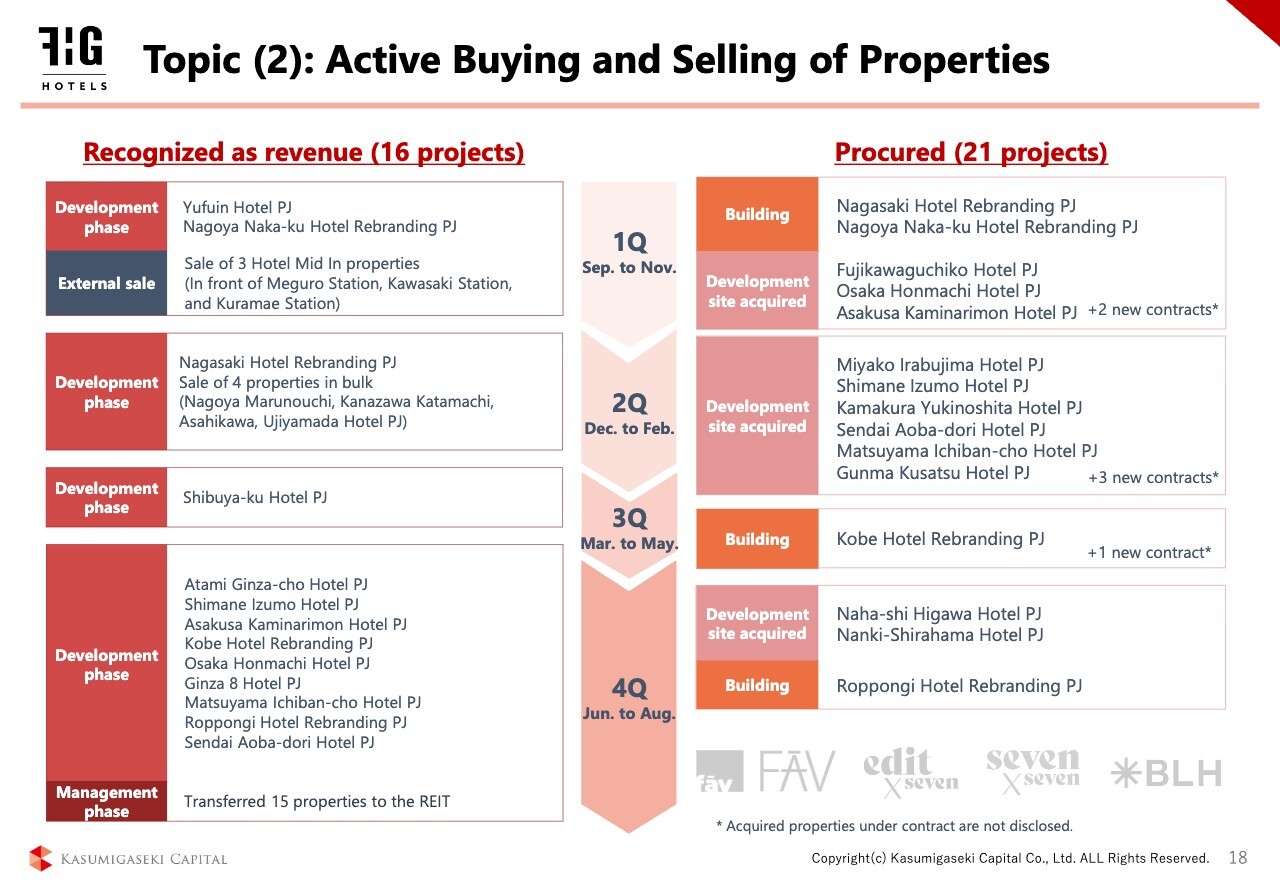

Topic (2): Active Buying and Selling of Properties

This slide shows our property transactions for the FYE8/2025. We recognized revenue mainly from property sales in 16 projects and procured 21 new projects, both exceeding our initial plan and showing very strong progress.

Topics (3)-1: 5 Development Hotels Opened

This is about hotel openings. Five properties, including a new brand, opened in the FYE8/2025. Notably, "FAV LUX Sapporo Susukino," which opened in July 2025, is the first hotel under the "fav" brand to feature a large public bath.

In addition, "edit x seven," a derivative brand of "seven x seven," opened in Gotemba. This property features pet-friendly facilities and a full range of saunas, both hallmarks of our hotel brand.

Along with private saunas, a variety of room-based saunas are also available.

Although we have already opened hotels in the Kanto area that specialize in overnight stays, such as "fav Tokyo Ryogoku" and "fav Tokyo Nishi-nippori," "edit x seven" marks our first leisure-oriented hotel in the region.

We will continue to design and plan products that will strongly appeal to trend-conscious guests in the Kanto area.

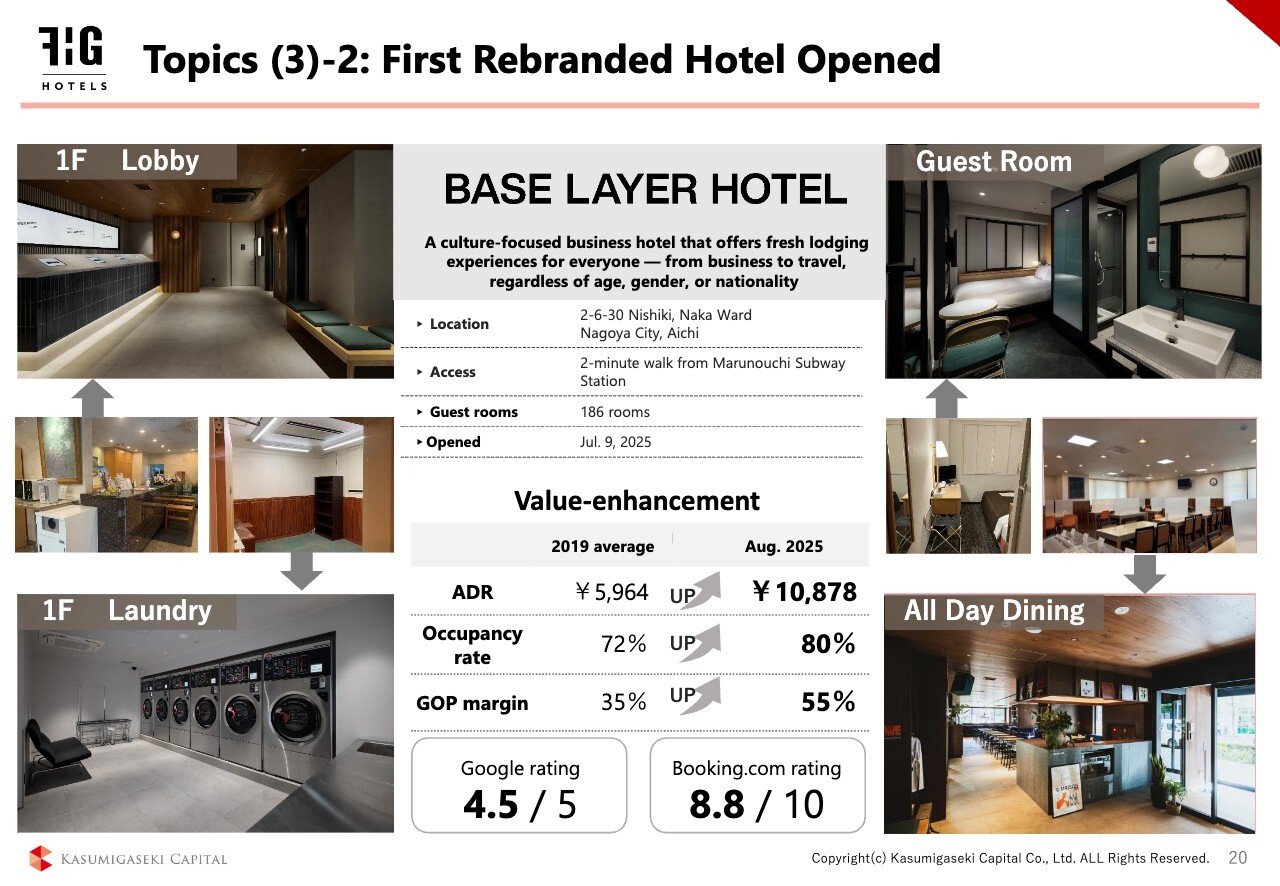

Topics (3)-2: First Rebranded Hotel Opened

BASE LAYER HOTEL opened its first rebranded hotel in July of this year. This is the first project in which we renovated a 25-year-old business hotel and transformed it into a lifestyle hotel.

The value-enhancement results in the lower part of the slide show that in 2019, before the COVID19 pandemic, the average ADR was about 5,900 yen with an occupancy rate of 72%. After reopening in July of this year, however, the August 2025 results show an ADR of around 10,800 yen and an occupancy rate of 80% for the single month results, more than doubling the top line.

Since September, things have continued to go very well, with ADR exceeding 13,000 yen in the September preliminary figures. Occupancy has also remained very steady since October.

Regarding the GOP margin, which was originally around 35%—a typical level for hotels—it reached 55% for the single month. This result comes from applying the self-hospitality practices cultivated in "fav" to the BASE LAYER HOTEL business, enabling us to secure a high profit margin. We believe that combining these factors allowed us to more than double the value in this value-enhancement project.

In addition, we have received very high evaluations from our guests, as shown at the bottom of the slide, including representative ratings from Google and Booking.com. Sustaining performance in this area requires not only operational results but also strong customer satisfaction, and we have received top marks compared to typical hotels. We intend to continue operating the hotel successfully going forward.

Topics (4): Award Recognition and Media Event

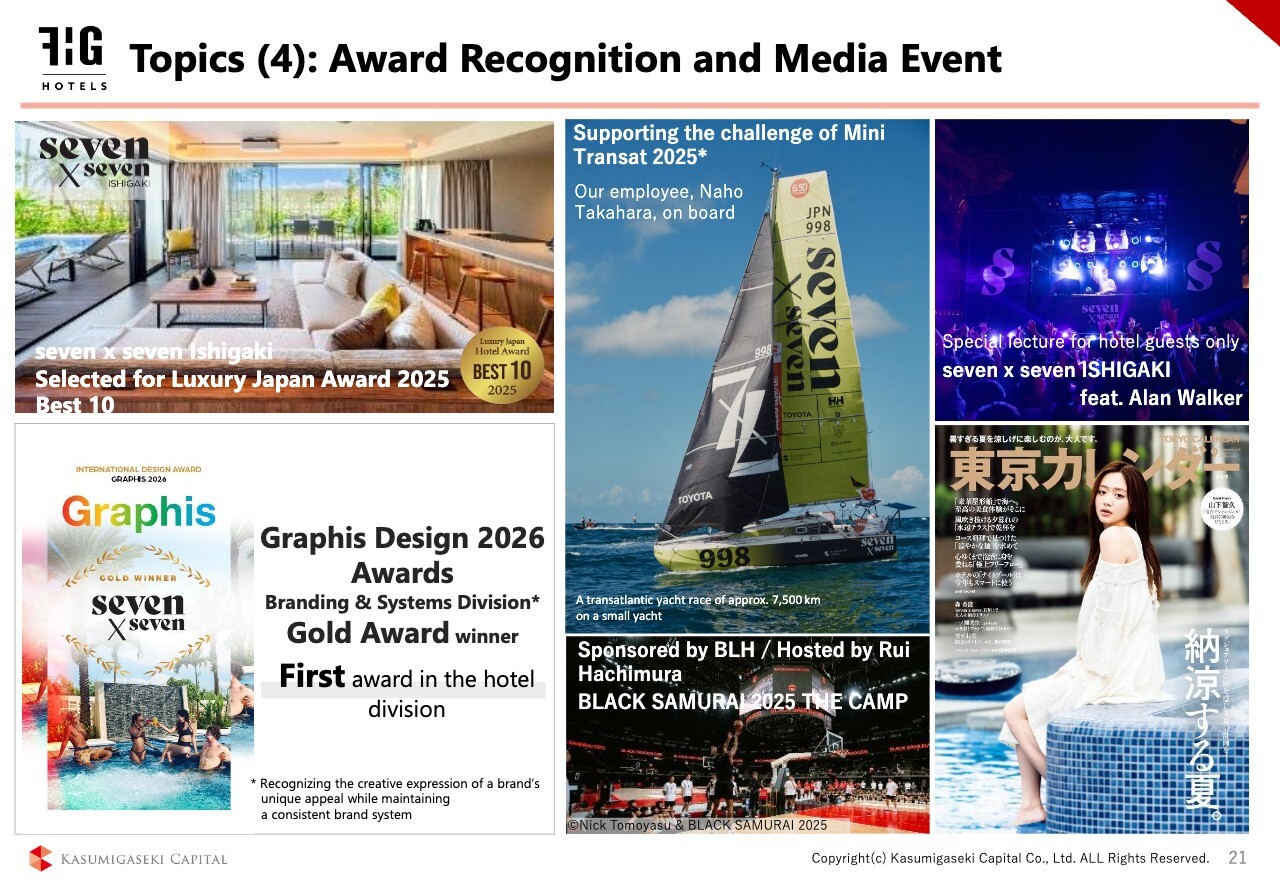

This is about awards and media coverage. Regarding awards, "seven x seven Ishigaki" was selected as one of the top 10 in the "Luxury Japan Award 2025" during the first half of the year. We are very proud that our Ishigaki hotel was selected among one of the top 10 hotels in Japan, along with other leading Japanese hotel brands such as Palace Hotel Tokyo, Bvlgari Hotel Tokyo, and Aman Tokyo.

It also received its first Gold Award at the Graphis Design 2026 Awards this past August. This is a highly prestigious international design award, and it marks the first time a Japanese hotel has won it. Furthermore, it is the first time globally that the brand as a whole has received a Gold Award.

This recognition has resulted in "seven x seven" being featured in numerous articles, especially in Europe and the United States, and I have heard that it has been covered by over 1,000 media outlets to date.

On the right side of the slide, you will find information on media and events, and we actively participate in these as well. The image of the yacht represents a transatlantic race called "Mini Transat 2025," which we are supporting as a sponsor.

On the lower part of the slide, "BLACK SAMURAI 2025," Rui Hachimura hosted a basketball school for elementary, middle, and high school students at the basketball court of the IG Arena in Nagoya, with our company participating as the hotel sponsor.

Furthermore, at the opening event for “seven x seven,” we invited world-renowned DJ Alan Walker, and in media, our hotel was used as a shooting location for the issue of Tokyo Calendar featuring Kasumi Mori on the cover. As our brand power has grown, we are receiving numerous opportunities for events and sponsorships.

We intend to continue making a meaningful contribution to the local community and society through our hotels.

Planned Openings

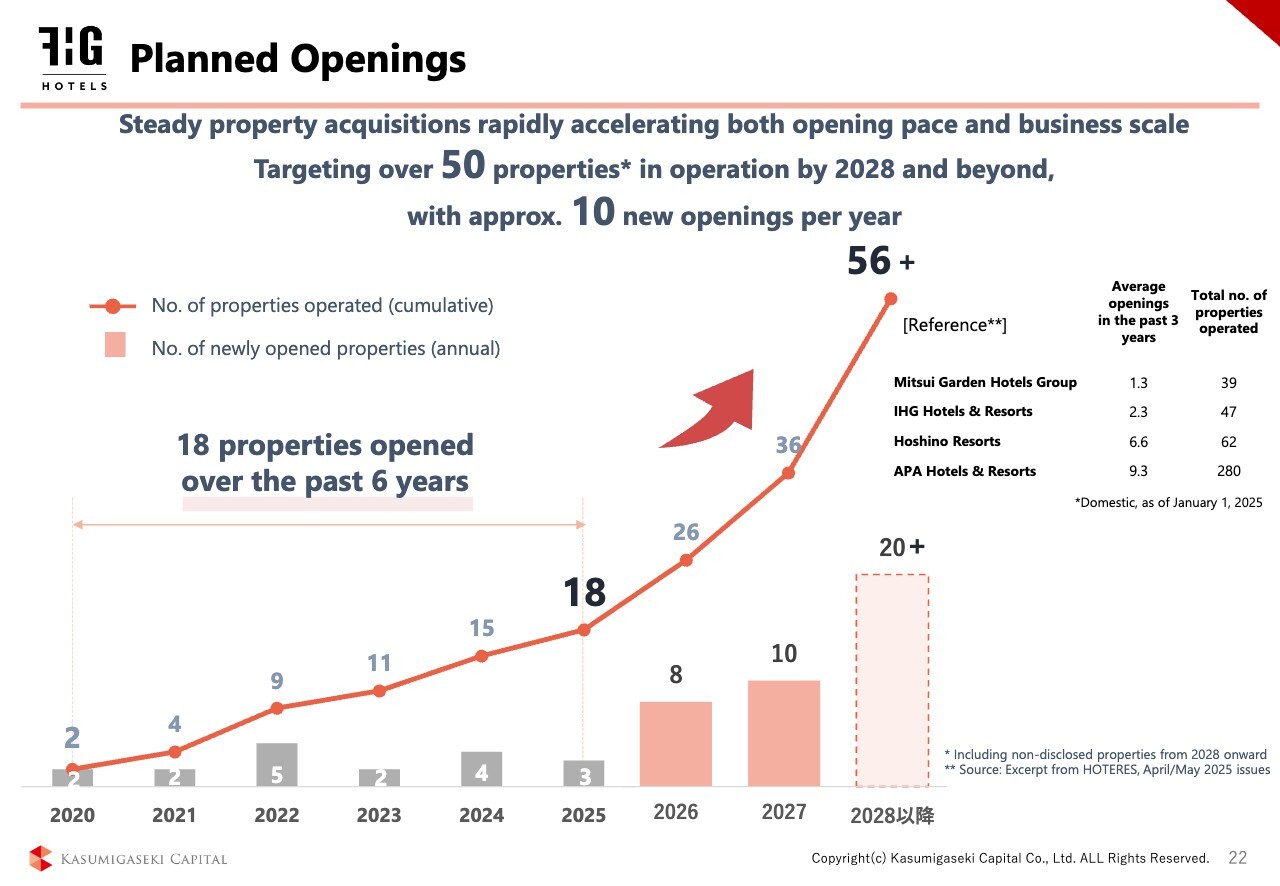

Let me explain our planned openings. With 18 properties opened over the past six years, we now have a cumulative pipeline of 56 properties and expect to exceed 50 openings over the next three years. The pace of openings over the past six years has averaged three per year, but it is expected to increase significantly over the next three years to an average of more than 10 per year.

For reference, other hotel brands are listed on the right. Mitsui Garden Hotels Group and IHG Hotels & Resorts are opening an average of two to three hotels per year, with total number of properties operated of 39 and 47, respectively. Our FHG hotel brand aims to achieve a comparable number of properties.

In terms of the pace of openings, the largest hotel operator, APA Hotels & Resorts, has opened an average of nine new hotels over the past three years, and we intend to exceed this pace.

This is a very large number for a typical hotel operator, but as we have explained in the past, our hotels operate on a franchise model.

Regarding brand and operational manuals, Kasumigaseki Capital provides robust oversight. With multiple operators and partners involved, we have various operators manage the hotels under these operational rules. This approach makes it possible to open hotels simultaneously all over Japan.

Project Pipeline List

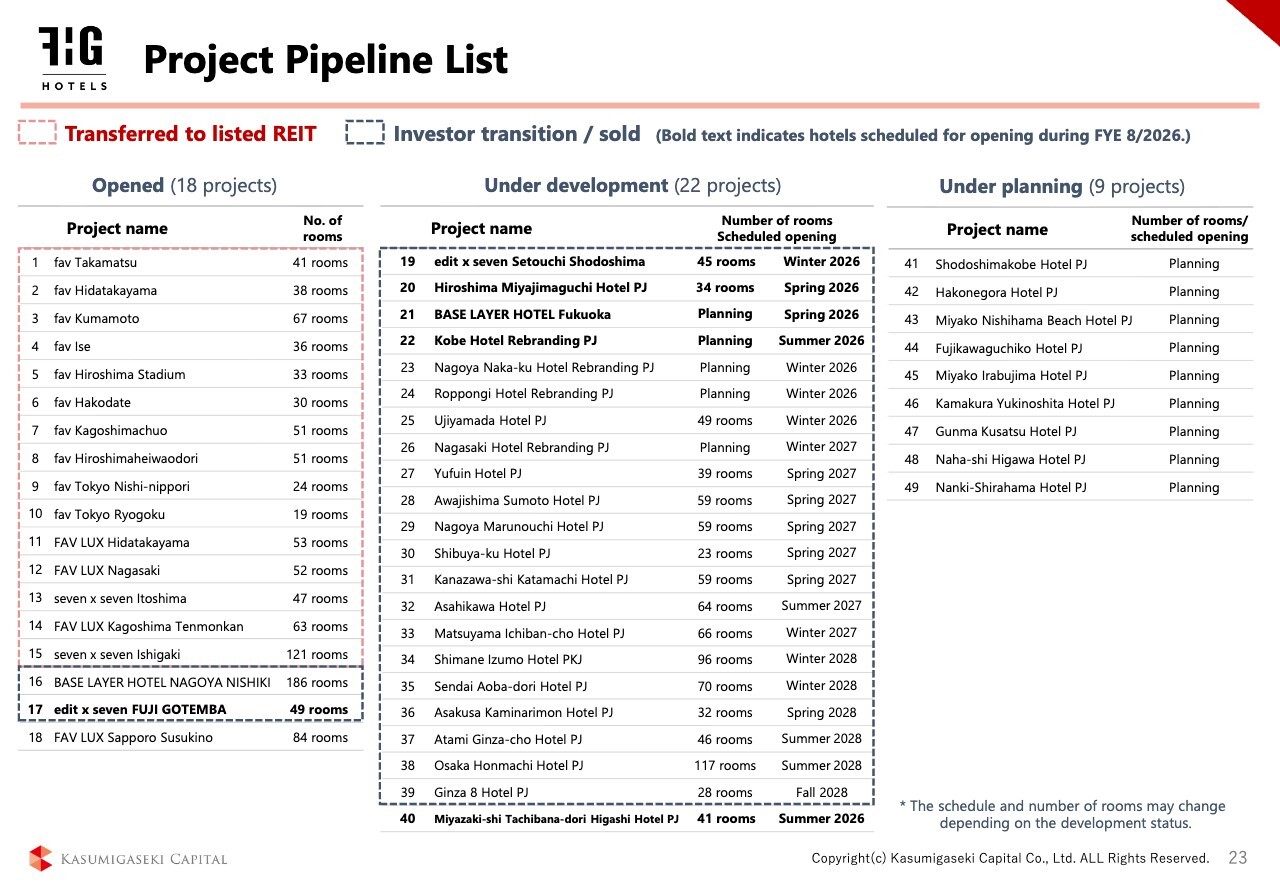

This is our current pipeline. On the left are 18 properties that have already opened, in the center are 22 properties under development, and on the right are 9 properties under planning that have not yet been developed, totaling 49 properties.

A red box indicates properties that have already been transferred to the listed REIT, while blue boxes indicate properties that are off-balance, such as those in development funds or managed funds, rather than the listed REIT.

All properties are off-balance except for FAV LUX Sapporo Susukino (#18) and Miyazaki-shi Tachibana-dori Higashi Hotel PJ (#40). Future planned projects will generally remain off-balance by sequentially incorporating them into the development fund, which is also performing very well.

Projects in the Planning/Development Pipeline

Finally, this slide shows pictures of our current project pipeline. Let me introduce a few properties. In the upper left is Yufuin Hotel, scheduled to open between the end of next year and early 2027. It will be the third brand under the "seven x seven" brand and is located in Yufuin, Oita Prefecture.

In the lower right is "edit x seven Setouchi Shodoshima," the second property under the "edit x seven" brand following our first opened in Gotemba. This will be our first facility to feature a thermal spring, a mixed gender sauna, a swimming pool, and a spa, and shows very promising potential.

The day before yesterday, I had the opportunity to see the soon-to-be-completed facility, which I believe will be of very high quality and a hotel that everyone will enjoy.

At the bottom of the slide is the Nagoya Naka-ku Hotel Rebranding PJ (project), a renovation under the "BASE LAYER HOTEL" series. This will be our first hotel to feature a wedding hall.

We aim to open this hotel within the next fiscal year and will actively promote new content and initiatives.

We will continue to expand our hotel business by opening new properties. We appreciate your continued support. This concludes the explanation of the hotel business. Thank you very much.

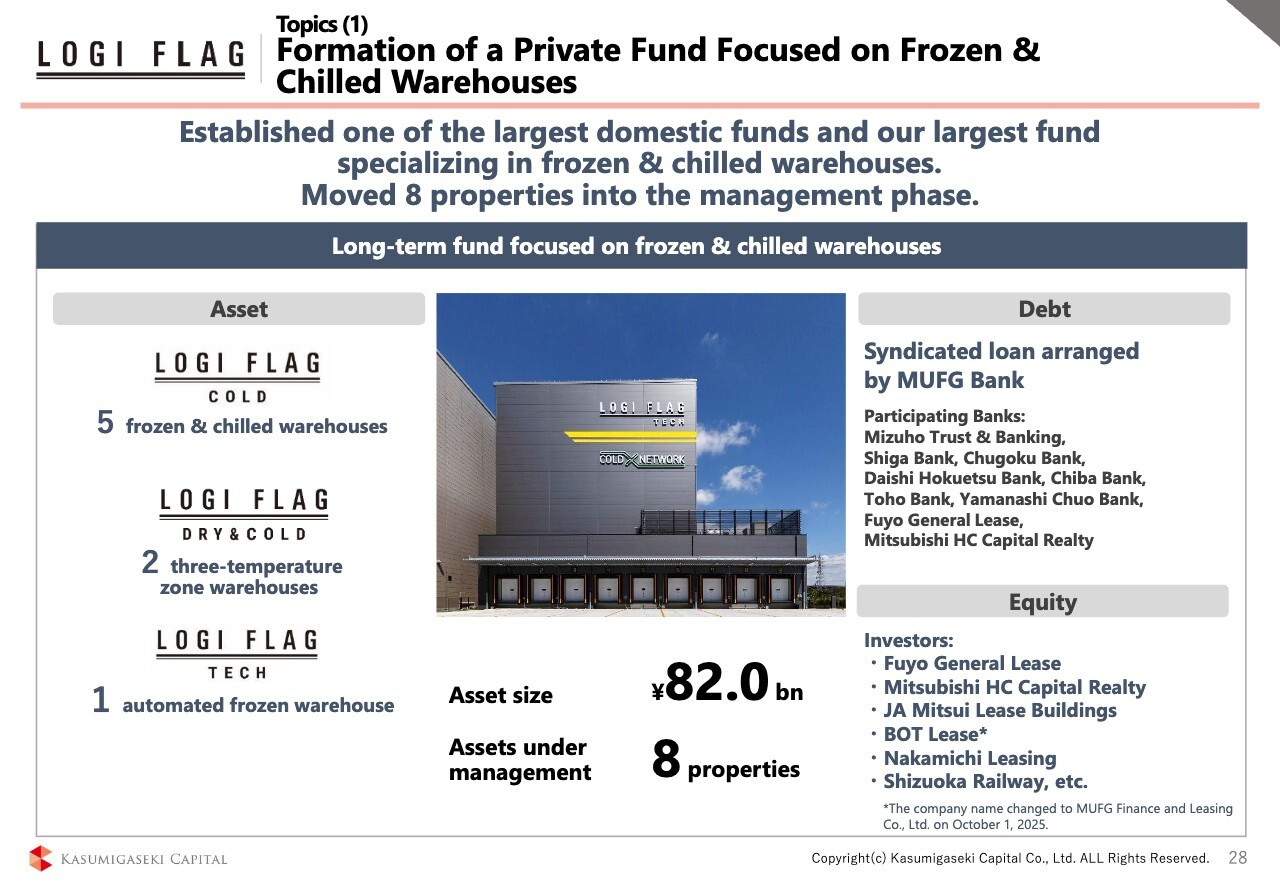

Topics (1) Formation of a Private Fund Focused on Frozen & Chilled Warehouses

Ryo Sugimoto: Hello everyone. I am Sugimoto, Deputy President of Kasumigaseki Capital. Thank you very much for joining us today. I will now provide an overview of the logistics business.

First, let me touch on the key topics. One major topic was the launch of a large private fund last year. Since we began developing frozen warehouses in logistics in 2020, five years have passed. We believe that the formation of a private fund at this milestone—by consolidating all the assets we have developed to date—represents a significant initiative.

As noted on the slide, we would like to express our sincere gratitude to all parties involved with debt and equity for their tremendous support since the development phase. We sincerely appreciate your continued support for this fund as well.

We look forward to continuing our development efforts in the future and greatly appreciate your ongoing support.

I believe this marked the culmination of our Phase 1 Medium-Term Management Plan. From the next page, we will explain how we have successfully laid the foundation for achieving Phase 2 Medium-Term Management Plan, our current medium-term management plan.

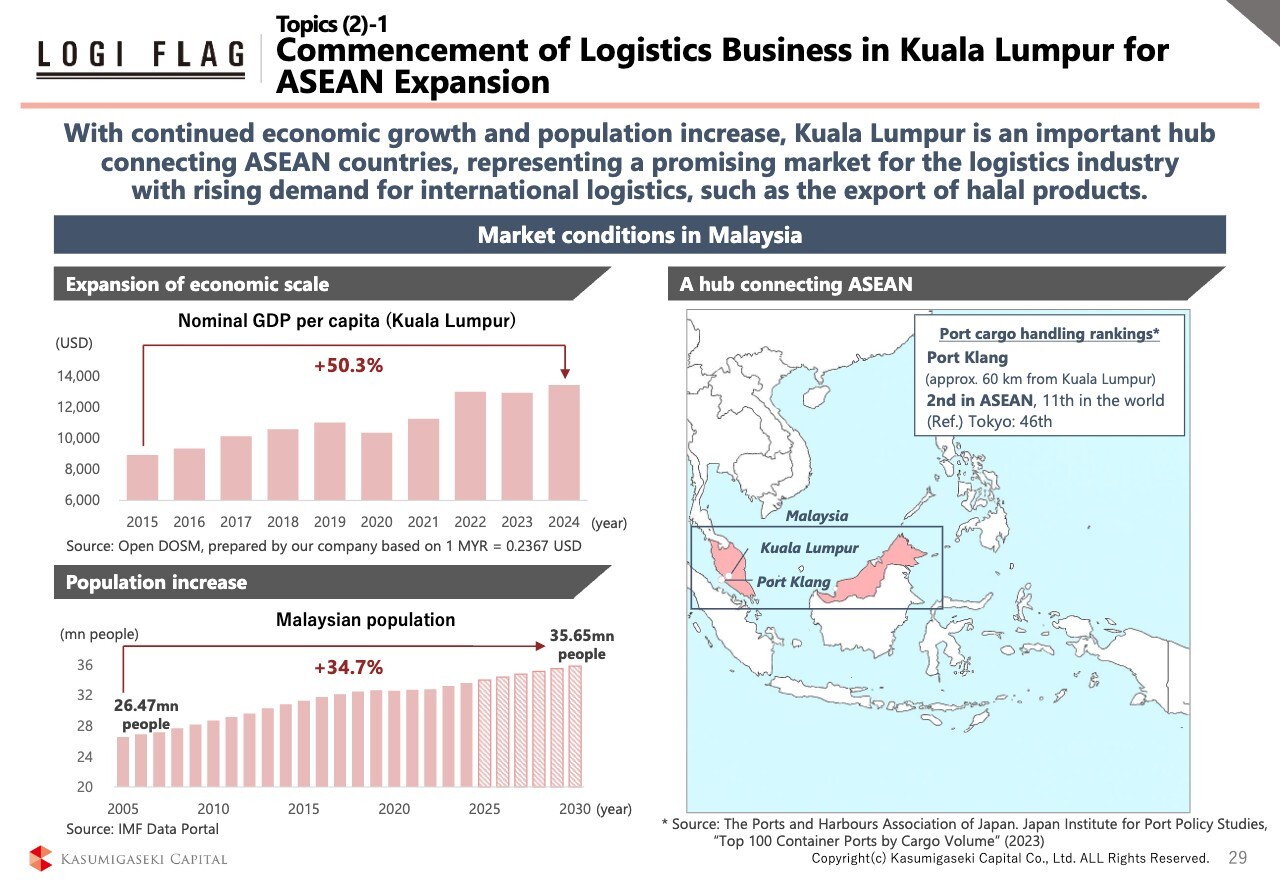

Topics (2)-1 Commencement of Logistics Business in Kuala Lumpur for ASEAN Expansion

First, let me talk about our overseas initiatives. We plan to move forward with this project in the ASEAN region. Rather than taking a country-by-country approach, we intend to target ASEAN as a whole, focusing on major cities. Specifically, Kuala Lumpur, Malaysia has been selected as our first market to enter.

You may wonder why we chose Kuala Lumpur, Malaysia. There are several reasons. In particular, the population is increasing and the economy is growing rapidly.

Furthermore, Malaysia is one of the few countries where real estate investment with 100% ownership is possible, rather than leasehold land ownership, which makes it an attractive market for us.

For example, in Thailand, although ownership is possible, foreign investment is restricted to 49%. Vietnam, on the other hand, allows 100% foreign investment, but only on leased land. In this regard, Malaysia is attractive because it allows 100% ownership.

In addition, the presence of the Port Klang is highly significant. It is the 11th largest port in the world. To illustrate its scale, the port of Tokyo, the largest port in Japan, handles approximately 4.5 million TEUs of containers annually. In addition, Japan’s five major ports—Tokyo, Yokohama, Osaka, Nagoya, and Kobe—together handle around 15 million TEUs per year.

Port Klang alone handles approximately 14 million TEUs annually, nearly equivalent to the combined volume of Japan's five major ports, making it an exceptionally large and capable port.

As this is an important logistics hub, it is highly attractive, and we would like to start our initiatives in Malaysia.

Topics (2)-2 Commencement of Logistics Business in Kuala Lumpur for ASEAN Expansion

In Malaysia, we believe that the prime location lies between the large Port Klang (mentioned earlier) and the capital city, Kuala Lumpur. We have acquired land in "Setia Alaman" in this area and plan to develop an automated frozen warehouse there. There has been considerable interest in Malaysia regarding a Japanese developer constructing an automated frozen warehouse using the latest Japanese technology, and we feel that the initial feedback has been very positive.

Starting with this project, we aim to expand our automated frozen warehouses across the ASEAN region.

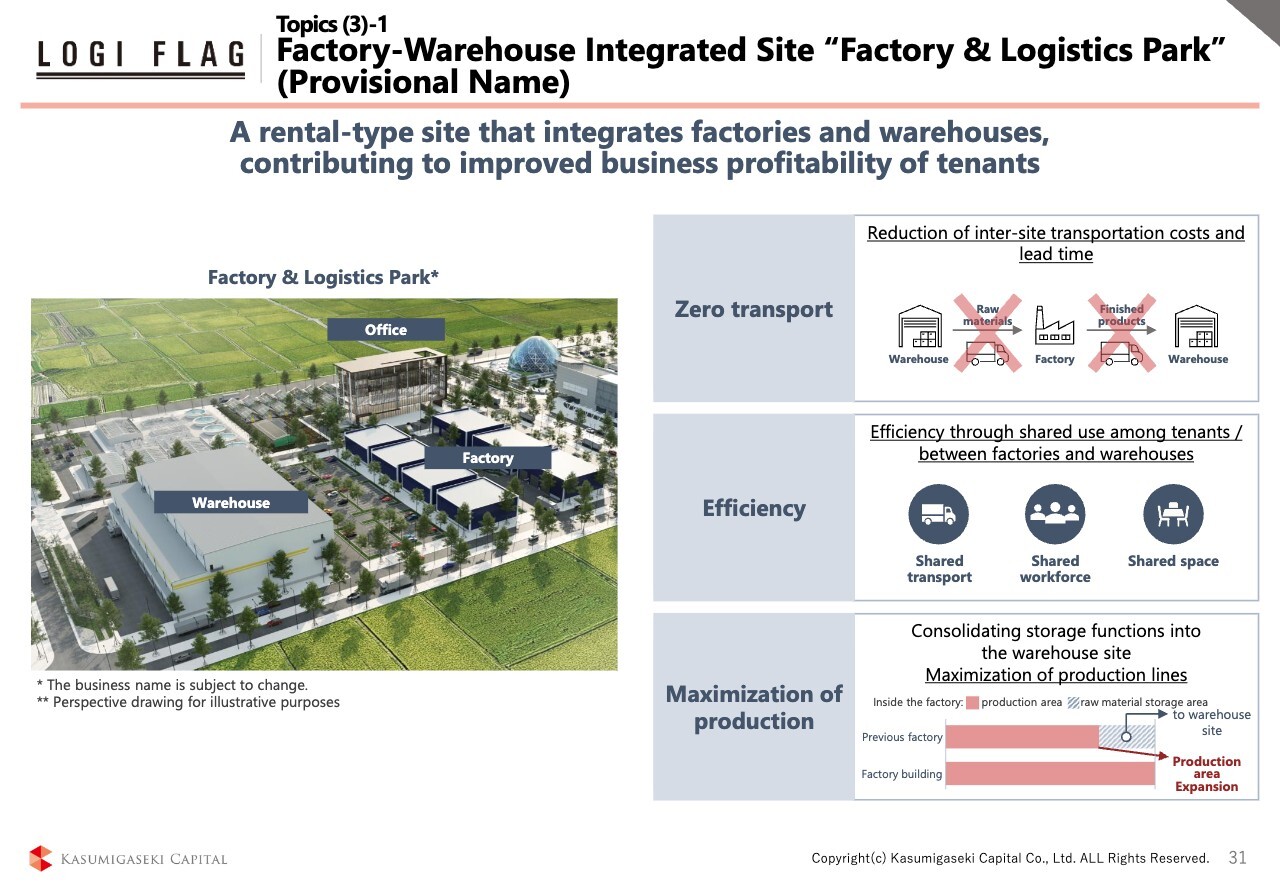

Topics (3)-1 Factory-Warehouse Integrated Site “Factory & Logistics Park” (Provisional Name)

Next is our second initiative. Under the provisional name "Factory & Logistics Park," we plan to promote a mixed-use development centered around logistics facilities, integrating rental factories within the same site. We believe that operational efficiency will be a key component of what is expected from this project.

When factories operate on a stand-alone basis, each tenant must have its own meeting rooms, warehouses and other facilities. However, by developing a large-scale integrated site like this, a shared-use business model becomes possible, allowing tenants to jointly operate and utilize common facilities such as meeting rooms and warehouses. We believe this approach will deliver significant benefits to all tenants involved.

In addition, we would like to explore the potential for a shared workforce. In the operation of various businesses, fluctuations between peak and off-peak seasons are inevitable, and the same applies to factory operations. Some factories experience peak demand in winter, while others are busiest in summer. If a single company were to manage such situations independently, it would need to hire additional personnel to cover both the summer and winter peaks.

For example, we believe that if businesses with opposite peak seasons—summer and winter—were housed in the same facility, it would be possible to reduce labor costs. In this way, we aim to actively promote the sharing of both workforce and space.

We also believe that the ability to reduce transportation costs through a shared transport system, which will be discussed on the next page, is highly important.

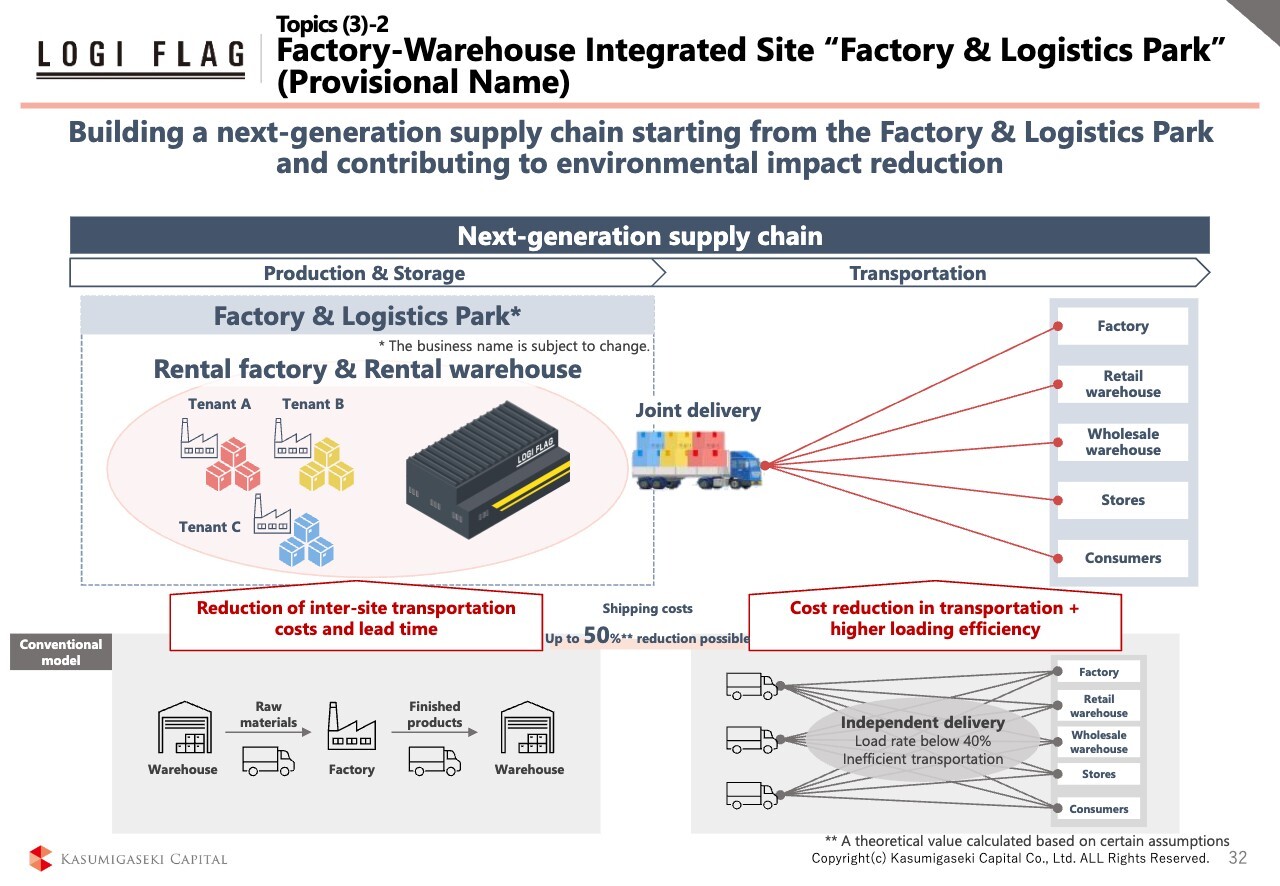

Topics (3)-2 Factory-Warehouse Integrated Site “Factory & Logistics Park” (Provisional Name)

After all, when a factory operates as a stand-alone unit, its operations follow a conventional model, as shown in the lower part of the slide. The factory itself exists, but it requires a warehouse to store raw materials, which must then be transported to the factory by truck.

This transportation process may seem natural, but by integrating operations under a system like the Factory & Logistics Park, this cost can effectively be reduced to zero.

With a warehouse for storing raw materials located adjacent to the factory, manufacturing can be carried out without incurring transportation costs, and finished products can also be stored in the same warehouse. This ability to eliminate transportation costs is considered a major advantage.

In addition, we are also exploring the implementation of joint delivery. Currently, the average truck load rate is said to be about 40%. For example, if a truck carries 80% of its capacity from Tokyo to Osaka but returns empty, the overall load rate for the round trip is only 40%. We believe such inefficiencies in loading can be improved through joint delivery, leading to greater overall efficiency.

This approach will be highly beneficial for factory tenants located here, as they can reduce transportation costs by utilizing joint delivery for their shipments.

For those who rent this warehouse, it is also possible to store raw materials and transport finished products efficiently, since the warehouse is attached to the factory. We believe this creates a strong win-win opportunity, and we aim to further develop such a system in the future.

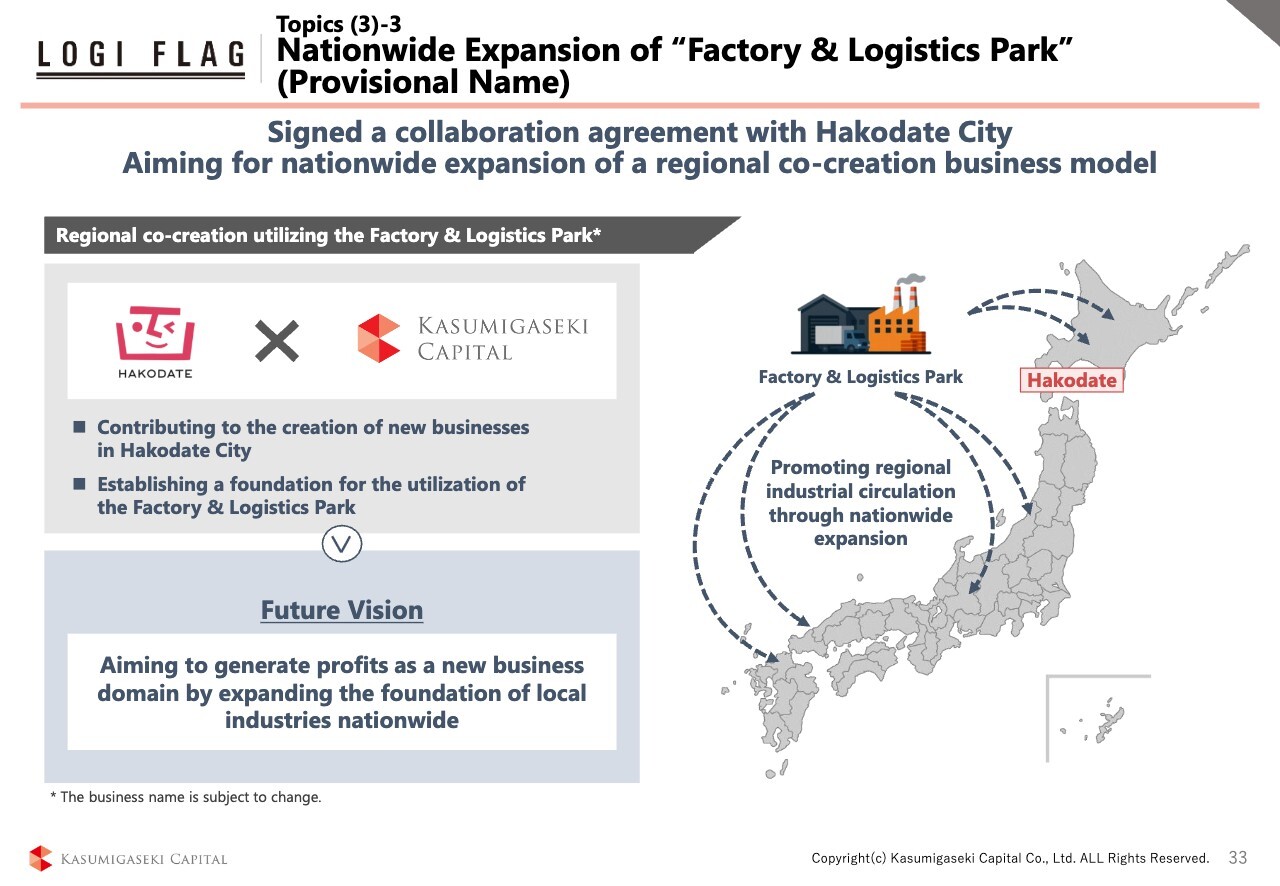

Topics (3)-3 Nationwide Expansion of “Factory & Logistics Park” (Provisional Name)

As the first step of regional co-creation utilizing the Factory & Logistics Park, we signed a regional collaboration agreement with Hakodate City.

We had hoped that this initiative would inspire other cities outside Hakodate to pursue similar collaborations—and just a couple of days later, we received a response from the mayor of another city in Hokkaido.

Having seen the news, he visited our office without an appointment, expressing his strong desire to launch a similar initiative in his own city, saying that Hakodate City's initiatives were truly impressive.

This morning, the mayor of a city in the Hokuriku region—outside Hokkaido—also visited us to request a similar collaboration. We have been receiving numerous inquiries and expressions of interest from various municipalities.

This concept can be applied not only in Japan but also overseas, and we believe that the demand for such services may in fact be even higher abroad.

In Japan, these initiatives are more likely to take place in the context of rebuilding or relocating existing factories. On the other hand, in regions such as Malaysia, where industrial infrastructure is still developing, demand is expected to emerge through the construction of new factories from the ground up.

Since we see this as a market driven by new construction, our goal is to refine this model in Japan and eventually expand it across ASEAN countries.

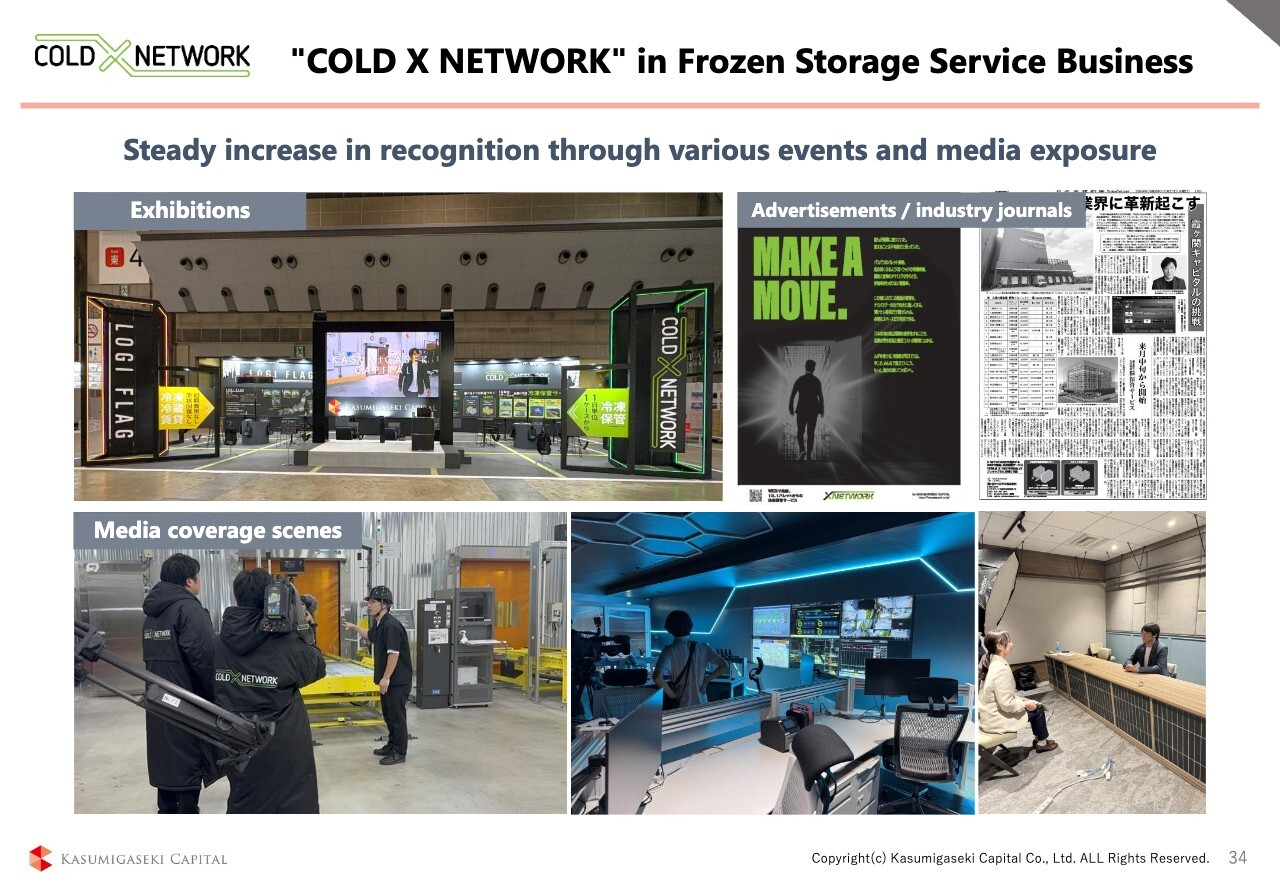

"COLD X NETWORK" in Frozen Storage Service Business

The third initiative was launched around October last year. In the past, renting a warehouse typically required long-term or large-volume contracts. However, we are now introducing COLD X NETWORK, a frozen storage service available by the case or by the pallet. This service allows users to rent space by the pallet, by the case, or even for just a single day.

Over the past year, we have achieved a steady increase in recognition through various media exposure, including exhibitions, advertisements, and media coverage. As a result, we temporarily achieved an occupancy rate close to 100% around July of this year.

We aim to further improve this business. Last year, as this was our first project, we had to proceed cautiously. As a result, we operated with a deliberately low utilization rate to minimize the risk of operational errors.

Thanks to this careful approach, we were able to operate successfully throughout the last fiscal year without a single incident of erroneous shipments or receipt of incorrect goods. For FYE8/2026, we plan to increase capacity, handle more cargo, and strengthen operations while developing new business opportunities.

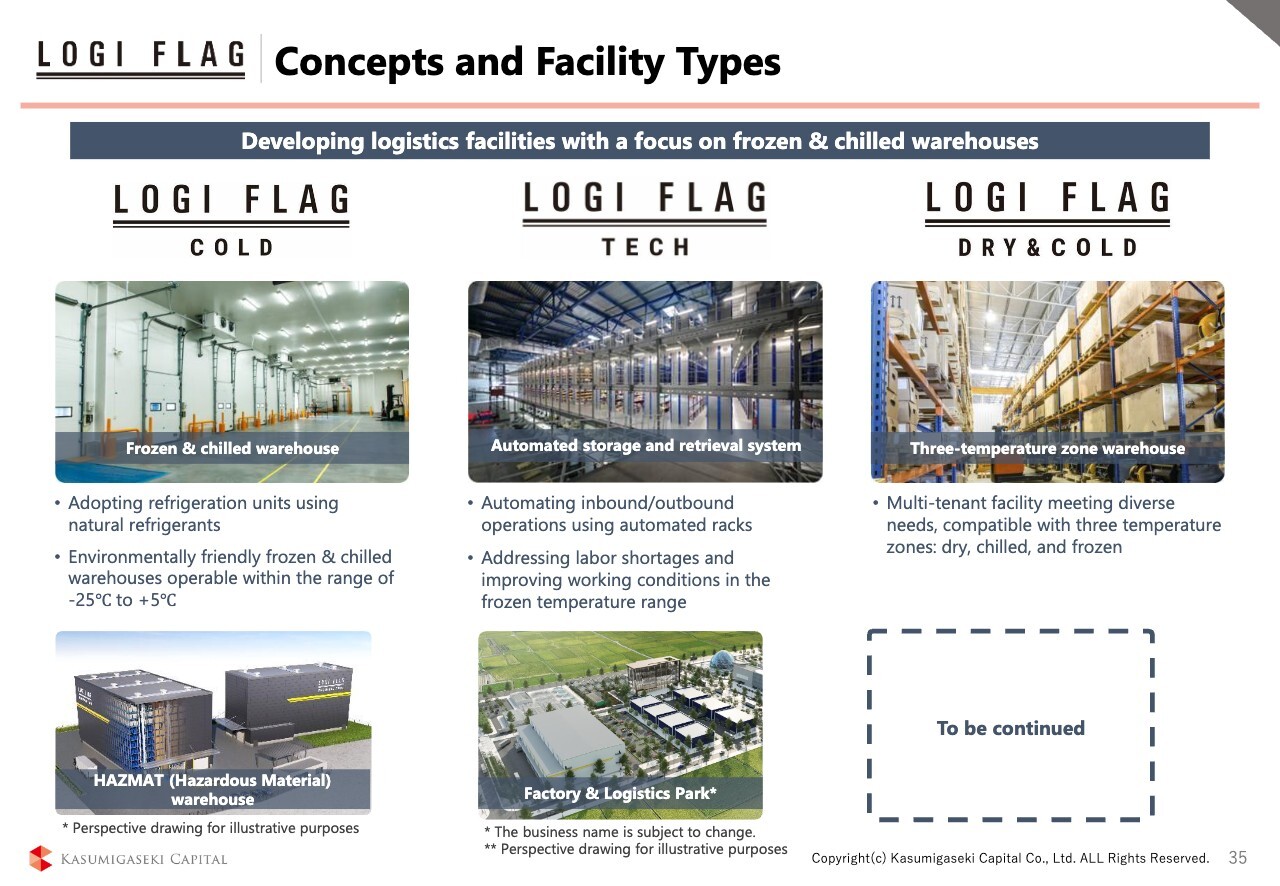

Concepts and Facility Types

So far, we have built an automated frozen warehouse and a three-temperature zone warehouse, as shown in the upper part of the slide. In addition, we have been developing various other facilities, such as the HAZMAT (hazardous materials) warehouse last year and the Factory & Logistics Park this year. Since we plan to continue working on various projects in the future, the slide is marked "To be continued."

Regarding the organization, we had given the Logistics Business Division a name limited to logistics. However, starting this fiscal year, we will rename it to the Infrastructure Innovation Business Division, and we will work to expand our business domain to cover all industrial assets, not just logistics.

One example is the Factory & Logistics Park, but we plan to expand our business across a variety of industries, not just in this area.

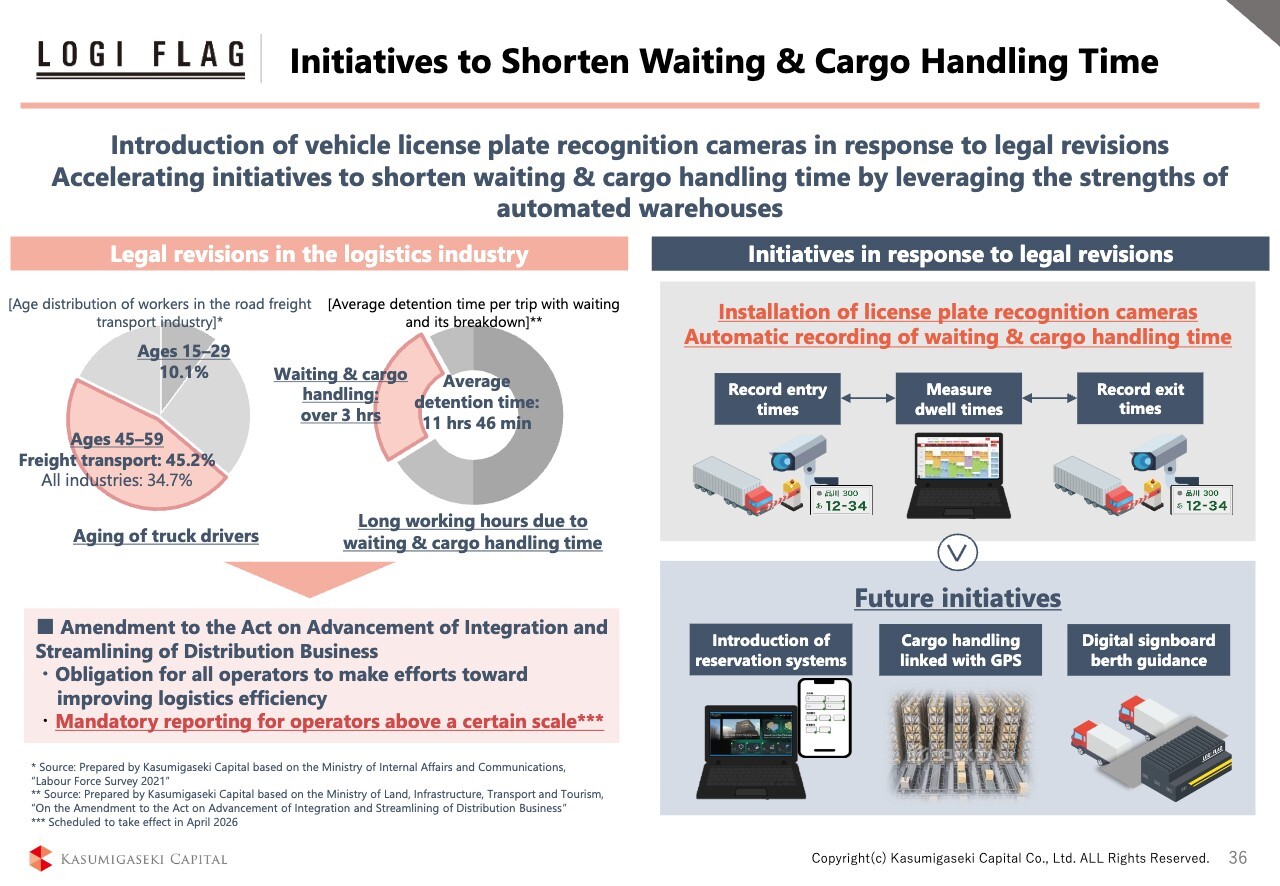

Initiatives to Shorten Waiting & Cargo Handling Time

Next, I would like to explain our initiatives to shorten waiting and cargo handling times. As one approach to developing a business story, we focused on the Act on Advancement of Integration and Streamlining of Distribution Business, which was revised in April of this year.

The revision of this law is driven by the growing labor shortage and the need to reform work styles. Specifically, the basic policy of the Act is to require businesses to shorten waiting and cargo handling times, as there will come a time when goods cannot be transported unless these times are reduced.

Monitoring waiting and cargo handling times is the first issue to address, and in the process of resolving it, we will explore ways to commercialize the project in the future.

For example, we envision a system in which trucks are linked to the warehouse via GPS, and robots at the warehouse are automatically activated when a GPS signal indicates that a truck has entered a 10-kilometer radius. The robots then begin preparing cargo so that it is ready for shipment in sync with the truck’s arrival.

Alternatively, we aim to apply this approach to warehouse development that can shorten waiting and cargo handling times through the same GPS linkage, such as by preparing in advance to receive cargo. We would like to create new businesses in accordance with the purpose of the Act.

We also believe that such an automated framework is by no means limited to frozen warehouses, although we cannot specify the timing. Currently, we are focusing only on frozen warehouses, but we see potential opportunities to enter new markets by building automated facilities for dry, room temperature warehouses as well.

Looking ahead, we plan to explore the potential of automated dry warehouses as well, extending beyond frozen warehouses.

This concludes the explanation of the Logistics and Infrastructure Innovation Businesses. Thank you for your attention.

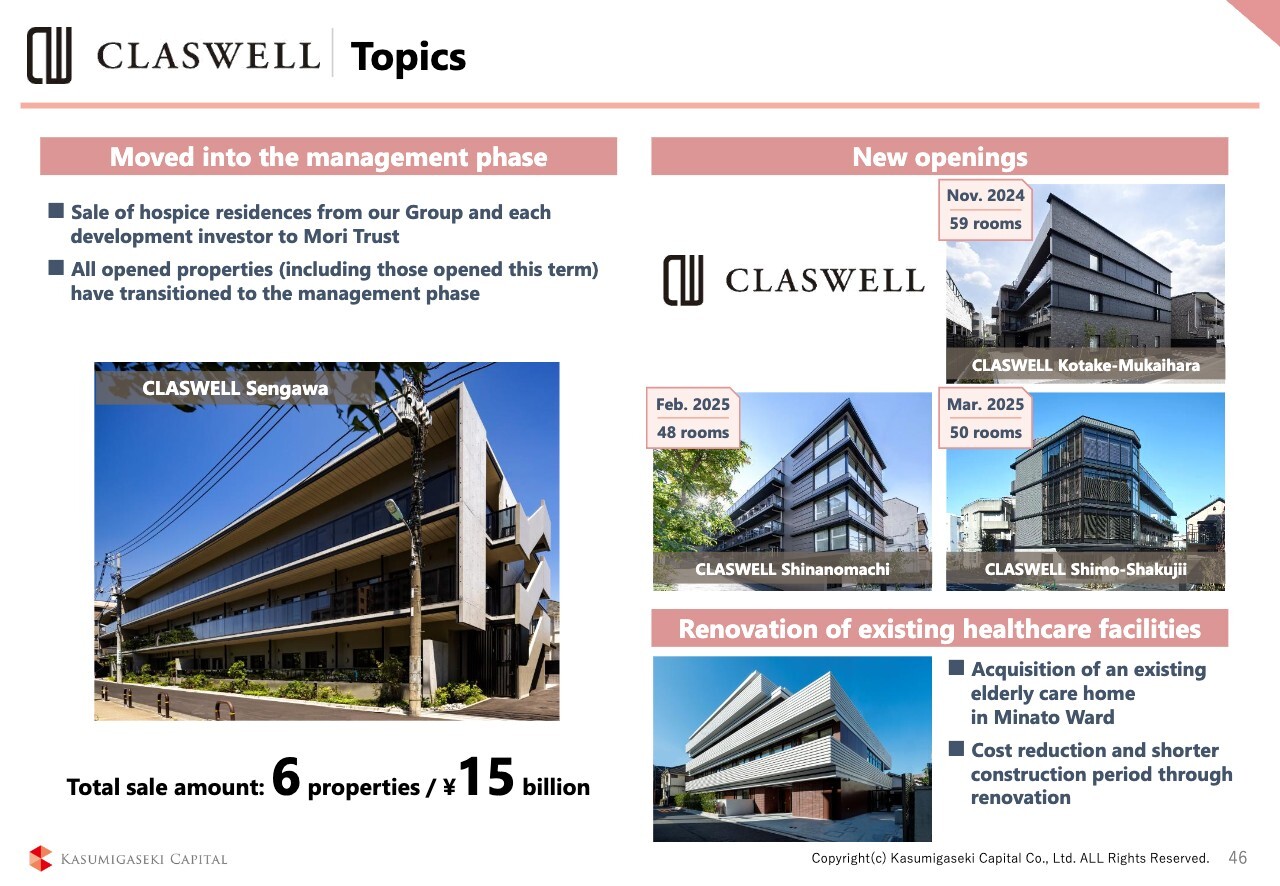

CLASWELL Topics

Komoto: I would like to explain our healthcare business and our overseas operations, with a particular focus on our Dubai business.

As I mentioned at the beginning, we have established a 15 billion yen private placement fund for six hospice residences. We believe that both the quality of these properties and their locations are higher than those of typical hospices.

CLASWELL Brand Concept

This slide illustrates the concept of the hospices we are developing. The name "CLASWELL" reflects our desire for our residents to live a good and fulfilling life. In simple terms, the goal is to create a facility where users would be happy for their own parents to live.

Please take a look at the photos on the slide. You may not be very familiar with hospices in general, so at first glance they may not seem remarkable, but these photos actually reveal many surprising features.

First, the facility is spacious and bright. We also hold various events almost every month, including concerts, band performances, and Christmas parties.

Furthermore, to ensure that residents enjoy "eating," our hospice offers delicious meals. All of these are full of surprising innovations.

In addition, many common spaces are provided for multi-purpose use, featuring amenities such as a mahjong table and a soft-serve ice cream machine. As a result, we have created a hospice that families are delighted to visit every day.

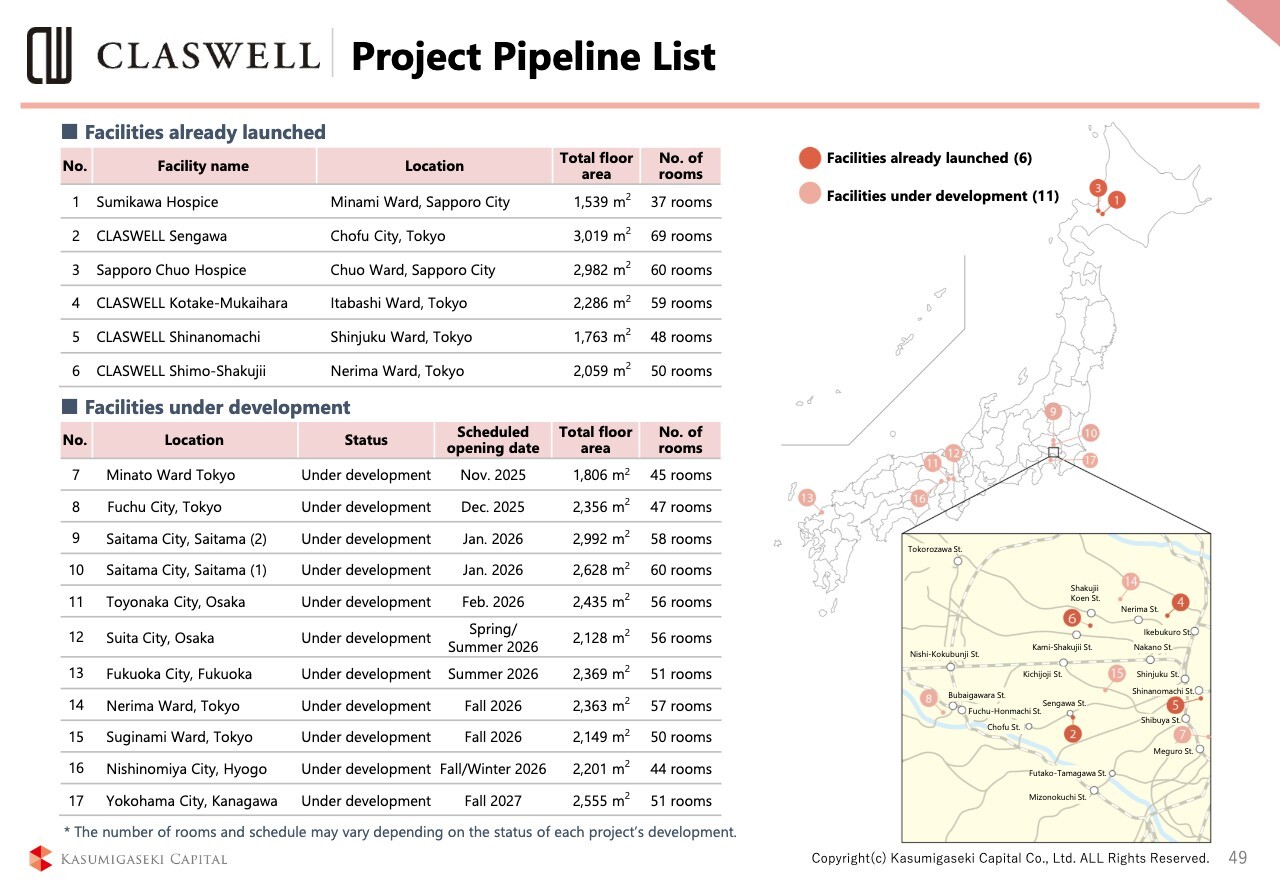

CLASWELL Project Pipeline List

A list of hospice projects in our pipeline is shown on this slide. The six properties in the upper row are already part of the stable fund, while the 11 properties in the lower row belong to the development fund. Once development is completed, we plan to gradually transfer these properties into the stable fund for medium- to long-term management.

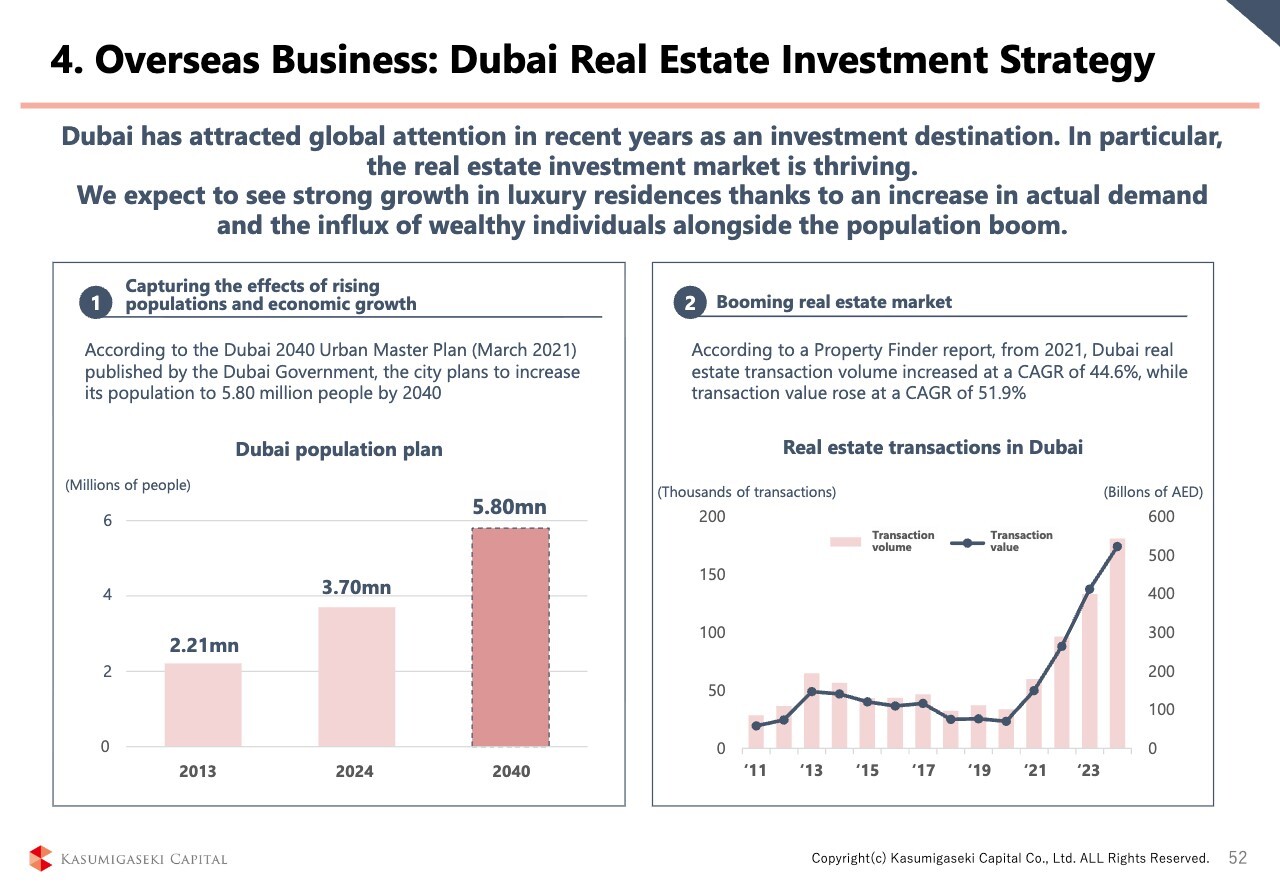

4. Overseas Business: Dubai Real Estate Investment Strategy

Moving on to Dubai. First, the real estate market in Dubai is extremely active. According to a TripAdvisor’s survey, Dubai has ranked as the world's most popular tourist destination for three consecutive years.

Housing demand is very strong. Over the past decade, the city’s population has increased by 1.5 million, which is equivalent to the population of Kobe City in Hyogo Prefecture or Kawasaki City in Kanagawa Prefecture.

In addition, according to the master plan published by the Dubai government, the city plans to increase its population by approximately 2.0 million people over the next 15 years. This figure is roughly equivalent to the population of Sapporo City in Hokkaido, and is comparable to Fukuoka City in Fukuoka Prefecture (1.6 million) and Nagoya City in Aichi Prefecture (2.3 million).

We have witnessed remarkable growth in Dubai. As a result, we are now transforming our business model there. So far, we have focused on the value-enhancement project of existing condominiums and detached houses, but going forward, we plan to develop residential properties.

Over the past three years, we have been operating in Dubai, building our know-how and network. Our business model there is similar to the one we use in Japan: we handle land preparation, design planning, permit acquisition, and general contractor arrangements, while our partners provide funding during the development phase. Profits from the sale of completed properties are then shared with these partners.

As the first step, we have launched a project in partnership with Daito Trust Construction Co., Ltd. This marks the first development project in Dubai undertaken by a Japanese company. Going forward, we will continue to collaborate with Daito Trust Construction Co., Ltd. and other partners to further expand our development business in Dubai.

This concludes the explanation of our business operations. With that, we will now conclude our presentation of the financial results for the FYE8/2025. Finally, I would like to share a few closing remarks.

Greetings from Mr. Komoto

I have always said that our employees are truly talented, and we are extremely proud of them. They are capable of achieving double growth as if it were nothing. What is especially remarkable is their ambition. They are highly motivated to grow the business, and when they receive feedback, they embrace it and use it to improve. Thanks to these employees, we were able to achieve the net income target of 10 billion yen set in the Phase 1 Medium-Term Management Plan.

However, growth cannot be achieved by employees alone. We were able to achieve these results thanks to the cooperation of everyone involved, including all of you here today. On behalf of the company, I would like to express my sincere gratitude once again. Thank you very much.

The FYE8/2025 marked both the completion of the Phase 1 Medium-Term Management Plan and the beginning of Phase 2, and we are off to a strong start. Kasumigaseki Capital continues to grow. As a venture company, we see ourselves as a "do-venture"—we have not yet done enough of what we aim to accomplish.

None of our employees, myself included, are satisfied with the status quo. We deeply appreciate your continued support and guidance.

That concludes my remarks. Thank you very much for your attention.